Technology, Media and Telecom

5th MayPricing Strategy for Semiconductor Components

3 Min Read

The Media Gateways Market Report is Segmented by Type (Analog and Digital), Technology (Wireline, Wireless, and Hybrid), Deployment Model (Virtual/Cloud-native, Hybrid Deployments, and More), Protocol Support (SIP-Only Gateways, TDM-IP Gateways, and More), End User (BFSI, Manufacturing, Government, Healthcare, Telecommunications, and Transportation), and Geography.

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

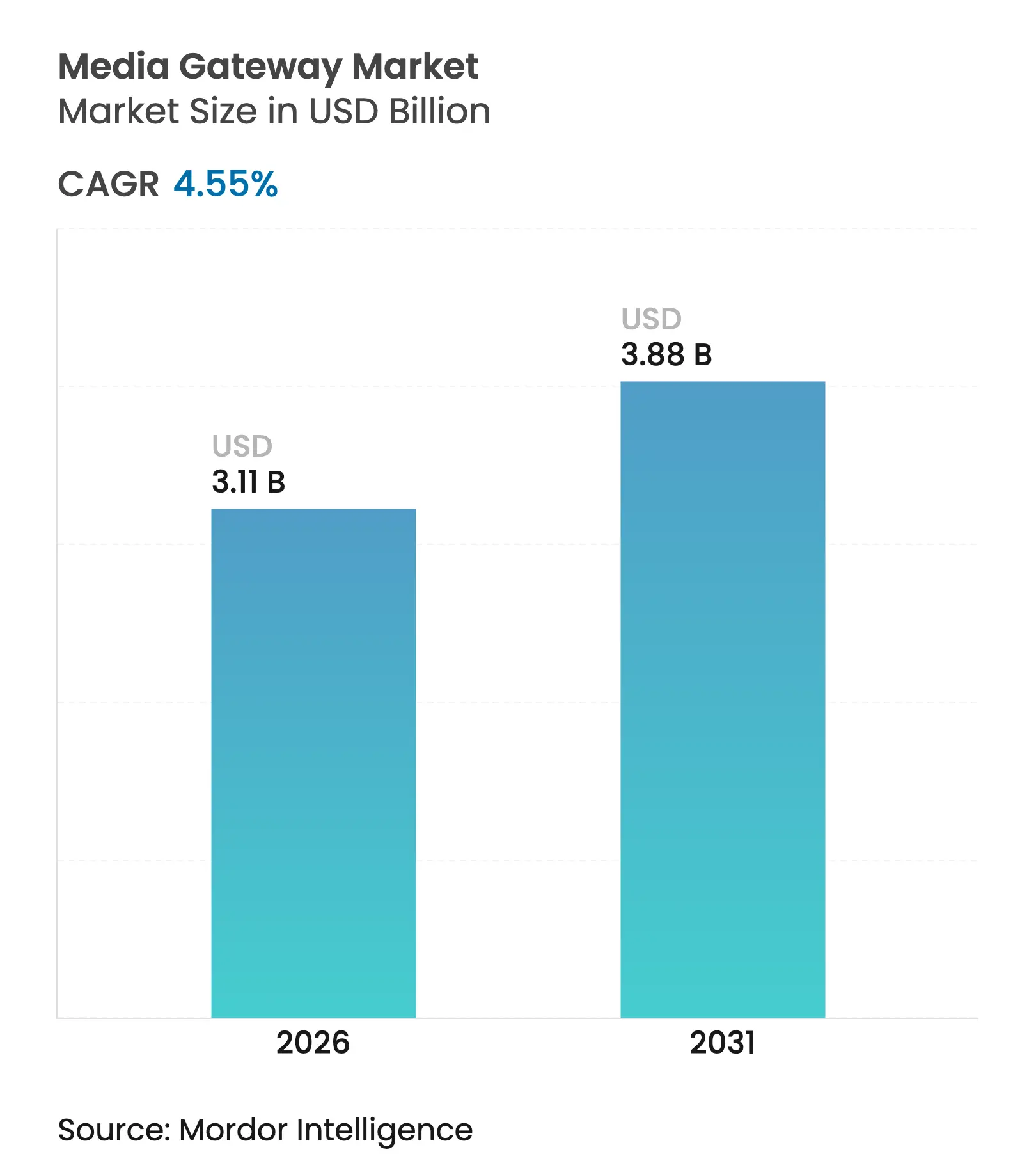

| Market Size (2026) | USD 3.11 Billion |

| Market Size (2031) | USD 3.88 Billion |

| Growth Rate (2026 - 2031) | 4.55 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The media gateway market size is expected to grow from USD 2.97 billion in 2025 to USD 3.11 billion in 2026 and is forecast to reach USD 3.88 billion by 2031 at 4.55% CAGR over 2026-2031. Sustained growth reflects the global shift from Time Division Multiplexing to Internet Protocol infrastructure, heightened demand for Next Generation 911 services, and 5G roll-outs that need sophisticated interworking gateways. Adoption of unified communications platforms is accelerating gateway virtualization, while private 5G networks in factories and transport systems require low-latency protocol conversion. Energy-efficiency targets set by major operators add pressure to deploy cloud-native gateways that trim power use, and the rising focus on secure, encrypted voice drives investment in advanced media processing.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Migration from TDM to VoIP/IP networks Migration from TDM to VoIP/IP networks | +1.2% | North America, Europe | Medium term (2–4 years) | (~) % Impact on CAGR Forecast:+1.2% | Geographic Relevance :North America, Europe | Impact Timeline :Medium term (2–4 years) |

Expansion of 5G and LTE requiring interworking gateways Expansion of 5G and LTE requiring interworking gateways | +0.9% | Asia Pacific, global spill-over | Long term (≥ 4 years) | |||

Growing demand for unified communications in enterprises Growing demand for unified communications in enterprises | +0.8% | North America, Europe | Short term (≤ 2 years) | |||

Edge-computing roll-outs needing ultra-low-latency transcoding Edge-computing roll-outs needing ultra-low-latency transcoding | +0.6% | Manufacturing hubs in Asia Pacific | Medium term (2–4 years) | |||

Regulatory mandates for NG911/112 IP emergency services Regulatory mandates for NG911/112 IP emergency services | +0.7% | North America, EU | Short term (≤ 2 years) | |||

Private industrial 5G networks needing protocol conversion Private industrial 5G networks needing protocol conversion | +0.5% | Industrial regions worldwide | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Migration from TDM to VoIP/IP networks accelerates modernization

Legacy circuit-switched assets are being retired as carriers migrate to all-IP cores. BT plans to disconnect the United Kingdom’s public switched telephone network in 2027, covering 25 million premises with gigabit broadband.[1]BT Group, “PSTN Switch-Off Timeline Update,” bt.com Network architects rely on carrier-grade Ethernet switches with circuit emulation to keep services running during the transition. Multi-Protocol Label Switching aggregation supports gradual migration without stranded assets, and vendors are adding software-based circuit emulation to gateway portfolios to smooth conversion.

5G network expansion drives interworking gateway requirements

China Unicom Beijing and Huawei activated a 5.5 G three-carrier-aggregation network covering 70% of Beijing’s Fourth Ring Road through more than 4,000 base stations that support immersive video and cloud gaming.[2]Huawei Technologies, “China Unicom Beijing and Huawei Launch Three-Carrier Aggregation 5.5 G Network,” huawei.com Interworking gateways handle signaling between legacy 4G gear and 5G Standalone cores, while Ericsson offers a hybrid core that retains 4G nodes yet enables rapid Standalone deployment.[3]Ericsson, “Ericsson and Google Cloud Introduce SaaS 5G Core,” ericsson.com Release 18 features such as L1/L2 triggered mobility cut handover delays to 30 milliseconds, underscoring the need for real-time transcoding.

Enterprise unified communications adoption transforms voice infrastructure

Microsoft Teams Direct Routing and Operator Connect services have driven double-digit adoption of software-based voice. AudioCodes posted 13% revenue growth from Microsoft-aligned services in Q4 2024, reaching USD 34.2 million.[4]AudioCodes, “Q4 2024 Results,” audiocodes.comSession Border Controllers hosted in the cloud replace appliance gateways, and vendors monetize recurring software licenses instead of hardware refresh cycles. Ribbon’s cloud-to-cloud connectivity keeps PSTN calls on existing PBX trunks while gradually shifting users to Teams, illustrating mixed topologies that still depend on media gateways for protocol mediation.

Edge computing integration demands ultra-low-latency processing

Intel’s Core Ultra processors demonstrated 5.8× faster media performance at CES 2025, supporting predictions that half of all edge workloads will embed machine learning by 2026. The University of Wisconsin Milwaukee integrated Ericsson private 5G with manufacturing systems, using Generic Routing Encapsulation tunnels to handle standalone 5G devices on factory floors. Multi-Access Edge Computing control APIs steer traffic to the nearest media node, keeping latency below 20 milliseconds for computer-vision quality checks.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Shift toward softswitches and SBCs curbing hardware demand Shift toward softswitches and SBCs curbing hardware demand | –0.8% | North America, Europe | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast:–0.8% | Geographic Relevance :North America, Europe | Impact Timeline :Short term (≤ 2 years) |

Shortage of skilled integration workforce Shortage of skilled integration workforce | –0.6% | Global | Medium term (2–4 years) | |||

Semiconductor supply-chain volatility Semiconductor supply-chain volatility | –0.5% | Manufacturing regions | Short term (≤ 2 years) | |||

Energy-efficiency compliance cost escalation Energy-efficiency compliance cost escalation | –0.4% | Europe, North America | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Softswitch and SBC migration challenges traditional hardware models

Network-function virtualization lets carriers deploy voice control on commercial servers, shrinking appliance shipments. AudioCodes offers a carrier-grade virtual SBC with five-nines availability for enterprises that prefer cloud deployment over rack-mounted gear. Ribbon integrates Operator Connect for Microsoft Teams to provide SIP trunks without on-premises hardware. Appliance makers must recast portfolios around containers and micro-services, or risk revenue erosion as operators redirect budgets to software.

Skilled workforce shortage constrains integration capabilities

Industry groups warn of an 85 million-person global skills gap by 2030 that could erase USD 8.5 trillion in unrealized revenue weforum.org. Complex media-gateway roll-outs require expertise in VoIP signaling, 5G traffic flows, encryption, and container orchestration. Smaller operators turn to managed-service contracts or public-cloud solutions to offset shortages, contributing to rising adoption of turnkey hosted gateways.

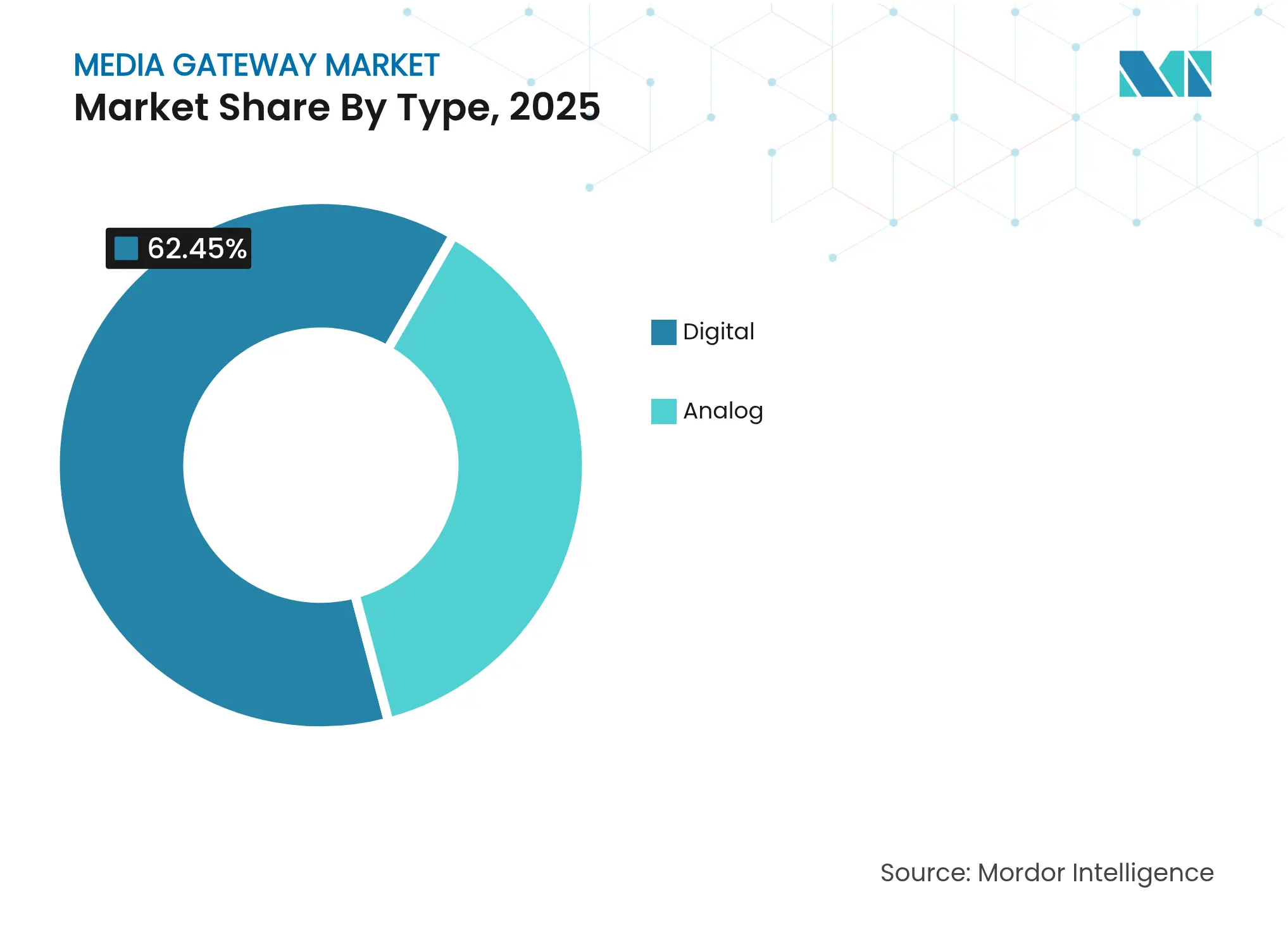

By Type: Digital dominance drives protocol evolution

Digital solutions generated 62.45% of 2025 revenue and are forecast to grow at a 4.74% CAGR through 2031 as enterprises swap circuit-switched trunks for SIP and WebRTC. The digital share equated to USD 1.86 billion of the media gateway market size in 2025. Analog units remain relevant for niche industrial endpoints but will shrink as carriers dismantle copper access. Nokia renewed its voice-core contract with AT&T, pivoting to a cloud-native IMS core that will carry 5G voice across the United States.

Operators preparing for 3GPP Immersive Voice and Audio Services need gateways that support metadata-assisted spatial audio, a capability under joint development by Nokia, Vodafone, and RingCentral. The upgrade moves digital gateways beyond simple protocol mediation into full media enrichment, reinforcing their central role in the media gateway market.

Note: Segment shares of all individual segments available upon report purchase

By Technology: Hybrid solutions bridge legacy and modern networks

Wireline platforms still held 47.20% revenue in 2025, yet hybrid approaches that blend wireline reliability with wireless flexibility are climbing at 6.52% CAGR. T-Mobile selected Nokia’s Multi-Access Gateway to route high-speed internet traffic across LTE, 5G NSA, and 5G SA, proving that one platform can span multiple access modes. Hybrid configurations help carriers phase out legacy nodes without disrupting customers, anchoring demand in the media gateway market.

Wireless gateways serve private 5G and fixed-wireless access. Factory deployments in Japan and South Korea highlight the need for robust protocol mediation when mobile robots, cameras, and legacy production lines converge on a single 5G core. The flexible form factor keeps capital intensity low, a key buying criterion for manufacturers entering Industry 4.0.

By Deployment Model: Cloud-native architecture reshapes market dynamics

Hardware appliances still contribute 67.10% of 2025 revenue, equal to USD 1.99 billion of the media gateway market size. However, cloud-native gateways are expanding at 7.61% CAGR as operators pursue elastic scaling and usage-based pricing. Ericsson and Google Cloud’s On-Demand platform lets a carrier spin up a complete 5G core, including media processing, within hours, cutting lead times from months to days.

Containerized media functions appeal to edge scenarios where workload spikes are unpredictable. Broadcasters migrating live content to the cloud after pandemic disruptions underscore how cloud-native paths reduce time-to-air while preserving quality. Hybrid deployments allow mission-critical traffic to stay on physical hardware until operators confirm parity on the virtual side.

Recognized by Experts. Trusted by Leaders.

A trusted intelligence partner to global decision-makers across 90+ countries.

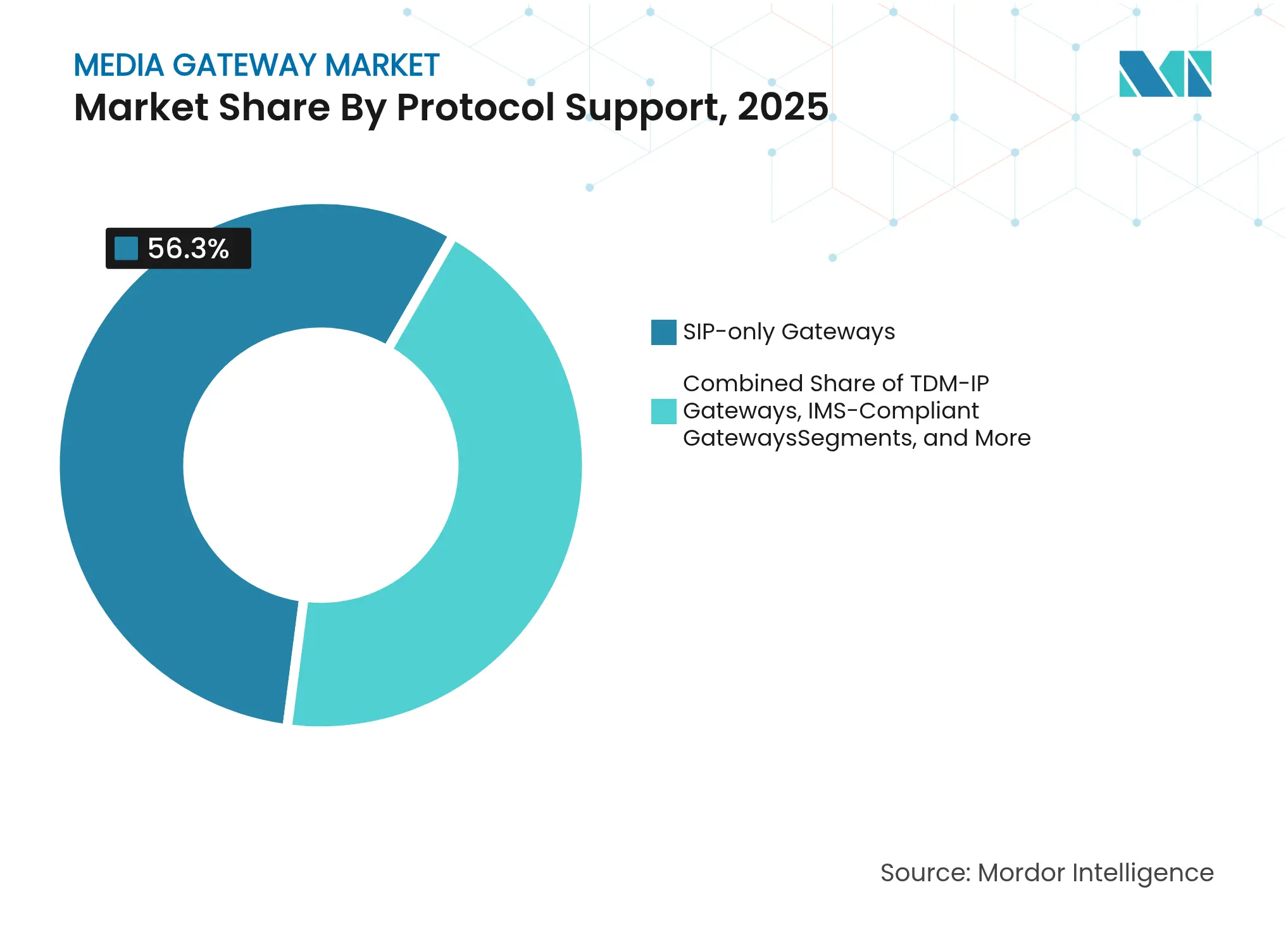

By Protocol Support: Multi-protocol gateways address interoperability complexity

SIP-only models led with 56.30% revenue in 2025. Yet multi-protocol products that support SIP, H.323, and Media Gateway Control Protocol are rising at 8.28% CAGR because large enterprises often maintain mixed infrastructures during migration phases. Cisco’s service-management framework shows call-flow intricacies when 5G session management interacts with charging and policy control

IMS-compliant gateways, capable of secure end-to-end encryption, are gaining traction in financial services. Federal rules on NG911 state that emergency calls must arrive at public safety answering points in SIP with embedded location data, driving uptake of gateways that can translate older trunks while satisfying new standards.

Note: Segment shares of all individual segments available upon report purchase

By End-User: Telecommunications sector leads while transportation accelerates

Operators generated 33.65% of 2025 revenue owing to nationwide 5G upgrades and voice-core modernization. Transportation is projected to expand at the fastest 5.24% CAGR as connected-vehicle systems lean on ultra-reliable voice links. The United States Department of Homeland Security expects 5G to transform vehicle automation and roadway coordination, creating a new layer of communications infrastructure that depends on secure protocol conversion.

Banking, manufacturing, and government domains follow. Banks are early adopters of encrypted SIP trunking for regulatory compliance, while factories deploy private 5G networks to support industrial robots. Public agencies invest in NG911 migration, keeping the media gateway market firmly rooted in long-term public-safety funding cycles.

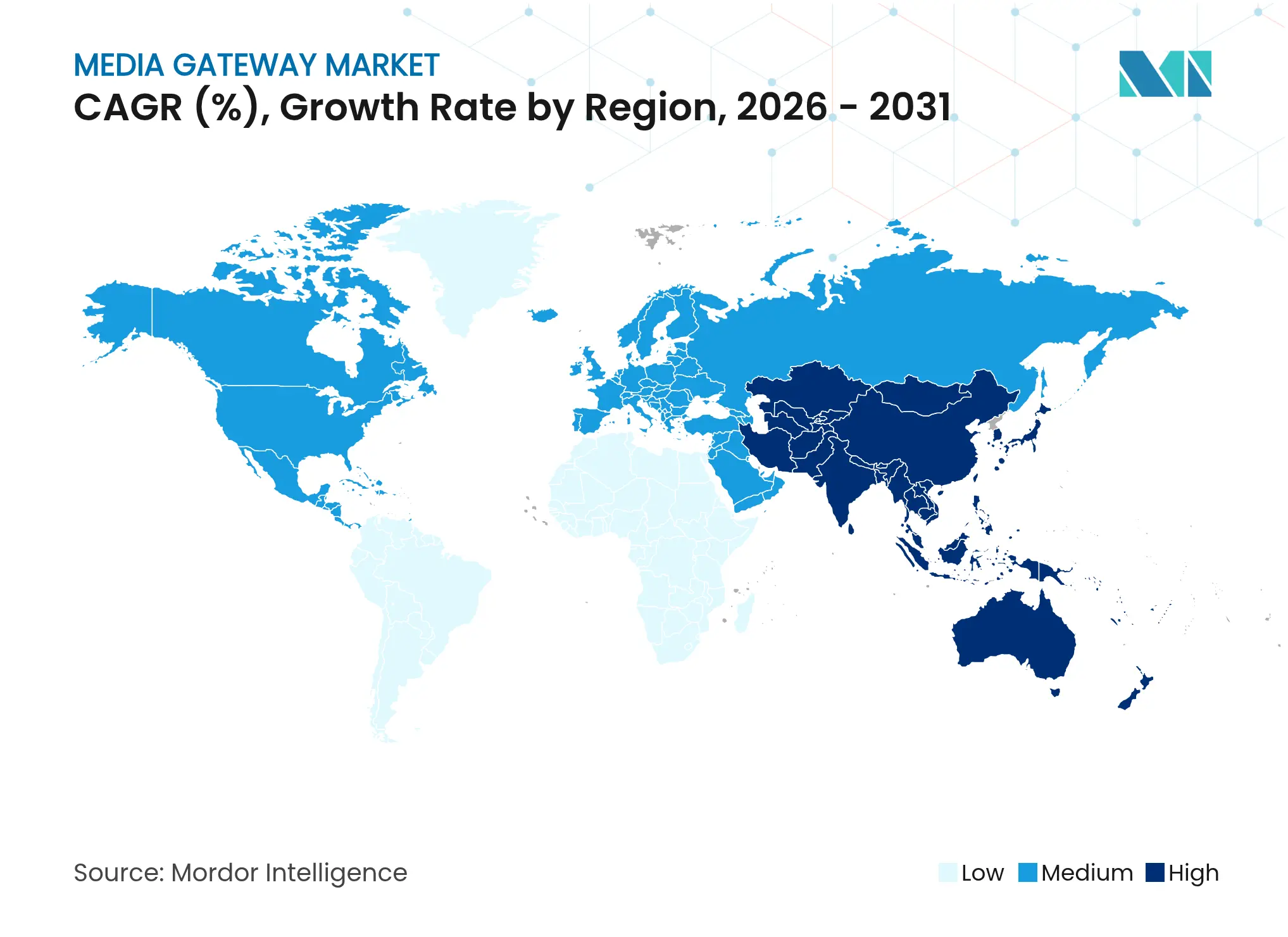

Asia Pacific dominates with 41.70% revenue in 2025, driven by aggressive 5G Standalone deployments and private network investment. China Unicom’s city-wide 5.5 G coverage around Beijing’s Fourth Ring Road illustrates the sheer scale of protocol-mediation demand. Japanese automakers run private 5G lines inside smart factories, reinforcing the region’s leadership in next-generation communications.

North America remains pivotal because of NG911 mandates and enterprise cloud collaboration uptake. The Federal Communications Commission has set milestones for full IP connectivity across emergency services, ensuring steady procurement of gateways that insert location data into SIP messages. Nokia’s USD 2.3 billion acquisition of Infinera aligns with a strategy to capture optical transport upgrades linked to voice-core refresh cycles.

Europe advances on PSTN switch-off deadlines and stringent carbon-reduction targets. BT’s timeline for retiring copper access networks sustains hybrid gateway demand, while EU climate regulations push carriers to select energy-efficient media hardware. The combination of modernization and sustainability keeps Europe growing at a stable mid-single-digit rate through 2030.

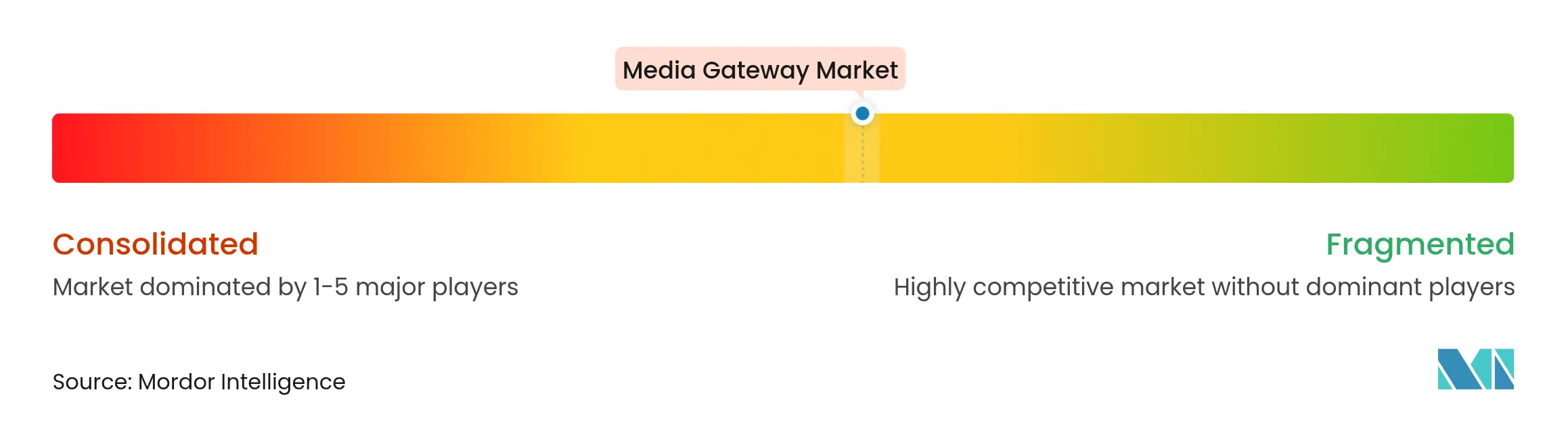

Market Concentration

The media gateway market is moderately fragmented. Nokia’s planned acquisition of Infinera seeks to boost optical networking share to 20% and deepen North-American reach, underscoring a consolidation trend among equipment suppliers. Ericsson’s alliance with Google Cloud to deliver carrier-grade core-as-a-service shows how traditional vendors tap hyperscalers for elasticity and artificial-intelligence automation.

Tier-two specialists carve out success in software niches. AudioCodes focuses on Microsoft-centric unified communications and reported USD 34.2 million in services revenue for Q4 2024. Ribbon Communications emphasizes cloud-to-cloud SIP trunking, targeting enterprises that have mixed PBX and Teams estates. Vendors differentiate through AI-assisted voice analytics, digital twins that model network energy use, and open APIs that expose programmable media functions.

White-space opportunities arise in private 5G for factories, mining, and ports where bespoke protocols persist. Suppliers that pair low-latency media conversion with industrial-grade ruggedization can build defensible positions. Long-term success hinges on blending high availability with granular software control, a balance the media gateway market rewards with recurring licenses and managed-service contracts.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

Market Definitions and Key Coverage

Our study defines the media gateway market as global revenue generated from physical or virtual appliances that translate voice, video, or data streams between circuit-switched (PSTN/TDM) and packet-based (IP, LTE, 5G) networks, including analog and digital form factors deployed across carrier, enterprise, and public-safety domains. According to Mordor Intelligence, the baseline year value equals USD 2.97 billion in 2025, rising to USD 3.71 billion by 2030.

Scope exclusion: session border controllers and pure softswitch software are not counted.

Segmentation Overview

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed network-planning engineers, procurement heads at tier-1 telcos, and channel partners across North America, Europe, Asia-Pacific, Latin America, and the Middle East. Discussions validated lifecycle replacement rates, virtualization adoption pace, and average selling prices, and then reconciled regional disparities hinted at in secondary material.

Desk Research

We began with public data from tier-1 sources such as the International Telecommunication Union, GSMA Mobile Economy, FCC Voice Traffic Statistics, Eurostat digital-infrastructure series, and United Nations Comtrade shipment codes for gateway boards. Company 10-Ks, investor decks, and reputable trade journals supplied recent unit shipments and pricing cues. Paid streams, chiefly Dow Jones Factiva for deal flow and D&B Hoovers for vendor financials, rounded out the fact base. These sources illustrate but do not exhaust the references tapped during data gathering, cross-checks, and clarification.

Market-Sizing & Forecasting

A top-down construct converts installed PSTN lines, VoIP subscriber counts, and 5G base-station rollouts into annual demand pools, which are then sanity-checked against sampled supplier sales and ASP × volume snapshots that act as a selective bottom-up lens. Key variables like legacy-line retirement rate, unified-communications seat penetration, gateway virtualization share, regional capex trends, and regulatory NG911/112 deadlines feed a multivariate-regression forecast that extends to 2030.

Where vendor roll-ups left gaps, regional interpolation used proxy indicators such as fiber-to-the-home coverage or mobile data-traffic growth to temper estimates.

Data Validation & Update Cycle

Outputs pass variance filters that flag deviations from historical ratios, after which a senior analyst reviews assumptions with the primary-research team. Models refresh each year, and we trigger interim updates when material events, large spectrum auctions or major vendor exits, shift the baseline.

Why Mordor's Media Gateway Baseline Stands Firm

Benchmark comparison

Published figures frequently diverge because researchers choose different inclusion rules, currency bases, and update cadences. Our analysts document every assumption, so clients see exactly how traffic patterns convert into gateway dollars.

Key gap drivers usually trace to scope (for example, some studies drop virtual gateways), aging price decks, or one-off scenario pushes that inflate aggressive cases. By anchoring forecasts to verifiable telecom indicators and by refreshing annually, Mordor Intelligence reduces such drift.

| Market Size | Anonymized source | Primary gap driver | ||

|---|---|---|---|---|

USD 2.97 B (2025) | Mordor Intelligence | - | Anonymized source:Mordor Intelligence | Primary gap driver:- |

USD 2.47 B (2024) | Global Consultancy A | Excludes cloud-native deployments; older FX averages | ||

USD 2.83 B (2024) | Market Database B | Counts hardware only, omits software revenue | ||

USD 3.13 B (2025) | Industry Journal C | Blends session border controllers into scope |

Pricing Strategy for Semiconductor Components

3 Min Read

Accelerating Additive Manufacturing Adoption in India

3 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.