5G Private Network Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

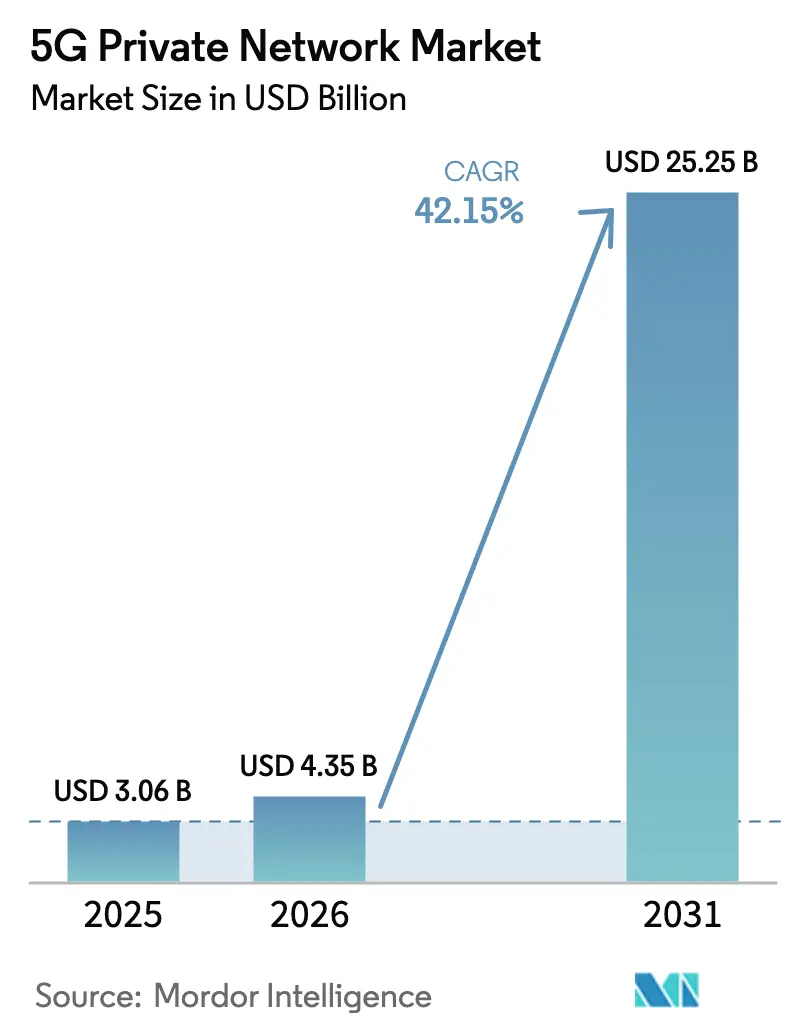

| Market Size (2026) | USD 4.35 Billion |

| Market Size (2031) | USD 25.25 Billion |

| Growth Rate (2026 - 2031) | 42.15% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

5G Private Network Market Analysis by Mordor Intelligence

The 5G Private Network Market size is expected to grow from USD 3.06 billion in 2025 to USD 4.35 billion in 2026 and is forecast to reach USD 25.25 billion by 2031 at 42.15% CAGR over 2026-2031.

Growing preference for deterministic cellular connectivity over Wi-Fi, the global roll-out of 5G Standalone cores, and liberalized local-licence spectrum schemes underpin this expansion. Declining prices of 5G industrial IoT modules and small cells further lower entry barriers, allowing mid-tier manufacturers, ports, and utilities to justify new deployments. Strategic collaborations between network vendors and hyperscalers accelerate adoption by bundling managed services with edge compute for data-sovereign workloads. Together, these forces position the 5G private network market for sustained double-digit growth while reshaping enterprise connectivity strategies across regions and verticals.

Key Report Takeaways

- By vertical, Manufacturing led with 32.35% revenue share of the 5G private network market in 2025, while Healthcare is projected to grow at a 42.78% CAGR through 2031.

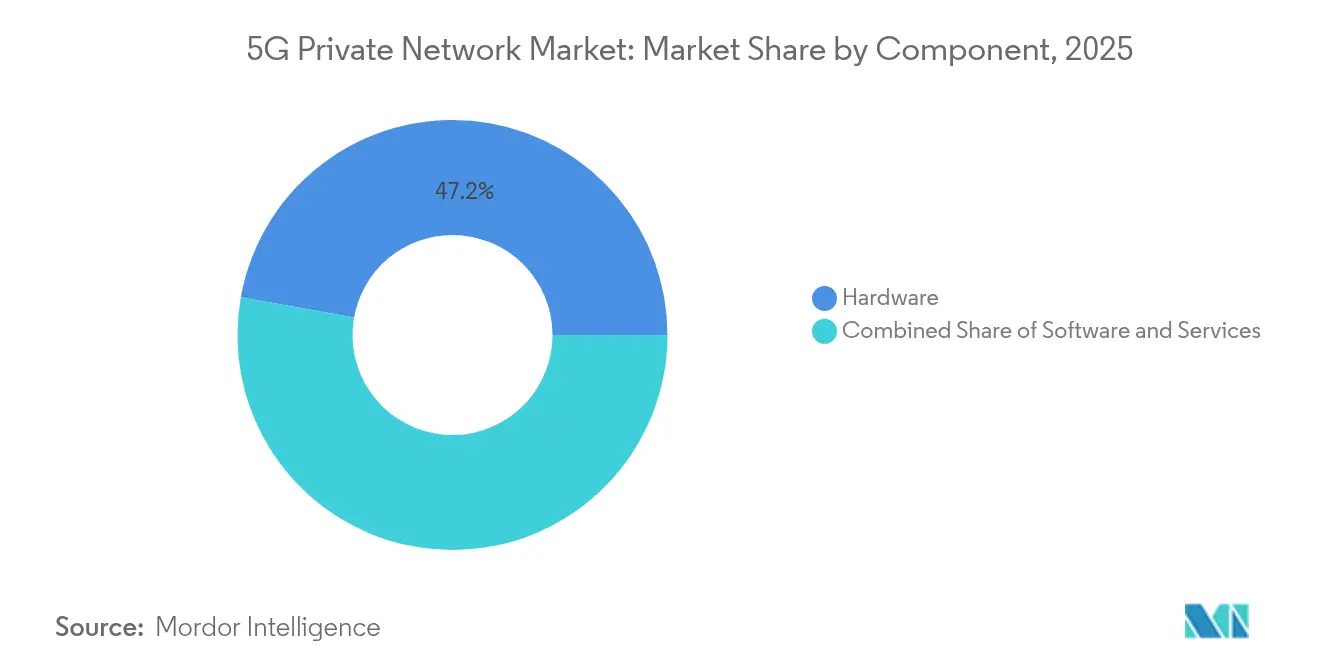

- By component, Hardware held 47.20% of the 5G private network market share in 2025, but Services are anticipated to expand at a 44.10% CAGR between 2026-2031.

- By frequency, Sub-6 GHz accounted for 61.10% share of the 5G private network market size in 2025; mmWave deployments are advancing at a 43.80% CAGR over the same period.

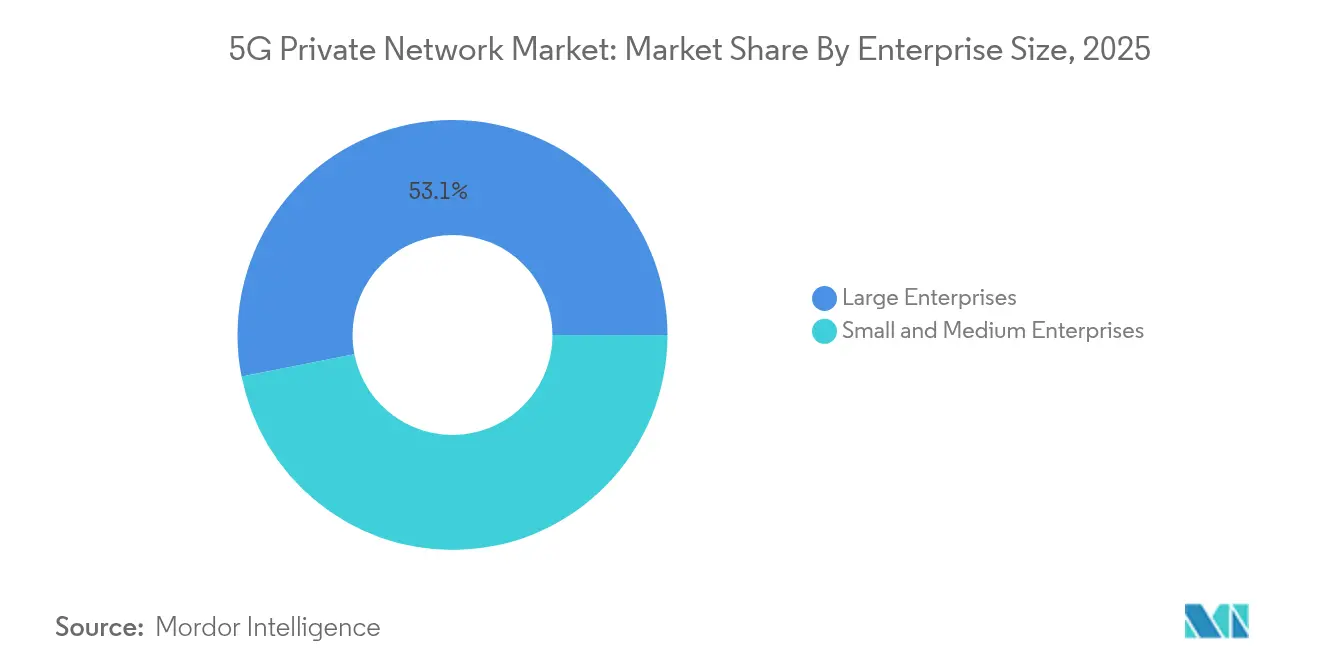

- By enterprise size, Large enterprises controlled 53.10% of the 5G private network market in 2025, whereas SMEs are forecast to post a 43.25% CAGR to 2031.

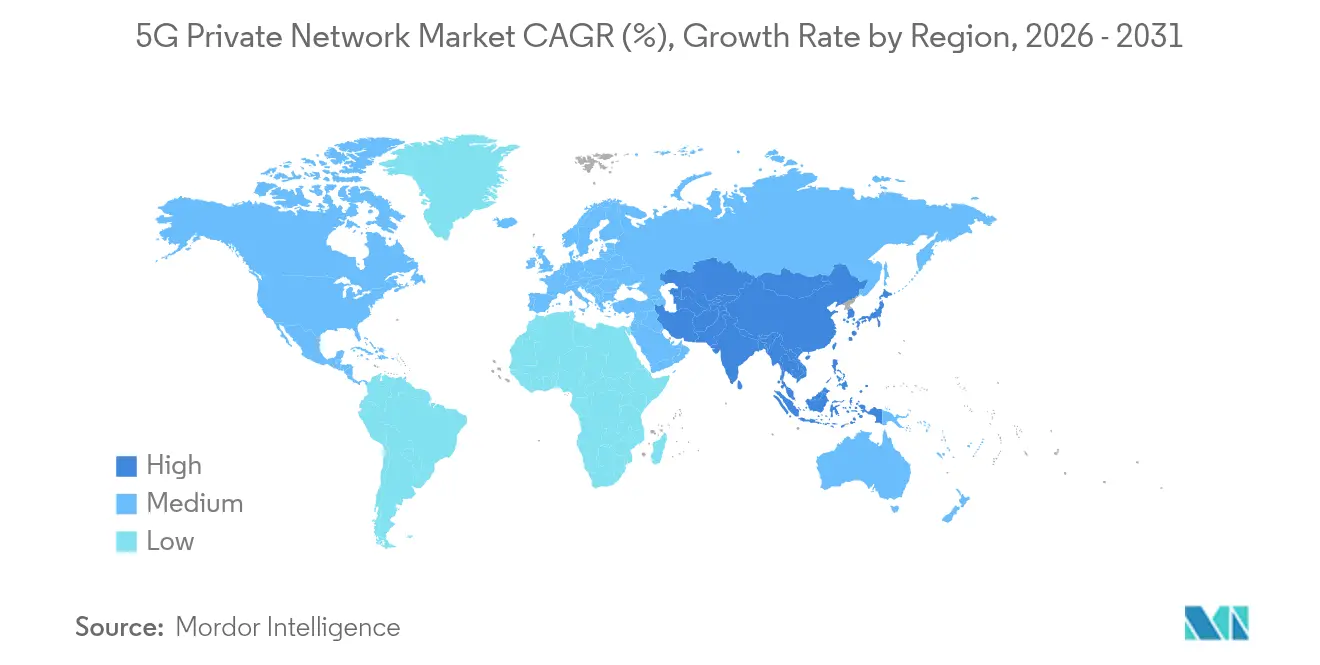

- By geography, North America captured 30.50% of the 5G private network market in 2025; Asia-Pacific is expected to record a 44.00% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global 5G Private Network Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mature 5G SA core availability for SASE integration | 8.20% | North America, EU, Asia | Medium term (2-4 years) |

| 700 MHz, CBRS & local-licence spectrum liberalisation | 7.50% | North America, Asia-Pacific | Short term (≤ 2 years) |

| Falling price of 5G-IIoT modules & private-RAN small cells | 6.80% | Global with a manufacturing focus in Asia | Medium term (2-4 years) |

| Edge-native 5G network-as-a-service offers from hyperscalers | 5.90% | Global developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Mature 5G SA Core Availability for Enterprise SASE Integration

Cloud-native 5G Standalone cores now ship with built-in SASE functions, allowing enterprises to apply zero-trust policies across OT and IT domains from a single pane of glass. Ericsson and Google Cloud jointly run 5G Core-as-a-Service, giving manufacturers elastic scaling without on-site EPC specialists. Microsoft mirrors this model by embedding a full 5G core inside Azure Stack Edge so that regulated facilities can retain data on-prem while managing the network from the Azure portals. Unified identity, segmentation, and traffic optimisation cut integration time for multi-site factories and logistics hubs. Early adopters report faster rollout cycles and reduced maintenance overhead because policy updates propagate automatically to every site. Together, these efficiencies raise the attainable ROI threshold, broadening the addressable base for the 5G private network market.

700 MHz, CBRS & Local-Licence Spectrum Liberalisation

Shared and lightly licensed spectrum unlocks private networks for entities that do not own nationwide mobile concessions. The FCC’s expanded CBRS rules lengthen transmission windows and trim Dynamic Protection zones, giving utilities and campuses predictable radio conditions. Japan’s local 5G model has already issued 153 Sub-6 GHz licences, proving that simplified processes can fast-track enterprise networks. NTIA data show more than 270,000 new CBRS device activations since 2021, many in rural manufacturing clusters[1]National Telecommunications & Information Administration, “CBRS Deployment Data 2021-2024,” ntia.gov. Access to affordable spectrum lowers total cost of ownership, pressures operators to offer wholesale slices, and propels the 5G private network market toward wider vertical adoption.

Falling Price of 5G-Industrial IoT Modules & Private-RAN Small Cells

High-volume chipsets now integrate RF, baseband, and security primitives on a single die, shrinking 5G IIoT module ASPs by double-digit percentages over two years. Sub-$150 industrial routers let mid-sized factories retrofit robotics without tearing out Ethernet runs. ZTE’s hospital pilot cut upgrade costs by 80% and installation time by 90%, demonstrating the capex impact of cheaper radios. While shortages linger for multimode SA/NSA chipsets, multi-sourcing and vendor-financed inventory buffers help maintain rollout schedules. Lower hardware cost widens addressable use cases, amplifying demand across the 5G private network market.

Edge-Native 5G Network-as-a-Service Offers from Hyperscalers

AWS, Microsoft, and Google now pre-integrate 5G cores with edge compute so enterprises can spin up private slices under a pay-per-use model. Verizon and NVIDIA demonstrate AI inference over such edge nodes, turning quality-of-service into a variable cost rather than a fixed asset. Consumption pricing lets seasonal industries like ports boost bandwidth during peak flows without stranded capex. Hyperscaler reach also standardises DevOps pipelines, enabling continuous application deployment across thousands of micro-cells. As a result, enterprises that once lacked radio expertise can outsource complexity and still meet latency or sovereignty mandates, fuelling long-run expansion of the 5G private network market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Scarcity of multi-band certified 5G devices for vertical-specific use | −4.3% | Global industrial & healthcare | Medium term (2-4 years) |

| Complex systems-integration skill gap at mid-tier partners | −3.8% | Global, acute in emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Scarcity of Multi-Band Certified 5G Devices for Vertical-Specific Use Cases

Enterprises often require devices that roam across Sub-6 GHz and mmWave bands while meeting stringent safety or sterility norms. Yet only a handful of suppliers certify rugged tablets, cameras, or AR headsets across all target bands, forcing hybrid network designs that raise support costs. Healthcare deployments struggle even more because medical device approvals add another regulatory layer. Until broader certification coverage emerges, device scarcity will temper the pace at which new verticals join the 5G private network market.

Complex Systems-Integration Skill Gap at Mid-Tier Integrators

Private 5G converges RF planning, MEC, IT security, and OT automation. Most regional system integrators know Wi-Fi but lack spectrum engineering and core orchestration skills, leading enterprises to delay or down-scope projects. Specialist consultancies are scarce outside mature markets, inflating project costs for SMEs. Vendor-led turnkey models help but limit customisation. Persistent skill shortages therefore subtract a modest, but material drag on the 5G private network market growth outlook.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Expand as Integration Demands Rise

Hardware commanded 47.20% of the 5G private network market in 2025, reflecting the upfront spend on radios, evolved packet cores, and edge compute clusters. Yet, Services are projected to grow at a 44.10% CAGR, outpacing equipment sales as enterprises favour managed lifecycle models. Nokia finds 78% of customers achieve payback within six months when adopting a service-led rollout, thanks to faster commissioning and continuous optimisation. The shift also mirrors the spread of cloud-native orchestration, which moves value from boxes to software and support. As complexity rises, managed detection and response, performance tuning, and application onboarding become core revenue streams. Consequently, Services will narrow the revenue gap with Hardware by 2030, reshaping vendor monetisation across the 5G private network market.

Software sits between the two, providing policy control, network slicing, and digital twin analytics that translate radio data into business insights. Low-code orchestration lets OT engineers spin up slices for new production lines without ticketing an operator. Over time, Software margins are likely to exceed both Hardware and Services, but their growth pace will track platform adoption curves. Together, these dynamics ensure the 5G private network industry remains a multi-revenue-stream arena where integration value grows fastest.

By Frequency: Sub-6 GHz Dominates Coverage, mmWave Fuels Capacity

Sub-6 GHz held 61.10% share of the 5G private network market size in 2025 because one-kilometre cell radii suit large plants, mines, and campuses. Rugged handhelds and sensors also favour mid-band because antenna footprints stay small. mmWave, while confined to tens-of-metre footprints, posts a 43.80% CAGR as factories deploy high-definition machine vision and AR maintenance at workstations. Hybrid deployments emerge, mid-band provides blanket coverage, mmWave overlays pump gigabits to assembly cells. Open-RAN roadmaps that support dual-band radios promise to simplify such mixed topologies, boosting uptake.

This nuanced spectrum play widens vendor differentiation. RAN suppliers with beamforming optimisations for reflective indoor spaces win mmWave bids, whereas incumbents strong in macro radio planning dominate Sub-6 GHz tenders. Over the forecast horizon, mmWave’s share will rise yet remain below mid-band because many brownfield plants cannot justify dense small-cell grids. Even so, the combined spectrum toolkit cements private 5G as a superior upgrade path over Wi-Fi 7 for industrial digitalisation.

By Enterprise Size: SMEs Gain Ground via Opex-Friendly Models

Large enterprises retained 53.10% control of the 5G private network market in 2025, but SMEs are on track for a 43.25% CAGR through 2031. Vendor financing, consumption pricing, and prefabricated edge kits reduce entry pain for smaller factories and campuses. Comcast Business proves the neutral-host approach at the University of Virginia, where multiple carriers share a single CBRS infrastructure to lower total cost. Such models let SMEs secure deterministic coverage without becoming mobile operators.

At the same time, large multinationals push complexity boundaries by deploying private 5G across dozens of plants on three continents. They require global SIM lifecycle management, roaming governance, and zero-trust overlays. Consequently, solution providers must straddle both ends of the customer spectrum, delivering simplified starter kits for SMEs and hyper-scalable orchestration for Fortune 500 clients. This duality will define competitive positioning throughout the 5G private network market.

By Vertical: Manufacturing Leads, Healthcare Accelerates

Manufacturing commanded a 32.35% share of the 5G private network market in 2025, anchored by proven use cases such as AGV fleet optimisation and real-time quality inspection. Predictable ROI, cyber-hardened isolation, and ease of retrofitting keep factories at the forefront of adoption. However, Healthcare tops the growth chart with a 42.78% CAGR to 2031. Europe’s Oulu Hospital demonstrates latency-sensitive patient monitoring on a standalone private 5G core, validating mission-critical reliability. Regulatory moves toward remote surgery trials further stoke demand.

Energy & Utilities, Transportation & Logistics, and Defense follow close behind, each leveraging deterministic connectivity for safety-critical controls. Southern California Edison’s grid-modernisation blueprint shows how utilities integrate LTE relay layers with 5G micro-cells for fault isolation in milliseconds. Such cross-vertical momentum broadens solution portfolios, sustaining multi-decadal opportunity across the 5G private network market.

Geography Analysis

North America captured 30.50% of the 5G private network market in 2025, thanks to ready CBRS spectrum, early IIoT pilots, and strong federal funding for critical-infrastructure modernisation. Manufacturing clusters in the Midwest and Gulf Coast rapidly migrate from Wi-Fi because cellular provides interference-immune mobility for autonomous robots. Public-safety agencies also invest, with Verizon offering dedicated 5G slices for first responders across 29 cities, ensuring priority communications during congestion.

Asia-Pacific is forecast to record a 44.00% CAGR, narrowing the leadership gap by 2031. Japan’s regulator issues dedicated local-licence spectrum in both Sub-6 GHz and 4.7 GHz bands, prompting more than 150 enterprise networks within two years. China pilots 5.5G (5G-Advanced) features such as deterministic scheduling and RedCap devices, underpinning large-scale campus deployments in automotive and mining. Emerging economies like India ride the Production-Linked Incentive scheme to embed private 5G in new semiconductor fabs and logistics parks, further boosting regional momentum.

Europe follows with a slower but steady uptake as spectrum fees remain higher and industrial policy varies by member state. Nonetheless, initiatives like Germany’s Industrie 4.0 subsidies and France’s smart-city pilots keep demand rising. The Port of Riga’s private 5G for autonomous sea drones proves how EU maritime corridors can extend coverage 100 miles offshore, a feat unviable with Wi-Fi links. South America and the Middle East & Africa remain in nascent stages, yet early oil, gas, and mining proofs hint at rising demand once device availability widens. Taken together, regional dynamics ensure the 5G private network market gains depth as well as breadth over the forecast horizon.

Competitive Landscape

The market shows moderate consolidation; Nokia alone holds about 55% share of deployed private wireless networks, leveraging turnkey bundles spanning RAN, core, and digital-twin applications. Ericsson follows by pairing its Enterprise Wireless Solutions unit with Google Cloud and AWS Wavelength, targeting USD 1.5 billion enterprise revenue by 2027. Samsung, Huawei, and ZTE concentrate on defense, ports, and mega-factory projects, progressively eroding incumbent shares outside North America.

Strategic playbooks center on vertical-specific blueprints. Nokia curates “Factory-in-a-Box” reference architectures for automotive lines, while Ericsson pilots “Hospital-in-a-Cloud” bundles with real-time patient analytics. Hyperscalers enter via edge zones: Azure Private MEC, AWS Private 5G, and Google Distributed Cloud Host each integrate 5G core functions into existing cloud footprints. Specialists such as Celona and Betacom address the SME niche with subscription-priced CBRS kits that include SIM lifecycle management. As vendors jostle, partner ecosystems widen to cover industrial automation, security, and analytics, making solution breadth a decisive factor in the 5G private network market.

M&A and investment trends echo this convergence. In 2024, Ericsson bought a slice-management start-up to embed per-application QoS controls into its core. Huawei channelled CNY 179.7 billion into R&D, pivoting toward AI-optimised radios amid export restrictions. Meanwhile, operators like Verizon and T-Mobile launch network-slicing products for public-safety customers, blurring the line between public and private domains. Over the planning period, competitive intensity will hinge less on hardware supremacy and more on ecosystem orchestration and domain knowledge.

5G Private Network Industry Leaders

Telefonaktiebolaget LM Ericsson

Nokia Corporation

Samsung Electronics Co., Ltd.

AT&T Inc.

Verizon Communications

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Ericsson launched “Ericsson On-Demand,” a SaaS 5G core platform with Google Cloud that bills on elastic consumption.

- June 2025: Ericsson deployed a city-wide private 5G network in Istres, France, to support encrypted video surveillance and public-safety communications.

- May 2025: The Freeport of Riga activated a private 5G link for cargo ships and autonomous sea drones, extending coverage 100 miles offshore.

- February 2025: Samsung and KT deployed a private 5G network for the Korean Navy to bolster secure maritime communications.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the 5G private network market as all standalone or hybrid 5G radio-access and core systems that are engineered, owned, or leased by an enterprise, campus, or government agency for its exclusive use; revenue covers hardware, software, and recurring managed services sold in licensed, shared, or unlicensed spectrum. According to Mordor Intelligence, this market reached USD 3.06 billion in 2025 and is projected to touch USD 18.68 billion by 2030.

Scope exclusion: Wi-Fi, public 5G slices delivered from macro networks, and 4G-only private LTE installations are not counted.

Segmentation Overview

- By Component

- Hardware

- Software

- Services

- By Frequency

- Sub-6 GHz

- mmWave (More than 24 GHz)

- By Enterprise Size

- Small and Medium Enterprises

- Large Enterprises

- By Vertical

- Manufacturing

- Energy and Utilities

- Transportation and Logistics

- Oil and Gas

- Healthcare

- Defense and Public Safety

- Enterprises and Campus

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- South Africa

- Rest of Middle East and Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed spectrum regulators, industrial-IoT integrators, private-network operators, and CFOs at factories across North America, Europe, and Asia. The conversations clarified live device counts, project budgets, and migration timelines, and they provided real-time feedback on assumptions that desk work alone could not reveal.

Desk Research

We started with public data series from bodies such as the GSMA, 3GPP, the Federal Communications Commission, and the European Spectrum Observatory, which map band releases and licence uptake. Trade associations like 5G-ACIA, GSA, and the CBRS Alliance supply adoption dashboards, while filings from listed equipment vendors illuminate shipment trends and average selling prices. Our team also drew company 10-Ks, investor decks, regional import-export manifests, and peer-reviewed papers on 5G URLLC performance. Select paid databases, including D&B Hoovers for enterprise spending and Dow Jones Factiva for project announcements, helped validate customer wins. The sources named above are illustrative; many additional records were examined to complete the evidence base.

Market-Sizing & Forecasting

We built a top-down model in which national spectrum releases, industrial value-added output, and average cell-site costs generate the demand pool, which is then cross-checked through selective bottom-up roll-ups of vendor shipments and sampled campus deployments. Key variables include CBRS licence activations, the count of 5G-SA devices certified, industrial automation CAPEX, the average selling price of small cells, the number of private-network contracts announced, and regional manufacturing PMI indices. Multivariate regression links these drivers to revenue, while scenario analysis adjusts for spectrum-pricing shocks and device shortages. Gaps in bottom-up data are bridged with median cost curves confirmed during interviews.

Data Validation & Update Cycle

Before sign-off, a second analyst triangulates the model with independent metrics such as tender volumes and carrier financials, and any variance beyond five percent triggers re-checks with sources. Reports refresh every twelve months, and we issue interim updates when policy or supply events materially shift the baseline.

Why our 5G Private Network Baseline commands reliability

Published estimates often diverge because firms pick different inclusion rules, cost lines, and refresh cadences. Our disciplined scope, the use of live spectrum-release data, and annual primary-source calibration keep Mordor's numbers anchored, whereas other publishers may pool public slices or mix 4G and 5G revenues, inflating totals. Additional gaps arise when some studies apply aggressive mmWave uptake or one-time licence fees without normalizing currency year.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 3.06 B | Mordor Intelligence | - |

| USD 3.86 B | Global Consultancy A | mixes public-slice revenue and treats spectrum fees as sales |

| USD 2.69 B (2024) | Industry Association B | aggregates 4G and 5G figures and excludes managed services |

| USD 2.93 B (2024) | Regional Consultancy C | counts device hardware only, omits recurring service revenue |

In short, our framework traces every dollar to clear variables, validates assumptions with front-line experts, and revises swiftly, so decision-makers receive the most balanced and transparent baseline.

Key Questions Answered in the Report

What is the current value of the 5G private network market?

The 5G private network market size is USD 4.35 billion in 2026.

How fast will the market grow over the next five years?

The market is expected to register a 42.15% CAGR, lifting revenue to USD 25.25 billion by 2031.

Which segment of the market is expanding the quickest?

Services, covering integration and managed operations, are forecast to grow at a 44.10% CAGR.

Why are manufacturers early adopters of private 5G?

Deterministic connectivity improves robotic automation, asset tracking and quality control, delivering clear ROI.

What spectrum bands do enterprises prefer?

Sub-6 GHz delivers broad coverage, while mmWave satisfies ultra-high-bandwidth tasks such as AR and machine vision.

Can small and medium enterprises afford private 5G?

Yes. Financing programs and network-as-a-service models reduce capex, enabling SMEs to adopt at a 43.25% CAGR pace.

Page last updated on: