Small Cell 5G Network Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 8.54 Billion |

| Market Size (2031) | USD 33.2 Billion |

| Growth Rate (2026 - 2031) | 31.20% CAGR |

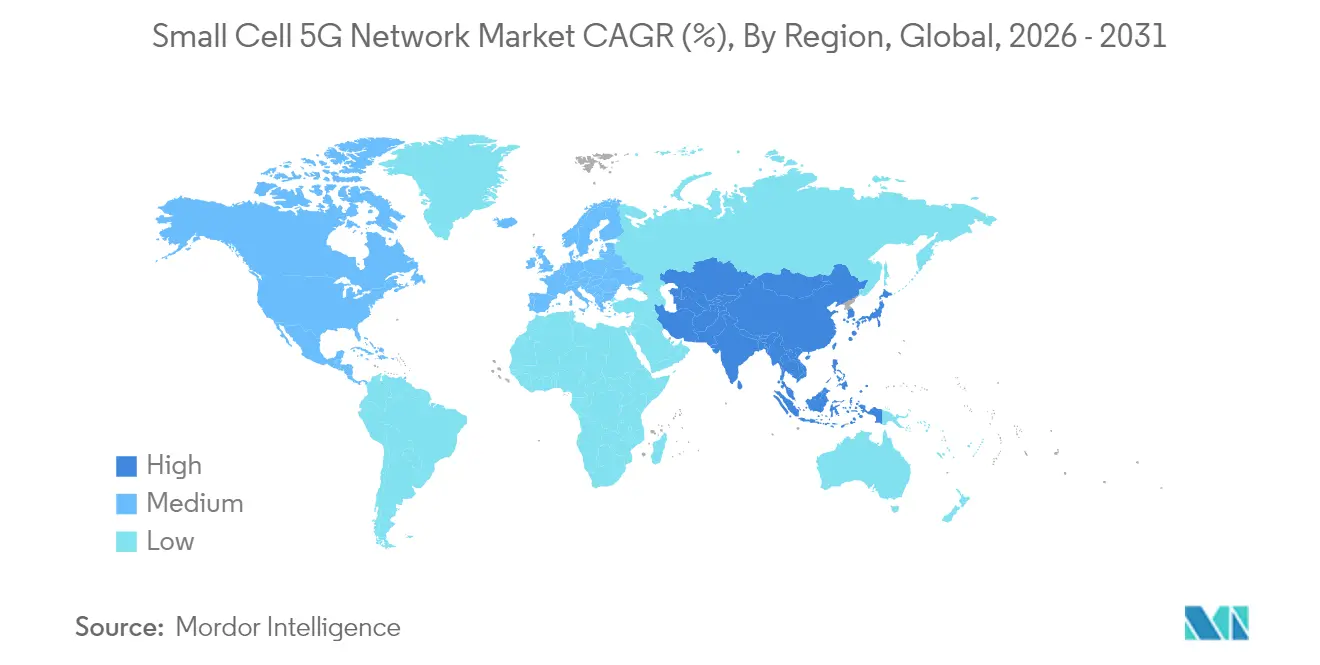

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Small Cell 5G Network Market Analysis by Mordor Intelligence

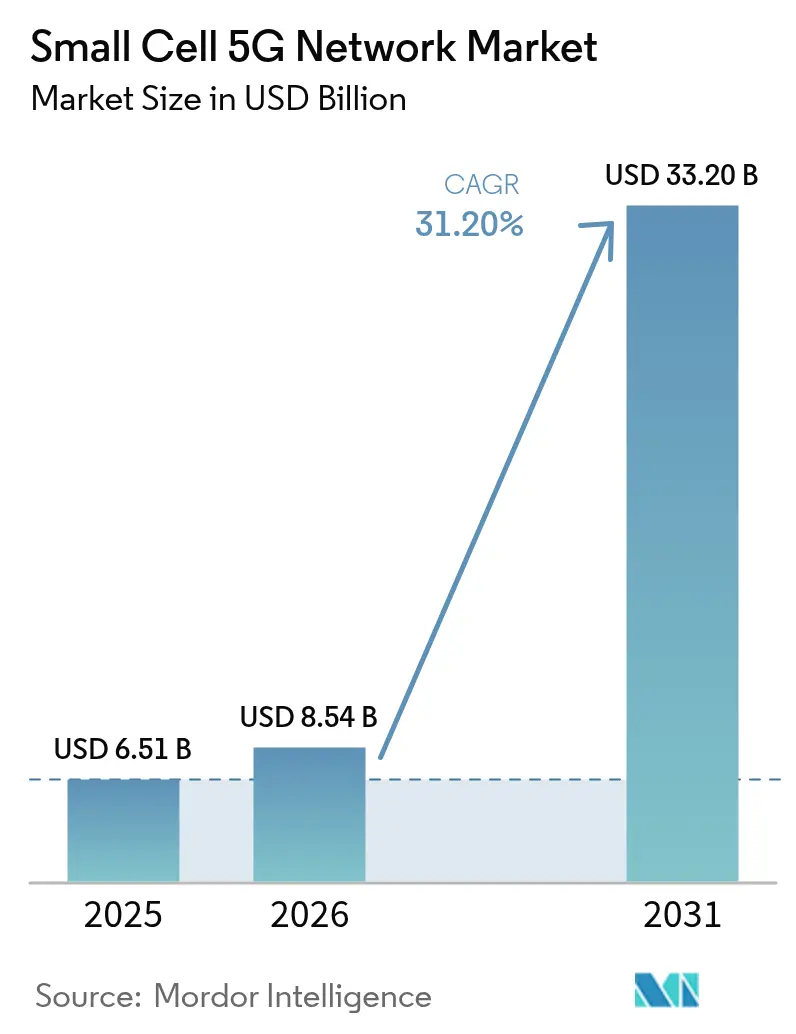

The Small Cell 5G Network market size is expected to grow from USD 6.51 billion in 2025 to USD 8.54 billion in 2026 and is forecast to reach USD 33.2 billion by 2031 at 31.2% CAGR over 2026-2031.

Ongoing densification in urban corridors, enterprise digitalization, and the roll-out of AI-native network management systems are accelerating uptake across telecom operators and private-network deployments. Picocells, neutral-host models, and Release-17 NR-U capabilities are expanding addressable use cases by easing spectrum and site constraints. Asia Pacific commands attention through infrastructure scale, yet North America converts infrastructure into premium revenue more efficiently, while Europe’s regulatory clarity promises a delayed but sizable second wave of growth. Competitive dynamics feature established radio vendors pivoting toward software-defined architectures even as AI-enabled chipmakers and Open RAN specialists carve out niches.

Key Report Takeaways

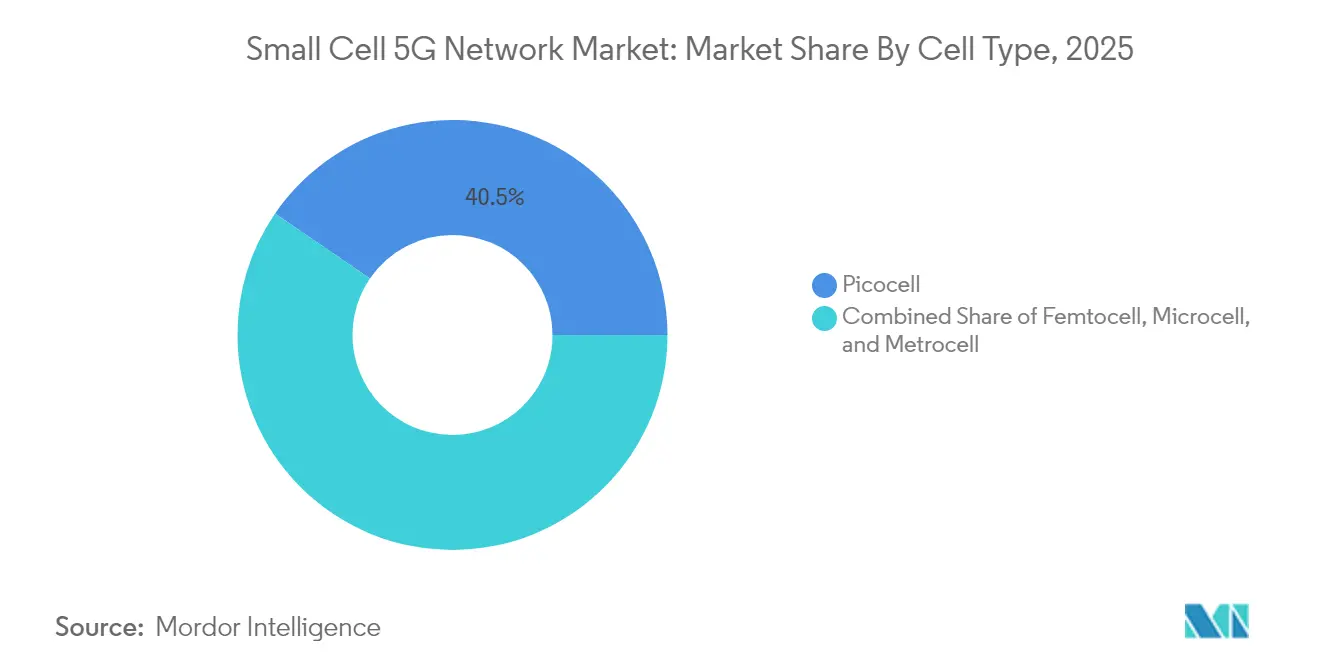

- By cell type, picocells led with a 40.45% revenue share of the Small Cell 5G Network market in 2025, while mmWave picocells are projected to post the fastest 35.2% CAGR through 2031.

- By operating environment, indoor systems accounted for 62.10% of the Small Cell 5G Network market share in 2025; outdoor deployments are forecast to rise at a 32.4% CAGR through 2031.

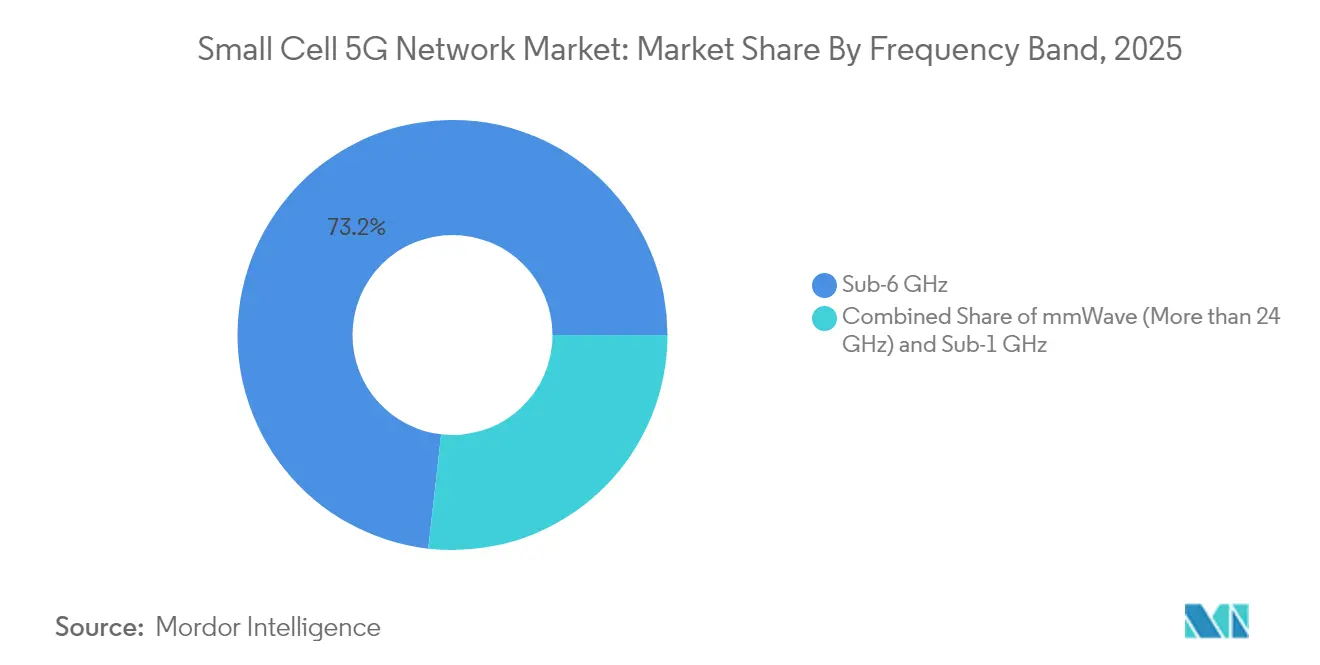

- By frequency band, sub-6 GHz held 73.20% of the Small Cell 5G Network market size in 2025; mmWave solutions are expanding at a 35.9% CAGR to 2031.

- By end user, telecom operators retained 55.15% of 2025 revenue, yet enterprise private networks are advancing at a 32.35% CAGR across the forecast window.

- Asia Pacific captured 37.60% of global revenue in 2025; North America achieved the highest monetization per site, supported by a USD 14 billion contract between AT&T and Ericsson.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Small Cell 5G Network Market Trends and Insights

Drivers Impact Analysis*

| Driver | Impact on CAGR Forecast (~%) | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid densification needs in urban 5G rollouts | +8.20% | Global, concentrated in Asia Pacific and North America | Medium term (2–4 years) |

| Enterprise private network demand (manufacturing, logistics) | +7.80% | Global, led by China, Germany, the US, manufacturing hubs | Long term (≥ 4 years) |

| Release-17 5G NR-U enabling unlicensed small-cell spectrum | +4.10% | North America and the EU regulatory domains | Short term (≤ 2 years) |

| AI-driven self-optimizing networks cutting OpEx | +5.20% | Global, early adoption in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid densification needs in urban 5G rollouts

Operators have confirmed that macro cells alone cannot satisfy 5G service-level agreements in dense cities. EE has activated more than 1,000 small cells across the United Kingdom, with 25 London sites moving 7.5 TB of data each week, easing congestion in traditional sectors. Virgin Media O2 introduced the first UK 5G standalone small cells, unlocking network slicing and lower latency that macro sites cannot match. Fractional frequency reuse within small cells improves spectrum utilization, which is critical as uplink-heavy applications such as AR and industrial IoT become mainstream. Municipalities are cutting red tape, and more than 100 neutral-host installations are now live worldwide. Combined, these factors reinforce the densification imperative over the medium term.

Enterprise private-network demand (manufacturing, logistics)

Government policy and Industry 4.0 roadmaps are pushing factories and logistics sites toward deterministic wireless connectivity. China already hosts roughly 4,000 5G factory networks and targets 10,000 by 2027. Nokia counted 850 private 5G customers by Q4 2024, adding 55 in a single quarter. Operational outcomes are compelling: a Thai appliance plant reported 15-20% productivity gains after 5G-enabled automation. Seven European states now license the 26 GHz band locally, and six allocate 100 MHz in the 3.4-3.8 GHz range, making spectrum procurement easier for enterprises. Small cells remain the preferred radio layer because they enforce tight coverage boundaries, integrate edge compute, and support concurrent network slices.

Release-17 5G NR-U enabling unlicensed small-cell spectrum

The new specification lets 5G radios operate in 5 GHz and 6 GHz bands, cutting spectrum costs that once dominated the total cost of ownership. The United States allowed very-low-power use across the entire 6 GHz band in December 2024, while Brazil approved 6425-7125 MHz for IMT in January 2025. Listen-before-talk protocols coexist with Wi-Fi and guarantee service quality for mission-critical users. Removing licensing fees accelerates rollout timelines, giving neutral hosts a viable business case in indoor venues and public hot spots.

AI-driven self-optimizing networks cutting OpEx

Deutsche Telekom has demonstrated AI-assisted planning that cuts manual tasks while lifting key performance indicators. Samsung’s Energy Saving Manager dynamically adapts power levels, lowering energy consumption in live networks. Machine learning also predicts component failures and orchestrates interference mitigation between adjacent cells. As algorithms train on localized traffic patterns, performance and savings compound without fresh capital expenditure.

Restraints Impact Analysis*

| Restraint | Impact on CAGR Forecast (~%) | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Challenging fiber/backhaul economics in suburban & rural zones | –6.8% | Global, acute in rural North America, and developing markets | Long term (≥ 4 years) |

| Persistent security concerns around Open RAN small cells | –3.1% | Enterprise segments, globally, government networks | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Challenging fiber/backhaul economics in suburban and rural zones

Aerial fiber construction costs between USD 60,000 and USD 170,000 per mile in suburbs, depressing returns where population density is low. Crown Castle shelved 7,000 U.S. small-cell sites, preserving USD 800 million in future capital spending, after recognizing unfavorable backhaul math. Microwave and satellite backhaul trim capex but cannot yet meet 5G capacity or latency targets. Federal Highway Administration data show that using micro-trenching still leaves a six-to-eight-year breakeven in suburban settings[3]Federal Highway Administration, “Fiber Deployment Cost Quick Reference,” ops.fhwa.dot.gov. Consequently, operators hesitate to densify beyond profitable metros until next-generation wireless backhaul proves commercially viable.

Persistent security concerns around Open RAN small cells

Academic audits have documented over 100 vulnerabilities in LTE and 5G, many linked to open interfaces that broaden the attack surface. The O-RAN Alliance is standardizing threat models and test specifications, yet multi-vendor integration remains complex. Researchers have demonstrated KPI poisoning that cripples near real-time control loops, and adversarial AI attacks can slash network throughput. Enterprises and public agencies demand more thorough supply-chain assurance before adopting Open RAN-based small cells at scale, slowing uptake in security-sensitive verticals.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Cell Type: Picocells Lead Dense Urban Deployments

Picocells contributed 40.45% of 2025 revenue, confirming their suitability for 100-200 m coverage zones in crowded downtown corridors. The Small Cell 5G Network market size for picocells is on course to expand sharply as mid-band spectrum and multi-user MIMO raise per-site capacity. mmWave picocells show the sharpest 35.2% CAGR, propelled by private networks and fixed wireless access that exploit 28 GHz and 39 GHz to deliver multi-gigabit throughput. Silicon innovation, such as EdgeQ’s base-station-on-a-chip, brings integrated AI that shrinks power, cost, and footprint.

Femtocells hold niche residential and small-office positions but face pressure from Wi-Fi 7, while microcells support wider suburban blocks where picocell density is cost-prohibitive. ORAN-compliant micro-radio units from Comba Telecom reflect a drift toward standardized multi-vendor ecosystems. As AI-enabled optimization narrows performance gaps between form factors, operators gain flexibility to match each site’s capacity requirements without sacrificing operating efficiency.

By Operating Environment: Indoor Dominance Faces Outdoor Growth Surge

Indoor sites represented 62.10% of 2025 deployments, since mid-band 5G signals fade through modern building materials. Neutral-host systems and smart-building management keep indoor investments compelling for enterprises seeking quality-of-service across offices, stadiums, and factories. The outdoor category is accelerating at a 32.4% CAGR as faster municipal permitting, Release-17 NR-U, and shared infrastructure lower siting friction. Initiatives such as Virgin Media O2’s outdoor cells in central Manchester underline this pivot.

Hybrid solutions are emerging, with Freshwave integrating all four UK carriers into a single outdoor-indoor small cell enclosure, cutting costs by 65% and energy by 60% relative to earlier systems. Indoor providers must now defend against Wi-Fi 7, which advertises 46 Gbps theoretical speeds, by highlighting deterministic latency, security, and slice management that Wi-Fi cannot match.

By Frequency Band: Sub-6 GHz Stability Meets mmWave Innovation

Sub-6 GHz maintained 73.20% of shipments in 2025, offering the best mix of propagation and capacity for mainstream deployments. Carrier aggregation and dynamic spectrum sharing help operators maximize spectral efficiency while preserving network economics. The mmWave segment is scaling at a 35.9% CAGR, buoyed by fixed wireless access and high-density enterprise zones. Ericsson, NBN Co, and Qualcomm recently validated 14 km mmWave links delivering gigabit speeds in rural Australia.

Extended-range performance plus AI-guided beam steering has moved mmWave beyond its original line-of-sight stigma. ZTE’s 30 Gbps FWA prototype positions mmWave as a fiber alternative for premium households and factories. Low-band sub-1 GHz retains value for coverage extension but remains a smaller contributor given tight spectrum inventories and modest throughput.

By End-User: Enterprise Acceleration Challenges Operator Dominance

Telecom operators still supplied 55.15% of 2025 revenue thanks to licensed spectrum and tower portfolios. Yet enterprise customers posted a 32.35% CAGR, outpacing all other user groups as Industry 4.0 digitization takes hold. The Small Cell 5G Network market size for enterprises is set to climb further as European regulators dedicate 26 GHz and mid-band spectrum to local permits.

Nokia’s tally of 850 private-network customers exemplifies enterprise momentum, while China alone supports 4,000 industrial sites and has set a 10,000-site target by 2027. Residential uptake lags because Wi-Fi remains cost-advantaged, but multi-tenant buildings are piloting neutral-host cells that serve several carriers without new indoor wiring. Emerging MVNO interest in managed private 5G promises another layer of competitive pressure on traditional operators.

Geography Analysis

Asia Pacific owns 37.60% of 2025 revenue and tracks a 31.95% CAGR to 2031, propelled by China’s 4.4 million 5G base stations and CNY 3 billion earmarked for 5G-Advanced overlays in 300 cities. China Unicom Beijing and Huawei achieved downlink peaks of 11.2 Gbps across a population of 10 million, setting a reference point for future dense overlays. Japan and South Korea push enterprise mmWave, and India’s post-auction build-out supplies scope for densification through public-private partnerships.

North America showcases revenue realization efficiency. Ericsson’s regional revenue climbed 55% year over year on the back of AT&T’s USD 14 billion contract, underlining robust investment returns. More than 50 U.S. neutral-host projects operate in CBRS, and Canada’s TELUS is rolling out the first commercial virtualized Open RAN, positioning the region at the forefront of cloud-native RAN experimentation. Still, Crown Castle’s canceled deployments highlight suburban economics as a persistent hurdle. Europe enjoys a clear spectrum policy yet lags in standalone 5G coverage, reaching only 2% penetration by late 2024. Virgin Media O2 and EE are ramping small-cell footprints, but many operators wait for a business-case inflection once device penetration rises. In the Middle East, the UAE logged record 30.5 Gbps 5G speeds, and du committed AED 2 billion to hyperscale data centers, signaling that Gulf operators will leapfrog directly to 5G-Advanced. Latin America sees Brazil’s Brisanet and Uruguay’s Antel expanding public 5G, though macroeconomic constraints and spectrum scarcity temper small-cell rollouts.

Regulatory Landscape

Small-cell 5G deployment economics are increasingly shaped by infrastructure-siting policy, with a focus on reducing municipal permitting delays, fees, and enforcement timelines. In the United States, the FCC opened additional scrutiny of local barriers through an infrastructure-focused NPRM (WT Docket No. 25-276, September 2025), and followed with further rulemaking activity in June 2026 that emphasizes shot-clock compliance and fee reasonableness for small wireless facilities under the Communications Act framework.

Standards work is also moving alongside these siting pressures. ETSI published 3GPP TS 38.300 v18.9.0 in April 2026 (Release 18), updating the overall NR description that ecosystem players use to align radio behavior, feature support, and certification workflows. Meanwhile, ongoing Release 19 work (including small-cell enhancement scenarios) keeps the standards roadmap active for indoor, outdoor, and shared-infrastructure small-cell configurations.

Competitive Landscape

Competition is moderate as long-standing infrastructure vendors wrestle with AI-centric silicon entrants and Open RAN service companies. Ericsson, Nokia, Samsung, and Huawei retain scale advantages but face price pressures from component inflation. EdgeQ raised USD 126 million to commercialize an AI-integrated base-station-on-a-chip, demonstrating investor appetite for disruptors.

Strategically, incumbents pivot to software differentiation. Ericsson partnered with Google Cloud to unveil 5G Core-as-a-Service, giving operators a cloud-native on-ramp that shrinks time-to-market and supports elastic scaling[2]Cloud Google, “Ericsson and Google Cloud unveil 5G Core-as-a-Service,” cloud.google.com. Samsung plans more than 53,000 commercial vRAN sites by 2025 and bundles Energy Saving Manager to reduce OpEx. Patent filings on extended-reality optimization and AI orchestration from Qualcomm, Meta, and Apple indicate a future battleground in user-experience-driven capacity planning.

Neutral-host specialists and private-network integrators carve out growth lanes where legacy vendor commercial models fall short. Shared infrastructure lowers cost barriers for property managers, while managed services offer appeal to enterprises lacking telecom expertise. Supply chain volatility favors bigger vendors that pre-book inventory, yet persistent shortages open doors for second-tier suppliers willing to customize radio modules in exchange for share gains.

Small Cell 5G Network Industry Leaders

Qualcomm Technologies Inc.

Huawei Technologies Co. Ltd

Telefonaktiebolaget LM Ericsson

Cisco Systems Inc.

Nokia Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Near-term whitespace is concentrated in operationally complex indoor and venue environments, where neutral-host and enterprise-owned networks reduce reliance on a single operator build plan and support multi-tenant coverage. Industry bodies including the Small Cell Forum framed 2026 as a critical year for reducing deployment complexity, with a push to scale neutral-host and enterprise models alongside carrier moves toward 5G standalone capabilities and higher automation in planning and optimization.

Rollout activity also points to opportunities tied to densification, industrial sites, and Open RAN-driven supply diversity. Virgin Media O2 reported around 2,500 small cells deployed by June 2026 (up from about 2,000 in 2025) to manage traffic growth, and in July 2026 O2 and Ontix announced small-cell deployment at Deeside Industrial Park in Wales using existing municipal street assets as hosting infrastructure. On the vendor side, Mavenir secured a supply agreement with MagtiCom (announced May 2026) for 4G and 5G small cells with deployments starting in Q2 2026, and AT&T expanded Open RAN small-cell rollouts to New York and Phoenix using radios from 1Finity (reported June 2026), highlighting how open interfaces, automation, and streamlined siting can translate into new procurement paths.

Recent Industry Developments

- July 2026: O2 and Ontix partnered to deploy 4G and 5G small cells at Deeside Industrial Park in Wales, leveraging existing municipal street assets for faster site access. The project targets industrial-park coverage and capacity needs that are difficult to satisfy with macro-only builds. It also reinforces neutral-host style collaboration models that can be replicated across dense towns and enterprise corridors.

- May 2026: Mavenir announced it was selected by MagtiCom to supply 4G and 5G small-cell technology for rollout across Georgia, with deployment starting in Q2 2026. The award expands Mavenir's footprint in operator-grade small cells and supports broader Open RAN-aligned procurement choices. It adds a reference deployment for vendors competing on flexible architectures and faster time-to-deploy.

- February 2025: Ericsson launched the Indoor Fusion Unit 8828, a compact 5G indoor solution positioned for small and medium-sized enterprise deployments. The product push aligns with indoor coverage being a major driver of small-cell demand where building materials degrade mid-band propagation. It strengthens vendor portfolios that bundle indoor radios, software, and support into repeatable enterprise deployment packages.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is defined as revenue generated from 5G small cell network nodes and closely linked software and services that enable dense indoor and outdoor 5G coverage and capacity. The sizing reflects spending tied to deploying and operating these low power radio access points for 3GPP-compliant 5G NR.

Scope exclusions: Large macro radio sites, 4G-only small cells, and passive distributed antenna systems are excluded from this market sizing.

Segmentation Overview

- By Cell Type

- Femtocell

- Picocell

- Microcell

- Metrocell

- By Operating Environment

- Indoor

- Outdoor

- By Frequency Band

- Sub-6 GHz

- mmWave (More than 24 GHz)

- Sub-1 GHz

- By End-User

- Telecom Operators

- Enterprises

- Residential

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- UAE

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by building a fact base from 5G rollout indicators, spectrum availability, and site densification levels, so the demand pool is realistic by region. We rely on public and official sources such as the ITU for telecom indicators, the FCC and other national spectrum regulators for band releases, and OECD and World Bank datasets for macro checks that influence infrastructure spending.

This is supported with practical industry references like operator and infrastructure company filings, investor presentations, and rollout announcements tied to coverage targets. For grounding unit economics, we also review standards and ecosystem notes from organizations such as 3GPP and GSMA, plus selective peer-reviewed engineering literature on small cell performance constraints. Where needed, paid subscriptions for company financials and intelligence, news and financials, and patent databases are used to confirm revenue exposure, product focus, and timing of technology shifts. The sources listed here are illustrative and not exhaustive, and other public references were also used to collect inputs, validate assumptions, and clarify gaps.

Primary Interviews and Surveys

Primary work focuses on what the desk model cannot fully capture, especially deployment pace, indoor versus outdoor mix, and how pricing moves as volumes scale. We speak with network planners, small cell solution teams, system integrators, and enterprise connectivity buyers across APAC, EMEA, and the Americas, so our assumptions on node counts, attach services, and upgrade cycles align with what is happening in the field.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 14% | APAC: 38% |

| Mid tier: 52% | Functional/Unit leaders: 32% | EMEA: 36% |

| Smaller Players: 17% | Managers: 54% | Americas: 26% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where regional 5G rollout intensity is reconstructed using indicators like 5G subscriber growth, licensed mid-band and mmWave spectrum availability, urban traffic density signals, and public coverage obligations. Those drivers are translated into expected small cell site additions by year, and then converted into value using typical node price ranges plus attach rates for software licenses, installation, and support.

To keep the totals grounded, the outputs are corroborated with selective bottom-up approximations, including supplier revenue exposure checks, sampled average selling price multiplied by estimated unit shipments, and channel feedback on project sizes in dense hot spots. In locations where the bottom-up view is incomplete, gaps are handled by scaling from markets with similar spectrum timing and densification patterns, and then adjusted after expert feedback. For forecasting, we use scenario analysis supported by operator capex outlook and planned densification programs. The scenarios are further tuned using interview consensus on timing of indoor enterprise rollouts and neutral host activity.

Data Validation & Update Cycle

Validation is done through triangulation across independent signals, then checked for odd jumps that do not match rollout reality. We compare implied node volumes, revenue per site, and regional shares against public coverage milestones, capex guidance, and the pacing of spectrum deployment, and any large variance is reviewed before final sign-off.

A multi-step internal review follows, where assumptions are challenged and recalculated if the model behavior looks inconsistent across regions or years. If major events occur, such as a sharp change in spectrum policy or a sudden capex shift, respondents are re-contacted to confirm the direction and likely magnitude. Reports are refreshed annually, with interim updates for material events, and a final pre-delivery pass is completed so clients receive the latest updated view.

Mordor Intelligence's Small Cell 5g Network Market Size Compared With Other Published Estimates

Published market sizes for small cell 5G networks can differ widely, even when the topic sounds the same, because scope and what gets counted as revenue are not consistent. Differences also come from how firms treat services, which year they anchor to, and how they convert rollout activity into dollars.

Passive distributed antenna systems are kept outside Mordor Intelligence's scope, and that exclusion can shift totals because some publications bundle DAS with small cells in venue coverage projects. Gaps also show up when one estimate counts only hardware nodes, while another adds installation and support, or when aggressive assumptions are used for mmWave densification and indoor enterprise uptake before those programs are widely funded.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 8.54 B (2026) | |

| Industry Research Publisher A | USD 10.73 B (2026) | Uses a broader growth runway and can apply faster scaling assumptions for deployments, which tends to lift the near-term value even when scope language looks similar. |

| Global Research Group B | USD 12.30 B (2026) | Often leans on a higher 2026 starting value by assuming stronger early densification in large cities and a fuller inclusion of related components and architectures in project budgets. |

The spread across sources is mainly explained by what adjacent infrastructure gets bundled, how much service revenue is attached to node sales, and how quickly early deployments are assumed to ramp. By tying the model to observable rollout signals and then rechecking value with practical volume times price checks, we keep a repeatable line of sight from demand drivers to the final number.

Key Questions Answered in the Report

What is the current value of the Small Cell 5G Network market?

The market is worth USD 8.54 billion in 2026 and is projected to expand at a 31.2% CAGR to USD 33.2 billion by 2031.

Which region leads the Small Cell 5G Network market?

Asia Pacific commands 37.60% of 2025 revenue, driven by China’s extensive 5G infrastructure and aggressive enterprise adoption.

Why are enterprises investing in private 5G small-cell networks?

Manufacturing and logistics firms need deterministic latency, localized data processing, and spectrum control, which small cells deliver more reliably than macro sites or Wi-Fi.

How important is mmWave to future small-cell growth?

The mmWave segment is forecast to grow at a 35.9% CAGR as extended-range breakthroughs enable fixed wireless access and high-capacity private networks.

What major restraint could slow small-cell deployment?

High fiber and backhaul costs in suburban and rural areas remain the most significant economic barrier, particularly in North America and emerging markets.

How are vendors differentiating their small-cell offerings?

Incumbents focus on software-defined and AI-optimized solutions, while new entrants target cost and integration advantages through Open RAN-compatible chipsets and neutral-host models.

Page last updated on: