Contact Center Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

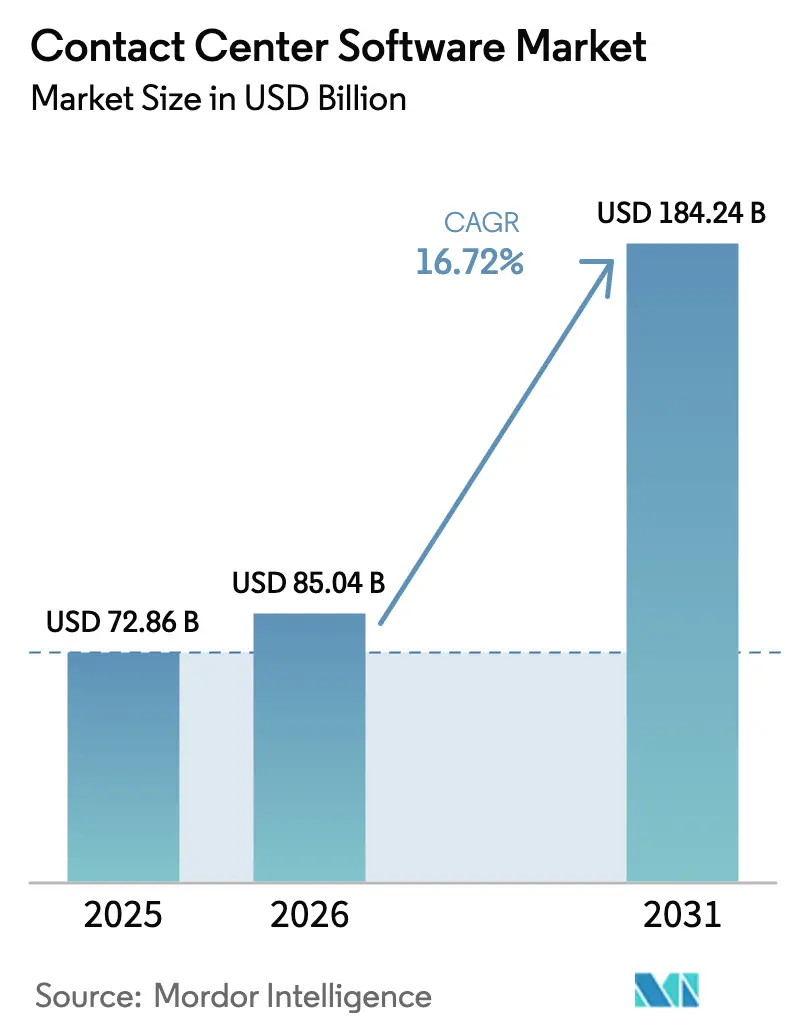

| Market Size (2026) | USD 85.04 Billion |

| Market Size (2031) | USD 184.24 Billion |

| Growth Rate (2026 - 2031) | 16.72% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Contact Center Software Market Analysis by Mordor Intelligence

The Contact Center Software Market size is projected to be USD 72.86 billion in 2025, USD 85.04 billion in 2026, and reach USD 184.24 billion by 2031, growing at a CAGR of 16.72% from 2026 to 2031. This strong growth stems from enterprises pivoting away from rigid voice-centric telephony toward cloud-native, generative-AI-orchestrated engagement platforms that collapse call-handling time and sharpen customer-experience metrics. GenAI agents now resolve a majority of routine inquiries, while real-time sentiment analytics intervene when emotions spike, reducing customer churn and boosting first-contact resolution rates. Cloud deployments have become the default choice, with enterprises favoring consumption-based CCaaS subscriptions that trim deployment cycles to weeks and eliminate capital expenditure. Small and mid-sized enterprises (SMEs) are adopting at the fastest clip, exploiting pay-per-seat pricing to access features once restricted to multimillion-dollar on-premise suites. Geography matters as well: Asia Pacific is the most dynamic region, driven by telecom mandates and rapid digital commerce expansion, whereas North America continues to anchor overall revenue on the strength of healthcare and financial-services demand.

Key Report Takeaways

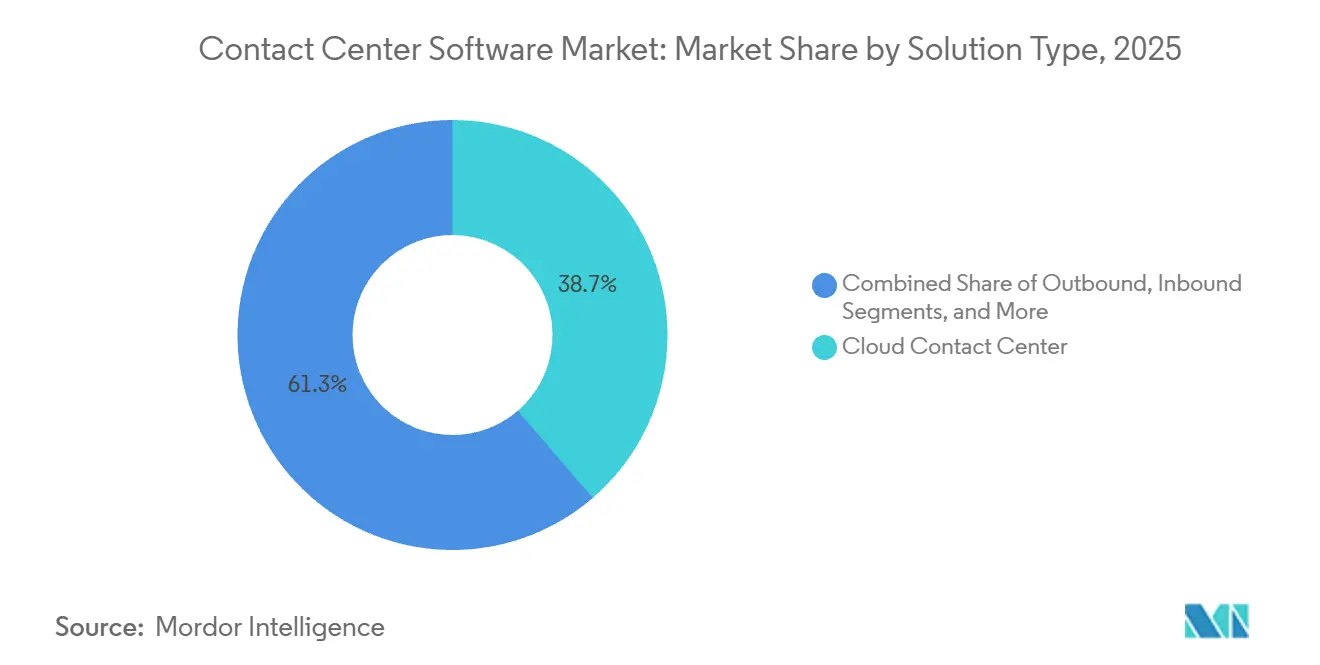

- By solution type, cloud contact center solutions held 38.68% of the contact center software market share in 2025, while GenAI-driven autonomous agents are projected to expand at an 18.43% CAGR, outpacing all other segments through 2031.

- By deployment model, cloud commanded 74.24% of the contact center software market share in 2025, while managed services are forecast to expand at a 17.91% CAGR through 2031.

- By service, professional services held a 61.43% revenue share in 2025, while managed services recorded the fastest growth at a 19.58% CAGR.

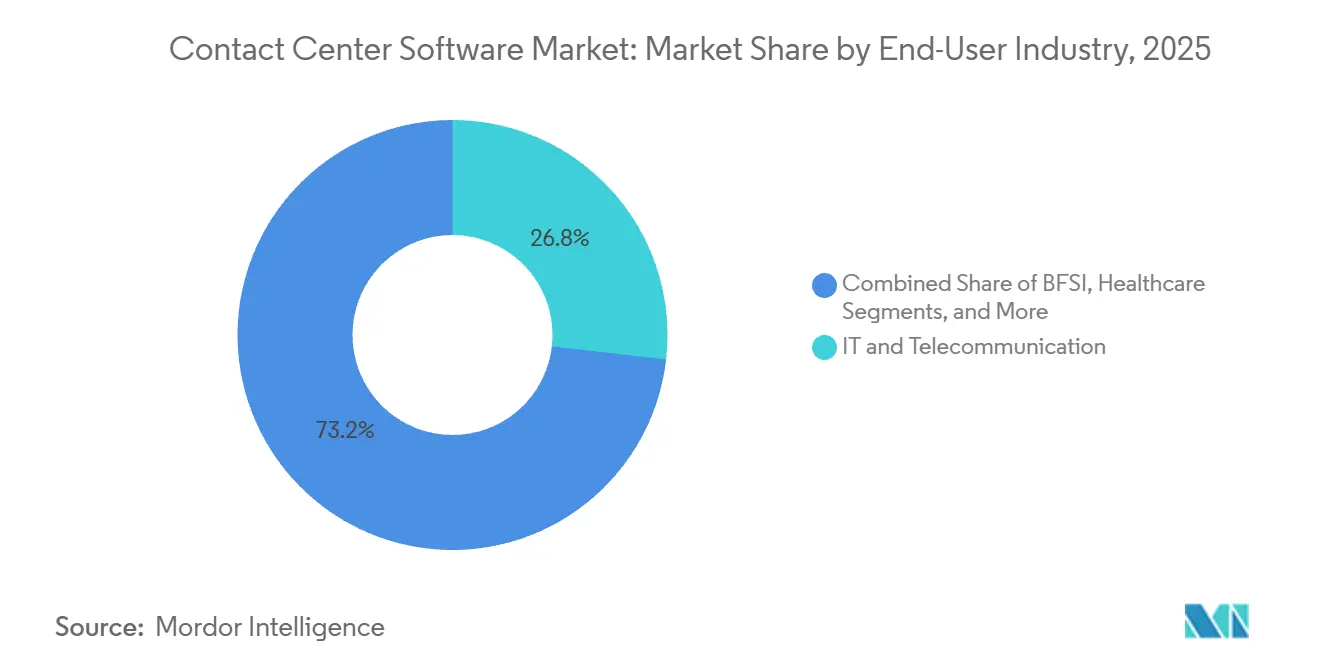

- By end-user industry, IT and telecommunications commanded 26.81% of the contact center software market share in 2025, while healthcare led with a 17.79% CAGR outlook between 2026 and 2031, reflecting the rapid uptake of HIPAA-compliant voice biometrics and real-time translation features.

- By organization size, Large Enterprises commanded 64.27% of the contact center software market share in 2025. SMEs recorded the steepest growth trajectory, with a 19.32% CAGR through 2031, as pay-per-seat CCaaS licensing eliminated six-figure upfront costs.

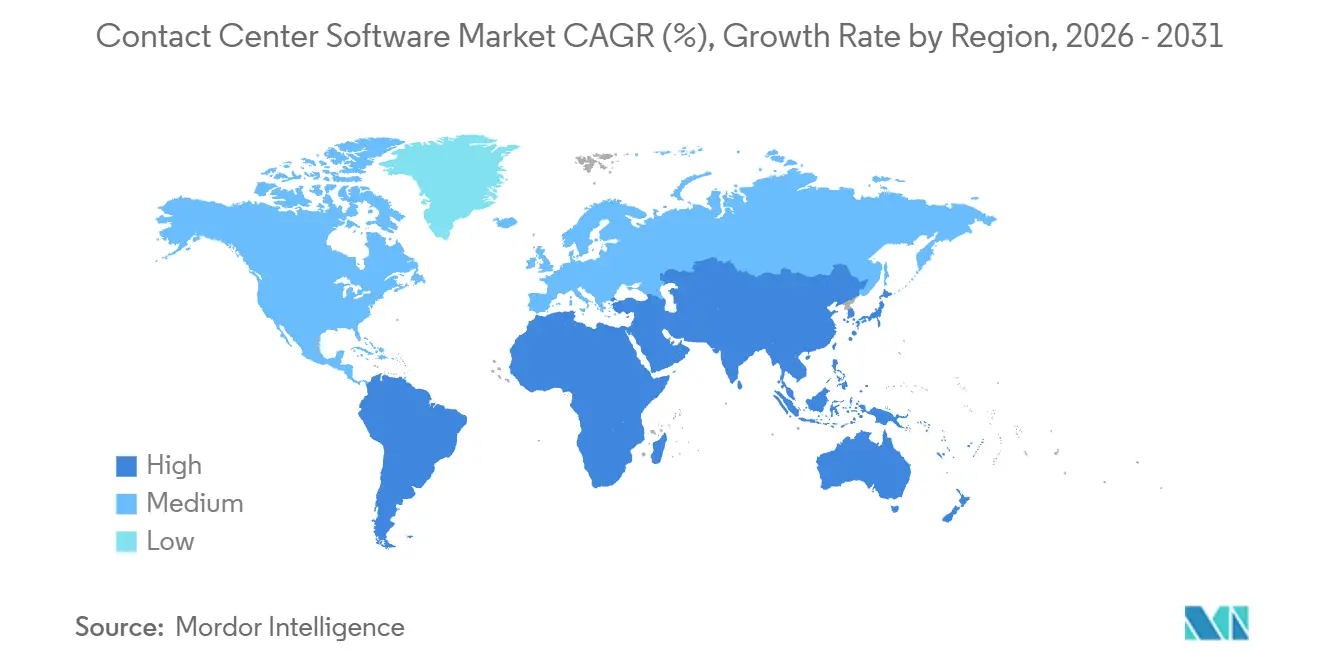

- By geography, North America held 39.58% of the market in 2025, and Asia Pacific is projected to post a 19.46% CAGR through 2031, eclipsing every other region in percentage growth terms.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Contact Center Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| GenAI Autonomous-Agent Breakthroughs | +3.2% | Global, concentrated in North America and Western Europe | Medium term (2-4 years) |

| Surge in Omnichannel CX Demand | +2.8% | Global, strongest in Asia Pacific retail and e-commerce | Short term (≤ 2 years) |

| Rapid Cloud-First CCaaS Adoption | +2.5% | North America and Europe lead, Latin America accelerating | Short term (≤ 2 years) |

| AI-Driven Workforce Optimization | +2.1% | Global, highest ROI in 500-plus-agent enterprises | Medium term (2-4 years) |

| Real-Time Sentiment Analytics Compliance | +1.6% | Europe and North America | Long term (≥ 4 years) |

| Telco-Network API Embedded CC Functions | +1.4% | Asia Pacific and Middle East | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

GenAI Autonomous-Agent Breakthroughs

Large-language-model agents now close 60% of tier-1 inquiries without human escalation, delivering annual savings that can exceed USD 1 million per 100-seat center. Five9’s GPT-4-turbo-powered virtual agent automatically sends personalized follow-up emails and schedules call-backs, trimming post-call work by one-third. Genesys similarly embedded retrieval-augmented generation to consult knowledge articles mid-dialogue and achieved an 82% first-contact resolution rate during 10 million pilot interactions. Financial-services deployments must still offer “co-pilot” modes to satisfy the EU AI Act requirement for human oversight, adding roughly 15% to development costs but opening a path into high-value banking and healthcare verticals. Collectively, GenAI agents are redefining productivity benchmarks and are the single-largest catalyst for platform refresh cycles within the contact center software market.

Surge in Omnichannel CX Demand

Consumers touch an average of 4.2 channels before resolving an issue, up sharply from 2020. Qualtrics’ real-time sentiment scoring now flags frustrated customers and elevates them to senior agents in under eight seconds, a capability that reduced churn by double digits during European telecom pilots. Retail brands have jumped on asynchronous messaging, with 68% offering pause-and-resume threads across devices. NICE’s Digital-First Routing tilts volume toward chat and SMS when a customer's history indicates a digital preference, reducing the average handle time by 22%.[1] NICE, “Digital-First Routing Launch,” nice.com Compliance frameworks, such as ISO 18295-1, meanwhile, require providers to maintain audit trails for each escalation path, thereby solidifying demand for unified routing and analytics engines.

Rapid Cloud-First CCaaS Adoption

Cloud subscriptions account for the majority of new seats, facilitated by 30-day proofs of concept that replace traditional 10-year refresh cycles. RingCentral reported a 42% year-over-year growth in CCaaS bookings, driven by retailers' demand for elastic capacity to handle Black Friday peaks. Microsoft extended Teams Phone in September 2025 with third-party CCaaS connectors, allowing enterprises to layer contact center capabilities onto existing collaboration estates without forklift upgrades. Usage-based pricing reduces capital outlay but introduces vendor lock-in: AWS egress fees run USD 0.09 per gigabyte, translating into five-figure monthly bills when recordings accumulate. Multi-cloud hedging remains a niche approach, adopted by fewer than one-fifth of enterprises.

AI-Driven Workforce Optimization

Real-time analytics now feed scheduling engines that balance service-level goals with agent preferences. Calabrio reduced scheduling variance from 12% to 3% in a 1,200-seat financial services rollout. NICE predicts call-volume spikes 72 hours ahead by correlating historic data with external events, trimming over-staffing costs. Zoom’s AI Companion transcribes calls on the fly and surfaces knowledge-base answers, shaving new-hire onboarding from six weeks to three. While labor efficiencies are material, regulators still lag: only Europe currently mandates impact assessments for automated workforce decisions, leaving other regions to self-regulate.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legacy Integration Complexity | -1.8% | Global, greatest in enterprises running 10-year-old Avaya or Cisco gear | Short term (≤ 2 years) |

| Data-Privacy and Security Regulation | -1.5% | Europe and North America | Medium term (2-4 years) |

| Cloud-Vendor Egress-Fee Lock-In | -0.9% | Global, pronounced at petabyte-scale | Long term (≥ 4 years) |

| Bias and Audit Risk in GenAI Models | -0.7% | Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Legacy Integration Complexity

Enterprises migrating from Avaya Communication Manager or Cisco Unified Contact Center Enterprise face 18- to 24-month timelines that require parallel support contracts, creating latency spikes of up to 300 milliseconds and degrading voice quality. Middleware such as Twilio Flex bridges new digital channels to legacy trunks but fragments dashboards and complicates agent training. Public-sector buyers suffer most because procurement cycles stretch three years, yet budget approvals demand ROI inside two, stalling a large share of modernization projects.

Data-Privacy and Security Regulation

The European Data Protection Board recorded a 60% surge in enforcement actions tied to cross-border call-recording transfers, with penalties averaging EUR 4.5 million (USD 5.1 million).[2]European Data Protection Board, “Guidelines on Cross-Border Transfers,” edpb.europa.eu California’s CCPA amendments give consumers 45 days to request the deletion of voice biometrics, thereby forcing automated purge workflows. AWS responded by allowing users to pin recordings to specific regions, although this feature increases storage costs by more than 12%. China’s Personal Information Protection Law introduces mandatory security reviews for AI models trained on domestic data, delaying launches by up to nine months.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution Type: GenAI Agents Radically Expand First-Contact Resolution

Cloud contact center solutions held 38.68% of the contact center software market share in 2025. GenAI-powered autonomous agents are experiencing the fastest expansion rate, at an 18.43% CAGR, reflecting an enterprise migration away from rules-based chatbots. In 2025, inbound modules still processed roughly 70% of all interactions; yet, their feature set increasingly relies on large language model reasoning that retrieves knowledge articles in real-time. Genesys demonstrated an 82% first-contact resolution rate during extensive pilots, underlining why CIOs allocate fresh budget to conversational AI. Predictive-dialer revenue, however, slipped after U.S. regulators restricted robocalls to pre-consented lists, shifting investments toward compliant outreach methods.

Omnichannel routing engines now unify voice, SMS, WhatsApp, email, and chat within a single queue, with NICE showing a 22% average reduction in handle time when digital channels shoulder routine inquiries. Workforce-optimization modules, spanning quality recording and AI coaching, experienced double-digit growth due to the rise of hybrid work, while analytics stacks, such as Verint’s speech engine, identified 95% of calls as compliance triggers. Integration middleware maintains relevance as 35% of Fortune 500 centers still route legacy trunks through cloud APIs to de-risk full migrations. The contact center software market continues to reward vendors that couple GenAI scale with turnkey compliance features.

By Deployment Model: Cloud Dominance Becomes Irreversible

Cloud captured 74.24% of 2025 spend and is projected to rise at a 17.91% CAGR through 2031, underscoring that subscription economics have redrawn procurement criteria. RingCentral’s rapid adoption of CCaaS among mid-market retailers highlighted the power of elastic licensing during seasonal peaks. Microsoft reinforced its cloud momentum by opening Teams Phone connectors, allowing enterprises to add voice routing capabilities without replacing their collaboration infrastructure. On-premise systems persist in government and defense, but even those buyers are experimenting with hybrid hand-offs that store sensitive recordings locally while utilizing cloud AI for sentiment scoring.

The shift exposes lock-in risk. AWS outbound data charges can surpass USD 50,000 per month for high-volume centers, discouraging provider swaps once petabyte-scale archives accumulate. Although multi-cloud remains a niche market, vendors are courting demand by touting region-based redundancy and automated failover. Leaderboard positioning is increasingly based on API ecosystems rather than core call routing, with providers embedding turnkey integrations for CRM, ITSM, and ERP systems to enhance daily workflow relevance.

By Service: Managed Models Supplant Time-and-Materials Consulting

Professional services accounted for 61.43% of 2025 revenue, as new platform deployments still require IVR scripting, data migration, and agent training. Yet, managed services are forecast to outpace them at a 19.58% CAGR as enterprises shift from seat-based billing to outcome-driven contracts tied to CSAT and first-contact-resolution targets. Global BPO majors now blend AI coaching with offshore labor arbitrage. Teleperformance reported a 28% productivity lift after rolling out real-time agent assistance across its Philippine hubs. Data-localization laws, however, force providers to replicate their infrastructure. Indonesia’s 2024 mandate triggered a USD 22 million data center build in Jakarta, illustrating that compliance costs are associated with the managed-service model.

System integrators continue to play a crucial role in complex transformations that combine omnichannel routing, CRM consolidation, and workforce analytics modernization. Migrating a 500-seat center still averages USD 150,000 to USD 300,000 in consulting fees, reinforcing that expertise remains indispensable even as subscription models proliferate. The contact center software market, therefore, supports a hybrid service mix, where pure-play CCaaS vendors partner with integrators for strategic engagements, while BPOs absorb day-to-day performance risk.

By End-User Industry: Healthcare Leads the Vertical Charge

IT and telecommunications accounted for 26.81% of 2025 revenue. Healthcare is poised for a 17.79% CAGR through 2031, fueled by HIPAA-grade voice biometrics that cut identity-verification time and multilingual translation engines that serve increasingly diverse patient bases. AWS bundled transcription and medical comprehension APIs into a dedicated health contact-center solution that reduced prior-authorization queues by 40% during pilot use.[3]Amazon Web Services, “Amazon Connect Data Residency,” aws.amazon.com BFSI firms continue heavy investment in fraud detection, NICE flagged USD 18 million in attempted wire fraud across 200,000 calls, exhibiting clear ROI for predictive analytics.

Retail brands double down on asynchronous messaging to manage shoppers who drift across devices, while telecom operators rely on CCaaS to stem subscriber churn. Public-sector adoption lags behind because procurement timelines often stretch over three years, yet recent subsidy programs in Germany and Japan are helping to close the gap. Overall, industry segmentation highlights that compliance-ready AI capabilities are the primary purchase trigger in regulated verticals, while cost elasticity influences adoption in commerce and media.

By Organization Size: SME Adoption Sets the Speed Record

SMEs will race ahead at a 19.32% CAGR through 2031, challenging the historic dominance of large enterprises that held 64.27% of 2025 revenue. Dialpad saw sub-100-seat deals jump 55% as bundled voice, video, and contact-center licenses priced below USD 100 per user drove rapid conversions. 8x8’s Shopify-ready connectors further simplify onboarding by auto-populating order details, enabling e-commerce merchants to shrink handle time by nearly one-third.

Large organizations, meanwhile, pursue global platform consolidation: Cisco helped a multinational bank shift 8,000 agents across 14 countries onto a unified cloud stack that delivered 99.95% uptime. Despite deeper pockets, big enterprises progress cautiously, prioritizing rollback options and data-sovereignty controls. SMEs remain more volatile, with 22% switching vendors within two years, prompting providers to invest in white-glove onboarding and proactive customer success programs to curb churn.

Geography Analysis

North America retained 39.58% of 2025 spending, driven by early adoption of CCaaS in healthcare and financial services. U.S. hospitals deploy HIPAA-compliant voice biometrics, and financial institutions layer real-time fraud analytics onto cloud platforms. Canada’s privacy commissioner now requires explicit consent for AI call analysis, forcing vendors to bake opt-in workflows into release roadmaps. Mexico’s near-shoring wave spurred BPO giants to open twelve new contact-center hubs serving bilingual support within favorable time zones. Outbound dialing continues to face headwinds after stricter FCC robocall rules, redirecting investment toward inbound and digital channels.

The Asia Pacific is the fastest-growing region, with a 19.46% CAGR through 2031. India’s telecom policy compels operators to expose customer-service APIs by December 2026, effectively embedding contact-center logic into core networks.[4] Department of Telecommunications India, “National Digital Communications Policy,” dot.gov.in China’s State Council requires explainability audits for all consumer-facing AI, extending deployment cycles but raising the bar for transparency. Japan’s JPY 50 billion (USD 0.32 billion) subsidy spurred a 38% increase in SME CCaaS bookings, while Australia’s data-breach regime encouraged encryption and multifactor authentication as minimum requirements. Vendors succeeding in the region localize data storage and language models to comply with diverging national requirements.

Europe remains compliance-centric, GDPR enforcement actions on cross-border recordings jumped 60%, nudging providers to carve out region-specific data lakes. The United Kingdom’s ICO mandates algorithmic explainability for routing decisions, prompting platforms to publish API-level audit feeds. Germany earmarked EUR 200 million to help manufacturing SMEs adopt cloud contact-center tools, a windfall that Genesys and Cisco quickly converted into 140 new accounts. Across the Middle East, Saudi Arabia’s Vision 2030 plan requires all government hotlines to migrate to cloud models by December 2026, drawing AWS and Oracle into a data-center race. South America’s appetite grows steadily as Brazilian retailers integrate WhatsApp Business APIs into CCaaS stacks, capitalizing on the region’s dominant messaging culture.

Regulatory Landscape

Regulation affecting contact center software is tightening around consumer protection, cross-border data handling, and AI transparency. In the United States, the Federal Communications Commission (FCC) advanced call-center related actions in 2026, including an NPRM (FCC 26-16) exploring measures to incentivize onshoring and strengthen customer service standards. Related proposals published in the Federal Register in April 2026 address sensitive data exposure in foreign call centers and extend protections to non-voice channels such as email and text.

In Europe, the EU AI Act (Regulation 2024/1689) sets direct compliance requirements for AI-enabled contact centers. Article 50 transparency obligations begin to be enforced from August 2026, requiring clear disclosure when customers interact with AI (voice bots, chatbots, and virtual assistants). That same timeframe lifts compliance expectations for certain contact center use cases, including emotion inference and automated routing systems, which can increase documentation and governance burdens. Vendors are therefore moving toward configurable disclosure, logging, and audit-trail capabilities alongside data residency controls.

Value Chain Analysis

The value chain centers on software platforms (CCaaS and associated modules), hyperscale cloud infrastructure, and an integration layer that connects CRM/ITSM/ERP systems, telecom networks, and data/AI services. Core platform vendors (for example, Genesys, NICE, Five9, Cisco, and Amazon Connect) package routing, workforce optimization, and analytics. Cloud providers supply compute, storage, and regional data residency options that shape architecture choices and ongoing operating costs, including egress. Upstream, AI model providers and enterprise AI stacks increasingly deliver agent-assist and autonomous-agent functions through orchestration layers that coordinate human and AI interactions.

Downstream, system integrators, telecom operators, and BPOs drive deployment, migration, and ongoing operations through professional and managed services. Partnerships show how distribution and delivery are bundling into broader enterprise stacks: HCLTech expanded work with Microsoft in January 2025 to operationalize migrations to Dynamics 365 Contact Center. Genesys and Mitel announced a go-to-market relationship in February 2025 to integrate Genesys Cloud with Mitel communications. Tata Communications partnered with NICE in November 2025 to pair Kaleyra with NICE CXone Mpower. Industry bodies also shape implementation practices, with TM Forum and Huawei publishing the IG1465 AI4Contact-Center whitepaper, and the Contact Center Intelligence Maturity Model (CCIMM) in June 2026, to standardize AI-native transformation pathways across stakeholders.

Competitive Landscape

Market concentration is moderate: the top five providers, Genesys, NICE, Five9, Cisco, and Amazon Connect, control about 45% of global revenue, leaving space for specialists to target vertical niches. AI capability is the primary battleground. Genesys filed 14 patents on real-time sentiment routing, establishing barriers against fast followers. NICE and Five9 revolve their roadmaps around GenAI agent assistance, touting average handle time cuts exceeding one-third.

Vertical specialization offers room for insurgents. Talkdesk captured 18% of 2024 healthcare wins by pre-integrating with Epic and Cerner electronic health record systems. Dialpad and 8x8 undercut legacy vendors by bundling unified communications and CCaaS below USD 100 per user, resonating with cost-sensitive SMEs. Incumbents counter through acquisitions: Cisco acquired IMImobile for USD 730 million to enhance its CPaaS messaging reach, and Genesys acquired Radarr Technologies to integrate churn-prediction analytics into its cloud suite.

Ecosystem openness increasingly determines vendor stickiness. Twilio Flex’s programmable voice APIs enable enterprises to integrate legacy PBX trunks into cloud routing, supporting hybrid coexistence during phased migrations. Providers that cultivate robust developer communities and pre-built CRM connectors widen moats as customers weave deeper operational logic into the platform. The contact center software market therefore rewards both product breadth and domain-specific depth.

Contact Center Software Industry Leaders

Genesys Telecommunications Laboratories Inc.

NICE Ltd.

Five9 Inc.

Cisco Systems Inc.

Amazon Web Services Inc. (Amazon Connect)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

One major whitespace is compliance-led AI orchestration that can be audited, disclosed, and localized by region without undermining automation benefits. The EU AI Act enforcement of Article 50 transparency obligations from August 2026 creates an immediate need for configurable AI disclosure across voice and digital channels, along with logging and governance that can be mapped to specific use cases such as emotion inference and automated routing. In the United States, FCC activity around 2026 NPRMs involving foreign call centers and sensitive data handling extends pressure beyond voice into text and email. This opens demand for platforms that combine customer-service workflows with data minimization, retention controls, and channel-consistent compliance reporting.

A second opportunity is telco-led and enterprise-built AI layers that sit on top of CCaaS, shifting differentiation toward orchestration, integration, and domain-tuned models. Evidence of this shift includes TM Forum and Huawei releasing the CCIMM in June 2026 to codify AI-native maturity steps for contact centers, alongside telecom-focused initiatives such as Amdocs collaborating with Google Cloud (Gemini Enterprise integrated with Amdocs Cognitive Core) for agentic AI in telecom contact centers. Large-scale internal adoption also points to spend moving toward governed AI deployment in service operations, with Deutsche Telekom reporting an early-2026 rollout of ChatGPT Enterprise reaching 50,000 monthly active users and embedding AI into customer care and operational tools. That progression reinforces demand for secure connectors, knowledge grounding, and measurable automation inside contact center environments.

Recent Industry Developments

- July 2026: Genesys announced the acquisition of Pinkfish to enhance agentic orchestration workflows inside Genesys Cloud. The acquisition strengthens Genesys ability to coordinate actions across systems of record during customer interactions, supporting broader autonomous experience orchestration beyond routing and analytics.

- September 2025: Microsoft extended Teams Phone with third-party connector support, enabling enterprises to overlay CCaaS capabilities on existing collaboration deployments. This lowers integration friction for cloud contact center adoption and increases the importance of certified app ecosystems and pre-built connectors.

- March 2024: Vodafone Business expanded its global communications portfolio to include RingCentral RingCX as a native contact center solution. Carrier-led packaging broadened CCaaS distribution through telecom channels and reinforces demand for scalable, multi-country deployments with standardized administration.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers software platforms used by organizations to handle customer interactions across voice and digital channels, including routing, agent desktop, quality monitoring, analytics, and workforce tools, delivered through cloud or on-premise deployments.

Scope exclusions: We exclude contact center hardware and telecom carrier connectivity services (such as headsets, desk phones, switches, and network access).

Segmentation Overview

- By Solution Type

- Outbound

- Inbound

- Omnichannel Routing

- Workforce Optimisation

- Reporting And Analytics

- Integration

- Other Solutions

- By Deployment Model

- Cloud

- On-Premise

- By Service

- Professional

- Managed

- By End-User Industry

- IT And Telecommunication

- BFSI

- Healthcare

- Retail And Consumer Goods

- Government And Public Sector

- Media And Entertainment

- Education

- Other End-User Industries

- By Organisation Size

- Large Enterprises

- Small And Mid-Sized Enterprises

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Kenya

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts with building the market boundary and the demand environment for contact center software spend. We reviewed public sources such as US SEC filings and annual reports, US Bureau of Labor Statistics series for call center employment and wage trends, US FCC and EU Digital regulations for customer communications, and International Telecommunication Union indicators on connectivity and broadband readiness.

To shape regional adoption and pricing context, we also used sources such as OECD digital economy indicators, World Bank macro data, and reputable press coverage of enterprise software spending cycles and AI feature rollouts. Along with this, we referenced paid subscriptions for company financials and intelligence, and for patent databases to understand the cadence of AI driven features that can move average selling prices over time. These desk sources are illustrative, and many other references were also used for data collection, cross-checking, and clarification.

Primary Interviews and Surveys

Primary work was used to validate how contact center software is purchased, packaged, and priced across cloud subscriptions and on-premise licenses, and how services are attached to those deals. We spoke with a mix of software providers, system integrators, and enterprise buyers across Americas, EMEA, and APAC to close gaps from public data and to confirm adoption and churn assumptions against real buying cycles and procurement timelines.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 15% | APAC: 40% |

| Mid tier: 57% | Functional/Unit leaders: 38% | EMEA: 33% |

| Smaller Players: 16% | Managers: 47% | Americas: 27% |

Market-Sizing & Forecasting

Sizing is built by first reconstructing the addressable demand pool using region level enterprise counts, contact center seat density by industry, and the share of seats using modern software stacks, and then translating that into spend using observed pricing structures. While a top-down approach is used to connect adoption signals to total spend, the totals are corroborated with selective bottom-up approximations such as sampled seat based subscription pricing multiplied by estimated deployed seats, plus channel checks for services attach rates.

Key inputs used in the model include contact center agent employment trends, cloud versus on-premise migration pace, average seats per site, subscription price per agent per month and its progression, services penetration for implementation and managed operations, and replacement cycles tied to compliance and security needs. Forecasts are produced using scenario analysis supported by expert inputs, where seat growth, cloud conversion speed, and price uplift from AI features are varied within realistic ranges, and then reconciled back to macro IT spending conditions. When bottom-up signals are missing in smaller regions, proxy ratios from similar markets are applied and then adjusted after interview feedback.

Data Validation & Update Cycle

Outputs are validated through multiple checks so the final number does not rely on one single assumption. We compare implied spend per agent, cloud share movement, and regional growth rates against independent signals from public datasets and what interviewees report as normal budget behavior, and then investigate outliers before the model is approved.

A second analyst reviews key inputs, conversion steps, and currency handling, followed by a final consistency pass across regions and deployment types. Reports are refreshed annually, and interim updates are made when material events occur, such as major pricing model shifts or step changes in cloud adoption. Right before delivery, we run a final update sweep so clients receive the most current view available.

Mordor Intelligence's Contact Center Software Market Size Measured Against Other Published Estimates

Published market sizes for contact center software can look far apart even when they are talking about a similar product category, because the line between software, services, and adjacent customer experience tools is drawn differently. Differences also come from base year choices, whether the estimate is anchored on seats or on vendor revenues, and how currency timing and inflation are handled.

The benchmark table shows a spread mainly because some studies fold broader customer experience suites and wider services into the total, while under Mordor Intelligence's scope the value is counted for contact center software platforms and their directly attached professional and managed services, with hardware kept out and cloud share movement used as a key cross-check.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 72.86 B (2025) | |

| Industry Analytics Firm A | USD 63.88 B (2025) | Uses a narrower build in some regions by leaning on reported company revenues, which can undercount multi product bundles and channel delivered implementations when they are not separately disclosed. |

| Global Research Publisher B | USD 50.78 B (2024) | Anchors on a 2024 base year and applies a different deployment split assumption, where on-premise dominates, which can compress the implied subscription spend and delay cloud migration value. |

Taken together, the variance is mostly explained by what gets included around the software core, which year is treated as the base, and how cloud subscription pricing and services attach rates are modeled. By keeping the inputs tied to seats, deployment mix, and realistic price and adoption checks, the estimate remains traceable to clear steps that can be repeated when new evidence appears.

Key Questions Answered in the Report

How large is the contact center software market in 2026?

The market is valued at USD 85.04 billion in 2026 based on Mordor Intelligence estimates.

What CAGR is expected for contact center platforms through 2031?

Revenue is projected to increase at a 16.72% CAGR between 2026 and 2031.

Which deployment model grows fastest?

Cloud subscriptions are forecast to post a 17.91% CAGR as organizations abandon on-premise infrastructure.

Why is healthcare adoption accelerating?

HIPAA-compliant voice biometrics and real-time translation tools reduce verification friction and enhance multilingual support, driving a 17.79% CAGR between 2026 and 2031.

What is the main barrier to cloud migration?

Legacy integration complexity extends project timelines to two years and can introduce latency that degrades call quality.

Which region offers the greatest growth upside?

Asia Pacific is projected to expand at a 19.46% CAGR owing to telecom mandates, government incentives and booming e-commerce.

Page last updated on: