Offshore Oil And Gas Communications Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

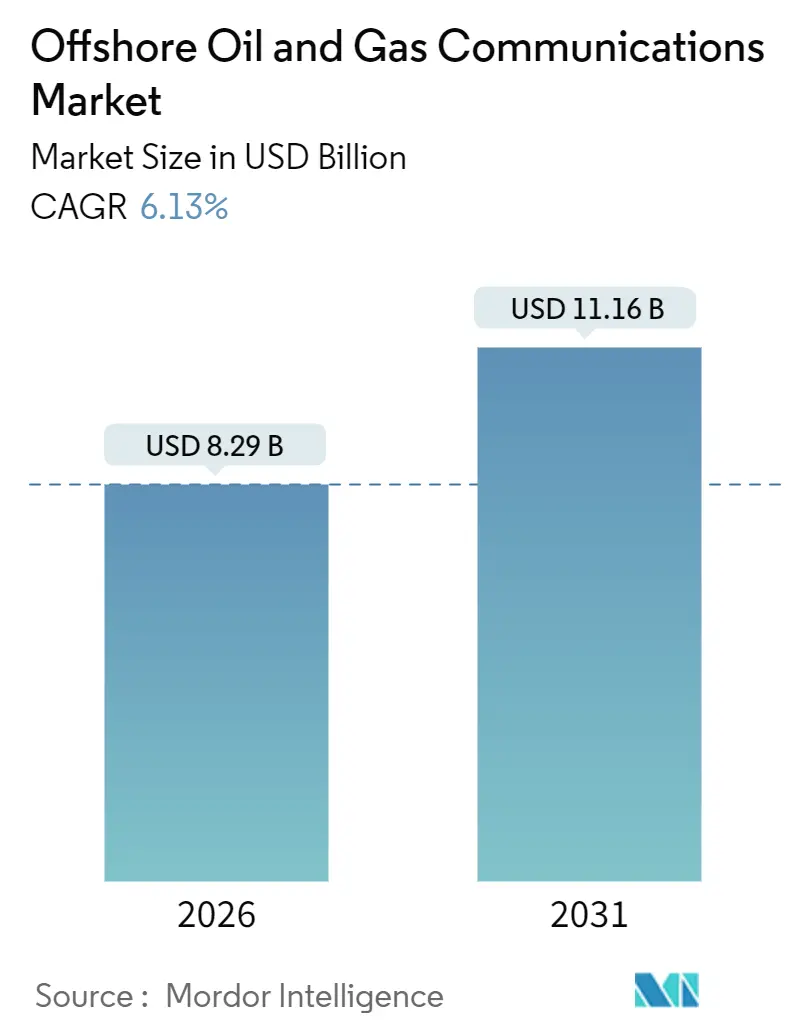

| Market Size (2026) | USD 8.29 Billion |

| Market Size (2031) | USD 11.16 Billion |

| Growth Rate (2026 - 2031) | 6.13% CAGR |

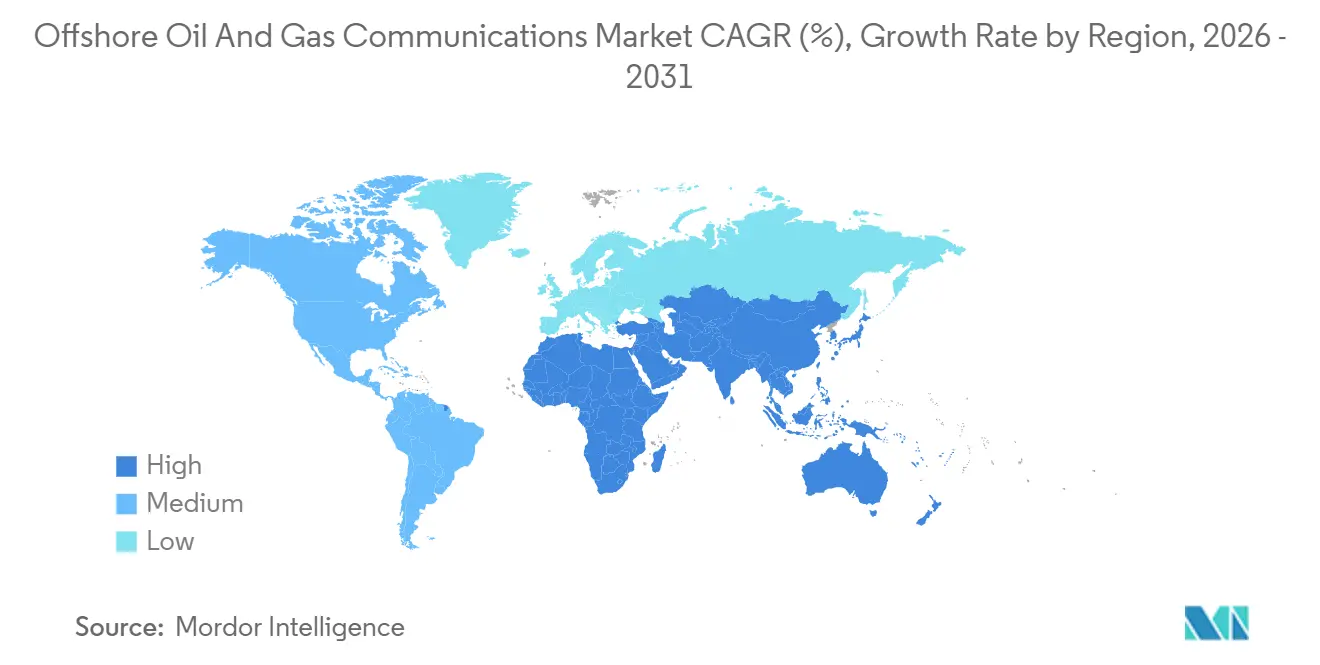

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Offshore Oil And Gas Communications Market Analysis by Mordor Intelligence

The offshore oil and gas communications market size reached USD 8.29 billion in 2026 and is projected to rise to USD 11.16 billion by 2031, reflecting a 6.13% CAGR. The expansion is underpinned by operators replacing single-link very small aperture terminal (VSAT) systems with hybrid architectures that combine low-Earth-orbit satellites, private 5G cells, and subsea fiber to enable real-time analytics on both fixed and floating assets. Operators view connectivity as an operational lever that supports remote command centers, predictive-maintenance software, and unmanned platform concepts, collectively reducing offshore headcount and increasing equipment uptime. High-throughput satellites are bridging coverage gaps while 5G private networks supply deterministic latency for safety-instrumented systems. Demand growth also correlates with sanctions on deep-water projects in Brazil and Guyana that require resilient links beyond 2,500 m water depth. Finally, tightening IEC 62443 cybersecurity mandates are forcing asset owners to upgrade legacy radios in favor of monitored, software-defined networks that pass regulatory audits.

Key Report Takeaways

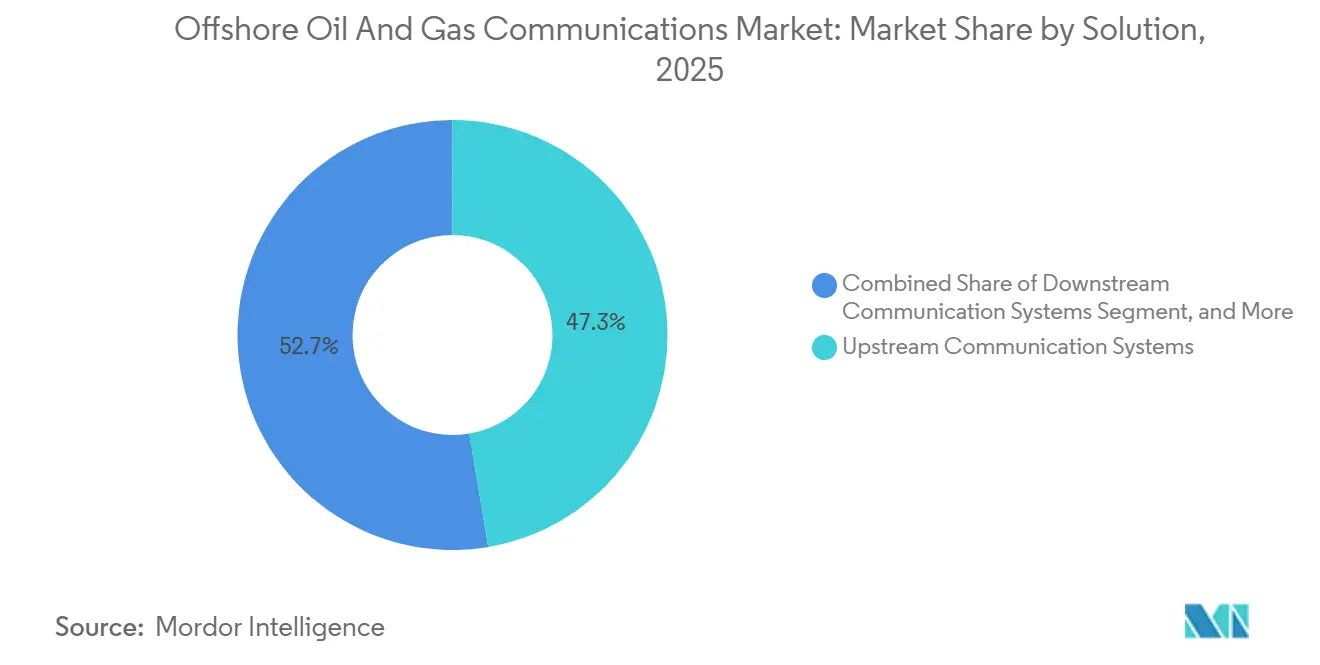

- By solution, upstream systems led the offshore oil and gas communications market with 47.34% market share in 2025, while downstream systems are advancing at a 6.77% CAGR through 2031.

- By communication network technology, VSAT captured 39.77% of the offshore oil and gas communications market size in 2025, and 5G or private LTE networks are expanding at a 6.96% CAGR through 2031.

- By component, hardware held 56.13% of the offshore oil and gas communications market share in 2025, and software revenues are climbing at a 6.72% CAGR through 2031.

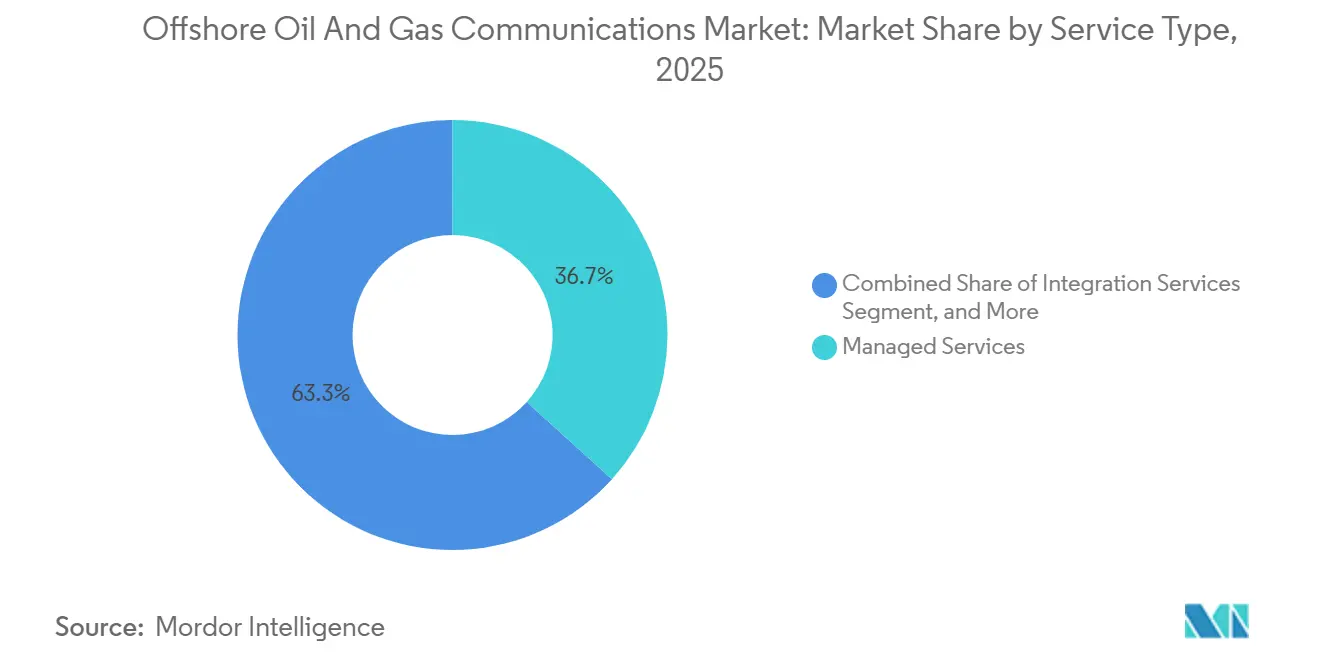

- By service type, managed services accounted for 36.71% of the offshore oil and gas communications market size in 2025, whereas integration services are growing at a 6.93% CAGR during the forecast period.

- By offshore installation type, fixed platforms commanded 42.39% of the offshore oil and gas communications market share in 2025, and floating production storage and offloading units are set to grow at a 7.17% CAGR to 2031.

- By geography, Asia-Pacific generated 28.82% of 2025 revenue, but the Middle East is forecast to register a 7.11% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Offshore Oil And Gas Communications Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising bandwidth needs for real-time rig monitoring | +1.2% | North America, Europe, global offshore | Medium term (2-4 years) |

| Expansion of deep-water projects beyond 2,500 m | +1.4% | South America, Africa, Asia-Pacific | Long term (≥ 4 years) |

| 5G-enabled private LTE roll-outs on floating assets | +1.3% | North America, Europe, Middle East | Short term (≤ 2 years) |

| Growing use of edge-based AI for predictive maintenance | +0.9% | Global, early in North America and Europe | Medium term (2-4 years) |

| Energy-industry cybersecurity regulations tightening | +0.7% | Europe, North America, Middle East | Short term (≤ 2 years) |

| Satellite mega-constellations providing low-latency links | +1.0% | South America, Africa, Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Bandwidth Needs for Real-Time Rig Monitoring

Drilling units now generate multi-terabyte datasets each day, far exceeding the capacity of 2 Mbit/s VSAT links. The adoption of private 5G cells on assets such as the Maersk Integrator delivered 50 Mbps uplinks in 2025, enabling 4K video and downhole telemetry to reach onshore centers in seconds.[1]Maersk Drilling, “Maersk Integrator Gains 5G Uplink,” maerskdrilling.com Real-time visibility reduced non-productive time on deepwater wells by up to 20% and improved crew retention by doubling welfare bandwidth during off-peak periods. Providers now bundle tiered bandwidth that prioritizes operational traffic, aligning cost with utilization.

Expansion of Deepwater Projects Beyond 2,500 m

Ultra-deep fields require sub-50-ms latency for subsea blowout preventer controls and dynamic positioning systems. Petrobras’s Mero FPSO program relies on managed fiber rings that guarantee low latency, while Shell’s Whale platform added triple-redundant links in 2025 to protect 100,000 barrels-per-day output.[2]Subsea 7 Project Brief, “Mero Fiber Network,” subsea7.com The scaling of deepwater acreage is therefore accelerating orders for hybrid satellite-fiber topologies and edge servers that synchronize with onshore high-performance clusters.

5G-Enabled Private LTE Roll-Outs on Floating Assets

Nokia and Tampnet installed licensed 3.5 GHz micro-cells on eight North Sea platforms in 2025, allowing Aker BP to retire copper fieldbus loops and cut maintenance costs by 40%. 5G’s deterministic latency supports wearable gas detectors, wireless emergency buttons, and industrial IoT sensors on mobile FPSOs, eliminating the cabling constraints that hamper rotating modules. Regulatory support, such as Ofcom’s fast-tracking of offshore spectrum license deployments that were previously delayed by coordination hurdles, is also accelerating adoption.

Growing Use of Edge-Based AI for Predictive Maintenance

Platforms now run inference engines next to programmable logic controllers, reducing alert latency from hours to seconds. Murphy Oil’s 2024 pilot predicted gearbox failures 72 hours in advance, avoiding three shutdowns worth an estimated USD 18 million. Vendors charge subscription fees for containerized AI modules at a pace that is lifting software revenue faster than hardware sales. Although inference runs locally, model retraining triggers episodic bandwidth spikes that managed-service providers must accommodate through dynamic quality-of-service policies.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Harsh-weather signal degradation on Ka-band links | -0.8% | North Atlantic, North Sea, Southern Ocean | Short term (≤ 2 years) |

| High CAPEX of subsea fiber backbones | -1.1% | Gulf of Mexico, Brazil pre-salt, West Africa, Southeast Asia | Long term (≥ 4 years) |

| Limited spectrum allocation in offshore blocks | -0.5% | Indonesia, India, Nigeria, Angola, Argentina | Medium term (2-4 years) |

| Shortage of RF technicians willing to work offshore | -0.6% | North America, Europe, Middle East | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Harsh-Weather Signal Degradation on Ka-Band Links

Ka-band delivers ten-fold throughput improvements but experiences rain fade that drops uptime below 95% during severe storms. North Sea platforms historically logged 120 hours of Ka-band outages each year versus 30 hours on Ku-band. Operators now deploy site-diversity gateways and multi-orbit terminals to maintain continuity, yet residual risks deter fully latency-sensitive workloads from migrating off Ku-band.[3]Baker Hughes Investor Update, “Edge AI in Offshore,” bakerhughes.com

High CAPEX of Subsea Fiber Backbones

Installing armored fiber at USD 50,000-100,000 per kilometer pushes 200 km links into a USD 10-20 million range. Shell’s Whale cable, completed in 2025 at a USD 18 million budget, is viable only for fields with multi-decade lifespans and high production rates. Smaller operators often defer fiber upgrades because vessel availability and hot-work permits lengthen payback horizons.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution: Upstream Dominates, Downstream Accelerates

The upstream portion of the offshore oil and gas communications market accounted for 47.34% of the market size in 2025, reflecting heavy capital allocation to exploration and production assets, where real-time data directly improves drilling efficiency. Edge telemetry from intelligent well completions, now embedded in 60% of new deepwater wells, anchors demand for continuous high-bandwidth links.

Downstream installations, although smaller today, are forecast to grow at a 6.77% CAGR through 2031 as refineries add 10,000-sensor wireless networks for emissions and leak monitoring, creating communication loads approaching those of upstream installations. Midstream operators are also commissioning fiber-optic sensing cables that detect pipe intrusion events in real time, extending the offshore oil and gas communications market into pipeline integrity-monitoring niches.

By Communication Network Technology: VSAT Leads, 5G and Private LTE Surge

VSAT maintained a 39.77% revenue lead in 2025 because a 1.2 m dish can be installed in a few days, enabling rapid commissioning of new rigs. The technology, therefore, anchors remote start-up schedules for wildcat wells, cementing its dominance in the offshore oil and gas communications market.

That grip is loosening as 5G and private LTE networks expand at a 6.96% CAGR, enabled by licensed-spectrum allocations that provide predictable latency for safety loops and industrial IoT. Meanwhile, fiber remains the bandwidth ceiling where economics allow, as exemplified by Equinor’s 120 km Johan Sverdrup cable, which replaced VSAT links altogether.

By Component: Hardware Dominates, Software Gains Momentum

Hardware accounted for 56.13% of 2025 revenue, as every platform still requires antennas, radios, and cabling that can cost USD 0.5-2 million per site. This hardware foundation supports a large share of the offshore oil and gas communications market, even as procurement gradually shifts to opex models.

Software, on the other hand, is expanding at a 6.72% CAGR as vendors license analytics, network management suites, and cybersecurity stacks that deliver value independent of physical hardware. Subscription pricing aligns with production uptime metrics, converting one-off licenses into long-term revenue streams.

By Service Type: Managed Services Lead, Integration Services Accelerate

Managed services accounted for 36.71% of service revenue in 2025, as operators prefer outsourcing 24 × 7 network monitoring and troubleshooting to vendors such as Harris CapRock. This model shifts performance risk to providers and frees operators from staffing RF specialists who are in short supply.

Integration services, growing at a 6.93% CAGR, address the complexity of converting 1,000 legacy analog loops into Ethernet-based traffic on brownfield assets. Spectrum-coordination studies and VLAN segmentation projects, therefore, keep specialist system integrators fully booked through the forecast window.

By Offshore Installation Type: Fixed Platforms Lead, FPSOs Surge

Fixed platforms accounted for 42.39% of installations in 2025, underpinned by decades of Gulf of Mexico and North Sea jacket developments that provide stable mounting positions for microwave dishes and phased-array antennas. Their mature status sustains a core hardware replacement cycle within the offshore oil and gas communications market.

Floating production, storage, and offloading vessels, however, are set to grow at a 7.17% CAGR because nations such as Brazil and Guyana sanction deepwater fields that can only be monetized with mobile processing units. This trend intensifies demand for omnidirectional satellite terminals and private 5G cells that maintain connectivity as FPSOs weathervane around their turrets.

Geography Analysis

Asia-Pacific generated 28.82% of 2025 revenue, driven by Petronas, ONGC, and CNOOC, which are retrofitting aging jack-up fleets with fiber-to-the-rig links and private LTE that feed remote operations centers in Kuala Lumpur, Mumbai, and Shenzhen. Government spectrum approvals are generally streamlined in Malaysia, allowing trials to move from the lab to the field in under 6 months. North America retains its status as a technology testbed. Chevron’s Anchor platform in the Gulf of Mexico combines low-Earth-orbit satellites with 5G meshing that routes high-priority safety traffic across cellular links while relegating non-critical data to VSAT circuits. Hurricane resilience remains a central driver, leading to dual-orbit antenna installations that keep uptime near 99.9%.

Europe continues to invest in subsea fiber retrofits. Equinor’s 120 km cable to Johan Sverdrup, completed in late 2024, enabled the operator to decommission geostationary links and cut annual bandwidth costs by 60%. The NIS2 Directive, effective in 2024, further pushes operators to adopt managed security services that monitor operational technology traffic for anomalies. The Middle East is the fastest-growing regional market with a 7.11% CAGR outlook. Saudi Aramco’s 2025 award of USD 180 million in private 5G contracts for 15 gas platforms signals regional appetite for unmanned platform concepts that rely on continuous gigabit-class links. ADNOC is following suit on the Zakum and Hail projects, embedding cybersecurity gateways to comply with IEC 62443.

South America rides on Brazil’s pre-salt boom. Petrobras’s seven-year, USD 120 million deal with Speedcast covers 12 FPSOs that stream real-time reservoir data to onshore analytics hubs, locking in long-duration service revenues. Smaller operators in Guyana and Suriname use Starlink Maritime to avoid the CAPEX of fixed VSAT contracts. Africa remains fragmented. Angolan operators still rely on traditional Ku-band VSAT because near-shore fiber landing stations are sparse, while Nigerian independents are testing flat-panel antennas from Kymeta to reduce deck footprint. Regulatory clarity on offshore spectrum remains a bottleneck that can add up to 12 months to deployment timelines in Nigeria and Angola.

Competitive Landscape

The offshore oil and gas communications market is moderately fragmented. The top five vendors, Inmarsat, Hughes Network Systems, Nokia, Ericsson, and ABB, collectively hold about 40% revenue share, leaving ample space for regional satellite operators, subsea-cable specialists, and integration firms. Starlink Maritime’s flat-rate model at USD 5,000 per month has forced incumbent VSAT providers to introduce usage-based tiers that erode margins by 10-15%. Equipment suppliers now favor outcome-based contracts. Nokia’s ATEX Zone 1-certified private LTE, for example, replaced Wi-Fi meshes on 25 North Sea platforms, guaranteeing deterministic latency for safety systems. ABB’s Ability Marine Advisory System bundles edge computing with satellite bandwidth, reducing integration complexity for FPSO operators.

Patent filings underscore innovation pressure. Ericsson submitted 12 patents in 2024-2025 on network slicing that partitions a single 5G radio into virtual lanes with guaranteed performance for drilling control, crew welfare, and surveillance video. Subsea-cable firms such as Subsea 7 capture niche demand on flagship projects but face adoption limits because installed cost can exceed USD 100,000 per kilometer. Integration skills are a differentiator. Harris CapRock operates multi-tenant network operation centers that monitor links for more than 50 offshore assets, helping fill a labor gap created by a 22% vacancy rate in offshore RF roles in 2025. Redline Communications maintains a microwave niche for tightly clustered North Sea platforms that want latency below 3 ms without fiber CAPEX.

Offshore Oil And Gas Communications Industry Leaders

ABB Ltd

Alcatel-Lucent Submarine Networks

AT&T Inc.

Baker Hughes Co.

CommScope Holding Co. Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Inmarsat launched the ELERA network of five high-throughput geostationary satellites that employ site-diversity gateways to sustain 99.9% availability during tropical storms.

- November 2025: Saudi Aramco issued USD 180 million in contracts to Nokia and Ericsson for private 5G across 15 offshore gas platforms, with project completion expected in mid-2027.

- October 2025: Subsea 7 finished a 150 km fiber link to Shell’s Whale platform in the Gulf of Mexico at a cost of USD 18 million.

- September 2025: Petrobras signed a USD 120 million managed-services deal with Speedcast covering connectivity for 12 FPSOs in Brazil’s pre-salt province.

Global Offshore Oil And Gas Communications Market Report Scope

The Offshore Oil and Gas Communications Market Report is Segmented by Solution (Upstream Communication Systems, Midstream Communication Systems, Downstream Communication Systems), Communication Network Technology (Cellular Communication Network, VSAT Communication Network, Fiber Optic-based Communication Network, Microwave Communication Network, 5G/Private LTE), Component (Hardware, Software, Services), Service Type (Managed Services, Professional Services, Maintenance and Support Services, Integration Services), Offshore Installation Type (Drilling Rigs, Floating Production Storage and Offloading (FPSO), Fixed Production Platforms, Support Vessels and Supply Ships, Subsea Production Systems), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

| Upstream Communication Systems |

| Midstream Communication Systems |

| Downstream Communication Systems |

| Cellular Communication Network |

| VSAT Communication Network |

| Fiber Optic-based Communication Network |

| Microwave Communication Network |

| 5G/Private LTE |

| Hardware |

| Software |

| Services |

| Managed Services |

| Professional Services |

| Maintenance and Support Services |

| Integration Services |

| Drilling Rigs |

| Floating Production Storage and Offloading (FPSO) |

| Fixed Production Platforms |

| Support Vessels and Supply Ships |

| Subsea Production Systems |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Solution | Upstream Communication Systems | ||

| Midstream Communication Systems | |||

| Downstream Communication Systems | |||

| By Communication Network Technology | Cellular Communication Network | ||

| VSAT Communication Network | |||

| Fiber Optic-based Communication Network | |||

| Microwave Communication Network | |||

| 5G/Private LTE | |||

| By Component | Hardware | ||

| Software | |||

| Services | |||

| By Service Type | Managed Services | ||

| Professional Services | |||

| Maintenance and Support Services | |||

| Integration Services | |||

| By Offshore Installation Type | Drilling Rigs | ||

| Floating Production Storage and Offloading (FPSO) | |||

| Fixed Production Platforms | |||

| Support Vessels and Supply Ships | |||

| Subsea Production Systems | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

How large is the offshore oil and gas communications market in 2026?

The offshore oil and gas communications market size reached USD 8.29 billion in 2026 and is forecast to grow steadily at a 6.13% CAGR.

Which communication technology is growing fastest for offshore platforms?

5G and private LTE networks are the fastest-growing options, advancing at a 6.96% CAGR as operators seek deterministic latency and licensed-spectrum reliability.

Why are FPSOs creating new connectivity demand?

Floating production vessels work in deep-water fields where fixed structures are impossible, so they rely on hybrid satellite and 5G links that function as the vessel changes heading, driving a 7.17% CAGR segment growth.

What is the biggest restraint facing Ka-band satellite services offshore?

Severe rain fade in harsh-weather basins such as the North Sea can drop Ka-band availability below 95%, leading operators to maintain dual-band or multi-orbit backups.

Which region is forecast to expand fastest through 2031?

The Middle East is projected to record a 7.11% CAGR due to large private 5G deployments on new Saudi Aramco and ADNOC gas projects.

How are cybersecurity rules affecting offshore networks?

Regulations such as IEC 62443 and the European NIS2 Directive require continuous monitoring of operational-technology traffic, prompting operators to adopt managed security services and next-generation firewalls.

Page last updated on: