Netherlands Containerboard Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.42 Billion |

| Market Size (2026) | USD 1.46 Billion |

| Market Size (2031) | USD 1.58 Billion |

| Growth Rate (2026 - 2031) | 1.58% CAGR |

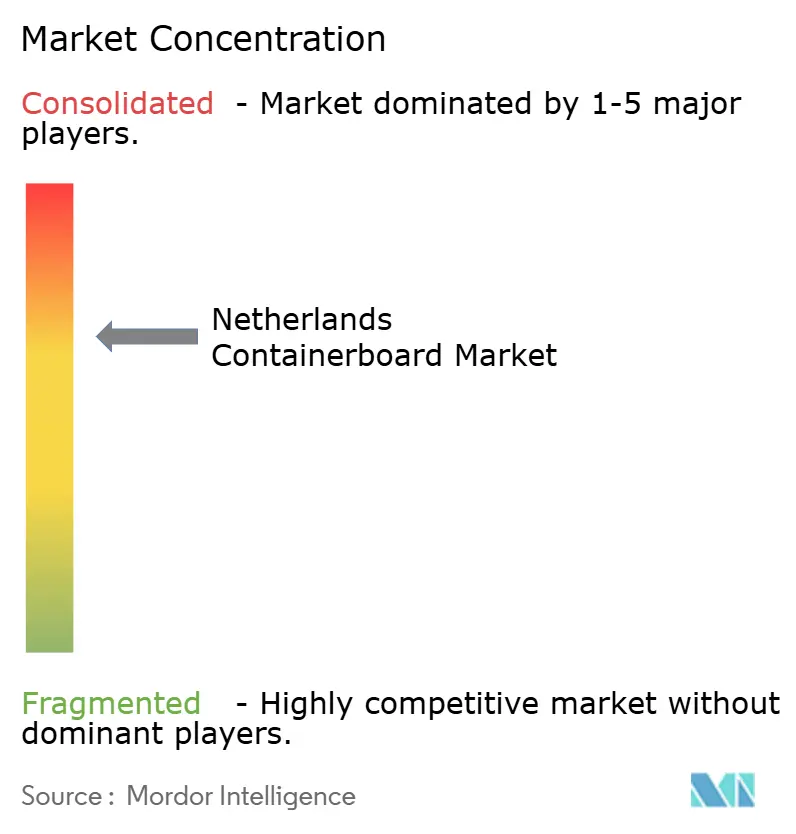

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Netherlands Containerboard Market Analysis by Mordor Intelligence

The Netherlands containerboard market size is projected to expand from USD 1.42 billion in 2025 and USD 1.46 billion in 2026 to USD 1.58 billion by 2031, registering a CAGR of 1.58% between 2026 to 2031. The Netherlands containerboard market continues to benefit from the country’s dual role as a domestic packaging user and a production and transit hub for Northwestern Europe. The Port of Rotterdam remains a core support for demand because export-oriented food, chemical, and consumer goods flows depend on steady corrugated packaging availability. The Netherlands containerboard market is moving forward in a restrained way because Western European overcapacity still weighs on pricing, even as food transit and e-commerce fulfillment keep baseline demand stable. Regulation is also shifting investment priorities toward right-sized recyclable corrugated formats across Dutch converting plants. Market opportunities remain strongest in premium performance grades, automated packaging solutions, and logistics-led packaging formats, while manufacturing softness and reusable packaging pilots continue to act as limiting factors.

Key Report Takeaways

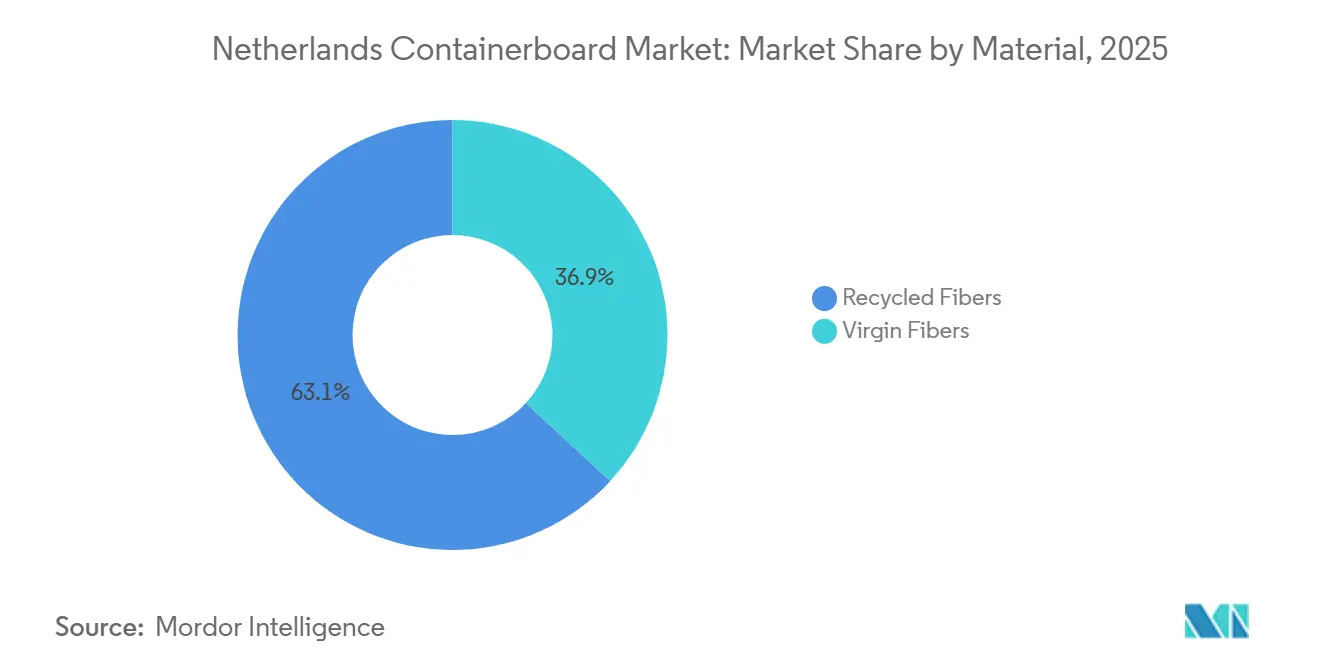

- By material, recycled fibers captured 63.11% of the Netherlands containerboard market share in 2025.

- By product type, the Netherlands containerboard market size for the kraftliners segment is forecast to advance at a 1.97% CAGR through 2031.

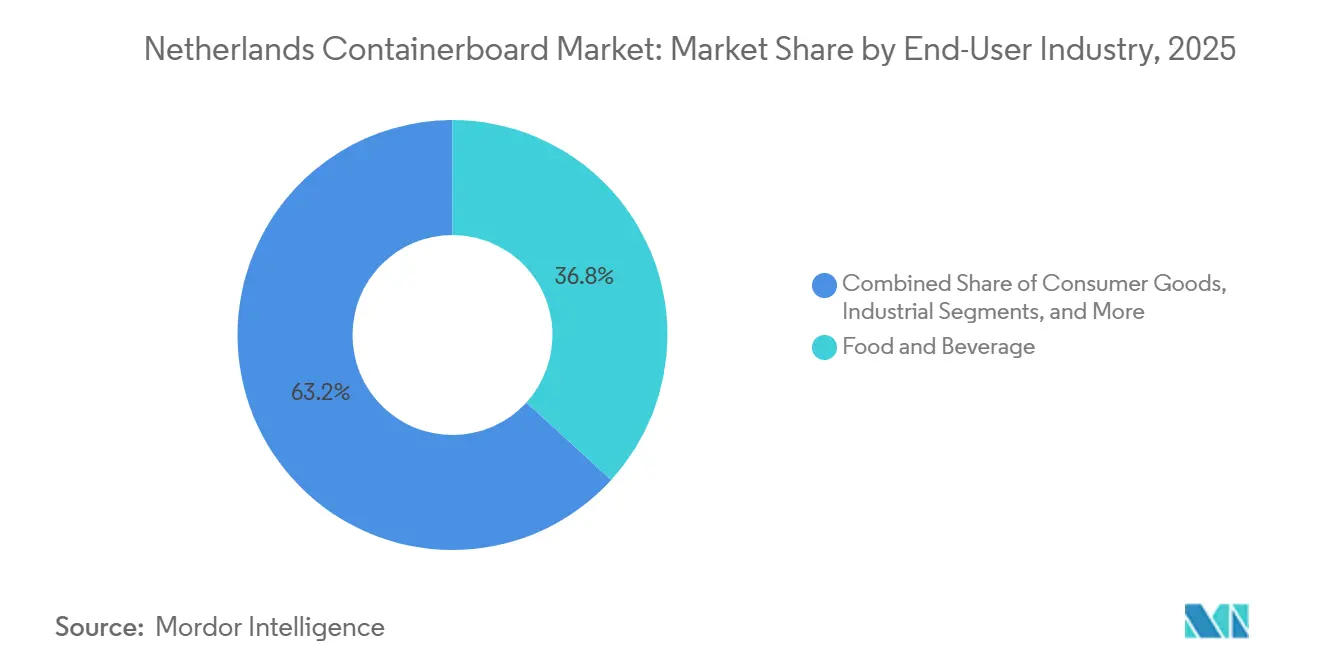

- By end-user industry, food and beverage captured 36.77% of the Netherlands containerboard market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Netherlands Containerboard Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Fiber-Based Food Transit Packaging | +0.5% | National, with concentration in Westland, Aalsmeer, and North Brabant horticultural zones | Medium term (2-4 years) |

| Expansion of Dutch E-Commerce Parcel Flows | +0.4% | National, with early gains in Randstad, Amsterdam, Rotterdam, and Utrecht | Short term (≤ 2 years) |

| PPWR-Driven Shift Toward Recyclable Transport Packaging | +0.3% | EU-wide, with accelerated compliance demand in the Netherlands and Belgium | Medium term (2-4 years) |

| Retail Migration to Shelf-Ready Corrugated Formats | +0.2% | National, with early adoption in supermarket distribution centers in Noord-Holland and Zuid-Holland | Medium term (2-4 years) |

| Tighter Empty-Space Rules Accelerating Right-Sized Box Demand | +0.1% | EU-wide, with impact concentrated in Netherlands e-commerce and logistics hubs | Short term (≤ 2 years) |

| Humidity-Resistant Fluting Demand in Cold-Chain Produce Exports | +0.1% | National, with export-facing impact in the North Sea corridor toward the United Kingdom and Scandinavia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand For Fiber-Based Food Transit Packaging

The Netherlands containerboard market is closely tied to the country’s position as a horticultural and food logistics center, making corrugated packaging part of the transport infrastructure rather than a discretionary packaging choice. Dutch produce, flowers, and processed foods move through high-speed, temperature-controlled distribution systems that rely on standardized corrugated formats to reduce handling delays and maintain steady throughput. Corrugated cardboard already carries close to 75% of goods across European food, pharmaceutical, and consumer goods supply chains, which supports the baseline role of containerboard in the Netherlands containerboard market. Demand from greenhouse clusters in Westland, West Friesland, and Aalsmeer remained resilient even amid broader softness across Western Europe in 2024 and 2025. Retailers are also asking for stronger board grades to reduce in-transit damage claims, which is raising effective grammage requirements even as lightweighting remains a broader European theme.

Expansion Of Dutch E-Commerce Parcel Flows

The Netherlands containerboard market is still supported by parcel activity because the Dutch parcel system handled 606 million parcels in 2024, up 2% year over year, and the average household received 59 parcels during the year. Cross-border parcel volumes increased 12% in 2024, while Dutch reporting in late 2025 indicated that close to 3 million parcels a day were entering through Rotterdam and Schiphol as Chinese platforms expanded their presence. Dutch online consumer spending reached EUR 36 billion (USD 40.7 billion) at the 2024 average exchange rate, which sustained demand for shipping cases and custom-sized corrugated mailers in the Netherlands containerboard market. PostNL restructured its Parcels division into separate E-commerce and Platforms units from January 1, 2026, and it plans to add 600 locker sites each year to reach 3,600 points by the end of 2028. The shift now is less about simple volume growth and more about smaller, more frequent shipments that require cleaner printability, tighter dimensions, and better presentation quality in corrugated packaging.

PPWR-Driven Shift Toward Recyclable Transport Packaging

The Netherlands containerboard market is being reshaped by the Packaging and Packaging Waste Regulation, which entered into force in February 2025 and applies from August 12, 2026.[1]European Commission, “Packaging and Packaging Waste Regulation (PPWR) Frequently Asked Questions,” European Commission, europa.eu The regulation requires all EU packaging to be recyclable by 2030 and limits the space in grouped, transport, and e-commerce packaging to 50%, directing investment toward automated right-sizing equipment at Dutch converting plants.[2]EUROPEN, “Packaging and Packaging Waste Regulation (PPWR) Final Text,” EUROPEN, europen-packaging.eu FEFCO stated in late 2024 that corrugated cardboard is exempt from the PPWR reuse target obligations under Article 29, which removed a major substitution concern for the Netherlands containerboard market during the drafting phase. The Dutch market entered this compliance cycle with a strong paper packaging collection base, which reduces adjustment pressure relative to less developed collection systems. The practical result is that non-recyclable transport packaging options face a tougher regulatory path, while corrugated formats become the default solution for retailers and logistics operators working under the new rules.

Retail Migration To Shelf-Ready Corrugated Formats

The Netherlands containerboard market is benefiting from retail demand for shelf-ready packaging, as Dutch grocery chains increasingly seek corrugated packs that serve both as transit containers and in-store display units. Micro flute formats, such as E and F flutes, reduce store restocking labor and create greater value through high-quality print coverage, which brand owners now treat as part of a commercial presentation rather than a simple packaging expense.[3]EBC Golfkarton, “Vijf Trends in Shelf Ready Packaging (SRP),” EBC Golfkarton, ebc-golfkarton.nl EBC Golfkarton identified full-color branding, dual e-commerce and retail functionality, and cold-chain-resistant constructions as key SRP trends in the Dutch market in September 2025. As SRP adoption increases, converters need faster job changes and better die management, which is making sub-10-minute changeovers a practical requirement for participation in this part of the Netherlands containerboard market. Golfkarton confirmed in February 2026 that SRP is being positioned as a sustainability solution because it combines transit and display functions in a single recyclable fiber format.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Recovered Paper and Energy Cost Volatility | -0.6% | National, with upstream price transmission from German and Belgian OCC markets | Short term (≤ 2 years) |

| Western European Containerboard Overcapacity and Price Pressure | -0.4% | EU-wide, with strongest price erosion in Northwestern European spot markets including the Netherlands | Medium term (2-4 years) |

| Dutch Labor Tightness in Converting and Logistics Operations | -0.2% | National, with acute shortages in technical roles in Noord-Holland, Zuid-Holland, and Noord-Brabant | Short term (≤ 2 years) |

| Reusable Transport-Packaging Trials in Fresh-Produce Loops | -0.1% | National, with early displacement in the Westland and Aalsmeer produce and floriculture corridors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Recovered Paper And Energy Cost Volatility

The Netherlands containerboard market remains exposed to raw material swings, as OCC prices at Rotterdam moved between EUR 80 (USD 90) and EUR 140 (USD 158) per tonne during 2024 and 2025. IMtrade reported in February 2025 that recovered paper spot prices rebounded after the December 2024 trough, with subgrade prices rising by EUR 10 (USD 11.2) per tonne as post-holiday collection volumes fell and sorting output tightened. Energy exposure adds a second cost burden because Dutch paper mills still operate at natural gas prices that remained close to double pre-2020 benchmarks through 2025. This combination squeezes mid-sized converting plants more than integrated producers because independent operators usually lack cogeneration or biogas assets that can soften sudden input spikes in the Netherlands containerboard market.[4]Billerud Aktiebolag, “Interim Report January-March 2025,” Billerud, billerud.com Billerud also confirmed that, from 2026, its European mills will face additional carbon dioxide taxation as free EU Emissions Trading System rights are phased out, which will continue to put pressure on regional pricing.

Western European Containerboard Overcapacity And Price Pressure

The Netherlands containerboard market is also constrained by Western European oversupply because nearly 1.5 million tonnes of new capacity ramped up in 2025, and the regional three-month moving operating ratio stood close to 82% in August 2025. Smurfit Westrock’s chief executive described the European market as “pretty bad right now” in October 2025, after the expected fourth-quarter demand improvement failed to materialize. For Dutch producers and converters, that surplus translated into ongoing pressure on testliner and fluting pricing, especially when buyers could access discounted German or Belgian spot material. Conditions improved in March and April 2026 as prices rose on stronger demand and higher energy costs, but Smurfit Westrock still indicated that full operating rate normalization across Western Europe is unlikely before mid-2027.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Recycled Fibers Lead While Virgin Grades Regain Selective Momentum

Recycled fibers held 63.11% of the Netherlands containerboard market share in 2025, supported by the country’s strong recovered paper system and the cost position of testliner and fluting production based on Old Corrugated Containers feedstock. Paper and cardboard packaging collection in the Netherlands remained high, at close to 85%, which reinforces the role of recycled board across the Netherlands containerboard market. Germany remained the main source of Dutch recovered paper imports in 2024, and its role strengthened the cross-border fiber link that underpins much of the recycled material flow used by converters. FSC and PEFC certification standards have become common reference points for both recycled and virgin sourcing, as food and retail buyers increasingly ask suppliers to support emission-reduction reporting and procurement compliance.

Virgin fibers are the fastest-growing material category, with the Netherlands containerboard market size outlook for this segment pointing to a 1.86% CAGR during 2026-2031. This growth is tied to a shift toward specifications that require stronger burst performance, better print surfaces, and higher moisture resistance than recycled grades can always provide in cold-chain settings. The change is most visible in premium produce exports, floriculture shipments, and branded e-commerce packaging, where board failure carries a higher commercial cost. Billerud’s investment in a new headbox at the Gruvön mill, announced in December 2025 with upgraded product availability planned for H2 2026, shows how suppliers are targeting the Netherlands containerboard industry with performance-led virgin fluting for demanding logistics channels.

By Product Type: Testliners Hold Scale While Kraftliners Gain On Performance Needs

Testliners accounted for 40.18% of the Netherlands containerboard market size in 2025. Their lead came from a close fit with the cost needs and sustainability priorities of Dutch converters, in which mid-weight single-wall boxes for food, fast-moving consumer goods, and e-commerce accounted for the largest share of production volume. Flutings remained the companion medium in the corrugated structure, and Dutch mills continued to serve both domestic converters and nearby export customers in Germany and Belgium with recycled and semichemical grades. Together, testliners and flutings still define the operating core of the Netherlands containerboard market because both products align with a recycled-fiber converting base and with policy pressure favoring recyclable formats.

Kraftliners are the fastest-growing product type and are forecast to expand at a 1.97% CAGR during 2026-2031. Demand is increasing for export applications in chemicals, machinery, agriculture, and premium logistics, where stronger double- or triple-wall structures are needed that testliner-based combinations cannot reliably support. Shelf-ready micro flute trays are also supporting this shift because the outer layer must combine print quality with higher burst resistance to meet retailer expectations. The Netherlands containerboard market also saw Kraftliner pricing hold up better than recycled grades through much of 2025 because virgin supply was more concentrated in Nordic mills and less exposed to the most severe part of Western European overcapacity.

By End-User Industry: Food And Beverage Provides Stability While Consumer Goods Expands Faster

Food and beverage led the Netherlands containerboard market with 36.77% in 2025. This segment held up well because it is tied to everyday consumption and because Dutch horticultural zones move tomatoes, peppers, cucumbers, flowers, and processed food through corrugated packaging on continuous schedules. The Netherlands containerboard market, therefore, retained a stable demand base even when wider Western European industrial activity remained softer. Reporting in late 2025 also described the Netherlands as a major gateway for fresh produce, with repacking and re-export to Germany, Scandinavia, and the United Kingdom, reinforcing the need for dependable food-grade corrugated packaging.

Consumer goods are the fastest-growing end-user segment, with the Netherlands containerboard market size for this application expected to rise at a 2.14% CAGR during 2026-2031. Growth comes from the shift away from rigid plastics in personal care and household products, and from the rise of e-commerce-oriented brands seeking printed corrugated mailers and secondary packs. A 2025 consumer survey cited in Dutch packaging reporting found that 77% of consumers considered recyclability very important in packaging decisions, giving brand owners a clear reason to shift more packaging spend toward fiber formats. Industrial demand remained steady through chemicals, machinery, and electronics exports, while other end-user industries, such as pharmaceuticals and agriculture, created smaller but more specialized opportunities around GDP-compliant micro flute and humidity-resistant board.

Geography Analysis

The Netherlands containerboard market is well-positioned within Western Europe because the country serves as both a domestic consumption market and a production node, as well as a transit point for corrugated trade to Germany, Belgium, the United Kingdom, and France. The Port of Rotterdam handled close to 430 million tonnes of cargo in 2024, which supported both inbound raw material flows and outbound shipments of finished corrugated products. Western European containerboard net exports reached record levels in January 2025, more than 20% higher than a year earlier, helping the Netherlands containerboard market benefit from its strong logistics base and converting capacity. The Randstad corridor, including Amsterdam, Rotterdam, Utrecht, and The Hague, concentrates a large share of national demand because it combines fulfillment centers, food distribution hubs, and third-party logistics activity. That concentration favors converting plants that can respond quickly to short replenishment cycles and custom packaging runs.

Zuid-Holland and North Holland are the most intensive food-led demand zones in the Netherlands containerboard market because the Westland, De Lier, and Aalsmeer corridors require high-throughput corrugated packaging for produce and floriculture shipments. Dutch horticultural exports were valued at EUR 36 billion (USD 40.7 billion), underscoring how closely packaging demand is tied to agricultural logistics rather than solely to local consumer demand. Eastern provinces such as Gelderland and Overijssel support a different demand profile because they host mid-sized converting plants that serve machinery, food processing, and chemical customers on longer planning cycles. These sub-regional differences keep the grade mix uneven across the country, with produce corridors favoring humidity-resistant, high-burst-strength boards over commodity transit formats.

Germany is the dominant cross-border counterpart for the Netherlands containerboard market because it is both the main source of recovered paper inputs and the largest nearby destination for Dutch corrugated exports. In 2024, Germany accounted for 68.42% of the value of Dutch recovered paper imports, leaving Dutch converters exposed to German fiber price movements. Reliance on Sweden and Finland for some kraft grades adds a second procurement risk as Nordic pulpwood costs rise. Managing the Rotterdam-to-Germany corridor efficiently will remain a central margin issue for the Netherlands containerboard market through 2031.

Competitive Landscape

The Netherlands containerboard market remains oligopolistic at the integrated producer level because a limited group of large European players controls much of the supply through linked Benelux mill-to-box-plant networks. These groups use the OCC purchasing scale, energy assets, and downstream converting operations to absorb volatility more effectively than stand-alone converters can. In April 2026, Smurfit WestRock began consultations on closing four converting facilities in the Netherlands as part of a broader asset optimization plan, indicating that capacity rationalization remains active in the Netherlands containerboard market. The same company also used its Q1 2026 European Innovation Event to showcase AI-enabled packaging capabilities to more than 200 customers, underscoring how digital design tools are now part of competitive differentiation. Independent Dutch converters continue to compete in areas such as shelf-ready packaging, industrial transit packaging, and protective e-commerce formats, but they still face cost and automation disadvantages against the larger integrated groups.

Independent activity in the Netherlands containerboard market still matters in specialized niches, but the business model is under clear pressure. Solidus Solutions completed a financial restructuring in February 2025, closed its Bad Nieuweschans site in June 2025, and then installed two new large-format presses in April 2026, which reflects a restructure-and-reinvest pattern rather than simple expansion. White-space opportunities remain strongest in humidity-resistant fluting for produce exporters, GDP-compliant micro flute for pharmaceutical logistics, and right-sized automated corrugated boxing for e-commerce fulfillment hubs. Smaller converters have also been able to win selected SRP orders by combining computer-aided die libraries with fast-set folder gluers that can switch jobs in under 10 minutes.

Competition in the Netherlands containerboard market is also shifting at the grade level, as product performance can now push specifications away from incumbent recycled-fiber formats in difficult applications. Billerud’s headbox investment at Gruvön is intended to improve strength, sheet uniformity, and fiber orientation in Billerud Flute, and the company stated that converters may reduce grammage by one specification level in some produce applications while preserving packaging performance. The end of free carbon allowances from 2026 also shifts the advantage toward producers with biomass, biogas, or cogeneration assets, gradually reshaping the supply base serving the Netherlands containerboard market. Even with that change, the overall structure remains concentrated because large, integrated European groups still set the main competitive terms, while specialists retain room in narrower applications.

Netherlands Containerboard Industry Leaders

Smurfit Westrock plc

International Paper Company

Mondi plc

VPK Group NV

Stora Enso Oyj

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Smurfit Westrock plc entered formal consultations regarding the potential closure of four converting facilities located in the Netherlands, alongside one mill in the United Kingdom, as part of an asset optimization program disclosed in its Q1 2026 earnings release filed via Business Wire. The Netherlands consultations involve converting operations and reflect the company's strategy to rationalize its Benelux footprint amid continued European containerboard overcapacity. Adjusted EBITDA for the EMEA and APAC segment reached USD 421 million in Q1 2026, up from USD 389 million in Q1 2025, as containerboard prices rose in March and April 2026 amid higher energy costs and improved demand conditions.

- April 2026: Solidus Solutions B.V. installed two new Koenig and Bauer Rapida large-format presses, a Rapida 145 at its Oude Pekela, Netherlands, plant and a Rapida 164 at its Hoogstraten, Belgium, facility, to address rising quality demands and accelerate penetration of sustainable solid board markets as a replacement for plastic-based packaging, per the company's press release. The hybrid 6-color presses handle materials from 500 gsm to 1.8 mm thickness and support UV, food-safe, and water-resistant Sapino-processed inks, expanding the company's capability in high-specification food and personal care packaging.

- January 2026: PostNL restructured its Parcels division into two distinct business units, E-commerce and Platforms, effective January 1, 2026, shifting from a volume-driven to a value-driven operational model, per its 2025 Annual Report. The restructuring is accompanied by a plan to expand the company's parcel locker network by 600 sites per year from 2026, targeting 3,600 nationwide locker points by the end of 2028, which will alter packaging format specifications as out-of-home delivery volumes grow and demand for optimally sized corrugated formats intensifies.

- December 2025: Billerud Aktiebolag announced an investment in a new headbox for its paper machine at the Gruvön mill in Sweden to enhance the strength, sheet uniformity, and fiber orientation of Billerud Flute, a primary northern birch fiber fluting, with the rebuild scheduled for April 2026 and commercial availability of the upgraded product planned for H2 2026, per the company's investor communications. The investment targets demanding cold-chain logistics and fresh produce packaging environments, including Dutch horticultural export channels, and is expected to allow converters to reduce grammage by one specification level in certain applications while maintaining performance.

Netherlands Containerboard Market Report Scope

The Netherlands Containerboard Market encompasses the production, distribution, and consumption of containerboard used in the manufacturing of corrugated packaging solutions. It includes containerboard made from virgin and recycled fibers, covering key product types such as kraftliners, testliners, and flutings. These materials are primarily used in protective and transport packaging applications across various end-user industries, including food and beverage, consumer goods, industrial, pharmaceuticals, and agriculture. The increasing demand for sustainable, lightweight, and durable packaging solutions drives the market.

The Netherlands Containerboard Market Report is Segmented by Material (Virgin Fibers, and Recycled Fibers), Product Type (Kraftliners, Testliners, and Flutings), and End-User Industry (Food and Beverage, Consumer Goods, Industrial, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Virgin Fibers |

| Recycled Fibers |

| Kraftliners |

| Testliners |

| Flutings |

| Food and Beverage |

| Consumer Goods |

| Industrial |

| Other End-User Industries |

| By Material | Virgin Fibers |

| Recycled Fibers | |

| By Product Type | Kraftliners |

| Testliners | |

| Flutings | |

| By End-User Industry | Food and Beverage |

| Consumer Goods | |

| Industrial | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the size outlook for containerboard demand in the Netherlands?

The Netherlands containerboard market was valued at USD 1.42 billion in 2025, stands at USD 1.46 billion in 2026, and is projected to reach USD 1.58 billion by 2031 at a 1.58% CAGR.

Which material segment leads demand in the Netherlands?

Recycled fibers led with a 63.11% share in 2025 because Dutch recovery systems and OCC-based cost economics support broad use of testliner and fluting grades.

Which product type is growing the fastest through 2031?

Kraftliners are forecast to expand at a 1.97% CAGR because higher-strength and better-printing grades are gaining use in premium e-commerce, retail, and industrial export applications.

Why does food and beverage remain the largest end-use category?

Food and beverage held 36.77% of demand in 2025 because Dutch horticulture, fresh produce distribution, and processed food trade require steady corrugated packaging flow through temperature-sensitive logistics chains.

How is e-commerce affecting packaging specifications in the Netherlands?

Parcel growth, cross-border shipments, and PostNL's locker expansion are increasing the need for right-sized boxes, printed mailers, and corrugated formats with better dimensional accuracy and presentation quality.

What is the main competitive theme over the next few years?

Large integrated European suppliers are likely to keep their lead through scale, energy assets, and network reach, while niche Dutch converters compete in SRP, protective transit formats, and specialized cold-chain applications.

Page last updated on: