Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

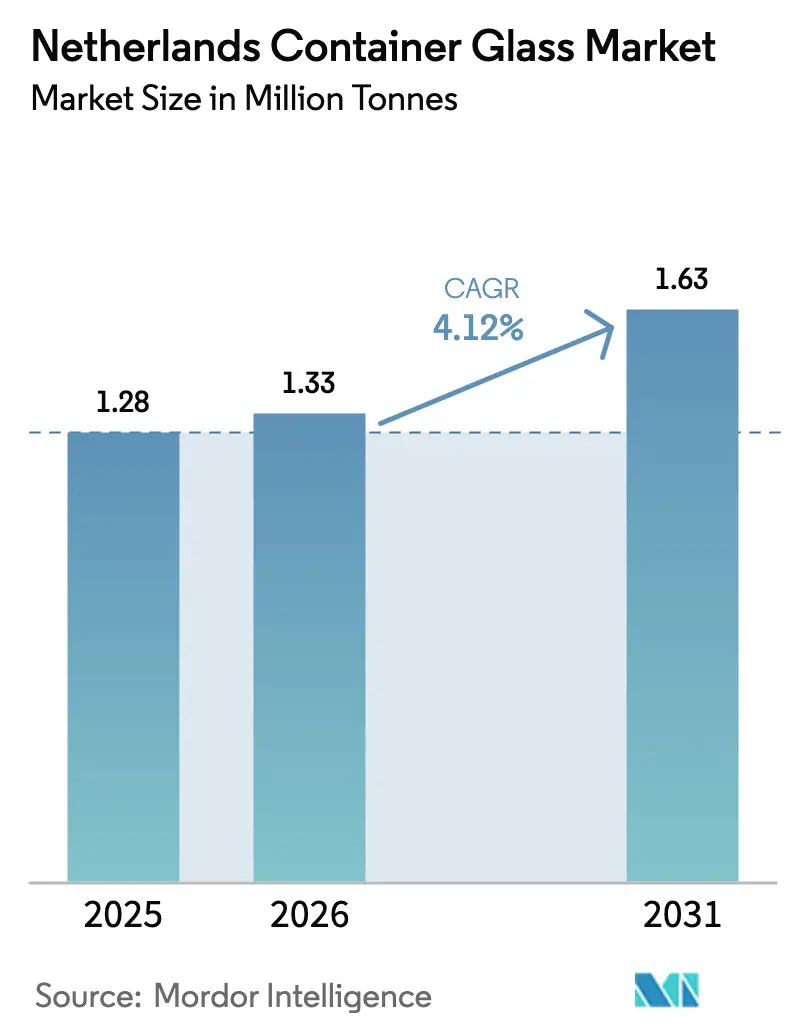

| Base Year Market Size (2025) | 1.28 Million tonnes |

| Market Volume (2026) | 1.33 Million tonnes |

| Market Volume (2031) | 1.63 Million tonnes |

| Growth Rate (2026 - 2031) | 4.12% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Netherlands Container Glass Market Analysis by Mordor Intelligence

The Netherlands Container Glass Market size was valued at 1.28 million tonnes in 2025 and estimated to grow from 1.33 million tonnes in 2026 to reach 1.63 million tonnes by 2031, at a CAGR of 4.12% during the forecast period (2026-2031). Rising demand for low-carbon packaging from beverage, cosmetics, and pharmaceutical brand owners, together with the country’s well-established recycling infrastructure, underpins steady volume expansion. Domestic consumption benefits from premiumization in beer, craft drinks, and luxury personal-care products, while export-oriented fillers leverage the Netherlands’ world-class logistics networks to serve adjacent European markets. Glass makers also gain a strategic advantage from regulatory tailwinds as the new EU Packaging and Packaging Waste Regulation incentivizes infinitely recyclable materials. Energy transition investments in hybrid or fully electric furnaces are gradually lowering production costs and carbon footprints, strengthening the competitive proposition of glass versus metal and paper alternatives.

Key Report Takeaways

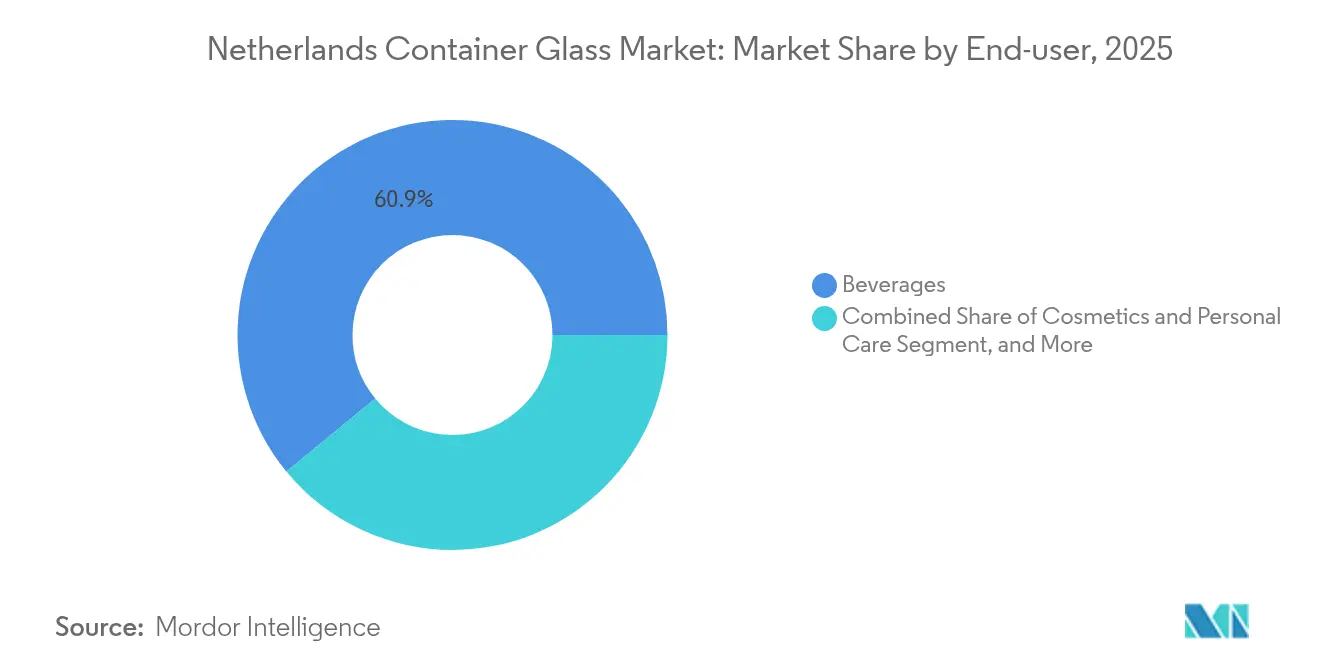

- By end-user, beverages captured 60.94% of the Netherlands container glass market share in 2025.

- By color, the Netherlands container glass market size for the amber glass segment is forecast to advance at a 5.4% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Netherlands Container Glass Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Demand for Sustainable Packaging Solutions | +1.2% | Netherlands and EU-wide | Medium term (2-4 years) |

| Growth in Beverage and Food Industry | +0.8% | Netherlands domestic market | Short term (≤ 2 years) |

| Technological Advancements in Glass Manufacturing | +0.6% | Netherlands and regional EU | Long term (≥ 4 years) |

| Government Regulations Promoting Recycling | +0.7% | EU-wide with Netherlands implementation | Medium term (2-4 years) |

| Rising Consumer Awareness about Environmental Impact | +0.5% | Netherlands and Western Europe | Short term (≤ 2 years) |

| Expansion of Pharmaceutical and Cosmetic Industries | +0.9% | Netherlands and Benelux region | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Demand for Sustainable Packaging Solutions

Glass enjoys infinite recyclability, absence of chemical migration and a premium look that resonates with eco-conscious Dutch and EU consumers. The EU Packaging and Packaging Waste Regulation pushes brands toward higher recycled content and stricter recyclability thresholds, effectively favoring glass over complex multilayer plastics.[1]European Union, “Regulation (EU) 2025/40 on Packaging and Packaging Waste,” europa.eu Dutch municipalities already collect 86% of glass packaging, supplying cullet that lowers furnace energy demand and furnace emissions. Heineken allocated EUR 583 million (USD 659 million) in returnable-glass deposits at end-2024, underscoring brand commitment to closed-loop solutions. Consumer surveys show 73% of Europeans consider glass ocean-friendly, bolstering retailer decisions to replace plastic jars with glass formats.[2]Consumer Goods Technology, “U.S. Glass Shortage Putting a Crack in CPG Sustainability Efforts,” consumergoods.com Collectively, these attitudes lift long-term demand in the Netherlands container glass market.

Growth in Beverage and Food Industry

The Netherlands hosts flagship breweries such as Heineken and AB InBev franchises, plus a vibrant craft-beer cluster that embraces distinctive bottle designs to reinforce brand identity. Heineken’s Texels brand grew 20% domestically in 2024 on premium positioning despite modest overall beer volume softness. On the logistics side, Dutch ports handled 545 million tonnes of freight in 2023, accelerating throughput of packaged beverages to Germany, France and Scandinavia. Organic foods packed in flint glass jars capture higher margins at supermarkets, reflecting consumer trust in the material’s inertness. E-commerce grocery channels further catalyze volume because glass survives parcel shipment with minimal product waste when properly designed.

Technological Advancements in Glass Manufacturing

Hybrid and fully electric furnaces unlock substantial CO₂ reductions and cost savings over time. Ardagh’s NextGen furnace in Obernkirchen achieves 60% renewable electricity input and 60% lower emissions per bottle. Verallia’s 100% electric furnace in Cognac operates at 180 tons per day with a 60% carbon cut, providing a template for Dutch glassworks targeting forthcoming zero-emission requirements.[3]Verallia, “2024 First Half Financial Report,” verallia.com Lightweighting breakthroughs, such as Vidrala’s 260-gram 75 cl bottle, trim raw material use and transport fuel burn. Vetropack’s Echovai process hardens bottles thermally so they can be reused longer while weighing 30% less. Adoption of these innovations cements the competitiveness of the Netherlands' container glass market.

Government Regulations Promoting Recycling

EU-wide targets require 90% collection of glass packaging by 2030, up from the 80.8% average achieved in 2023. Dutch policymakers already impose producer-responsibility fees linked to recyclability, lowering levies on mono-material glass and boosting its cost advantage over composite packaging. FEVE, the European container glass federation, has committed to net-zero roadmaps that align with Dutch climate policy, signaling regulatory certainty for investments in furnace electrification and high-cullet formulations. The Kennisinstituut Duurzaam Verpakken confirms glass safety for food contact, reinforcing its status in nutrient-sensitive applications.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost of Raw Materials | -0.9% | Netherlands and European supply chain | Short term (≤ 2 years) |

| Competition from Alternative Packaging Materials | -1.1% | Netherlands and broader EU markets | Medium term (2-4 years) |

| Energy-Intensive Production Process | -0.7% | Netherlands and European manufacturing | Medium term (2-4 years) |

| Stringent Environmental Regulations | -0.6% | EU-wide with Netherlands compliance focus | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost of Raw Materials

Glass production remains energy-intensive, with furnace melting responsible for roughly 70% of manufacturing energy load. Verallia’s Northern and Eastern Europe EBITDA margin fell 747 basis points to 20% in 2024 amid high gas prices. Chinese flat-glass spot prices climbed 30% during early 2025, rippling into European soda ash and cullet markets. The Netherlands imported only USD 1.16 million of quartz in 2022, indicating exposure to supply disruptions from concentrated mining regions. Forward hedging eases some volatility, yet capital needed for hybrid furnaces competes with working-capital requirements, pressuring balance sheets in the Netherlands container glass industry.

Competition from Alternative Packaging Materials

Metal cans, paperboard cartons and advanced flexible films encroach on occasions historically reserved for glass. Ardagh Metal Packaging recorded 5% shipment growth in Europe in 2024 as beverage brands chased lighter formats. O-I Glass estimates brand owners begin shifting at a 15% price gap between glass and cans, with rapid migration once the gap exceeds 25%. EU weight-reduction targets exempt paper, accelerating paperization of certain food lines. To defend share, Dutch producers intensify lightweighting and develop refillable ecosystems that mitigate logistic cost disadvantages relative to one-way containers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-User - Beverages Anchor Demand while Cosmetics Accelerate Growth

The beverages segment contributed 60.94% of the Netherlands' container glass market volume in 2025. Domestically brewed beer, imported specialty wines, and export-bound spirits collectively absorb the bulk of furnace capacity, and the segment will still represent well above half of the Netherlands' container glass market size in 2031. Craft breweries specify embossed or bespoke bottles to differentiate shelf presence, sustaining value per tonne. Meanwhile, international drinks groups increasingly stipulate minimum cullet content or insist on returnable pool schemes, bolstering demand for high-grade flint bottles.

Cosmetics and personal care packaging are on course for a 5.12% CAGR between 2026 and 2031, the highest among end-users. Luxury skincare and fragrance houses favor heavy-wall flint or colored flacons that signal prestige and sustainability. SGD Pharma recently commercialized jars containing 20% post-consumer recycled glass, reducing energy use and helping brand owners hit Scope 3 targets. Pharmaceuticals also present upside: SCHOTT Pharma expanded syringe capacity across Central Europe to meet injectable biologics demand, channeling incremental orders to Dutch distributors. Overall, premium-focused categories underpin revenue resilience in the Netherlands container glass market.

By Color - Flint Maintains Leadership while Amber Gains Momentum

Flint bottles and jars accounted for 41.78 of % Netherlands' container glass market share in 2025. Transparent packaging enables shoppers to verify product quality visually, a decisive factor for organic sauces, craft beers, and vitamins. The Netherlands container glass market size for flint packaging is anticipated to expand steadily through 2031 as lightweighting lowers transport emissions without compromising clarity. Manufacturers now routinely produce 0.33-liter beer bottles under 190 grams, a 20% reduction relative to 2020 designs.

Amber glass, forecast to post a 5.4% CAGR, shields contents from ultraviolet degradation, making it ideal for light-sensitive spirits, nutraceuticals, and biologic drugs. Pharmaceutical fill-and-finish plants in Breda and Den Bosch increasingly request amber vials with tight dimensional tolerances. Vista bottles from Verallia, made with 100% post-consumer recycled amber cullet, demonstrate that color innovation can align with carbon neutrality ambitions. Green glass maintains a niche in continental lager and wine formats linked to heritage branding, while specialty blues and metallic sheens appear in ultra-premium gin launches, adding visual distinctiveness that commands price premiums.

Geography Analysis

Dutch container glass output benefits from the country’s central location within the European single market. Producers leverage short transit times to German fillers and French cosmetic hubs, keeping freight costs and carbon emissions competitive. Seamless highway and deep-sea port networks facilitate the import of soda ash and the export of finished bottles, reinforcing the logistics leadership of the Netherlands' container glass market.

Recycling infrastructure outperforms EU averages, with 86% collection, translating into abundant high-quality cullet for domestic furnaces. Alignment with EU deposit-return schemes ensures readiness for the 90% collection target by 2030, mitigating cullet supply disruptions. Regional technology spillovers are evident: Dutch plants evaluate Verallia’s electric furnace blueprint and Ardagh’s 60% renewable hybrid design to meet decarbonization roadmaps.

Cross-border market signals can still create volatility. German demand softened 2.5% in 2024, prompting capacity rationalization under O-I’s Fit to Win program that trims 14% of European. Conversely, high-growth Belgian investments such as Ciner’s 1,300 tons-per-day plant in Lommel will tighten skilled-labor supply along the Dutch border by 2026. These developments highlight the need for Dutch producers to safeguard energy hedges and automation funding to maintain regional cost leadership.

Competitive Landscape

Global multinationals dominate but do not monopolize Dutch capacity, yielding a moderately concentrated arena. O-I Glass operates furnaces in Leerdam and Maastricht within its 34-plant European network, catering to beverage and food clients. Verallia strengthened its Benelux presence after purchasing Vidrala’s Italian business for EUR 230 million (USD 260 million) and is piloting 100% electric melting technology to raise sustainability credentials. Ardagh’s NextGen furnace showcases hybrid heating at scale, attracting marquee contracts like the Jägermeister 14 million-bottle agreement, evidence that decarbonization roadmaps win business in premium spirits.

Specialists thrive in higher-margin niches. SCHOTT Flat Glass in Tiel supplies specialty architectural panels and laboratory glassware, posting EUR 250.1 million (USD 270.6 million) in sales during its latest fiscal year. Vetropack advances thermal-hardening technology, enabling reusable bottles 30% lighter than conventional returnable glass, appealing to circular-economy retailers. TricorBraun’s acquisition spree of Euroglas and Glaspack expands the distribution of custom flacons to regional beauty brands, intensifying downstream competition.

Strategic themes center on footprint optimization, recycled content scalability and service innovation. O-I’s capacity closures free capital for furnace upgrades, while Verallia invests EUR 1.6 billion (USD 1.73 billion) across Europe through 2030 to decarbonize melt shops. White-space opportunities exist in digital printing, smart labeling and reusable infrastructure, segments where incumbents collaborate with technology startups to preserve glass’s premium status in the Netherlands container glass market.

Netherlands Container Glass Industry Leaders

Ardagh Group S.A.

O-I Glass, Inc.

Verallia SA

Vidrala S.A.

Vetropack Holding Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Vetropack partnered with Iprotec to scale lightweight reusable bottles, targeting commercial output in Q2 2026.

- August 2025: Ciner Glass arranged EUR 504 million (USD 545 million) financing for a 1,300 tons-per-day greenfield plant in Lommel, Belgium.

- July 2025: Ardagh Glass Packaging secured a contract to deliver 14 million low-carbon emerald bottles annually to Jägermeister using its hybrid NextGen furnace.

- July 2025: Verallia completed a EUR 230 million (USD 248 million) purchase of Vidrala’s Italian operations, adding 225 kilotons of capacity.

Netherlands Container Glass Market Report Scope

Container glass is used in the alcoholic and non-alcoholic beverage industries due to its ability to maintain chemical inertness, sterility, and non-permeability. Glass packaging is valued for its unique properties, including its transparency, inertness, and ability to preserve the quality and integrity of its contents. It is often chosen for products where purity, safety, and environmental sustainability are paramount concerns.

The Netherlands container glass market is segmented by end-user vertical (beverages [alcoholic beverages (beer, wine, spirits, and other alcoholic beverages {cider and other fermented drinks}), non-alcoholic beverages (juices, carbonated drinks (CSDs), dairy product-based drinks, other non-alcoholic beverages)], food [jam, jelly, marmalades, honey, sausages and condiments, oil, pickles], cosmetics and personal care, pharmaceuticals (excluding vials and ampoules), and perfumery, by color (green, amber, flint and other colors). The report offers market forecasts and size in volume (kilotons) for all the above segments.

By End-user

| Beverages | Alcoholic | Beer |

| Wine | ||

| Spirits | ||

| Other Alcoholic Beverages (Cider and Other Fermented Drinks) | ||

| Non-Alcoholic | Juices | |

| Carbonated Drinks (CSDs) | ||

| Dairy Product Based Drinks | ||

| Other Non-Alcoholic Beverages | ||

| Food (Jam, Jelly, Marmalades, Honey, Sausages and Condiments, Oil, Pickles) | ||

| Cosmetics and Personal Care | ||

| Pharmaceuticals (excluding Vials and Ampoules) | ||

| Perfumery | ||

By Color

| Green |

| Amber |

| Flint |

| Other Colors |

| By End-user | Beverages | Alcoholic | Beer |

| Wine | |||

| Spirits | |||

| Other Alcoholic Beverages (Cider and Other Fermented Drinks) | |||

| Non-Alcoholic | Juices | ||

| Carbonated Drinks (CSDs) | |||

| Dairy Product Based Drinks | |||

| Other Non-Alcoholic Beverages | |||

| Food (Jam, Jelly, Marmalades, Honey, Sausages and Condiments, Oil, Pickles) | |||

| Cosmetics and Personal Care | |||

| Pharmaceuticals (excluding Vials and Ampoules) | |||

| Perfumery | |||

| By Color | Green | ||

| Amber | |||

| Flint | |||

| Other Colors | |||

Key Questions Answered in the Report

What is the current volume of the Netherlands container glass market?

The market stands at 1.33 million tonnes in 2026 and is projected to grow steadily through 2031.

Which end-user category drives the highest demand?

Beverages account for 60.94% of total volume, anchored by major breweries and premium drink producers.

Why is amber glass gaining popularity?

Amber glass blocks ultraviolet light, protecting pharmaceuticals and cosmetics that are sensitive to photodegradation, leading to a forecast 5.4% CAGR for the segment through 2031.

How are Dutch manufacturers reducing carbon emissions?

Firms are adopting hybrid or fully electric furnaces, boosting cullet use above 60% and pursuing lightweight bottle designs that cut transport fuel consumption.

What regulatory changes influence packaging choices?

The EU Packaging and Packaging Waste Regulation mandates higher recyclability and collection targets, favoring infinitely recyclable materials like glass.

Page last updated on: