Nigeria Containerboard Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

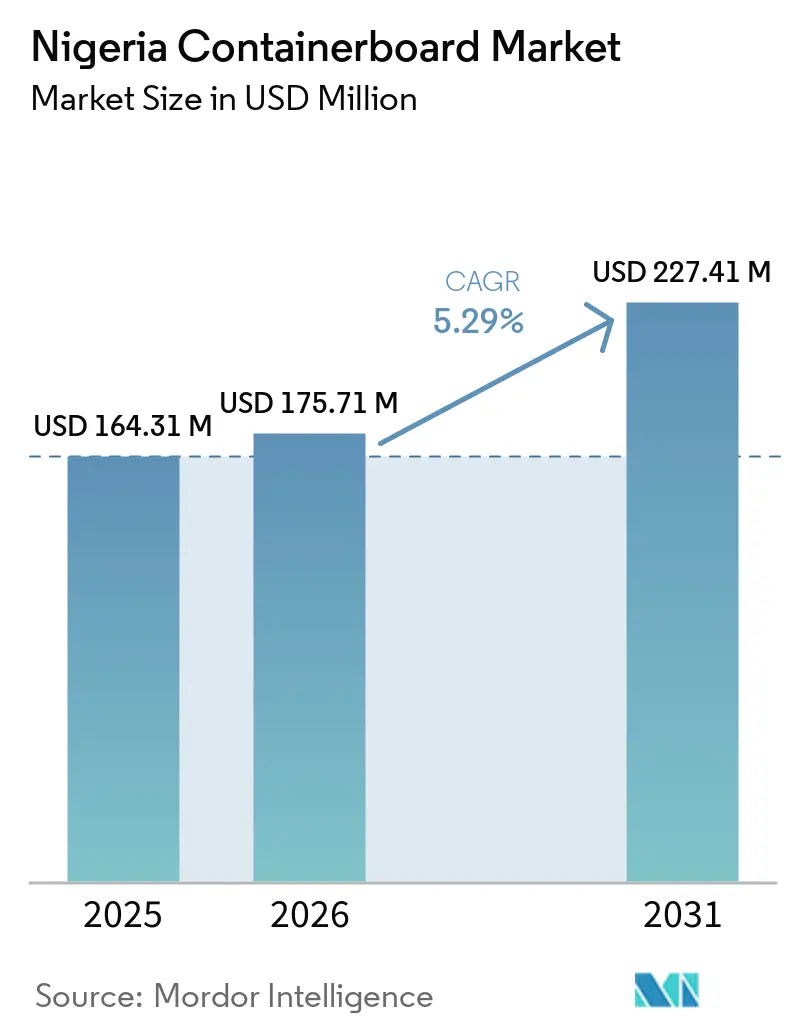

| Base Year Market Size (2025) | USD 164.31 Million |

| Market Size (2026) | USD 175.71 Million |

| Market Size (2031) | USD 227.41 Million |

| Growth Rate (2026 - 2031) | 5.29% CAGR |

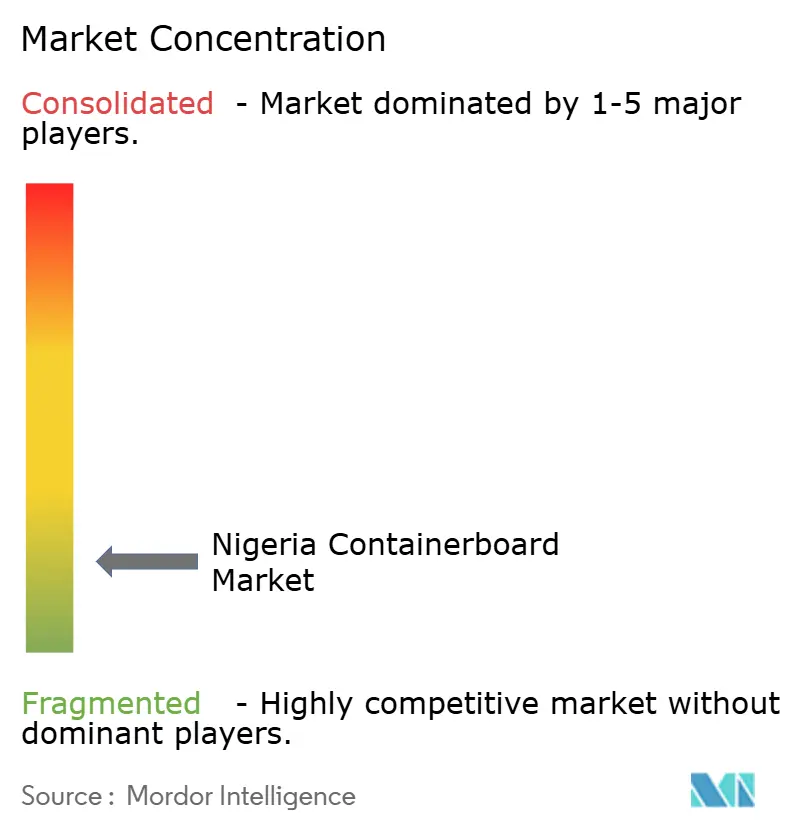

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Nigeria Containerboard Market Analysis by Mordor Intelligence

The Nigeria containerboard market size is projected to expand from USD 164.31 million in 2025 and USD 175.71 million in 2026 to USD 227.41 million by 2031, registering a CAGR of 5.29% between 2026 to 2031. A durable demand base supports the Nigerian containerboard market because the country remains the largest FMCG and food manufacturing center in West Africa. Demand is no longer driven solely by population growth, as export shippers, e-commerce operators, and formal retail chains are moving toward stronger, better-certified corrugated formats. This shift is increasing revenue per board meter because buyers are choosing burst-tested, compliance-ready constructions over commodity grades. Cost conditions remain a major constraint because imported reels, replacement parts, and power inputs have become more expensive in naira terms, keeping converter margins under pressure. Even with those constraints, the Nigerian containerboard market continues to offer opportunities in printed shelf-ready trays, moisture-barrier boards for agro-export routes, and precision-die-cut secondary cartons, where domestic supply remains limited.

Key Report Takeaways

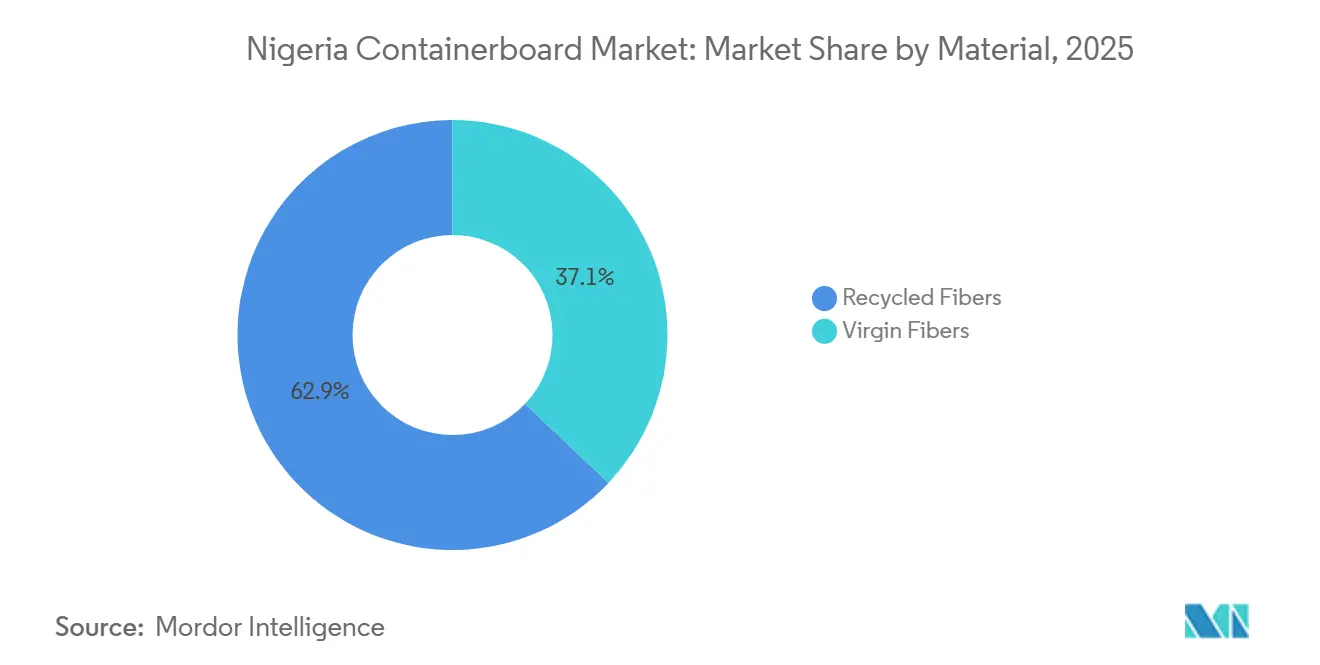

- By material, recycled fibers captured 62.91% of the Nigeria containerboard market share in 2025.

- By product type, the Nigeria containerboard market size for the kraftliners segment is forecast to advance at a 5.84% CAGR through 2031.

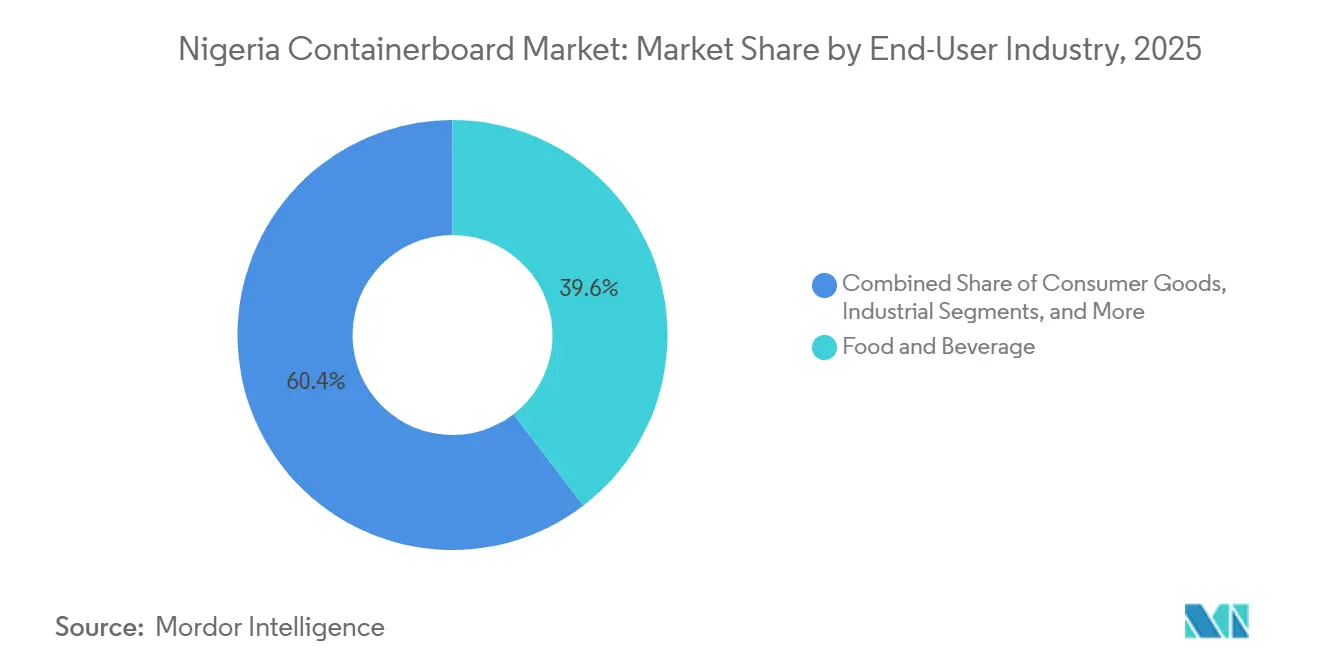

- By end-user industry, food and beverage captured 39.58% of the Nigeria containerboard market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Nigeria Containerboard Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand From Food And Beverage Packaging | +1.5% | National, with highest concentration in Lagos, Kano, and Ogun industrial belts | Short term (≤ 2 years) |

| E-Commerce And Omnichannel Parcel Expansion | +1.1% | Lagos, Abuja, and secondary cities including Port Harcourt and Ibadan | Short term (≤ 2 years) |

| Growth In Consumer Goods Distribution And Modern Retail | +0.9% | National, with spillover to the Southeast corridor including Enugu and Onitsha | Medium term (2-4 years) |

| AfCFTA-Led Need For Stronger Transit Packaging | +0.5% | National, with early gains along Lagos and border-trade corridors | Medium term (2-4 years) |

| Import Substitution Through Local Kraft And Corrugation Capacity Additions | +0.4% | Ogun State and Lagos State | Long term (≥ 4 years) |

| Traceability And Quality Compliance In Agro-Export Corrugated Packaging | +0.3% | National, with concentration in agro-export hubs such as Borno, Kaduna, and Cross River | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand From Food And Beverage Packaging

Food and beverage packaging remains the strongest recurring demand stream in the Nigerian containerboard market because breweries, packaged-water producers, edible-oil bottlers, and snack manufacturers need dependable corrugated outer cartons for daily distribution volumes.[1]National Agency for Food and Drug Administration and Control, “Current Good Manufacturing Practice Guidelines for Food and Food Products 2025-2030,” NAFDAC, nafdac.gov.ng NAFDAC's cGMP guidelines for 2025-2030 require sourcing traceable, food-safe packaging materials, raising the compliance floor for formal processors and favoring converters that can document board quality consistently. That requirement is changing purchasing behavior because brand owners are placing more value on verified material quality than on the lowest available box price. Smaller converters that cannot provide validated board grades are therefore losing formal supply contracts, while larger operators with traceability systems and stable test performance are gaining share in better-regulated accounts. The same compliance environment also helps the Nigerian containerboard market hold up during periods of weaker household spending because food, beverage, and basic consumer staples still move through regulated logistics channels.[2]United States Department of Agriculture Foreign Agricultural Service, “FAIRS Country Report Annual, Lagos, Nigeria,” USDA FAS, apps.fas.usda.gov Demand is also broadening because pharmaceutical and personal-care products are increasingly shipped in corrugated secondary trays that share similar packaging control requirements with food categories

E-Commerce And Omnichannel Parcel Expansion

E-commerce is strengthening the Nigerian containerboard market because parcel volumes are rising across both major cities and smaller distribution corridors that require sturdier outer cartons.[3]Jumia Technologies, “Jumia Reports First Quarter 2026 Results,” Jumia Investor Relations, investor.jumia.com Jumia Nigeria reported a 42% year-on-year increase in physical goods GMV in Q1 2026, while physical goods orders reached 5.9 million, and 62% of those orders came from secondary cities and rural communities. That geographic spread matters because parcels shipped over longer, less predictable road routes often require stronger boards, tighter edge crush performance, and more reliable box construction. Jumia's internally managed logistics arm, launched in May 2025, is also pushing fulfillment processes toward more standardized carton handling and outer-pack specifications, which support demand for certified grades rather than low-cost commodity stock. The Nigerian containerboard market also benefits from the fact that e-commerce packaging in the country still faces more transport stress than in mature logistics systems, so volume growth translates into a stronger pull for reinforced corrugated packaging. As more online demand originates outside Lagos, converters with dependable board quality and wider delivery reach are likely to capture a larger part of this expanding shipment base.

Growth In Consumer Goods Distribution And Modern Retail

Consumer goods distribution is driving quality demand in the Nigerian containerboard market because organized retail and direct-to-store delivery models require more presentable, consistent, and shelf-ready corrugated packaging. Chain retail formats and formal FMCG channels are creating space for shelf-ready trays and display-ready cases that carry more value than standard bulk cartons. The shift is not only about appearance, since household chemicals and personal-care products often require a heavier-gauge board that can preserve stacking stability on long truck routes. BusinessDay NG cited an industry estimate placing Nigeria's packaging sector at USD 2.5 billion and noted annual growth of 5%, which supports the view that premium-format demand is widening across corrugated packaging applications. This matters for the Nigerian containerboard market because modern retail procurement usually rewards print quality, dimensional consistency, and moisture resistance, rather than only low board cost. As local sourcing deepens, converters that can supply display formats and durable transit-ready cartons are better placed to move beyond volume competition and into higher-value accounts

AfCFTA-Led Need For Stronger Transit Packaging

AfCFTA is increasing demand for stronger board grades because export shipments from Nigeria must meet packaging and labeling standards that are more demanding than many domestic logistics requirements.[4]Federal Ministry of Information and National Orientation, “Nigeria Strengthens Trade Leadership With Launch Of AfCFTA Market Intelligence Tool And Uganda Airlines Partnership,” Federal Ministry of Information and National Orientation, fmino.gov.ng In May 2025, the Federal Ministry of Industry, Trade, and Investment and UNDP launched a Market Access Tool for 13 African markets, and the program directly addressed packaging compliance as a requirement for Nigerian MSMEs seeking cross-border trade. The same month also saw the launch of Nigeria's first intra-African air cargo corridor with Uganda Airlines, which reduced delivery times from 90 days to under a week and lowered logistics costs by up to 75%, making export-compliant corrugated packaging more commercially relevant for time-sensitive goods. SMEDAN's packaging and branding training in Lagos showed that smaller exporters still need support in meeting AfCFTA packaging requirements, confirming that stronger, more compliant board formats are becoming part of export readiness rather than an optional upgrade. Digital customs integration also reinforces that direction, as the SIGMAT Connectivity platform between Nigeria and Benin underscores the need for machine-readable, traceable packaging across trade corridors. For the Nigerian containerboard market, this means that export growth not only raises box volumes, but it also shifts buyers toward better-performing liner and fluting combinations that can survive longer transit and stricter border scrutiny.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Imported Fiber, Linerboard, And Machinery Cost Inflation | -1.4% | National, most severe at Lagos port-proximate mills | Short term (≤ 2 years) |

| Unreliable Power And High Diesel Dependence | -1.1% | National, most acute in industrial belts of Ogun, Lagos, and Kano | Short term (≤ 2 years) |

| Apapa Port Dwell Time And Inland Trucking Friction | -0.7% | Lagos Metropolitan Area and inland distribution routes | Medium term (2-4 years) |

| Waste Paper Collection And Sorting Gaps Limiting Recycled-Fiber Quality | -0.5% | National, with highest severity in cities lacking formal waste management systems | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Imported Fiber, Linerboard, And Machinery Cost Inflation

Imported input inflation remains a major brake on the Nigerian containerboard market because converters still rely on foreign linerboard, fluting inputs, and replacement parts for aging equipment bases. Industry reports stated that Nigeria's paper import bill increased from NGN 328.9 billion (USD 0.22 billion) in 2021 to NGN 1.11 trillion (USD 0.00076 trillion) in 2025, indicating how quickly external cost dependence has intensified. Naira depreciation since mid-2023 has made the situation harder, as every imported reel, roll, and machine component now carries a higher local-currency burden before inland logistics costs are added. The Federal Government's May 2026 review of fiscal barriers to paper mill inputs signals that policymakers now recognize the problem, and the initiative aims to achieve NGN 250 billion (USD 151.5 million) in annual savings. The Nigerian containerboard market will still face delayed relief because older corrugators and paper lines need imported modernization parts, and those purchases remain exposed to both currency pressure and longer procurement cycles. This cost structure gives a clear advantage to integrated players with better access to working capital, while smaller converters remain more exposed to volatile landed input prices.

Unreliable Power And High Diesel Dependence

Power instability is another structural limit on the Nigerian containerboard market, as corrugators, die-cutters, and printing lines require steady electricity for alignment, print registration, and production continuity. MAN reported that manufacturers spent NGN 1.11 trillion (USD 672.7 million) on alternative energy in 2024, rising to NGN 1.5 trillion (USD 909.1 million) in 2025. The national grid collapsed 12 times in 2024, and by H1 2025, the manufacturing sector had already spent NGN 676.6 billion (USD 410.1 million) at 2025 average exchange rates, on generator and alternative energy costs. Some manufacturers cited monthly diesel spending rising from NGN 30 million (USD 18,200) to NGN 45 million (USD 27,300) - NGN 50 million (USD 30,300), underscoring how difficult it is to protect margins in a price-sensitive corrugated business. These cost pressures matter more in Nigeria than in better-supplied power markets because energy is not a temporary surcharge; it is now embedded in day-to-day conversion economics. The result is that larger diversified groups can absorb volatility more easily, while smaller mills and converters face tighter operating limits and slower reinvestment cycles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Recycled-Fiber Mills Anchor Supply, Virgin Grades Gain Ground

Recycled fibers held 62.91% of the Nigeria containerboard market share in 2025, making them the clear base material for domestic supply. This leadership reflects the cost advantage of waste-paper-fed production and the fact that recycled-fiber capacity requires less capital than greenfield virgin-pulp projects. Specialty Pulp and Paper Limited produces corrugating medium, testliner, and white-top testliner at its Ogun State facility and sources recovered paper locally while also supplementing with imported waste paper from North America and the Bahamas. That sourcing model shows why recycled grades remain firmly established in the Nigerian containerboard industry, because local converters can build around available recovered fiber while using imports only to balance quality or volume gaps. It also explains why many investors still favor recycled lines when expanding capacity, since these projects can be commissioned more quickly than large virgin-fiber ventures in markets with power and water constraints. Compliance requirements are also becoming more important in this segment, as NAFDAC's 2025-2030 cGMP framework requires traceable sourcing of packaging materials for food processors. That does not remove recycled fiber's cost advantage, but it does raise expectations on documentation, process control, and consistent board performance. As a result, recycled-fiber producers that can pair low-cost sourcing with traceability are likely to hold the strongest positions across mainstream packaging demand. The Nigeria containerboard market therefore remains anchored in recycled material economics even as buyers demand better verification and tighter performance standards.

Virgin fibers are projected to grow at a 5.71% CAGR through 2031, which makes them the faster-moving material category within the Nigeria containerboard market size outlook. This faster growth reflects rising demand for stronger kraftliners and industrial transport boards used in export-facing supply chains. Multinational FMCG buyers and AfCFTA-linked shippers are asking for board constructions that can meet higher burst-strength and box-compression standards, and recycled grades do not always deliver the same consistency for those applications. Nigeria also has untapped agricultural fiber options such as bamboo, kenaf, and sugarcane bagasse, but the economics for domestic virgin-pulp development remain difficult under current import-cost and infrastructure conditions. Vanguard News reported in April 2026 that local paper mills lose NGN 674 billion (USD 408.5 million) annually, to foreign producers, which highlights how far domestic paper capacity still sits below national demand. That gap gives virgin-fiber investment a strategic importance beyond ordinary product diversification because it touches industrial policy, import substitution, and export readiness at the same time. The Nigeria containerboard industry is therefore likely to keep recycled fiber as its volume base while using virgin-grade investments to serve higher-specification packaging needs. If duty reforms and input-cost relief move ahead, virgin capacity will become more commercially viable for a broader group of operators. Until then, growth in virgin fibers will come mainly from targeted investments linked to premium corrugated use cases rather than wide market conversion.

By Product Type: Testliners Lead Volume, Kraftliners Accelerate

Testliners commanded 42.15% of the market in 2025, giving them the broadest product footprint across everyday corrugated applications. Their position reflects steady use in beverages, detergents, packaged food, and other consumer goods where domestic logistics, not export standards, still define most box specifications. In that sense, testliners continue to hold the floor of the Nigeria containerboard market because they meet a wide range of local distribution needs at manageable cost. Broad installed familiarity also supports this segment, since many local mills and converters are already configured around testliner and fluting combinations rather than premium virgin-facing constructions. That installed base matters because it reduces the switching burden for converters serving high-volume domestic customers who value continuity and price discipline. Demand for testliner remains linked to industrial and consumer staples shipments that move every day through Nigeria's wholesale and retail channels. Even as quality expectations rise, this product still benefits from the large share of use cases where export-grade strength is not essential. The Nigeria containerboard market size for testliner therefore remains tied to routine logistics demand, recurring FMCG shipments, and the practical need for affordable corrugated packaging across formal and informal trade. That keeps testliner central to volume throughput even as newer specifications gain attention. The segment should remain widely used because it offers a workable balance between performance and cost for mainstream corrugated applications.

Kraftliners are forecast to grow at 5.84% CAGR during 2026-2031, the fastest pace among product types in the Nigeria containerboard market. This growth is tied to export-oriented packaging demand, where stronger outer facings and better-certified performance are becoming more important. Domestic mills that historically focused on testliner and fluting are now upgrading, or planning to upgrade, their forming sections toward multi-ply kraftliner production as import substitution becomes more commercially attractive. AfCFTA trade routes and the Uganda Airlines air cargo corridor are pushing breweries, edible-oil exporters, and other Nigerian shippers toward stronger master-case constructions that can handle longer-distance movement and stricter compliance checks. That change expands revenue per board meter because the value of a kraftliner-facing box is higher than that of a standard testliner construction. Fluting also remains important within the product mix, and Speciality Group states that its integrated operation includes fluting media as well as a cassava starch business that supports its packaging chain. The group's 18,000-tonne-per-annum cassava starch operation reduces imported chemical dependence and supports supply-chain localization around corrugated production. This form of backward integration does not change the leadership of testliners, but it does show how local players can improve margins and reduce input exposure around growing higher-value grades. The Nigeria containerboard market is therefore moving toward a two-track product structure where testliners remain the volume base and kraftliners capture a rising share of premium demand. Over time, the mills that can certify stronger grades and localize more inputs should see the greatest benefit from this shift.

By End-User Industry: Food And Beverage Holds The Floor, Consumer Goods Accelerates

Food and beverage accounted for 39.58% of the market in 2025, making it the largest end-user segment for corrugated demand. This share reflects Nigeria's position as the main food manufacturing center in West Africa and the routine need for secondary packaging across breweries, bottled water, edible oils, snacks, and processed staples. In practical terms, this segment provides the Nigerian containerboard market with its most dependable volume stream, as logistics compliance, not discretionary consumption alone, drives a large part of carton usage. Food processors need traceable, safe, and transport-ready packaging, and those requirements create recurring offtake agreements for corrugated converters. Breweries and packaged-water operators also ship high volumes on demanding road networks, so they rely on sturdy outer cartons that can protect product integrity in transit. The result is a demand floor that is more stable than many other manufacturing-linked packaging categories. Nigeria Export Promotion Council-linked packaging and labeling capacity-building is also raising quality expectations for food-related exporters, gradually shifting procurement from simple price checks to verified board performance. That change strengthens the premium end of food-related corrugated demand without weakening the large base of everyday carton consumption. The Nigerian containerboard market continues to lean on this segment because it combines scale, compliance, and frequency better than any other end-user group. As long as formal food production expands and distribution networks deepen, food and beverages will remain the core stabilizer for corrugated demand.

Consumer goods are projected to grow at a 5.93% CAGR during 2026-2031, making it the fastest-growing end-user category. The main reasons are the formalization of retail distribution and the preference for locally sourced secondary packaging that supports both presentation and transport performance. Personal-care and household-chemical lines are contributing to this growth because they often require moisture-resistant and heavier-gauge double-wall board to maintain stack integrity during inland movement. Industrial end users also continue to represent an important volume block through building materials, chemicals, and spare parts packaging, especially where heavier-duty corrugated construction can replace less efficient packaging formats. Other industries, such as pharmaceuticals, personal care, and agro-exporters, remain smaller in share, but they are among the quickest adopters of premium board constructions due to stricter compliance and handling requirements. This pattern matters for the Nigerian containerboard market because premium adoption is not limited to one vertical; it is spreading across multiple specialized uses. The segment mix is therefore becoming more value-sensitive, with faster growth coming from customers that need better print control, stronger boxes, and more traceable packaging materials. That broadens the addressable market for converters that can serve different specification tiers, rather than only commodity grades. The Nigerian containerboard market is not moving away from staple end users, but is adding premium demand from diversified customer categories. This makes end-user growth more balanced and supports better monetization even if total board volumes rise at a measured pace.

Geography Analysis

Nigeria accounted for 70% of ECOWAS corrugated packaging consumption by volume at 1.2 million tons, which underlines the country's dominant role in the regional corrugated trade base. That regional weight gives the Nigerian containerboard market a scale advantage because the country combines large consumer demand with a deep manufacturing footprint. Lagos State and neighboring Ogun State remain the core production and consumption corridor, and they host many of the largest corrugated converting facilities and major inflows of imported linerboard through Apapa and Tin Can Island ports. Abuja and Port Harcourt act as secondary demand centers, supported by consumer goods flows, industrial activity, and formal retail distribution. Kano and Kaduna also contribute through agro-processing, textile-related movement, and northern trade routes that rely on corrugated secondary packaging. Nigeria's per-capita containerboard consumption remains below the African continental average, leaving room for expansion as FMCG distribution moves further into smaller cities and rural markets. This means the Nigerian containerboard market can continue growing without depending on a single structural break in industry economics.

Geographic concentration around Lagos also creates a supply-side weakness because much of the market's imported input flow still passes through one stressed logistics gateway. Reporting that cited SERAC showed cargo dwell time at Nigerian seaports averaging more than 15 days in Q1 2026, compared with a global benchmark of 3-5 days, while vessel turnaround time ranged from 4-6 days. Those delays matter because imported linerboard shortages can move quickly from the port area into the broader converting tier when mills and converters are operating with limited buffers. Punch Newspapers also cited Dynanmar estimates of daily losses at NGN 20 billion (USD 12.1 million) which illustrates the scale of efficiency loss tied to port bottlenecks. For converters in southeastern corridors such as Onitsha and Enugu, the problem is magnified because feedstock still has to be moved inland from Lagos, adding cost and time before production even starts.

Longer term, geography could become more balanced if newer logistics assets and cross-border trade systems work as intended. The Lekki Deep Sea Port offers a path toward spreading cargo flows beyond Apapa, which could gradually reduce the concentration risk built into the current import chain. Nigeria's first intra-African air cargo corridor with Uganda Airlines also improves the case for export-ready corrugated packaging by shortening delivery windows and making compliant packaging more commercially meaningful for regional trade. The SIGMAT Connectivity platform between Nigeria and Benin supports this direction because machine-readable and traceable packaging becomes more valuable when customs systems are becoming more digital. International packaging interest is also rising, with companies such as Mpact Group Limited linked to the Nigerian context and Interpack identifying Nigeria as a key African demand center for new packaging equipment. The Nigeria containerboard market is therefore becoming more than a domestic consumption story, because investors increasingly view it as a production and logistics base for West and Central Africa. If logistics diversification improves, the geographic risk profile of the market will become more manageable and support broader capacity utilization across the country.

Competitive Landscape

The Nigeria containerboard market remains fragmented at the converting level, with many small and mid-size box plants operating alongside a small group of more integrated producers. Specialty Pulp and Paper Limited is one of the clearest examples of integration, and the company states that its Ogun State facility produces corrugating medium, testliner, white-top testliner, kraft liner, and fluting media. That breadth matters because integrated players can control more of the cost chain and reduce their exposure to imported boards purchased on the open market. The company has also linked its corrugated operations to a cassava starch business, which helps reduce its dependence on imported chemicals and provides a more localized supply structure. In July 2024, Specialty Group commissioned its white paper manufacturing plant, further strengthening its position as an integrated paper producer, with brown-paper and corrugated carton operations already in place. Moves like that show that scale in the Nigerian containerboard market is increasingly tied to asset depth, input control, and the ability to supply multiple board grades from one operating base.

Another strategic pattern is the push toward import substitution and higher-grade local capacity. In May 2026, the Federal Government held a stakeholders' roundtable with Specialty Group and Nixin Paper Mill Nigeria to review fiscal barriers and to discuss targeted input duty relief for the paper mill sector. That discussion matters because Nixin and Specialty together represent a visible local manufacturing base that could improve utilization if cost conditions become more favorable. Vanguard News also reported in April 2026 that the combined 140,000-tonne annual capacity of Nixin and Specialty could meet a meaningful share of national demand if operated at higher levels. International companies such as Mondi plc and Mpact Group Limited add another layer of competition by bringing certified production standards, broader sourcing networks, and stronger compliance systems into customer conversations. In the Nigerian containerboard market, this raises the competitive bar for exporters and multinational buyers who care about packaging documentation as much as they do about physical board supply. Smaller converters such as Veepee Industries Limited and Quantum Paper Limited remain relevant because they can offer localized service and faster turnaround, but they face clear limits when formal customers ask for validated board certification and repeatable print quality.

Compliance and technology are now shaping rivalry as much as installed capacity. Export-oriented buyers increasingly prefer converters that can support traceability, testing, and stable performance in line with SON and food-related packaging requirements. That trend favors better-capitalized suppliers and could gradually shift the Nigerian containerboard market toward fewer serious bidders for regulated supply contracts. White-space demand remains visible in printed retail display boxes, moisture-barrier-treated board for agro-export routes, and precision-die-cut pharmaceutical secondary cartons because domestic supply still trails buyer requirements in these categories. Technology-enabled packaging platforms are also starting to compete at the margins by offering digital procurement and short-run, customized printing without large minimum order quantities. This model does not yet change the structure of the whole market, but it does make responsiveness and customization more important for selected customer groups. Over time, the Nigerian containerboard market is likely to remain fragmented in terms of count, but less fragmented in quality tiers, with a stronger separation between certified suppliers and purely commodity converters. That is why commercial advantage is shifting away from simple volume presence and toward integration, documentation, and the ability to deliver premium corrugated formats with fewer supply interruptions.

Nigeria Containerboard Industry Leaders

Speciality Pulp and Paper Limited

Veepee Industries Limited

Quantum Paper Limited

Good One Carton Nigeria Co., Ltd.

Onward Paper Mill Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: The Federal Government of Nigeria initiated a review of fiscal barriers for the paper mill sector, including targeted import duty cuts on manufacturing inputs, following a stakeholders' roundtable convened by the Ministry of Industry, Trade and Investment with Speciality Group and Nixin Paper Mill Nigeria. The initiative targets NGN 250 billion (USD 151.5 million) in annual savings and has the potential to materially lower input costs for containerboard manufacturers if implemented within the anticipated 12 to 18 months, per Vanguard News.

- April 2026: Vanguard News reported that local paper mills collectively lose NGN 674 billion (USD 408.5 million) annually to foreign producers, with domestic production capacity far below the national demand for paper and board grades. The combined 140,000-tonne annual capacity of Nixin and Speciality Group could potentially satisfy a significant portion of national demand if operated at full utilization, signaling the import-substitution potential awaiting policy and infrastructure support.

- May 2025: The Federal Ministry of Industry, Trade and Investment and the United Nations Development Programme jointly launched a Market Access Tool covering packaging compliance standards for Nigerian MSMEs across 13 African markets, alongside Nigeria's first intra-African air cargo corridor operated by Uganda Airlines. The corridor reduced delivery times from 90 days to under a week and slashed logistics costs by up to 75%, creating new economics for corrugated export packaging, per the Federal Ministry of Information and National Orientation.

- May 2025: SMEDAN launched a dedicated packaging and branding training program in Lagos, equipping NMSMEs with AfCFTA export packaging requirements and internationally compliant corrugated outer-box specifications, per SMEDAN and MSME Africa reporting. The program formed part of a broader government strategy to close Nigeria's agro-export packaging compliance gap.

Nigeria Containerboard Market Report Scope

The Nigeria Containerboard Market encompasses the production, distribution, and consumption of containerboard materials used in manufacturing corrugated packaging solutions. It includes containerboard made from virgin and recycled fibers, covering key product types such as kraftliners, testliners, and flutings. These materials are primarily used in protective and transport packaging applications across various end-user industries, including food and beverage, consumer goods, industrial, pharmaceuticals, and agriculture. The market is driven by the increasing demand for sustainable, lightweight, and durable packaging solutions.

The Nigeria Containerboard Market Report is Segmented by Material (Virgin Fibers, and Recycled Fibers), Product Type (Kraftliners, Testliners, and Flutings), and End-User Industry (Food and Beverage, Consumer Goods, Industrial, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Virgin Fibers |

| Recycled Fibers |

| Kraftliners |

| Testliners |

| Flutings |

| Food and Beverage |

| Consumer Goods |

| Industrial |

| Other End-User Industries |

| By Material | Virgin Fibers |

| Recycled Fibers | |

| By Product Type | Kraftliners |

| Testliners | |

| Flutings | |

| By End-User Industry | Food and Beverage |

| Consumer Goods | |

| Industrial | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the size outlook for the Nigeria containerboard market?

The Nigeria containerboard market was valued at USD 164.31 million in 2025, is estimated at USD 175.71 million in 2026, and is projected to reach USD 227.41 million by 2031 at a 5.29% CAGR.

Which material type currently leads containerboard demand in Nigeria?

Recycled fibers led with a 62.91% share in 2025, supported by domestic waste-paper feedstock and lower capital requirements than virgin-pulp projects.

Which product type is expanding the fastest through 2031?

Kraftliners are projected to grow at a 5.84% CAGR through 2031 because export packaging and stronger transit-performance requirements are lifting demand for higher-grade board.

Why does food and beverage remain the biggest end-user base?

Food and beverage held 39.58% of demand in 2025 because breweries, edible-oil processors, packaged-water companies, and snack manufacturers rely on recurring corrugated secondary packaging.

How is e-commerce changing corrugated box demand in Nigeria?

Q1 2026 order growth at Jumia, especially from secondary cities and rural communities, is increasing the need for stronger parcel cartons that can handle longer and rougher transport routes.

What are the main risks for suppliers and converters?

Imported input inflation, grid instability, diesel dependence, and port congestion remain the biggest risks because they raise board conversion costs and can interrupt linerboard availability.

Page last updated on: