Neocloud Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

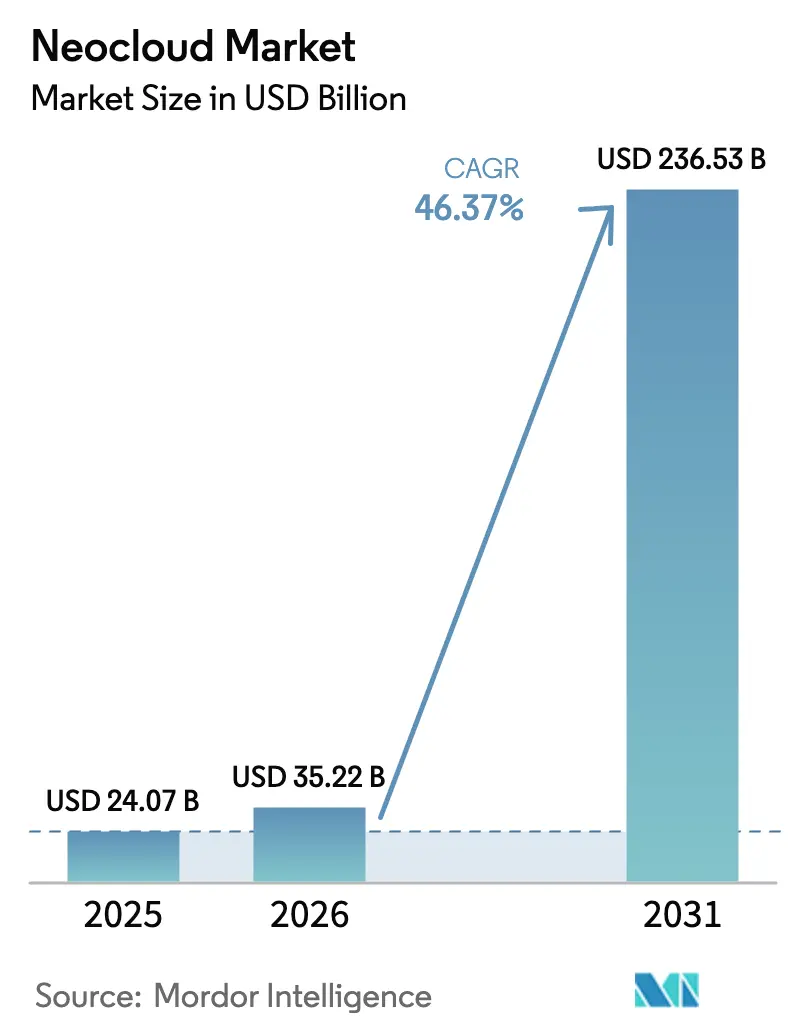

| Market Size (2026) | USD 35.22 Billion |

| Market Size (2031) | USD 236.53 Billion |

| Growth Rate (2026 - 2031) | 46.37% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Neocloud Market Analysis by Mordor Intelligence

The neocloud market size in 2026 is estimated at USD 35.22 billion, growing from 2025 value of USD 24.07 billion with 2031 projections showing USD 236.53 billion, growing at 46.37% CAGR over 2026-2031. Enterprises are shifting workloads away from broad hyperscaler estates toward purpose-built platforms tuned for AI inference, edge latency, and sovereign-data controls. These providers deploy disaggregated compute, GPU-optimized networking, and carbon-aware schedulers that cut energy use 30-50% relative to conventional clouds. The result is a rapidly widening addressable base spanning manufacturing automation, healthcare analytics, and data-regulated public services. Regional demand remains strongest in North America, yet Asia Pacific now delivers the steepest growth curve as 5G and industrial digitalization converge with protective data policies. Moderately concentrated competition allows nimble specialists, such as CoreWeave, Lambda Labs, and Nebius, to raise multi-hundred-million-dollar rounds to build out GPU-optimized capacity that traditional providers cannot easily duplicate.

Key Report Takeaways

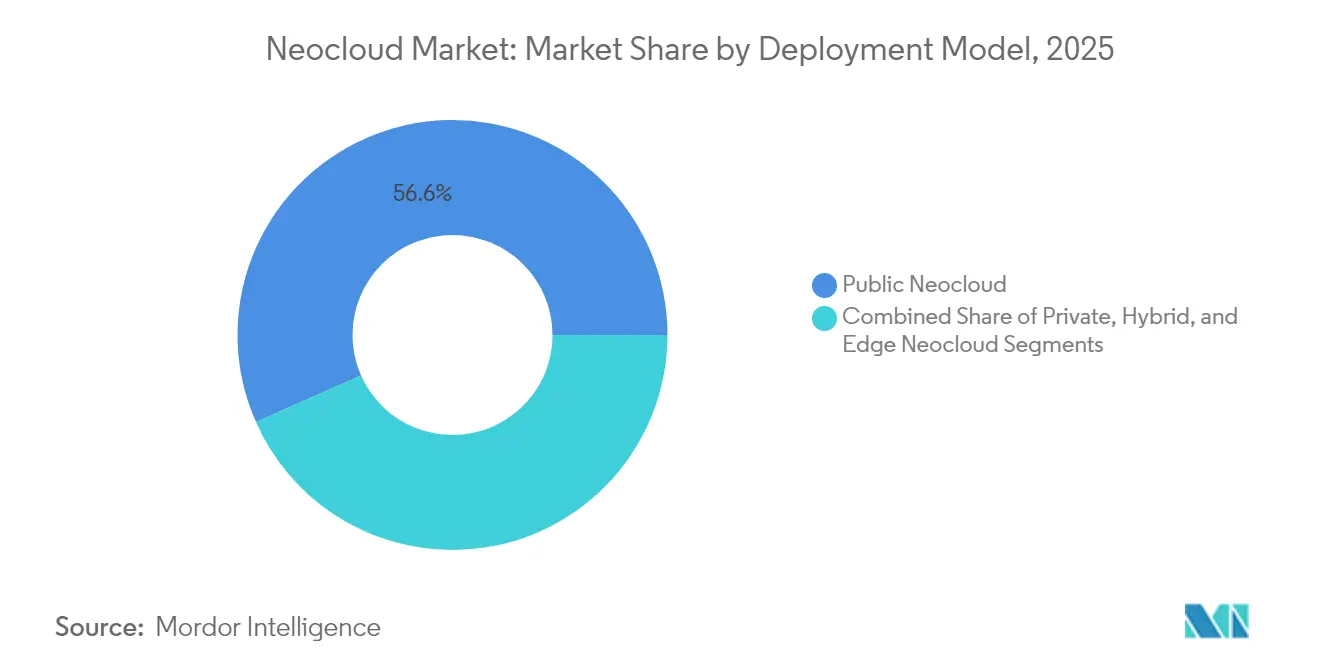

- By deployment model, public infrastructure held 56.64% of the neocloud market share in 2025, while the edge segment is forecast to accelerate at a 67.72% CAGR through 2031.

- By service type, Infrastructure as Code and DevOps enablement led with 35.62% revenue share in 2025, while the same category is projected to expand at a 52.62% CAGR through 2031.

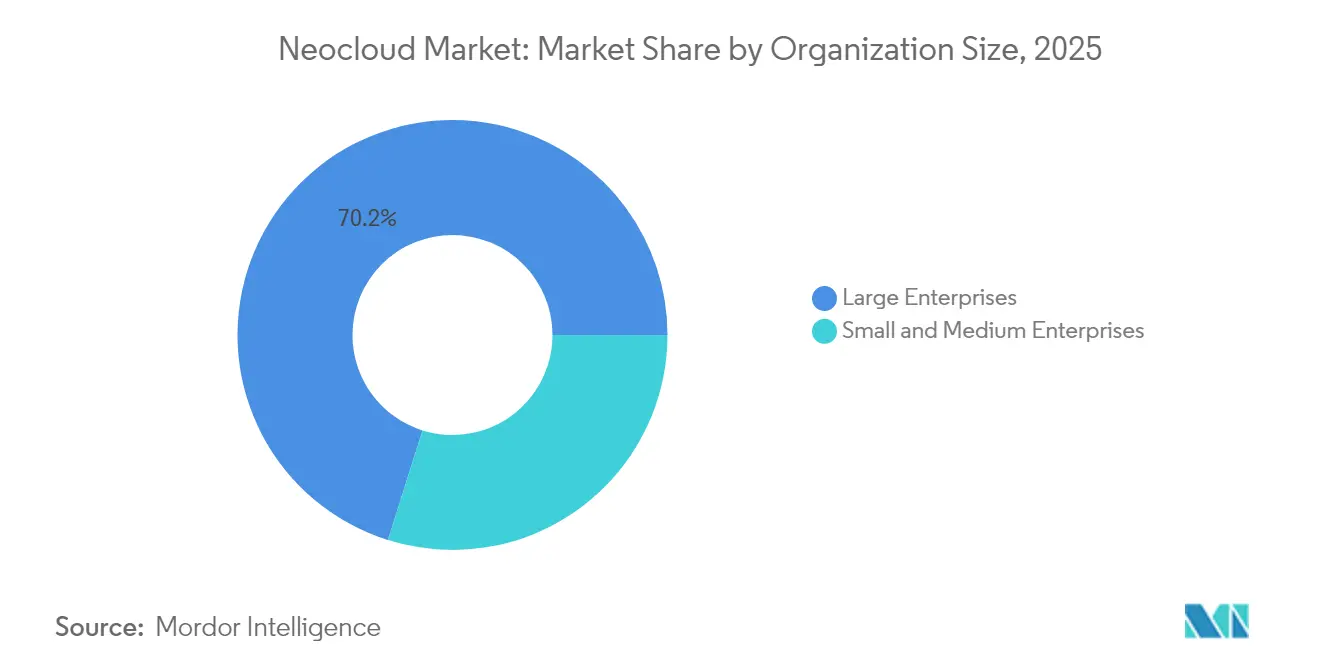

- By organization size, large enterprises accounted for 70.15% of the neocloud market size in 2025, whereas small and medium enterprises are expected to advance at a 48.83% CAGR through 2031.

- By end-user industry, information technology and telecom captured 26.98% share of the neocloud market size in 2025, but healthcare and life sciences is on track for a 55.09% CAGR to 2031.

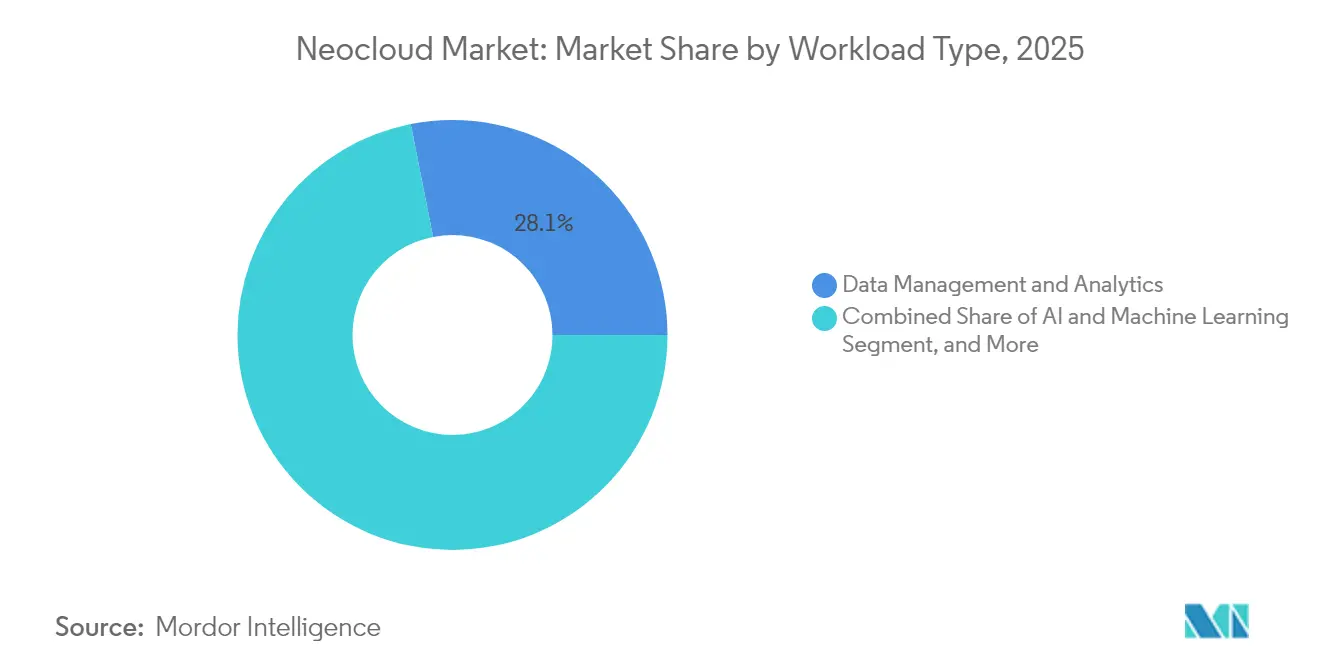

- By workload type, data management and analytics accounted for 28.11% of the neocloud market size in 2025, and AI and machine learning workloads are projected to grow at a 63.95% CAGR between 2026 and 2031.

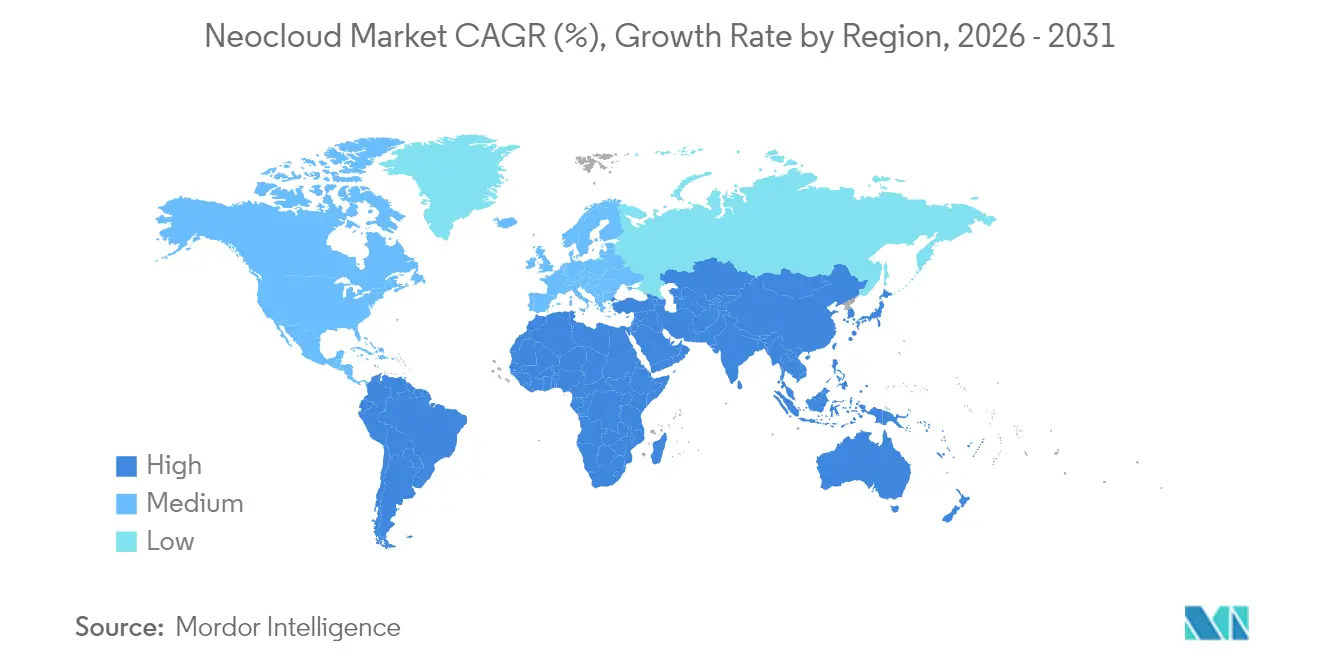

- By geography, North America maintained 41.22% neocloud market share in 2025, while the Asia Pacific is forecast to post a 54.5% CAGR during the same horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Neocloud Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Edge-centric Workload Proliferation | +11.8% | Global, early gains in North America and Asia Pacific | Medium term (2-4 years) |

| Sovereign-Cloud Compliance Mandates | +8.2% | Europe and Asia Pacific core, spill-over to Americas | Long term (≥ 4 years) |

| AI-native DevOps Toolchain Adoption | +12.7% | Global | Short term (≤ 2 years) |

| Carbon-aware Cloud Orchestration | +6.3% | Europe and North America, expanding to Asia Pacific | Medium term (2-4 years) |

| Disaggregated Compute and Storage Architectures | +7.1% | Global, concentration in North America | Medium term (2-4 years) |

| Open-source FinOps Acceleration | +5.4% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Edge-centric Workload Proliferation

Latency-sensitive applications now require sub-10 millisecond response times that centralized data centers cannot guarantee. Manufacturers are deploying edge-based quality-control systems, and healthcare providers are rolling out near-patient inference to comply with privacy rules, generating USD 2.3 billion in incremental spend each year. Edge installations are climbing at a 71.28% CAGR, far outstripping centralized alternatives, and Kubernetes extensions such as KubeEdge lower bandwidth costs by as much as 60% while sustaining performance.[1]ACM Editors, “Edge Computing Orchestration: A Comprehensive Survey,” ACM Digital Library, dl.acm.org Telecom operators integrate edge neocloud nodes into 5G base stations so ultra-reliable low-latency communication applications stay within 20 kilometers of end users. This driver delivers the strongest uplift to the neocloud market by creating new buying centers outside traditional information technology departments.

Sovereign-Cloud Compliance Mandates

Data-residency statutes arising from Europe’s Digital Services Act and analogous Asia Pacific rules compel enterprises to localize processing, spurring demand for AI neocloud platforms with granular sovereignty controls. European firms now budget 23% more for compliant infrastructure than for standard cloud services, helping domestic specialists seize share from global hyperscalers.[2]European Commission, “Digital Services Act Package: Ensuring Safe and Accountable Online Environment,” European Commission, digital-strategy.ec.europa.eu Financial institutions must confine transactional data within national borders, and government IT agencies across 47 nations have forbidden foreign processing for critical workloads, thereby ring-fencing USD 8.2 billion in addressable opportunity through 2030. While the policy outlook is long-term, buyers are already moving workloads to sovereign neocloud regions, accelerating market expansion.

AI-native DevOps Toolchain Adoption

Development teams are embedding artificial intelligence directly into CI/CD pipelines, sparking demand for Infrastructure as Code frameworks that automate provisioning and configuration across multi-cloud estates. GitLab shows 89% of organizations plan AI-enabled DevOps by 2026, pushing workloads onto programmable APIs that classic clouds struggle to streamline.[3]GitLab Research, “Global Developer Survey: AI-Enhanced DevOps Adoption Trends,” GitLab, about.gitlab.com Neocloud vendors now ship turnkey DevOps stacks-complete with testing harnesses, continuous deployment pipes, and audited templates-that slash release cycles 70% versus manual builds. Kubeflow and MLflow marry with these IaC scripts so data scientists deploy models from version-controlled manifests rather than hand-tuned servers. Compliance mandates under the EU AI Act further reinforce this motion, as automated policy scans baked into IaC files ensure each environment stays secure and explainable at scale.

Carbon-aware Cloud Orchestration

Corporate sustainability commitments are driving customers to shift workloads to regions rich in renewables during peak generation windows. Research from Carnegie Mellon University shows carbon-aware schedulers can slash data center energy use by as much as 50%. Neocloud providers embed real-time carbon telemetry into resource managers, a level of visibility still emerging at most hyperscalers, and European buyers are increasingly making procurement decisions contingent on ISO 14001 alignment. As emissions-reporting regulations tighten, carbon-optimized scheduling becomes a competitive differentiator and an incremental growth lever for the neocloud market, particularly in mid-term horizons.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating Cross-border Data Localization Costs | -3.2% | Europe and Asia Pacific core, spill-over to Americas | Long term (≥ 4 years) |

| Supply-chain Volatility in Advanced Node Chips | -4.1% | Global | Medium term (2-4 years) |

| Multi-cloud Talent Scarcity | -2.8% | Global, acute in North America and Europe | Long term (≥ 4 years) |

| Rising Green-datacenter CAPEX Burden | -2.3% | Europe and North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating Cross-border Data Localization Costs

Seventy-three nations now impose data-localization clauses that raise operating expenses 15-25% versus globally distributed architectures. Brazil’s General Data Protection Law and India’s Personal Data Protection Bill compel providers to build local facilities, eroding economies of scale.[4]Reuters Staff, “Brazil Data Protection Authority Fines Temu 3 Million Reais,” Reuters, reuters.com Legal reviews of Standard Contractual Clauses add as many as 60 days to project timelines, denting the neocloud market’s agility advantage. Small providers lacking in-house counsel must divert scarce funds toward compliance, reducing capital available for innovation and slowing adoption in cost-sensitive verticals.

Supply-chain Volatility in Advanced Node Chips

GPU and AI-accelerator shortages persist as semiconductor foundries prioritize consumer electronics over data-center volumes. Delivery of high-bandwidth-memory packages now trails demand by 12-18 months, constraining 40% of planned neocloud deployments. Export controls add further friction for cross-border hardware sourcing. Providers re-architect around available parts instead of best-fit devices, compromising performance and postponing service launches that could otherwise widen the neocloud market footprint in the medium term

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Edge Infrastructure Drives Specialized Computing Demand

Public platforms controlled 56.64% of the neocloud market share in 2025, as enterprises sought turnkey AI infrastructure without incurring capital outlays. Edge installations, however, represent the fastest-growing slice, sprinting at a 67.72% CAGR through 2031. This pattern underscores how the neocloud market size continues to migrate toward latency-dependent use cases in manufacturing automation, autonomous mobility, and real-time analytics. Private deployments remain vital in financial services and healthcare, where dedicated hardware simplifies compliance, while hybrid topologies give enterprises flexible workload placement and cost optimization.

Telecom carriers extend distributed compute nodes to cell-tower shelters to enable 5G network slicing and augmented reality services, narrowing the round-trip latency well below the 10-millisecond mark. Standardization under ETSI Multi-access Edge Computing and 3GPP guidelines legitimizes such roll-outs and further pulls workloads from centralized metros into edge territories. The resulting diversification of demand cements edge infrastructure as the premier growth engine inside the broader neocloud market.

By Service Type: DevOps Automation Drives Infrastructure Programmability Adoption

Infrastructure as Code and DevOps enablement captured 35.62% of the neocloud market share in 2025 and is forecast to accelerate at a 52.62% CAGR through 2031. This dominance underscores how the neocloud market size increasingly mirrors enterprise craving for automated pipelines, declarative configurations, and zero-touch rollbacks. Platform-as-a-Service bundles AI toolchains for faster model iteration, while cloud-native infrastructure layers Kubernetes and microservices atop GPU pools to run distributed applications seamlessly.

Kubernetes, OpenShift, and Terraform now integrate natively with Neocloud APIs so developers orchestrate infrastructure from code instead of consoles. Regulatory frameworks such as FedRAMP and ISO 27001 amplify appeal because IaC templates embed policy controls that propagate from dev to prod without drift. The convergence of security, compliance, and speed cements DevOps automation as the defining growth engine within the service-type mix of the neocloud market.

By Organization Size: Enterprise AI Adoption Drives SME Infrastructure Democratization

Large enterprises captured 70.15% of the neocloud market share in 2025, owing to their substantial budgets and skilled staff capable of orchestrating complex hybrid estates. Nevertheless, small and medium enterprises are expanding at a 48.83% CAGR as simplified onboarding packages reduce technical friction. SaaS-like consoles, transparent usage pricing, and managed compliance artifacts enable SMEs to leverage the same GPU clusters once restricted to Fortune 500 firms.

The democratization trend also benefits from vendor-provided SOC 2 attestations and GDPR processing addenda, enabling resource-constrained businesses to satisfy regulators without establishing in-house security teams. As self-service portals and API-first architectures proliferate, the customer mix within the neocloud market broadens, limiting over-reliance on a few deep-pocketed buyers and improving revenue resiliency.

By End-user Industry: Healthcare AI Applications Drive Regulatory-Compliant Infrastructure Demand

Information technology and telecom led spending with a 26.98% share in 2025, primarily targeting network optimization and NFV workloads. The healthcare and life sciences sector is projected to be the growth pacesetter at a 55.09% CAGR, adopting neocloud platforms for AI-assisted drug discovery, medical imaging analytics, and remote monitoring that must meet HIPAA rules. Banking and insurance firms deploy real-time fraud detection pipelines on low-latency GPUs, while manufacturers lean on predictive maintenance analytics at edge sites to cut downtime.

Government agencies in 47 countries enforce sovereign-cloud requirements that lock sensitive workloads inside national borders, channeling demand toward regional providers. These verticalized compliance requirements incentivize vendors to specialize, further segmenting the neocloud market and creating defensible niches with higher margin profiles.

By Workload Type: AI and Machine Learning Applications Drive Infrastructure Specialization

Data management and analytics accounted for 28.11% of spending in 2025, yet AI and machine learning workloads are advancing at a 63.95% CAGR. The shift is driven by rising adoption of generative models, conversational interfaces, and computer vision pipelines for quality assurance. Such workloads thrive on GPU clusters with high-bandwidth memory and fast interconnects, assets that are the hallmark of the neocloud market.

Regulators are simultaneously rolling out AI governance blueprints mandating explainability and bias checks. These tasks introduce computationally expensive interpretability stages, effectively increasing infrastructure intensity per deployment. As the spectrum of AI use cases widens, the workload mix will further tilt toward specialized compute needs, reinforcing the strategic positioning of neocloud providers.

Geography Analysis

North America retained 41.22% neocloud market share in 2025, buoyed by USD 3.2 billion in venture inflows and a policy environment that privileges innovation over strict data-residency constraints. U.S. providers such as CoreWeave and Lambda Labs used abundant capital to build GPU fleets that entice enterprises seeking faster AI iteration cycles. Canada advanced sovereign-cloud initiatives for federal workloads, widening domestic opportunity while keeping private-sector policy relatively liberal. The region’s CAGR is projected at 42.61% through 2031, even as supply-chain bottlenecks throttle immediate hardware availability.

Asia Pacific is forecast to record a 54.5% CAGR, the fastest worldwide, as manufacturing automation, smart-city programs, and expansive 5G roll-outs generate unrelenting edge compute demand. China’s protected environment reserves a domestic share for local operators, which are already handling 34% of enterprise workloads in 2025. India attracts overseas providers with 40-60% lower data-center operating costs, while South Korea and Australia emphasize ultra-low-latency platforms for autonomous mobility and immersive media. Fragmented regulation nevertheless obliges market entrants to navigate a complex matrix of privacy statutes, sharpening the need for region-specific compliance playbooks.

Europe prioritizes sovereign cloud and sustainability. GDPR enforcement propels buyers toward providers that embed fine-grained data zoning and carbon-aware scheduling. Germany leans on Industry 4.0 initiatives, France channels public-sector workloads to homegrown platforms, and the United Kingdom crafts post-Brexit rules that still echo EU norms yet loosen cross-border controls for certain commercial data classes. Carbon-tracking standards such as EU Taxonomy and ISO 14001 grow influential, encouraging enterprises to weigh emissions ratings alongside cost and performance when selecting neocloud partners.

Competitive Landscape

Competition remains moderately concentrated as vertically integrated specialists scale infrastructure banks to rival hyperscalers on price-performance for AI tasks. CoreWeave’s USD 1.1 billion Series C at a USD 19 billion valuation exemplifies investor conviction that GPU-centric models will capture a disproportionate share of the neocloud market. Lambda Labs followed with USD 480 million to install 65,000 NVIDIA H100 GPUs, and Nebius secured USD 700 million to widen European coverage. Strategic playbooks center on early hardware procurement, software optimization stacks, and managed services that can compress deployment timelines by up to 50%.

White-space remains abundant in edge, sovereign, and green-optimized subsegments. Emerging disruptors leverage open hardware specifications and commodity optics to undercut legacy cost structures, compelling incumbents to reassess their margin assumptions. Barriers to entry harden in regulated verticals as FedRAMP, ISO 27001, and PCI DSS certifications create capital-intensive moats. Meanwhile, partnerships between semiconductor vendors and neocloud operators are intensifying to secure forward chip allocations, potentially reshaping supplier-client power dynamics over the next three years.

The competitive narrative also includes traditional hyperscalers that launch sovereign regions and implement carbon-aware controls; however, their broad service portfolios dilute their focus on AI-first workloads. Consequently, mid-sized specialists carve out defensible territory by promising shorter procurement cycles, lower latency, and granular compliance guardrails. The resulting ecosystem strikes a balance between scale and specialization, keeping price erosion in check while driving technical innovation forward.

Neocloud Industry Leaders

CoreWeave, Inc.

Nebius International B.V.

Lambda Labs, Inc.

Genesis Cloud GmbH

Vast.ai, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: CoreWeave completed a USD 1.1 billion Series C funding round at a USD 19 billion valuation, with participation from Coatue Management and NVIDIA. This expansion of GPU infrastructure capacity will support enterprise AI workload migration, establishing CoreWeave as the largest independent AI cloud provider globally.

- December 2024: Lambda Labs has secured USD 480 million in Series D funding to construct GPU-backed cloud facilities. The company plans to deploy 65,000 NVIDIA H100 GPUs across multiple data centers to support AI model training and inference workloads for its enterprise customers.

- November 2024: Nebius International B.V. has raised USD 700 million in funding to accelerate European market expansion and deploy AI accelerator infrastructure, positioning the company to compete directly with hyperscalers in sovereign cloud markets that require data residency compliance.

- October 2024: Genesis Cloud GmbH announced a strategic partnership with NVIDIA to deploy next-generation AI accelerator infrastructure across European data centers, enabling sub-10-millisecond latency for edge computing applications in manufacturing and telecommunications sectors.

Global Neocloud Market Report Scope

The Neocloud Market Report is Segmented by Deployment Model (Public, Private, Hybrid, and Edge), Service Type (IaaS, PaaS, SaaS, and FaaS), Organization Size (Large Enterprises, and SMEs), End-user Industry (IT and Telecom, BFSI, Healthcare, Manufacturing, Retail, and Government), Workload Type (AI and ML, Data Analytics, Web and Mobile, Development, and Backup), and Geography (Americas, Europe, Asia Pacific, and Rest of World). The Market Forecasts are Provided in Terms of Value (USD).

| Public Neocloud |

| Private Neocloud |

| Hybrid Neocloud |

| Edge Neocloud |

| Cloud-Native Infrastructure |

| Platform-as-a-Service (PaaS) |

| Infrastructure as Code (IaC) and DevOps Enablement |

| Edge and Hybrid Cloud Services |

| AI/ML and Data Services |

| Security and Compliance as a Service |

| Large Enterprises |

| Small and Medium Enterprises |

| IT and Telecom |

| BFSI |

| Healthcare and Life Sciences |

| Manufacturing |

| Retail and E-commerce |

| Government and Public Sector |

| AI and Machine Learning |

| Data Management and Analytics |

| Web and Mobile Applications |

| Development and Testing |

| Backup and Disaster Recovery |

| Americas | United States |

| Rest of Americas | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Rest of the World |

| By Deployment Model | Public Neocloud | |

| Private Neocloud | ||

| Hybrid Neocloud | ||

| Edge Neocloud | ||

| By Service Type | Cloud-Native Infrastructure | |

| Platform-as-a-Service (PaaS) | ||

| Infrastructure as Code (IaC) and DevOps Enablement | ||

| Edge and Hybrid Cloud Services | ||

| AI/ML and Data Services | ||

| Security and Compliance as a Service | ||

| By Organization Size | Large Enterprises | |

| Small and Medium Enterprises | ||

| By End-user Industry | IT and Telecom | |

| BFSI | ||

| Healthcare and Life Sciences | ||

| Manufacturing | ||

| Retail and E-commerce | ||

| Government and Public Sector | ||

| By Workload Type | AI and Machine Learning | |

| Data Management and Analytics | ||

| Web and Mobile Applications | ||

| Development and Testing | ||

| Backup and Disaster Recovery | ||

| By Geography | Americas | United States |

| Rest of Americas | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Rest of the World | ||

Key Questions Answered in the Report

What is the 2026 value of the neocloud market?

The neocloud market size reached USD 35.22 billion in 2026.

How fast is the neocloud market expected to grow?

Revenue is projected to advance at a 46.37% CAGR, taking total value to USD 236.53 billion by 2031.

Which deployment model is growing the quickest?

Edge Neocloud platforms exhibit the fastest trajectory with a 67.72% CAGR over the forecast period.

Why are healthcare organizations adopting neocloud services?

Healthcare and life sciences workloads require HIPAA-compliant AI training and low-latency patient monitoring, propelling a 55.09% CAGR for the segment.

What is the primary restraint on neocloud expansion?

Supply-chain volatility for advanced node GPUs and accelerators restricts infrastructure build-outs, subtracting an estimated 4.1% from potential CAGR.

Which region will lead growth through 2031?

Asia Pacific is forecast to post a leading 54.5% CAGR supported by 5G roll-outs, manufacturing automation, and data-sovereignty initiatives.

Page last updated on: