Finance Cloud Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

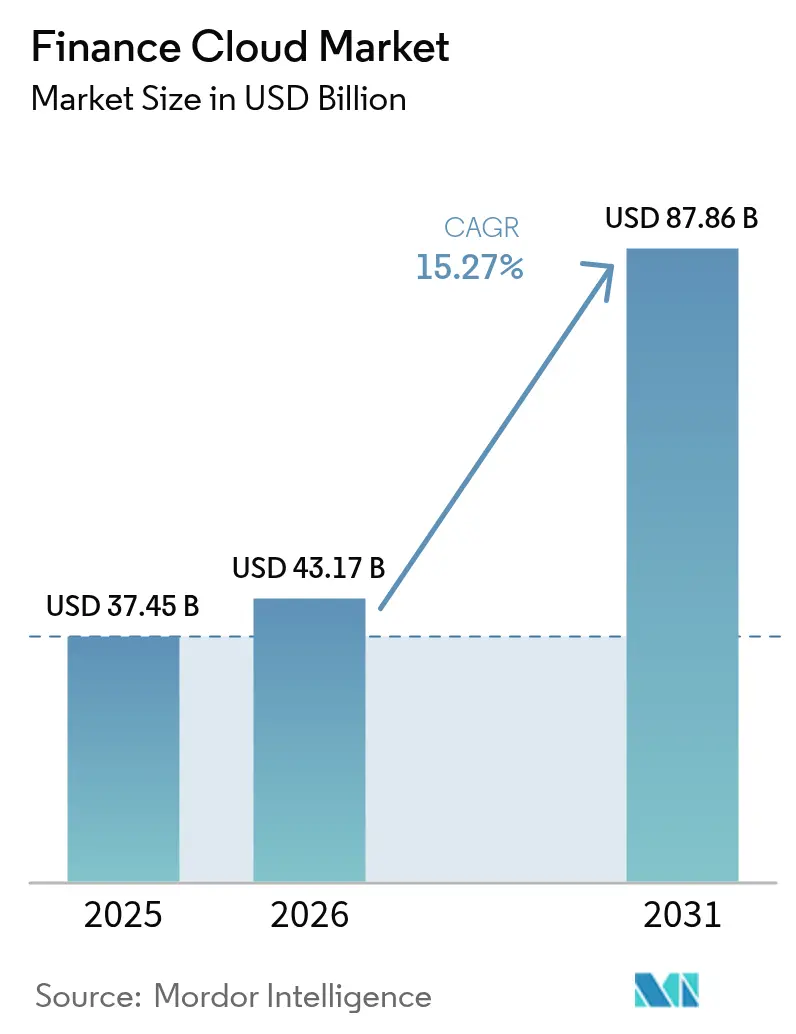

| Market Size (2026) | USD 43.17 Billion |

| Market Size (2031) | USD 87.86 Billion |

| Growth Rate (2026 - 2031) | 15.27% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Finance Cloud Market Analysis by Mordor Intelligence

The finance cloud market size is expected to grow from USD 37.45 billion in 2025 to USD 43.17 billion in 2026 and is forecast to reach USD 87.86 billion by 2031 at 15.3% CAGR over 2026-2031. Rising digital-first consumer expectations, tighter regulatory oversight, and the maturation of cloud security frameworks are driving widespread migration of core finance workloads to public and hybrid clouds. The European Union’s Digital Operational Resilience Act (DORA) alone mandates upgraded ICT risk controls for about 22,000 financial entities and their technology partners, accelerating platform modernization across the region[1]European Banking Authority, “Digital Operational Resilience Act Portal,” eba.europa.eu. At the same time, 98% of financial institutions globally already use at least one cloud service, up from 91% in 2020, confirming that the finance cloud market has reached critical mass. Generative AI roll-outs on cloud infrastructure now underpin everything from automated reconciliation to predictive cash-flow modelling, turning cloud providers into strategic partners for competitive differentiation. North American banks fund multibillion-dollar tech budgets to migrate thousands of applications, while Asia-Pacific institutions scale cloud-native cores to serve massive digital customer bases—all of which keeps the finance cloud market on a steep growth trajectory.

Key Report Takeaways

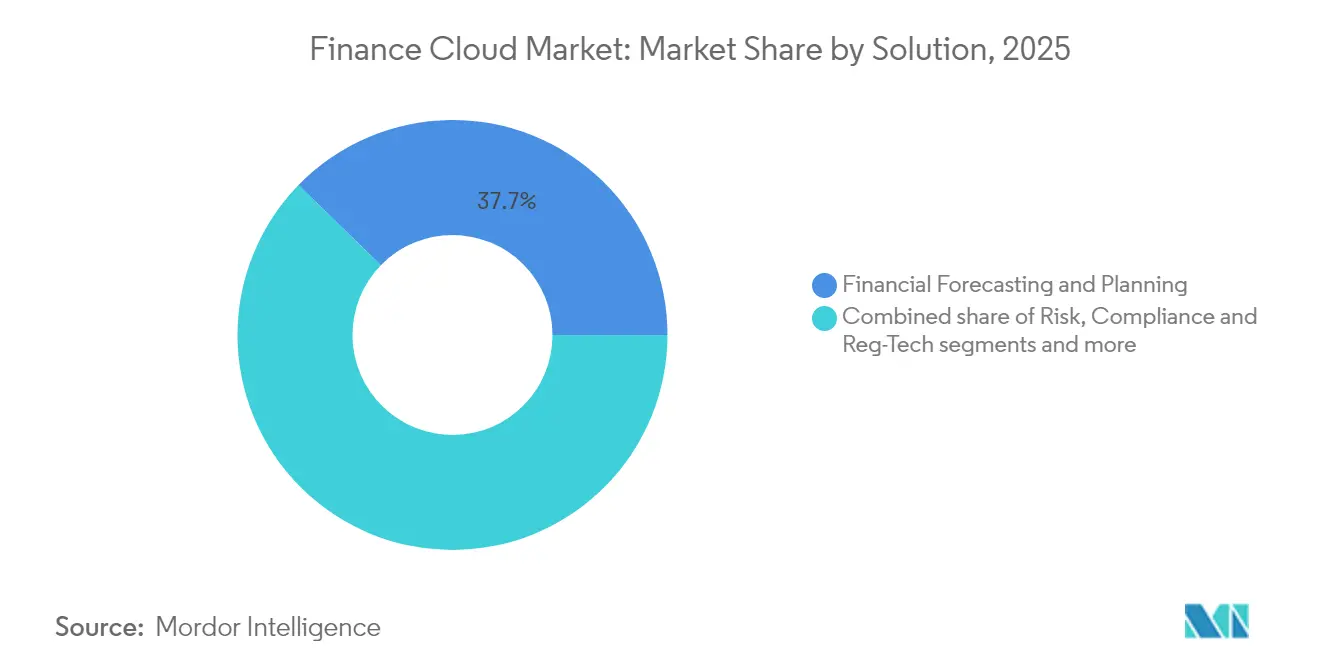

- By solution, Financial Forecasting and Planning led with 37.70% revenue share in 2025; Risk, Compliance and RegTech is projected to expand at a 15.62% CAGR through 2031.

- By deployment model, Public Cloud held 56.90% of the finance cloud market share in 2025, while Hybrid/Multi-Cloud configurations are forecast to advance at 16.55% CAGR through 2031.

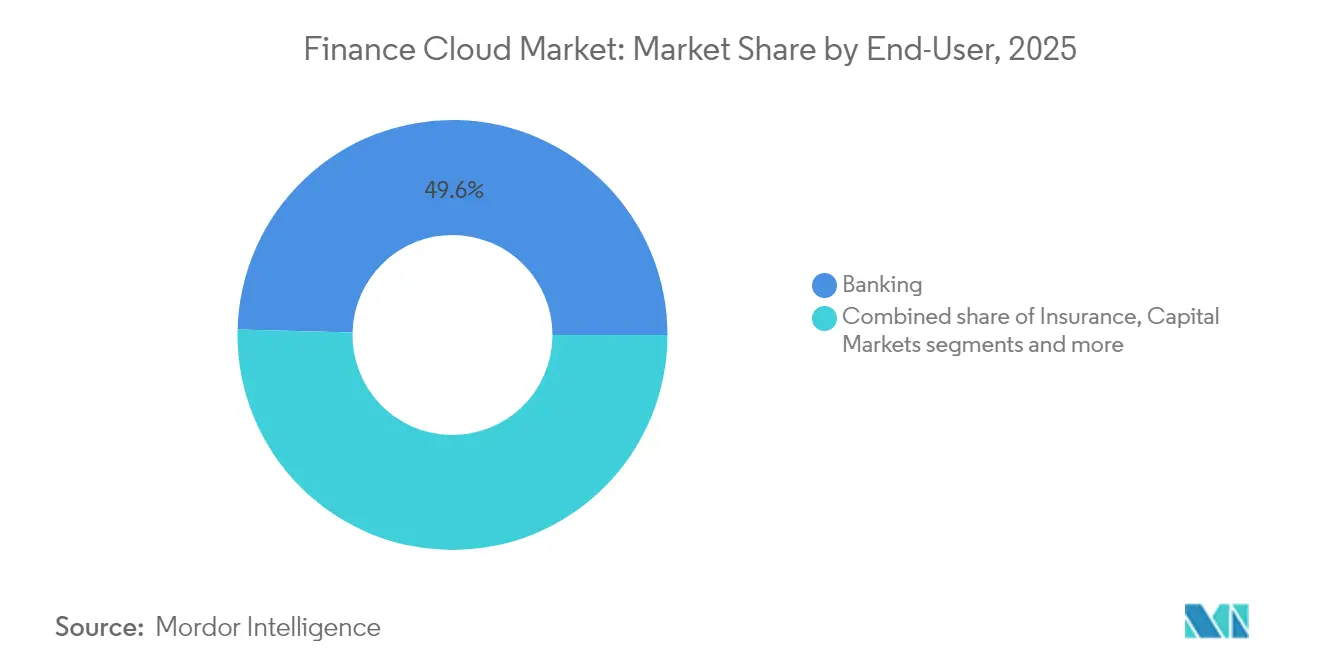

- By end-user, banking commanded 49.60% share of the finance cloud market size in 2025; FinTech and neo-banks are poised to grow at 16.12% CAGR to 2031.

- By organisation size, large enterprises accounted for 70.55% share of the finance cloud market size in 2025; SMEs exhibit the fastest growth at 16.84% CAGR.

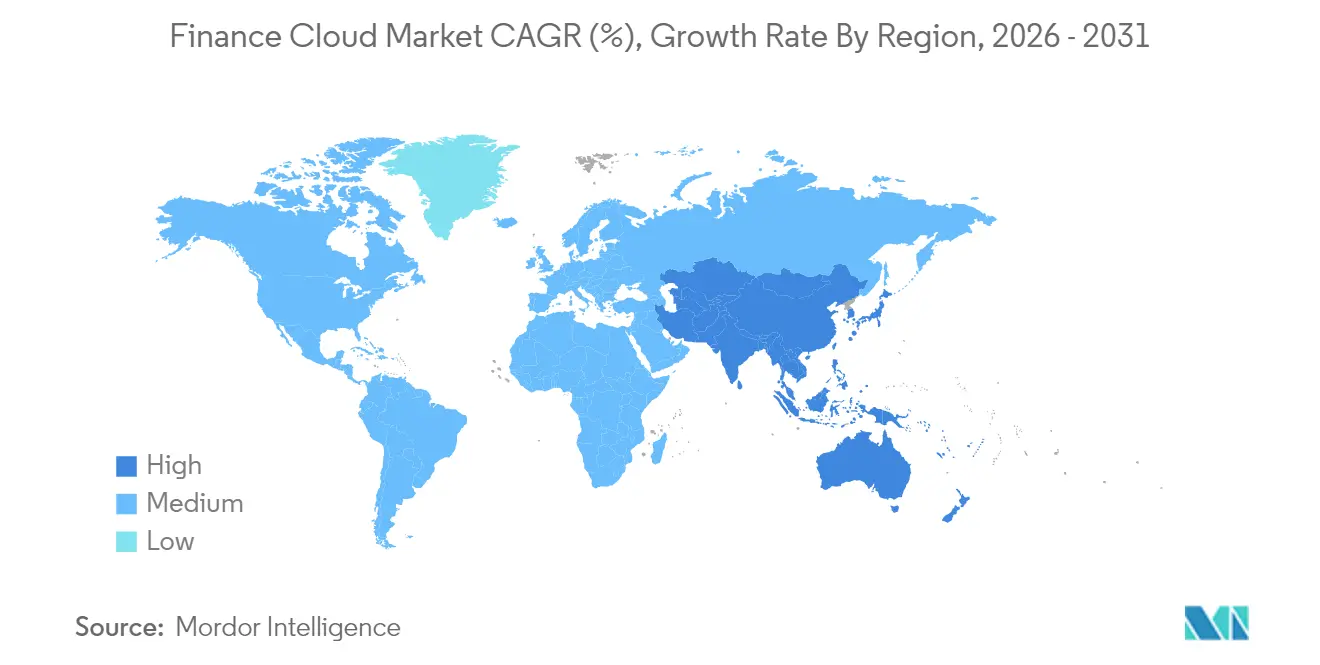

- By geography, North America contributed 40.60% of 2025 revenue, whereas Asia-Pacific is projected to record the quickest regional CAGR of 15.96% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Finance Cloud Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Need for improved customer relationship management | +2.8% | Global, stronger in North America and APAC | Medium term (2-4 years) |

| Demand for operational efficiency in financial sector | +3.2% | Global, pronounced in Europe and North America | Short term (≤2 years) |

| Regulatory push for real-time transparency and reporting | +4.1% | Europe leading, expanding globally | Short term (≤2 years) |

| GenAI-enabled self-service finance analytics | +2.9% | North America and APAC core, spill-over to Europe | Medium term (2-4 years) |

| FinOps adoption to optimise cloud spending | +1.8% | Global, early uptake in North America | Long term (≥4 years) |

| Industry-cloud platforms for BFSI verticals | +2.2% | Global, stronger in developed markets | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Need for Improved Customer Relationship Management

Cloud-based CRM suites give financial institutions real-time insight into behavioural patterns, enabling hyper-personalised offers that improve retention in crowded markets. Asia-Pacific banks run cloud platforms capable of supporting tens of millions of concurrent sessions, as illustrated by AIBank’s micro-services core that serves more than 100 million customers. In parallel, North American lenders integrate cloud analytics with loyalty engines to cut churn that still affects over 60% of legacy institutions. Because finance data is highly regulated, vendors differentiate through in-platform encryption, audit trails, and data-residency controls that satisfy regulators while still allowing cross-channel orchestration. As customer lifetime value becomes a pivotal KPI, the finance cloud market gains further momentum from banks’ willingness to replace ageing CRM tools with elastic, AI-ready alternatives.

Demand for Operational Efficiency in Financial Sector

Moving finance workloads to consumption-based clouds converts capital expenditure into variable operating cost, releasing cash for product innovation. Institutions that completed full cloud migrations report 20-30% reductions in month-end close cycles and similar gains in regulatory reporting speed. Automation natively embedded in cloud ERPs eliminates manual journals, while serverless compute handles unpredictable spikes in payment volumes without performance degradation. Discover Financial Services, for example, relies on a hybrid estate to flex resources during seasonal spending peaks. As margins tighten, cost-to-income ratios now appear on board dashboards alongside revenue, reinforcing the efficiency narrative that will continue to propel the finance cloud market.

Regulatory Push for Real-Time Transparency and Reporting

Since January 2025, DORA obliges European banks to log, test, and report ICT incidents in near real time. The regulation directly subjects critical third-party cloud providers to supervisory scrutiny, prompting institutions to adopt compliant platforms equipped with automated audit evidence capture, immutable logs, and cross-jurisdiction data-residency controls. Similar operational-resilience frameworks are in draft stages in North America and Asia-Pacific, creating a domino effect that favours cloud architectures offering built-in controls libraries. Vendors that embed continuous security validation, threat-intelligence feeds, and zero-trust networking stand to capture outsized wallet share within the finance cloud market.

GenAI-enabled Self-service Finance Analytics

Generative AI embedded in cloud ERP and EPM suites delivers conversational insight generation, letting business users query ledgers or generate forecasts via natural-language prompts. Workday’s Spring 2025 release introduced AI-Powered Accounts Payable and 350 other features that cut invoice processing times and speed financial closes. FIS followed with Treasury GPT, an Azure-based assistant that won industry innovation awards[2]FIS Global, “Treasury GPT Wins TMI Award,” fisglobal.com. Large-language-model deployments need scalable GPUs and high-bandwidth storage that public clouds supply on demand, securing a fresh layer of growth for the finance cloud market. Nevertheless, banks must implement rigorous model-governance and data-quality frameworks to satisfy auditors, an area where enterprise clouds again offer pre-configured services.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rise of cloud-based cyber threats | −2.1% | Global, heightened in North America and Europe | Short term (≤2 years) |

| Legacy-core integration complexity | −1.8% | Global, acute in markets with older infrastructure | Medium term (2-4 years) |

| Talent gap in cloud FinOps and data engineering | −1.3% | Global, severe in APAC and emerging regions | Long term (≥4 years) |

| Vendor lock-in and GenAI cost overruns | −0.9% | Mainly developed markets with high cloud adoption | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rise of Cloud-based Cyber Threats

Financial services remain the top target for sophisticated attacks, and cloud environments enlarge the threat surface. US regulators report escalating ransom incidents that disrupt critical payment infrastructures, prompting banks to double investments in zero-trust architectures and extended detection platforms. Migrating sensitive data without commensurate security uplift exposes institutions to regulatory fines that can exceed annual IT budgets. Cloud providers answer with confidential computing, hardware-rooted encryption, and sovereign-cloud blueprints, yet implementing these controls adds cost and complexity, muting short-term acceleration in the finance cloud market.

Legacy-core Integration Complexity

Roughly 90% of European banks still run parts of their ledger or payments stack on platforms older than a decade. Bridging these monoliths with cloud micro-services calls for scarce mainframe-to-Kubernetes skillsets and extended parallel-run periods that inflate project costs. Institutions therefore adopt phased coexistence strategies—lifting non-core workloads first and gradually refactoring the core—stretching realisation timelines. Emerging AI code-conversion tools promise to automate refactoring, yet are only beginning to reach production maturity. This integration overhang continues to cap upside in the finance cloud market during the medium term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution: Planning Dominance Amid RegTech Acceleration

The Financial Forecasting and Planning segment retained 37.70% revenue in 2025, reflecting the universal need for scenario modelling when economic volatility remains high. Cloud-based EPM suites let finance teams generate rolling forecasts across thousands of cost centres, elevating data-driven decision-making. Integrated driver-based models update profit outlooks instantly after rate or FX shocks, reinforcing migration urgency. Concurrently, Risk, Compliance, and RegTech is the fastest-growing solution line, advancing at 15.62% CAGR through 2031 on the back of DORA and comparable regimes. Vendors embed API-ready regulatory libraries so institutions can push granular transaction data to supervisors with one-click reporting. Continuous control monitoring features lower audit-prep workloads, translating compliance budgets directly into demand for the finance cloud market.

Core Accounting and General Ledger platforms remain indispensable, acting as system-of-record anchors for all other cloud finance modules. Treasury and Cash-Management tools gain new momentum as volatile funding markets prioritise real-time liquidity insight. Citigroup, for instance, expanded its cloud treasury workspace to aggregate global cash positions minute-by-minute. Payroll and Workforce Finance applications benefit from tight finance-HR convergence; Workday’s latest release bundles headcount planning with spend analytics, underscoring how integrated suites improve enterprise alignment. As vendors package these capabilities under unified data fabrics, upsell pipelines expand, driving sustainable revenue streams within the finance cloud market.

By Deployment Model: Public Cloud Leadership with Hybrid Momentum

Public clouds controlled 56.90% of 2025 revenue due to hyperscalers’ global footprints, advanced security certifications, and continuous innovation roadmaps. Banks routinely adopt managed PaaS databases to accelerate new product rollouts without provisioning hardware. Yet dependence on a single provider raises resilience concerns, propelling Hybrid and Multi-Cloud uptake at 16.55% CAGR. European lenders, mindful of concentration risk outlined by regulators, increasingly split workloads across at least two vendors, while retaining ultra-low-latency trading engines on private clouds. Form3’s payment platform exemplifies this strategy, abstracting routing logic so banks can toggle endpoints among clouds during outages.

Private clouds remain vital for use cases with stringent performance or data-sovereignty requirements. JPMorgan Chase is spending USD 2 billion on four new private cloud data centres that anchor latency-sensitive risk computations. Unified observability stacks and policy-as-code reduce operational friction across mixed estates, making hybrid truly seamless. Because regulatory discourse now explicitly references “exit plans,” institutions favour containerised workloads and open APIs to avoid lock-in, a development that further broadens addressable opportunity for the finance cloud market.

By End-User: Banking Stability Contrasts FinTech Dynamism

Traditional banking institutions delivered 49.60% of 2025 revenue, reflecting their scale and compulsory compliance spend. Core-modernisation programmes migrate deposit systems and payment rails to elastic architectures, releasing innovation bandwidth for embedded finance partnerships. FinTech and neo-banks, however, post the highest CAGR at 16.12%, showcasing how cloud-native cores permit faster iteration cycles and lower per-account costs. A 2024 MDPI study found that digital-only lenders can launch new features 4-5 times quicker than peers. This agility forces incumbents to accelerate adoption, sustaining a virtuous circle of demand inside the finance cloud market.

Insurance carriers deploy cloud ML models to refine underwriting and automate claims triage, while capital-markets firms need low-latency data fabrics for algorithmic trading and near-real-time risk aggregation. Nasdaq and AWS launched the Eqlipse suite to modernise market infrastructure, signalling widespread buy-side and sell-side readiness for cloud execution. Collectively, these segments diversify growth sources and amplify the resilience of the finance cloud industry against cyclical slowdowns in any single vertical.

By Organisation Size: Enterprise Scale Meets SME Agility

Large enterprises contributed 70.55% of revenue in 2025, leveraging multi-year, multi-million-dollar transformation budgets. Complex global operations need regional data-residency, 24×7 availability, and granular segregation-of-duty controls that leading platforms now embed out of the box. Governance risk committees, therefore, green-light enterprise-wide adoption, reinforcing the size of the finance cloud market. Yet SMEs grow fastest at 16.84% CAGR as vendors introduce pay-as-you-grow tiers and pre-configured best-practice charts of account. Treasury-as-a-Service bundles combine payments, liquidity dashboards, and FX hedging into a single portal, removing the need for specialist staff.

SMEs represent 99% of OECD businesses, and surveys show over 40% still suffer from credit or cash-flow gaps. Cloud platforms that integrate bank feeds, predictive invoice-collection analytics, and embedded financing options unlock working-capital insights previously reserved for corporates. Because implementation is lightweight, SME rollouts often conclude within weeks, allowing vendors to scale via digital channels. This high-volume, low-touch model broadens the finance cloud market beyond the top tier while creating attractive recurring revenue streams for providers.

Geography Analysis

North America retained 40.60% of 2025 revenue thanks to deep technology budgets and regulatory clarity that fosters accelerated migration. The United States anchors the region, with JPMorgan Chase alone allocating USD 17 billion annually to tech and moving 6,000 applications to cloud platforms. Canada follows with open-banking guidelines that encourage secure API ecosystems, while Mexican banks adopt cloud to meet cross-border reporting standards. Public-private collaboration on cybersecurity and digital-identity frameworks further de-risks adoption, strengthening the finance cloud market in the region. Providers leverage dense data-centre footprints to meet sub-10-millisecond latency thresholds demanded by high-frequency traders.

Asia-Pacific is the fastest-growing territory at 15.96% CAGR through 2031. Government-backed digital-economy blueprints place cloud at the centre of financial-inclusion agendas, underpinning a regional digital-economy value expected to reach USD 1 trillion by 2030. China’s AIBank demonstrates cloud scalability by serving over 100 million customers on a containerised platform. India’s public-cloud policy now allows regulated entities to host core data offshore under strict encryption keys, unlocking broader hyperscaler adoption. Japan and Australia endorse Industry-Cloud models that deliver pre-certified compliance artefacts for local supervisory bodies. Coupled with rising fee-based revenue targets—APAC banks expect digital adjacencies to supply 40% of profit pools by 2030—these trends ensure sustained upside for the finance cloud market.

Europe accelerates cloud modernisation under DORA’s operational-resilience mandate, affecting roughly 22,000 financial organisations. Germany, France, and the United Kingdom roll out shared testing frameworks for cyber-incident simulations, incentivising the adoption of platforms that automate evidence collection. Sovereign-cloud regions operated by large providers satisfy data-sovereignty clauses, while multi-vendor strategies mitigate systemic risk. South America charts high growth, powered by Brazil’s branchless challenger banks such as Nubank, which posted USD 2 billion profit in 2024 while operating entirely on cloud infrastructure. Middle East and Africa adoption climbs swiftly; 83% of MENA financial firms now run cloud workloads and expect USD 21.14 million in annual savings within two years. Gulf Cooperation Council banks align national cloud mandates with ambitious digital transformation roadmaps, solidifying new demand pockets for the finance cloud market.

Competitive Landscape

The finance cloud market shows moderate concentration, with a mix of hyperscale cloud vendors, enterprise-software incumbents, and cloud-native specialists contesting share. Oracle reported USD 12.5 billion in new AI-linked bookings and deepened its alliance with Microsoft to host Oracle Databases inside Azure regions, enabling customers to co-locate data and application tiers. Amazon Web Services teamed with Nasdaq to co-engineer the Eqlipse suite, signalling a vertical-platform play aimed at capital-markets clients. IBM augmented its FinOps posture by acquiring Kubernetes cost-management vendor Kubecost and rolling out sovereign-cloud blueprints tailored to DORA compliance[4]IBM, “IBM Launches Sovereign Cloud Capabilities,” ibm.com.

Specialist vendors inject competitive tension. Planful serves more than 1,300 customers with AI-enhanced planning tools that promise sub-second scenario refreshes, while Treasury-as-a-Service start-ups target SME white spaces. Private-equity activity intensifies: Vista Equity Partners will absorb Acumatica by Q3 2025 to accelerate product innovation around AI-first ERP modules. Consolidation trends continue as smaller providers struggle with escalating compliance and GPU-compute costs, pushing them into partnerships or acquisitions. Market winners increasingly differentiate by quantifying efficiency savings; several banks report 25% faster book-close cycles after implementing cloud AI automation suites. Overall, vendor success hinges on security certifications, local data centre expansion, and the ability to embed end-to-end compliance artefacts that de-risk adoption for regulated buyers.

Finance Cloud Industry Leaders

IBM Corporation

Microsoft Corporation

Salesforce.com Inc.

SAP SE

Oracle Corporation(Netsuite)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Acumatica’s acquisition by Vista Equity Partners is expected to close in Q3 2025, with a focus on AI-first product strategy and vertical ERP innovation.

- May 2025: IBM Cloud introduced sovereign-cloud and high-performance AI infrastructure aimed at regulated industries, aligning with new DORA obligations.

- April 2025: Nasdaq and AWS launched the Eqlipse marketplace-technology suite to boost global liquidity with built-in data-sovereignty features.

- March 2025: Workday’s Spring 2025 release delivered 350 new finance and HR features, including AI-Powered Accounts Payable and automated services CPQ.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the finance cloud market as the spending that banks, insurers, payment firms, asset managers, and fintechs channel into cloud-delivered software, platforms, and infrastructure for regulated finance workloads, core banking, risk analytics, treasury, and statutory reporting. Deployment models assessed include public, private, and hybrid environments offered by hyperscale and specialist vendors.

Scope exclusion: Generic office-productivity or customer-experience SaaS that is not purpose-built for financial compliance sits outside this study.

Segmentation Overview

- By Solution

- Core Accounting and GL

- Financial Forecasting and Planning

- Risk, Compliance and Reg-Tech

- Treasury and Cash-Management

- Payroll and Workforce Finance

- By Deployment Model

- Public Cloud

- Private Cloud

- Hybrid / Multi-Cloud

- By End-User

- Banking

- Insurance

- Capital Markets

- FinTech / Neo-banks

- By Organisation Size

- Large Enterprises

- Small and Medium Enterprises (SMEs)

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Nigeria

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Structured conversations with tier-1 bank CTOs, regional-insurer compliance leads, cloud-procurement heads, and fintech architects across North America, Europe, and Asia-Pacific refined migration timelines, average contract sizes, and security-premium assumptions that public sources could not capture.

Desk Research

Mordor analysts pieced together baseline figures using respected open sources such as the Bank for International Settlements technology-spend survey, IMF ICT satellite accounts, FDIC call-report archives, and the European Banking Authority's cloud-outsourcing register. Patent landscapes were mined via Questel, while earnings transcripts on Dow Jones Factiva and customs records for 'managed cloud services' provided directional cross-checks. The items named are illustrative; many additional datasets and association white papers supported data collection and anomaly screening.

Market-Sizing & Forecasting

We begin with a top-down rebuild of total BFSI ICT outlays, isolate the cloud share disclosed by regulators and vendors, then distribute value across solutions and deployments through penetration-rate demand pools. A targeted bottom-up roll-up of sampled ASP × active instances validates totals. Key variables like digital-only bank launches, share of core workloads moved off-premise, DORA compliance deadlines, public-cloud price index shifts, and fintech funding flows feed a multivariate regression projecting demand to 2030, with deal benchmarks plugging residual gaps.

Data Validation & Update Cycle

Outputs face three analyst reviews, variance tests against independent benchmarks, and anomaly flags before sign-off. Reports refresh yearly; material events trigger interim updates, followed by a final sweep so clients receive our latest view.

Why Mordor's Finance Cloud Baseline Commands Trust

Published estimates often diverge because firms choose different scopes, currencies, and refresh cadences; decision-makers therefore need one dependable anchor.

Divergence typically arises when other studies include horizontal SaaS, rely on historic FX rates, omit hybrid workloads, or apply uniform CAGR without variable testing.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 37.45 B | Mordor Intelligence | - |

| USD 135.60 B | Global Consultancy A | Broader scope; no primary checks |

| USD 23.23 B | Industry Association B | Excludes hybrid deployments; blanket CAGR |

The comparison shows that our disciplined scope, annual refresh, and dual validation steps deliver a balanced, traceable baseline clients can trust.

Key Questions Answered in the Report

What is the current size of the finance cloud market?

The finance cloud market stands at USD 43.17 billion in 2026 and is projected to grow to USD 87.86 billion by 2031.

Which deployment model leads the finance cloud market?

Public cloud solutions currently dominate with 56.90% market share, although hybrid and multi-cloud setups are expanding the fastest at a 16.55% CAGR.

How does DORA influence finance cloud adoption in Europe?

DORA enforces stricter ICT-risk controls and real-time reporting, prompting European banks to implement compliant cloud platforms equipped with automated audit and resilience features.

Why are SMEs adopting finance cloud platforms rapidly?

Pay-as-you-grow pricing, embedded AI automation, and Treasury-as-a-Service bundles allow SMEs to access enterprise-grade financial tools without heavy upfront investment, driving a 16.84% CAGR.

What role does generative AI play in the finance cloud market?

Generative AI powers self-service analytics, intelligent payables, and conversational treasury assistants, boosting operational efficiency and strengthening the business case for cloud migration.

Who are the major players in the finance cloud market?

Leading providers include Oracle, Amazon Web Services, Microsoft, IBM, SAP, and specialist firms like Planful and Acumatica, each differentiating through AI capabilities and compliance-ready architectures.

Page last updated on: