Cloud Native Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

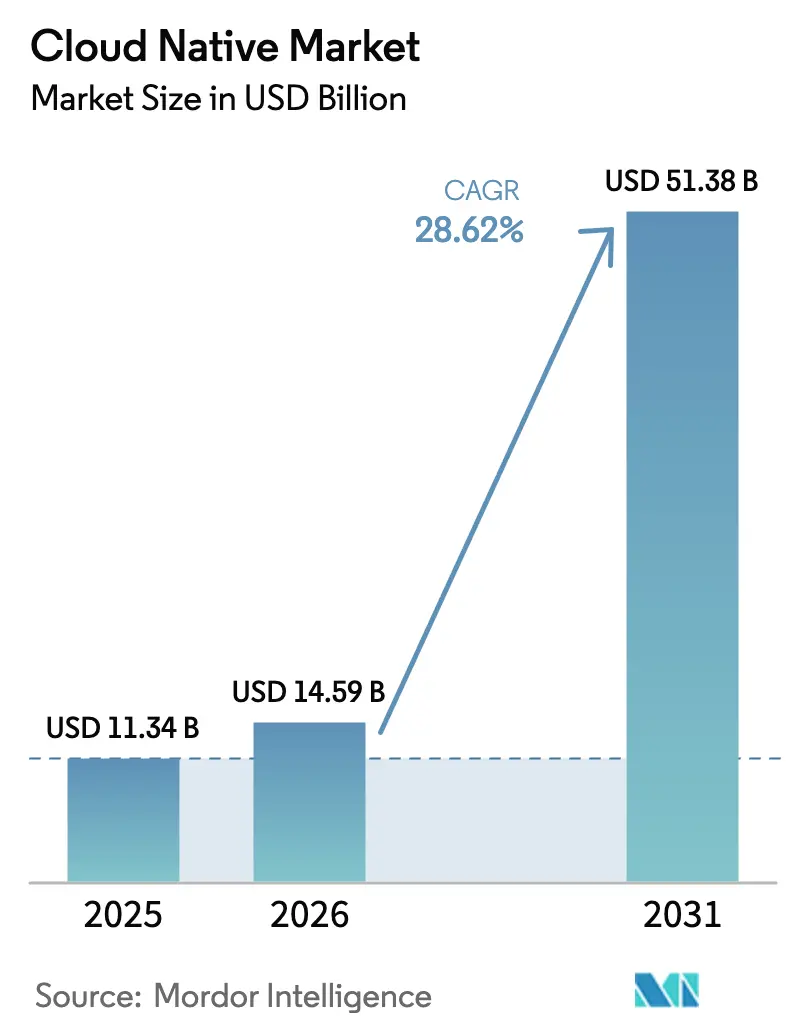

| Market Size (2026) | USD 14.59 Billion |

| Market Size (2031) | USD 51.38 Billion |

| Growth Rate (2026 - 2031) | 28.62% CAGR |

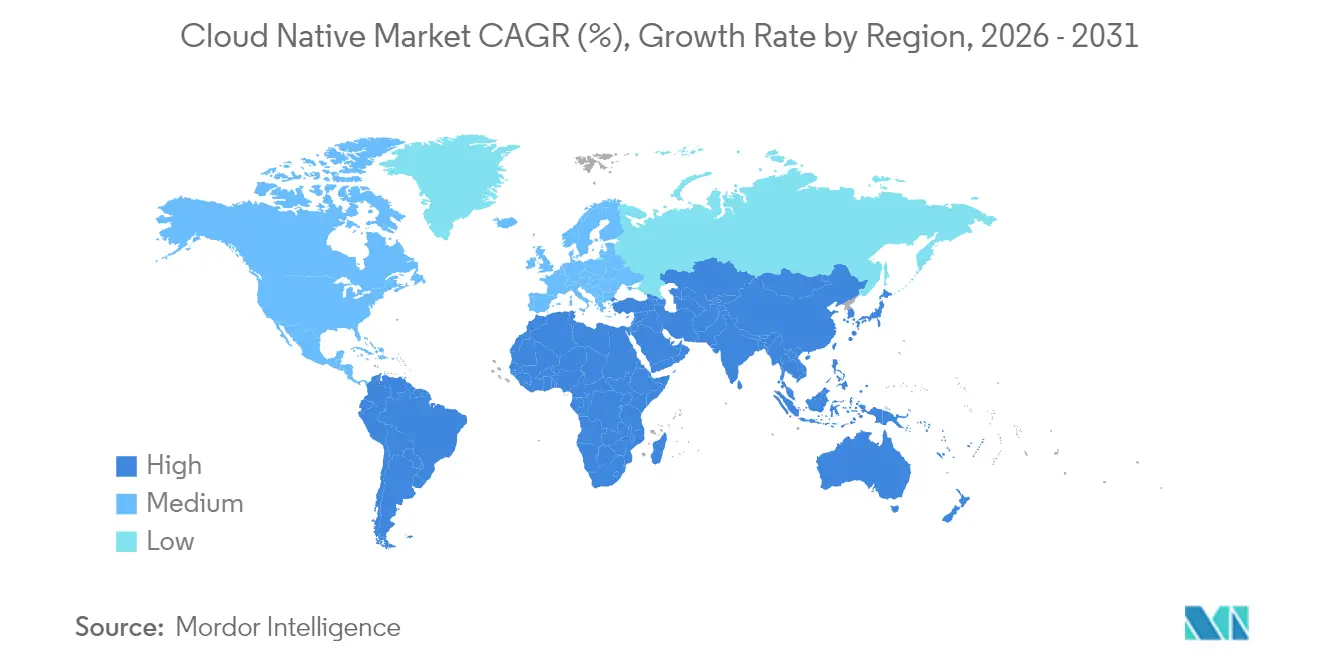

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cloud Native Market Analysis by Mordor Intelligence

The cloud native market size is expected to grow from USD 11.34 billion in 2025 to USD 14.59 billion in 2026 and is forecast to reach USD 51.38 billion by 2031 at 28.62% CAGR over 2026-2031. Growth accelerators include platform engineering adoption, Kubernetes-native data services, and the surge of generative-AI workloads that now drive half of cloud infrastructure expansion. GPU consumption for AI training has risen 336% year-over-year at Oracle, illustrating how specialized compute reshapes infrastructure demand. Enterprises use these technologies to maintain hybrid consistency, reduce vendor lock-in, and satisfy rising sovereign-cloud compliance. Public cloud keeps its lead, yet hybrid and multi-cloud patterns grow faster as organizations seek workload portability and data-localization conformity.

Key Report Takeaways

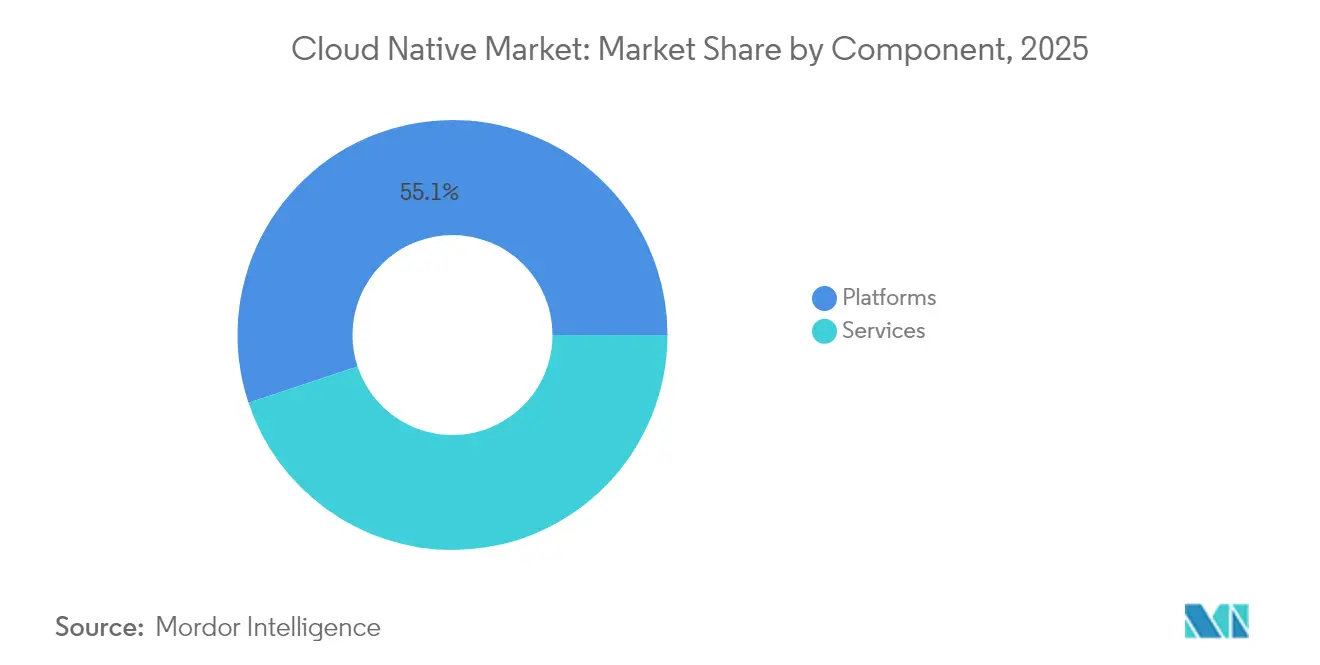

- By component, platforms held 55.10% of cloud native market share in 2025, while services are projected to expand at a 32.04% CAGR to 2031.

- By deployment model, public cloud led with 61.05% revenue share in 2025; hybrid and multi-cloud configurations are forecast to grow at 34.06% CAGR through 2031.

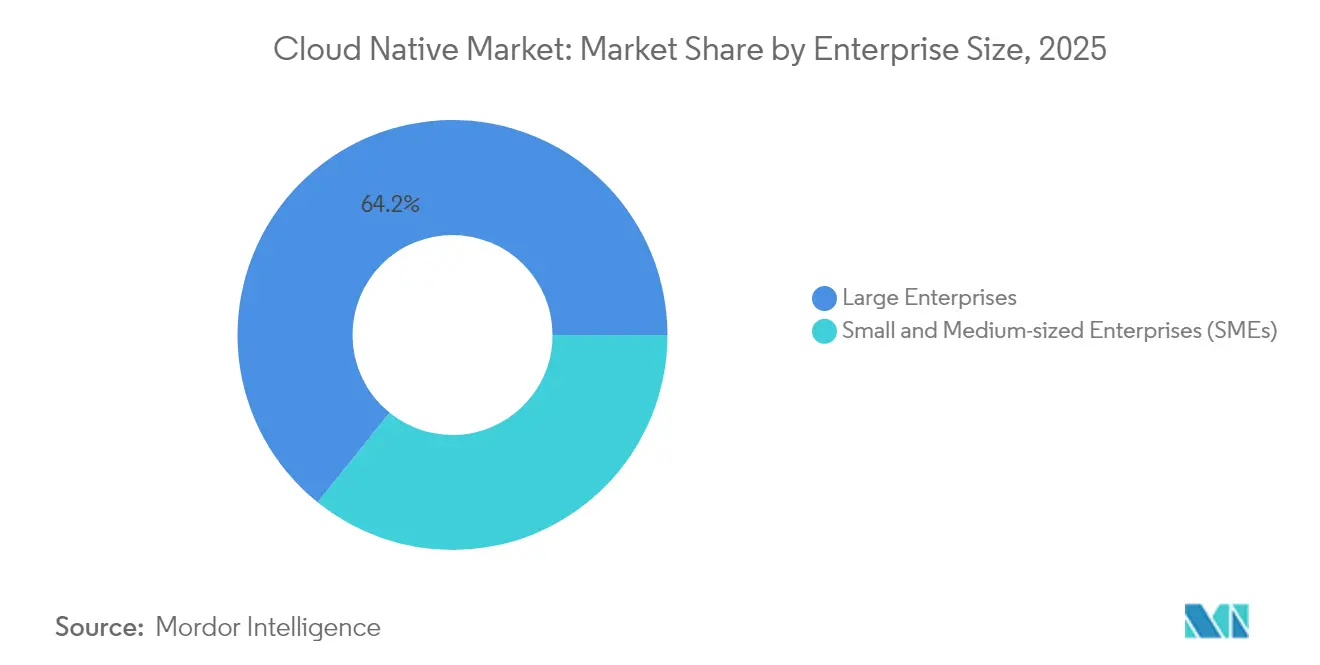

- By enterprise size, large enterprises accounted for 64.20% of the cloud native market size in 2025; SMEs exhibit the fastest growth at 31.82% CAGR.

- By end-user industry, BFSI captured 29.10% of cloud native market share in 2025, while healthcare and life sciences will progress at a 35.59% CAGR to 2031.

- By geography, North America commanded 41.20% revenue share in 2025; Asia-Pacific is advancing at 33.88% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cloud Native Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Generative-AI-driven workload explosion | +8.5% | Global, with North America and Asia-Pacific focus | Medium term (2-4 years) |

| Mandatory carbon-aware cloud optimisation | +3.2% | Primarily EU, secondary North America | Long term (≥ 4 years) |

| Enterprise shift to platform engineering teams | +6.1% | Global, led by North America and Europe | Short term (≤ 2 years) |

| Kubernetes-native data services maturation | +4.8% | Global | Medium term (2-4 years) |

| Hyperscaler sovereign-cloud programmes | +3.9% | Core in Asia-Pacific, spill-over to MEA | Medium term (2-4 years) |

| Accelerated industry-cloud blueprints | +2.9% | Global, regulation-driven in EU and Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Generative-AI-driven workload explosion

Specialized compute for large language models forces redesign of application architectures around containers that can scale inference across heterogeneous hardware. Oracle’s 336% GPU-use surge underscores the magnitude of demand for AI-ready capacity. WebAssembly runtimes achieve 35.4 microsecond start-up times, enabling near-native performance for micro-services and ML inference.[1]Fastly Engineering, “Improving Cold Start with WebAssembly,” fastly.com Platform teams now pair wasmCloud with distributed ML frameworks to cut latency from edge to core while keeping security isolation. Standardisation momentum is visible in the CNCF’s 2025 release of Dapr AI Agents, which reduces orchestration complexity for multi-cloud AI deployments.[2]Cloud Native Computing Foundation, “Annual Survey 2025,” cncf.io

Enterprise shift to platform engineering teams

Platform engineering abstracts infrastructure complexity and promotes secure self-service. Adoption reached 55% of organisations, with 90% planning expansion. Graduated CNCF projects such as cert-manager automate certificate life-cycles, cutting manual security overhead. Vendors weave AI assistance into these platforms; Red Hat and Stability AI integrated generative tooling into OpenShift, aiming at productivity gains and cost control.[3]Red Hat, “Hybrid Cloud Strategy Update 2025,” redhat.com

Kubernetes-native data services maturation

Sixty-nine percent of technology leaders report advanced stages of running databases on Kubernetes. Operators like CloudNativePG automate failover and backup, allowing stateful workloads to gain the same portability as stateless services. Multi-cluster tools such as k8gb route traffic during region outages, increasing fault tolerance. Multiple data-focused projects have graduated from the CNCF incubator, signalling readiness for production-critical applications across sectors.

Hyperscaler sovereign-cloud programmes

Data-localisation laws accelerate adoption of region-specific cloud environments. Nineteen percent of Asia-Pacific firms plan higher sovereign-cloud spending to meet compliance demands. AWS’s commitment of EUR 7.8 billion for a European sovereign cloud shows capital intensity behind localisation.[4]Gcore, “AWS European Sovereign Cloud Investment,” gcore.com Oracle’s alliances with Microsoft and Google add choice for regulated workloads that need boundary control while retaining hyperscaler capabilities.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Exit-strategy and repatriation cost shock | -4.2% | North America and Europe | Short term (≤ 2 years) |

| Shortage of cloud-native security talent | -3.8% | Global | Medium term (2-4 years) |

| Emerging-nation data-localisation mandates | -2.1% | Primarily Asia-Pacific, secondary MEA | Long term (≥ 4 years) |

| Escalating e-waste from fast server refresh | -1.9% | Global, EU regulatory focus | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Exit-strategy and repatriation cost shock

Eighty-three to 86% of CIOs plan some workload shifts, yet hidden extraction costs often eclipse forecast savings. Dependencies on cloud-native services mean that data movement, redesign of integrations, and new hardware investments offset repatriation gains. Firms now design for portability from day-one using open-source orchestration and database operators to protect future exit options.

Shortage of cloud-native security talent

A projected 3.5 million cybersecurity roles remain unfilled in 2025. Container runtime hardening and service-mesh policy design require skills beyond traditional security. Vendors respond with security-by-design layers baked into developer workflows, and AI assistants automate routine vulnerability management. Human expertise, however, remains essential for strategic architecture.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Surge Past Platform Dominance

Services are forecast to expand at 32.04% CAGR through 2031 as enterprises outsource managed Kubernetes, security monitoring, and lifecycle operations. Platforms maintained 55.10% cloud native market share in 2025, but the steep rise of services shows preference for vendor expertise when internal complexity grows. Red Hat’s estimated USD 5–10 billion annual hybrid cloud revenue underlines demand for integrated software and advisory bundles.

The services wave intersects with platform engineering adoption because 75–80% of organisations intend to form dedicated teams. Consulting and managed offerings help design, build, and run these platforms, letting customers keep focus on product delivery. Vendors embed AI into support layers, allowing proactive optimisation. This blend of automation and service know-how sustains the cloud native market growth trajectory.

By Deployment Model: Hybrid Architectures Reshape Cloud Economics

Public cloud held 61.05% of revenue in 2025, yet hybrid and multi-cloud segments will grow 34.06% CAGR to 2031. Organisations use multi-provider strategies to avoid lock-in and meet localisation rules, a pattern validated by Oracle’s 115% sequential jump in MultiCloud database revenue. Sovereign programmes from yperscalers align with this trend, packaging compliance controls with familiar services.

Private cloud remains crucial for industries needing on-premises data, but they increasingly adopt cloud-native tooling for parity with public services. Hybrid control planes unify operational experience, trimming skills gaps and speeding deployment. These factors reinforce demand across every deployment category and widen the overall cloud native market.

By Enterprise Size: SME Adoption Accelerates Through Platform Simplification

Large enterprises accounted for 64.20% of cloud native market size in 2025, yet SMEs will grow 31.82% CAGR through 2031. Simplified SaaS-delivered platforms and managed Kubernetes clusters lower entry barriers for resource-constrained firms. Kubernetes commands 60% orchestration penetration, promoting open standards that appeal to SMEs wary of vendor dependency.

AI-assisted automation trims operational burden, letting small teams manage sophisticated architectures. At the same time, internal platform engineering in large firms standardises governance and security. These dual motions expand the install base across both segments and ensure steady adoption momentum for the cloud native market.

By End-user Industry: Healthcare Digitization Drives Vertical Transformation

BFSI led with 29.10% revenue in 2025, but healthcare and life sciences will progress at 35.59% CAGR through 2031 as telemedicine, genomic analytics, and AI-aided diagnostics demand elastic compute. Industry cloud blueprints package compliance frameworks and domain APIs, speeding adoption in regulated fields. Ninety-five percent of firms recognise value in vertical-specific solutions.

Manufacturing and retail embrace edge orchestration for 5G and supply-chain telemetry, while IT-telecom sectors move network functions to containers. The EU AI Act adds sector guidelines that vendors bake into industry clouds, prompting steady uptake. This vertical diversification bolsters resilience of the wider cloud native industry.

Geography Analysis

North America contributed 41.20% of revenue in 2025 thanks to early hyperscaler penetration, a dense startup ecosystem, and robust AI spending. Strong platform engineering communities accelerate knowledge sharing and tooling maturity. Federal guidance on secure software supply chains also reinforces demand for Kubernetes-centric DevSecOps.

Asia-Pacific is the fastest-growing region with 33.88% CAGR to 2031. Localisation mandates spur sovereign-cloud offerings and domestic provider growth. China’s market shows preference for Alibaba, Huawei, and Tencent, illustrating how policy shapes vendor mix. India, Indonesia, and Vietnam record double-digit expansion as digital-first initiatives leapfrog legacy infrastructure.

Europe benefits from GDPR and the EU AI Act, which push enterprises toward region-based data residency. AWS’s European Sovereign Cloud investment exemplifies hyperscaler adaptation. Middle East and Africa adopt cloud native to support digital transformation projects in finance, public services, and oil-and-gas, though infrastructure gaps slow progress in some countries.

Competitive Landscape

The cloud native market shows moderate concentration. AWS, Microsoft, and Google together hold 63% of the larger cloud infrastructure arena. Yet specialist vendors gain traction by focusing on platform engineering, WebAssembly, and industry-cloud blueprints. Oracle’s USD 30 billion annual contract pipeline highlights appetite for performance-optimised AI platforms.

Salesforce’s Data Cloud surpassed USD 1 billion ARR, confirming that data-centric services layered on Kubernetes drive incremental value. Venture capital supports niche innovators: Spectro Cloud raised USD 75 million to simplify fleet-scale Kubernetes, and wasmCloud graduated within CNCF, signalling community confidence.

Consolidation continues as large vendors buy specialised capabilities. IBM’s USD 6.4 billion HashiCorp deal adds infrastructure-as-code depth, while Red Hat ties platform services with AI. These moves tighten integration between software, services, and hardware, creating higher switching costs and enlarging the total addressable cloud native market.

Cloud Native Industry Leaders

Amazon.com, Inc.

Google LLC

International Business Machines Corporation (IBM)

Oracle Corporation

Alibaba Group Holding Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Oracle announced a cloud agreement expected to generate above USD 30 billion annually from FY2028, citing 100%+ MultiCloud database revenue growth.

- May 2025: Salesforce posted USD 9.8 billion revenue for Q1 FY2026, raised full-year guidance, and disclosed Data Cloud and AI ARR topping USD 1 billion.

- April 2025: Databricks secured USD 10 billion funding, lifting valuation to USD 62 billion and confirming demand for unified data and AI platforms.

- October 2024: Salesforce launched Agentforce, letting customers create autonomous AI agents to automate sales and service workflows.

Global Cloud Native Market Report Scope

Cloud native is the software approach of building, deploying, and managing modern applications in cloud computing environments. Modern companies want to build highly scalable, flexible, and resilient applications that they can update quickly to meet customer demands.

The cloud native market is segmented by component (platforms, services), by deployment (public cloud, private cloud, hybrid cloud), by enterprises (large enterprises, medium and small enterprises), by end-users (BFSI, IT and telecom, manufacturing, retail and e-commerce, healthcare, other end-users), by geography (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Platforms |

| Services |

| Public Cloud |

| Private Cloud |

| Hybrid / Multi-Cloud |

| Large Enterprises |

| Small and Medium-sized Enterprises (SMEs) |

| Banking, Financial Services and Insurance (BFSI) |

| Information Technology and Telecommunications |

| Manufacturing |

| Retail and E-Commerce |

| Healthcare and Life Sciences |

| Other Industries (Media, Government, Education, etc.) |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| UAE | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Component | Platforms | ||

| Services | |||

| By Deployment Model | Public Cloud | ||

| Private Cloud | |||

| Hybrid / Multi-Cloud | |||

| By Enterprise Size | Large Enterprises | ||

| Small and Medium-sized Enterprises (SMEs) | |||

| By End-user Industry | Banking, Financial Services and Insurance (BFSI) | ||

| Information Technology and Telecommunications | |||

| Manufacturing | |||

| Retail and E-Commerce | |||

| Healthcare and Life Sciences | |||

| Other Industries (Media, Government, Education, etc.) | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia and New Zealand | |||

| Southeast Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| UAE | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the cloud native market and its growth outlook?

The cloud native market stands at USD 14.59 billion in 2026 and is projected to climb to USD 51.38 billion by 2031, reflecting a 28.62% CAGR over 2026-2031

Why are generative-AI workloads so important for cloud native adoption?

Large language models need specialised GPU clusters that traditional virtualisation cannot support, driving enterprises toward container-based, Kubernetes-orchestrated architectures that scale inference efficiently

How does platform engineering differ from DevOps?

Platform engineering creates centrally managed self-service layers that abstract infrastructure, combining governance with developer autonomy. This organisational model now spans 55% of enterprises and is expanding rapidly

Which deployment model is growing the fastest?

Hybrid and multi-cloud configurations are the quickest-growing segment, expected to advance at 34.06% CAGR over 2026-2031 as firms seek workload portability and sovereignty compliance

What are the main obstacles slowing cloud native projects?

Hidden repatriation costs, a global shortage of cloud-security talent, and emerging localisation mandates can all delay or complicate roll-outs

Page last updated on: