Disposable Face Mask Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.69 Billion |

| Market Size (2031) | USD 2.97 Billion |

| Growth Rate (2026 - 2031) | 1.98% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Disposable Face Mask Market Analysis by Mordor Intelligence

The Disposable Face Mask Market size is expected to increase from USD 2.65 billion in 2025 to USD 2.69 billion in 2026 and reach USD 2.97 billion by 2031, growing at a CAGR of 1.98% over 2026-2031.

Stable institutional procurement by national stockpiles, reinforced workplace-safety rules, and standardized filtration tests are anchoring the Disposable face mask market in a post-pandemic equilibrium. Government reserve mandates convert what were once emergency purchases into recurring budget lines, while updated OSHA and CDC regulations keep employer demand intact.[1]Occupational Safety and Health Administration, “Respiratory Protection,” U.S. Department of Labor, osha.gov Material-cost swings in melt-blown polypropylene and tightening single-use-plastic legislation continue to influence pricing strategies, yet producers with vertically integrated resin capacity are better able to absorb volatility. E-commerce disintermediation, especially in Latin America and Southeast Asia, reshapes distribution economics by steering buyers toward lower-priced private-label stock-keeping units. Competitive pressure remains high as large multinationals exit commoditized masks, leaving a fragmented field dominated by Asian contract manufacturers.

Key Report Takeaways

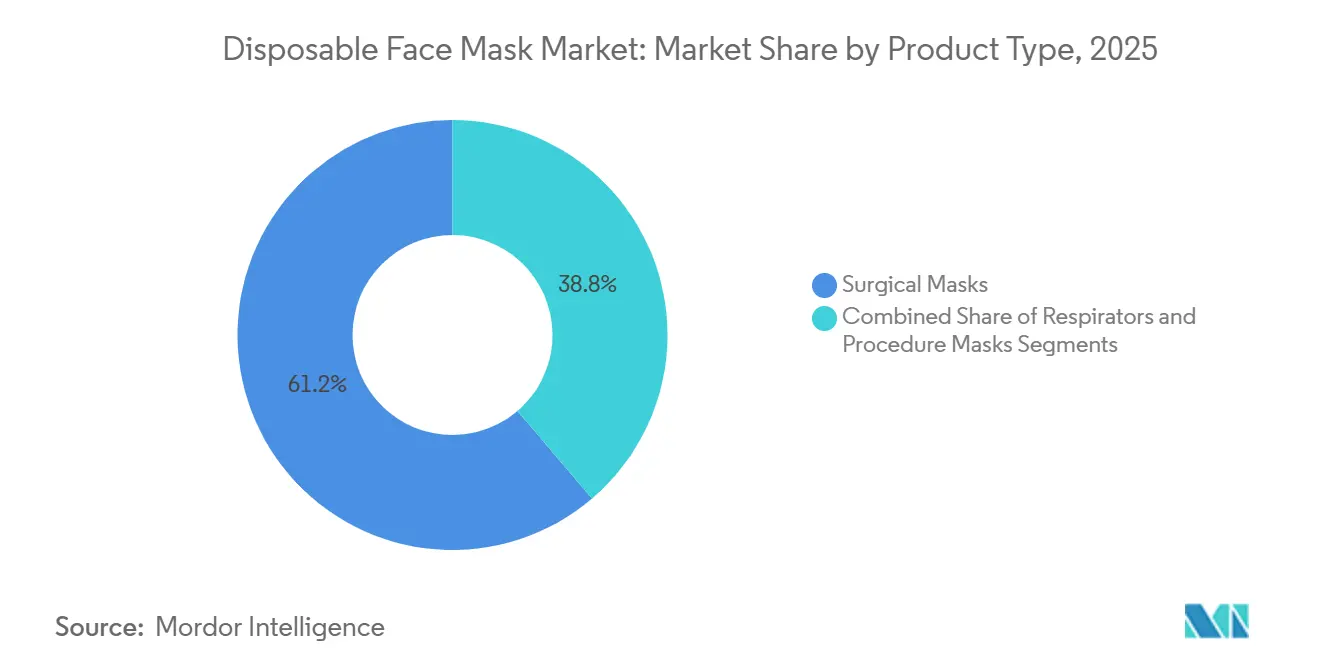

- By product type, surgical masks led with 61.24% revenue share in 2025, while respirators are projected to expand at a 4.42% CAGR through 2031.

- By material, melt-blown polypropylene accounted for 86.32% of 2025 value, whereas the “Others” category of bamboo, silk, and bioplastics is forecast to grow at a 5.53% CAGR over 2026-2031.

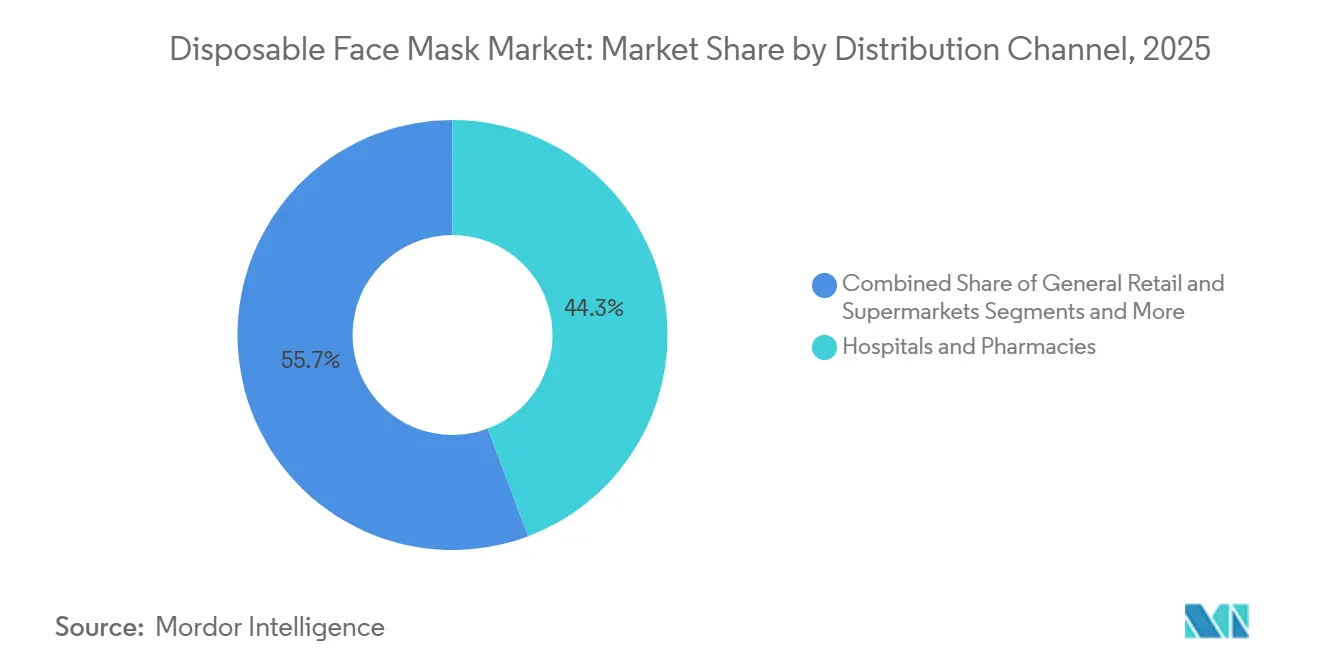

- By distribution channel, hospitals and pharmacies captured 44.26% of sales in 2025, yet online and direct-to-consumer outlets are advancing at a 6.03% CAGR to 2031.

- By user demographic, adults dominated with 81.67% of demand in 2025; the pediatric segment is expanding at a 3.13% CAGR through 2031.

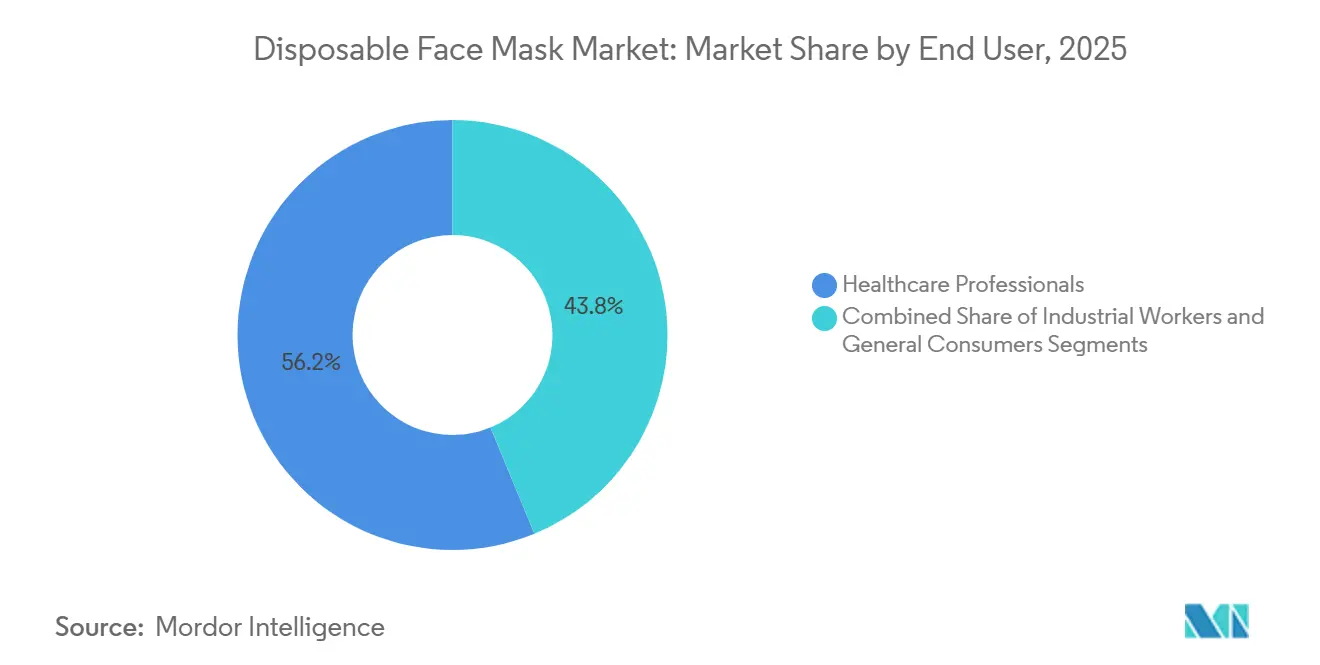

- By end user, healthcare professionals held 56.22% share in 2025, while industrial and construction workers represent the fastest-growing group at a 4.62% CAGR to 2031.

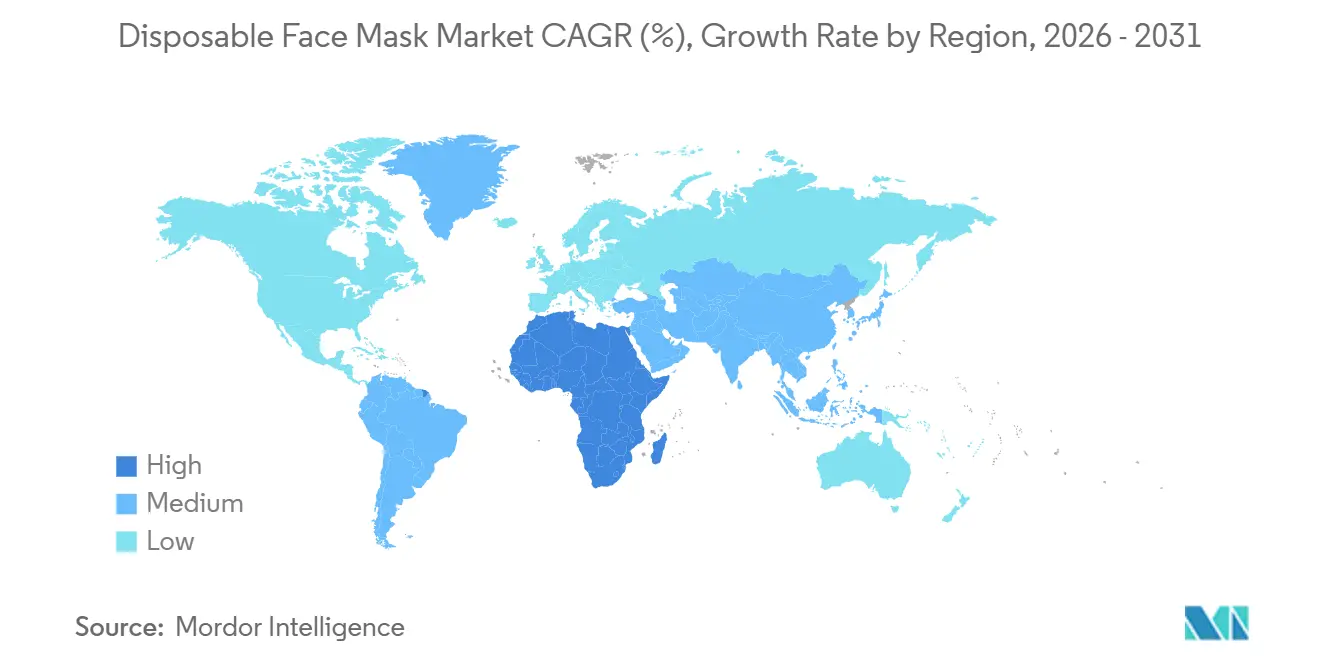

- By geography, Asia-Pacific led with 39.62% of 2025 value, and the Middle East & Africa region is on track for the highest growth at a 4.89% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Disposable Face Mask Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Post-COVID Pandemic Stockpiling by National Strategic Reserves | +0.4% | North America, Europe, APAC core | Long term (≥ 4 years) |

| Re-Institutionalization of Infection-Prevention Standards in Non-Acute Healthcare Settings | +0.3% | Global, with concentration in North America & EU | Medium term (2-4 years) |

| Mandated Use in Severe Seasonal Flu Outbreaks Across Asia | +0.3% | APAC core (China, Japan, South Korea, India) | Short term (≤ 2 years) |

| Corporate "Air-Quality First" ESG Commitments | +0.2% | Global, led by North America & EU multinationals | Medium term (2-4 years) |

| Rapid E-Commerce Private-Label Penetration in LATAM | +0.2% | South America (Brazil, Argentina, Mexico) | Short term (≤ 2 years) |

| WHO-Led Filtration-Test Standardization (ISO 16890, ASTM F3502) Triggers Mask-Replacement Cycles | +0.3% | Global, with early adoption in North America & EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Post-COVID Stockpiling by National Strategic Reserves

Federal agencies converted emergency buys into permanent rotation programs that guarantee multi-year respirator volumes. The United States Strategic National Stockpile held 350 million N95s in 2024, 26 times pre-2020 levels, while Canada’s vendor-managed model forces suppliers to backfill expiring lots.[2] Centers for Disease Control and Prevention, “Strategic National Stockpile,” cdc.gov Similar six-month supply buffers in Germany and France institutionalize base-line demand, particularly for certified respirators, and motivate manufacturers to maintain NIOSH-compliant production lines.

Re-Institutionalized Infection-Prevention in Non-Acute Healthcare Settings

CMS embedded documented mask policies into Medicare reimbursement rules for nursing homes in 2024, turning episodic mask use into a compliance requirement.[3]Centers for Medicare & Medicaid Services, “Infection Prevention and Control,” U.S. Department of Health and Human Services, cms.gov Outpatient dialysis centers and home-health agencies now purchase year-round stock, decoupling demand from public sentiment. Occupational health frameworks such as ISO 45001 further normalize respiratory protection across ancillary healthcare services.

Mandated Mask Use During Severe Seasonal Flu in Asia

Japanese, South Korean, Chinese, and Indian health ministries activate mask advisories whenever WHO flu surveillance flags elevated A(H3N2) prevalence. Because vaccination penetration remains low in several South-East Asian economies, governments find disposable masks a cost-effective prophylaxis, creating predictable Q3-Q4 procurement spikes.

Corporate “Air-Quality First” ESG Programs

Revised OSHA respiratory-protection rules issued in 2024 compel employers to fit-test staff facing particulate hazards, and many multinationals disclose compliance metrics in sustainability reports. Public companies subject to SEC and EU CSRD reporting treat mask provision as a tangible health-and-safety deliverable, locking annual volumes into operating budgets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-Material Cost Spikes for Melt-Blown Polypropylene | -0.3% | Global, with acute impact in APAC manufacturing hubs | Short term (≤ 2 years) |

| Saturation of Low-End SKUs Driving ASP Erosion | -0.2% | Global, most severe in APAC & South America | Medium term (2-4 years) |

| Legislative Clampdown on Single-Use Plastics in the EU & Canada | -0.2% | Europe, North America (Canada) | Long term (≥ 4 years) |

| Rise of Reusable Respirators & Biodegradable Mask Substitutes | -0.2% | North America, Europe, with spillover to APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Raw-Material Cost Spikes for Melt-Blown Polypropylene

Polypropylene prices averaged USD 1,378 per metric ton in Q4 2025, and smaller suppliers could not hedge feedstock exposure. Fixed-price government contracts squeeze margins during cost surges, discouraging long-term capacity investments outside vertically integrated firms.

Saturation of Low-End SKUs Drives ASP Erosion

Pandemic-era capacity expansions left a glut of procedure masks selling for USD 0.10-0.15 in bulk, barely above variable cost. Commodity producers face a volume-versus-margin dilemma that bifurcates the Disposable face mask market between certified respirators and undifferentiated low-end masks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Respirators Gain Ground in Certified Segments

Surgical masks captured 61.24% of Disposable face mask market share in 2025, while respirators are advancing at a 4.42% CAGR through 2031. Certified N95 and FFP2 devices command ASPs of USD 1.50-3.00, offering superior margin profiles that coax manufacturers to retool. OSHA fit-testing mandates reinforce the Disposable face mask market trend toward certified options, and ASTM F3502 provides an intermediate “Workplace Performance” tier for buyers who want better protection without full respirator protocols. Procedure masks retreat to cost-sensitive niches such as food service. Manufacturers capable of offering the entire certified-to-value continuum remain best positioned to capture shifting procurement patterns.

Second-order effects include the widening gap between brand-anchored respirators and commodity procedure masks. Companies with in-house melt-blown lines integrate vertically to control filtration media quality, while others outsource but differentiate through packaging or ear-loop comfort. Replacement cycles driven by standard updates ensure periodic demand spikes that benefit respirator portfolios, further tilting revenue mix toward certified SKUs.

By Material: Polypropylene Dominance Masks Emerging Alternatives

Melt-blown polypropylene held 86.32% of the Disposable face mask market size in 2025, owing to high filtration efficiency per cost unit. Yet bamboo fiber and PLA bioplastics are projected to scale at a 5.53% CAGR as EU recycling mandates steer R&D budgets into compostable substrates. Producers juggle the economics of premium-priced bioplastics against uncertain willingness-to-pay, targeting European tenders that value sustainability metrics. For now, polypropylene remains unmatched in electrostatic charge retention and breathability, but pilot electro-spinning lines for nanocellulose composites point to a measured diversification of raw-material risk.

Cost volatility further motivates diversification. Vertically integrated suppliers hedge feedstock swings by controlling refinery off-takes, whereas mid-tier firms pursue long-term resin contracts or lightweight mask designs that use less polypropylene per unit. In parallel, consumer brands tap into eco-conscious niches by blending PLA outer layers with conventional melt-blown cores, a hybrid approach that meets filtration thresholds while signaling environmental progress.

By Distribution Channel: E-Commerce Disrupts Traditional Retail

Hospitals and pharmacies retained a 44.26% revenue share in 2025, but online channels are registering a 6.03% CAGR to 2031 as Latin American and South-East Asian shoppers pivot to mobile marketplaces. Disposable face mask market dynamics favor platforms that bundle masks with related health items for free shipping thresholds. Subscription models create predictable monthly volumes for work-from-home consumers, while direct-to-consumer manufacturer sites reclaim 15-20% margin otherwise lost to wholesalers.

Brick-and-mortar outlets respond with value-added services such as on-site fit checks and immediate availability for urgent needs, yet foot traffic continues to drop outside acute outbreak windows. Pharmacies retain an advantage for regulated N95s when buyers require authenticity verification, but private-label imports erode price corridors. Future distribution strategies will hinge on last-mile logistics efficiency and real-time inventory visibility.

By User Demographics: Adult Segment Dominates, Pediatric Niche Expands

Adults generated 81.67% of Disposable face mask market demand in 2025. Pediatric masks, though smaller in absolute volume, are advancing at a 3.13% CAGR as schools and daycare centers integrate mask policies aligned with CDC congregate-setting guidance. Manufacturers confront design challenges related to seal integrity on small faces and must pass FDA pediatric device validation, raising barriers to entry.

The geriatric demographic grows steadily as long-term care facilities institutionalize infection-control protocols mandated by CMS, ensuring constant reorder cycles. Market segmentation by workplace role also shapes adult demand: healthcare and industrial masks require differing durability and breathability specs, enabling tiered product positioning.

By End User: Industrial Workers Emerge as Growth Segment

Healthcare professionals accounted for 56.22% of Disposable face mask market size in 2025, anchored by surgical-suite norms and airborne precaution guidelines. Industrial and construction users, driven by a 4.62% CAGR outlook, now procure certified respirators for dust and fume exposure after OSHA issued more than 1,200 citations in 2024. Consumer demand normalizes to lower baselines except in Asia-Pacific cultures with high voluntary mask adoption.

Institutional buyers in manufacturing increasingly specify reusable half-facepiece respirators for full-shift wear, reserving disposables for visitors and short tasks. This procurement mix change pressures disposable-only vendors and rewards firms with hybrid portfolios that include filter cartridges and cleaning supplies.

Geography Analysis

Asia-Pacific retained 39.62% of Disposable face mask market share in 2025, buoyed by domestic consumption in China, Japan, South Korea, and India and by the region’s export leadership. WHO flu advisories sustain periodic consumer spikes, while industrial demand climbs with large-scale infrastructure projects. Domestic manufacturers scale melt-blown capacity quickly, allowing rapid response to regional outbreaks and price changes.

North America stands as the second-largest market. The U.S. and Canada continue to fund strategic stockpiles that impose rolling replenishment schedules under vendor-managed inventory contracts. Mexico leverages nearshoring to supply polypropylene masks to U.S. buyers seeking diversification away from Asia. Yet emerging single-use-plastic rules in Canada foreshadow tighter scrutiny on non-medical disposables.

Europe’s demand is driven by EN 149 FFP2 adoption and sustainability legislation. Regulation 2025/40 requires high recycled content in consumer packaging, nudging R&D toward compostable masks. Fragmented national procurement encourages localized production, often supported by government grants aimed at strategic autonomy.

Middle East and Africa, the fastest-growing cluster at 4.89% CAGR, benefits from expanded GCC hospital networks and South African centralized tenders that stipulate ISO and ASTM compliance. Price sensitivity slows certified respirator adoption in sub-Saharan economies, but multilateral financing for pandemic preparedness is bridging the affordability gap.

South America experiences strong e-commerce penetration. Brazilian and Argentine online retailers push private-label masks that undercut pharmacy prices by up to 40%, fragmenting the Disposable face mask market landscape. Currency volatility and import duties complicate supply planning, yet favorable demographics keep baseline volumes resilient.

Competitive Landscape

The market reflects moderate fragmentation. Honeywell’s USD 1.325 billion sale of its PPE unit in November 2024 underlined how multinational conglomerates view masks as margin-dilutive. Solventum, spun out of 3M, posted USD 8.2 billion in 2024 sales but recorded USD 574 million in litigation accruals for respirator liability, revealing regulatory risk. Kimberly-Clark’s professional segment cited USD 5.1 billion in Q3 2024 revenue yet noted commodity input cost pressure.

Asian contract manufacturers, many vertically integrated into melt-blown fabric, compete on unit cost and speed, often supplying white-label inventory to Western distributors. European mid-size firms carve niches in biodegradable materials, while U.S. producers target domestic hospitals with supply-chain-resilience narratives. Barriers to entry center on NIOSH certification and sustained quality-control audits, insulating top respirator brands but leaving procedure mask segments open to new entrants.

Future competitive advantage will hinge on automation in sealing and packaging, regulatory affairs agility, and omnichannel distribution partnerships. Companies that can certify product lines to evolving ISO or ASTM standards in weeks rather than months will win institutional tenders tied to compliance milestones.

Disposable Face Mask Industry Leaders

Honeywell International Inc.

Kimberly-Clark Corporation

Owens & Minor Inc.

Alpha Pro Tech Ltd.

Solventum

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Honeywell sold its personal protective equipment business for USD 1.325 billion, exiting disposable masks to focus on automation and aerospace.

- January 2025: The European Union enacted Regulation 2025/40 on packaging waste, pushing mask suppliers to explore biodegradable materials despite current medical-device exemptions.

Global Disposable Face Mask Market Report Scope

As per the scope, a disposable face mask is a medical mask used by the population (mostly healthcare professionals) to cover and protect themselves from viruses and contaminants present in the environment that can cause infections.

The Disposable Face Mask Market Report is segmented by Product Type, Material, Distribution Channel, User Demographics, End User, and Geography. By Product Type, the market is segmented into Surgical Masks, Respirators, and Procedure Masks. By Material, the market is segmented into Melt‑blown Polypropylene, Cotton & Cellulose, and Others. By Distribution Channel, the market is segmented into Hospitals & Pharmacies, General Retail & Supermarkets, and Online & Direct‑to‑Consumer. By User Demographics, the market is segmented into Adult, Pediatric/Child, and Geriatric users. By End User, the market is segmented into Healthcare Professionals, Industrial/Construction Workers, and General Consumers. By Geography, the market is segmented into North America, Europe, Asia‑Pacific, Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. Market Forecasts are Provided in Terms of Value (USD).

| Surgical Masks |

| Respirators (N95/KN95/FFP2) |

| Procedure Masks |

| Melt-blown Polypropylene |

| Cotton & Cellulose |

| Others (Bamboo, Silk, Bioplastics) |

| Hospitals & Pharmacies (Offline) |

| General Retail & Supermarkets |

| Online & Direct-to-Consumer |

| Adult |

| Pediatric / Child |

| Geraitric |

| Healthcare Professionals |

| Industrial/Construction Workers |

| General Consumers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Surgical Masks | |

| Respirators (N95/KN95/FFP2) | ||

| Procedure Masks | ||

| By Material | Melt-blown Polypropylene | |

| Cotton & Cellulose | ||

| Others (Bamboo, Silk, Bioplastics) | ||

| By Distribution Channel | Hospitals & Pharmacies (Offline) | |

| General Retail & Supermarkets | ||

| Online & Direct-to-Consumer | ||

| By User Demographics | Adult | |

| Pediatric / Child | ||

| Geraitric | ||

| By End-User | Healthcare Professionals | |

| Industrial/Construction Workers | ||

| General Consumers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the Disposable face mask market in 2026?

It reached USD 2.69 billion in 2026 and is on track to hit USD 2.97 billion by 2031 at a 1.98% CAGR.

Which product segment is growing fastest?

Certified respirators such as N95, KN95, and FFP2 devices show the highest growth at a 4.42% CAGR through 2031.

What region leads demand today?

Asia-Pacific holds the largest share at 39.62% thanks to dense populations, local manufacturing capacity, and cultural mask acceptance.

Why are polypropylene prices critical for producers?

Melt-blown polypropylene accounts for up to 80% of unit material cost, so feedstock volatility directly affects margins.

How is e-commerce changing distribution?

Online and direct-to-consumer channels are expanding at a 6.03% CAGR as platforms in Latin America and South-East Asia undercut traditional retail prices.

Are sustainability regulations influencing the market?

Yes, EU and Canadian single-use-plastic laws are pushing suppliers to trial biodegradable fibers, adding cost but opening new premium niches.

Page last updated on: