Medical Filters Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 6.68 Billion |

| Market Size (2031) | USD 9.55 Billion |

| Growth Rate (2026 - 2031) | 7.41% CAGR |

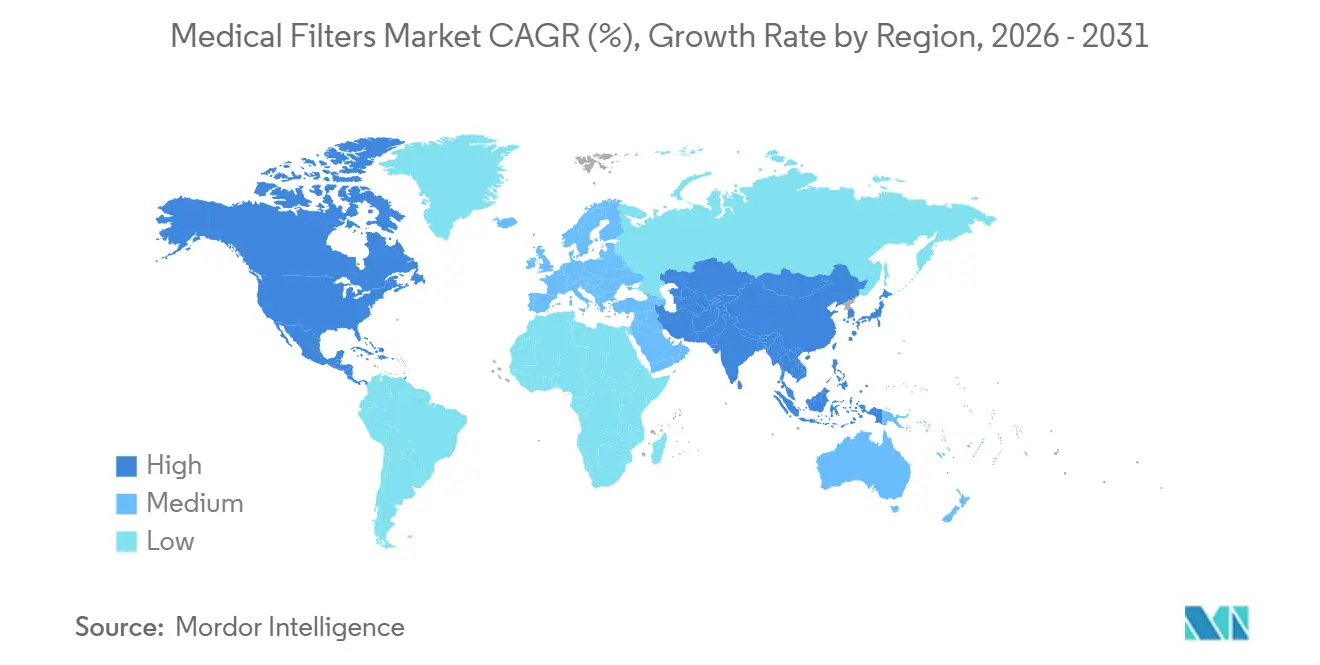

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

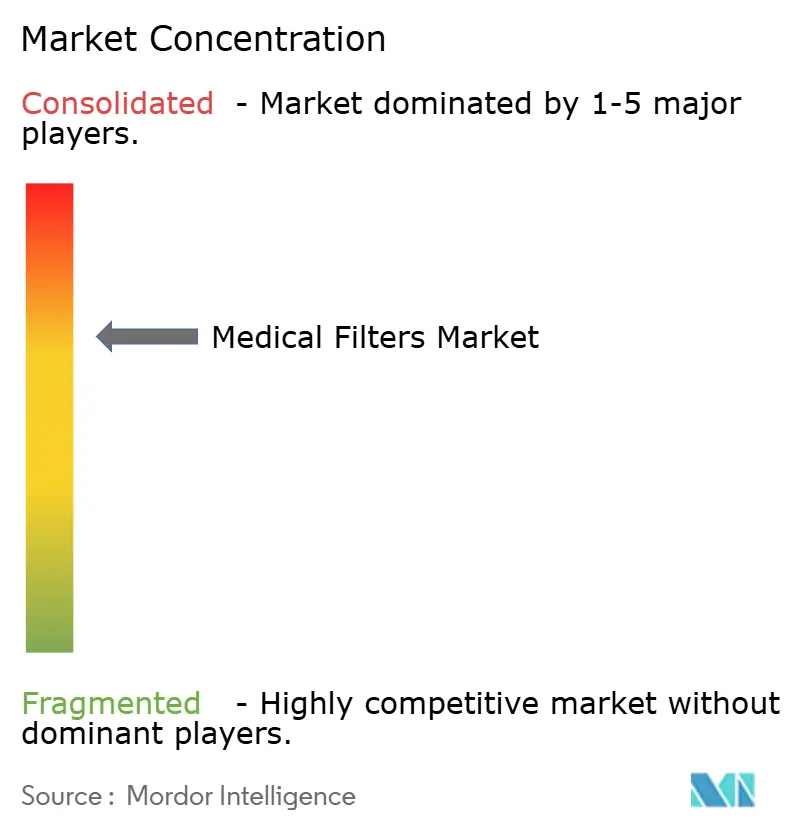

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Medical Filters Market Analysis by Mordor Intelligence

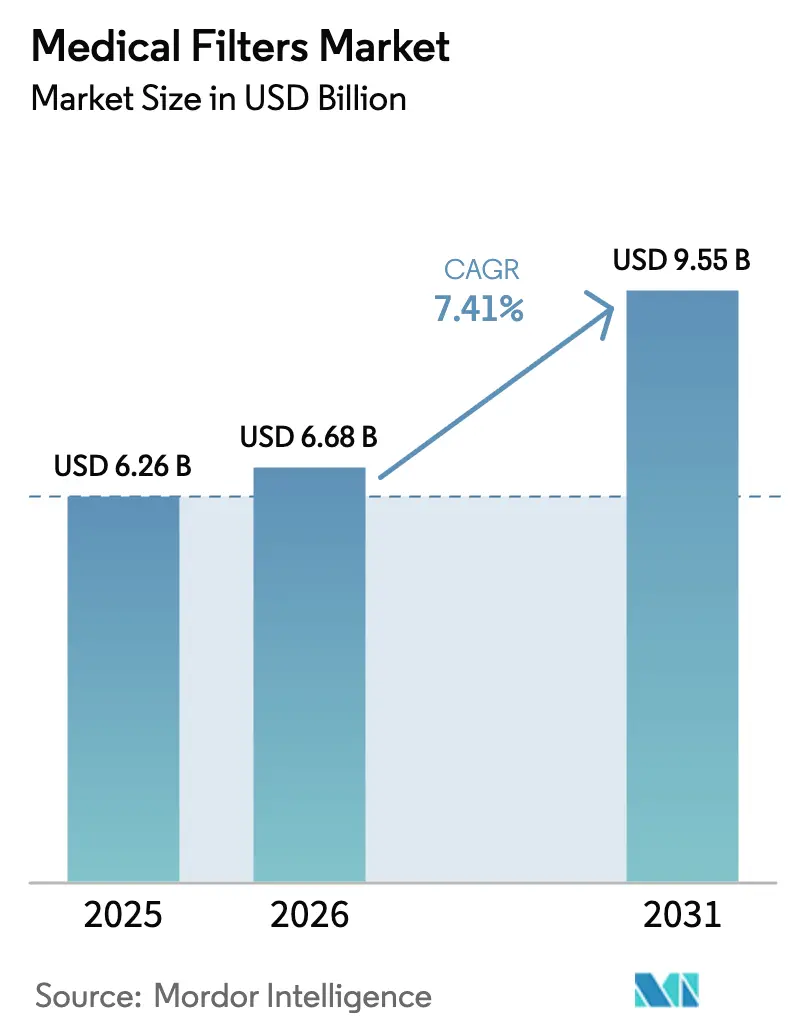

The medical filters market size is projected to expand from USD 6.26 billion in 2025 and estimated to USD 6.68 billion in 2026 to USD 9.55 billion by 2031, registering a CAGR of 7.41% between 2026 to 2031. Solid demand stems from the convergence of chronic disease prevalence, stringent infection-control mandates, and steady advances in membrane science. Hospitals, pharmaceutical manufacturers, and an expanding base of home-care users are collectively raising order volumes for high-performance liquid, air, and gas filters. Post-pandemic ventilation standards have redirected capital budgets toward HVAC retrofits, while dialysis clinics and biologics plants continue to prioritize ultrafiltration modules that safeguard patient safety and batch integrity. Technology suppliers are answering with composite membranes that resist fouling, embedded sensors that predict end of life, and disposable formats that eliminate reprocessing labor. On the competitive front, vertically integrated multinationals leverage in-house membrane casting to retain pharmaceutical contracts, yet regional specialists continue to undercut on commodity SKUs, especially across Asia-Pacific.

Key Report Takeaways

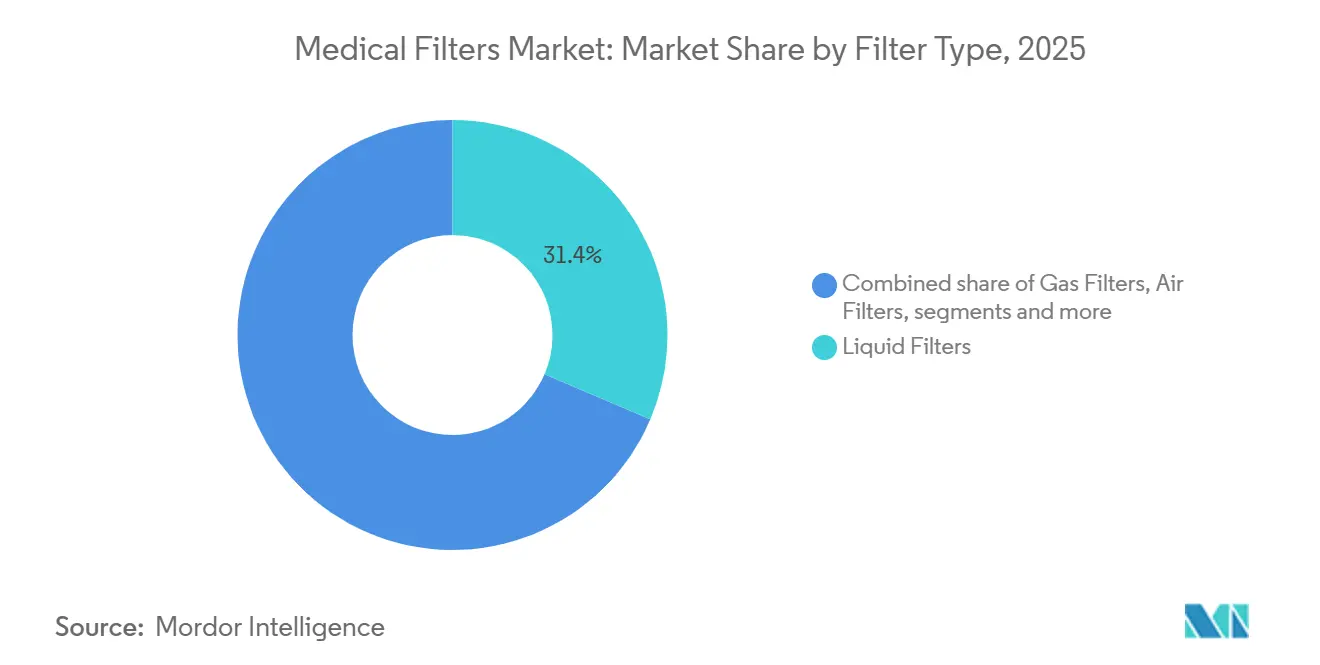

- By filter type, liquid filters captured 31.43% revenue share in 2025, whereas air filters are advancing at an 8.66% CAGR through 2031.

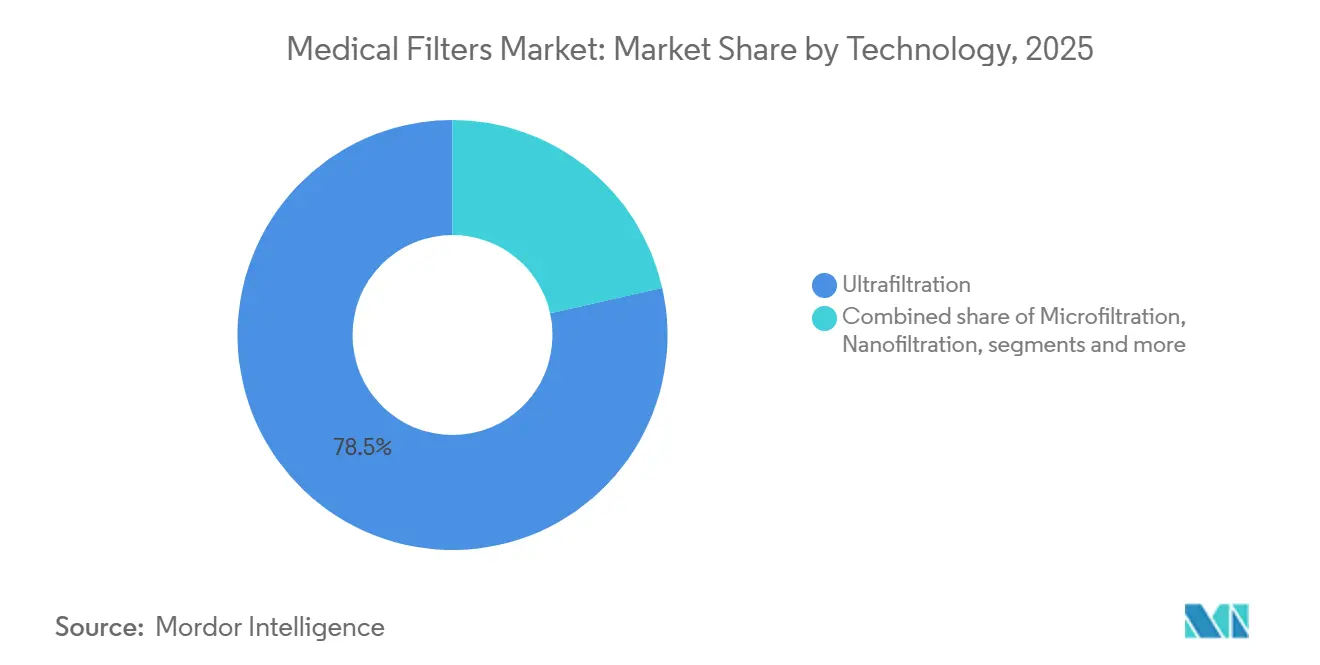

- By technology, ultrafiltration commanded 78.51% of the medical filters market share in 2025, while nanofiltration is growing at a 10.13% CAGR to 2031.

- By application, hospitals and clinics held 37.61% share in 2025 and home healthcare is expanding at a 9.01% CAGR through 2031.

- By material, polymer filters accounted for 74.47% of the medical filters market size in 2025 and composite filters are rising at a 9.74% CAGR to 2031.

- By usage, disposable filters represented 57.24% share in 2025, with the category progressing at an 8.02% CAGR to 2031.

- By geography, North America led with 42.10% revenue share in 2025, while Asia-Pacific is forecast to post an 8.43% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Medical Filters Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Incidence of Chronic Diseases | +1.80% | Global, with peaks in North America and Europe | Long term (≥ 4 years) |

| Stringent Infection Control Regulations | +1.50% | North America, Europe, APAC core | Medium term (2–4 years) |

| Technological Advancements in Filter Materials | +1.30% | Global | Medium term (2–4 years) |

| Growth in Medical Device Usage | +1.20% | APAC core with spill-over to MEA and South America | Long term (≥ 4 years) |

| Integration of Smart Technologies | +0.90% | North America, Europe, early APAC adopters | Short term (≤ 2 years) |

| Post-COVID Emphasis on Air Quality | +0.70% | Global, with regulatory push in North America and EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of Chronic Diseases

Global diabetes and end-stage renal disease trends are lifting demand for blood and dialysis filtration modules. The International Diabetes Federation counted 589 million adults living with diabetes in 2024 and projects 853 million by 2050[1]International Diabetes Federation, “IDF Diabetes Atlas 10th Edition,” idf.org. Each hemodialysis patient averages 156 treatments annually, and every session consumes a high-flux polysulfone filter, which stabilizes supplier cash flows across economic cycles. Cardiovascular procedures are another pull-through segment; the American Heart Association reported more than 1 million percutaneous coronary interventions in the United States in 2024, each using inline blood filters to capture microemboli. Home-based peritoneal dialysis advanced 12% year on year in 2025, spawning a market for compact single-use cartridges that patients can manage without clinical oversight. Collectively, these factors keep the medical filters market on a steady upward trajectory.

Stringent Infection Control Regulations

Revised surgical air-change guidelines require 20 air changes per hour in operating theatres with 99.97% HEPA efficiency at 0.3 microns, as documented in ASHRAE 170 (2024). Compliance audits by The Joint Commission are compelling hospitals to retrofit HVAC decks with electrostatic pre-filters and ULPA terminal stages, setting off a three-to-five-year replacement cadence. Water systems face similar scrutiny; the EU Drinking Water Directive now mandates Legionella monitoring, pushing facilities to install 0.01-micron ultrafiltration cartridges at outlets. Pharmaceutical producers must validate 0.2-micron sterilizing-grade filters under FDA sterile-drug guidance, and every lot release requires bacterial challenge and integrity testing. Together these rules amplify recurring demand for high-specification filtration products.

Technological Advancements in Filter Materials

Composite membranes that pair a ceramic backbone with a polymer selective layer now last 40% to 50% longer than monolithic polymer cartridges, cutting total cost of ownership for dialysis chains. Zwitterionic-coated polyethersulfone, commercialized in 2025 under Sartorius Hydrosart, lowers protein fouling and keeps flux stable in monoclonal antibody purification campaigns. Electrospun nanofiber mats under 200 nanometers are being laminated into surgical masks to trap sub-micron aerosols while keeping breath resistance low, a feature important for operating room staff. Graphene-oxide coatings are entering extracorporeal circuits where antimicrobial activity reduces biofilm formation, and metal-fiber filters sintered from stainless steel survive hundreds of autoclave cycles without dimensional creep. These innovations upgrade performance benchmarks and enlarge the addressable medical filters market.

Post-COVID Emphasis on Air Quality

The pandemic elevated awareness of airborne transmission, prompting revisions to ventilation standards in healthcare facilities, schools, and commercial buildings. ASHRAE updated its Position Document on Infectious Aerosols in 2024, recommending MERV 13 or higher filtration in all air-handling units serving occupied spaces, a shift from the previous MERV 8 baseline. Hospitals are retrofitting operating rooms with HEPA filters rated to capture 99.97% of particles at 0.3 microns, and installing UV-C germicidal irradiation modules downstream of filters to inactivate any pathogens that penetrate the media, a dual-barrier approach that Camfil commercialized in its ProSafe line during 2025. Portable air purifiers equipped with medical-grade HEPA filters saw a 60% increase in hospital procurement between 2024 and 2025, deployed in isolation rooms, emergency departments, and outpatient clinics to supplement central HVAC systems. The U.S. Centers for Disease Control and Prevention issued guidance in 2024 recommending 6 to 12 air changes per hour in patient rooms, up from the previous 2 to 6 range, a mandate that is accelerating filter-replacement cycles and boosting demand for high-capacity pleated designs that minimize pressure drop[2]Centers for Disease Control and Prevention, “Airborne Infection Isolation Guidelines 2024,” cdc.gov.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Maintenance & Operational Costs | −0.8% | Global, with acute pressure in emerging markets | Medium term (2–4 years) |

| Complex Regulatory Compliance | −0.6% | North America, Europe, with expansion to APAC | Long term (≥ 4 years) |

| Limited Penetration in Emerging Markets | −0.5% | MEA, South America, rural APAC | Long term (≥ 4 years) |

| Compatibility Challenges with Legacy Systems | −0.4% | Global, where infrastructure is aging | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

High Maintenance & Operational Costs

Reusable stainless-steel housings demand validated cleaning cycles that consume up to six labor hours per unit, costing a mid-sized 20-station dialysis center more than USD 15,000 annually. Disposable designs eliminate cleaning but shift expenses to consumables; each hemodialysis patient spends about USD 1,900 per year on single-use cartridges. High-efficiency HVAC filters raise fan energy draw by 15% to 20%, inflating utility bills in high-tariff regions such as Germany and Japan. Capital outlays for variable speed drives or demand-controlled ventilation exceed USD 500,000 per hospital. Pharmaceutical processors also incur downtime for backwashing or chemical clean-in-place when running continuous campaigns, cutting net production capacity by up to 15%. These factors compress operating margins and moderate adoption among cost-sensitive buyers.

Complex Regulatory Compliance

Medical-filter makers must navigate FDA 510(k) submissions that require predicate comparisons, ISO 10993 biocompatibility, and bacteriostatic validation, often taking 12–18 months and USD 200,000–400,000 in testing fees. Europe’s MDR 2017/745 adds clinical-evidence requirements and frequent notified-body audits, delaying launches by another six to twelve months. China’s NMPA demands domestic clinical trials for novel membranes, extending timelines by up to three years. Limited mutual recognition among regulators forces repeat testing and documentation across jurisdictions. On market entry, post-market surveillance absorbs 5% to 8% of annual revenue for mid-tier manufacturers. The burden narrows the competitive field to firms with deep regulatory budgets, dampening innovation velocity for smaller challengers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Filter Type: Liquid Share Remains High while Air Segments Accelerate

Liquid filters dominated the medical filters market size with 31.43% share in 2025 as dialysis, intravenous therapy, and pharmaceutical water systems depend on high-throughput modules. Air filters are climbing at an 8.66% CAGR to 2031 as post-pandemic ventilation rules spur HVAC retrofits across operating suites and ICUs. Dialysis cartridges now employ 1.5–2.1 square-meter hollow fibers engineered for enhanced hydrophilicity that reduce clot formation. Surgical filters are shifting to single-use designs that trim cross-contamination risks, a strategy showcased by Medtronic when it phased out reusable anesthesia filters in 2024. Meanwhile, gas filters used in respiratory therapy integrate activated-carbon layers to adsorb volatile anesthetics, lowering the need for separate scavenging systems. Air filters for HVAC service are adopting pleated media that pack 50% more surface area into standard frames, cutting pressure drop and doubling service life. The line between modalities blurs as suppliers bundle liquid and air modules into modular operating-theatre skids, an integrative approach that expands addressable revenue per project.

Operational efficiencies and infection-control demands encourage hospitals to synchronize replacement cycles, which strengthens vendor relationships and raises switching costs. Commodity liquid filter producers face price pressure from regional manufacturers in Asia; however, high-spec air filters with ULPA performance retain premium margins. As ventilation codes tighten across emerging economies, air-filter growth could narrow the revenue gap with liquid modules, reshaping the medical filters market hierarchy.

By Application: Hospitals Continue to Anchor while Home Care Gains Momentum

Hospitals and clinics generated 37.61% of 2025 demand, backed by a vast installed base of capital equipment and continuous procurement of consumables. At the same time, home-care demand is rising at a 9.01% CAGR as portable dialysis devices, oxygen concentrators, and infusion pumps migrate chronic disease management into residential environments. Laboratory demand remains robust as diagnostic labs pursue ultrapure water fed through multi-stage filtration trains to meet CLSI reagent standards. Pharmaceutical manufacturers enforce zero-defect requirements, and any single integrity-test failure can force batch rejection, which places a premium on brand-name filters with extensive validation histories. Medicare expanded reimbursement for home hemodialysis in 2024, offering a USD 271.02 per-session premium for connected devices, which accelerates uptake of cartridge-based systems featuring in-situ sensor feedback[3]Centers for Medicare & Medicaid Services, “End Stage Renal Disease Prospective Payment System Final Rule 2024,” cms.gov.

Medical gas and infusion device adoption also lifts aftermarket volumes; each infusion pump cycles through four to six filters per admission. Hospitals extend filtration beyond clinical wards, installing cartridges in cafeterias, laundries, and potable-water dispensers, broadening consumption profiles per facility. With aging populations and remote monitoring technologies proliferating, the medical filters market sees home care evolving from a niche into a strategic channel that could rival institutional demand over the next decade.

By Material: Polymer Dominance Faces Composite Advancements

Polymer membranes captured 74.47% share in 2025, owing to their balanced chemistry, broad compatibility, and cost advantages. Polyethersulfone ultrafiltration remains the backbone for dialysis and protein concentration, aided by zwitterionic surface treatments that deter fouling. Hydrophobic polyvinylidene fluoride leads in air-filter builds where moisture repellency keeps media rigid under variable humidity. Glass-fiber remains critical for HEPA assemblies that must secure 99.97% removal efficiency at 0.3 microns. Composite filters are the fastest climbers at a 9.74% CAGR, as hybrid ceramic-polymer laminates extend service life in dialysis circuits by nearly half, lowering downtime and cartridge rotations. Metal-fiber sintered varieties hold a niche in reusable surgical instrumentation trays thanks to resilience under 134 °C autoclave cycles.

Sustainability mandates emerging in Europe favor filter housings that enable easier material separation and recycling. Suppliers now prototype blends that combine renewable polymer layers bonded to ceramic cores, lowering plastic mass while improving durability. These developments gradually chip away at polymer dominance, especially in premium applications, ensuring that material innovation remains a lively battleground within the medical filters market.

By Technology: Ultrafiltration Governs yet Nanofiltration Scales Quickly

Ultrafiltration controlled 78.51% of 2025 revenue thanks to cross-functional use in dialysis, bioprocessing, and potable-water conditioning. Systems operate at moderate transmembrane pressures yet achieve virus reduction and protein fractionation, granting them universal appeal for healthcare settings. Nanofiltration, while smaller in base, is growing at a 10.13% CAGR, prized for molecular-weight cutoffs between 200 and 1,000 daltons that align with gene therapy and precision medicine purification needs. Microfiltration remains ubiquitous for cell debris removal, operating at lower pressures of 5–15 psi, which suits budget-sensitive contract manufacturers. Reverse osmosis has re-emerged in dialysis centers to soften feed water and minimize downstream scaling.

Electrostatic media using charged fibers enable surgical masks and anesthesia circuits to capture sub-micron aerosols at low airflow resistance, making headway in personal protective equipment. Hybrid cascades combining micro, ultra, and nanofiltration stages are now standard in biopharmaceutical plants, where each layer targets a distinct contaminant category to secure GMP compliance. These cascades create multi-module purchase orders and reinforce long-term service contracts, further enlarging the medical filters market size.

By Usage: Disposable Units Advance while Reusable Designs Hold Strategic Niches

Disposable cartridges accounted for 57.24% of 2025 demand and are expanding at an 8.02% CAGR through 2031 because infection-prevention protocols disfavor reprocessing. The FDA tightened reprocessing guidance in 2024, after which many hospitals phased out on-site sterilization of single-use devices. Disposable anesthesia-circuit filters became the baseline, and ventilator manufacturers removed reusable SKUs from catalogs. Pharmaceutical producers still purchase stainless-steel housings validated for up to 1,000 steam-in-place cycles, which cuts per-batch cost by roughly two-thirds over disposable equivalents in high-volume lines. Sartorius offers hybrid capsules with disposable membrane cores inside reusable shells as a mid-path that shrinks waste volumes without compromising turnaround speed.

Environmental policy is beginning to influence future purchasing patterns. The European Union proposed a Medical Device Waste Directive for 2027 that would impose extended producer responsibility, potentially adding 2%–4% to the factory cost of disposables. Scandinavian hospitals are piloting take-back schemes where filter frames are recycled and contaminated media is incinerated under controlled conditions. Should such programs scale, they could narrow ownership-cost gaps and keep reusable options viable in selected service lines of the medical filters industry.

Geography Analysis

North America commanded 42.10% of 2025 revenue, backed by high per-capita healthcare expenditure, an extensive dialysis clinic network, and forceful FDA oversight. More than 7,500 U.S. dialysis centers serve 550,000 patients, each scheduling three to four filter swaps per week, creating predictable demand. Canada uses group purchasing organizations to lock in volume contracts that favor suppliers able to bundle technical support and staff training. Mexico is evolving into a manufacturing base for disposable cartridges, capitalizing on nearshore logistics. The FDA’s 2024 update on bacterial endotoxin thresholds compelled firms to reformulate membrane chemistries, temporarily constraining inventory and lifting average selling prices by 8%–12% during early 2025.

Asia-Pacific is the fastest riser at an 8.43% CAGR to 2031, powered by policy-driven investments in China, India, and Southeast Asia. China earmarked USD 12 billion in 2025 to upgrade county hospitals, explicitly funding HVAC retrofits with HEPA assemblies and water systems meeting Chinese Pharmacopoeia purity rules. India’s Ayushman Bharat scheme reimburses dialysis treatments, making home peritoneal dialysis financially viable and catalyzing filter demand. Japan’s aging profile elevates home-care device uptake; its Long-Term Care Insurance scheme subsidizes rental of oxygen concentrators and portable dialysis machines that incorporate disposable filters. South Korea’s biotechnology cluster channels orders toward single-use systems to cut changeover time in biologics plants, deepening penetration of advanced filtration technologies.

Europe retains a sizable piece of the medical filters market despite slower growth. Germany enforces DIN hospital air standards requiring quarterly integrity checks, ensuring recurring sales. The UK National Health Service pilots value-based procurement that rewards suppliers delivering lower lifecycle costs. France, Spain, and Italy follow similar pathways yet face budget ceilings under public health financing. Middle East and Africa register uneven progress; the United Arab Emirates opened three dialysis centers in 2025 fully equipped with reverse-osmosis pre-treatment and ultrafiltration modules, while South Africa’s private chains retrofit operating suites with ULPA media to win international accreditation. South American momentum is hindered by economic volatility, yet Brazil’s SUS system broadens dialysis coverage, and Argentina mandated bacterial filters on ICU ventilators in 2024, prompting incremental imports despite currency headwinds.

Competitive Landscape

The medical filters market shows moderate concentration. The five largest players—Danaher’s Pall division, Sartorius, Thermo Fisher Scientific, Merck KGaA, and Freudenberg—control a significant share of global revenue, yet a long tail of regional specialists keeps pricing competitive in commodity microfiltration and HVAC pre-filter lines. Vertical integration is pivotal; Danaher operates membrane casting, converter lines, and application labs that co-engineer solutions with pharmaceutical clients, which anchors multi-year supply contracts. Sartorius chairs ISO/TC 198 workgroups that define sterilizing-grade test methods, subtly steering standards toward its Sartopore architecture.

Regional challengers in Asia offer 20%–30% price discounts for commodity cartridges, prompting multinationals to differentiate through digital features, faster lead times, and validation support. Sensor-enabled products such as Pentair’s predictive-maintenance platform cut unplanned downtime by up to 20%, adding service-based revenue streams that soften price pressure. Sustainability emerges as a competitive wedge; Camfil and Freudenberg operate take-back programs and supply recycled-content media, earning extra points under European public procurement rules. White-space opportunities are forming around lab-on-a-chip diagnostics and wearable artificial kidneys, where filter requirements diverge sharply from legacy devices, giving innovators room to carve new niches.

Overall, top suppliers continue to consolidate through M&A, while still facing agile newcomers in select geographies and product corridors. The balance yields steady innovation without tipping the market into extreme concentration, sustaining healthy rivalry that ultimately benefits end users through continuous performance gains and lifecycle-cost reductions.

Medical Filters Industry Leaders

Danaher Corporation

Freudenberg Filtration Technologies GmbH & Co. KG

Merck KGaA

Sartorius AG

Thermo Fisher Scientific Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Camfil acquired F.C.R., an Italian company specializing in air filtration solutions. The acquisition expands Camfil’s presence in Italy and strengthens its ability to serve customers with reliable, energy‑efficient solutions for cleaner air.

- November 2025: Nephros signed a license and supply agreement with Medica S.p.A. covering ultrafiltration technology for medical applications.

- October 2025: Merck KGaA bought the chromatography business of JSR Life Sciences, enhancing its downstream processing capabilities for monoclonal antibody production.

- September 2025: Merck KGaA announced a EUR 150 million filter manufacturing facility in Cork, Ireland, adding 3,000 square meters of cleanroom space to serve global demand for critical filtration products.

Global Medical Filters Market Report Scope

According to the report's scope, the medical filters market refers to the global industry focused on the design, manufacturing, and distribution of filtration devices and systems used in healthcare settings to remove contaminants, particulates, microorganisms, and unwanted substances from gases, liquids, and biological fluids. These filters are critical for infection control, patient safety, and ensuring the purity of medical processes and products.

The medical filters market is segmented by filter type, application, material, technology, usage, and geography. By filter type, the market is segmented into gas filters, liquid filters, air filters, blood filters, dialysis filters, and surgical filters. By application, the market is segmented into hospitals and clinics, diagnostic laboratories, home healthcare, pharmaceuticals, and others. By material, the market is segmented into polymer filters (PES, PVDF, PTFE), metal filters, ceramic filters, composite filters, and glass filters. By technology, the market is segmented into microfiltration, ultrafiltration, nanofiltration, reverse osmosis, and electrostatic filters. By usage, the market is segmented into disposable and reusable. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers values (USD) for all the above segments.

| Gas Filters |

| Liquid Filters |

| Air Filters |

| Blood Filters |

| Dialysis Filters |

| Surgical Filters |

| Hospitals and Clinics |

| Diagnostic Laboratories |

| Home Healthcare |

| Pharmaceuticals |

| Others |

| Polymer Filters (PES, PVDF, PTFE) |

| Metal Filters |

| Ceramic Filters |

| Composite Filters |

| Glass Filters |

| Microfiltration |

| Ultrafiltration |

| Nanofiltration |

| Reverse Osmosis |

| Electrostatic Filters |

| Disposable |

| Reusable |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Filter Type | Gas Filters | |

| Liquid Filters | ||

| Air Filters | ||

| Blood Filters | ||

| Dialysis Filters | ||

| Surgical Filters | ||

| By Application | Hospitals and Clinics | |

| Diagnostic Laboratories | ||

| Home Healthcare | ||

| Pharmaceuticals | ||

| Others | ||

| By Material | Polymer Filters (PES, PVDF, PTFE) | |

| Metal Filters | ||

| Ceramic Filters | ||

| Composite Filters | ||

| Glass Filters | ||

| By Technology | Microfiltration | |

| Ultrafiltration | ||

| Nanofiltration | ||

| Reverse Osmosis | ||

| Electrostatic Filters | ||

| By Usage | Disposable | |

| Reusable | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the medical filters market today?

The medical filters market size is USD 6.68 billion in 2026 and it is projected to reach USD 9.55 billion by 2031.

What is the forecast growth rate for medical filters through 2031?

Between 2026 and 2031 the market is forecast to grow at a 7.41% CAGR.

Which filter technology currently holds the largest share?

Ultrafiltration leads with 78.51% revenue share in 2025 due to its versatility in dialysis and bioprocessing.

Which region is growing the fastest for medical filtration products?

Asia-Pacific is expanding at an 8.43% CAGR through 2031 on the back of healthcare infrastructure investments in China and India.

Are disposable or reusable filters gaining traction?

Disposable units dominate with 57.24% share and are advancing at an 8.02% CAGR, driven by infection-control priorities.

Page last updated on: