U.S. Healthcare Personal Protective Equipment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

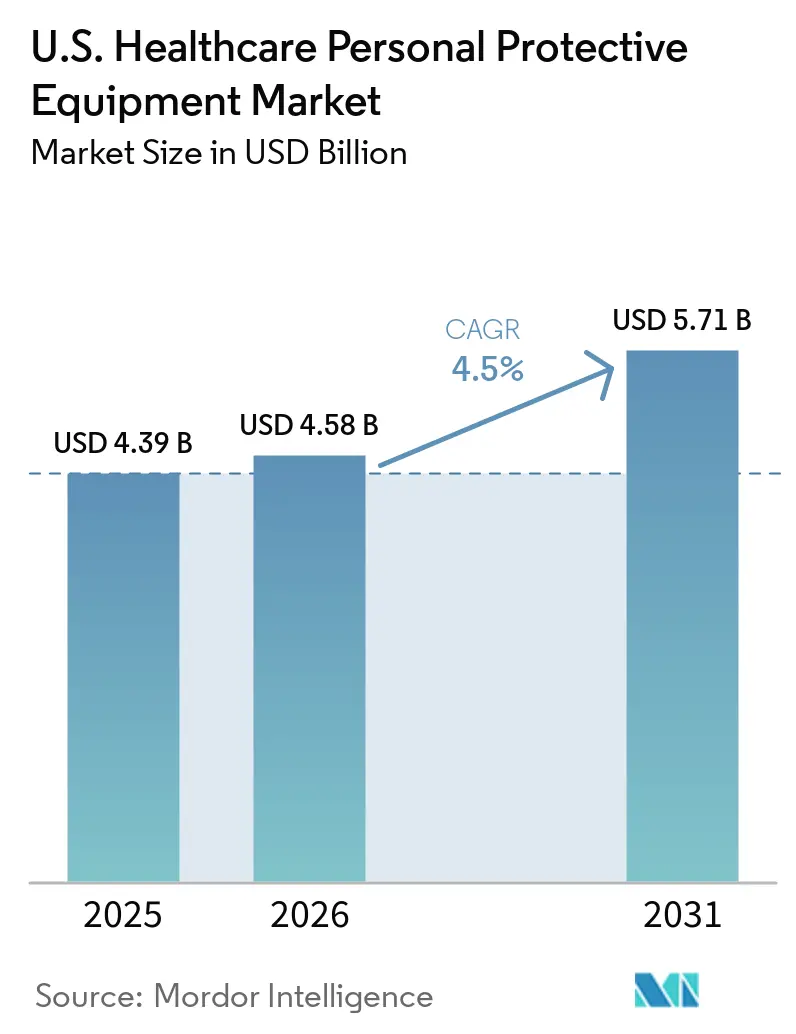

| Base Year Market Size (2025) | USD 4.39 Billion |

| Market Size (2026) | USD 4.58 Billion |

| Market Size (2031) | USD 5.71 Billion |

| Growth Rate (2026 - 2031) | 4.50% CAGR |

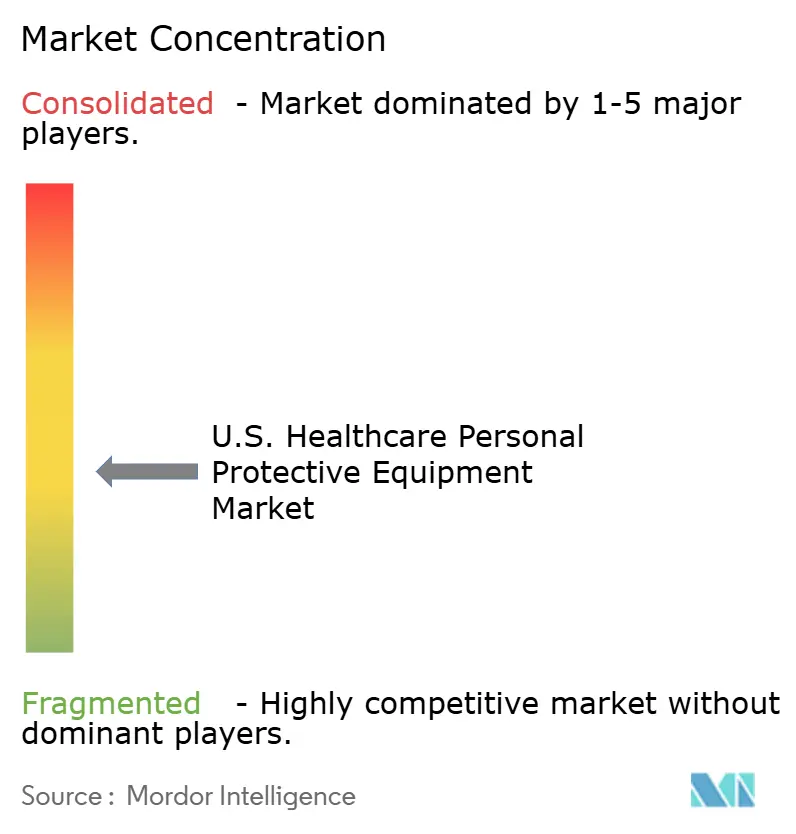

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

U.S. Healthcare Personal Protective Equipment Market Analysis by Mordor Intelligence

The U.S. Healthcare Personal Protective Equipment Market size is projected to be USD 4.39 billion in 2025, USD 4.58 billion in 2026, and reach USD 5.71 billion by 2031, growing at a CAGR of 4.5% from 2026 to 2031.

The U.S. healthcare PPE market is undergoing a reset as pandemic-driven volume surges have normalized, but long-term clinical demand remains strong. A significant policy shift is influencing purchasing behavior, with a CMS proposal requiring Medicare-participating hospitals to source 25% to 75% of PPE from domestic manufacturers under the Secure American Medical Supplies designation starting January 2026. This policy is expected to drive structural cost changes, as domestic nitrile gloves are priced 1.5 to 3 times higher than imported alternatives.[1]Centers for Medicare & Medicaid Services, “Medicare Program, Ensuring Safety Through Domestic Security With Made in America Personal Protective Equipment (PPE) and Essential Medicine Procurement by Medicare Participating Hospitals,” Federal Register, federalregister.gov Additionally, steady demand for infection prevention, driven by the ongoing burden of healthcare-associated infections in U.S. hospitals, continues to support the market. Compliance requirements, procurement policy changes, and a shift toward higher-specification products are key factors sustaining growth in the U.S. healthcare PPE market.

Key Report Takeaways

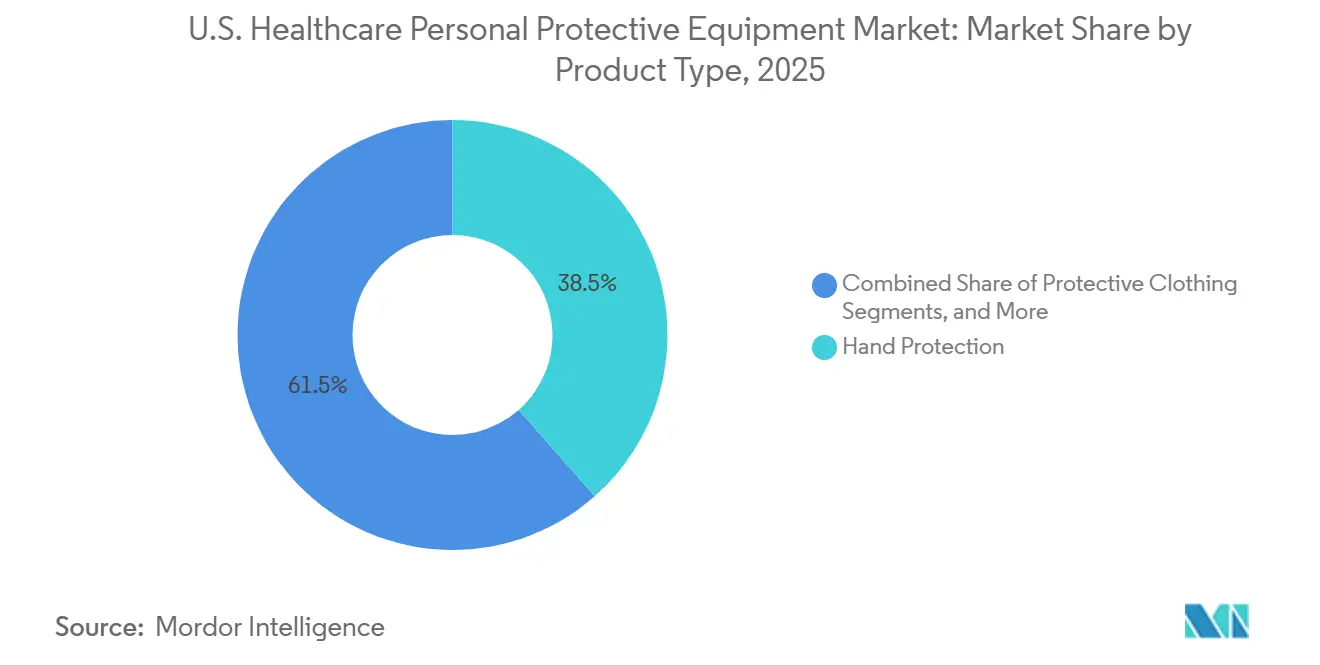

- By product type, hand protection held 38.50% of the U.S. healthcare PPE market size in 2025, while protective clothing is projected to expand at a 5.10% CAGR through 2031.

- By end user, hospitals held 54.40% of U.S. healthcare PPE market share in 2025 and are also expected to record the highest growth at a 5.25% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

U.S. Healthcare Personal Protective Equipment Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Healthcare-associated infection control compliance | +1.4% | National, with concentrated impact in major hospital markets including New York, California, Texas, and Illinois | Long term (≥ 4 years) |

| Aging patient base and higher clinical-touch volumes | +1.1% | National, with early intensity in Sun Belt states including Florida, Arizona, Nevada, and Texas | Long term (≥ 4 years) |

| Strategic stockpiling and domestic sourcing mandates | +0.9% | National, with CMS and federal procurement requirements affecting Medicare-participating hospitals and federal buyers | Medium term (2-4 years) |

| Care migration to outpatient and home settings | +0.7% | National, with earlier adoption in Mid-Atlantic, Pacific Coast, and Sun Belt states | Medium term (2-4 years) |

| Reusable respiratory PPE for preparedness and total cost of ownership | +0.5% | National, with stronger uptake in large health systems in the Northeast and Pacific Coast | Medium term (2-4 years) |

| Tariff-driven preference for U.S.-made supply | +0.4% | National, with greater restructuring pressure in import-dependent southeastern and Gulf Coast states | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Healthcare-Associated Infection Control Compliance

In the U.S., hospitals increasingly view adherence to PPE protocols as both a clinical necessity and a financial priority. Healthcare-associated infections remain a significant challenge, with approximately 1.7 million incidents occurring annually in U.S. hospitals. This ensures the consistent use of gloves, gowns, masks, and respiratory protection in patient care. CMS has introduced updates to NHSN HAI measures, effective FY 2029, under the Hospital-Acquired Condition Reduction Program. As performance standards tighten, procurement teams face growing pressure to prioritize compliance-driven PPE purchasing, solidifying its role in the U.S. healthcare PPE market.

Aging Patient Base And Higher Clinical-Touch Volumes

The aging U.S. population is driving increased demand for PPE due to the higher care intensity required for older patients. These patients often need extended monitoring, longer hospital stays, and more frequent staff interactions, leading to greater usage of gloves, gowns, and respiratory protection. This trend extends beyond hospitals to home-based and ambulatory care settings, where infection control remains critical. Consequently, the aging demographic is strengthening the demand base of the U.S. healthcare PPE market, even as overall growth remains steady.

Strategic Stockpiling And Domestic Sourcing Mandates

Strategic stockpiling and domestic sourcing are reshaping procurement strategies in the U.S. healthcare PPE market. Policies like the Infrastructure Investment and Jobs Act and CMS proposals for Medicare-participating hospitals emphasize domestic sourcing thresholds and payment adjustments to address cost disparities. These measures are driving buyers to prioritize resilience, traceability, and supplier eligibility. Domestic manufacturing credentials are becoming increasingly important in the competitive landscape of the U.S. healthcare PPE market.

Care Migration To Outpatient And Home Settings

The shift of care to outpatient and home settings is broadening the demand for PPE in the U.S. healthcare market. Outpatient centers now handle more complex procedures, requiring specialized protective equipment, while home-based care adds demand for infection control during professional visits. This diversification reduces reliance on hospital purchasing and ensures stable long-term demand for PPE across various care environments.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Post-pandemic inventory digestion and price resets | -0.3% | National, with the strongest effect in large regional health systems in the Northeast and Midwest | Short term (≤ 2 years) |

| Hospital margin pressure and SKU rationalization | -0.2% | National, with greater pressure in community and critical access hospitals in rural and Midwestern states | Medium term (2-4 years) |

| Fit-testing and program burden for advanced respirators | -0.2% | National, with higher compliance costs in large hospital systems and expanding ASC networks | Medium term (2-4 years) |

| Waste and sustainability scrutiny of single-use PPE | -0.1% | National, with the strongest ESG pressure in California, the Pacific Coast, and Northeastern markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Post-Pandemic Inventory Digestion And Price Resets

The U.S. healthcare PPE market continues to face challenges stemming from pandemic-era overstocking. Major health systems are managing surplus inventories of gloves, isolation gowns, and masks, which has slowed reorder activity despite consistent clinical usage. Suppliers are navigating stable demand but reduced purchasing momentum. Additionally, trade and sourcing policy discussions are emphasizing concerns over import reliance and procurement costs. Short-term revenue remains under pressure, reflecting inventory clearance delays, price adjustments, and uneven restocking.

Hospital Margin Pressure And SKU Rationalization

Hospitals are increasingly selective about PPE products due to budget constraints. Procurement teams are consolidating glove, gown, and mask options to secure better pricing from fewer vendors. This approach can delay the adoption of specialty or premium products, even when clinically justified. OSHA's proposed rule for July 2025 on respiratory protection is expected to save USD 81 million annually for healthcare workers, offering marginal relief. However, broader financial pressures continue to drive SKU rationalization, leaving mid-tier suppliers vulnerable as large systems narrow vendor lists.[2]Occupational Safety and Health Administration, “Proposed Rule, Respiratory Protection Standard, Medical Evaluation Requirements,” Federal Register, govinfo.gov

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Hand Protection Anchors Volume While Protective Clothing Sets The Growth Agenda

Hand protection captured 38.50% of U.S. healthcare PPE market share in 2025, making it the largest product category in the U.S. healthcare PPE market. Hand protection dominates the U.S. healthcare PPE market, holding the largest share due to the widespread use of gloves in patient interactions across various care settings. Examination gloves see the highest consumption due to routine usage, while surgical gloves remain a premium segment driven by procedure volumes, sterility needs, and clinician preferences. Respiratory protection also holds strategic importance as health systems maintain preparedness standards, supported by regulatory guidance on air-purifying respirators.

Protective clothing is projected to grow at the fastest CAGR through 2031, driven by increased demand for isolation and surgical gowns as procedural activities expand across care environments. Domestic sourcing rules enhance the strategic importance of gowns, while AAMI barrier classifications guide purchasing decisions by balancing comfort, exposure risk, and procedure complexity. Face and eye protection categories, though smaller, benefit from ongoing standardization in infection control practices.

By End User: Hospitals Dominate Spend And Set The Specification Standard For The Broader Market

Hospitals held 54.40% of U.S. healthcare PPE market size in 2025 and are projected to expand at a 5.25% CAGR through 2031. Hospitals lead the U.S. healthcare PPE market, driven by high patient acuity, diverse procedures, and strict infection control requirements. PPE purchasing in hospitals supports care delivery, regulatory compliance, and quality standards, with a preference for validated, premium products in high-risk scenarios. As the largest segment, hospitals influence product standards and purchasing trends across the market.

Ambulatory and outpatient settings are gaining significance as more procedures shift outside traditional hospital environments, increasing PPE usage per visit. Home healthcare adds recurring demand, with each visit requiring gloves, masks, and other protective items. This diversification in end-users broadens the demand base and reshapes supplier strategies in product offerings and distribution.

Geography Analysis

The U.S. healthcare PPE market operates as a unified national entity, but demand varies due to differences in healthcare infrastructure, demographic age distributions, and purchasing frameworks. The Southern states, particularly Texas and Florida, are emerging as key demand hubs. Florida's older population drives consistent demand for examination gloves, isolation gowns, and PPE for long-term care. Texas, with its extensive hospital networks and expanding outpatient services, demonstrates a diverse procurement strategy across various care settings. Discussions around domestic sourcing and import reviews are prompting southern healthcare systems to reassess contract structures and supplier selections.

The Northeast, including states like New York, Massachusetts, Pennsylvania, and New Jersey, has the highest concentration of academic medical centers in the country. These institutions often set product standards that influence broader hospital networks. They are early adopters of advanced measures such as high-barrier gowns, elastomeric respirators, and preparedness-focused PPE protocols. In the Midwest, volume stability and price competitiveness dominate, driven by the reliance on Group Purchasing Organizations (GPOs). This results in visible supplier consolidation and SKU rationalization across hospitals in the region.

California, leading the Pacific Coast, is at the forefront of sustainability-driven PPE decisions. State-level waste reduction mandates are driving interest in reusable and environmentally friendly protective apparel. The region also adopts high-specification products when infection control and environmental goals align, making it a key indicator for broader trends in the U.S. healthcare PPE market.

Competitive Landscape

While the U.S. healthcare PPE market is moderately fragmented at the manufacturing level, distribution holds a more concentrated influence. Key players like Cardinal Health, Medline, and Owens & Minor dominate access across major acute care networks. The competitive landscape includes multinationals such as 3M, DuPont, and Ansell, alongside healthcare specialists like Mölnlycke, O&M Halyard, and Medicom. Domestic producers, including Prestige Ameritech, Alpha Pro Tech, and Armbrust American, further contribute to the market. Routine categories remain price-competitive, while premium and policy-linked categories are becoming more distinct.

Recent strategic moves highlight supplier adaptability in the U.S. healthcare PPE market. Prestige Ameritech secured a USD 99 million NIH IDIQ contract for American-made PPE through September 2026 after acquiring S2S Global. Alpha Pro Tech reported 5.5% growth in protective apparel, surpassing the overall market growth rate. Platinum Equity completed the acquisition of Owens & Minor's Products & Healthcare Services segment for USD 375 million, creating a standalone acute-care distribution platform and allowing Owens & Minor to focus on its patient direct home-care business.

Competitive differentiation is shifting toward transparent sourcing, compliance readiness, and usage efficiency. Medline's SmartBox dispensing system demonstrates that reduced waste and improved point-of-use access can drive formulary wins. Similar trends are evident in respirator and gown categories, where preparedness, domestic content, and sustainability are influencing vendor selection. These factors present growth opportunities for reusable respirators and eco-friendly protective clothing in the U.S. healthcare PPE market.

U.S. Healthcare Personal Protective Equipment Industry Leaders

B. Braun Melsungen AG

Cardinal Health, Inc.

Medline Inc.

Mölnlycke Health Care AB

PAUL HARTMANN AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: The FDA added Medline Industries' neurosurgical patties, sponges, and strips to its medical device shortage list. This followed a March 2026 recall due to elevated endotoxin levels, with disruptions expected to continue through late 2026, prompting health systems to address single-source supply chain risks.

- April 2026: The FDA issued draft guidance for NIOSH-approved air-purifying respirators. It proposed a simplified regulatory pathway for surgical N95s, standard N95s, elastomeric half-masks, and PAPRs to reduce premarket barriers and strengthen domestic supply resilience.

- March 2026: DuPont launched the Tyvek APX 400 protective coverall, combining Type 5-B and 6-B chemical protection with advanced breathability. The product addressed the comfort-protection gap in single-use protective clothing for clinical environments.

- January 2026: CMS proposed the "Secure American Medical Supplies" designation for Medicare hospitals meeting domestic PPE procurement thresholds of 25%, 50%, or 75%. Payment adjustments were suggested to offset higher domestic costs, with final rulemaking expected during the forecast period.

U.S. Healthcare Personal Protective Equipment Market Report Scope

As per the scope of the report, healthcare personal protective equipment (PPE) is specialized gear and clothing designed to create a physical barrier between healthcare workers and infectious agents. It minimizes exposure to biological hazards, protecting both the provider from contamination and the patient from hospital-acquired infections.

The U.S. Healthcare Personal Protective Equipment Market is segmented by product type and end-user. By product type, the market includes hand protection (examination gloves and surgical gloves), protective clothing (isolation gowns, surgical gowns, coveralls, lab coats & procedure apparel, and headwear & footwear), respiratory protection (surgical N95 respirators, standard N95 respirators for care settings, elastomeric half-mask respirators, and powered air-purifying respirators), face protection, eye protection, and other types. By end-user, the market is segmented into hospitals, ambulatory & outpatient care, home healthcare, diagnostic & laboratory settings, and other settings. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Hand Protection | Examination gloves |

| Surgical gloves | |

| Protective Clothing | Isolation gowns |

| Surgical gowns | |

| Coveralls | |

| Lab coats and procedure apparel | |

| Headwear and footwear | |

| Respiratory Protection | Surgical N95 respirators |

| Standard N95 respirators used in care settings | |

| Elastomeric half-mask respirators | |

| Powered air-purifying respirators | |

| Face Protection | |

| Eye Protection | |

| Others |

| Hospitals |

| Ambulatory and Outpatient Care |

| Home Healthcare |

| Diagnostic and Laboratory Settings |

| Others |

| By Product Type | Hand Protection | Examination gloves |

| Surgical gloves | ||

| Protective Clothing | Isolation gowns | |

| Surgical gowns | ||

| Coveralls | ||

| Lab coats and procedure apparel | ||

| Headwear and footwear | ||

| Respiratory Protection | Surgical N95 respirators | |

| Standard N95 respirators used in care settings | ||

| Elastomeric half-mask respirators | ||

| Powered air-purifying respirators | ||

| Face Protection | ||

| Eye Protection | ||

| Others | ||

| By End User | Hospitals | |

| Ambulatory and Outpatient Care | ||

| Home Healthcare | ||

| Diagnostic and Laboratory Settings | ||

| Others | ||

Key Questions Answered in the Report

What is the 2026 size of the U.S. healthcare PPE market?

The U.S. healthcare PPE market size stands at USD 4.58 billion in 2026 and is forecast to reach USD 5.71 billion by 2031 at a 4.50% CAGR.

What is driving demand for healthcare PPE in the United States?

The main demand supports are infection control compliance, an aging patient base, domestic sourcing policy shifts, and more procedures moving into outpatient and home settings.

Which product category leads spending in this space?

Hand protection was the largest product type with 38.50% share in 2025, supported by its use across nearly every patient interaction.

Which product type is growing the fastest through 2031?

Protective clothing is projected to post the fastest product growth, with a 5.10% CAGR through 2031.

Which end user is most important for suppliers?

Hospitals are the largest end user with 54.40% share in 2025, and they are also the fastest-growing end-user segment at a 5.25% CAGR through 2031.

How is domestic sourcing changing competition in healthcare PPE?

The proposed CMS Secure American Medical Supplies framework is increasing the value of domestic manufacturing credentials, supply chain transparency, and long-term procurement eligibility.

Page last updated on: