Safety Pen Needles Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

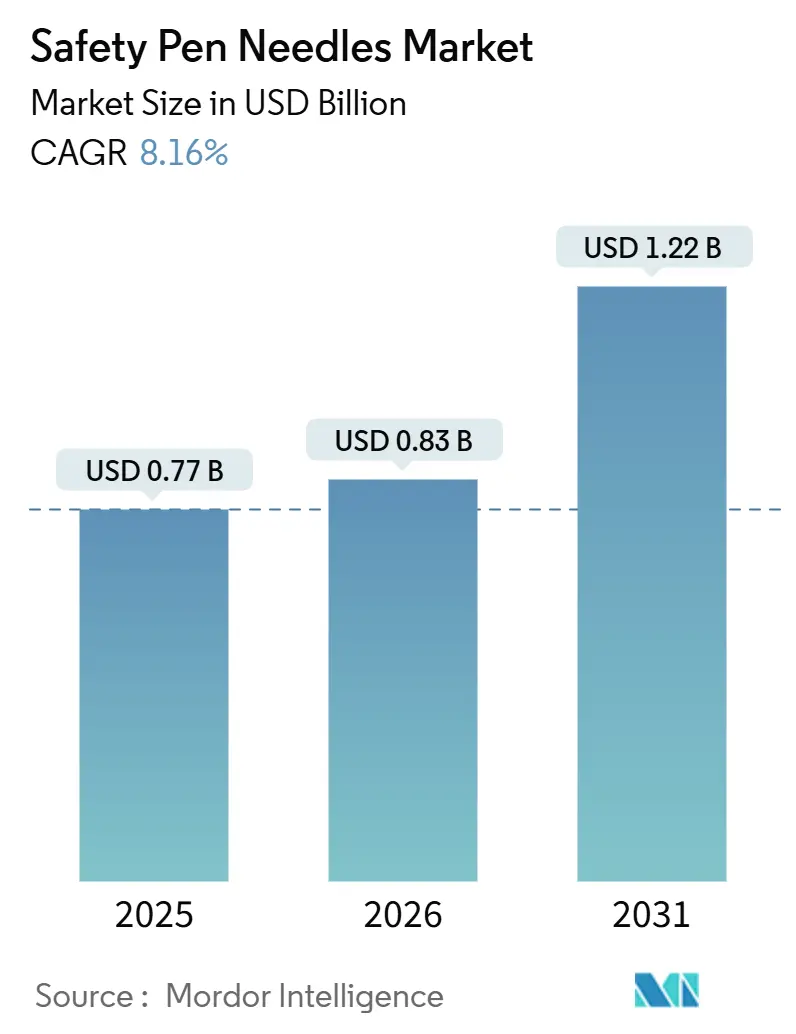

| Market Size (2026) | USD 0.83 Billion |

| Market Size (2031) | USD 1.22 Billion |

| Growth Rate (2026 - 2031) | 8.16% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Safety Pen Needles Market Analysis by Mordor Intelligence

The Safety Pen Needles Market was valued at USD 0.77 billion in 2025 and expected to grow from USD 0.83 billion in 2026 to reach USD 1.22 billion by 2031, at a CAGR of 8.16% during the forecast period (2026-2031).

Growth is propelled by global requirements that mandate sharps-injury prevention features, the surge in GLP-1 injectable therapies, and insurer support for home-based chronic care. Broad compliance with ISO 23908:2024, rising diabetes prevalence, and near-shoring of device production all reinforce demand. Device makers are scaling passive shielding technologies, expanding sterilization capacity, and integrating pen needles with connected autoinjectors to meet clinician and patient expectations. North America remains the single largest regional buyer, but Asia-Pacific will add the most new volume through 2031.

Key Report Takeaways

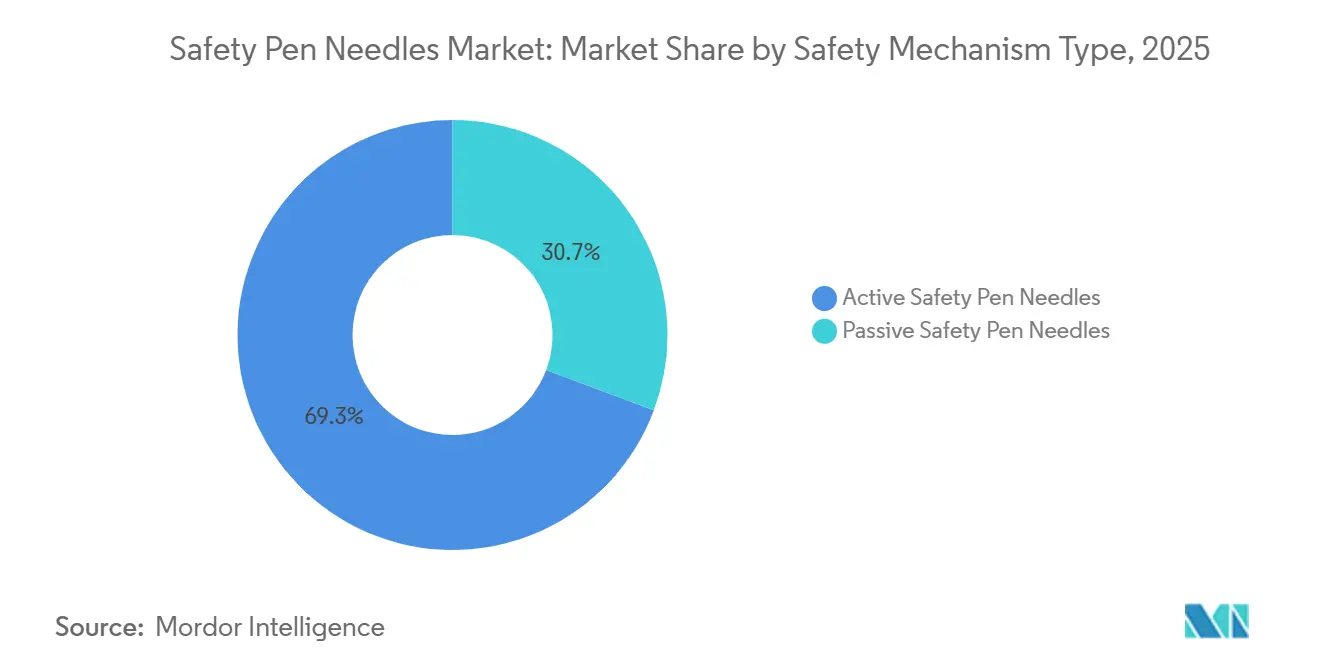

- By safety mechanism, active designs held 69.31% of the safety pen needles market share in 2025, while passive designs are advancing at a 10.12% CAGR to 2031.

- By needle length, 5 millimeter products led with 31.58% revenue share in 2025; 6 millimeter variants are growing fastest at an 11.01% CAGR through 2031.

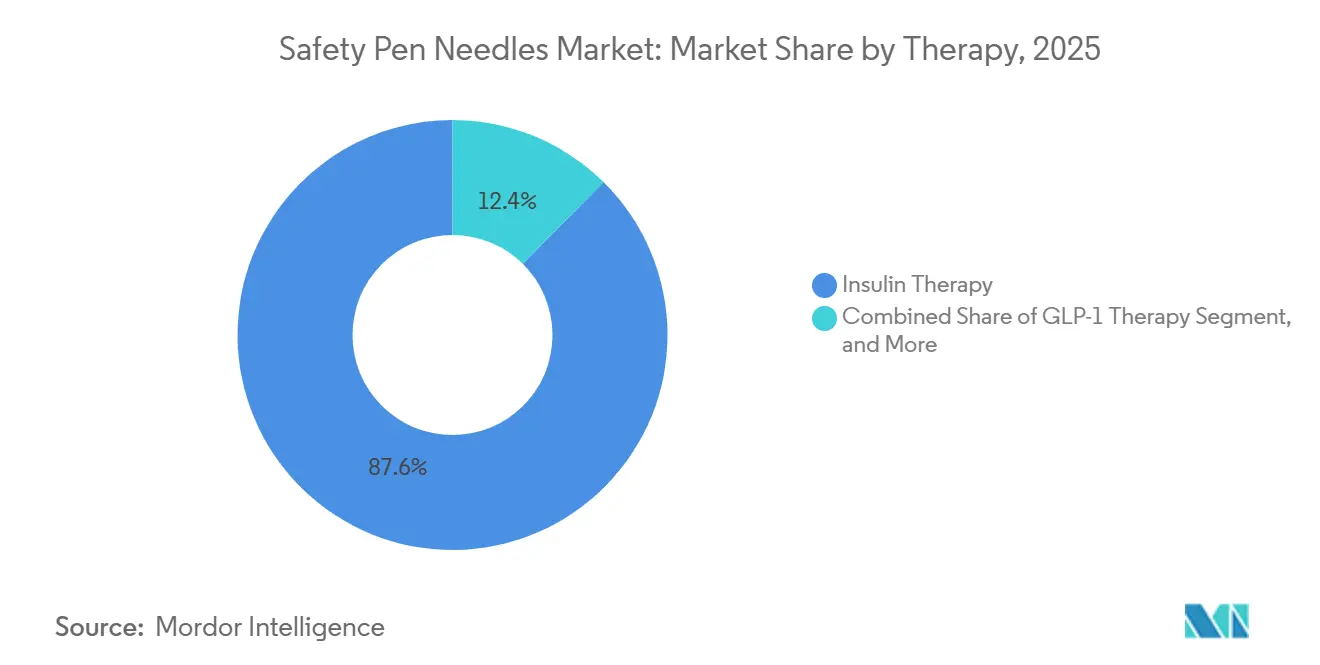

- By therapy, insulin accounted for 87.62% of the safety pen needles market size in 2025, and GLP-1 therapy is set to expand at a 13.84% CAGR to 2031.

- By end-user, hospitals and clinics held a 48.13% share in 2025, whereas home-care settings are rising at a 11.81% CAGR through 2031.

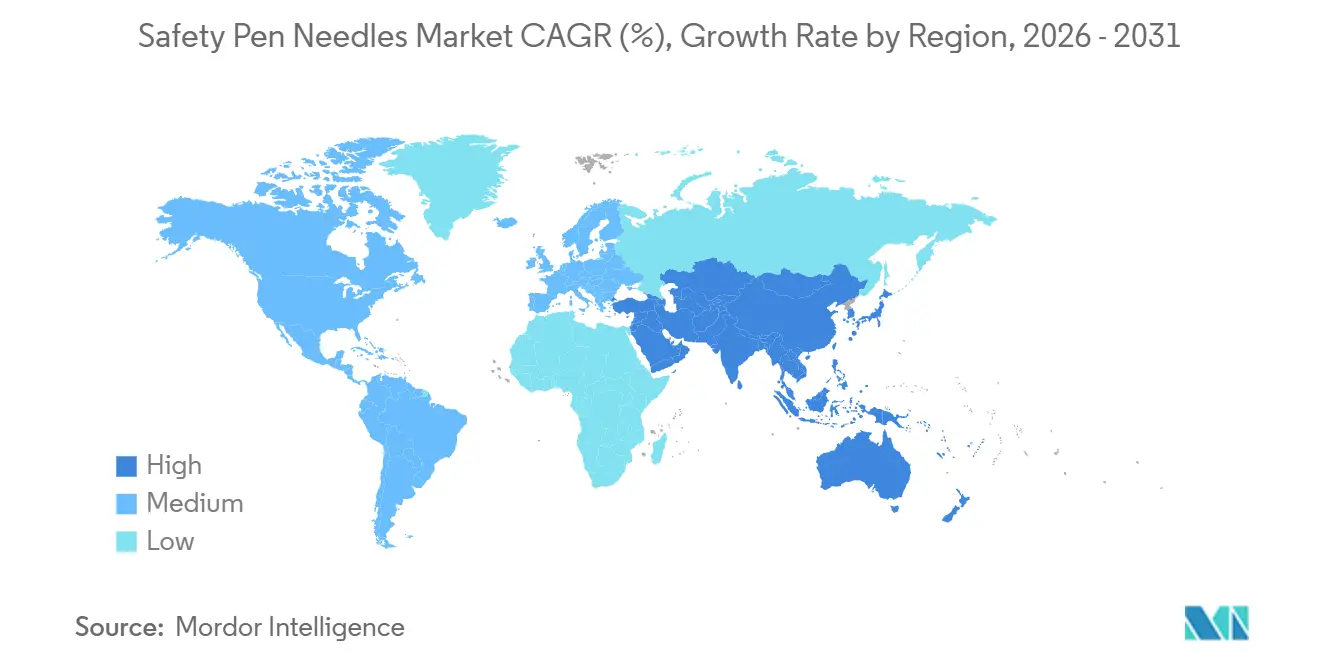

- By geography, North America dominated with a 43.83% share in 2025, but Asia-Pacific is pacing the field at a 14.67% CAGR for the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Safety Pen Needles Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory Mandates for Sharps-Injury Prevention | +1.8% | Global, with strongest enforcement in North America & EU | Medium term (2-4 years) |

| Diabetes Prevalence Fueling Injection Volumes | +2.1% | Global, APAC core with spillover to MEA | Long term (≥ 4 years) |

| Shift to Home-Based Self-Administration | +1.5% | North America & EU, expanding to APAC urban centers | Medium term (2-4 years) |

| Passive Auto-Disable Innovations Reduce Training Burden | +1.2% | Global, accelerated adoption in home-care and ambulatory settings | Short term (≤ 2 years) |

| Trade-Driven Near-Shoring of Needle Production | +0.9% | North America, EU, select APAC markets | Medium term (2-4 years) |

| Shift Toward Safety Pen Needles to Curb Needlestick Injuries | +1.6% | Global, regulatory-driven in North America & EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory Mandates for Sharps-Injury Prevention

ISO 23908:2024 establishes global test protocols that demonstrate a pen needle can prevent needlestick exposure during injection and disposal, accelerating approvals for products that include auto-disable shields or retractable cannulas.[1]International Organization for Standardization, “ISO 23908:2024—Sharps Injury Protection,” ISO.org U.S. OSHA rules require hospitals to purchase engineering controls, while the European Union Medical Device Regulation mandates strict post-market surveillance. Intermountain Healthcare documented a 51% drop in injuries after standardizing on a 6-millimeter safety syringe, confirming regulatory aims in practice. These frameworks shift purchasing away from standard needles and narrow the historic price gap.

Diabetes Prevalence Fueling Injection Volumes

NCD-RisC pegged the global diabetes population at 828 million adults in 2022, and China plus India account for 217 million of those cases. The U.S. CDC reported that 26.5% of American adults with diabetes were on GLP-1 injectables in 2024, showing momentum for once-weekly regimens. Eli Lilly logged USD 5.2 billion in Mounjaro sales in 2024, while Novo Nordisk crossed USD 20 billion in GLP-1 revenue, underscoring the upside from compatible pen needles.

Shift to Home-Based Self-Administration

CMS data revealed that U.S. home health spending rose 7.8% in 2024, outpacing spending in other service lines.[2]Centers for Medicare & Medicaid Services, “National Health Expenditure Data,” cms.gov Patients need devices that work without complex training, and passive shields automatically engage on completion, lowering risk in the living room as effectively as in the ward. A BMJ Open review of growth-hormone pens confirmed that ease of use outweighs price when patients select injection hardware. The trend extends to diabetes and weight-management drugs delivered outside clinical settings.

Passive Auto-Disable Innovations Reduce Training Burden

BD markets passive safety pen needles with front- and rear-end shields that auto-deploy, reducing staff training time and simplifying patient instructions.[3]Becton, Dickinson and Company, “Product Information,” bd.com Embecta uses similar designs, and health systems increasingly include auto-disable clauses in tenders. The Intermountain study validated passive devices by cutting injury rates in half, even across varying user skill levels.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Availability of Alternate Drug-Delivery (Pumps, Patch Pens) | -1.4% | North America & EU, early adoption in affluent APAC urban centers | Long term (≥ 4 years) |

| Premium Pricing Versus Standard Pen Needles | -0.9% | Emerging markets in APAC, Latin America, MEA with limited reimbursement | Medium term (2-4 years) |

| Stringent ISO / FDA Biocompatibility Test Cycles | -0.6% | Global, with highest compliance burden in North America & EU | Short term (≤ 2 years) |

| Ethylene-Oxide Sterilization Capacity Bottlenecks | -1.1% | North America, with secondary impact on EU and APAC supply chains | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Availability of Alternate Drug-Delivery (Pumps, Patch Pens)

Embecta secured FDA clearance in 2025 for a disposable patch pump that can run for three days per reservoir, removing nearly 1,500 needles per converted patient annually. Insulet and Tandem pumps are also gaining users, especially among tech-savvy cohorts. Yet pump penetration remains below 40% even in well-funded markets, and GLP-1 drugs do not have pump formulations today, limiting near-term erosion of the safety pen needles market.

Premium Pricing Versus Standard Pen Needles

Safety designs cost 20% to 50% more than standard needles, which caps use in health systems with tight budgets. Embecta cited price pressure in emerging regions in its 2022 filing, noting volume-based procurement squeezes margins. Where patients pay cash, higher unit prices hinder uptake until reimbursement widens or local production cuts cost.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Safety Mechanism Type: Passive Designs Accelerate

Active models accounted for 69.31% of revenue in 2025, reflecting established training protocols in hospitals. Passive models are growing at 10.12% CAGR through 2031, the fastest of any mechanism, because they protect users without extra steps. Payers link passive designs to lower injury claims, and ISO 23908:2024 clearly favors automatic activation. Manufacturers now market dual-shield cannulas that auto-deploy once the dose is delivered, meeting both clinician and home-user needs.

Passive uptake is strongest in home care, retail clinic, and ambulatory surgery settings, where staff turnover is high, and patient dexterity varies. The safety pen needle market continues to tilt toward these devices as regulators audit compliance logs and insurers tie reimbursements to safety outcomes. Active designs will remain relevant in high-volume hospital wards that value tactile confirmation, but their relative weight will fall as self-administration rises.

By Needle Length: Mid-Range Cannulas Gain Momentum

Five-millimeter needles held a 31.58% share in 2025, thanks to comfort and low pain scores. Six-millimeter models are expanding at 11.01% CAGR because they reach consistent subcutaneous depth in patients with higher BMI. Manufacturers refine thin-wall stainless tubes that sustain flow even at mid-lengths, and real-world evidence shows equal comfort scores compared with shorter cannulas.

Longer 8 and 10-millimeter needles serve niche cases but see limited consumer acceptance. Ultra-short 4 millimeter variants target pediatric users and sensitive adults, yet their contribution to overall volume remains small. Technological advances that enable smaller outer diameters without compromising rigidity will likely reinforce the mid-range trend and keep 5 to 6-millimeter products at the core of the safety pen needles market.

By Therapy: GLP-1 Demand Lifts Volume Beyond Insulin

Insulin accounted for 87.62% of revenue in 2025, yet GLP-1 therapy is clocking the highest growth rate at a 13.84% CAGR. Weekly doses mean fewer sticks per patient, but script counts are skyrocketing as obesity and cardiovascular indications widen. Dual-therapy regimens also pair basal insulin with GLP-1, pushing needle consumption above levels seen with insulin alone.

Growth hormone and osteoporosis treatments form smaller but durable revenue streams because patients inject daily for long periods. Use cases in fertility and immunology remain niche but add diversity that cushions against insulin pump substitution. Overall, drug-mix shifts favor steadier unit demand than headline injection frequency suggests, keeping the safety pen needles market on its upward curve.

By End-User: Home-Care Outpaces Institutional Purchasing

Hospitals and clinics owned a 48.13% share in 2025, underpinned by bundle contracts and OSHA compliance audits. Home care, however, is accelerating at an 11.81% CAGR as Medicare and private payers lean into telehealth and chronic care at home. Patients prize low-force, auto-shield designs that minimize handling risk.

Ambulatory surgery centers and retail clinics are small today but expand steadily as outpatient models gain traction. Suppliers tailor packaging configurations, direct-to-patient delivery, and instructional videos to capture the rising share of home-based orders. Manufacturers that integrate passive safety with sharps-containment accessories stand to win loyalty in this channel.

Geography Analysis

North America generated 43.83% of 2025 revenue, driven by OSHA rules, CMS reimbursement for safety devices, and the rapid uptake of GLP-1 prescriptions. Domestic capacity investments by BD and Sharps Technology validate the region’s strong demand base and reflect policy moves to shorten supply chains.

Europe follows with solid value per unit, thanks to MDR enforcement and high safety expectations in public tenders. Germany, France, and the United Kingdom remain anchor markets even as budget constraints pressure prices. Central and Eastern Europe shows room for penetration as hospital groups modernize.

Asia-Pacific is on track for a 14.67% CAGR to 2031, the highest globally. The prevalence of diabetes in China and India, along with local manufacturing scale, makes the region crucial for volume. Regulators in both countries are aligning with ISO 23908, opening tenders to safety designs. Mature markets such as Japan and Australia maintain high adoption rates, while Southeast Asia is moving up the curve as urban incomes rise.

Latin America and the Middle East & Africa post modest but improving growth. Brazil and Mexico lead Latin America as private pay segments expand. In the Gulf Cooperation Council, investment in chronic-disease programs increases demand, though public-sector price caps slow the uptake of premium devices. Safety needle penetration should increase as injury data becomes more visible and local sterilization capacity improves.

Competitive Landscape

BD and Ypsomed renewed collaboration in January 2026 to support 5.5 milliliter autoinjectors, demonstrating strategic bets on higher-viscosity biologics. Embecta, spun off from BD, produces roughly 8 billion injection devices a year but relies on BD for cannulas, posing a supply-chain sensitivity.

Regional players such as HTL-STREFA, Nipro, and Hindustan Syringes & Medical Devices exploit cost advantages and local distribution to challenge incumbents in tenders. Patent estates covering dual-shield mechanics, bevel geometry, and lubricious coatings preserve some moat, yet expiring patents invite fast followers. Competitors are adding adherence-tracking chips, ultra-fine gauges, and e-commerce storefronts to ignite differentiation.

Mergers and joint ventures keep reshaping capacity footprints. Reshoring patterns in the United States and Europe enhance resilience but may compress margins if unit costs rise faster than prices can be realized. Firms with distributed sterilization networks and flexible tooling are better placed to comply with evolving EtO standards and ISO updates.

Safety Pen Needles Industry Leaders

Becton, Dickinson & Company

NIPRO Corporation

Novo Nordisk A/S

Ypsomed AG

ARKRAY Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: BD and Ypsomed expanded their alliance to co-develop a 5.5 milliliter Neopak XtraFlow syringe for YpsoMate autoinjectors, enabling faster self-injection of large-volume biologics.

- January 2026: Global enforcement of sharps‑injury prevention standards and compliance with ISO 23908:2024 are major catalysts for the adoption of safety‑engineered needle devices (SENDs). The increasing emphasis on occupational safety in both clinical and home‑care settings is driving demand for automatic protection mechanisms.

- November 2025: BD pen needles and insulin syringes began transitioning to embecta branding in late 2025, signaling a major identity shift for one of the largest global suppliers.

- August 2025: Trividia Health launched its TRUEplus five‑bevel insulin pen needles in the United Kingdom, offering multiple gauges and lengths designed for improved comfort and affordability.

Global Safety Pen Needles Market Report Scope

The Safety Pen Needles Market refers to the global industry for pen needles that incorporate safety mechanisms to prevent accidental needlestick injuries during insulin or other injectable drug delivery. These devices are primarily used by patients with diabetes and healthcare providers, offering enhanced protection compared to standard pen needles.

The Safety Pen Needles Market Report is Segmented by Safety Mechanism Type (Active, Passive), Needle Length (5mm, 6mm, 8mm, 10mm, Others), Therapy (Insulin, GLP-1, Growth Hormone, Osteoporosis, Others), End-User (Home-Care, Hospitals & Clinics, Ambulatory Surgery Centers, Others), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). Market Forecasts are Provided in Value (USD).

| Active Safety Pen Needles |

| Passive Safety Pen Needles |

| 5 mm |

| 6 mm |

| 8 mm |

| 10 mm |

| Others |

| Insulin Therapy |

| GLP-1 Therapy |

| Growth-Hormone Therapy |

| Osteoporosis |

| Other Therapies |

| Home-Care Settings |

| Hospitals & Clinics |

| Ambulatory Surgery Centers |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Safety Mechanism Type | Active Safety Pen Needles | |

| Passive Safety Pen Needles | ||

| By Needle Length | 5 mm | |

| 6 mm | ||

| 8 mm | ||

| 10 mm | ||

| Others | ||

| By Therapy | Insulin Therapy | |

| GLP-1 Therapy | ||

| Growth-Hormone Therapy | ||

| Osteoporosis | ||

| Other Therapies | ||

| By End-User | Home-Care Settings | |

| Hospitals & Clinics | ||

| Ambulatory Surgery Centers | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the safety pen needles market?

The safety pen needles market size is USD 0.83 billion in 2026.

How fast will revenue grow over the next five years?

Revenue is projected to rise to USD 1.22 billion by 2031, registering an 8.16% CAGR.

Which safety mechanism type is expanding most quickly?

Passive auto-disable needles are increasing at a 10.12% CAGR through 2031.

Why is Asia-Pacific seen as the main growth engine?

The region combines high diabetes prevalence, local manufacturing expansion, and regulatory alignment, supporting a 14.67% CAGR.

How do GLP-1 drugs affect needle demand?

Rising prescriptions for weekly GLP-1 injections are driving double-digit growth in needle volumes despite lower sticks per patient.

Page last updated on: