Medical Coating Additives Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

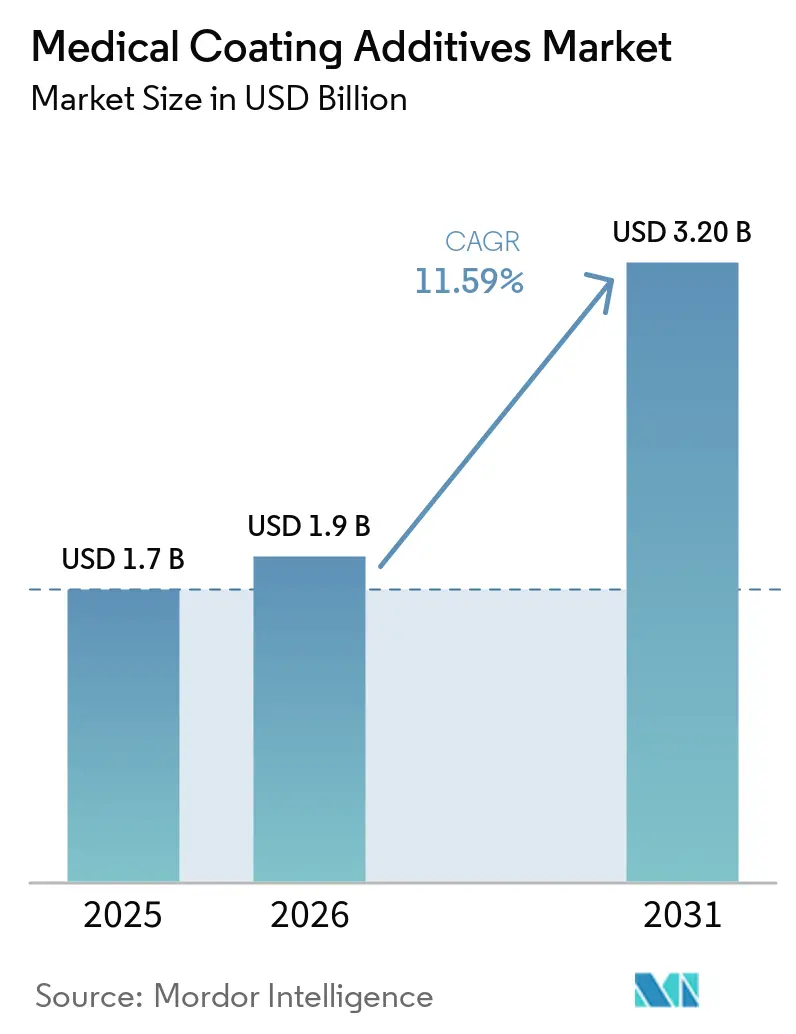

| Market Size (2026) | USD 1.9 Billion |

| Market Size (2031) | USD 3.20 Billion |

| Growth Rate (2026 - 2031) | 11.59% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Medical Coating Additives Market Analysis by Mordor Intelligence

The Medical Coating Additives Market size is expected to increase from USD 1.7 billion in 2025 to USD 1.9 billion in 2026 and reach USD 3.20 billion by 2031, growing at a CAGR of 11.59% over 2026-2031.

The medical coatings additives market is experiencing significant growth, driven by the increasing demand for specialized, biocompatible, and infection-resistant surfaces on medical devices, surgical tools, and implants, with a strong focus on antimicrobial and hydrophilic functional additives. As healthcare-associated infections (HAIs) rise, there is a surge in demand for active coatings, particularly those containing silver, chlorhexidine, or drug-eluting agents to enhance patient safety.

Key Report Takeaways

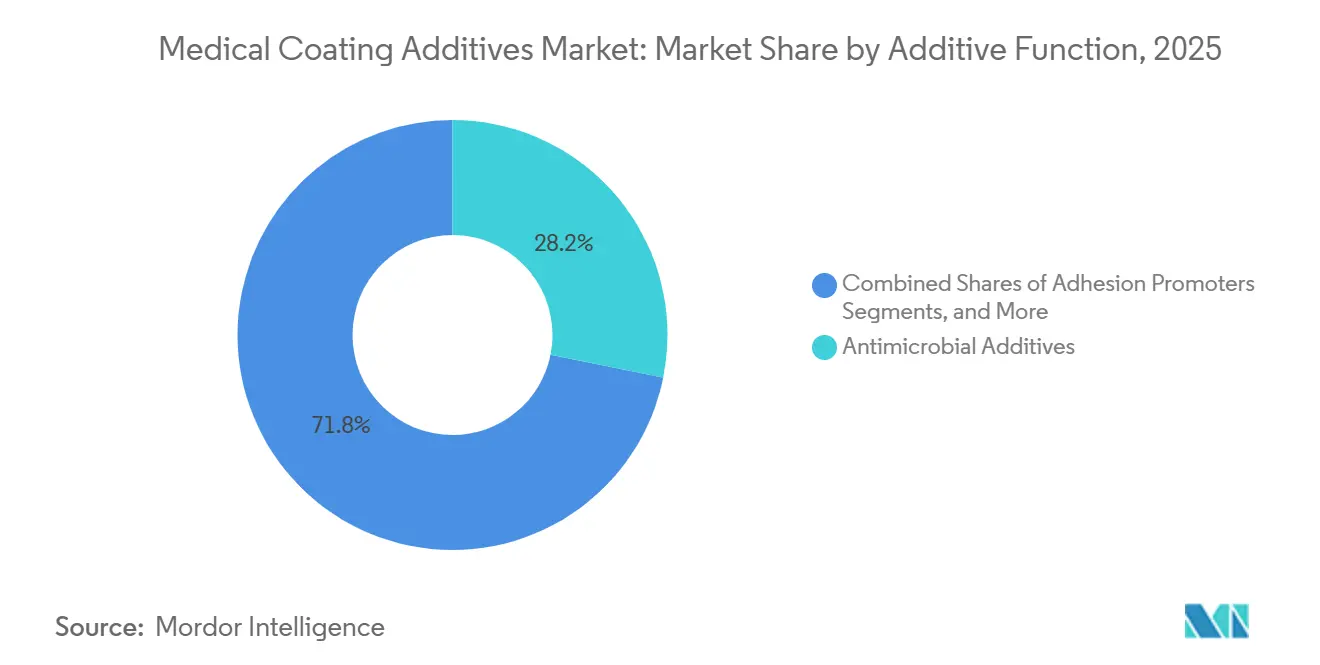

- By additive function, antimicrobial additives remained the largest functional segment at 28.16% of revenue in 2025, while slip and lubricity modifiers are expanding more quickly at 13.17% CAGR

- By application, catheters and guidewires accounted for 36.15% of the medical coating additives market share in 2025. Implantable devices are advancing at a 14.14% CAGR to 2031, the fastest among all end uses.

- By additive chemistry, silicones captured 26.15% share of the medical coating additives market size in 2025, while inorganic nano-additives are projected to post a 14.98% CAGR between 2026 and 2031.

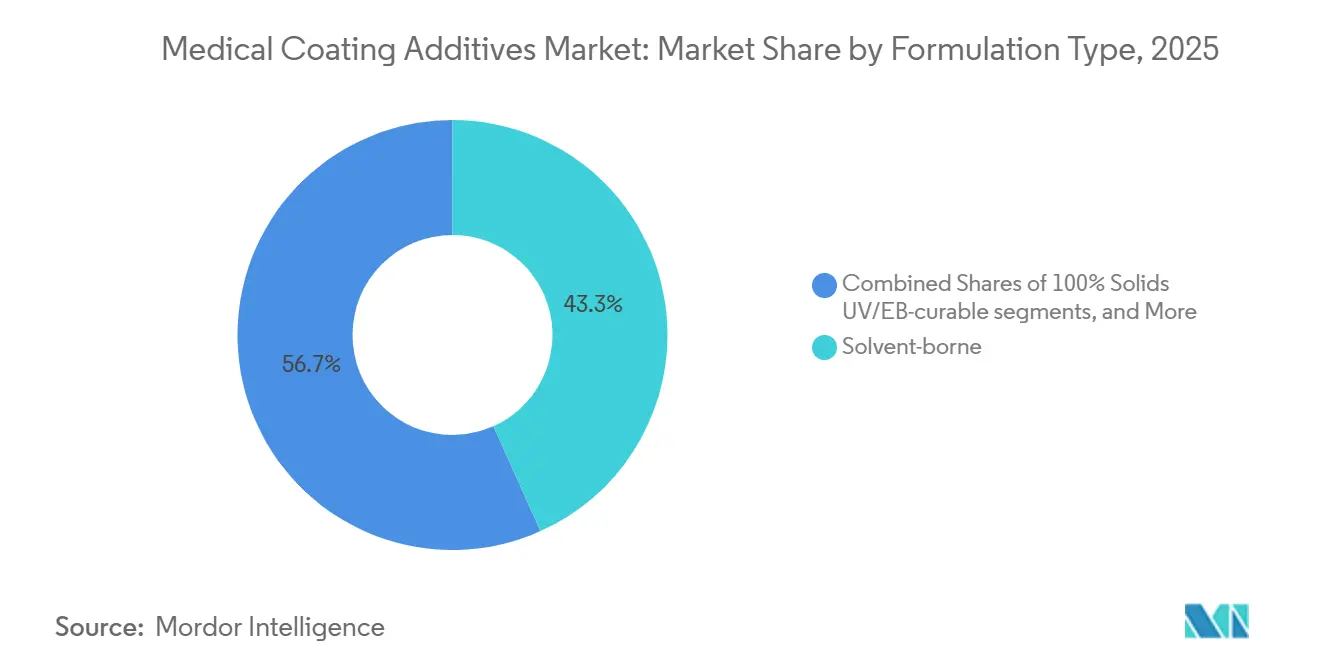

- By formulation type, solvent-borne captures 43.28% share of the medical coating additives market size in 2025.

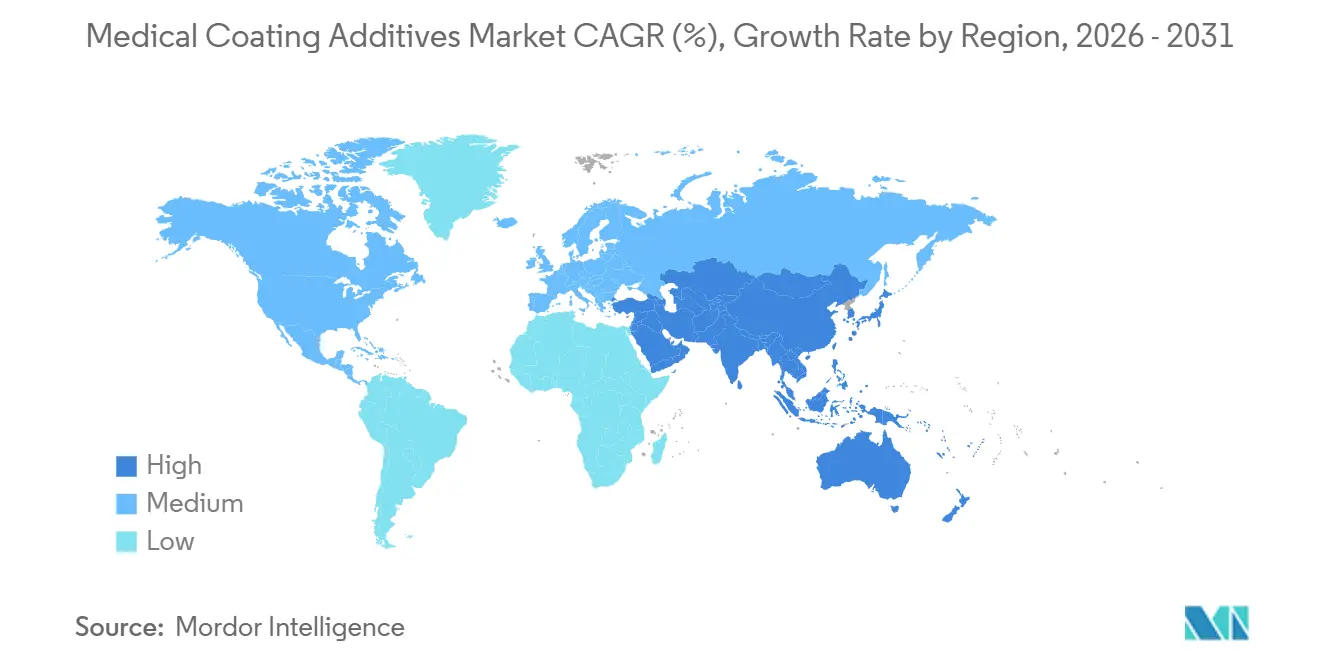

- By geography, North America led with 36.71% revenue share in 2025, whereas Asia-Pacific is expected to register the highest regional CAGR at 14.56% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Medical Coating Additives Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Minimally invasive procedures expand catheter and guidewire volumes | +2.1% | Global, led by North America and Europe | Medium term (2-4 years) |

| Healthcare-associated infection (HAI) burden | +1.8% | Global, acute in North America and EU | Short term (≤ 2 years) |

| Shift to waterborne and UV/EB-curable systems | +1.5% | North America and EU; accelerating in Asia-Pacific | Medium term (2-4 years) |

| Recognition of VHP sterilization | +1.3% | North America and EU; emerging in Asia-Pacific | Medium term (2-4 years) |

| EtO emissions rule drives revalidation | +1.0% | United States; indirect global supply-chain impact | Short term (≤ 2 years) |

| PFAS restriction trajectory | +2.0% | EU; expanding U.S. state-level bans | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Minimally Invasive Procedures Boost Demand for Catheters and Guidewires

As procedures like percutaneous coronary intervention, transcatheter valve replacement, and neurovascular thrombectomy gain traction, the global demand for lubricious-coated catheters and guidewires continues to grow. These devices, which historically achieved friction coefficients below 0.05 with PTFE micropowders, are now increasingly utilizing blends of polyvinylpyrrolidone, polyethylene glycol, and silicone fluids for their hydrophilic coatings. The rise in catheter interventions, coupled with growing safety expectations, has driven the need for devices offering both lubricity and antimicrobial features.

Hospital-Acquired Infections (HAIs) Strain U.S. Healthcare

Hospital-acquired infections impose costs exceeding USD 28 billion annually on the U.S. healthcare system.[1]Centers for Disease Control and Prevention, “Healthcare Cost and Utilization Project: Catheter-Associated Interventions,” cdc.gov These financial pressures, along with reimbursement penalties, are encouraging hospitals to adopt antimicrobial-coated catheters and implants. Methicillin-resistant S. aureus and C. difficile remain prevalent in intensive care settings, increasing the demand for additives such as silver-ion, zinc-oxide, and quaternary-ammonium. Devices treated with antimicrobial solutions have demonstrated significant bacterial reduction within 24 hours. While compliance with toxicological risk assessments can raise validation costs, it also reinforces the demand for antimicrobial technologies.

Waterborne and UV/EB-Curable Systems Gain Traction Amid Stricter VOC Regulations

Stricter VOC limits in North America and the EU are reducing the solvent-borne market, accelerating the transition to waterborne dispersions and 100% solids UV or electron-beam (EB) curable formulas. UV and EB chemistries cure rapidly, enhance production efficiency, and eliminate harmful emissions. Although the capital investment for LED UV or EB cure units can exceed USD 500,000 per line, the benefits of reduced inventory and full VOC compliance are driving adoption among major device manufacturers.

FDA's 2024 Endorsement of VHP Sterilization Broadens Options for Heat-Sensitive Devices

With the FDA's 2024 endorsement of ISO 22441:2022, VHP has become a recognized sterilization method for heat-sensitive devices. However, VHP's oxidative nature presents challenges for certain organosilanes and acrylate crosslinkers.[2]U.S. Food and Drug Administration, “Recognition of ISO 22441 for Vaporized Hydrogen Peroxide Sterilization,” fda.gov Operating at 4-6 mg/L hydrogen peroxide and temperatures between 30-50 °C, VHP cycles introduce chain-scission risks, necessitating the use of peroxide-stable additives. In response to these challenges, collaborations are underway to develop VHP-compatible packaging and reformulate additives to meet evolving requirements.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Stringent biocompatibility and MDR/ISO 10993 requirements | -1.2% | Global; acute in EU under MDR | Medium term (2-4 years) |

| Intravascular particulate shedding scrutiny | -0.9% | North America and EU | Short term (≤ 2 years) |

| Sterilization material compatibility limitations | -0.7% | North America and EU | Medium term (2-4 years) |

| PFAS substitution risks slow adoption | -1.0% | EU; expanding U.S. state-level bans | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Biocompatibility and MDR/ISO 10993 Requirements Extend Time-To-Market

EU MDR-mandated extractables and leachables studies, costing USD 15,000 to 50,000 per formulation, extend approval cycles by up to 18 months.[3]European Commission, “Regulation (EU) 2017/745 on Medical Devices,” europa.eu ISO 10993-5 cytotoxicity and ISO 10993-10 sensitization protocols often identify residual photoinitiators and slip agents overlooked by routine quality control, necessitating reformulation. The requirement for dual compliance with FDA and MDR extraction conditions further increases testing burdens, particularly for Asia-Pacific OEMs with limited access to accredited laboratories.

Intravascular Particulate Shedding Scrutiny Elevates Integrity Testing

FDA 2019 guidance and AAMI TIR42 have intensified scrutiny on coating durability after simulated use. The lack of harmonized particulate limits requires manufacturers to establish device-specific acceptance criteria, increasing the risk of non-conformance. Increasing coating thickness to prevent delamination can paradoxically raise particulate mass if failure occurs, emphasizing the critical balance between durability and profile integrity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Additive Function: Antimicrobials Lead as Slip Modifiers Surge

In 2025, antimicrobial additives dominated the medical coating additives market with 28.16% shares. Silver-ion, zinc-oxide, and quaternary-ammonium systems meet hospital procurement standards and align with infection-control reimbursement incentives. However, varying pathways under the EPA and EU Biocidal Products Regulation extend global launch timelines. Slip modifiers are experiencing rapid growth, driven by a shift toward minimally invasive procedures and the phase-out of PFAS. By 2031, the market share for slip modifiers in medical coating additives is expected to increase by 230 basis points. This growth is attributed to the transition from PTFE micropowders to blends of silicone fluids, polyethylene glycol, and polyvinylpyrrolidone, maintaining key lubricity benchmarks.

By Additive Chemistry: Silicones Anchor While Nano-Additives Accelerate

In 2025, silicones accounted for 26.15% of revenue, driven by their unmatched thermal stability, ability to reduce surface energy, and tolerance to sterilization. However, silicone migration can disrupt downstream printing and adhesive bonding. This challenge has led formulators to limit cyclic siloxane content below emerging regulatory thresholds. By 2031, the market size for inorganic nano-additives in medical coatings will mark the segment's fastest CAGR at 14.98%. Silver nanoparticles, effective at sub-1 wt% loading, offer antimicrobial benefits, while zinc oxide nanoparticles, with their dual UV protection and antibacterial properties, are increasingly favored for wearable and implantable devices.

By Formulation Type: Solvent-Borne Dominates but UV/EB-Curable Gains

In 2025, solvent-borne systems accounted for 43.28% of revenue, supported by established qualification data and their versatility across resin families. While waterborne chemistries are gaining traction as OEMs pursue lower VOC profiles, challenges in drying kinetics and humidity sensitivity limit their adoption in high-volume lines. Formulations that are 100% solids and either UV or EB-curable are experiencing a robust CAGR of 15.55%. This growth is driven by mandates for zero-VOC emissions and the need for rapid cure times, even with a capital investment of USD 0.5-1 million for curing hardware. Solventless silicone systems are carving out premium niches, particularly in long-term implants and neurostimulation leads, where biostability is prioritized over cost.

By Application: Catheters Dominate as Implantables Accelerate

In 2025, catheters and guidewires will be driven by over 20 million procedures in North America and Europe. Implantables are emerging as the fastest-growing segment by 2031. Applications like drug-eluting stents, antimicrobial orthopedic plates, and neurostimulator leads are pushing for coating thicknesses of ≤5 µm, while requiring robust sterilization. Syringes and needles, staples in the volume market, rely on silicone oils to reduce plunger break-away force in pre-filled biologic platforms.

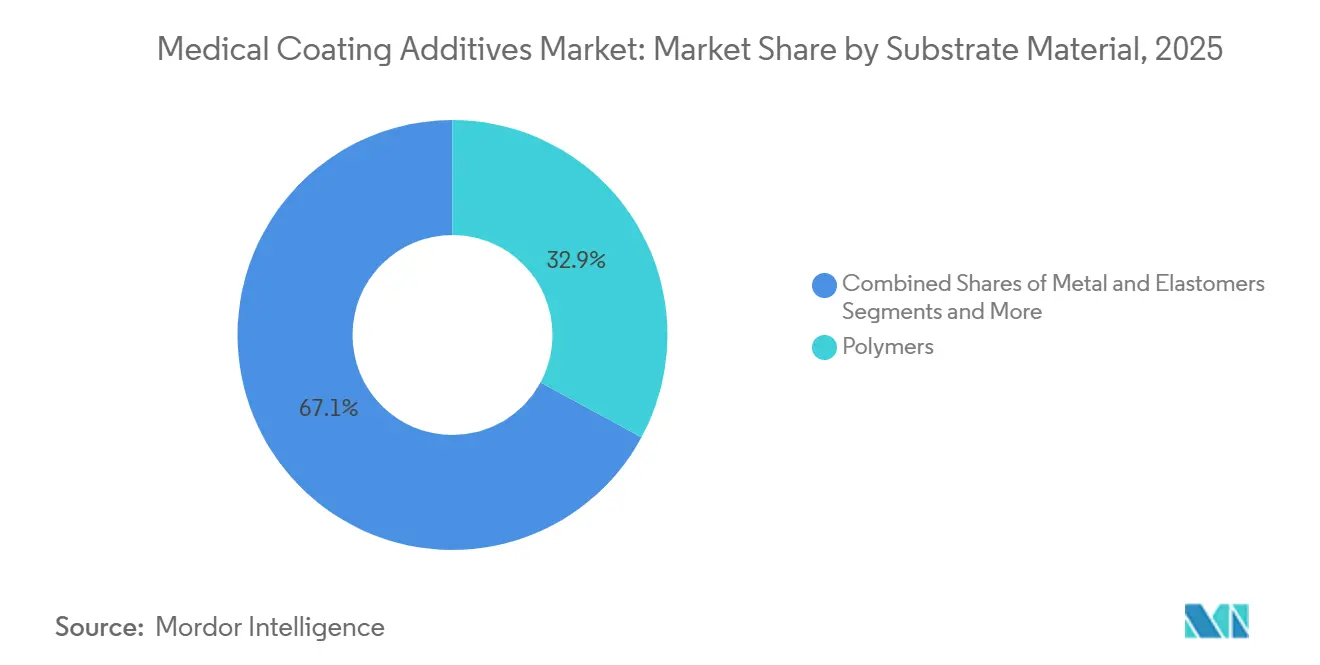

By Substrate Material: Polymers Lead and Accelerate

Polymers, capturing 32.89% of revenue in 2025, are also the fastest-growing substrate, with a CAGR of 14.35%. This growth is largely due to the replacement of traditional materials like steel and titanium with thermoplastic polyurethanes (TPU), PEEK, and nylon. Achieving the necessary surface energy often requires silane primers or atmospheric-plasma etching before coating, but the advantages of being lightweight and design-flexible make it worthwhile. Metal substrates continue to be essential for critical-load implants and guidewire cores. Properties like nitinol’s superelasticity and titanium’s ability to integrate with bone ensure sustained demand for coatings, though they come with the challenge of more intricate adhesion treatments.

Geography Analysis

In 2025, North America accounted for 36.71% of global revenue, driven by high per-capita health spending, widespread adoption of interventional cardiology, and established regulatory pathways for Class III devices. The FDA's recognition of VHP sterilization and the EPA's EtO emission limits necessitate requalification budgets, benefiting established suppliers with robust R&D and regulatory teams. While Mexico's near-shoring surge increases its capacity for catheter and syringe assembly, the region continues to rely on imports of high-purity silanes and UV oligomers from the United States and Europe.

Europe held a significant market share in 2025, supported by Germany's manufacturing strength and the United Kingdom's med-tech hubs. However, the EU's MDR mandates on chemical characterization are extending validation timelines and increasing costs, creating challenges for SMEs. Germany's orthopedic implant sector is driving demand for antimicrobial nano-silver powders, while France's catheter industry is adopting UV-curable, solvent-free topcoats to align with the EU's Green Deal. The Asia-Pacific region is set to lead with the highest CAGR of 14.56% through 2031. China's regulatory reforms are accelerating device registrations and encouraging local sourcing of silicone fluids and nano-silver additives. In India, Production-Linked Incentives (PLI) are being utilized to establish lines for catheter and implant coatings, although challenges persist with supply-chain fragmentation for high-purity organosilanes. Meanwhile, ASEAN's Medical Device Directive is harmonizing labeling and performance testing, reducing costs for multi-country launches and expanding market opportunities for regional OEMs.

Competitive Landscape

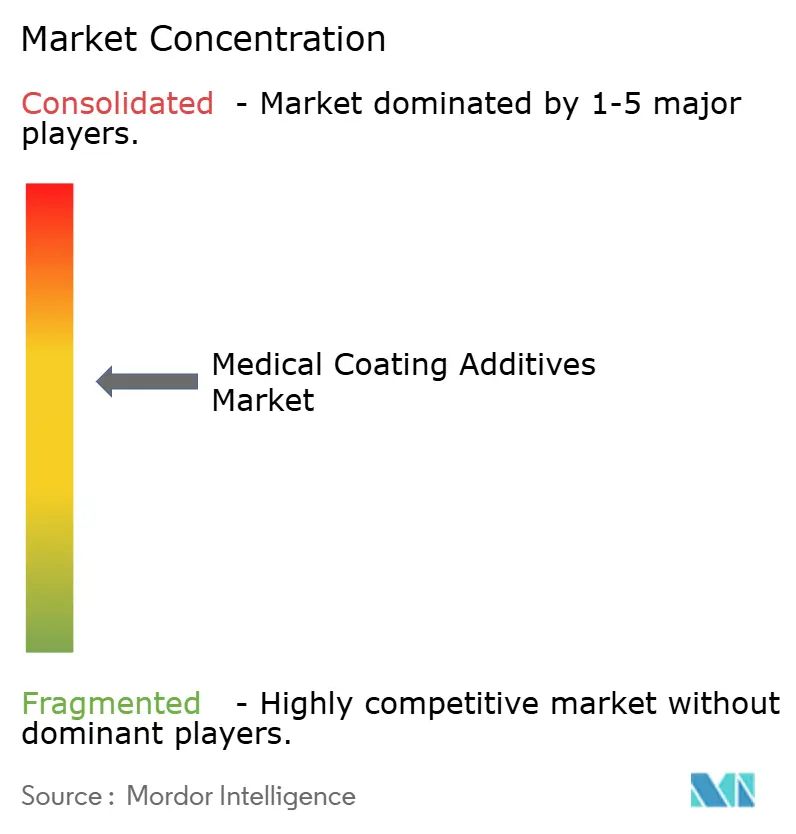

The medical coating additives market is moderately concentrated. DuPont, Wacker, Evonik, Arkema, and Elkem collectively secured 44% of the 2025 revenue, leveraging their supply of vertically integrated silicone, silane, and specialty acrylates. DuPont has strengthened its ecosystem position through partnerships for Tyvek-based VHP-compatible packaging. Wacker is expanding its silicone dispersion capacity to support PFAS-free slip agents. Evonik is utilizing its AEROSIL fumed-silica platform to enhance the stability of nano-silver suspensions. While Arkema's 2025 expansion in PVDF is linked to PFAS, it highlights the company's strategy to protect its fluoropolymer niches while investing in silicone alternatives. Elkem is advancing with high-purity medical-grade silicones and has introduced UV-curable SBS-silicone hybrids, which retain a sub-0.07 friction coefficient even after 20 cycles of VHP or EtO.

New entrants are focusing on comprehensive solutions. Microban’s AkoTech, launched in March 2025, integrates water- and solvent-based antimicrobial coatings with regulatory backing, simplifying the formulation process for contract manufacturers. Gelest, through a new distribution agreement with Nordmann in EMEA, is boosting the regional supply of adhesion promoters by expanding its silane-functional acrylate capacity. Lubrizol’s Tolerathane TPU, introduced in February 2026, caters to implantable device designers in need of oxidative-resistant elastomers supported by proven biocompatibility. In the zero-VOC UV/EB landscape, a divide emerges: major OEMs with their own coating lines absorb the capital costs, while smaller entities turn to contract coaters, who spread the equipment investment across various clients. These service providers enhance their offerings by combining formulation services, coatings, and requalification of sterilization modalities, streamlining the transition processes for EPA EtO and FDA VHP.

Medical Coating Additives Industry Leaders

DuPont

Evonik Industries AG:

Biocoat

Covalon Technologies Ltd.

Lubrizol Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Lubrizol launched Tolerathane TPU for implantable leads and structural heart devices.

- February 2026: Microban showcased Ascera, LapisShield, and MicroGuard antimicrobial technologies at PLASTINDIA 2026.

- February 2026: Lubrizol introduced LED chlorination technology, potentially enhancing CPVC resin biocompatibility.

- January 2026: DuPont opened entries for the 3rd Tyvek Sustainable Healthcare Packaging Awards.

- December 2025: Gelest appointed Nordmann as its primary EMEA distributor for specialty silanes and silicones.

Global Medical Coating Additives Market Report Scope

As per the scope of the report, medical coating additives are specialized chemicals incorporated in small quantities (typically less than 5%) into medical device coatings or pharmaceutical films to enhance their performance, stability, application properties, and functionality. These additives ensure the coating provides necessary features such as lubricity, biocompatibility, antimicrobial protection, or controlled drug release.

The medical coating additives market is segmented by additive function, additive chemistry, formulation type, application, substrate material, and geography. By additive function, the market includes antimicrobial additives, slip/lubricity modifiers, adhesion promoters, crosslinkers/curing agents, photoinitiators/UV stabilizers, wetting/flow/leveling & defoamers, and biocompatible pigments/UV absorbers. By additive chemistry, the market is segmented into silicones & silicone fluids, organosilanes, fluoropolymers/PTFE micropowders, polyurethane-based additives, acrylics/methacrylates (UV), inorganic nano-additives, and polyolefin waxes & specialty biobased polymers. By formulation type, the market includes solvent-borne, water-borne, 100% solids UV/EB-curable, and solventless silicone systems. By application, the market is divided into catheters & guidewires, syringes & needles, implantable devices, surgical instruments & electrosurgery, diagnostics & consumables, and wound care & dressings. By substrate material, the market is segmented into metals (stainless steel, nitinol, titanium), polymers (polyolefins (PE, PP), polyurethanes/TPU, PEBAx, nylon, PEEK, PVC, PC), elastomers, and glass & composites. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Antimicrobial Additives |

| Slip/Lubricity Modifiers |

| Adhesion Promoters |

| Crosslinkers/Curing Agents |

| Photoinitiators/UV Stabilizers |

| Wetting/Flow/Leveling & Defoamers |

| Biocompatible Pigments/UV Absorbers |

| Silicones & Silicone Fluids |

| Organosilanes |

| Fluoropolymers/PTFE Micropowders |

| Polyurethane-based Additives |

| Acrylics/Methacrylates (UV) |

| Inorganic Nano-additives |

| Polyolefin Waxes & Specialty Biobased Polymers |

| Solvent-borne |

| Water-borne |

| 100% Solids UV/EB-curable |

| Solventless Silicone Systems |

| Catheters & Guidewires |

| Syringes & Needles |

| Implantable Devices |

| Surgical Instruments & Electrosurgery |

| Diagnostics & Consumables |

| Wound Care & Dressings |

| Metals | Stainless steel |

| Nitinol | |

| Titanium | |

| Polymers | Polyolefins (PE, PP) |

| Polyurethanes/TPU, Pebax, Nylon | |

| PEEK, PVC, PC | |

| Elastomers | |

| Glass & Composites |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of APAC | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of MEA | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Additive Function | Antimicrobial Additives | |

| Slip/Lubricity Modifiers | ||

| Adhesion Promoters | ||

| Crosslinkers/Curing Agents | ||

| Photoinitiators/UV Stabilizers | ||

| Wetting/Flow/Leveling & Defoamers | ||

| Biocompatible Pigments/UV Absorbers | ||

| By Additive Chemistry | Silicones & Silicone Fluids | |

| Organosilanes | ||

| Fluoropolymers/PTFE Micropowders | ||

| Polyurethane-based Additives | ||

| Acrylics/Methacrylates (UV) | ||

| Inorganic Nano-additives | ||

| Polyolefin Waxes & Specialty Biobased Polymers | ||

| By Formulation Type | Solvent-borne | |

| Water-borne | ||

| 100% Solids UV/EB-curable | ||

| Solventless Silicone Systems | ||

| By Application | Catheters & Guidewires | |

| Syringes & Needles | ||

| Implantable Devices | ||

| Surgical Instruments & Electrosurgery | ||

| Diagnostics & Consumables | ||

| Wound Care & Dressings | ||

| By Substrate Material | Metals | Stainless steel |

| Nitinol | ||

| Titanium | ||

| Polymers | Polyolefins (PE, PP) | |

| Polyurethanes/TPU, Pebax, Nylon | ||

| PEEK, PVC, PC | ||

| Elastomers | ||

| Glass & Composites | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of APAC | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of MEA | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large will the medical coating additives market be by 2031?

The medical coating additives market size is forecast to reach USD 3.2 billion by 2031, expanding at an 11.59% CAGR from 2026.

Which application area is growing fastest within coating additives?

Implantable devices are projected to advance at a 14.14% CAGR through 2031 as drug-eluting stents, antimicrobial orthopedic implants, and neurostimulator leads proliferate.

What region will post the highest growth rate?

Asia-Pacific is expected to lead regional growth with a 14.56% CAGR through 2031, driven by manufacturing localization and regulatory harmonization.

Which chemistry segment is expanding most rapidly?

Inorganic nano-additives, especially silver and zinc oxide nanoparticles, are projected to register the highest CAGR at 14.98% through 2031.

How are PFAS restrictions influencing product development?

EU and U.S. state PFAS bans accelerate the shift from PTFE slip agents to silicone, silane, and hydrocarbon wax alternatives, prompting iterative validation to maintain low friction coefficients while meeting new compliance thresholds.

Who are the leading suppliers of medical coating additives?

DuPont, Wacker, Evonik, Arkema, and Elkem collectively held 44% market share in 2025, underscoring their influence on pricing and technology roadmaps.

Page last updated on: