Multi-Mode Receiver Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 1.55 Billion |

| Market Size (2030) | USD 1.92 Billion |

| Growth Rate (2025 - 2030) | 4.41% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Multi-Mode Receiver Market Analysis by Mordor Intelligence

The multi-mode receiver market size stands at USD 1.55 billion in 2025 and is forecast to reach USD 1.92 billion by 2030, expanding at a 4.41% CAGR. Fleet modernization, mandatory performance-based navigation (PBN) deadlines, and rapid advances in software-defined radio (SDR) architectures keep demand resilient despite supply-chain challenges. Commercial airframers embed multi-mode receivers during production to meet regulatory timelines, while retrofit programs tackle aging cockpit avionics. Cyber-secure, multi-constellation designs are now a competitive differentiator, particularly for operators that fly polar routes or into satellite-navigation-contested airspace. At the same time, certification hurdles, 5G C-band interference, and RF component shortages temper near-term growth.

Key Report Takeaways

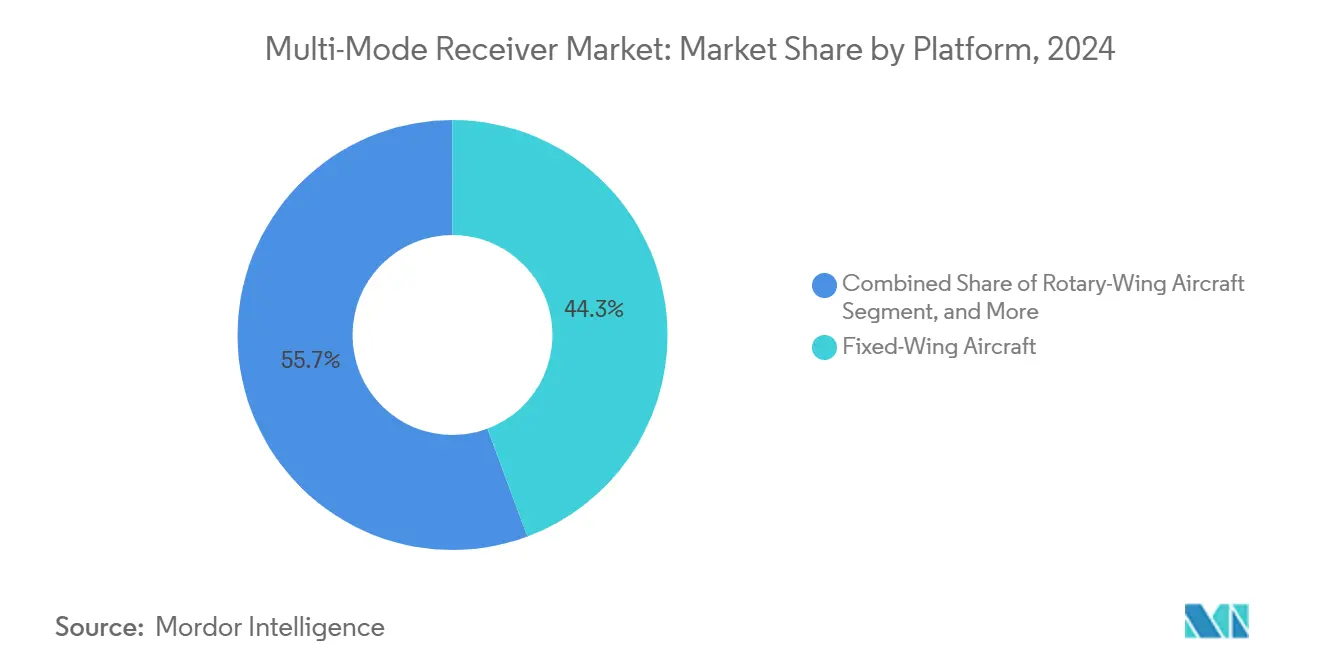

- By platform, fixed-wing aircraft led with 44.32% of multi-mode receiver market share in 2024, while unmanned aerial vehicles are projected to grow at a 5.13% CAGR through 2030.

- By fit, line-fit installations accounted for 62.16% of the multi-mode receiver market size in 2024, whereas retrofit programs are advancing at a 6.54% CAGR to 2030.

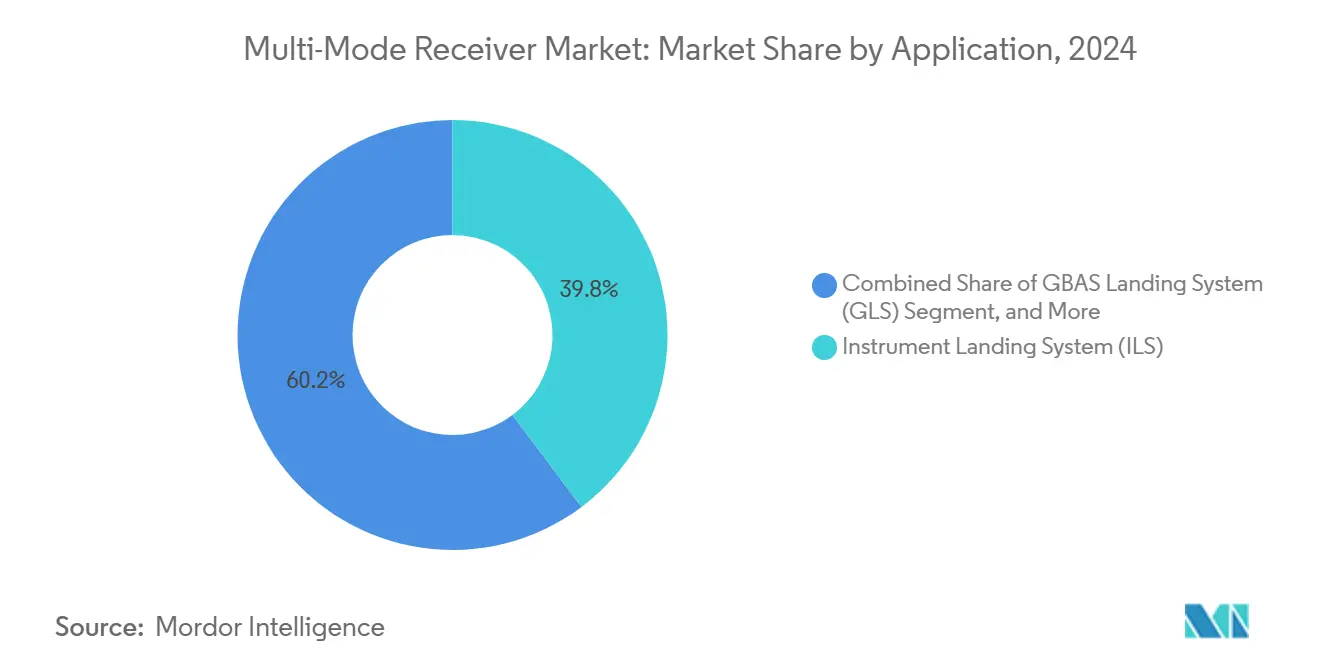

- By application, instrument-landing-system solutions held 39.76% of the multi-mode receiver market size in 2024; navigation and positioning systems are forecast to expand at a 5.32% CAGR during the same horizon.

- By end user, commercial aviation captured 55.89% of the multi-mode receiver market size in 2024, while business and general aviation shows a 5.17% CAGR outlook to 2030.

- By geography, North America commanded 37.91% of the multi-mode receiver market share in 2024, while the Middle East and Africa region is forecast to grow at a 4.96% CAGR through 2030.

Market Trends and Insights

Drivers Impact Analysis of Multi-Mode Receiver Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising commercial aircraft deliveries | +0.8% | Asia-Pacific, Middle East | Medium term (2-4 years) |

| Mandatory PBN deadlines | +1.2% | North America, Europe | Short term (≤ 2 years) |

| Fleet modernization and retrofit programs | +0.9% | North America, Europe | Medium term (2-4 years) |

| Shift toward software-defined integrated avionics | +0.7% | Global | Long term (≥ 4 years) |

| Urban-air-mobility certification needs | +0.4% | North America, Europe | Long term (≥ 4 years) |

| SBAS adoption for polar routes | +0.3% | Arctic and Antarctic corridors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Commercial Aircraft Deliveries

Boeing and Airbus backlog levels force OEMs to prioritize SDR-capable navigation suites on every new production line-fit, locking in orders for high-channel multi-mode receivers well before final assembly. [1]U.S. Government Accountability Office, “Commercial Aviation Manufacturing: Supply-Chain Challenges,” gao.gov Middle-East carriers enlarge fleets faster than any other region, elevating baseline receiver demand for narrow-body and wide-body types serving hub-and-spoke networks.

Mandatory Performance-Based Navigation Deadlines

ICAO’s PBN roadmap replaces legacy ground-based aids with satellite-augmented navigation, compelling air operators to retrofit or retire non-compliant fleets by 2027 in the United States and 2028 in the European Union. [2]International Civil Aviation Organization, “Performance-Based Navigation,” icao.int As a result, the multi-mode receiver market registers predictable replacement cycles insulated from discretionary capital-budget delays.

Fleet Modernization and Retrofit Programs

U.S. Army C-130 avionics upgrades and business-jet cockpit refreshes show how combined line-fit and retrofit activity expands total addressable volume. Programs bundle new flight-management systems, enhanced vision, and SBAS-enabled receivers in single-supplier packages, shortening downtime while boosting residual aircraft values.

Shift Toward Software-Defined Integrated Avionics

SDR architectures from Collins Aerospace and Honeywell reduce form-factor, weight, and certification costs by loading multiple navigation waveforms onto common hardware. Over-the-air updates let operators add Galileo E6 or GPS III signals without removing the receiver, future-proofing fleets against spectrum reallocation events. [3]Collins Aerospace, “Open Architecture Terminal for U.S. Air Force,” collinsaerospace.com

Restraints Impact Analysis of Multi-Mode Receiver Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High certification and compliance costs | -0.6% | North America, Europe | Short term (≤ 2 years) |

| RF-component supply-chain disruptions | -0.4% | Global | Medium term (2-4 years) |

| Cybersecurity risks in multi-sensor fusion | -0.3% | Global | Long term (≥ 4 years) |

| 5G spectrum reallocation pressures | -0.5% | North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Certification and Compliance Costs

DO-178C and DO-254 approvals can double non-recurring engineering expenses for mid-tier suppliers, tilting the playing field toward integrated primes with in-house design assurance resources. Smaller innovators, therefore, struggle to meet schedule-driven airline retrofits, delaying broader technology diffusion in the multi-mode receiver market.

RF-Component Supply-Chain Disruptions

End-of-life notices for gallium-arsenide mixers and SAW filters force redesigns just as avionics manufacturers submit qualification test plans, stretching receiver lead-times beyond 30 weeks. Government-funded “trusted foundry” agreements mitigate only part of the risk, leaving the multi-mode receiver market exposed to price spikes and allocation caps.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Multi-Mode Receiver Market Segment Analysis

By Platform:

Fixed-Wing Dominance Faces UAV DisruptionFixed-wing jets continue to anchor the multi-mode receiver market, yet UAV demand rises quickly as regulators craft beyond-visual-line-of-sight (BVLOS) rules that require certified navigation equipment. In 2024, fixed-wing platforms represented 44.32% of the multi-mode receiver market share, but the UAV segment shows a 5.13% CAGR to 2030. Manufacturers integrate lightweight SDR receivers with anti-interference algorithms, enabling drones to operate in GPS-contested zones. Commercial freighters and twin-aisle passenger aircraft still drive the largest unit volumes, especially on polar and oceanic routes where SBAS or GBAS signals sharpen waypoint accuracy. Meanwhile, defense forces equip Group 5 UAVs with M-Code-ready receivers to secure precision-strike missions. This interplay of civil and military adoption underscores how the multi-mode receiver market evolves in lockstep with airspace-integration policy.

By Fit:

Line-Fit Leadership Challenged by Retrofit GrowthLine-fit deliveries captured 62.16% of the multi-mode receiver market size in 2024 as airframers wired navigation modules directly into new cockpits. Retrofit spending, however, registers a faster 6.54% CAGR, propelled by carriers refreshing narrow-body fleets to comply with CAT III SBAS landing requirements. STC-approved upgrade kits allow installation during C-checks, minimizing downtime. In emerging markets, discretionary retrofit outlays lag because operators await clarity on PBN phase-in dates, but mandated equipage creates a step-function in demand once rules are finalized. Suppliers that bundle receivers with flight-management-system software stand to capture higher margins, particularly in the business-aviation aftermarket, where owners value integrated upgrade packages.

By Application:

ILS Maturity Contrasts Navigation GrowthInstrument Landing System (ILS) receivers remain ubiquitous, holding 39.76% of the multi-mode receiver market size in 2024. Yet satellite-based navigation and positioning solutions add new growth at a 5.32% CAGR, reflecting increasing GBAS and SBAS deployments worldwide. GBAS can support up to 48 approach procedures per installation, lowering airport CAPEX and extending service volumes beyond traditional localizer antennas. Airlines, therefore, favor receivers that decode VHF data broadcast (VDB) as well as L1/L5 dual-frequency GNSS signals. In remote Arctic routes, dual-constellation SBAS receivers provide LPV-200 minima, reducing diversion risks. Consequently, next-generation multi-mode receivers embed ILS, MLS, GBAS, and four-constellation GNSS in a single chassis, preparing operators for mixed-equipage environments during the transition decade.

By End User:

Commercial Leadership Faces Business-Aviation ChallengeCommercial airlines owned 55.89% of the multi-mode receiver market size in 2024, reflecting large installed bases and strict compliance timetables. Business and general aviation, though smaller today, expands at a 5.17% CAGR as corporations modernize cabins and cockpits to protect asset values. OEMs now offer factory-fit SBAS receivers on turboprops and light jets, closing capability gaps with airline transports. Military aviation secures long-term funding for M-Code equipment, but project pacing often trails civil-sector adoption because of platform-specific qualification testing. Special-mission operators-search-and-rescue, aerial survey, law enforcement-gravitate toward multi-sensor receivers that fuse GNSS with terrain-referenced navigation, creating pockets of premium demand within the broader multi-mode receiver market.

Geography Analysis

North America Multi-Mode Receiver Market

North America held a 37.91% share of the multi-mode receiver market in 2024, anchored by the FAA NextGen program and more than 100 runway ends equipped with GBAS precision-approach procedures. U.S. military M-Code rollouts sustain parallel demand in defense fleets, while Canadian regulators codify RPAS BVLOS frameworks that specify SBAS-capable receivers for command-and-control redundancy. Supply-chain concentration in U.S. semiconductor nodes partly shields local producers from export-control volatility, yet C-band radar-altimeter interference drives immediate retrofit cycles.

Europe Multi-Mode Receiver Market

Europe benefits from EGNOS Safety-of-Life services and two decades of EUROCONTROL GBAS research, positioning the region as both technology developer and early adopter. The European Commission’s Flightpath 2050 ambition for carbon-neutral growth supports widespread PBN adoption to shorten track miles. Airframers in France, Germany, and Spain integrate open-architecture navigation suites, and dual-qualified ILS-GBAS receivers become standard on A320 family retrofit programs. Military programs, such as German Eurofighter Arexis upgrades, further diversify demand.

MEA and APAC Multi-Mode Receiver Market

The Middle East and Africa post the highest regional CAGR at 4.96% as airport construction pipelines exceed USD 1 trillion in committed capex. Mega-hubs like Dubai International push for CAT II/III GBAS to raise peak runway throughput, and Gulf carriers prefer SDR-based receivers that ease fleet-wide software upgrades. Africa’s adoption rate hinges on multilateral SBAS coverage agreements, yet satellite-based services promise leapfrog gains where ground-based ILS is cost-prohibitive. Asia-Pacific markets deploy India’s GAGAN and Australia’s SouthPAN, creating localized standards that nonetheless align with RTCA DO-253D receiver performance, widening the multi-mode receiver market’s addressable base.

Competitive Landscape

The multi-mode receiver market is moderately fragmented, with the top five suppliers holding roughly 55% combined share. Honeywell, Thales, and Collins Aerospace leverage vertical integration and large installed bases to renew long-term service agreements for airlines and defense ministries. Honeywell’s M-Code-certified EAGLE-M EGI and quantum-sensor navigation contracts underscore the company’s push into GPS-denied capabilities. Thales couples receivers with airborne surveillance radars, providing a platform-agnostic growth conduit into UAV and MALE drone sectors.

Collins Aerospace’s open-mission-systems radios highlight the industry shift from hardware-centric to software-centric navigation, giving primes an upgrade-as-a-service revenue stream. Mid-tier firms-BAE Systems, Saab, Indra-differentiate via anti-jamming algorithms or electronic-warfare synergies. Startups targeting urban-air-mobility platforms pursue modular STC strategies to enter service quickly, but high DO-178C costs often necessitate partnerships with traditional avionics integrators.

M&A reshapes the landscape: Honeywell’s USD 1.9 billion CAES acquisition broadens RF-front-end capabilities, while Thales’ purchase of Cobham Aerospace Communications brings cockpit voice and satcom integration know-how. Competitive intensity centers on lifecycle cost, SWaP-C (size, weight, power, cost), and cybersecurity certification, pushing all players to adopt common avionics reference architectures that streamline retrofit labor.

Multi-Mode Receiver Industry Leaders

Honeywell International Inc.

Thales Group

Collins Aerospace (RTX Corporation)

BAE Systems plc

Garmin Ltd.

- *Disclaimer: Major Players sorted in no particular order

Multi-Mode Receiver Market Companies Covered in this Report

- Honeywell International Inc.

- Thales Group

- Collins Aerospace (RTX Corporation)

- BAE Systems plc

- Garmin Ltd.

- Leonardo S.p.A.

- Safran S.A.

- Saab AB

- Indra Sistemas S.A.

- Becker Avionics GmbH

- HENSOLDT AG

- Rohde & Schwarz GmbH & Co KG

- Curtiss-Wright Corporation

- Astronics Corporation

- L3Harris Technologies Inc.

- Cobham Limited

- Avidyne Corporation

- FreeFlight Systems Inc.

- Moog Inc.

- ACSS LLC (L3Harris & Thales JV)

Recent Industry Developments in Multi-Mode Receiver Market

- July 2025: Honeywell won U.S. Department of Defense contracts to develop quantum-sensor navigation under the Transition of Quantum Sensing program, targeting GPS-independent flight solutions.

- July 2025: Thales reported first-half 2025 revenue of EUR 10.3 billion, buoyed by defense avionics and a 26-unit Rafale Marine order from India.

- June 2025: Thales and Turgis Gaillard launched an all-French MALE drone and AirMaster S radar package for ISR missions.

- June 2025: RTX’s Collins Aerospace secured a multi-billion-dollar subcontract on the Survivable Airborne Operations Center program, incorporating advanced navigation systems.

Global Multi-Mode Receiver Market Report Scope

Segmentation Overview

| Fixed-Wing Aircraft |

| Rotary-Wing Aircraft |

| Unmanned Aerial Vehicles (UAV) |

| Advanced Air Mobility (eVTOL) |

| Regional Jets |

| Line-fit |

| Retrofit |

| Instrument Landing System (ILS) |

| GBAS Landing System (GLS) |

| Microwave Landing System (MLS) |

| Navigation and Positioning |

| Commercial Aviation |

| Military Aviation |

| Business and General Aviation |

| Special-Mission Aviation |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Platform | Fixed-Wing Aircraft | ||

| Rotary-Wing Aircraft | |||

| Unmanned Aerial Vehicles (UAV) | |||

| Advanced Air Mobility (eVTOL) | |||

| Regional Jets | |||

| By Fit | Line-fit | ||

| Retrofit | |||

| By Application | Instrument Landing System (ILS) | ||

| GBAS Landing System (GLS) | |||

| Microwave Landing System (MLS) | |||

| Navigation and Positioning | |||

| By End User | Commercial Aviation | ||

| Military Aviation | |||

| Business and General Aviation | |||

| Special-Mission Aviation | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is driving airlines to upgrade navigation receivers?

Regulatory PBN deadlines and the availability of GBAS and SBAS precision-approach services push operators to adopt multi-mode receivers quickly.

How fast is the multi-mode receiver market expected to grow?

The market is projected to expand at a 4.41% CAGR from USD 1.55 billion in 2025 to USD 1.92 billion by 2030.

Which aircraft platforms show the highest growth potential for new receivers?

Unmanned aerial vehicles lead growth with a forecast 5.13% CAGR as BVLOS regulations mature.

Why are software-defined radios important for future receivers?

SDR architectures enable over-the-air waveform updates, reducing hardware swaps and future-proofing fleets against new GNSS constellations.

What regional market shows the fastest expansion?

The Middle East and Africa region posts the highest CAGR, supported by large airport-expansion budgets and rapid fleet growth.

How do certification costs affect new entrants?

DO-178C and DO-254 compliance can double development budgets, restricting market entry to well-capitalized or partnered firms.

Page last updated on: