OTA Transmission Platform Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

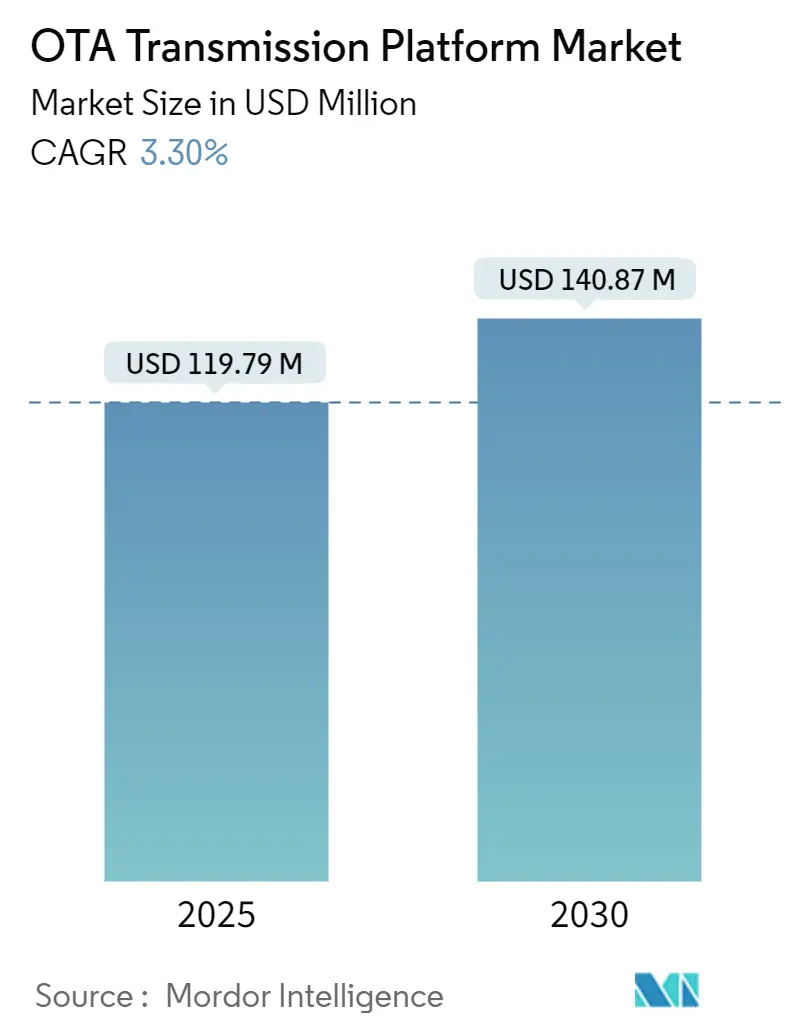

| Market Size (2025) | USD 119.79 Million |

| Market Size (2030) | USD 140.87 Million |

| Growth Rate (2025 - 2030) | 3.30% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

OTA Transmission Platform Market Analysis by Mordor Intelligence

The OTA transmission platform market size stands at USD 119.79 million in 2025 and is forecast to reach USD 140.87 million by 2030, reflecting a 3.30% CAGR over the period. Current momentum is shaped by broadcasters shifting capital from legacy analog equipment toward ATSC 3.0, 5G-Broadcast, and solid-state architectures that lower operating costs yet require significant up-front spending.[1]European Broadcasting Union, “NextGen TV: US Broadcasters Transition to Enhanced Quality and Services,” EBU.ch Regulatory milestones such as the United States ATSC 3.0 mandate and parallel digital switchover deadlines in Asia-Pacific are compressing investment cycles, while spectrum repack programs intensify the focus on energy-efficient and software-defined solutions. Competitive strategies pivot on integrating IP-native monitoring, predictive maintenance, and cloud orchestration as broadcasters balance operational continuity with next-generation service rollouts. Despite modest top-line expansion, the OTA transmission platform market offers targeted growth pockets in monitoring software, hybrid broadcast-broadband services, and government-funded emergency alert infrastructure.

Key Report Takeaways

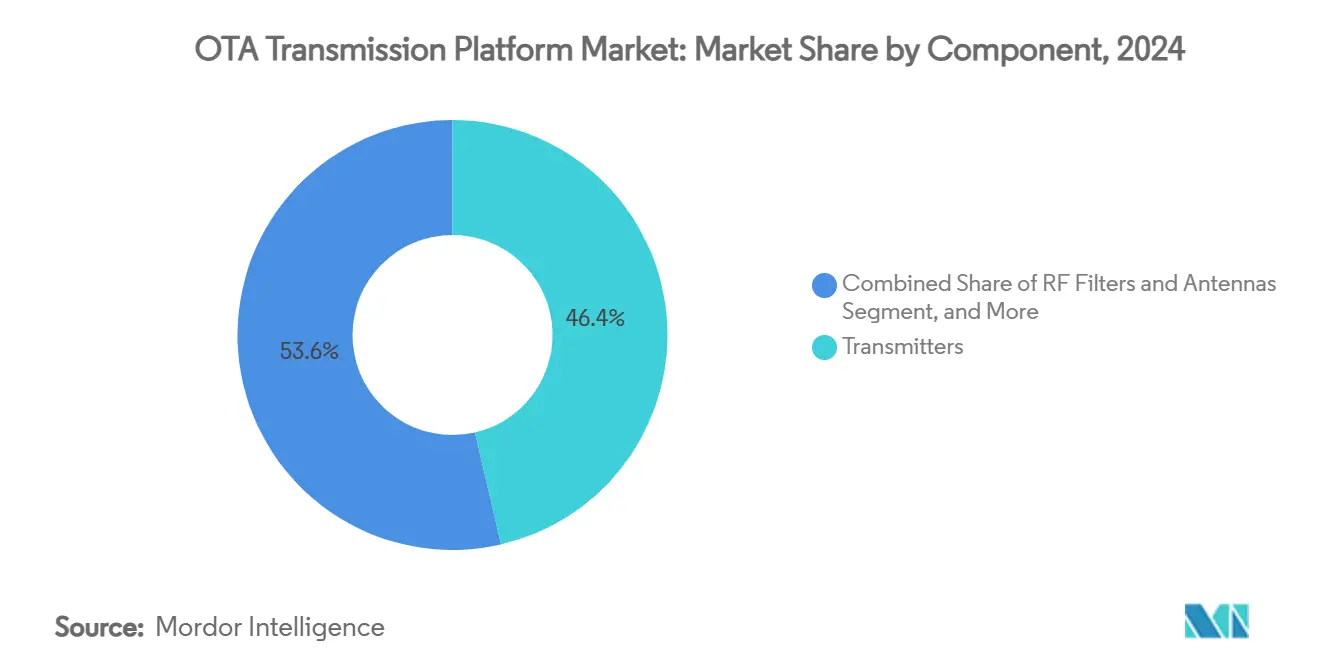

- By component, transmitters captured a 46.37% share of the OTA Transmission Platform market in 2024.

- By technology, the OTA Transmission Platform market for 5G-Broadcast/FeMBMS is projected to grow at a 5.83% CAGR between 2025 to 2030.

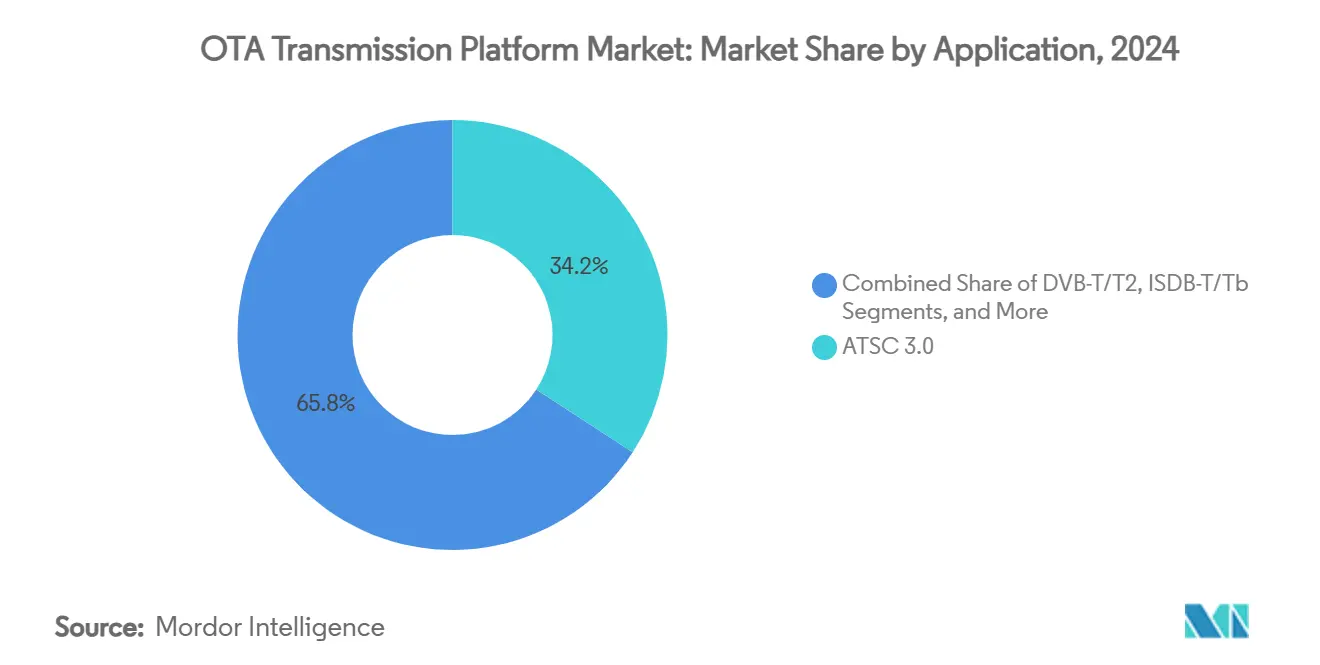

- By application, television broadcasting captured a 58.32% share of the OTA Transmission Platform market in 2024.

- By end-user, the OTA Transmission Platform market for government and defense is projected to grow at a 6.23% CAGR between 2025 to 2030.

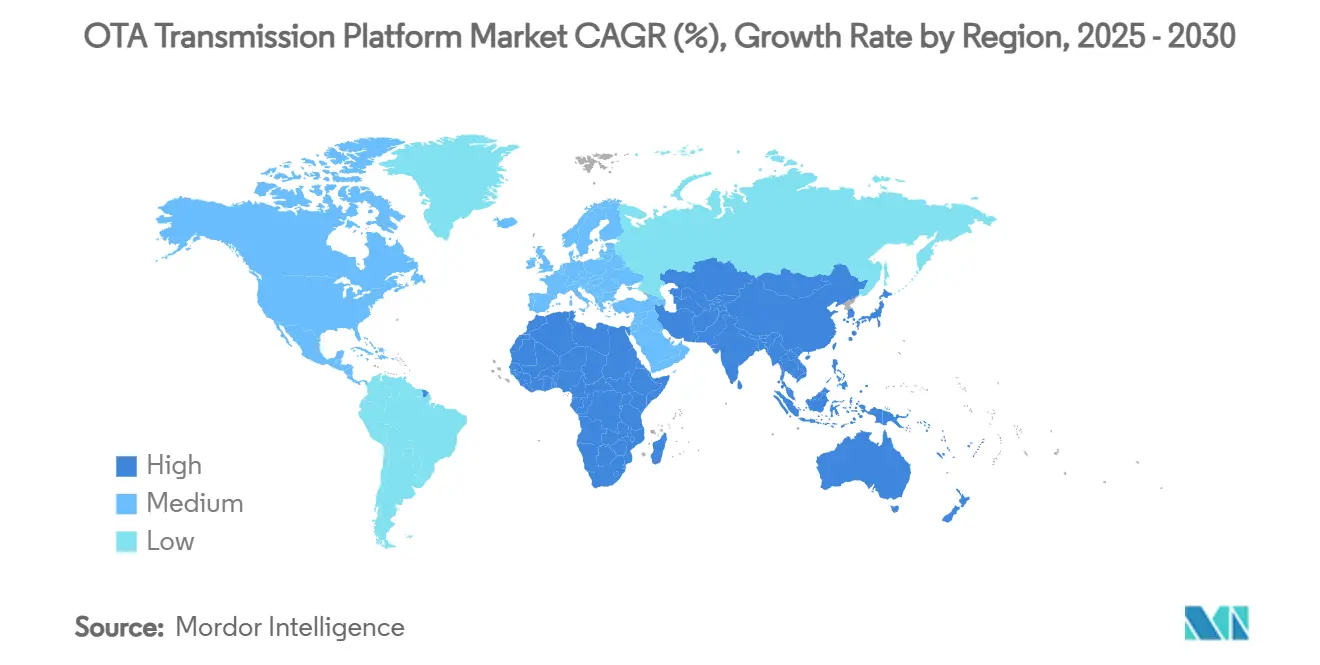

- By geography, North America captured a 33.54% share of the OTA Transmission Platform market in 2024.

Global OTA Transmission Platform Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid transition to ATSC 3.0 / NEXTGEN TV in the U.S. | +1.2% | North America, with spillover to Latin America | Medium term (2-4 years) |

| Global digital‐switchover deadlines accelerating cap-ex cycles | +0.8% | Global, with concentration in Asia-Pacific and Africa | Short term (≤ 2 years) |

| Growth of UHD/4K and HDR linear content | +0.6% | Global, led by North America and Europe | Long term (≥ 4 years) |

| Energy-efficient solid-state transmitters lowering TCO | +0.4% | Global, with early adoption in Europe and North America | Medium term (2-4 years) |

| 5G-Broadcast and multicast trials enabling hybrid networks | +0.5% | Global, with pilot programs in Europe and Asia-Pacific | Long term (≥ 4 years) |

| Government push for Direct-to-Mobile emergency alerts | +0.3% | Global, with priority in North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid transition to ATSC 3.0 / NEXTGEN TV in the U.S.

The FCC mandate obliges stations to simulcast ATSC 1.0 and ATSC 3.0, doubling transmission outlays without immediate monetization, yet 85% of current ATSC 3.0 markets already carry HDR content. Broadcasters must compress procurement cycles, manage spectrum-sharing constraints, and address consumer receiver adoption, creating a compliance-before-cashflow paradigm that shapes capital planning. Vendors able to deliver software-upgradable transmitters and remote monitoring gain favor as stations seek to defer full replacement costs. Financing models that bundle equipment, support, and license fees into service contracts alleviate liquidity pressures for smaller operators. ATSC 1.0 switch-off timing remains politically sensitive, so most buyers prioritize dual-mode gear that safeguards near-term coverage obligations

Global digital-switchover deadlines accelerating cap-ex cycles

Mandatory analog shut-off dates in Asia-Pacific and Africa pull forward orders for power amplifiers, antennas, and combiners, compressing vendor lead times and straining component supply chains. Roughly 89% of U.S. stations gained signal reach post-digital, while 11% required translators—an outcome now guiding emerging-market regulators toward proactive gap-fill planning. Developing markets often skip incremental upgrades and commit to all-IP control backbones, boosting demand for integrated encoder–multiplexer platforms. Equipment vendors must scale localized support and training as technical skills shortages could impede on-time deployments. Switchover clustering inflates short-term revenues yet risks mid-cycle troughs once compliance peaks subside.

Growth of UHD/4K and HDR linear content

Live sports, entertainment, and news producers increasingly specify 4K/HDR workflows, compelling broadcasters to upgrade encoders, exciters, and high-power solid-state transmitters able to sustain higher bit-rates within limited spectrum. The European Broadcasting Union guidance on HDR live production standardizes colorimetry and dynamic-range parameters, anchoring equipment specifications globally. Terrestrial players are under pressure to match the visual fidelity already common on OTT platforms, accelerating joint investments in compression algorithms such as HEVC and VVC. Premium picture quality also drives a virtuous device-upgrade cycle in consumer displays, indirectly raising the addressable advertising inventory for broadcasters. Power budgets increase with higher throughput, making energy-efficient transmitter design a strategic imperative.

Energy-efficient solid-state transmitters lowering TCO

Solid-state architectures replace high-maintenance vacuum-tube systems, cutting electricity consumption and downtime by double-digit percentages according to Department of Energy benchmarks. ENERGY STAR procurement criteria now cover high-power RF systems, allowing broadcasters to qualify for utility rebates that shorten payback periods.[2]U.S. Department of Energy, “Distribution Transformers,” Energy.govRemote diagnostics and hot-swappable modules reduce truck rolls, a decisive factor for unmanned mountain or rural sites. Vendors that integrate power-supply telemetry into cloud dashboards help operators benchmark site-level performance and negotiate favorable electricity tariffs. Environmental regulations and corporate ESG targets are turning energy efficiency from a cost-avoidance tactic into a board-level KPI.

Restraints Impact Analysis*

| Restraint | (~) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High up-front capex for high-power RF systems | -0.9% | Global, with acute impact in developing markets | Short term (≤ 2 years) |

| Cord-cutting and OTT substitution pressure on broadcaster ROI | -0.7% | Global, with concentration in North America and Europe | Long term (≥ 4 years) |

| Spectrum repack / re-allocation uncertainty | -0.4% | Global, with priority in North America and Europe | Medium term (2-4 years) |

| Patent and royalty burden of ATSC 3.0 / 5G-Broadcast IP | -0.3% | Global, with focus on ATSC 3.0 markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High up-front capex for high-power RF systems

Capital requirements for multi-megawatt solid-state stacks exceed the budget envelopes of many independent stations, prompting interest in leasing, build-operate-transfer, and shared-infrastructure models. Financing complexity compounds when stations must also fund encoders, antennas, and tower reinforcements within the same budget window. Where public subsidies are unavailable, broadcasters may stagger upgrades, slowing equipment order flow. Vendors that package financing or as-a-service contracts often secure market share in developing regions. Persistent cost barriers encourage demand for lower-power edge transmitters coupled with single-frequency networks that extend coverage without high mast investments.

Cord-cutting and OTT substitution pressure on broadcaster ROI

Linear viewership erosion trims advertising yields, shrinking the funds available for capital projects just as spectrum reclamation forces technical modernization. Operators redirect resources toward original content and digital apps to stem audience flight, delaying transmitter refresh cycles. The perceived risk of under-utilized broadcast capacity deters CFOs from sanctioning large RF purchases unless allied to hybrid OTT strategies. Equipment vendors counter by bundling analytics that quantify incremental reach gains over streaming only. Long-term, broadcaster viability hinges on demonstrating that free-to-air distribution complements on-demand platforms rather than cannibalizing them.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Transmitters anchor spend as monitoring systems race ahead

Transmitters contributed 46.37% of 2024 revenue, underscoring their indispensability in any over-the-air rollout. Mandatory digital conversion and power-boost requirements keep the category at the heart of the OTA transmission platform market, but growth now tilts toward solid-state designs that cut energy bills and maintenance visits. RF filters, combiners, and high-gain antennas round out site hardware, yet their sales track closely with transmitter refresh timelines. Meanwhile, monitoring and control platforms outperformed with a 4.57% CAGR and represent a rising share of the OTA transmission platform market size as broadcasters centralize network operations and deploy predictive analytics to reduce truck rolls.

Integration trends reveal a pivot from discrete hardware toward software-defined, IP-native ecosystems that bundle exciter, encoder, and telemetry in a single chassis. Vendors incorporating SNMP, REST, and cloud APIs allow broadcasters to automate fault detection and energy optimization. As remote-first management becomes standard, monitoring suites harness machine learning to forecast component wear and flag out-of-spec emissions. Compliance logging modules shorten audit cycles, a value driver in jurisdictions with stringent proof-of-performance rules. Consequently, monitoring system revenues are expected to command a larger fraction of OTA transmission platform market share by decade-end.

By Technology: ATSC 3.0 leads but 5G-Broadcast gains mindshare

ATSC 3.0 held 34.18% market share in 2024, buoyed by FCC mandates and strong North American vendor ecosystems. Its scalable OFDM architecture, interactive services, and robust mobile reception fulfill broadcaster ambitions for datacasting and addressable advertising. Yet the technology roadmap now intersects with 5G-Broadcast, projected to grow at 5.83% CAGR, as telecom operators pilot spectrum-efficient multicast overlays that dovetail with core cellular networks.

Hybrid solutions capable of toggling between DVB-T2, ISDB-T, and ATSC 3.0 modes within a unified exciter maximize asset life in regions where spectrum policy remains fluid. Multistandard chipsets reduce SKU complexity, enabling global OEMs to leverage scale advantages and shrink per-unit pricing. Software-licensed upgrades let stations activate new waveforms post-deployment, a hedge against evolving regulations. Long-term, convergence on IP-native delivery is likely, positioning the OTA transmission platform industry to operate seamlessly across broadcast and broadband pipes.

By Application: Television dominates while digital radio accelerates

Television broadcasting accounted for 58.32% of 2024 revenue, reflecting entrenched free-to-air consumption and regulatory must-carry provisions. The segment continues to invest in higher-order modulation, advanced error correction, and HEVC/VVC compression to support UHD services without additional spectrum. In parallel, radio/DAB recorded the fastest 4.37% CAGR as automotive OEMs integrate digital tuners and regulators sunset analog FM in parts of Europe and Asia.

Emerging datacasting, IoT broadcast, and direct-to-mobile alerting represent nascent but promising avenues that rely on broadcast’s point-to-multipoint economics. Public warning systems receive policy backing, ensuring stable funding streams independent of advertising cycles. Stations increasingly position themselves as wholesale distribution pipes for software updates, telemetry, and digital signage feeds, diversifying revenue beyond traditional programming. Such diversification strengthens demand across the OTA transmission platform market even as linear ratings plateau.

By End-User: Commercial players still top spend but government demand surges

Commercial broadcasters and MSOs generated 56.46% of 2024 demand, leveraging scale purchasing to negotiate fleet-wide upgrades. They prioritize multi-tenant architectures that support channel share agreements and virtualized encoding farms. Government and defense customers, however, are forecast to record the highest 6.23% CAGR as geopolitical tensions elevate secure, high-reliability broadcast links for command, control, and public alert functions.

Procurement differences shape vendor playbooks: commercial groups favor opex-light financing while defense ministries demand ruggedized, cyber-hardened gear certified to MIL-STD standards. Public service broadcasters fall between, balancing fiscal prudence with universal-service mandates. Shared tower companies emerge as neutral hosts, offering managed transmission services that convert capital expense into predictable leasing fees-a model gaining traction among budget-constrained regional stations within the OTA transmission platform industry.

Geography Analysis

North America generated 33.54% of 2024 revenue, underpinned by FCC timelines that compel ATSC 3.0 deployment and by mature advertising markets that sustain upgrade budgets.[3]Source: Federal Communications Commission, “DTV Transition Market Reports,” FCC.govStations exploit tax incentives for energy-efficient equipment, accelerating the shift to solid-state PAs. Equipment vendors benefit from predictable demand linked to ongoing repack reimbursements and broadband stimulus grants aimed at rural coverage expansion.

Europe occupies a technology vanguard position, emphasizing green broadcasting and agile spectrum use. DVB-T2 remains dominant, yet the EU’s push toward net-zero operations channels investment into high-efficiency transmitters and renewable-powered relay sites. Cross-border frequency coordination complicates network design but fosters demand for advanced planning software. Meanwhile, Eastern European markets, still completing analog switch-off, provide incremental growth for entry-level transmitter lines, balancing the more saturated Western landscape.

Asia-Pacific posts the highest 6.93% CAGR, propelled by India, Indonesia, and the Philippines racing toward full digital switchover. Government subsidies offset capex, yet supply-chain volatility and foreign-exchange swings challenge project timelines. China champions DTMB-A upgrades that integrate HDR and interactive services, offering domestic OEMs scale advantages. Australia and South Korea pilot 5G-Broadcast, creating testbeds for hybrid DTT-cellular business models. Elsewhere, Latin America and Africa display patchwork adoption levels, with Brazil nearing ISDB-T3 adoption and sub-Saharan nations reliant on multilateral development bank financing to close coverage gaps.

Competitive Landscape

The OTA transmission platform market features moderate concentration: top European and U.S. vendors collectively hold nearly 45% revenue, while agile Asian entrants erode share through cost-effective, software-centric solutions. Rohde & Schwarz, GatesAir, and NEC defend incumbency by doubling R&D on energy-sipping LDMOS amplifiers and containerized signal processing workflows. Their yearly firmware releases add ATSC 3.0 advanced features and 5G-Broadcast options, protecting installed bases.

Disruptors emphasize cloud-first architectures and SaaS monitoring that slash site visits. Some partner with tower-cos to offer “transmission-as-a-service,” bundling spectrum planning, licensing, and 24/7 NOC support. Traditional RF specialists respond by acquiring control-room software vendors, seeking end-to-end portfolios that tether customers long term. Patent licensing transparency-spurred by USPTO standard-essential patent initiatives-reduces royalty uncertainty and helps newer brands penetrate established accounts.

Strategic alliances span broadcast and telecom, as 5G-Broadcast prototypes demand converged hardware. Joint ventures target government frameworks that favor domestic manufacturing offsets. Amid this flux, differentiation hinges less on raw RF horsepower and more on AI-assisted diagnostics, power-saving algorithms, and security certifications. Vendors able to present audited sustainability metrics gain an edge with publicly listed broadcasters committed to ESG disclosures.

OTA Transmission Platform Industry Leaders

Rohde & Schwarz GmbH & Co KG

GatesAir, Inc.

NEC Corporation

Nautel Ltd.

KOKUSAI ELECTRIC CORPORATION

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: European Broadcasting Union released DVB-NIP, standardizing end-to-end IP broadcast delivery for simultaneous OTT and terrestrial distribution.

- January 2025: National Radio Systems Committee published NRSC-1-C-2024 and NRSC-2-C-2024, tightening AM emission limits and influencing monitoring equipment specs.

- December 2024: FCC amended 47 CFR 73.682 to incorporate ATSC A/85 loudness rules and certify ATSC 3.0 signal parameters, adding compliance checkpoints for transmitter vendors.

- October 2024: Comtech Telecommunications unveiled Digital Common Ground satellite modems, extending its footprint into integrated terrestrial-satcom transmission.

Global OTA Transmission Platform Market Report Scope

| Transmitters |

| RF Filters and Antennas |

| Multiplexers and Encoders |

| Monitoring and Control Systems |

| Ancillary Infrastructure |

| ATSC 3.0 |

| DVB-T/T2 |

| ISDB-T/Tb |

| DTMB |

| 5G-Broadcast / FeMBMS |

| Television Broadcasting |

| Radio / DAB |

| Direct-to-Mobile and Datacasting |

| Public Warning and Emergency Alert |

| Other Applications |

| Public Service Broadcasters |

| Commercial Broadcasters and MSOs |

| Network Operators / Facility Owners |

| Government and Defence |

| Other End-Users |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Component | Transmitters | ||

| RF Filters and Antennas | |||

| Multiplexers and Encoders | |||

| Monitoring and Control Systems | |||

| Ancillary Infrastructure | |||

| By Technology | ATSC 3.0 | ||

| DVB-T/T2 | |||

| ISDB-T/Tb | |||

| DTMB | |||

| 5G-Broadcast / FeMBMS | |||

| By Application | Television Broadcasting | ||

| Radio / DAB | |||

| Direct-to-Mobile and Datacasting | |||

| Public Warning and Emergency Alert | |||

| Other Applications | |||

| By End-User | Public Service Broadcasters | ||

| Commercial Broadcasters and MSOs | |||

| Network Operators / Facility Owners | |||

| Government and Defence | |||

| Other End-Users | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia and New Zealand | |||

| Southeast Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the OTA transmission platform market?

The OTA transmission platform market size is USD 119.79 million in 2025 and is projected to reach USD 140.87 million by 2030.

Which region is expanding fastest for over-the-air transmission platforms?

Asia-Pacific is forecast to post the highest 6.93% CAGR through 2030, driven by government-funded digital switchover programs.

How quickly is ATSC 3.0 being adopted compared with 5G-Broadcast?

ATSC 3.0 holds the largest 34.18% share today, but 5G-Broadcast is the fastest-growing technology at a 5.83% CAGR.

Which component segment offers the strongest growth outlook?

Monitoring and control systems lead growth with a 4.57% CAGR as broadcasters centralize network operations and embrace predictive maintenance.

Why are solid-state transmitters attracting investment?

Solid-state designs lower energy consumption, curb maintenance costs, and support advanced modulation, aligning with both ESG goals and total cost-of-ownership targets.

What restrains capex in the sector despite new standards?

High up-front equipment costs, cord-cutting revenue pressure, and uncertain spectrum repack timelines delay large-scale modernization projects.

Page last updated on: