Radio Modem Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 1.35 Billion |

| Market Size (2030) | USD 1.89 Billion |

| Growth Rate (2025 - 2030) | 6.93% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

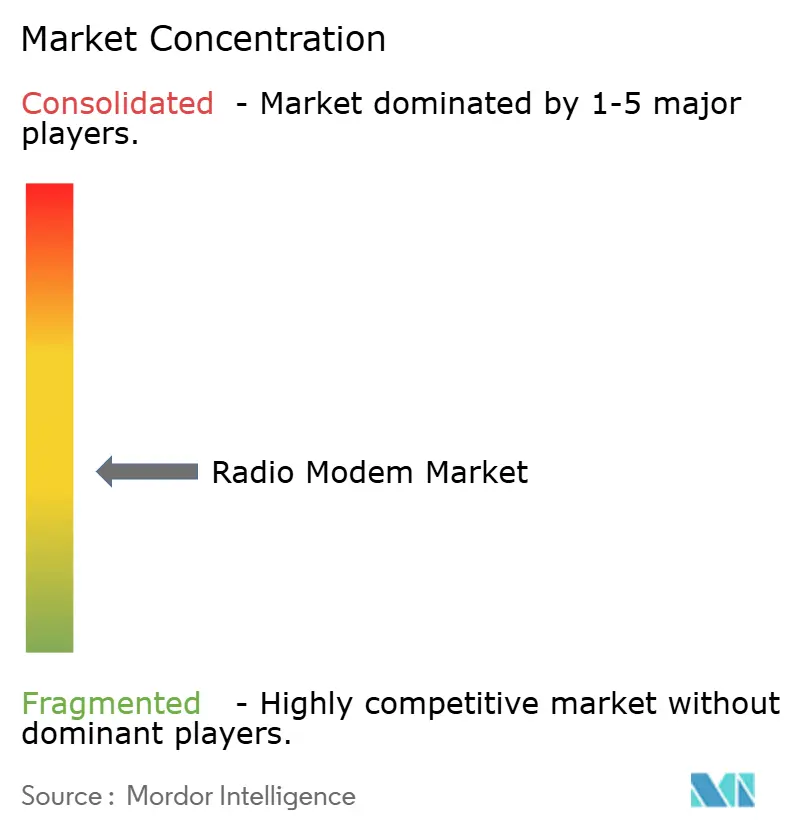

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Radio Modem Market Analysis by Mordor Intelligence

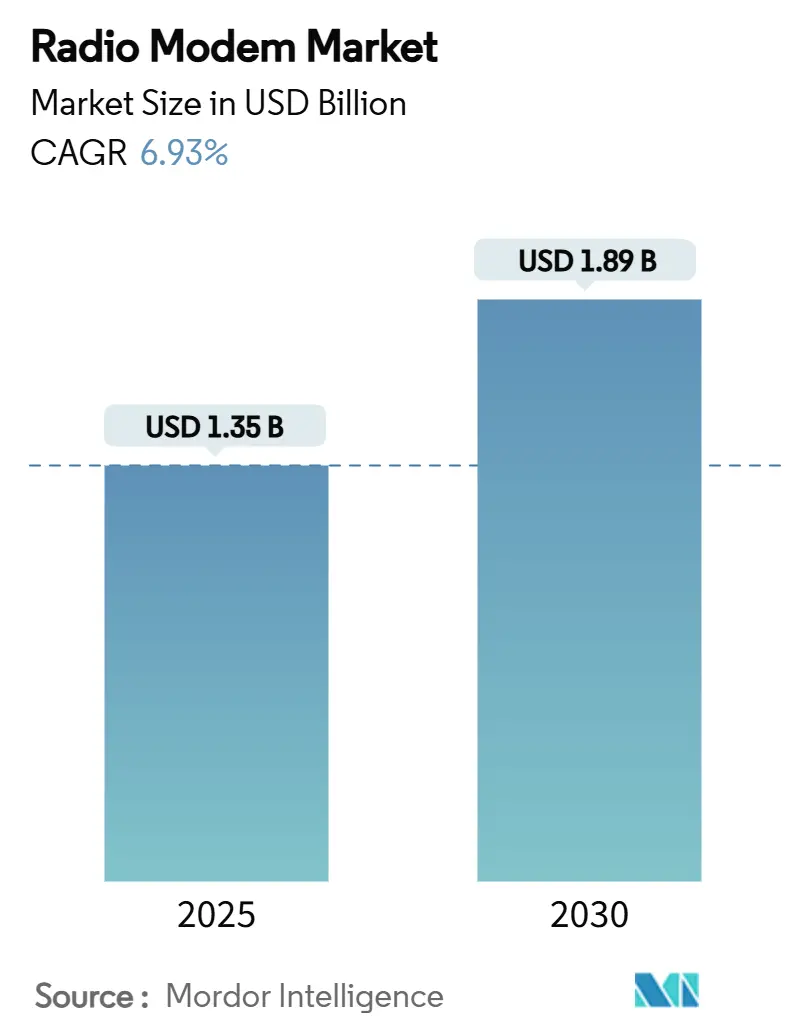

The radio modem market size reached USD 1.35 billion in 2025 and is forecast to climb to USD 1.89 billion by 2030, registering a 6.93% CAGR over the period. Accelerating migration from serial-based SCADA to IP-enabled networks, expanding industrial IoT roll-outs and government‐funded grid-modernization programs are fuelling adoption of robust wireless data links across critical infrastructure sectors. Vendors are innovating around sub-1 GHz LPWAN, 5G private networks and software-defined radio technologies to address rising demand for long-range, low-latency connectivity. Competitive intensity is increasing as cellular, satellite and traditional radio vendors converge around integrated edge-compute platforms, while spectrum-policy updates such as the 6 GHz unlicensed ruling in the United States expand high-bandwidth options for industrial users. Growing cyber-hardening mandates (IEC 62443, NERC CIP) and supply-chain constraints on RF components remain cost headwinds, but overall demand outlook stays resilient because utilities, mining, oil-and-gas and transportation operators view radio connectivity as mission-critical.

Key Report Takeaways

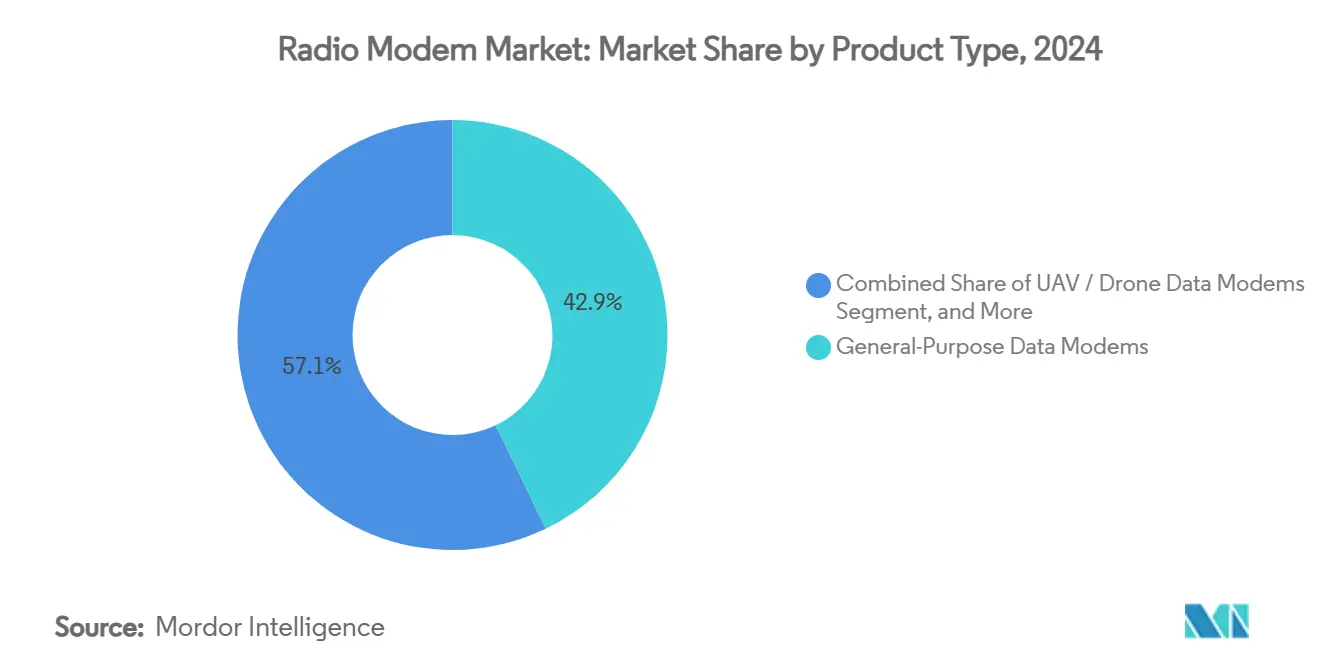

- By product type, General-Purpose Data Modems led with a 42.87% share of the radio modem market in 2024, whereas Long-Range Industrial Modems are advancing at a 6.97% CAGR through 2030.

- By frequency band, License-Free ISM captured 38.54% of the radio modem market share in 2024 and Sub-1 GHz LPWAN is set to expand at 7.13% CAGR to 2030.

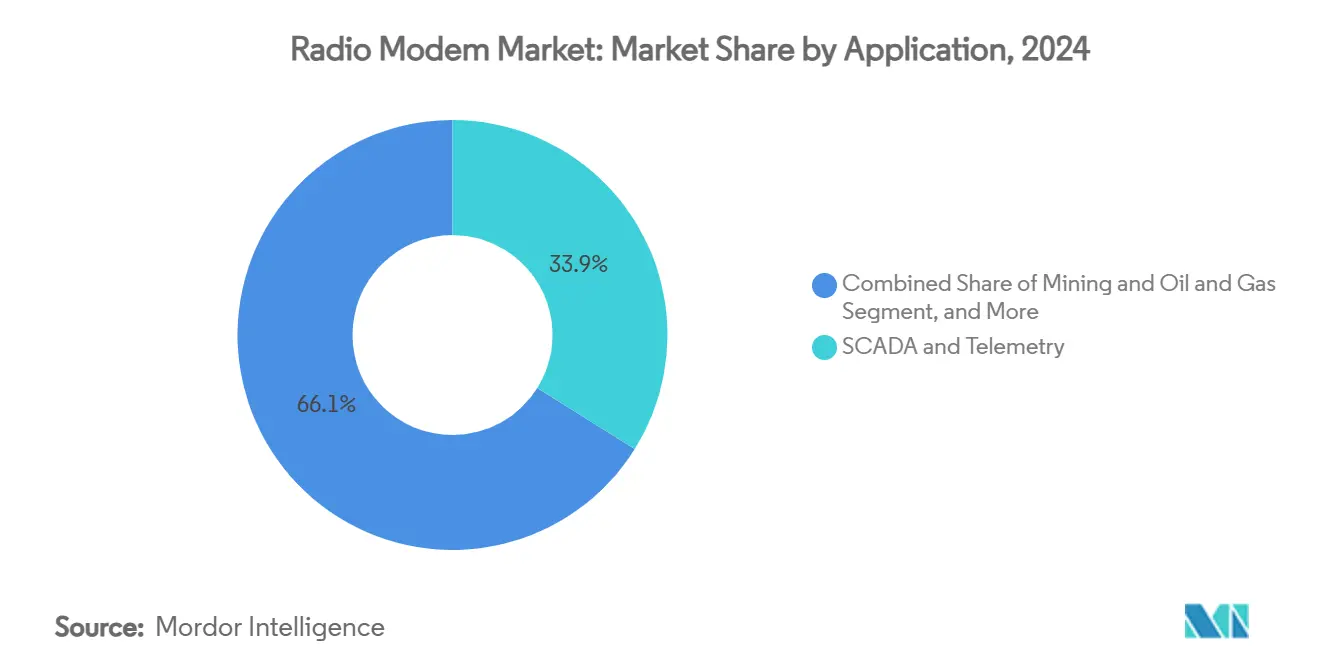

- By application, SCADA and Telemetry accounted for a 33.89% share of the radio modem market size in 2024, while Utilities and Smart Grid applications are growing at a 7.18% CAGR through 2030.

- By communication channel, Point-to-Multipoint held 46.92% of the radio modem market in 2024; Mesh Networking records the highest projected CAGR at 7.23% to 2030.

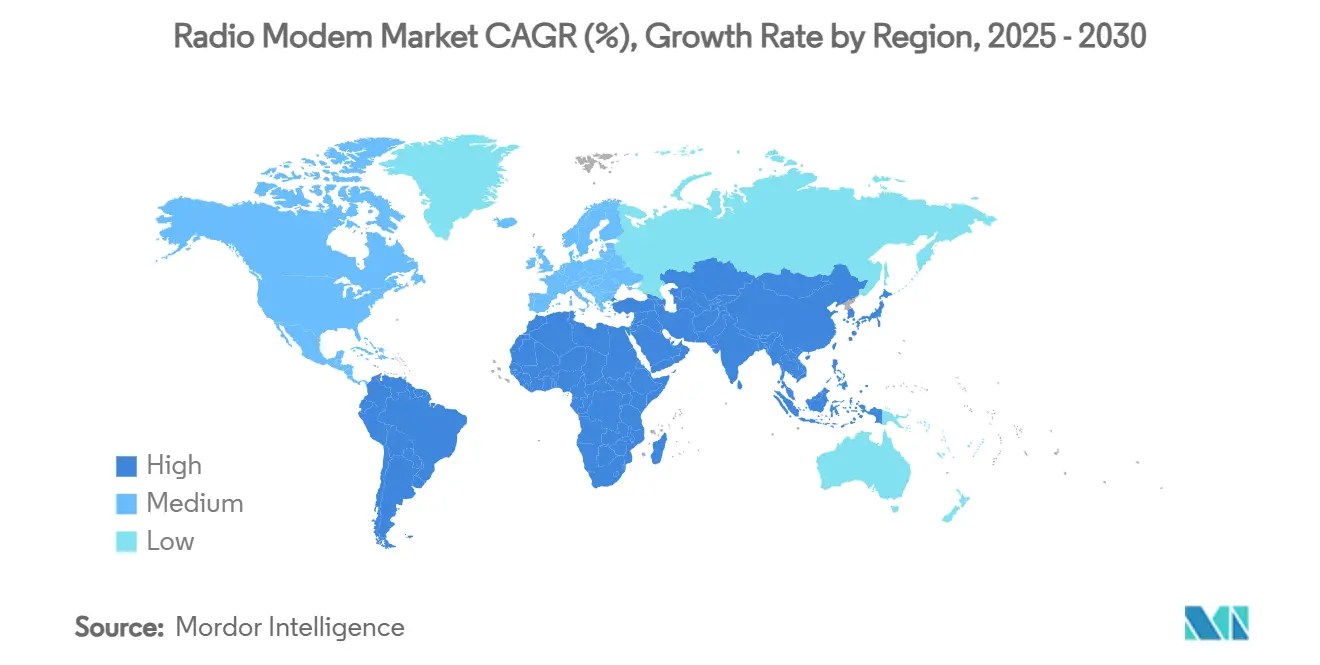

- By geography, Asia-Pacific commanded 34.76% of the radio modem market in 2024 and is forecast to grow at a 7.43% CAGR through 2030.

Global Radio Modem Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Migration from serial to IP-based SCADA networks | +1.8% | North America and Europe early adopters; global rollout | Medium term (2-4 years) |

| Surge in UAV and drone telemetry deployments | +1.2% | North America, Asia-Pacific | Short term (≤ 2 years) |

| 5G private-network roll-outs in industrial campuses | +1.5% | US, Germany, Japan, South Korea | Medium term (2-4 years) |

| Government smart-grid modernization mandates | +2.1% | North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| Shift to sub-1 GHz LPWAN for remote asset monitoring | +0.9% | Rural and remote sites worldwide | Short term (≤ 2 years) |

| Edge-AI enabled software-defined radio modems | +0.7% | US, Germany, Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Migration from Serial to IP-Based SCADA Networks

Utilities are phasing out legacy serial links in favor of Ethernet-compatible, deterministic radio systems that seamlessly bridge old and new protocols. DTE Energy’s SmartCurrents program deployed a private mesh network across 7,600 sq mi to connect 3.6 million smart meters and automate distribution assets, illustrating how IP migration boosts network visibility and reduces truck rolls. [1]International Society of Automation, “Update to ISA/IEC 62443 Standards,” isa.orgRadio-modem vendors now prioritize dual-port designs that support Modbus, DNP3 and IEC 60870 alongside IPv6 to ease retrofit projects. The transition also catalyzes demand for higher-throughput radios capable of transporting video diagnostics and edge-analytics data from substations. As more utilities digitalize assets to meet resiliency mandates, serial-to-IP bridge shipments are projected to stay elevated through 2028. Regional variations persist, yet North American grid-operators continue to set integration templates subsequently adopted in Europe and Asia-Pacific.

Surge in UAV and Drone Telemetry Deployments

Commercial drone fleets for precision agriculture, pipeline inspection and emergency response require low-latency links that maintain video and sensor integrity over tens of kilometres. Software-defined radio (SDR) modems enable operators to adjust coding schemes and power levels on the fly, optimizing performance for mission profile and airspace regulations. AI-enhanced payloads further increase upstream bandwidth needs to support onboard object recognition. Demand concentrates in North America and Asia-Pacific where drone regulations and subsidy programs stimulate enterprise investment. Vendors targeting this segment differentiate through AES-256 encryption, compact SWaP designs and seamless handoff between terrestrial and satellite links. The uptrend will remain pronounced as BVLOS (Beyond Visual Line-of-Sight) approvals broaden commercial use cases.

5G Private-Network Roll-Outs in Industrial Campuses

Manufacturing, logistics and energy facilities are adopting stand-alone 5G cores to secure deterministic URLLC (Ultra-Reliable Low-Latency Communications) without relying on public networks. Siemens’ Scalance MUM856-1 industrial router exemplifies the convergence of traditional radio-modem and cellular capabilities, supporting 1 Gbps traffic and automatic 4G fallback in harsh environments. Private spectrum frameworks in the US (CBRS) and Germany (3.7-3.8 GHz) lower barriers to entry. Integrators bundle edge-compute nodes with the radio stack, enabling closed-loop control of AGVs, machine vision and digital twins. Resulting productivity gains reinforce management buy-in, driving steady demand for 5G-capable radio modems through 2030.

Government Smart-Grid Modernization Mandates

Policy directives such as the US Energy Independence and Security Act and EU network-code harmonization compel utilities to deploy advanced metering infrastructure, distribution automation and integration of distributed energy resources. Thailand’s Provincial Electricity Authority adopted Huawei’s eLTE SCADA solution to meet national reliability goals, evidencing global policy diffusion. Mandates often bundle funding incentives that offset capital costs for communication upgrades, lifting radio-modem replacement cycles. Because regulatory reviews typically span multiple years, this driver exerts the strongest long-term pull on industry growth.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Scarcity of licensed sub-GHz spectrum in metros | -1.4% | Urban areas worldwide, acute in NA and EU | Medium term (2-4 years) |

| Rising cyber-hardening compliance costs (IEC 62443, NERC CIP) | -2.2% | Global critical infrastructure | Long term (≥ 4 years) |

| Supply-chain volatility for RF front-end components | -1.8% | Asia-Pacific manufacturing hubs most exposed | Short term (≤ 2 years) |

| Competition from low-orbit satellite IoT links | -1.1% | Remote/rural deployments worldwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Cyber-Hardening Compliance Costs

ISA’s 2024 update to the ANSI/ISA-62443-2-1 standard obliges asset owners to institute enterprise-wide risk programs, raising documentation and testing overheads for every new radio deployment. [2]Hitachi Energy, “DTE Energy SmartCurrents,” hitachienergy.com Industry surveys show industrial-cyber budgets increasing 15% y/y, with compliance consuming up to 25% of allocations. Smaller cooperatives and municipal utilities struggle to absorb the incremental cost, slowing refresh cycles. Vendors respond by embedding secure-element chips and FIPS-validated crypto stacks, but certification queues and audit fees still extend project timelines. Over the forecast horizon, elevated security spend will temper total unit growth even as overall revenue rises on higher ASPs.

Competition from Low-Orbit Satellite IoT Links

Rapid deployment of LEO constellations introduces an alternative to terrestrial radios for covering remote oilfields, maritime routes and wildlife reserves. Analysts expect 30.3 million satellite-IoT devices in service by 2025, shrinking the addressable base for very-long-range terrestrial modems. [3]Satellite Markets, “Satellite IoT: A Game Changer,” satellitemarkets.comSemiconductor leaders now ship chipsets supporting 3GPP 5G NTN Release 17, allowing direct-to-device messaging that bypasses backhaul repeaters. Radio-modem suppliers counter by integrating satellite backup modes and focusing on lower-latency niches that LEO systems cannot yet match. Nevertheless, substitution risk remains highest for sparsely populated geographies where tower economics are weakest.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Long-Range Devices Outpace General-Purpose Units

Radio modem market size for General-Purpose Data Modems stood at USD 0.58 billion in 2024 and commanded 42.87% of radio modem market share, anchored by decades of SCADA installations in utilities and oil-and-gas pipelines. Their popularity persists because drop-in replacements keep legacy assets online while adding IP pass-through. However, Long-Range Industrial Modems are posting a 6.97% CAGR to 2030 as renewable energy farms, midstream pipelines and rural mining sites scale remote asset monitoring. These units couple 30+ km line-of-sight ranges with multi-band capability, often embedding both VHF and sub-GHz ISM for redundancy. Manufacturers increasingly incorporate advanced forward-error-correction and AES-256 to comply with modern cyber rules, while optional GNSS timing ensures deterministic polling intervals.

Software-Defined Radio modems captured meaningful mindshare as industrial clients prioritize field-upgradable platforms. Hytera’s DS-6250S Cube supports eight carriers and dynamic bandwidth allocation, illustrating how SDRs lower total cost of ownership by postponing hardware refreshes. UAV-friendly data modems emphasize lightweight form-factors below 50 g and dual-antenna diversity for uninterrupted telemetry. Meanwhile, Cellular-IoT embedded modules pair LTE-M, NB-IoT or 5G NR bands with fallback to unlicensed LoRa or Wi-Fi, providing single-SKU global coverage for equipment OEMs that sell into multiple jurisdictions.

By Frequency Band: Sub-1 GHz LPWAN Gains Traction

License-Free ISM bands contributed 38.54% of radio modem market revenue in 2024 as 868/915 MHz devices balanced range, cost and licensing simplicity. Many utilities still favor these bands for distribution-automation and fault-reclosure controls given predictable propagation through foliage and buildings. Demand is shifting toward Sub-1 GHz LPWAN platforms such as LoRaWAN and Sigfox, which are advancing at a 7.13% CAGR, chiefly because they offer battery-lifetimes exceeding 10 years for condition-monitoring sensors deployed in remote wells and irrigation pumps. Vendors integrate dual-mode stacks that can switch from LoRa to FSK, widening applicability.

Licensed VHF/UHF bands maintain relevance where mission-critical reliability outweighs spectrum-lease fees; railway signaling and public-safety agencies illustrate sustained demand. Policy modifications unlocking 6 GHz for very-low-power devices in 2025 open new channels for augmented-reality work-instructions and machine-vision streaming. Above 5 GHz, mmWave radio modems leverage beamforming for short-haul links inside factories, shifting heavy video payloads to edge servers without congesting lower bands reserved for SCADA polling.

By Application: Utilities and Smart Grid Lead Growth Curve

SCADA and Telemetry preserved the largest slice of radio modem market size at USD 0.46 billion in 2024, representing a 33.89% share. Use cases span breaker status, load tap-changer control and cathodic-protection monitoring. Yet Utilities and Smart Grid projects are charting the fastest 7.18% CAGR to 2030 as regulators press operators to integrate distributed solar and energy-storage assets. Eagle Ford Oil Field achieved 40% OPEX savings after replacing leased lines with wireless mesh for SCADA and VoIP workloads, underscoring return-on-investment clarity.

Transportation and ITS deployments embrace Vehicle-to-Everything radios that meet sub-10 ms latency for collision avoidance. Mining and Oil-and-Gas operators test private 5G to control autonomous haulage and drilling rigs; Newmont’s Cadia mine reported safer operations after trialling the network, prompting global rollout plans. Agriculture continues to adopt LPWAN irrigation controls, lowering water consumption 16–30% while achieving 98% packet-success rates.

By Communication Channel: Mesh Topologies Accelerate

Point-to-Multipoint hubs represented 46.92% of radio modem market revenue in 2024, underpinning central-master SCADA architectures in power distribution and municipal water. These networks favour deterministic polling schedules and simplify NERC-CIP compliance assessments. Mesh Networking, however, is climbing at a 7.23% CAGR as utilities and smart-city operators prioritise self-healing, multi-hop reliability. Wirepas’ non-cellular 5G mesh runs on 1.9 GHz licence-exempt spectrum, supporting hundreds of nodes per square kilometre with <5 ms hop latency.

Point-to-Point links retain niche importance for high-resolution video backhaul, construction site monitoring and temporary events. Private LTE-5G backhaul segments carve share where enterprises need mobility along conveyor belts or port cranes yet want ownership of SLA parameters. Emerging network-slicing tools allow IT departments to carve deterministic VLANs for SCADA while allocating the same physical eNodeB to best-effort vehicle telemetry, harmonising divergent QoS demands under unified management.

Geography Analysis

Asia-Pacific generated 34.76% of 2024 radio modem market revenue and is on course for a 7.43% CAGR through 2030 as Beijing’s Made in China 2025 blueprint and Seoul’s smart-factory programs intensify demand for factory digitalization. Government-backed 5G private-network pilots in Japan’s manufacturing clusters have become reference architectures for neighbouring ASEAN economies. Electricity boards across India and Indonesia allocate budget for RF mesh AMI, accelerating shipments of sub-GHz modems. The region’s contribution to the radio modem market will therefore remain the primary volume driver.

North America sustains sizeable outlays on grid-modernization and cybersecurity. Department of Energy funding spurs utilities to refresh legacy licensed narrowband radios with hybrid IP designs, while CBRS spectrum encourages manufacturing plants to deploy private networks. Apple’s multibillion-dollar RF-chip sourcing deal with Broadcom illustrates a broader reshoring trend that enhances supply-chain resilience for radio-hardware OEMs.

Europe experiences steady demand owing to stringent cyber and environmental directives. Germany’s emphasis on open automation boosts interest in software-defined platforms, and regional energy companies leverage 450 MHz and 700 MHz licences for mission-critical infrastructure. Nordic utilities pioneer maritime and offshore-wind telemetry solutions, utilising multi-band radios that integrate VHF voice channels with LTE-M for data. UK spectrum-sharing frameworks allow port operators to reserve 3.8 GHz slices, stimulating adoption of dual-mode 5G/radio-modem gateways.

Competitive Landscape

The radio modem market remains moderately fragmented, with the top five suppliers accounting for an estimated 42% of global revenue. RACOM holds a strong footprint in SCADA projects across 120+ countries, leveraging deep protocol support and a comprehensive reseller network. Digi International expands via its subscription-based Digi 360 bundle that combines edge routers, cloud management and lifetime warranty to lock in annuity income. Ondas sees momentum in the rail sector after IEEE 802.16t standard adoption, posting triple-digit revenue growth in early 2025.

Technology convergence shapes competitive dynamics. Vendors integrate 5G NR, Wi-Fi 6 and satellite fallback into single-PCB solutions, aiming to be the de-facto “all-terrain” modem for industrial clients. Simpulse demonstrates SDR innovation tailored to unmanned systems, delivering real-time bandwidth scaling to conserve power while preserving link margin. Lime Microsystems targets developers with modular LimeNET Micro 2.0 priced from USD 899 to democratise custom waveform design.

Strategic partnerships between radio-hardware firms and major carriers accelerate commercialisation of private 5G solutions. Verizon and Honeywell integrate 5G into smart meters, giving utilities real-time load-management without truck dispatches. Component supply security also shapes moves; Semtech trimmed net debt by 68% in FY 2025 to prioritize investment in cloud-connected LoRa gateways. In parallel, Triad RF pushes 5G-specific CubeSat front ends to extend terrestrial modems with satellite redundancy.

Radio Modem Industry Leaders

SATEL Oy

Digi International Inc.

FreeWave Technologies Inc.

RACOM s.r.o.

4RF Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Digi International reported USD 104 million Q1 FY 2025 revenue and launched the Digi X-ON platform while achieving SOC 2 Type II compliance for SmartSense.

- January 2025: Semtech Corporation announced FY 2025 net sales of USD 909.3 million and a 50.2% GAAP gross margin, focusing on IoT portfolio optimisation.

- December 2024: EBYTE released a Global LoRa Module Export Market Analysis Report noting China’s 45% export share and an USD 8 billion LoRaWAN IoT market in 2024

- October 2024: Digi International unveiled the subscription-based Digi 360 cellular-IoT package with 24/7 support.

Global Radio Modem Market Report Scope

| General-Purpose Radio Modems |

| UAV / Drone Data Modems |

| SCADA and Telemetry Modems |

| Long-Range Industrial Modems |

| Cellular IoT Embedded Modems |

| Software-Defined Radio (SDR) Modems |

| Licensed VHF (30–300 MHz) |

| Licensed UHF (300–960 MHz) |

| License-Free ISM 868 / 915 MHz |

| 2.4 GHz ISM |

| 5 GHz and Above (sub-6 GHz and mmWave) |

| Sub-1 GHz LPWAN (LoRa, Sigfox, NB-IoT) |

| SCADA and Telemetry |

| Transportation and ITS |

| Mining and Oil and Gas |

| Agriculture and Precision Farming |

| Utilities and Smart Grid |

| Government and Defense |

| Industrial Automation and Smart Manufacturing |

| Point-to-Point |

| Point-to-Multipoint |

| Mesh Networking |

| Cellular Backhaul / Private LTE-5G |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Product Type | General-Purpose Radio Modems | ||

| UAV / Drone Data Modems | |||

| SCADA and Telemetry Modems | |||

| Long-Range Industrial Modems | |||

| Cellular IoT Embedded Modems | |||

| Software-Defined Radio (SDR) Modems | |||

| By Frequency Band | Licensed VHF (30–300 MHz) | ||

| Licensed UHF (300–960 MHz) | |||

| License-Free ISM 868 / 915 MHz | |||

| 2.4 GHz ISM | |||

| 5 GHz and Above (sub-6 GHz and mmWave) | |||

| Sub-1 GHz LPWAN (LoRa, Sigfox, NB-IoT) | |||

| By Application | SCADA and Telemetry | ||

| Transportation and ITS | |||

| Mining and Oil and Gas | |||

| Agriculture and Precision Farming | |||

| Utilities and Smart Grid | |||

| Government and Defense | |||

| Industrial Automation and Smart Manufacturing | |||

| By Communication Channel | Point-to-Point | ||

| Point-to-Multipoint | |||

| Mesh Networking | |||

| Cellular Backhaul / Private LTE-5G | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the radio modem market in 2025 and how fast is it growing?

It stands at USD 1.35 billion in 2025 and is forecast to reach USD 1.89 billion by 2030 at a 6.93% CAGR.

Which product category currently dominates shipments?

General-Purpose Data Modems lead with 42.87% 2024 share, driven by their installed base in legacy SCADA.

What is the fastest-growing application area for radio modems?

Utilities and Smart Grid projects grow at 7.18% CAGR owing to regulatory mandates for bidirectional power flow and DER integration.

Why is Asia-Pacific considered the growth engine for adoption?

Government-backed smart-city, 5G private-network and industrial automation investments push the region to a 7.43% CAGR.

How are cybersecurity regulations affecting procurement decisions?

Compliance with IEC 62443 and NERC CIP increases total ownership cost, leading vendors to embed secure elements and buyers to extend evaluation cycles.

Are satellite constellations a threat to terrestrial radio modem vendors?

LEO satellites offer coverage in remote zones, causing a potential 1.1% drag on CAGR, but terrestrial solutions retain an edge in latency-sensitive control loops.

Page last updated on: