Two-Way Radio Communication Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

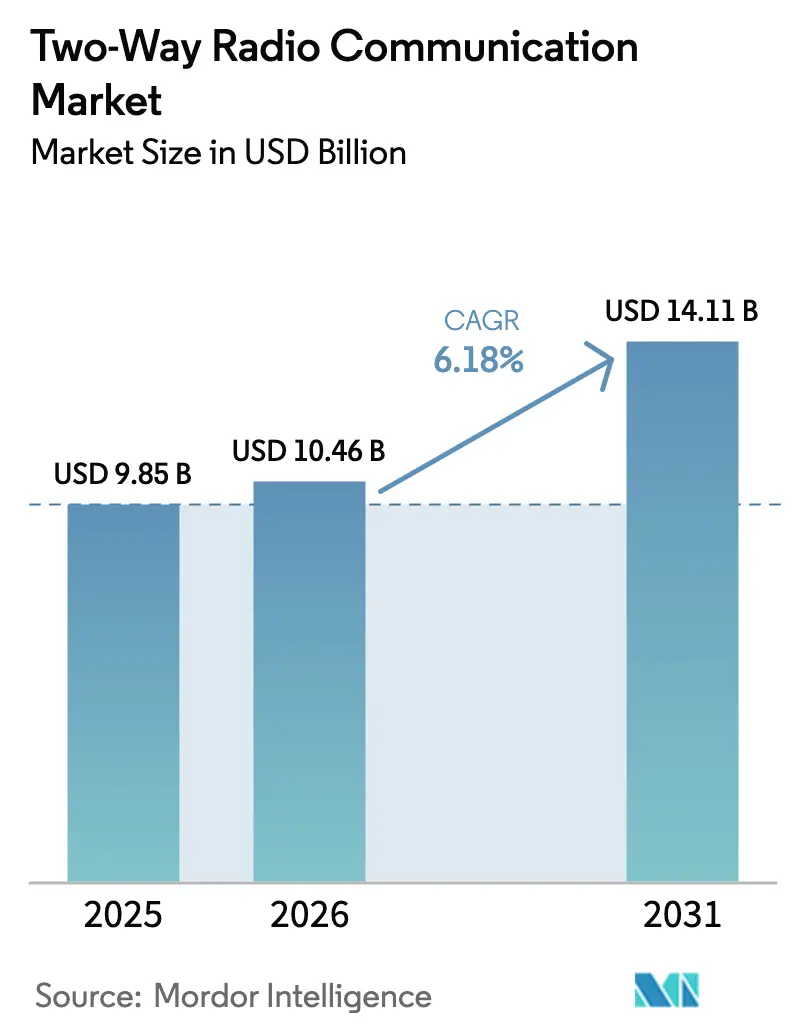

| Market Size (2026) | USD 10.46 Billion |

| Market Size (2031) | USD 14.11 Billion |

| Growth Rate (2026 - 2031) | 6.18% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Two-Way Radio Communication Market Analysis by Mordor Intelligence

Two-Way Radio Communication market size in 2026 is estimated at USD 10.46 billion, growing from 2025 value of USD 9.85 billion with 2031 projections showing USD 14.11 billion, growing at 6.18% CAGR over 2026-2031. Adoption momentum stems from the rapid migration to digital Land Mobile Radio (LMR) platforms, strict narrow-banding rules, and the need for mission-critical voice that interoperates with broadband data. Public safety agencies are upgrading legacy analog fleets, while industrial users in logistics, energy, and manufacturing view digital radios as gateways to telemetry, GPS, and remote diagnostics. Hybrid LTE/DMR architectures are widening the addressable base because they overlay broadband data on proven push-to-talk workflows. Simultaneously, private LTE/5G campus networks are reshaping enterprise communications, creating partnership opportunities for vendors that embed cellular modules into radios. Price pressure from Far-East ODMs is intensifying, yet incumbents defend share through encryption, cyber-hardening, and life-cycle services.

Key Report Takeaways

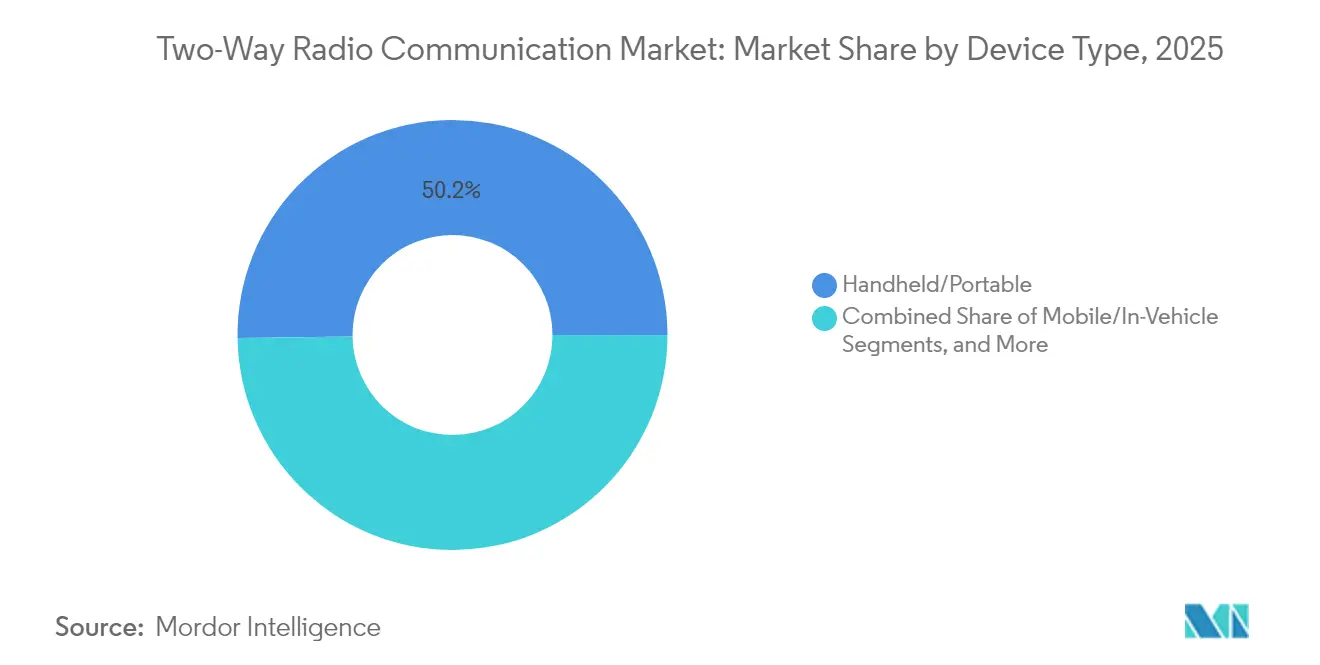

- By device type, handheld/portable units led with 50.22% of the two-way radio communication market share in 2025, while mobile/in-vehicle systems are forecast to expand at a 7.66% CAGR through 2031.

- By frequency band, UHF (400-512 MHz) held 44.12% share of the two-way radio communication market size in 2025, while SHF (1-6 GHz) is projected to rise at an 7.98% CAGR to 2031.

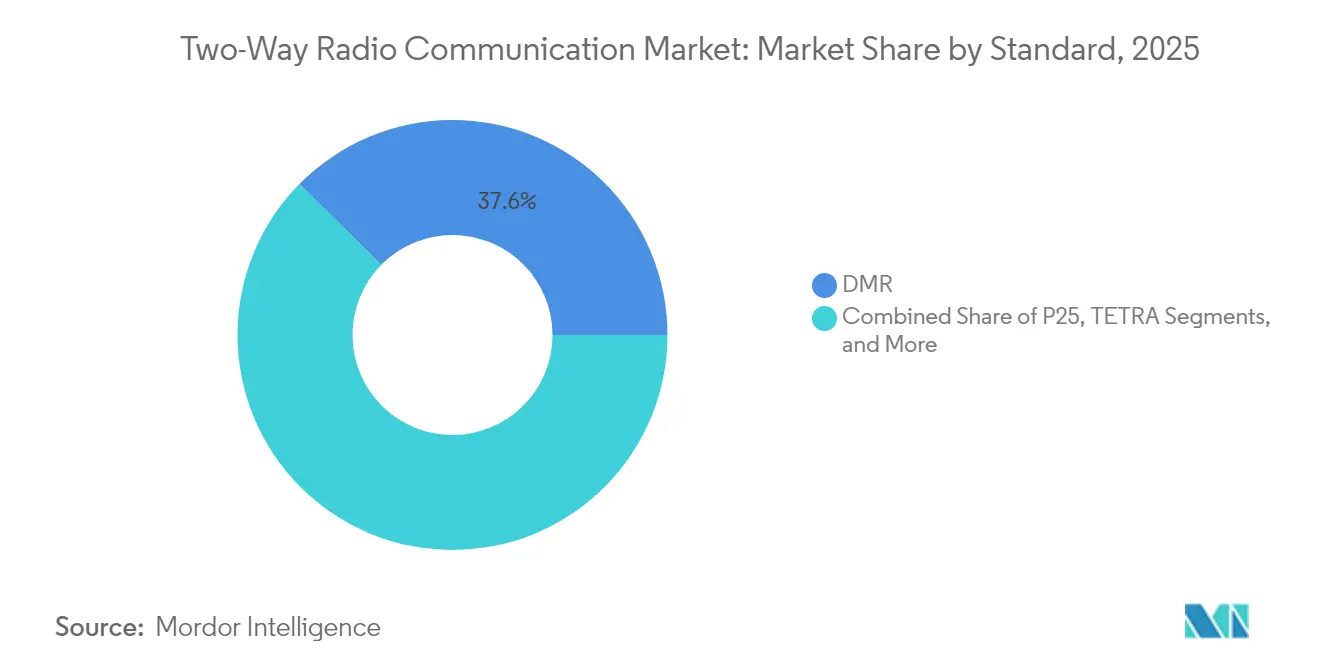

- By standard, DMR captured a 37.62% share of the two-way radio communication market in 2025, while PoC (Push-to-Talk-over-Cellular) technologies record the highest CAGR at 9.05% through 2031.

- By end-user, government and public safety accounted for a 40.62% share of the two-way radio communication market size in 2025, while transportation and logistics are advancing at an 8.44% CAGR through 2031.

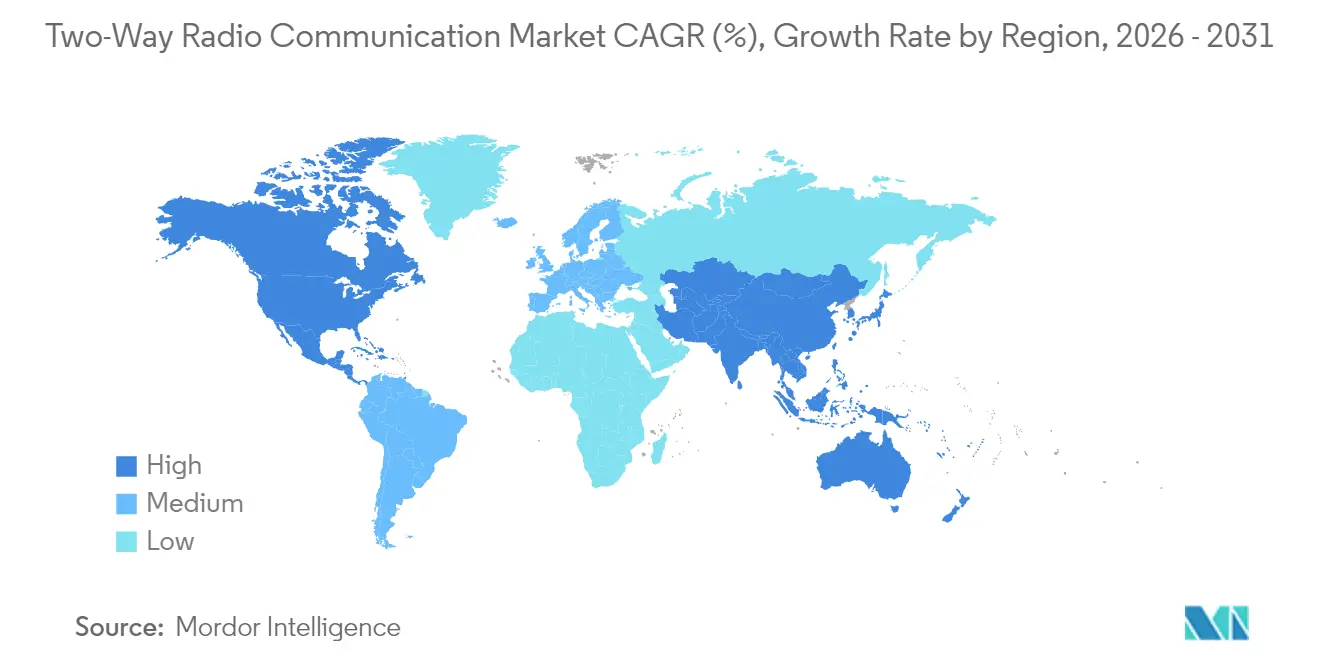

- By geography, North America commanded a 38.62% share of the two-way radio communication market in 2025, while the Asia Pacific is the fastest-growing region with a 7.75% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Two-Way Radio Communication Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital migration of global LMR installed base | +1.5% | North America, Europe, global spillover | Medium term (2-4 years) |

| Mandated narrow-banding and spectrum re-farming (VHF/UHF) | +1.2% | North America, EU | Short term (≤ 2 years) |

| Growing hybrid LTE/DMR deployments for public safety | +1.8% | North America, Asia Pacific | Medium term (2-4 years) |

| Proliferation of private LTE/5G campus networks | +1.1% | Global, early industrial adopters | Long term (≥ 4 years) |

| Surge in UK infrastructure projects (HS2, smart ports) | +0.8% | United Kingdom, EU transport corridors | Short term (≤ 2 years) |

| Circular-economy demand for refurbished radios | +0.6% | Cost-sensitive regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Digital Migration Accelerates Mission-Critical Modernization

Analog-to-digital transitions double spectrum efficiency while embedding encryption, text, and GPS features that public safety agencies deem indispensable. Leading states and provinces budget for P25 or DMR upgrades that unify fire, EMS, and police channels across counties. The economic hurdle is receding as digital handset prices converge with analog, prompting municipalities to refresh fleets sooner. Fleet managers in utilities and transport link digital voice with SCADA and telematics to streamline outage response. Because encryption keys are centrally managed, agencies reduce breach risks and comply with evolving cyber mandates.

Narrow-Banding Mandates Drive Spectrum Optimization

Regulators completed the 25 kHz-to-12.5 kHz shift in U.S. VHF/UHF bands and now eye 6.25 kHz splits, forcing refits across enterprise fleets.[1]Australian Communications and Media Authority, “Land Mobile Radio Spectrum,” ACMA, acma.gov.au Similar directives spread in Canada, Europe, and parts of Asia, accelerating replacement cycles for analog repeaters unable to meet tighter channel widths. Equipment vendors upsell dual-slot TDMA radios that exceed the quota and embed data channels without new spectrum. End-users face re-programming and site-testing costs but cite clearer audio and longer battery life as offsets. Spectrum re-farming further squeezes incumbents when regulators carve public safety slices for broadband, nudging agencies toward multi-band or hybrid devices.

Hybrid LTE/DMR Integration Transforms Public Safety Communications

FirstNet and comparable priority-service LTE grids let agencies keep predictable push-to-talk while adding bandwidth for body-cam video, GIS layers, and drone feeds.[2]Motorola Solutions Inc., “Motorola Solutions Reports Fourth Quarter and Full Year 2024 Results,” Motorola Solutions, motorolasolutions.com Dual-mode devices auto-switch between DMR voice and LTE data, safeguarding continuity when commercial networks congest. Command centers gain holistic dashboards that merge AVL, CAD, and situational video onto one pane. Gradual migration protects sunk LMR investments and eases training burdens. Multi-bearer gateways also shorten coverage gaps in canyons or basements by routing traffic across either bearer as the signal dictates.

Private LTE/5G Networks Reshape Enterprise Communication Architecture

Mining pits, refineries, and smart ports deploy CBRS or licensed-spectrum LTE to blanket sites with deterministic low-latency coverage. Industrial buyers then run VoIP, AGV control, and IoT sensors on one network instead of siloed Wi-Fi plus LMR. Two-Way Radio Communication market vendors counter by embedding SIM slots into radios, enabling voice fallback when cellular coverage lapses. Integrators bundle EPC cores, eNodeBs, and rugged handhelds as turnkey managed services, a business model that offsets hardware commoditization. Analysts expect private cellular sites to triple by 2030, contributing a fresh pipeline for hybrid devices.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Spectrum congestion in urban cores | -0.9% | Global megacities | Short term (≤ 2 years) |

| Rising substitution by ruggedized smartphones and PoC | -1.2% | Cost-sensitive enterprise segments | Medium term (2-4 years) |

| Price pressure from Far-East ODM brands | -0.7% | Global, budget segments | Short term (≤ 2 years) |

| CMA price-cap on UK Airwave network | -0.3% | United Kingdom | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Spectrum Congestion Constrains Traditional Radio Expansion

Urban VHF/UHF blocks suffer from overlapping taxi, security, and event channels that hike interference and licensing fees. Public safety planners must overlay micro-cell sites or migrate to 700/800 MHz to relieve dead zones, increasing capex. Dynamic sharing and cognitive radios promise relief but introduce policy complexity and certification delays. Channel scarcity prolongs permitting cycles for new systems, stretching deployment timelines. The squeeze nudges enterprises toward PoC apps that ride existing LTE spectrum instead of bidding for scarce land-mobile frequencies; this fragments the addressable pool for traditional vendors.

Ruggedized Smartphones Present Viable Radio Alternatives

IP68 smartphones with programmable push-to-talk buttons mimic radio ergonomics while offering full Android ecosystems.[3]Sonim Technologies, “Ruggedized Mobile Solutions,” Sonim Technologies, sonimtech.com Monthly PoC subscriptions start well below analog trunking airtime, making them attractive for hospitality, retail, and small warehouses. Battery runtimes have closed to a full 12-hour shift, and MCX (Mission-Critical Services) profiles over 5G promise prioritized voice. However, agencies remain cautious about cellular dependence during disasters. Radio OEMs now market “converged” devices featuring dual PTT buttons to keep low-capex buyers in the fold. Training and policy hurdles linger, but the substitution trend trims unit volumes in the lower tier.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Portability Drives Market Leadership

Handheld radios retained 50.22% of the Two-Way Radio Communication market share in 2025, affirming the centrality of personal mobility on factory floors and incident scenes. Their lightweight and belt-clip design suits first responders and crane operators who cannot rely on vehicle power. Feature migration replicates smartphone UX-touch displays, Wi-Fi, and camera modules, yet preserves glove-friendly knobs. Bluetooth-Low-Energy beacons pair with ear-protection headsets to streamline hazardous-area workflows. Mobile/in-vehicle rigs will outpace overall growth at a 7.66% CAGR as fleets digitize logistics. Dashboard-mounted screens blend voice, navigation, and electronic logging, trimming distracted-driver risk and paperwork loads.

Second-tier segments, such as base stations and repeaters, expand slowly because many agencies reuse towers by simply swapping controllers and exciters. Nonetheless, cloud-managed repeaters enable firmware pushes and performance analytics that improve mean-time-to-repair. Battery-backed micro-repeaters plug metro coverage gaps in tunnels and high-rises. Vendors bundle warranty extensions and remote health monitoring to offset slowing hardware velocity. As a result, the Two-Way Radio Communication market embeds value in software and services rather than fresh iron, positioning OEMs for recurring revenue.

By Frequency Band: UHF Dominance Faces High-Frequency Challenge

UHF’s 44.12% stake in the Two-Way Radio Communication market reflects its sweet-spot blend of building penetration and antenna practicality. Shopping malls, stadiums, and fire departments rely on UHF to cover stairwells and underground garages. Yet SHF links (1-6 GHz) will compound at 7.98% through 2031 as private LTE backhaul and Wi-Fi 6E edge devices take hold. SHF handsets integrate eSIMs and low-gain patch antennas that ride CBRS or local-carrier slices, delivering 200 Mbps for video drones. VHF remains entrenched in forestry and marine zones, where 40-mile line-of-sight range outweighs handheld bulk.

Higher frequencies impose shorter wavelengths, enabling compact antennas but demanding denser site grids. To minimize the total cost of ownership, integrators deploy multi-band radios that switch across VHF, UHF, and 700/800 MHz, reducing truck rolls. The Two-Way Radio Communication market size for dual-band portables is expected to rise in absolute terms even if single-band unit sales plateau. Agencies weigh coverage trade-offs, often settling on a blended architecture: UHF for indoor and SHF private LTE for data-rich applications.

By Standard: DMR Leadership Challenged by PoC Innovation

DMR cornered 37.62% of the Two-Way Radio Communication market share in 2025 because its TDMA efficiency slashes channel congestion without proprietary sites. Interoperable tier-II networks appeal to budget-sensitive municipalities migrating off analog, while tier-III trunking matches P25 features at lower cost. Yet PoC’s 9.05% CAGR signals green-field buyers skipping repeaters and roaming on carrier data. Standard bodies are finalizing MCPTT Release 17, boosting latency targets below 300 ms, and narrowing LMR advantage. Still, P25 retains supremacy in U.S. mission-critical contexts owing to AES-256 encryption and rigorous conformance testing.

NXDN and dPMR serve light-industrial users needing digital clarity on slim budgets. TETRA dominates European metro rail and airports but faces sunset cycles as 5G FRMCS (Future Railway Mobile Communication System) trials progress. Over the forecast span, the Two-Way Radio Communication market will see multi-protocol “software-defined” radios that re-flash between DMR and LTE waveforms on demand, protecting capex against standards churn. Services revenue grows as integrators host key-management servers and over-the-air programming portals.

By End-User Industry: Public Safety Dominance Faces Logistics Challenge

Government and public safety’s 40.62% command of the Two-Way Radio Communication market size remains anchored in statutory funding streams and life-safety mandates. Federal grants offset multiband handset premiums topping USD 1,500 per unit, sustaining OEM margins. Dispatch consoles integrate NG911 feeds, CAD, and facial recognition plugins that lift situational awareness. Meanwhile, transportation and logistics, aided by e-commerce surges, will clip along at an 8.44% CAGR as cross-dock hubs crave instant coordination. Warehouse pickers use Bluetooth-linked headsets to cut mis-pick rates and meet same-day shipping windows.

Utilities invest in hard-hat radios rated for 140°F and arc-flash zones, often coupling asset-health sensor data into the same bearer. Oil and gas customers specify intrinsically safe (IS) handsets with T4 temperature ratings, a niche where premium pricing persists. Hospitality and retail gravitate toward PoC to trim infrastructure overhead, yet contract radio rentals for peak seasons. Because each vertical values uptime, service-level agreements covering battery refresh, software patching, and 24/7 hot-swap remain pivotal to vendor lock-in, ensuring stable service annuities even as hardware ASPs slide.

Geography Analysis

North America retained 38.62% of the Two-Way Radio Communication market in 2025, powered by FirstNet rollouts, state-level interoperability mandates, and the replacement of aging analog fleets. Municipal grants covered multiband radio upgrades for fire, police, and EMS, lifting premium-tier shipments. Public safety broadband integration fosters demand for LTE-capable portables and vehicle routers that bridge to P25. Private sector spending stems from petrochemical corridors along the Gulf Coast, adopting converged LTE/LMR for hurricane resilience. Service revenues now outpace hardware in the region, reflecting extended managed-service contracts.

Asia Pacific is projected to register a 7.75% CAGR through 2031, underpinned by rail, port, and manufacturing megaprojects in China, India, and Southeast Asia. Public safety ministries in Indonesia and the Philippines are leapfrogging straight to digital trunked networks, bundling GPS and biometric log-ons. Factory automation drives private LTE pilots using 3.5 GHz spectrum and edge computing, spurring hybrid-device demand. Local ODMs undercut global brands, but multinationals still win critical-tier tenders requiring encryption and hazardous-area certifications. Australian mining firms pioneer 5G standalone pits, a template likely replicated in Latin America.

Europe maintains steady but moderate growth as countries harmonize cross-border TETRA roaming and invest in 700 MHz broadband for rail and emergency services. Sustainability regulations encourage refurbished radio procurement, supporting circular-economy channels. The region also confronts cost caps, such as the UK Competition and Markets Authority price ceiling on Airwave airtime, pressuring incumbents to diversify into software. The Middle East and Africa contribute incremental gains via security deployments for mega-events and oil installations, though political risk tempers long-term contracts. Latin America sees sporadic upgrades tied to public-safety tax allocations and mining expansions in Chile and Peru.

Competitive Landscape

The Two-Way Radio Communication market demonstrates moderate concentration: Motorola Solutions, Hytera, and L3Harris leveraging extensive patent portfolios and national-level certifications to sustain price premiums. ODM challengers from China and South Korea compete on cost, flooding sub-USD 200 analog and entry-digital units into Latin America and Africa. Yet high-security and intrinsic-safety niches remain sheltered due to stringent testing and export controls. Strategic focus has shifted toward software, with incumbents bundling cloud command consoles, AI-assisted incident analytics, and over-the-air provisioning that command recurring fees.

Hybrid LTE integrations draw convergence deals: Motorola acquired a CBRS core provider in 2024, while Hytera launched a dual-mode PoC/DMR handset targeting logistics. L3Harris pivoted toward “L3Harris-as-a-Service,” bundling radios, software, and lifecycle support on subscription to smooth capital outlays for county agencies. Meanwhile, PoC platform vendors partner with carrier groups to offer eSIM-based push-to-talk that integrates with Microsoft Teams, appealing to enterprise IT buyers. Litigation over codec and TDMA patents persists, adding royalty drag to smaller players.

Supply-chain diversification is accelerating post-pandemic, with OEMs localizing final assembly in Mexico, Poland, and Malaysia to mitigate tariff and logistics risk. Chip shortages prompted radio makers to redesign boards around readily available microcontrollers, expediting certification via software-defined architectures. ESG pressures push vendors to introduce battery recycling programs and RoHS-3 compliant components. Competitive intensity will hinge on vendors’ ability to embed AI-powered acoustic noise cancellation, cloud analytics, and cybersecurity hardening without inflating the bill of materials.

Two-Way Radio Communication Industry Leaders

Motorola Solutions, Inc.

Hytera Communications Corporation Limited

L3Harris Technologies, Inc.

Icom Incorporated

Sepura Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: L3Harris Technologies secured a USD 300 million contract from the U.S. Department of Defense to supply tactical radios for special operations forces.

- September 2024: Hytera Communications unveiled intrinsically safe DMR portables targeting Oil and Gas users with a lower total ownership cost.

Global Two-Way Radio Communication Market Report Scope

The term "two-way radio" refers to a technology that allows people to communicate with one other via radio waves. Each user is provided with a radio unit that transmits and receives voice and data over radio waves. A two-way radio system can be as simple as two radios connected directly to each other or as complicated as an encrypted nationwide network. The Global Two-Way Radio Market is segmented by Type ( Analog, Digital), End User Industry ( Business Use ( Government and Public Safety, Utilities, Industry, and Commerce), Private Use ), and Geography.

| Handheld / Portable |

| Mobile / In-Vehicle |

| Base Station / Repeater |

| VHF (25-174 MHz) |

| UHF (400-512 MHz) |

| 700/800/900 MHz |

| SHF (1-6 GHz incl. 900 MHz ISM) |

| DMR |

| P25 |

| TETRA |

| NXDN |

| dPMR |

| PoC (Push-to-Talk-over-Cellular) |

| Government and Public Safety |

| Utilities and Energy |

| Transportation and Logistics |

| Industrial and Manufacturing |

| Construction and Mining |

| Oil and Gas |

| Hospitality and Retail |

| Education and Campus Security |

| Other end-user industries |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia Pacific | |

| Middle East | GCC |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Device Type | Handheld / Portable | |

| Mobile / In-Vehicle | ||

| Base Station / Repeater | ||

| By Frequency Band | VHF (25-174 MHz) | |

| UHF (400-512 MHz) | ||

| 700/800/900 MHz | ||

| SHF (1-6 GHz incl. 900 MHz ISM) | ||

| By Standard | DMR | |

| P25 | ||

| TETRA | ||

| NXDN | ||

| dPMR | ||

| PoC (Push-to-Talk-over-Cellular) | ||

| By End-User Industry | Government and Public Safety | |

| Utilities and Energy | ||

| Transportation and Logistics | ||

| Industrial and Manufacturing | ||

| Construction and Mining | ||

| Oil and Gas | ||

| Hospitality and Retail | ||

| Education and Campus Security | ||

| Other end-user industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia Pacific | ||

| Middle East | GCC | |

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How big is the Two-Way Radio Communication market in 2026?

It stands at USD 10.46 billion and is on track to hit USD 14.11 billion by 2031.

Which region leads spending on professional radios?

North America holds 38.62% of 2025 revenue because of FirstNet and statewide modernization mandates.

Which device category is growing fastest?

Mobile/in-vehicle systems are forecast to rise at a 7.66% CAGR through 2031.

Are smartphones replacing traditional radios?

Rugged smartphones with PoC are gaining share for non-critical tasks, but public safety agencies still rely on LMR for mission-critical voice.

What standard dominates the professional radio space?

Digital Mobile Radio (DMR) captured 37.62% of 2025 shipments, balancing cost and interoperability.

How will private LTE impact the sector?

Private LTE/5G networks are creating demand for hybrid devices that blend push-to-talk reliability with broadband data.

Page last updated on: