Satellite Modem Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

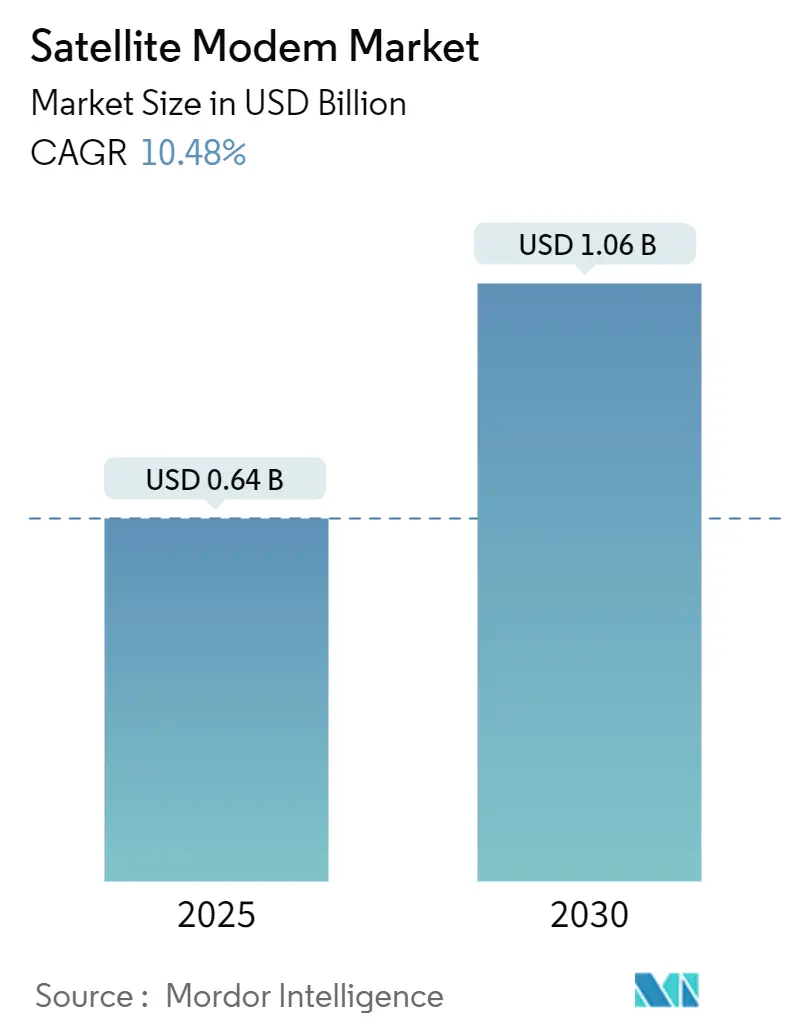

| Market Size (2025) | USD 0.64 Billion |

| Market Size (2030) | USD 1.06 Billion |

| Growth Rate (2025 - 2030) | 10.48% CAGR |

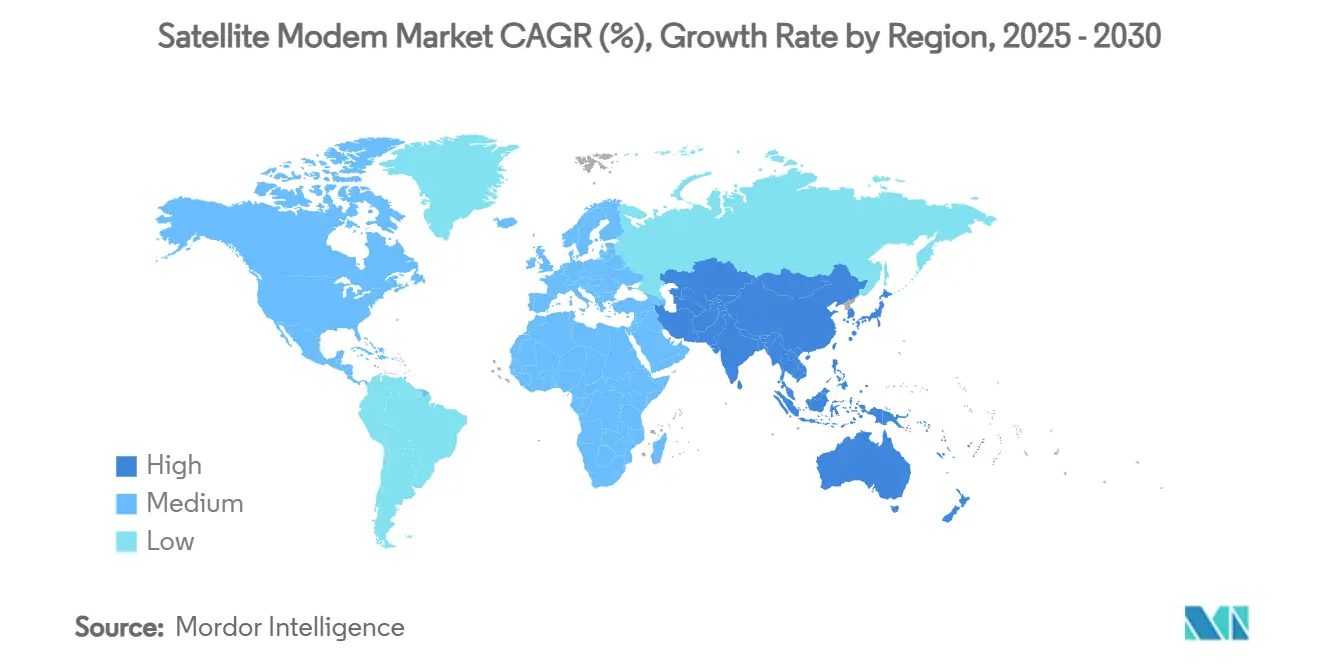

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Satellite Modem Market Analysis by Mordor Intelligence

The satellite modem market size stands at USD 0.64 billion in 2025 and is forecast to reach USD 1.06 billion by 2030, expanding at a 10.48% CAGR. Strong momentum stems from defense-led investments, high-throughput satellite (HTS) roll-outs, and 3GPP 5G-NTN standardization that embeds satellites inside mainstream mobile networks. Ku-band remains the workhorse of global fleets, yet Ka-band capacity is attracting fresh capital as operators chase higher spectral efficiency. Adaptive TDMA and hybrid waveforms are scaling quickly on virtualized ground segments, helping service providers match bandwidth supply with unpredictable demand patterns. Asia-Pacific has shifted from a follower to the fastest-growing buyer as governments link remote schools, clinics, and tower sites over LEO and GEO constellations. Meanwhile, multi-orbit procurement by the U.S. Department of Defense and the Space Development Agency underpins a resilient communication architecture strategy capable of riding out electronic-warfare stressors.[1]Josh Luckenbaugh, “Skyrocketing Demand Fuels Funding Boost for Commercial Space Program,” National Defense Magazine, nationaldefensemagazine.org

Key Report Takeaways

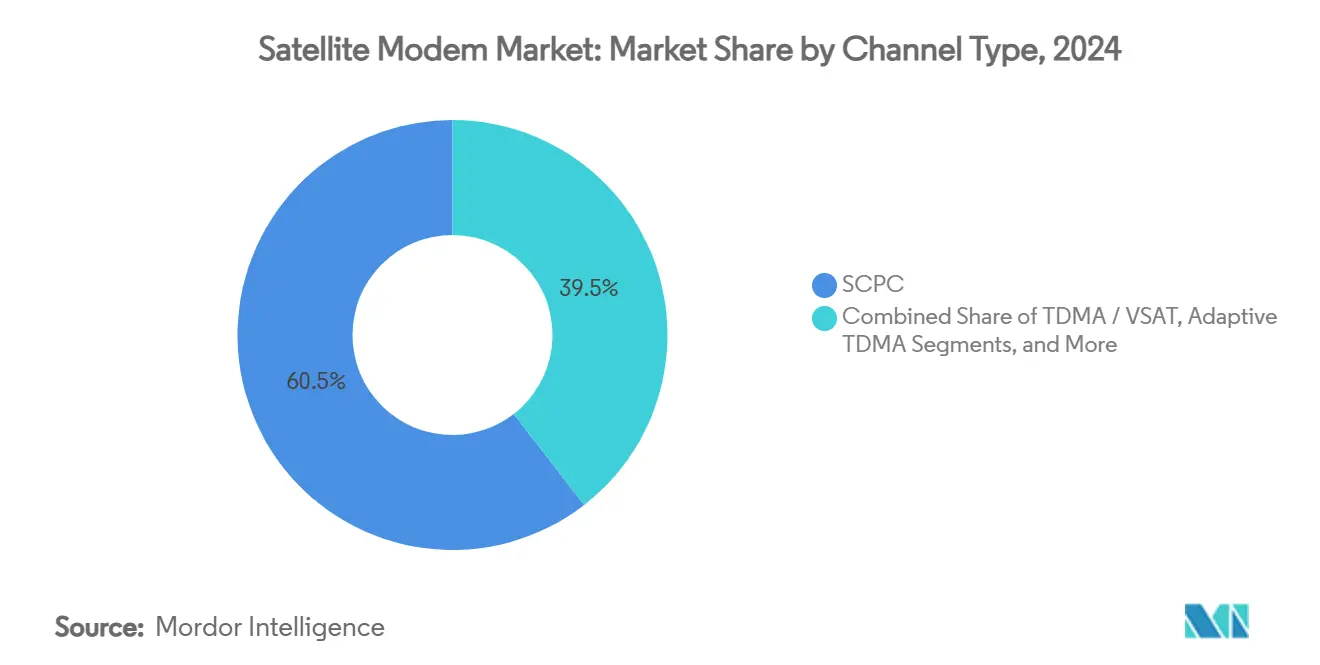

- By channel type, SCPC held 60.5% of the satellite modem market share in 2024, whereas Adaptive TDMA/Hybrid solutions are projected to grow at 11.45% CAGR to 2030.

- By frequency band, Ku-band commanded a 45.6% share of the satellite modem market size in 2024, while Ka-band is advancing at a 10.98% CAGR through 2030.

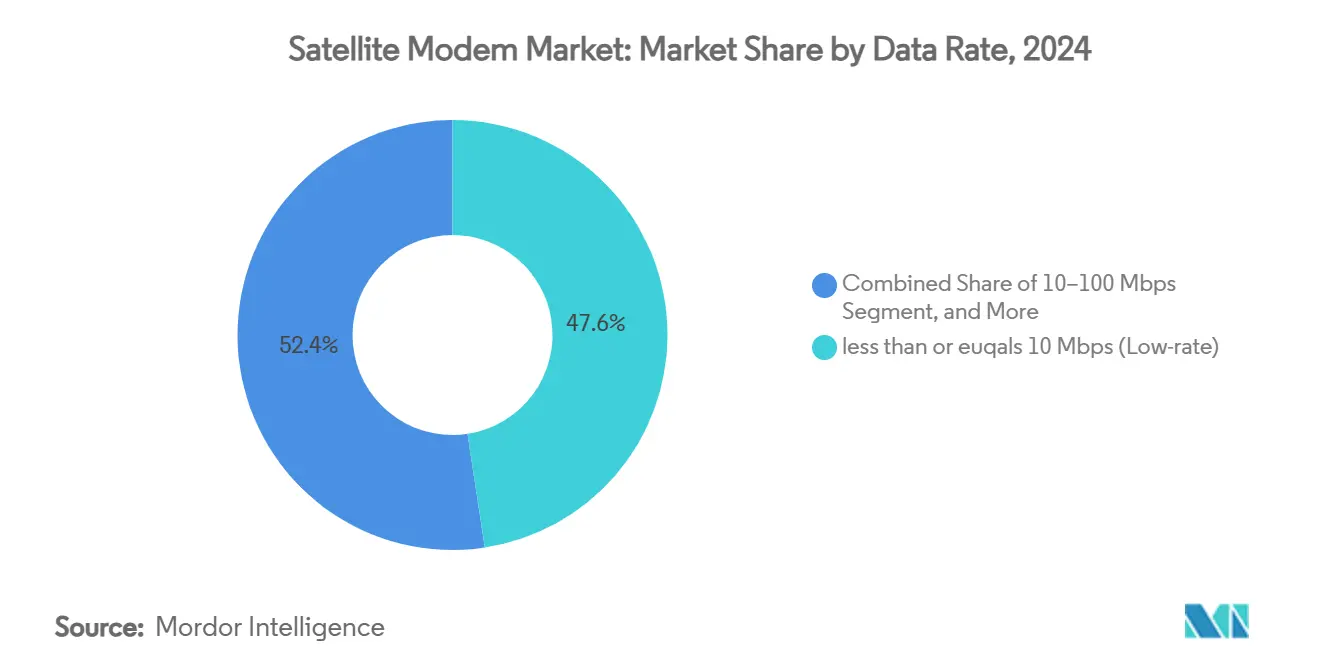

- By data rate, low-rate modems (≤10 Mbps) accounted for 47.6% of the satellite modem market size in 2024, and ultra-high-rate (>1 Gbps) products are set to expand at a 12.02% CAGR between 2025-2030.

- By application, government and defense led with 43.6% of the satellite modem market share in 2024, while cellular backhaul exhibits the highest CAGR at 10.56% to 2030.

- By geography, North America retained a 39.0% share of the satellite modem market in 2024; Asia-Pacific is poised for the quickest growth at 11.65% CAGR through 2030

Global Satellite Modem Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for HTS (High-Throughput Satellite) broadband connectivity | +2.1% | North America and Asia-Pacific | Medium term (2–4 years) |

| Expansion of satellite-based cellular backhaul for 5G | +1.8% | Asia-Pacific; spill-over to North America and Europe | Short term (≤ 2 years) |

| Defense and government spend on resilient links | +1.5% | North America and Europe; emerging Asia-Pacific | Long term (≥ 4 years) |

| 3GPP 5G-NTN standard enabling direct-to-device | +1.3% | Global; early adoption in North America and Europe | Medium term (2–4 years) |

| AI-enabled adaptive waveform optimisation | +0.9% | Global | Medium term (2–4 years) |

| Virtualised ground segment reducing TCO | +0.7% | Global; enterprise focus in North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for HTS Broadband Connectivity

HTS architecture multiplies capacity up to one-hundredfold over legacy GEO satellites, letting operators price services competitively in rural zones that fibre bypasses. Spot-beam reuse maximises spectral efficiency, and Ka-band payloads pair with adaptive coding to sustain throughput during rain fade. Eutelsat’s high-speed launch in Jordan illustrates how HTS unlocks stranded demand where right-of-way challenges stall terrestrial builds. The trend is cascading into the satellite modem market as service providers specify modems capable of 256-APSK and agile power control. Upgrades are cascading across fleet operators who are retrofitting ground hubs to speak both Ku- and Ka-band with software-defined flexibility.

Expansion of Satellite-Based Cellular Backhaul for 5G

Mobile network operators leverage satellites to light up remote cell towers, keeping licence obligations on track while deferring costly fibre spurs. LEO constellations have trimmed latency from 600 ms on GEO links to sub-50 ms, aligning with 3GPP Release 17 NTN integration that slots satellites into native 5G core networks.[2]3GPP Partners, “Non-Terrestrial Networks (NTN),” 3gpp.org Asia-Pacific tower counts rose to 5.79 million in 2024, and many rely on satellite backhaul during monsoon-induced fibre cuts. Adaptive TDMA modems distribute shared capacity across multiple eNodeBs, lowering per-site bandwidth costs. As multi-orbit terminals mature, operators will dynamically swing traffic between GEO and MEO to balance SLA and cost.

Defense and Government Spend on Resilient Satcom Links

The U.S. Space Development Agency has placed close to USD 10 billion in proliferated LEO contracts, driving demand for dual-band secure modems that interwork across orbital planes. Distributed architectures lower the risk of single-satellite failure during electronic attack, and governments worldwide are mapping similar strategies. Roughly USD 40.2 billion of 2023 global space defense outlays flowed to commercial providers, with satcom accounting for 18% of that pool. Domestic manufacturing moves, such as Hughes’ Maryland modem plant, reinforce supply-chain security while shortening lead times . Demand is especially strong for modems supporting TRANSEC and anti-jamming functions.

3GPP 5G-NTN Standard Enabling Direct-to-Device Links

Direct-to-device satellite service erases the need for bulky terminals as Release 17 smooths Doppler and timing offsets inside standard smartphones. T-Mobile’s partnership with Starlink validates the commercial path for mass-market NTN, which could shift modem volumes from thousands to millions of units annually. Samsung has unveiled a reference 5G NTN modem IP aimed at handset vendors, signalling the next battleground for chipmakers. Component miniaturisation and beam-forming advances will drive down cost per link, opening new revenue tiers such as text-only emergency connectivity, followed by full broadband. Legacy satcom operators are retooling spectra portfolios to secure contiguous S-band and L-band slices suited for handheld antennas.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High ground-segment CAPEX and OPEX | –1.4% | Global; acute in emerging markets | Long term (≥ 4 years) |

| Regulatory and spectrum-coordination hurdles | –0.8% | Global; regional variations | Medium term (2–4 years) |

| Rain-fade and link-reliability issues | –0.6% | Global; severe in tropical belts | Short term (≤ 2 years) |

| Rad-hard FPGA supply-chain shortages | –0.4% | North America and Europe hotspots | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

High Ground-Segment CAPEX and OPEX

Ground stations typically consume 30-40% of total satellite network budgets, a figure that rises further when multi-orbit tracking and switching are required. Complex terminals with phased-array antennas climb well above USD 50,000 per site, deterring deployments in lower-ARPU regions. Ongoing costs stack up through spectrum fees, energy, and specialist labour. Regulatory proposals to widen Ka- and W-band allocations could ease congestion but add coordination steps. Operators are therefore trialling cloud-hosted modems and shared gateways that amortise expenses across multiple tenants.

Regulatory and Spectrum-Coordination Hurdles

Securing ITU filings can stretch to two years, pushing revenue recognition timelines and chilling investor appetite. National regulators tighten orbital debris and licensing rules, mandating detailed end-of-life plans. Terrestrial 5G encroachment into C- and Ku-band uplinks forces satellite operators to invest in filter technology and coordination studies. Europe has made headway with CEPT decisions that fast-track IoT payloads below 1 GHz, yet higher bands still demand dense sharing analyses. Harmonised regulatory frameworks remain patchy, complicating multi-region service launches.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Channel Type: SCPC Strength Faces Adaptive Acceleration

SCPC technology accounted for 60.5% of the satellite modem market in 2024, prized for guaranteed bandwidth in mission-critical links.[3]Gilat Satellite Networks, “The Importance of Multi-Topology SCPC Modems,” gilat.com Dedicated carriers ensure predictable latency that defense, energy, and finance operators treat as non-negotiable. Adaptive TDMA/Hybrid, however, is scaling at an 11.45% CAGR as virtualised hubs slice bandwidth dynamically and close utilisation gaps.

TDMA/VSAT equipment remains attractive where cost per bit outweighs absolute performance, and carrier-in-carrier waveforms fill specialist niches requiring bandwidth overlays. Multi-topology SCPC modems now switch modes on the fly, merging the certainty of SCPC with the pooling efficiency of TDMA. Over the forecast window, SCPC will continue to hold the largest revenue pool, yet hybrid modes will win incremental deployments where operators monetise bursty traffic without forfeiting quality of service.

By Frequency Band: Ka-Band Upshifts Growth Trajectory

Ku-band retained 45.6% share of the satellite modem market size in 2024, benefiting from widespread gateways and established operator business models. Ka-band modems are forecast to post a 10.98% CAGR through 2030 as HTS fleets derive gigabit-class capacity from broader channel allocations.

Although Ka-band suffers from higher rain attenuation, fade-mitigation and adaptive code schemes narrow availability gaps, C-band persists for broadcast and high-reliability enterprise uses, while X-band remains a protected domain for government. Advanced terminals toggle Ku- and Ka-band automatically, letting airlines and maritime operators pick the least congested channel in real time. As spectrum crowding intensifies, multi-band flexibility will increasingly define procurement criteria.

By Data Rate: Ultra-High-Rate Modems Gain Momentum

Low-rate devices (≤10 Mbps) dominated the satellite modem market share at 47.6% in 2024, underpinning IoT telemetry, SCADA, and basic VoIP services. Yet ultra-high-rate (>1 Gbps) categories are set to climb 12.02% CAGR as broadcasters and cloud providers seek fibre-like throughput.

Modulation advances such as 128/256-APSK and GaN-on-Diamond amplifiers enable gigabit-class links within compact terminals. Mid-rate (10-100 Mbps) and high-rate (100 Mbps-1 Gbps) systems will remain staples for corporates balancing cost and performance. Growth in immersive media and remote surgery will push premium modem demand upward, while compression and caching temper bandwidth escalation for day-to-day enterprise traffic.

By Application: Cellular Backhaul Surges Ahead

Government and defense continued to lead revenue with 43.6% of the satellite modem market in 2024, supported by US and allied modernization budgets. Cellular backhaul is accelerating at a 10.56% CAGR on the back of universal-coverage pledges and tower densification in mountainous and island geographies.

Energy firms deploy ruggedized modems on offshore rigs, and enterprise banking networks rely on encrypted GEO circuits for continuity. Inflight connectivity is transitioning toward multi-orbit service to keep pace with passenger expectations, as demonstrated by Delta’s fleet upgrade. Broadcast contribution will preserve a specialist premium niche requiring ultra-stable latency and bandwidth guarantees.

Geography Analysis

North America held 39.0% of the satellite modem market in 2024, buoyed by Pentagon constellation awards near USD 10 billion and a 40% uplift in Space Force commercial satcom spend for 2025. Federal demand creates a stable revenue floor while private operators test direct-to-device services across rural communities. The FCC’s sweeping proposal to open 20,000 MHz more spectrum further secures long-term capacity pipelines.

Asia-Pacific is projected to clock the highest regional growth at 11.65% CAGR, underwritten by cellular tower expansion, government digitisation, and maritime trade lanes needing always-on connectivity.[4]ST Engineering iDirect, “Indonesia’s Satria-1 Satellite Expansion,” stengg.com Indonesia’s SATRIA-1 program highlights how archipelagic states leapfrog terrestrial constraints via GEO HTS links. China’s rapid satellite manufacturing ramp and India’s space-policy liberalisation intensify regional supply competition.

Europe shows steady momentum, aligned with digital sovereignty initiatives and ESA-backed secure connectivity programs. Operators here are experimenting with GEO-LEO hybrids to ensure coverage diversity and low latency. South America and the Middle East and Africa remain under-penetrated yet strategic. LEO constellations promise to shrink service costs, but currency volatility and regulatory friction slow adoption. As satellite modem prices ease, uptake across remote mining, oilfield, and humanitarian agencies is expected to accelerate

Competitive Landscape

The satellite modem market features a moderately concentrated field led by ST Engineering iDirect, Comtech EF Data, Viasat, Gilat Satellite Networks, and Hughes Network Systems. These incumbents differentiate through multi-orbit firmware, AI-enabled carrier recovery, and tight integration with cloud orchestration layers. Recent moves include MDA Space’s acquisition of SatixFy, reinforcing software-defined beamforming IP within its portfolio.

Emerging challengers focus on ASIC-level power savings and smartphone-grade NTN chips, vying for future direct-to-device traffic. Open-source waveform stacks and commercial off-the-shelf SDR platforms lower barriers, enabling regional OEMs to target niche national security and broadcast verticals. Concurrently, AI start-ups pitch predictive network-management algorithms that bolt onto legacy hubs, promising bandwidth gains without hardware swaps.

Strategic partnerships are proliferating. Hughes and Eutelsat extend low-earth coverage across Europe, while iDirect’s Intuition suite embeds container-based network functions to shorten service rollouts. Consolidation pressures will likely intensify after 2027 as softwarisation erodes hardware margins, pushing vendors to lock in ecosystem plays around cloud APIs and managed services.

Satellite Modem Industry Leaders

ST Engineering iDirect

Comtech EF Data

Gilat Satellite Networks

Viasat Inc.

Hughes Network Systems

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: MDA Space achieved an industry first in satellite digital beam forming with the MDA AURORA Ka-band direct radiating array.

- July 2025: MDA Space completed acquisition of SatixFy Communications to bolster software-defined satellite solutions.

- May 2025: Hughes partnered with Eutelsat to widen high-speed LEO connectivity across Europe.

- March 2025: Delta Air Lines selected Hughes’ Fusion multi-orbit inflight connectivity for more than 400 aircraft.

Global Satellite Modem Market Report Scope

| SCPC |

| TDMA / VSAT |

| Carrier-in-Carrier |

| Adaptive TDMA / Hybrid |

| Other Channel Types |

| C-band |

| X-band |

| Ku-band |

| Ka-band |

| Multi-band / Agile |

| less than or euqals 10 Mbps (Low-rate) |

| 10–100 Mbps (Mid-rate) |

| 100 Mbps–1 Gbps (High-rate) |

| above 1 Gbps (Ultra-high) |

| Government and Defense |

| Cellular Backhaul |

| Enterprise and Banking |

| Energy and Utilities |

| Maritime |

| Aeronautical |

| Broadcast and Media Contribution |

| Other Applications |

| North America |

| South America |

| Europe |

| Asia-Pacific |

| Middle East and Africa |

| By Channel Type | SCPC |

| TDMA / VSAT | |

| Carrier-in-Carrier | |

| Adaptive TDMA / Hybrid | |

| Other Channel Types | |

| By Frequency Band | C-band |

| X-band | |

| Ku-band | |

| Ka-band | |

| Multi-band / Agile | |

| By Data Rate | less than or euqals 10 Mbps (Low-rate) |

| 10–100 Mbps (Mid-rate) | |

| 100 Mbps–1 Gbps (High-rate) | |

| above 1 Gbps (Ultra-high) | |

| By Application | Government and Defense |

| Cellular Backhaul | |

| Enterprise and Banking | |

| Energy and Utilities | |

| Maritime | |

| Aeronautical | |

| Broadcast and Media Contribution | |

| Other Applications | |

| By Geography | North America |

| South America | |

| Europe | |

| Asia-Pacific | |

| Middle East and Africa |

Key Questions Answered in the Report

What is the current satellite modem market size and its forecast CAGR to 2030?

The satellite modem market size is USD 0.64 million in 2025 and is projected to grow at a 10.48% CAGR through 2030.

Which channel type currently dominates the satellite modem market?

Single Channel Per Carrier (SCPC) leads with 60.5% market share in 2024.

Which application segment is the fastest-growing in the satellite modem market?

Cellular backhaul shows the highest growth, expanding at a 10.56% CAGR to 2030.

Which geographic region is expected to record the fastest growth in satellite modem demand?

Asia-Pacific is forecast to grow at an 11.65% CAGR between 2025 and 2030.

Why is Ka-band gaining traction over Ku-band in satellite modems?

Ka-band offers larger bandwidth and supports high-throughput satellites, driving a 10.98% CAGR despite higher rain-fade challenges.

What key factor is propelling direct-to-device satellite modem adoption?

3GPP Release 17 Non-Terrestrial Network standards enable smartphones to connect directly to satellites, opening high-volume consumer markets.

Page last updated on: