Cellular Modem Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

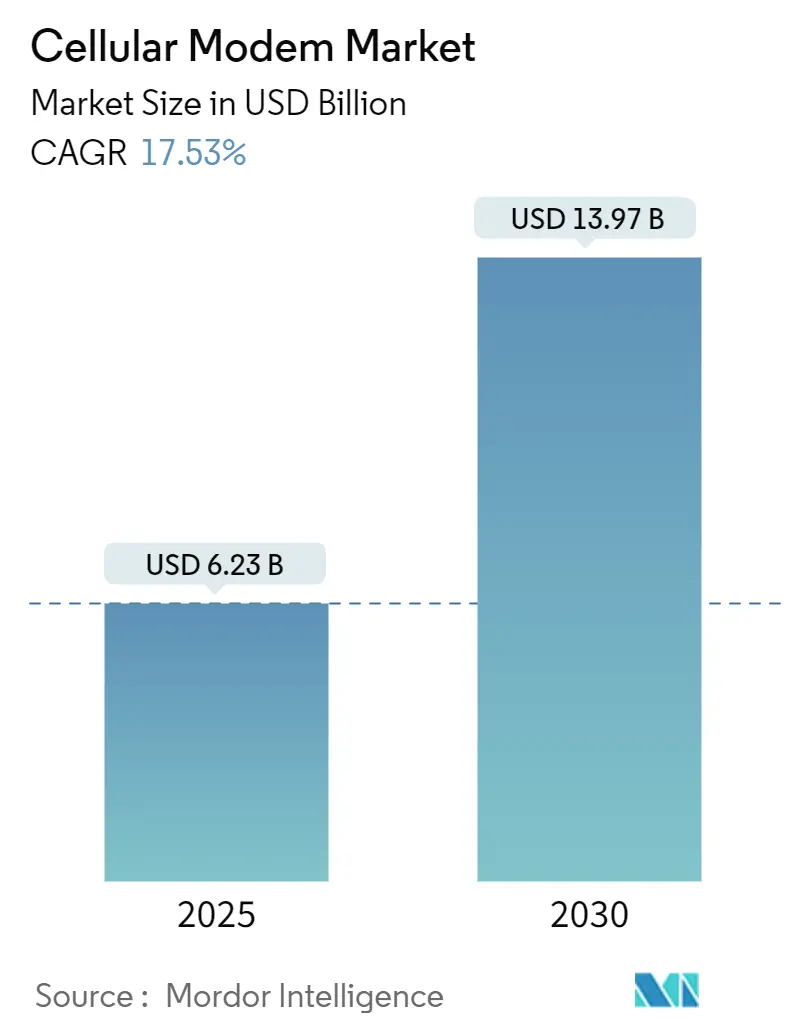

| Market Size (2025) | USD 6.23 Billion |

| Market Size (2030) | USD 13.97 Billion |

| Growth Rate (2025 - 2030) | 17.53% CAGR |

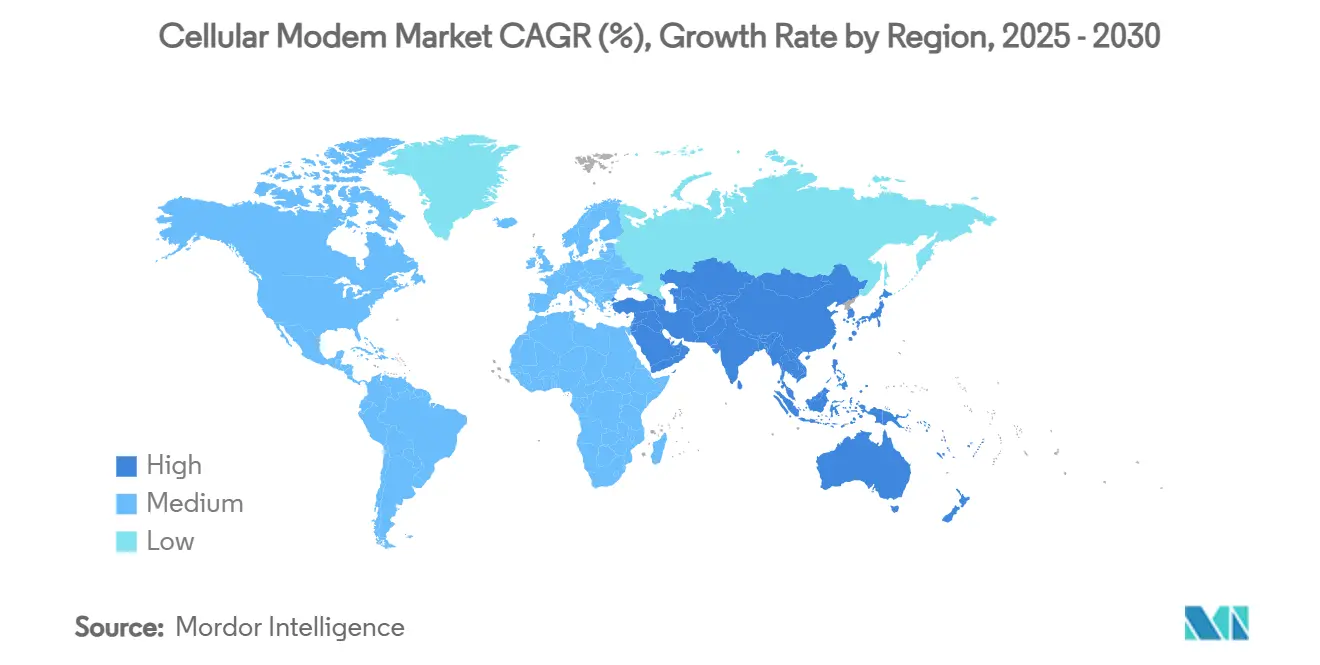

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Cellular Modem Market Analysis by Mordor Intelligence

The cellular modem market size is USD 6.23 billion in 2025 and is forecast to reach USD 13.97 billion by 2030, translating into a 17.53% CAGR over the period. Strong momentum comes from 5G network maturity, the surge of cellular-IoT endpoints beyond 4 billion in 2024, and rapid uptake of automotive telematics that together widen addressable demand across consumer, industrial, and fixed-access domains. Asia-Pacific leads current revenue, yet North America registers the fastest expansion on the back of fixed-wireless access (FWA) roll-outs and private 5G for enterprises[1]Ericsson Mobility Report, Ericsson, ericsson.com. Technology dynamics show 4G LTE preserving a cost-efficient mainstream while 5G RedCap scales as a reduced-capability bridge for massive IoT workloads. At the same time, form-factor convergence toward integrated system-on-chips (SoCs) compresses the total cost of ownership and accelerates design cycles for device makers.

Key Report Takeaways

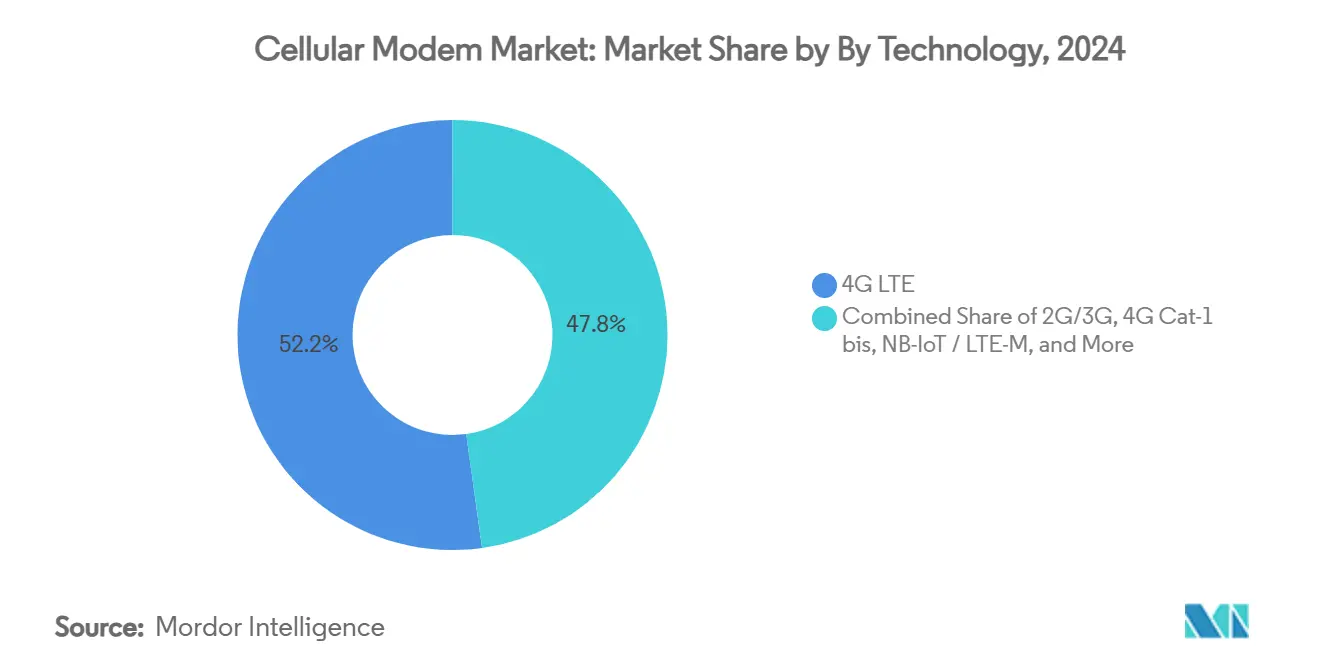

- By technology, 4G LTE commanded 52.2% of the cellular modem market share in 2024, while 5G RedCap is poised to advance at an 18.3% CAGR to 2030.

- By form factor, integrated SoC with modem held 50.2% revenue share in 2024; embedded cellular modules record the highest projected CAGR at 19.1% through 2030.

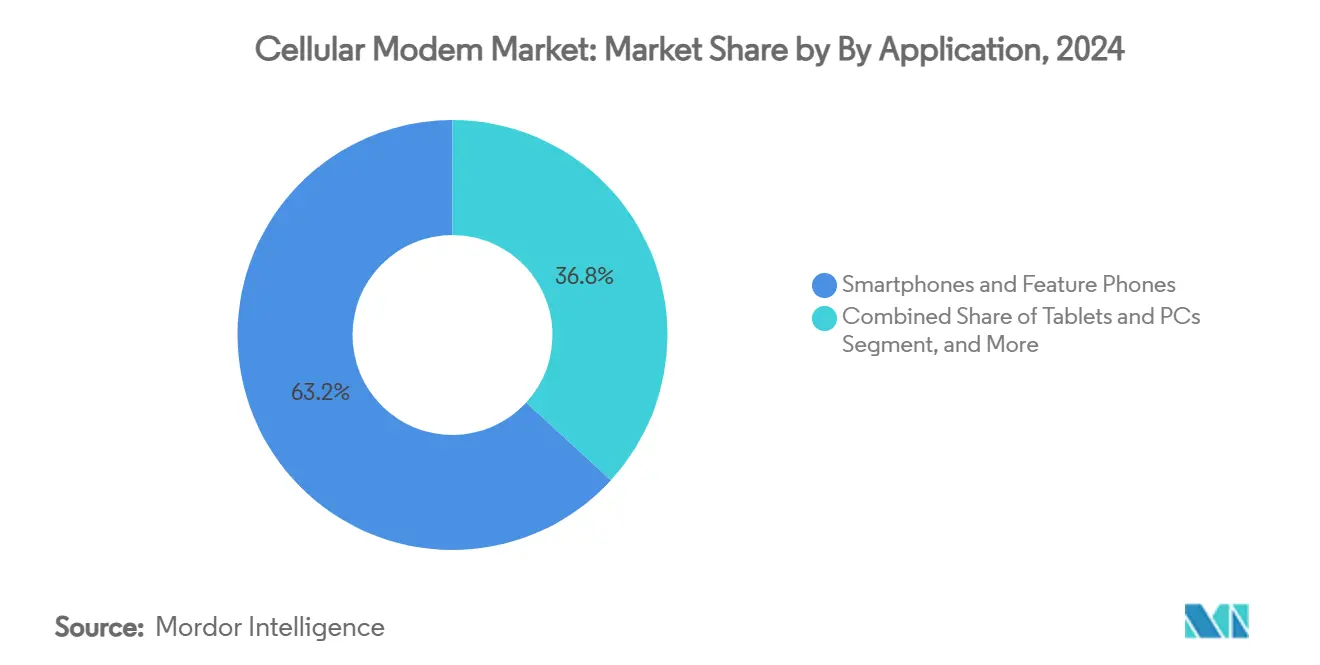

- By application, smartphones accounted for a 63.2% share of the cellular modem market size in 2024, and automotive & connected vehicles are accelerating at an 18.9% CAGR to 2030.

- By geography, Asia-Pacific led with 44.20% revenue share in 2024, whereas North America is forecast to expand at a 19.50% CAGR through 2030.

Global Cellular Modem Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Proliferation of global 5G roll-outs | +4.2% | Global (Asia-Pacific and North America lead) | Medium term (2-4 years) |

| Surging cellular-IoT connections across industries | +3.8% | Global, strongest in Asia-Pacific | Long term (≥ 4 years) |

| Connected vehicle and telematics adoption boom | +2.9% | North America and Europe | Medium term (2-4 years) |

| Rapid uptake of Fixed-Wireless Access (FWA) CPEs | +2.1% | North America and rural Europe | Short term (≤ 2 years) |

| Low-cost 4G Cat-1 bis for massive-IoT | +1.8% | Global cost-sensitive markets | Short term (≤ 2 years) |

| On-device AI accelerators embedded in modems | +1.5% | Premium markets worldwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Proliferation of global 5G roll-outs

More than 2.9 billion 5G subscriptions are expected worldwide by end-2025, enabling network-slice services and latency-sensitive industrial use cases. Operators increasingly deploy 5G RedCap to serve mid-tier IoT without full 5G complexity; T-Mobile’s first commercial RedCap device in North America exemplifies early adoption[2]T-Mobile Introduces First Commercial 5G RedCap Device in North America, 5G Americas, 5gamericas.org. AT&T’s nationwide RedCap footprint covering 200 million points of presence further validates operator confidence in reduced-capability 5G for scale. Infrastructure maturity lets modem suppliers optimize SKUs across premium and cost-centric tiers instead of pursuing monolithic designs. This diversity lifts the total available market and supports the cellular modem market’s double-digit trajectory.

Surging cellular-IoT connections across industries

Cellular-IoT endpoints passed 4 billion in 2024, driven by manufacturing, logistics, and utilities that prefer carrier-grade reliability over proprietary short-range protocols. LTE-M balances throughput and low power for factory sensors that must last multiple years on battery. Partnerships such as Nordic Semiconductor with Deutsche Telekom underline how device-network alignment accelerates deployment. Enterprises appreciate unified SIM management across global footprints, simplifying logistics and security. For modem vendors, multi-band support and low-power design become decisive differentiators, reinforcing demand across the cellular modem market.

Connected vehicle and telematics adoption boom

Global connected vehicles are experiencing high growth, reflecting regulative e-call mandates and consumer appetite for over-the-air upgrades. MediaTek’s Dimensity Auto Connect MT2739 integrates 5G-Advanced with satellite fallback, highlighting stringent automotive specifications around coverage continuity. Qualcomm’s automotive revenue jumped 61% year-on-year to USD 961 million in Q1 2025 as OEMs embed premium connectivity. Cellular modem suppliers benefit from higher ASPs tied to extended temperature and lifecycle requirements, enhancing profitability within the cellular modem market.

Rapid uptake of fixed-wireless access (FWA) CPEs

Dell’Oro predicts FWA equipment spending to exceed USD 40 billion as operators monetize under-utilized 5G spectrum for home broadband. FWA CPE shipments outpaced cable DOCSIS units for the first time in Q2 2024, signaling a structural change in fixed connectivity. Ericsson projects FWA to account for more than 35% of new fixed broadband connections by 2030, 80% of which will ride on 5G Modem makers capture incremental revenue by repurposing mobile chipsets for stationary CPEs while commanding premium margins for thermal-optimized designs. This reinforces growth prospects for the cellular modem market.

Restraints Impact Analysis*

| RESTRAINTS | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Supply-chain swings and module inventory corrections | -1.4% | Global; Chinese EMS most exposed | Short term (≤ 2 years) |

| Escalating multi-mode 5G design/licensing costs | -1.9% | Global; sharpest in value tiers | Medium term (2-4 years) |

| US-China export-control turbulence | -1.5% | Cross-border supply chains | Long term (≥ 4 years) |

| Ultra-low-power regulations (<1 mW idle) challenge | -0.9% | Europe and North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating multi-mode 5G design/licensing costs

Samsung’s Exynos Modem 5400 demonstration of 11.2 Gbps performance on FR1 alone underscores the R&D intensity required to stay competitive. Royalty payments-Qualcomm booked USD 1.54 billion in licensing fees during FY 2024-raise entry barriers for mid-tier chipmakers. The cost burden limits innovation among smaller houses, moderating total addressable expansion for the cellular modem market.

US-China export-control turbulence

Sanctions on advanced node tools restrict access to latest foundry processes, forcing Chinese suppliers onto trailing nodes that trail in power efficiency. OEMs hedge by dual-sourcing modems from Taiwanese and US vendors, complicating forecast visibility. These cross-border frictions inject risk and could dampen long-range CAGR for the cellular modem market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: 5G RedCap bridges performance gap

4G LTE retained 52.2% cellular modem market share in 2024 by offering reliable and cost-effective bandwidth for mainstream consumer and industrial devices. Yet the segment’s growth moderates as operators repurpose spectrum for 5G. Conversely, 5G RedCap is projected to grow at 18.3% CAGR because it operates on narrower channels and delivers longer battery life, making it ideal for wearables and wide-area sensors[3]RedCap: Bridging the Gap Between Performance and Efficiency in 5G, SGS, sgs.com . The cellular modem market size for 5G RedCap chips is set to broaden sharply once nationwide coverage matures. mmWave remains a niche confined to dense venues due to propagation limits, while NB-IoT maintains a foothold in utilities where deep indoor penetration outweighs throughput demands.

Smartphone OEMs have begun integrating Qualcomm’s Snapdragon X35, the first commercial 5G RedCap modem, to differentiate lower-mid tiers without incurring full-band silicon costs. Industrial routers leverage sub-6 GHz 5G NR for deterministic latency, supporting remote operation in mining and ports. This shift from one-size-fits-all to application-specific hardware underpins sustained segmentation and revenue diversity across the cellular modem market.

By Form Factor: Integration drives efficiency

Integrated SoCs captured 50.2% of revenue in 2024, combining baseband, RF, and often AI accelerators onto a single die that lowers bill-of-materials and eases thermal design. The cellular modem market size associated with SoC shipments benefits from smartphone and tablet refresh cycles that favor sleek, power-efficient designs. Embedded cellular modules, set to expand at 19.1% CAGR, appeal to industrial OEMs lacking RF expertise; off-the-shelf certification trims months from design schedules. Discrete basebands persist for custom RF front-ends in satellite hybrid devices, whereas USB/LTE dongles decline as connectivity becomes native to endpoints.

Apple’s in-house C1 modem is integrated into its A-series application processor, underscoring vertical strategies that threaten standalone chip vendors. Module specialists such as Quectel differentiate via firmware libraries, not raw silicon, thereby protecting margins even as hardware commoditizes. This evolving form-factor mix supports healthy volume expansion for the cellular modem market through 2030.

By Application: Automotive connectivity accelerates

Smartphones generated 63.2% of 2024 revenue, but replacement cycles lengthen, steering suppliers to diversify. Automotive & connected vehicles, growing at 18.9% CAGR, rely on resilient designs and multi-band antennas to deliver over-the-air updates and V2X messages. The cellular modem market size for automotive chips widens as regulatory mandates, such as e-call in Europe, standardize embedded connectivity. Tablets and PCs sustain volume as remote work endures, while industrial gateways anchor digital-factory use cases with redundant 4G/5G links. Wearables and XR devices lean on 5G RedCap for extended battery life, opening fresh niches for low-power modems.

Operators bundle FWA service with high-gain CPEs, elevating demand for temperature-hardened modems that can deliver fiber-like speeds. Collectively, application diversification cushions the cellular modem market against smartphone cyclicality.

Geography Analysis

Asia-Pacific generated 44.20% of 2024 revenue on the back of China’s 800 million 5G connections and tier-one OEM manufacturing clusters[4]The Mobile Economy China 2024, GSMA, gsma.com. China’s communication-equipment expenditure reached CNY 1.68 trillion in 2023 and is projected to top CNY 2.52 trillion (USD 355 billion) by 2030, further cementing supply-chain gravity. Japan and South Korea contribute premium ASPs via early adoption of industrial private 5G, while India climbs the value chain as contract manufacturers localize modem assembly to mitigate tariffs. The cellular modem market size within APAC, therefore, marries volume leadership with rising average selling prices.

North America, forecast to grow at a 19.50% CAGR, benefits from a wide mid-band spectrum and aggressive FWA subscriber acquisition. Hybrid cellular-satellite projects such as Terrestar–Monogoto highlight the appetite for ubiquitous coverage in logistics and agriculture. Mexico’s inclusion in USMCA encourages near-shoring of module assembly, reducing lead times for US carriers. This regional ecosystem underpins the fastest expansion rate in the cellular modem market.

Europe sustains steady demand via smart-factory roll-outs and automotive mandates. Energy-efficiency regulations spur low-power modem design, creating specialized pockets of growth. The Middle East & Africa leverage cellular connectivity to leapfrog fixed infrastructure, particularly through satellite-enhanced IoT for remote assets. Altogether, geographic diversification balances cyclical risks and supports the global cellular modem market trajectory.

Competitive Landscape

The cellular modem market shows moderate concentration. Qualcomm leads with broad IP and silicon-system verticals, reporting USD 11.67 billion revenue in Q1 2025 on an 18% annual rise. MediaTek narrowed the gap, lifting smartphone 5G share from 22.8% to 29.2% as sub-USD 250 handsets surged 62%. Samsung and Apple pursue in-house modems to secure differentiation and cost control, shrinking the accessible market for merchant suppliers. Qualcomm’s USD 200 million purchase of Sequans’ 4G IoT assets bolsters industrial portfolio depth while removing a rival.

Module vendors battle ASP erosion from Chinese peers; Quectel releases multiband antennas to embed more value around hardware. Nordic Semiconductor targets ultra-low-power niches with its nRF9151 system-in-package. Competitive advantage increasingly hinges on system software, certification services, and AI offload rather than raw throughput alone. Overall, the top five chipset suppliers account for appreciable but not dominating shares, rendering the cellular modem market moderately consolidated yet open to specialist disruptors.

Cellular Modem Industry Leaders

-

Qualcomm Technologies Inc.

-

MediaTek Inc.

-

Quectel Wireless Solutions

-

Fibocom Wireless Inc.

-

Samsung Electronics Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: AT&T extended 5G RedCap coverage to 200 million points of presence to accelerate mid-tier IoT, reflecting a strategy to monetize spectrum through differentiated service tiers.

- May 2025: MediaTek launched Dimensity 9400e with integrated AI and 5G to capture flagship handset design wins, aiming to erode Qualcomm’s premium dominance.

- March 2025: Nordic Semiconductor partnered with Deutsche Telekom to streamline “cellular-first” IoT, signaling telco-silicon alignment to speed enterprise deployments.

- February 2025: Apple unveiled the C1 integrated modem inside iPhone 16e, pursuing vertical integration to reduce supplier dependence and secure modem roadmap control.

Global Cellular Modem Market Report Scope

| 2G/3G |

| 4G LTE |

| 4G Cat-1 bis |

| 5G NR (Sub-6 GHz) |

| 5G NR (mmWave) |

| NB-IoT / LTE-M |

| Discrete Baseband Chips |

| Integrated SoC with Modem |

| Embedded Cellular Modules |

| Standalone USB/LTE Dongles |

| Smartphones and Feature Phones |

| Tablets and PCs |

| Automotive and Connected Vehicles |

| Industrial Routers and Gateways |

| IoT Sensors and Meters |

| Wearables and XR Devices |

| CPE / Fixed-Wireless Access |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Technology | 2G/3G | ||

| 4G LTE | |||

| 4G Cat-1 bis | |||

| 5G NR (Sub-6 GHz) | |||

| 5G NR (mmWave) | |||

| NB-IoT / LTE-M | |||

| By Form Factor | Discrete Baseband Chips | ||

| Integrated SoC with Modem | |||

| Embedded Cellular Modules | |||

| Standalone USB/LTE Dongles | |||

| By Application | Smartphones and Feature Phones | ||

| Tablets and PCs | |||

| Automotive and Connected Vehicles | |||

| Industrial Routers and Gateways | |||

| IoT Sensors and Meters | |||

| Wearables and XR Devices | |||

| CPE / Fixed-Wireless Access | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current cellular modem market size and how fast is it growing?

The cellular modem market size is USD 6.23 billion in 2025 and is projected to expand to USD 13.97 billion by 2030, reflecting a 17.53% CAGR.

Which technology segment is expanding the fastest?

5G Reduced Capability (RedCap) is the quickest-growing technology, advancing at an 18.3% CAGR as it balances battery life, bandwidth, and cost for massive-IoT and wearable devices.

Why is North America the quickest-growing region?

Aggressive fixed-wireless access roll-outs, abundant mid-band spectrum, and rising private-5G deployments position North America for a 19.50% CAGR through 2030.

How are automotive applications influencing demand?

Connected-vehicle and telematics adoption is driving an 18.9% CAGR in automotive modems, supported by e-call mandates, over-the-air updates, and emerging vehicle-to-everything use cases.

Page last updated on: