Cloud Security Posture Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

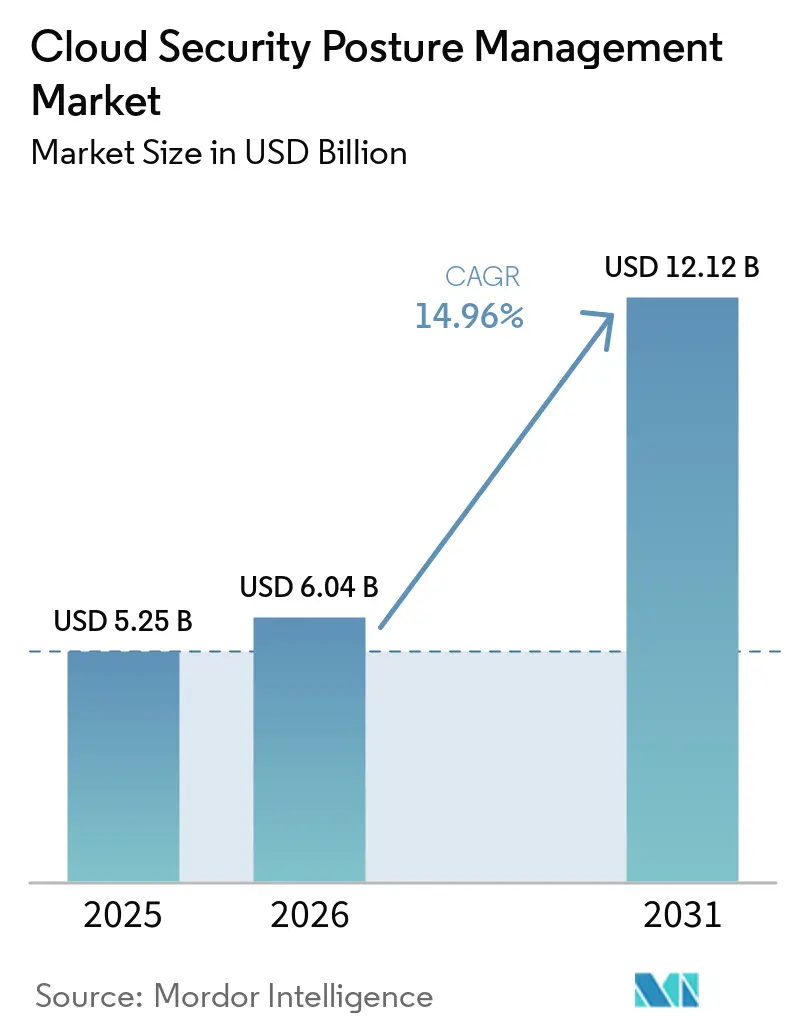

| Market Size (2026) | USD 6.04 Billion |

| Market Size (2031) | USD 12.12 Billion |

| Growth Rate (2026 - 2031) | 14.96% CAGR |

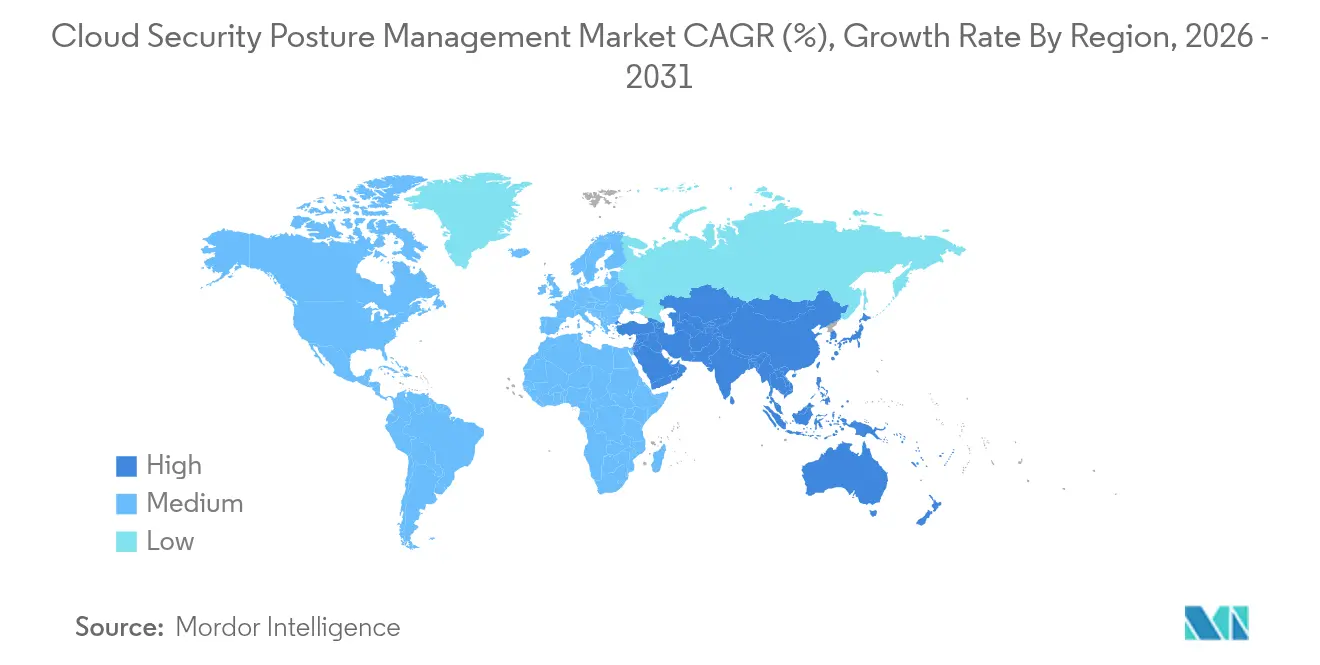

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cloud Security Posture Management Market Analysis by Mordor Intelligence

The Cloud Security Posture Management Market size is projected to expand from USD 5.25 billion in 2025 and USD 6.04 billion in 2026 to USD 12.12 billion by 2031, registering a CAGR of 14.96% between 2026 to 2031.

Heightened regulatory pressure, rapid multi-cloud expansion, and the shift toward AI-enabled risk mitigation combine to keep demand resilient even as overall IT spending slows in several regions. Vendors are embedding posture-management functions inside broader cloud-native security platforms so that security teams can move from reactive alert handling to continuous guardrail enforcement. The competitive context now favors suppliers that fuse CSPM with workload, entitlement, and application protection to give enterprises a single source of truth across development and runtime environments. Large deals involving hyperscalers and leading cybersecurity firms point to a maturing landscape in which platform breadth and deep provider integrations count more than feature novelty.

Key Report Takeaways

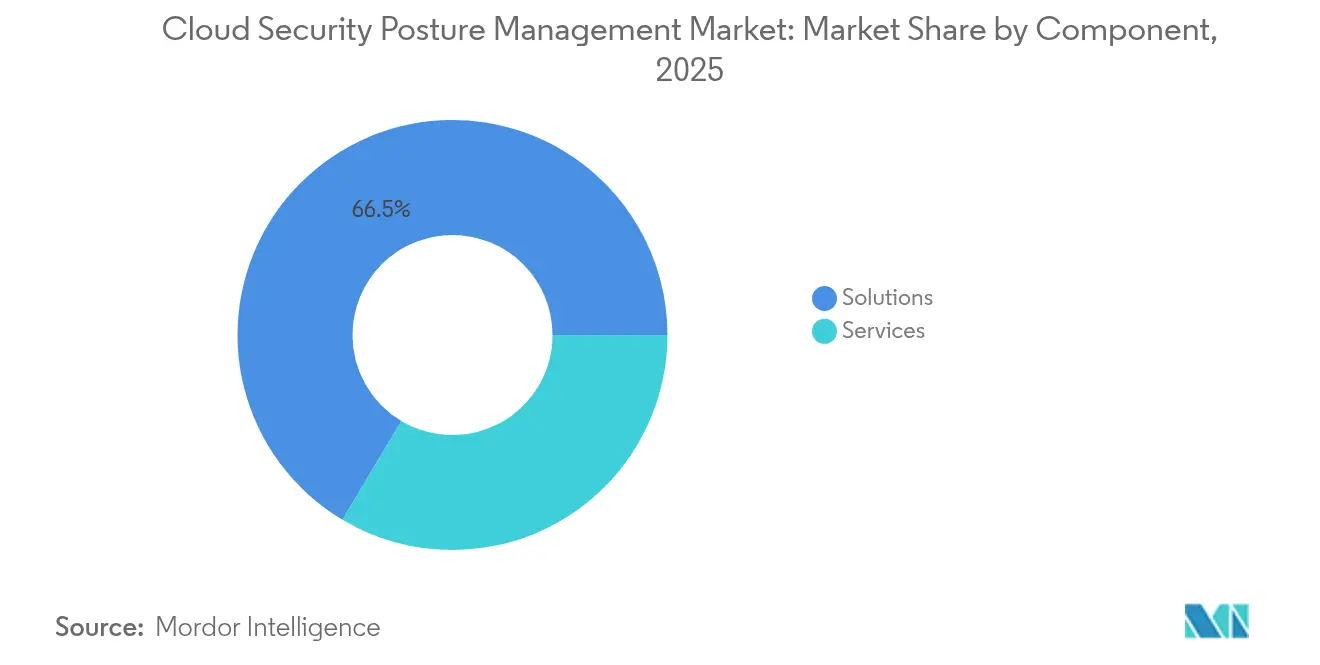

- By component, Solutions captured 66.45% of the Cloud Security Posture Management market share in 2025, while Services are set to expand at a 15.12% CAGR through 2031.

- By cloud model, Infrastructure as a Service held 48.92% of the Cloud Security Posture Management market size in 2025; Software as a Service is projected to grow at 15.2% CAGR to 2031.

- By deployment mode, public-cloud workloads made up 44.35% of 2025 deployments, yet hybrid architectures will outpace them with a 15.74% CAGR over the forecast period.

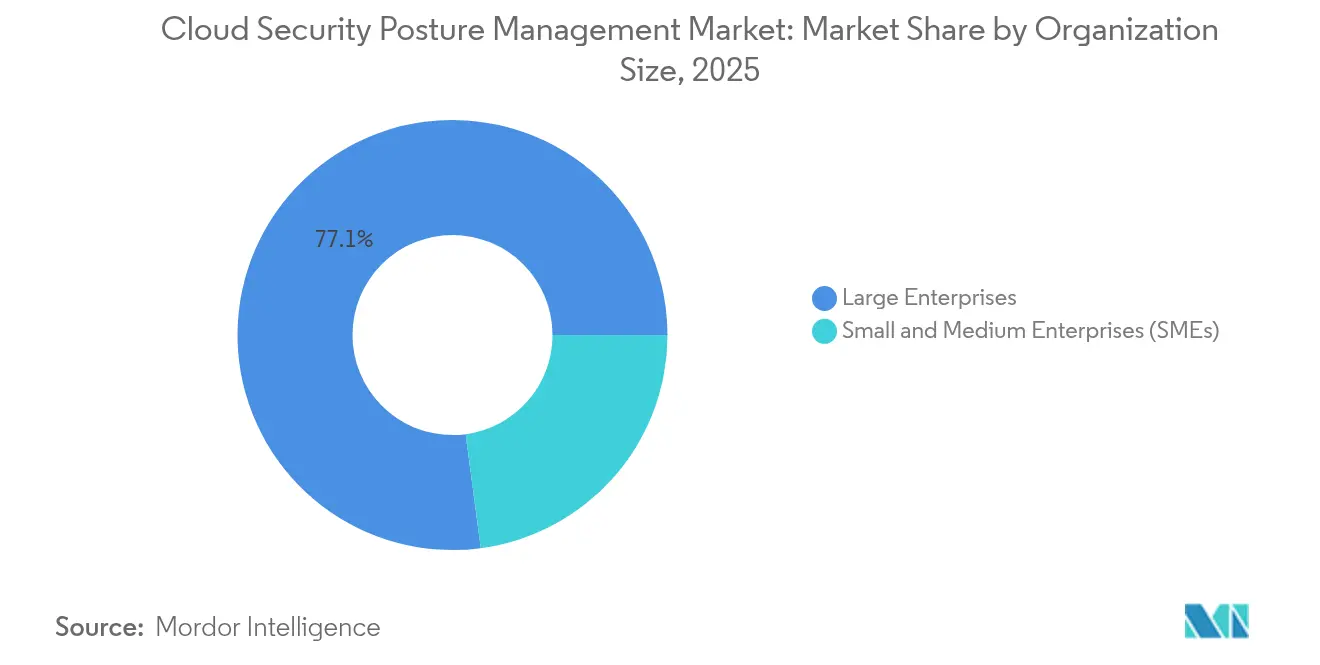

- By organization size, Large Enterprises commanded 77.10% share of the Cloud Security Posture Management market in 2025, whereas Small and Medium Enterprises are advancing at 15.08% CAGR through 2031.

- By industry vertical, Banking, Financial Services, and Insurance accounted for 29.12% of 2025 revenue; Healthcare is poised for 15.07% CAGR over the forecast period.

- By geography, North America led with 35.02% revenue share in 2025, while Asia-Pacific shows the highest regional CAGR at 15.55% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cloud Security Posture Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Integration of CSPM into CNAPP platforms | +2.8% | Global, early adoption in North America and EU | Medium term (2-4 years) |

| Rise of AI-assisted auto-remediation engines | +2.5% | Global, concentrated in technology-forward markets | Short term (≤ 2 years) |

| Expansion of zero-trust and shared-responsibility audits | +2.1% | North America and EU leading, APAC following | Medium term (2-4 years) |

| Regulatory push for real-time cloud-config reporting | +1.9% | EU and APAC core, expanding to the Americas | Long term (≥ 4 years) |

| Multi-cloud sprawl in mid-market enterprises | +1.7% | Global, with concentration in developed markets | Short term (≤ 2 years) |

| Insurance-driven security scorecard requirements | +1.4% | North America leading, expanding globally | Medium term |

| Source: Mordor Intelligence | |||

Integration of CSPM into Cloud-Native Application Protection Platform (CNAPP) ecosystems

cloud security posture management is rapidly shifting from a standalone dashboard to a foundational module inside unified CNAPP suites, a change that relieves security teams from juggling overlapping consoles and policies. Aqua Security’s decision to ship posture analytics alongside container and workload controls shows how a single policy plane can now trace misconfigurations from build to runtime This evolution is driving growth in the cloud security posture management market,[1]Aqua Security, “Aqua Platform Adds CSPM to CNAPP,” aquasec.comOrganizations deploying converged platforms report materially lower mean-time-to-remediate because alerts arrive already correlated with asset context and exploit pathways. The same console also pushes guardrails back into developer pipelines, which curbs drift before it reaches production resources. Integrations with identity governance modules further reduce hidden attack surfaces by exposing privilege creep inside cloud accounts. Collectively, these changes tighten the feedback loop between DevOps and SecOps and raise the switching costs for point-product providers.

Rise of AI-assisted auto-remediation engines

Artificial-intelligence tooling now reads configuration graphs, ranks findings by business impact, and triggers fixes through Infrastructure-as-Code pull requests. Early adopters note that auto-generated remediation often cuts the backlog of open cloud alerts in half during the first 90 days of use. Deterministic policy engines reduce human error by proposing precise JSON or YAML changes instead of generalized best-practice advice. The approach counters the global cloud-security skills gap and frees senior analysts to focus on threat hunting, For providers, remediation depth becomes a clear differentiator because customers evaluate not just what the platform detects but how quickly it can act without manual approval loops. Vendors that own both the analytics layer and the automation workflow gain further stickiness through proprietary machine-learning models that improve with tenant data volume.

Expansion of zero-trust and shared-responsibility audits

Enterprises rolling out zero-trust frameworks demand continuous verification of every workload, identity, and network flow. cloud security posture management modules now ingest identity-and-access-management telemetry to flag unused high-privilege accounts and suspicious delegation patterns, thereby aligning with zero-trust’s “never trust, always verify” principle[2]Cisco, “Zero Trust Architecture Guide,” cisco.com. At the same time, shared-responsibility boundaries are blurring as managed PaaS and SaaS gain traction. Modern tools, therefore, map provider versus customer obligations and alert owners only to misconfigurations that fall within their remit, reducing false positives. The confluence of zero-trust and sophisticated posture analytics raises executive awareness of configuration risk, which accelerates board-level funding for cloud-security modernization.

Regulatory push for real-time cloud-configuration reporting

Lawmakers worldwide are turning periodic audits into continuous oversight. Asia-Pacific data-sovereignty rules and new European directives both require near-real-time evidence that sensitive workloads stay within permitted regions, forcing organizations to automate snapshot collection and exportable compliance reports. Financial regulators in particular now expect automated drift detection in stress-testing scenarios. Failing to provide live posture evidence risks fines and restricted market access, so even budget-constrained firms treat cloud security posture management spending as a cost of compliance rather than a discretionary line item. Vendors that deliver template packs for multiple jurisdictions gain a competitive edge because multinational clients want to avoid piecemeal tooling for each region.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Alert-fatigue and skills shortage in SecOps teams | -1.8% | Global, acute in developed markets | Short term (≤ 2 years) |

| Tool overlap with CWPP/CIEM creating budget friction | -1.5% | North America and EU primarily | Medium term (2-4 years) |

| Limited API depth for some SaaS/PaaS providers | -1.2% | Global, varying by cloud provider | Long term (≥ 4 years) |

| Data-residency barriers in sovereign-cloud projects | -1.0% | APAC and EU core, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Alert fatigue and skills shortage in SecOps teams

The very success of cloud security posture management in surfacing risk has overwhelmed many security operations centers. Enterprises often receive thousands of posture alerts per day and cannot hire analysts fast enough to triage them. Fortinet field data show that even large teams investigate only a fraction of daily findings, leaving misconfigurations unaddressed and eroding trust in the tooling. Automation alleviates part of the burden, yet significant expertise remains necessary to tune policies and integrate fixes into CI/CD pipelines. As a result, managed-service options grow in popularity, but their cost pressures smaller businesses already coping with tight cybersecurity budgets.

Tool overlap with CWPP and CIEM creating budget friction

CIOs increasingly bundle workload, entitlement, and posture controls into a single procurement to curb license sprawl. When cloud security posture management vendors pitch an additional SKU, finance leaders question incremental value relative to existing CWPP or CIEM spend. Some pure-play suppliers respond with aggressive pricing, while platform vendors argue for higher total cost of ownership savings through consolidation. Buyers consequently elongate evaluation cycles, which slows revenue recognition for all providers and favors market entrants that position cloud security posture management as an embedded feature instead of a separate product line.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Acceleration Signals Market Maturation

Solutions segment retained 66.45% share of the Cloud Security Posture Management market in 2025, confirming that detection and reporting remain the entry point for most buyers. Yet the Services category is expanding at 15.12% CAGR through 2031 as enterprises confront the operational complexity of turning alerts into lasting policy change. Managed-service partners offer continuous tuning, custom rule engineering, and 24×7 triage, activities that many teams lack the internal bandwidth to perform. The surge in service contracts also reflects growing demand for posture assessments prior to mergers or compliance certifications, a niche that consulting firms are quick to monetize. Platform vendors therefore boost service alliances or build in-house advisory teams to prevent revenue leakage.

The widening skills gap further fuels service uptake, particularly among mid-market organizations that cannot afford full-time cloud-security architects. Providers that deliver packaged offerings with outcome-based pricing—rather than hourly billing—gain traction because they map directly to risk-reduction goals. Over the forecast horizon, integration services for AI-driven remediation should see the fastest growth, given that deterministic policy engines require careful governance to avoid unintended configuration changes in production environments.

By Cloud Model: SaaS Security Emerges as Growth Catalyst

Infrastructure as a Service environments held 48.92% share of the Cloud Security Posture Management market in 2025, underscoring the historical dominance of virtual-machine and container workloads. However, SaaS resources will log the highest 15.2% CAGR because business units continue to adopt productivity suites, CRM platforms, and collaboration tools that store sensitive data outside the traditional perimeter. SaaS Security Posture Management modules plug this gap by scanning tenant-level settings, unused API tokens, and excessive sharing links. Enterprises adopting these capabilities note rapid risk reduction when orphaned accounts and third-party integrations are disabled.

Platform as a Service also enters mainstream consideration as serverless and managed database services proliferate. Here, posture management must understand ephemeral functions and context-aware least privilege, tasks poorly addressed by legacy scrapers that assume persistent servers. Vendors that expose consistent policy languages across IaaS, PaaS, and SaaS win executive support by curbing the operational burden of three separate tooling stacks. The shift cements the perception of cloud security posture management as a universal control layer spanning the full spectrum of cloud-delivery models.

By Deployment Mode: Hybrid Cloud Complexity Drives Innovation

Public-cloud workloads made up 44.35% of 2025 deployments, yet hybrid architectures will outpace them with a 15.74% CAGR because risk teams prefer a phased migration path that leaves certain data on-premises for governance reasons. Hybrid estates complicate posture management because tooling must pull telemetry from hyperscaler APIs, private-cloud kernels, and traditional virtualized clusters. Vendors respond with lightweight collectors that normalize findings into a unified graph while respecting data-sovereignty constraints.

The governance challenge intensifies when data-location rules demand that configuration snapshots stay within national borders. Best-in-class platforms solve this by offering regional processing hubs and attribute-based access controls that let administrators set fine-grained visibility boundaries. As enterprises standardize on these multi-environment dashboards, they build confidence to decommission siloed scanners, thereby freeing budgets for analytics upgrades such as attack-path simulation.

By Organization Size: SME Adoption Accelerates Despite Budget Constraints

Large Enterprises exerted 77.10% market control in 2025, yet Small and Medium Enterprises are forecast to be the fastest-growing cohort at 15.08% CAGR as turnkey deployments lower adoption barriers. Vendor roadmaps now emphasize guided onboarding, pre-built compliance templates, and usage-based billing that aligns cost with scale. These attributes appeal to smaller firms whose security spending rarely matches that of Fortune 500 peers.

The risk calculus has also shifted. Ransomware actors increasingly target midsize companies that have fewer compensating controls, forcing boards to fund posture-management tools once deemed “enterprise-only.” Providers offering tiered feature sets capture this demand by letting firms start with core misconfiguration scanning and later add identity or workload modules. Community editions and free-trial periods further widen the funnel, though suppliers must balance generosity with sustainable support models.

By Industry Vertical: Healthcare Digitization Drives Vertical Expansion

Banking, Financial Services, and Insurance clients contributed 29.12% of 2025 revenue, a testament to heavy compliance mandates and high data-value density. These institutions require evidence of continuous control monitoring as part of regulatory examinations, making cloud security posture management a non-negotiable line item. Vendors compete on how quickly their platforms map findings to specific clauses in standards such as PCI DSS or FFIEC.

Healthcare, meanwhile, will record a 15.07% CAGR through 2031, fueled by accelerated electronic-medical-record migration and telehealth adoption. Clinical workloads carry strict data-retention and audit-logging obligations, so posture tools must integrate with hospital information systems and medical-device networks. Suppliers that certify HIPAA alignment and maintain region-specific patient-data isolation options gain an edge. Over time, predictive analytics based on anonymized clinical misconfiguration trends can further reduce exposure by flagging high-risk settings before deployment.

Geography Analysis

North America retained 35.02% revenue share in 2025 owing to mature cloud adoption, a dense concentration of security vendors, and stringent frameworks such as FedRAMP that push agencies and contractors to maintain documented configuration baselines. Continued federal investment in zero-trust programs sustains platform spending, while a healthy venture ecosystem funds disruptive start-ups that introduce AI-native remediation features. Canadian enterprises increasingly align with U.S. security standards, enabling cross-border managed-service deals that lift regional revenue.

Asia-Pacific will deliver the fastest regional CAGR at 15.55% as governments legislate data-localization practices and provide tax incentives for local cloud datacenter builds. Large-scale national digitization projects in Japan, India, and Australia embed cloud-security posture reporting in procurement guidelines, effectively mandating tool deployment in state-backed workloads. Meanwhile, the Malaysian Cyber Security Act of 2024 requires continuous monitoring for critical-sector operators, accelerating vendor entry into Southeast Asian markets and creating channel opportunities for local systems integrators.

Europe exhibits a complex compliance landscape anchored by GDPR and newly adopted artificial-intelligence regulations that demand transparency in algorithmic decision-making. Enterprises thus seek posture dashboards that can produce multi-jurisdiction audit trails on demand. Germany and France spearhead sovereign-cloud initiatives that call for in-country data processing, prompting providers to launch EU-only hosting zones. In parallel, the United Kingdom’s post-Brexit regulatory divergence drives demand for dual compliance mappings, which favors platforms with flexible policy engines. Latin America, the Middle East, and Africa remain nascent but attractive expansion territories as hyperscaler region launches bring modern APIs within reach of local businesses.

Competitive Landscape

The Cloud Security Posture Management market shows moderate fragmentation: no single vendor holds decisive control, yet the top five groups together account for a substantial slice of global revenue. Strategic consolidation illustrates the premium placed on comprehensive cloud-security stacks. Google’s USD 32 billion acquisition of Wiz gives the hyperscaler agentless graph technology that spans AWS, Azure, and Google Cloud workloads. Palo Alto Networks, for its part, folded posture analytics into Cortex Cloud, lowering analyst context-gathering time and reinforcing its platform narrative[4]Palo Alto Networks, “Q2 2025 Financial Results,” paloaltonetworks.com.

AI-centric start-ups push incumbents to innovate. Gomboc AI secured USD 13 million to commercialize deterministic remediation engines that create pull requests directly in infrastructure-as-code repositories. Such capabilities resonate with developer-led organizations that prefer self-healing infrastructure over after-the-fact ticket queues. Established vendors respond by embedding similar functionality or acquiring niche specialists, blurring the line between posture monitoring and workload protection.

Go-to-market strategies now hinge on ecosystem alliances. Providers with deep native-cloud integrations anchor marketplaces that bundle entitlement scanning, workload runtime protection, and compliance automation. Channel partners gain margin by layering managed services on top of these suites. Pure-play CSPM firms risk marginalization unless they secure lighthouse vertical wins or pivot toward embedded OEM models that feed their analytics into broader security platforms.

Cloud Security Posture Management Industry Leaders

Palo Alto Networks, Inc.

Check Point Software Technologies Ltd.

Trend Micro Incorporated

Microsoft Corporation

IBM Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Upwind acquired Nyx Security to deepen runtime threat detection for cloud-native workloads.

- April 2025: Qualys unveiled TotalCloud 2.0 with TruRisk Insights, combining workload and posture data for unified risk scoring.

- April 2025: Redington Limited partnered with Banyan Cloud to deliver agentless CNAPP services to Indian enterprises across regulated verticals.

- March 2025: Google completed its USD 32 billion Wiz acquisition, the largest cybersecurity deal to date.

- February 2025: Palo Alto Networks introduced Cortex Cloud, unifying detection, posture, and application security in a single console.

- February 2025: Blackpoint Cyber released CompassOne, bundling cloud-posture controls with broader security-response functions.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the cloud security posture management (CSPM) market as all software and managed-service offerings that continuously scan public, private, and hybrid cloud resources to detect, prioritize, and remediate misconfigurations, policy violations, and compliance gaps across IaaS, PaaS, and SaaS estates.

Scope exclusion: on-premises firewall, endpoint, and SIEM products remain outside this boundary.

Segmentation Overview

- By Component

- Solutions

- Services

- By Cloud Model

- Infrastructure as a Service (IaaS)

- Platform as a Service (PaaS)

- Software as a Service (SaaS)

- By Deployment Mode

- Public Cloud

- Private Cloud

- Hybrid Cloud

- By Organization Size

- Large Enterprises

- Small and Medium Enterprises (SMEs)

- By Industry Vertical

- Banking Finance Services and Insurances (BFSI)

- Healthcare

- Retail and E-commerce

- IT and Telecommunication

- Government and Public Sector

- Education

- Manufacturing

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts held structured interviews with CISOs, DevSecOps leads, regional cloud consultants, and regulatory auditors across North America, Europe, and Asia-Pacific. These conversations clarified typical license models, adoption triggers, and emerging price benchmarks, enabling us to pressure-test secondary findings and refine key assumptions.

Desk Research

We began by mapping the active workload pool using tier-one public sources such as the Cloud Security Alliance breach database, NIST NVD vulnerability feeds, US-CERT incident alerts, and European Data Protection Board enforcement logs, which are then balanced with international trade statistics on cloud spending and infrastructure roll-outs. Company 10-Ks, investor decks, and major cloud provider transparency reports supply unit economics, while Dow Jones Factiva and D&B Hoovers help us surface revenue signals and M&A clues for leading vendors. This list is illustrative, not exhaustive, and many additional sources informed the baseline.

Market-Sizing & Forecasting

A blended top-down approach starts with global public cloud spend, misconfiguration incidence rates, and average remediation tool penetration, which are then transformed into addressable value pools. Target totals are cross-checked through selective bottom-up roll-ups of leading supplier revenues and sampled average selling price times deployment volumes. Inputs include: annual IaaS spend growth, percentage of reported cloud breaches, new compliance mandates (e.g. GDPR fines), AI-driven auto-remediation uptake, and regional cloud workload distribution. A multivariate regression model, supported by expert consensus, projects each driver and feeds a five-year exponential smoothing forecast. Gaps in supplier disclosures are bridged using industry standard ratios validated during primary calls.

Data Validation & Update Cycle

Outputs undergo variance checks against independent market indicators; anomalies trigger re-verification with sources before senior review and sign-off. Reports refresh each year, with interim updates released when material events (for example, a major breach or regulatory change) shift assumptions.

Why Our Cloud Security Posture Management Baseline Earns Decision Maker Trust

Published estimates differ because firms choose varying scopes, base years, and conversion methods. We anchor on a pure-play CSPM definition, current 2025 currency, and documented adoption levers, giving users a consistent yardstick.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 5.25 B (2025) | Mordor Intelligence | - |

| USD 5.75 B (2024) | Global Consultancy A | Broader cloud security scope blends DSPM and CASB elements |

| USD 2.66 B (2024) | Trade Journal B | Conservative uptake assumptions and exclusion of managed services |

These contrasts show that when scope drift or outdated baselines creep in, valuations swing widely. By grounding every figure in transparent variables and a repeatable model, Mordor Intelligence delivers a balanced, defensible baseline clients can rely on.

Key Questions Answered in the Report

What is the market size of the Cloud Security Posture Management market expected to reach in 2026?

The Cloud Security Posture Management Market size is projected to reach USD 6.04 billion in 2026.

Which segment is expected to expand fastest by 2031?

Services are projected to grow at a 15.12% CAGR as organizations seek managed expertise to operationalize posture findings and close the cybersecurity skills gap.

How big is the Cloud Security Posture Management market size for SaaS deployments?

SaaS environments account for a growing share of the Cloud Security Posture Management market size and are forecast to post a 15.2% CAGR, the highest among cloud-delivery models.

Which region presents the strongest growth opportunity?

Asia-Pacific leads with a 15.55% CAGR through 2031 due to new data-sovereignty regulations and large-scale public-cloud initiatives backed by government programs.

How are vendors addressing alert fatigue within security operations centers?

Leading platforms now embed AI algorithms that prioritize alerts by business impact and, in many cases, execute policy-driven auto-remediation, cutting manual triage workload by up to 50%.

Why is healthcare becoming a pivotal vertical for CSPM vendors?

Accelerated electronic-health-record migration and strict patient-data protection rules make continuous posture monitoring essential, pushing healthcare workloads to record a 15.07% CAGR in tool adoption.

Page last updated on: