Cloud Security Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

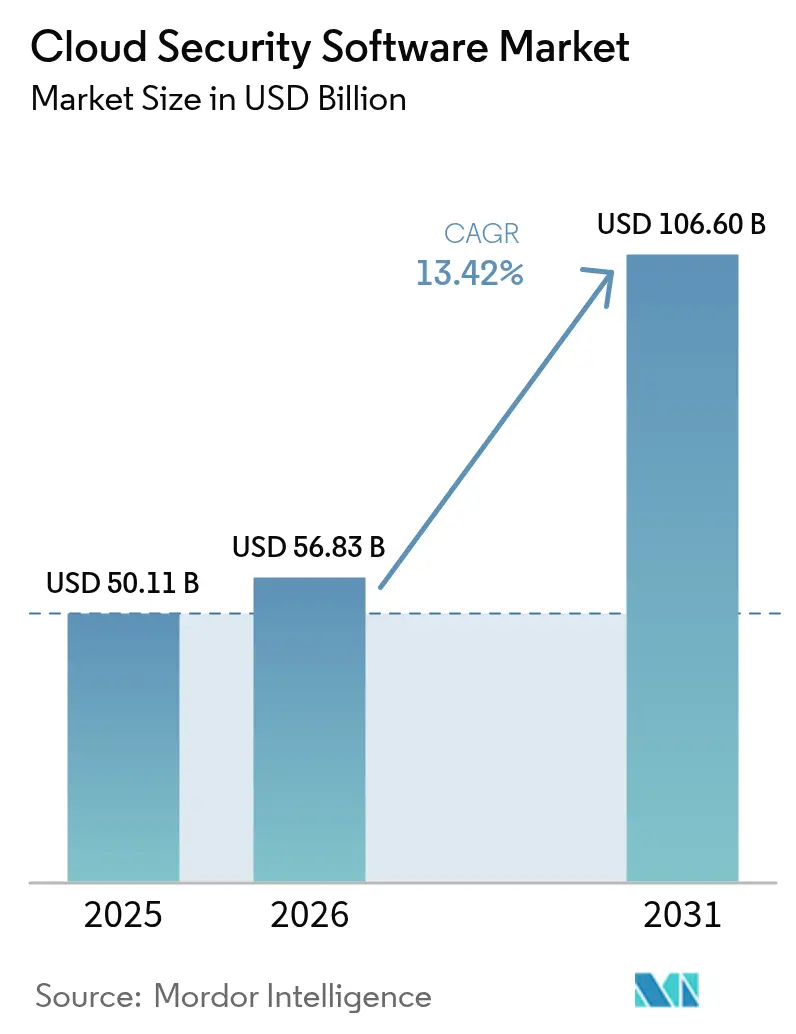

| Market Size (2026) | USD 56.83 Billion |

| Market Size (2031) | USD 106.6 Billion |

| Growth Rate (2026 - 2031) | 13.42% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cloud Security Software Market Analysis by Mordor Intelligence

The Cloud Security Software Market size was valued at USD 50.11 billion in 2025 and estimated to grow from USD 56.83 billion in 2026 to reach USD 106.6 billion by 2031, at a CAGR of 13.42% during the forecast period (2026-2031).

This growth trajectory confirms a robust cloud security software market size that is shaped by regulated industries racing to modernize digital infrastructure, the embrace of zero-trust frameworks, and the emergence of generative-AI-driven threats. Heightened compliance obligations, sovereign-cloud policies, and capital spending by hyperscalers have amplified demand for unified security orchestration across multi-cloud deployments. As enterprises shift critical workloads to the public cloud, they prioritize identity management, runtime protection, and automated compliance reporting to streamline risk management and sustain business velocity. Vendor competition now centers on platform consolidation and native AI capabilities that promise faster detection, lower false-positive rates, and seamless integration across diverse cloud environments.

Key Report Takeaways

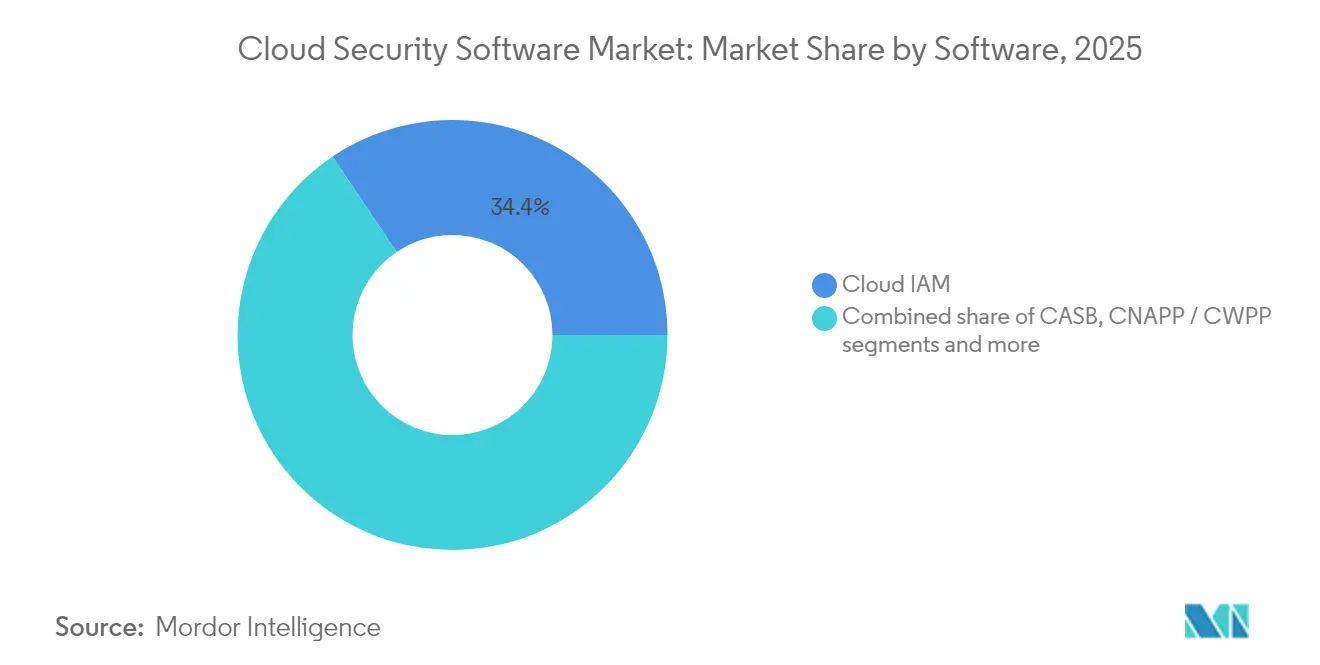

- By software product, Cloud Identity and Access Management led with 34.42% of the cloud security software market share in 2025, whereas Cloud-Native Application Protection Platforms are forecast to expand at a 14.12% CAGR through 2031.

- By deployment mode, public cloud retained 64.85% revenue share in 2025, while hybrid and multi-cloud configurations record the highest projected CAGR at 14.76% to 2031.

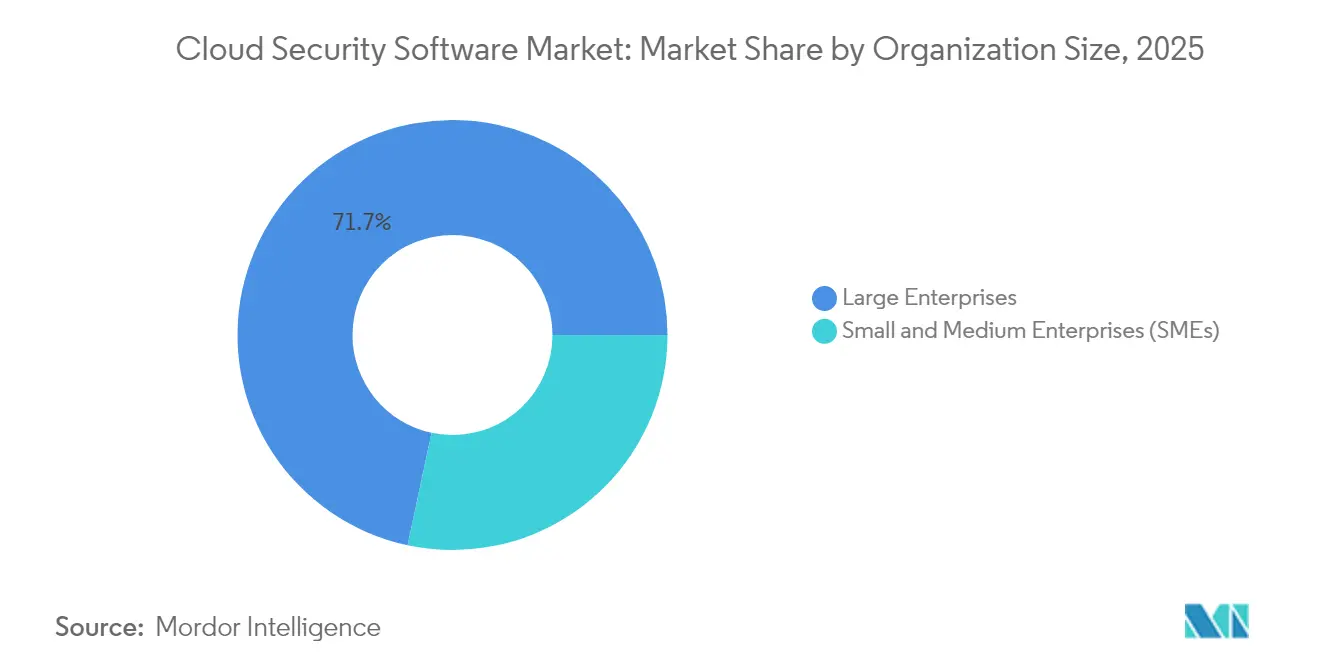

- By organization size, large enterprises held 71.65% of the cloud security software market in 2025; small and medium enterprises post the fastest 15.03% CAGR, signaling broader democratization of advanced security.

- By end-user industry, Banking, Financial Services, and Insurance captured 35.10% of the cloud security software market size in 2025, whereas Information Technology and Telecommunications posts a 13.62% CAGR through 2031.

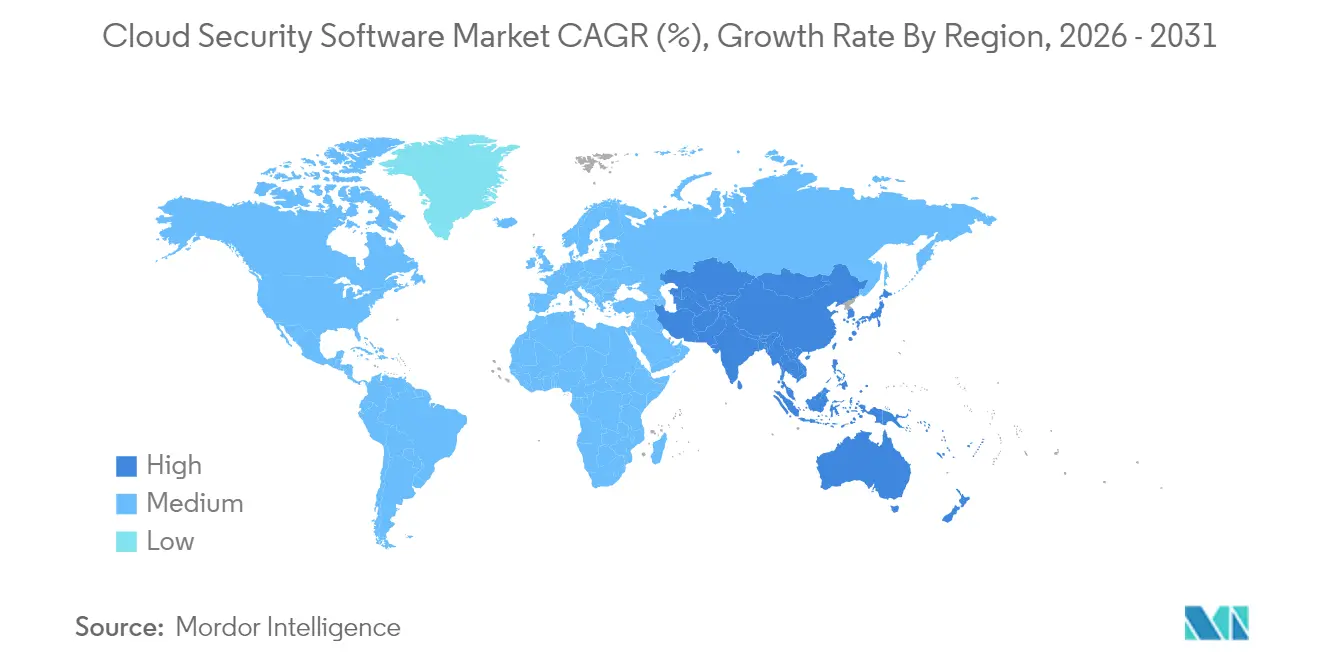

- By geography, North America maintained 40.95% revenue share in 2025, yet Asia-Pacific is the fastest-growing region at 14.32% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cloud Security Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fast-growing public-cloud adoption among regulated industries | +2.8% | Global, especially North America and EU | Medium term (2–4 years) |

| Surge in multi-cloud and hybrid-cloud complexity | +2.1% | Global, high in APAC and North America | Short term (≤ 2 years) |

| Zero-trust architecture mandates | +1.9% | North America and EU, expanding in APAC | Medium term (2–4 years) |

| Generative-AI-driven threat vectors | +1.7% | Global, earliest in North America | Short term (≤ 2 years) |

| Cyber-insurance premium incentives | +1.4% | North America and EU | Long term (≥ 4 years) |

| Sovereign-cloud initiatives | +1.2% | EU and APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fast-growing Public-cloud Adoption Among Regulated Industries

Regulated enterprises are re-tooling legacy architectures as supervisory bodies update cloud guidance. The Federal Financial Institutions Examination Council now stresses real-time third-party risk monitoring, prompting banks and insurers to adopt automated controls that verify compliance evidence continuously. Healthcare providers likewise align modernization plans with security certifications that deliver competitive benefit rather than mere regulatory box-ticking. Federal Risk and Authorization Management Program reforms further legitimize cloud migrations, cascading adoption expectations across contractors and suppliers. Vendors respond with pre-packaged compliance templates that shorten onboarding times and translate policy into programmatic guardrails across multi-cloud estates[1]Federal Financial Institutions Examination Council, “Cybersecurity Resource Guide,” ffiec.gov.

Surge in Multi-cloud and Hybrid-cloud Complexity

Enterprises typically run workloads on 3.2 cloud providers, multiplying policy silos and integration debt. Disparate APIs and variable security models fuel demand for centralized orchestration able to normalize controls independent of underlying infrastructure. Cloud-native application protection platforms thus gain favor by detecting misconfigurations and runtime anomalies across containers and serverless functions. Organizations originally pursued multi-cloud for diversification but now rely on orchestration to maintain operational viability as cost, performance, and jurisdictional requirements diverge.

Zero-trust Architecture Mandates

Zero-trust shifts perimeter-based defenses toward continuous verification of user, device, and application context. The National Institute of Standards and Technology issued draft API protection guidance that underscores risk-based policies across the full software lifecycle, accelerating procurement of identity-centric tooling that supports granular access decisions[2]National Institute of Standards and Technology, “Special Publication 800-228: API Security Guidance,” nist.gov. Adoption extends beyond federal agencies to commercial entities dealing with distributed workforces and hybrid data flows. Implementation success hinges on scalable identity and access management platforms capable of harmonizing policies without degrading user experience.

Generative-AI-driven Threat Vectors

Generative AI equips bad actors to produce polymorphic malware and persuasive phishing at unprecedented speed, forcing defenders to automate threat analysis at similar velocity. Organizations pilot AI-powered detection engines that sift cloud telemetry for anomalous behavior in real time. Security teams also craft AI governance policies to prevent model drift and data leakage, balancing automation gains against explainability and compliance imperatives.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Integration debt with legacy security stacks | –1.8% | Global, notably mature markets | Medium term (2–4 years) |

| Cloud-native skills shortage | –1.3% | Global, acute in APAC | Short term (≤ 2 years) |

| Compliance conflicts across jurisdictions | –0.9% | Global, cross-border firms | Long term (≥ 4 years) |

| Persistent shadow-IT and BYOD behavior | –0.7% | Global, industry-dependent | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Integration Debt with Legacy Security Stacks

Security leaders grapple with duplicated tooling and inconsistent policies as cloud controls overlay on-premises investments. Parallel environments obscure attack paths and inflate operating costs, especially when organizations retrofit zero-trust models onto hub-and-spoke networks. Without unified telemetry, threat intelligence remains siloed, and remediation cycles extend, undermining return on security spend.

Cloud-native Skills Shortage

Japan illustrates the global talent gap: 70% of companies cite deficits in cloud technology expertise versus 47% worldwide, even as 94% earmark upskilling as a top priority[3]Linux Foundation, “State of Cloud Native Security Skills Report 2024,” linuxfoundation.org. Scarcity drives project delays, misconfigurations, and rising service costs. Small and medium enterprises feel the pinch most acutely, reinforcing managed services demand to bridge expertise shortfalls.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Software: Identity Management Anchors Growth

Cloud Identity and Access Management accounted for a 34.42% cloud security software market share in 2025, reflecting its cornerstone role in zero-trust rollouts. The segment’s entrenched status underpins the broader cloud security software market as organizations prioritize least-privilege policies to mitigate lateral movement risks. Simultaneously, Cloud-Native Application Protection Platforms and Cloud Workload Protection Platforms achieve a 14.12% CAGR through 2031, mirroring the proliferation of containerized workloads that require runtime safeguards. Their ascent joins Cloud Access Security Brokers and vulnerability scanners that integrate within DevSecOps pipelines, offering continuous assessment across development and production.

Demand for unified logging drives Security Information and Event Management modernization, with platforms leveraging machine learning to parse cloud-scale telemetry and accelerate mean-time-to-detect. Vendors further experiment with quantum-resistant algorithms, as demonstrated by SEALSQ’s Crystal Kyber and Crystal Dilithium showcase, signaling the long-term evolution of encryption boundaries. These innovations collectively reshape category borders, encouraging platform vendors to fold adjacent capabilities into consolidated suites for simplified procurement and operations.

By Deployment Mode: Hybrid Complexity Drives Innovation

Public cloud retained 64.85% share of the cloud security software market size in 2025, buoyed by hyperscaler investments that reached USD 215 billion in 2025. Amazon alone allocated more than USD 75 billion, augmenting native security services and geographic redundancy. Despite public cloud scale advantages, hybrid and multi-cloud environments post the fastest 14.76% CAGR as enterprises seek workload portability, data residency assurance, and cost optimization.

Hybrid complexity magnifies the need for policy abstraction, prompting security providers to offer central dashboards that push uniform rules across Kubernetes clusters, SaaS applications, and on-premises assets. Private cloud adoption persists among industries with sensitive intellectual property or latency-critical workloads, though many treat private environments as transitional waypoints toward broader public adoption once compliance hurdles ease.

By Organization Size: SME Acceleration Signals Democratization

Large enterprises controlled 71.65% of the cloud security software market in 2025, shielded by skilled personnel and substantial budgets capable of supporting layered defenses. They invest in orchestration platforms that fuse vulnerability management, runtime protection, and automated compliance into a single pane of glass. Nevertheless, the 15.03% CAGR among small and medium enterprises demonstrates that automation and managed services lower barriers to entry. Low-touch deployment models and subscription pricing allow resource-constrained firms to inherit best-practice configurations without building extensive in-house teams.

Service providers now offer tiered bundles that map essential controls to specific regulatory obligations, delivering predictable cost structures. The democratization trend widens the addressable base, encouraging vendors to streamline user interfaces, integrate AI-based playbooks for incident response, and embed compliance reporting templates that satisfy auditors with minimal manual effort.

By End-User Industry: Financial Services Lead Digital Transformation

Banking, Financial Services, and Insurance maintained a 35.10% share of the cloud security software market size in 2025, captivated by regulatory oversight and high-value digital assets. The Federal Financial Institutions Examination Council’s guidance on third-party cloud risk amplifies spending on identity governance, encryption key management, and continuous control monitoring. Information Technology and Telecommunications industries record a 13.62% CAGR to 2031, reflective of their role as cloud infrastructure stewards and early adopters of AI-infused security.

Healthcare organizations invest in specialized compliance automation to reconcile electronic health record protection with operational efficiency. Retail and Consumer Goods prioritize fraud prevention and data integrity to sustain omnichannel commerce, while manufacturing entities secure industrial IoT deployments linking operational technology to enterprise clouds. This convergence of IT and OT estates accelerates demand for industry-tuned security blueprints capable of addressing unique production uptime and safety requirements.

Geography Analysis

North America retained a 40.95% revenue share in 2025, signifying the largest regional slice of the cloud security software market. Federal Risk and Authorization Management Program modernization boosts confidence in cloud controls across civilian agencies, contractors, and heavily regulated industries. Concurrently, the U.S. Department of Justice Data Security Program introduces fresh compliance layers for telecommunications firms handling foreign data traffic, generating opportunities for automated policy-mapping tools that reconcile overlapping rule sets.

Asia-Pacific is the fastest-growing territory with a 14.32% CAGR through 2031, underpinned by sovereign-cloud directives, 5G rollout, and broad-scale digitization. Yet acute talent shortages threaten execution timelines. Japan’s skills deficit underscores the training imperative, spurring partnerships between universities, cloud providers, and security vendors to expand certification access. China advances domestically sourced security stacks to meet sovereignty mandates, whereas India emphasizes low-cost, scalable solutions to service a diverse enterprise base. Australia, New Zealand, and South Korea leverage advanced network infrastructure to adopt real-time threat detection platforms that ensure low-latency protection for financial trading and smart-factory environments.

Europe navigates the delicate balance between innovation and sovereignty. General Data Protection Regulation and the evolving Network and Information Security Directive shape procurement criteria that favor providers offering data-localization options and transparent audit trails. Germany leads adoption in manufacturing, while France invests in nationally hosted cloud zones to underpin critical infrastructure projects. Post-Brexit, the United Kingdom crafts its own data security stance yet aligns closely enough to facilitate cross-border transfers. Regional harmonization efforts simplify vendor entry, although divergent national timelines for directive transposition continue to complicate uniform rollout strategies.

Regulatory Landscape

Cloud security requirements are shifting toward continuous assurance and machine-verifiable controls, which is changing how cloud security software is procured and audited across regions. In the United States, March 2025 Federal Risk and Authorization Management Program (FedRAMP) modernization and the 2026 FedRAMP consolidated approach to cloud-native architecture and key security indicators reinforce persistent monitoring expectations, while June 2026 NSPM-12 tightened national-security hosting requirements by pushing cloud providers supporting National Security Systems to deliver agency configuration baselines within a defined timeline. NIST also refreshed security guidance that maps to product requirements, including the March 2026 update to NIST SP 800-228 for API protection in cloud-native systems and the May 2026 NIST SP 800-70r5 update to the National Checklist Program that supports standardized, automated secure configuration baselines.

In Europe, sovereignty and harmonized assurance remain central, with Germanys Federal Office for Information Security (BSI) publishing C5:2026 to replace earlier criteria and align more explicitly with ISO/IEC 27001:2022 and requirements referenced from NIS2 and EU cloud certification directions. These moves push vendors and buyers toward auditable policy-as-code, API security, and configuration compliance capabilities that work across public, private, and hybrid/multi-cloud environments. They also increase the burden on cross-border organizations to reconcile overlapping frameworks and local assurance catalogs.

Value Chain Analysis

The cloud security software value chain begins with foundational technology suppliers (cloud platforms, confidential-computing and encryption primitives, identity directories, telemetry, vulnerability data, and threat intelligence). Software vendors then package capabilities such as Cloud IAM, CASB, CNAPP/CWPP, CSPM, data security posture management, web and email security, and SIEM/log management into SaaS or consumption-based offerings. Distribution is handled through cloud marketplaces and direct enterprise sales, while systems integrators and managed security service providers operationalize deployments through integration, policy tuning, monitoring, and incident response, especially as hybrid and multi-cloud estates add complexity.

A visible shift within the chain is hyperscaler-led consolidation of operations and security workflows across clouds. For example, AWS added AI workload protection and multicloud support for Microsoft Azure within AWS Security Hub (July 2026), reflecting how cloud providers increasingly act as aggregators of third-party signals and controls while moving more security operations into native consoles. Downstream, end users in regulated sectors prioritize continuous compliance evidence and multi-cloud visibility, and buyers increasingly scrutinize supplier risk, software supply chain exposure, and integration debt across legacy and cloud-native stacks.

Competitive Landscape

The cloud security software market demonstrates moderate consolidation, propelled by platform vendors acquiring niche innovators to assemble comprehensive suites. Palo Alto Networks posted USD 2.29 billion in quarterly revenue and revealed plans to absorb Protect.ai, signaling aggressive expansion toward AI-driven protection. CrowdStrike’s outage in 2024, which triggered USD 5.4 billion in downstream losses, amplified buyer scrutiny of release-management practices and uptime assurances, nudging vendors to adopt gradual deployment pipelines and real-time rollback mechanisms.

Hyperscalers embed security features inside infrastructure services, compelling specialized vendors to differentiate through deep analytics, policy portability, and verticalized compliance tooling. Start-ups market post-quantum encryption libraries, evidenced by SEALSQ’s IoT-oriented Crystal Kyber showcase, to prepare for quantum threats that could render present-day cryptography obsolete. Investors reward firms that translate AI research into practical detection gains without inflating operational costs. Consequently, product roadmaps prioritize contextual analytics, low-code policy creation, and seamless interoperability across multi-cloud APIs to minimize customer integration debt.

Vendor alliances proliferate as integrated solutions ease procurement fatigue. Service providers curate marketplaces that bundle identity, workload protection, and governance reporting, offering customers subscription flexibility with predictable budgeting. Competitive intensity is expected to persist as players vie for share in high-growth niches such as API security, data security posture management, and continuous compliance automation.

Cloud Security Software Industry Leaders

Check Point Software Technologies

IBM Corporation

Microsoft

Cisco Systems

Amazon Web Services (Security services)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Enterprise AI adoption and agentic workflows are opening new spend areas inside cloud security software, particularly around non-human identity, model and data governance, and machine-speed vulnerability remediation. June 2026 launches and announcements show continuing vendor investment: AWS introduced AWS Continuum for automated discovery, validation, and remediation of vulnerabilities, while CrowdStrike announced Continuous Identity for AI Agents to apply real-time, risk-aware authorization to non-human identities. F5 also launched the F5 AI Security Platform and acquired SurePath AI (June 2026), signaling a push toward dedicated controls for AI application traffic, AI governance, and AI-facing attack surface management.

Regulatory and assurance catalogs are also creating whitespace for automated compliance and high-assurance controls in cloud environments. Germanys BSI issued C5:2026, updating cloud compliance criteria in ways that raise expectations for auditable controls and newer security requirements, and US frameworks such as FedRAMP modernization and NIST updates including SP 800-228 reinforce API security and automated configuration baselines as procurement checklists. Together, these developments support platforms that unify identity, CNAPP/CWPP, SIEM/log analytics, and compliance reporting across multi-cloud deployments, and they also support managed-service bundles aimed at skills shortages and integration complexity for SMEs and regulated enterprises.

Recent Industry Developments

- July 2026: Check Point Software made its Cloud Firewall offering available on the AWS European Sovereign Cloud, targeting customers with strict EU data residency and operational autonomy requirements. The move strengthens sovereign-cloud aligned security deployments where buyers require demonstrable control segregation, auditability, and region-bound processing.

- June 2026: IBM, Red Hat, and Palo Alto Networks expanded Project Lightwell to help organizations respond to software vulnerabilities by combining remediation workflows with network-level compensating controls such as virtual patching. The collaboration highlights rising demand for automated vulnerability validation and response across hybrid environments where patch cycles and exposure windows drive cloud risk.

- June 2025: Palo Alto Networks agreed to acquire Protect.ai to expand its AI security portfolio and accelerate protection for AI models and pipelines. The deal reinforces the markets platform-consolidation trend, with large vendors absorbing specialized capabilities to deliver integrated controls across cloud, application, and AI layers.

Research Methodology Framework and Report Scope

Segmentation Overview

- By Software

- Cloud IAM

- CASB

- CNAPP / CWPP

- Vulnerability and Risk Management

- Web, Email and DNS Security

- SIEM and Log Management

- By Deployment Mode

- Public Cloud

- Private Cloud

- Hybrid / Multi-Cloud

- By Organization Size

- Large Enterprises

- Small and Medium Enterprises (SMEs)

- By End-User Industry

- BFSI

- IT and Telecom

- Healthcare and Life-Sciences

- Retail and Consumer Goods

- Manufacturing

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Key Questions Answered in the Report

What is the current value of the cloud security software market?

The cloud security software market generates USD 56.83 billion in 2026 and is on track for USD 106.6 billion by 2031 at a 13.42% CAGR.

Which software category holds the largest share?

Cloud Identity and Access Management leads with 34.42% of the cloud security software market share in 2025.

Why is Asia-Pacific the fastest-growing region?

Digital transformation programs, sovereign-cloud mandates, and 5G rollouts propel a 14.32% CAGR, although talent shortages temper momentum.

How are zero-trust mandates influencing demand?

Zero-trust guidelines from NIST emphasize continuous verification, driving investment in identity-centric tools and API protection platforms.

What impact will post-quantum cryptography have on vendors?

Demonstrations such as SEALSQ’s Crystal Kyber highlight future requirements, encouraging providers to embed quantum-resistant algorithms into product roadmaps to safeguard long-term data confidentiality.

How are SMEs adopting advanced cloud security?

Automation, managed services, and simplified interfaces allow SMEs to implement enterprise-grade defenses, fueling a 15.03% CAGR among small and medium enterprises within the cloud security software industry.

Page last updated on: