Middle East Cloud Applications Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

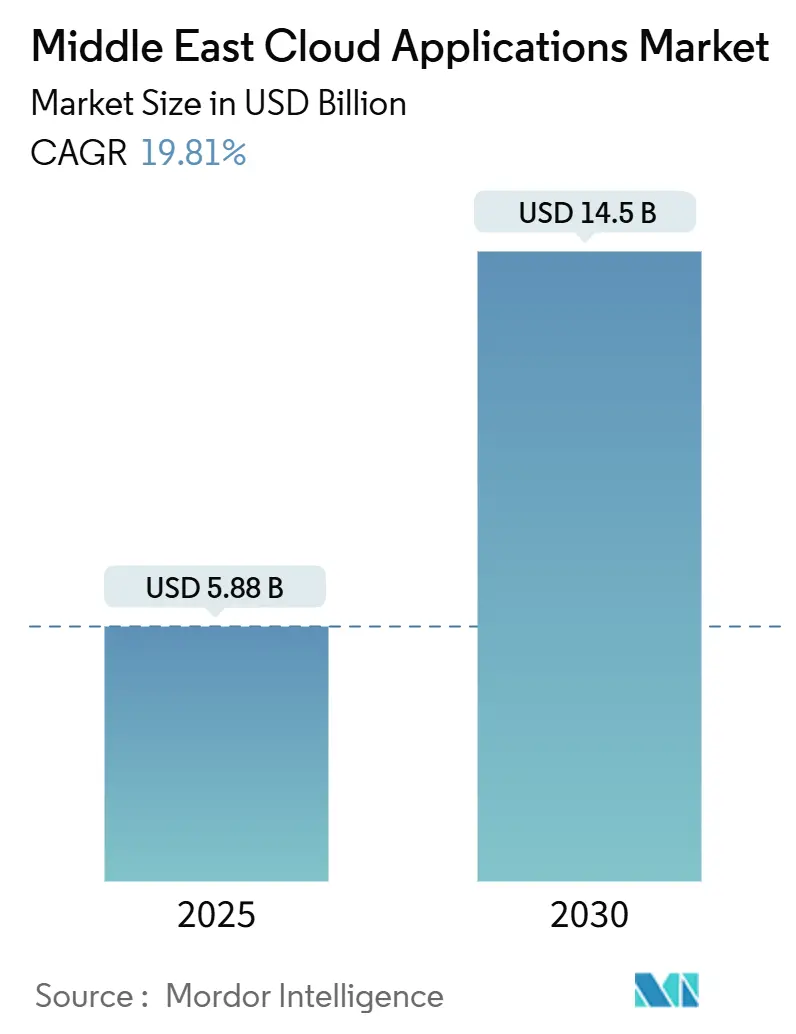

| Market Size (2025) | USD 5.88 Billion |

| Market Size (2030) | USD 14.5 Billion |

| Growth Rate (2025 - 2030) | 19.81% CAGR |

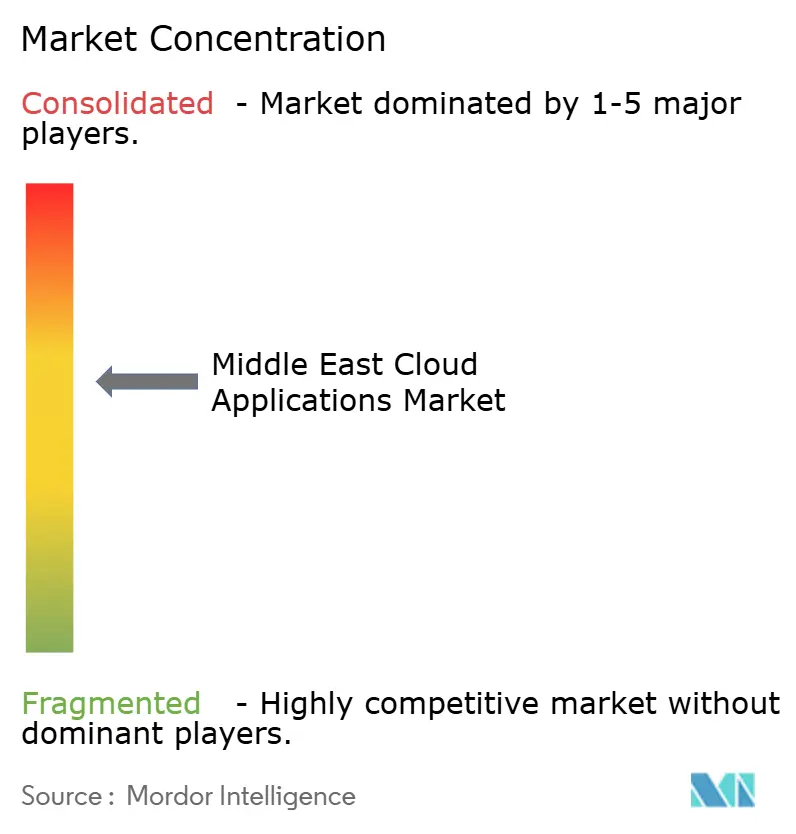

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East Cloud Applications Market Analysis by Mordor Intelligence

The Middle East cloud applications market size is projected to reach USD 5.88 billion in 2025 and is expected to expand to USD 14.50 billion by 2030, registering a 19.81% CAGR. Robust growth reflects sovereign digital economy agendas, accelerating hybrid work adoption, and deepening venture capital support for Arabic-native software start-ups. Hyperscale data-center localization, cloud-friendly regulatory reforms, and rising demand for AI-driven Arabic interfaces shape vendor strategies and unlock new addressable demand. Competitive intensity remains moderate as global providers secure regional alliances while local specialists leverage compliance expertise and cultural proximity to win share. Macro risks persist, with data sovereignty mandates, energy-related operating costs, and talent shortages complicating enterprise migration roadmaps. However, overall expansion momentum keeps the Middle East cloud applications market firmly on a double-digit trajectory.

Key Report Takeaways

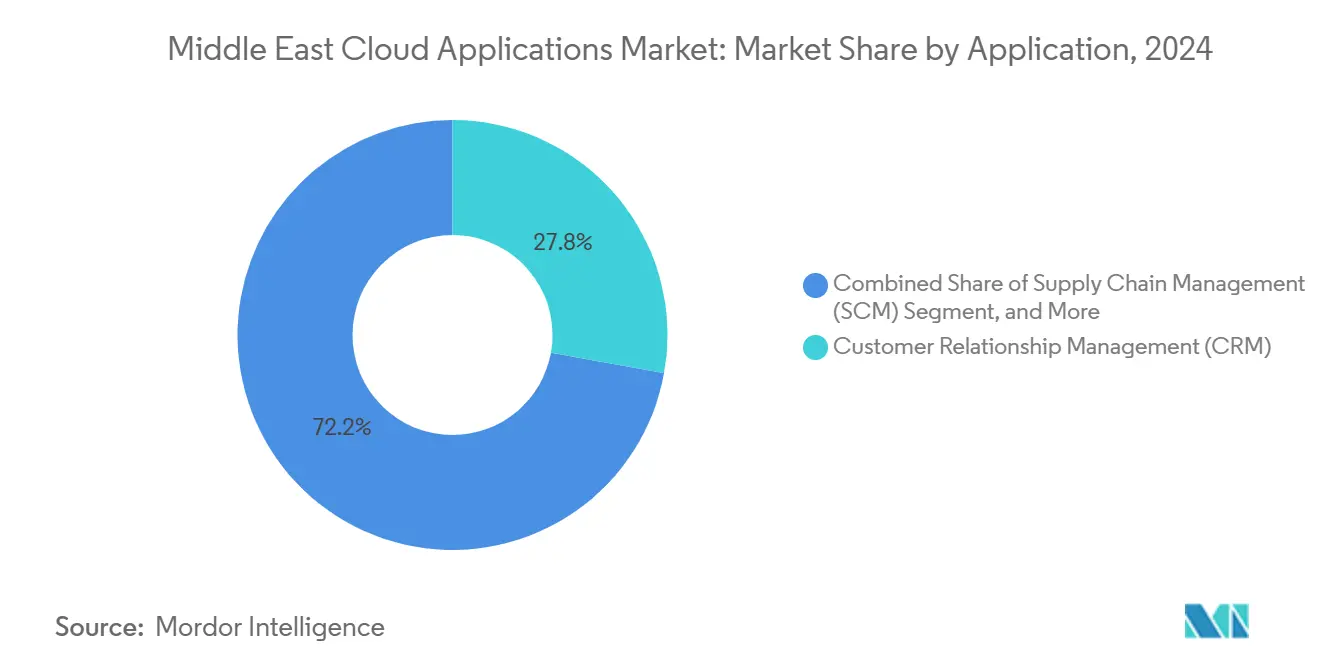

- By application, customer relationship management led with 27.83% of the Middle East cloud applications market share in 2024; enterprise resource planning is projected to rise at a 19.92% CAGR through 2030.

- By deployment model, the public-cloud segment held 71.34% of the Middle East cloud applications market size in 2024, while hybrid-cloud configurations are expected to advance at a 20.69% CAGR to 2030.

- By organization size, large enterprises accounted for 62.76% of the Middle East cloud applications market share in 2024, whereas small and medium enterprises recorded the highest 21.34% CAGR through 2030.

- By end-user industry, banking, financial services and insurance (BFSI) captured 22.43% of the Middle East cloud applications market size in 2024; retail and e-commerce climb at a 19.93% CAGR to 2030.

- By country, Saudi Arabia commanded 37.61% of the Middle East cloud applications market share in 2024, yet Qatar posts the fastest 20.11% CAGR between 2025-2030.

Middle East Cloud Applications Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government-led digital-transformation agendas | +4.2% | Saudi Arabia, UAE, Qatar with spillover to Kuwait and Bahrain | Medium term (2-4 years) |

| Accelerated SaaS adoption from remote and hybrid work | +3.1% | UAE, Saudi Arabia business hubs | Short term (≤ 2 years) |

| Rising cloud-friendly regulatory frameworks | +2.8% | GCC countries, early adoption in UAE and Saudi Arabia | Long term (≥ 4 years) |

| Surge of VC funding into regional SaaS start-ups | +2.0% | UAE and Saudi Arabia venture ecosystems; Egypt and Jordan | Medium term (2-4 years) |

| Localization of hyperscale data centers and low-latency Arabic UIs | +1.9% | Saudi Arabia, UAE primary; secondary across Arabic-speaking markets | Long term (≥ 4 years) |

| Demand for AI-driven Arabic modules in CRM and ERP suites | +1.7% | Arabic-speaking markets, premium adoption in GCC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government-led Digital-transformation Agendas

Vision-steered public spending accelerates cloud procurement. Saudi Arabia earmarked USD 20 billion for digital infrastructure under Vision 2030, mandating listed firms to file digital-transformation blueprints by 2025. The UAE pursues 100% digital public-service delivery by 2025, while Abu Dhabi’s AI Strategy 2031 prioritizes Arabic-language processing. These policies amplify enterprise demand for secure, Arabic-enabled applications and anchor multiyear project pipelines.

Accelerated SaaS Adoption from Remote and Hybrid Work

Enterprise cloud-application usage in the UAE rose 340% in 2024 as firms embedded collaboration suites to support hybrid labor models, according to du Enterprise survey findings. Emirates NBD integrated Microsoft Teams with core banking tools to provide 40,000 employees with regulated remote access, illustrating how CRM and collaboration modules converge around compliance needs. [1]Emirates NBD, “Annual Report 2024,” emiratesnbd.com Sustained flex-work norms maintain upward pressure on SaaS subscriptions.

Rising Cloud-friendly Regulatory Frameworks

The UAE Data Protection Law 2021 and Saudi Arabia’s 2024 Personal Data Protection Law clarify cross-border processing and bolster confidence in public-cloud adoption. GCC mutual-recognition schemes standardize security benchmarks, shrinking compliance overhead for multi-country rollouts. [2]GCC Standardization Organization, “GCC Common Criteria Certification Scheme,” gso.org.sa Qatar’s 2024-2030 cybersecurity blueprint codifies a cloud-first stance, aligning public and private sector incentives.

Surge of VC Funding into Regional SaaS Start-ups

Middle Eastern SaaS ventures attracted USD 1.2 billion in 2024, a 280% jump year on year. Riyadh-based Wafeq secured USD 8 million to scale Arabic-language accounting software, while Dubai’s Cercli raised USD 4 million for HR platforms tailored to GCC labor law. Capital inflows energize localized innovation and intensify competition with global incumbents.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-residency and sovereignty concerns | -2.3% | Saudi Arabia and UAE strictest; moderate across GCC | Long term (≥ 4 years) |

| Scarcity of cloud-skilled local talent | -1.8% | Region-wide, acute in Saudi Arabia and Qatar | Medium term (2-4 years) |

| Fragmented integration standards with legacy IT | -1.4% | UAE and Saudi Arabia enterprises | Medium term (2-4 years) |

| High electricity costs for private-cloud TCO | -0.9% | GCC economies | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Data-residency and Sovereignty Concerns

Local-processing mandates prolong migration cycles. Saudi Arabia’s Global AI Hub Law and UAE finance-sector residency rules force banks to deploy hybrid architectures, elevating costs and adding 18 months to Capital Bank Jordan’s transition schedule. [3]Capital Bank Jordan, “Annual Report 2024,” capitalbank.jo Divergent national standards restrict seamless GCC-wide deployments and inhibit economies of scale.

Scarcity of Cloud-skilled Local Talent

Oracle pledged to train 350,000 cloud professionals by 2026, yet immediate labor-pool shortages inflate project budgets and extend deadlines. Programs such as Saudi Arabia’s SAMAI target 20,000 AI specialists by 2030, but pipeline gaps persist. Limited bilingual developers constrain the delivery of Arabic-native modules, slowing adoption among non-English workforces.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: CRM Leadership Drives Arabic Localization

Customer Relationship Management retained 27.83% of the Middle East cloud applications market share in 2024, driven by the increasing demand for omnichannel banking and e-commerce. Enterprise Resource Planning (ERP) posts the fastest 19.92% CAGR as firms seek integrated finance, supply chain, and HR visibility. Americana Restaurants adopted Oracle Fusion Cloud Applications to harmonize operations across 2,000 venues, proving that AI-enabled Arabic dashboards lift staff productivity.

Second-generation CRM roadmaps now embed sentiment analysis and voice bots tuned to Gulf dialects. Vendors refining natural-language models achieve higher renewal rates as enterprises prioritize culturally aligned customer engagement. Meanwhile, ERP vendors bundle pre-configured VAT and e-invoicing workflows, shortening time-to-value for regional manufacturers. Strong SaaS economics and pay-as-you-grow licensing models broaden accessibility, reinforcing the primacy of CRM and ERP across various industries.

By Deployment Model: Hybrid Configurations Accelerate

Public-cloud options represented 71.34% of the Middle East cloud applications market size in 2024. Yet hybrid installations expand at a 20.69% CAGR because they satisfy sovereignty rules without forsaking global scalability. Microsoft and du committed AED 2 billion (USD 544 million) to UAE data-center builds, enabling enterprises to keep sensitive datasets in-country while tapping Azure AI services.

Telecoms, banks, and healthcare providers leverage dual-zone architectures to segment workloads by risk tier. Edge nodes in Riyadh, Dubai, and Doha cut latency for mobile-commerce apps, enhancing customer experience. Hybrid adoption also aligns with multicloud procurement strategies that curb vendor lock-in and optimize cost. Over time, the Middle East cloud applications market share of pure private cloud will shrink as utilities and government ministries shift non-critical workloads outward to lower capex.

By Organization Size: SME Acceleration Democratizes Access

Large enterprises held 62.76% of the Middle East cloud applications market share in 2024, anchored by multi-year transformation budgets. Nonetheless, SMEs register a 21.34% CAGR, propelled by government e-invoicing mandates and SaaS freemium pricing. The Middle East cloud applications market size captured by SMEs is forecast to triple by 2030, introducing vibrant demand for simplified dashboards and Arabic self-service onboarding.

Al Futtaim Logistics, an SME logistics provider, deployed SAP cloud modules to orchestrate cross-border shipments while satisfying divergent GCC customs codes. Local SaaS start-ups emulate this blueprint, offering SME-friendly bundles that integrate mobile payments, VAT automation, and Arabic chatbots. Regional banks complement the trend by bundling cloud-app vouchers into SME loan packages, lowering adoption friction and deepening stickiness.

By End-user Industry: Retail Surge Transforms Commerce

BFSI controlled 22.43% of the Middle East cloud applications market size in 2024, driven by open-banking APIs and digital-onboarding imperatives. Retail and e-commerce ride a 19.93% CAGR as omnichannel merchants deploy inventory, loyalty, and last-mile analytics tools. Emirates NBD’s USD 272 million technology program underscored financial-sector appetite for cloud-native CRM, risk, and AI chat services.

Fashion and grocery chains enrich web stores with Arabic search and GCC payment gateways. Healthcare providers digitize electronic medical records, adding Arabic voice-to-text for clinicians. Manufacturing adopters focus on predictive-maintenance SaaS to mitigate supply-chain shocks. Cross-industry, demand converges on compliance-ready, low-latency modules that elevate customer experience and operational resilience.

Geography Analysis

Momentum in Saudi Arabia stems from consistent annual government technology spend of more than USD 20 billion, integrated with Public Investment Fund commitments to hyperscale data centers. UAE adoption remains ahead of regional averages, supported by cross-border digital-trade corridors that lift demand for multilingual, multicurrency SaaS. Qatar’s National Development Strategy allocates 15% of state tech budgets to cloud services, ensuring fertile ground for fintech and health-tech pilots.

Israel’s cybersecurity domain spurs the adoption of encrypted SaaS primitives, which are exported across GCC partners via Abraham Accords channels. Turkey leverages its customs union ties with the EU to position Istanbul as a gateway for hybrid cloud services. Egypt and Jordan capitalize on favorable wage rates and Arabic workforce to win managed-services contracts from Gulf conglomerates. Cross-market system integrators refine playbooks that reconcile localized compliance with shared micro-services architectures, promoting a federated yet scalable regional cloud.

lower-priced hydrocarbon supply in Saudi Arabia offsets cooling costs, whereas higher power rates in Oman dampen private-cloud economics. Edge-zone rollouts in Bahrain and Kuwait counter latency hurdles for streaming and fintech apps. Government procurement frameworks increasingly stipulate carbon-footprint metrics, nudging vendors to add renewable-energy credits to a trend likely to spread across the Middle East cloud applications market.

Competitive Landscape

The vendor landscape is moderately fragmented. Microsoft, Oracle, AWS, and SAP anchor the top tier, partnering with local champions such as du, G42, e&, and STC to navigate data-sovereignty rules. Microsoft-du’s AED 2 billion infrastructure plan, AWS-e&’s USD 1 billion regional-expansion pact, and Oracle-Mashreq’s multi-country banking deployment illustrate this alignment.

Localization depth differentiates contenders. Global players embed Arabic UX, VAT workflows, and Sharia-compliant finance modules; local specialists such as Wafeq and Cercli counter with faster customization cycles and lower integration costs. Price competition centers on value-added services, such as managed security, data migration tooling, and verticalized analytics, rather than base subscription fees. Vendor lock concerns drive enterprises toward multi-cloud frameworks, elevating service-broker and observability platforms.

M&A prospects rise as capital-rich Gulf conglomerates scout AI-driven SaaS brands to shore up national-champion plays. Talent-acquisition motives underpin cross-border deals, especially for Arabic NLP teams. Over the horizon, sovereign-AI policies could shift the balance of power toward operators pledging in-region model training and governance, further reshaping the competitive landscape of the Middle East cloud applications market.

Middle East Cloud Applications Industry Leaders

Oracle Corporation

SAP SE

Salesforce, Inc.

Microsoft Corporation

Workday, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Nvidia announced its AI Factories initiative for Saudi Arabia, delivering sovereign compute capacity for Arabic language model training

- April 2025: Microsoft and du committed AED 2 billion (USD 544 million) to new UAE data-center zones to fuel hybrid-cloud growth

- March 2025: Microsoft revealed plans for an AI-enabled Azure region in Kuwait to support public-sector cloud mandates

- November 2024: Pure Data Centres partnered with Dune Vaults to construct hyperscale facilities in Saudi Arabia, enhancing compliant hosting options

Middle East Cloud Applications Market Report Scope

| Customer Relationship Management (CRM) |

| Enterprise Resource Planning (ERP) |

| Human Capital Management (HCM) |

| Supply Chain Management (SCM) |

| Customer Experience and Collaboration |

| Public Cloud |

| Private Cloud |

| Hybrid Cloud |

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| Banking, Financial Services and Insurance (BFSI) |

| Retail and E-commerce |

| Healthcare |

| Manufacturing |

| Government and Public Sector |

| IT and Telecom |

| Other End-user Industries |

| Saudi Arabia |

| United Arab Emirates |

| Qatar |

| Kuwait |

| Oman |

| Bahrain |

| Israel |

| Turkey |

| Jordan |

| Egypt |

| Rest of Middle East |

| By Application | Customer Relationship Management (CRM) |

| Enterprise Resource Planning (ERP) | |

| Human Capital Management (HCM) | |

| Supply Chain Management (SCM) | |

| Customer Experience and Collaboration | |

| By Deployment Model | Public Cloud |

| Private Cloud | |

| Hybrid Cloud | |

| By Organization Size | Large Enterprises |

| Small and Medium Enterprises (SMEs) | |

| By End-user Industry | Banking, Financial Services and Insurance (BFSI) |

| Retail and E-commerce | |

| Healthcare | |

| Manufacturing | |

| Government and Public Sector | |

| IT and Telecom | |

| Other End-user Industries | |

| By Country | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Kuwait | |

| Oman | |

| Bahrain | |

| Israel | |

| Turkey | |

| Jordan | |

| Egypt | |

| Rest of Middle East |

Key Questions Answered in the Report

What is the current valuation of the Middle East cloud applications market?

The market is valued at USD 5.88 billion in 2025 and is forecast to reach USD 14.50 billion by 2030 at a 19.81% CAGR.

Which application category leads spending across the region?

Customer Relationship Management tops spending, holding 27.83% share in 2024.

Why are hybrid-cloud models gaining popularity among Gulf enterprises?

Hybrid configurations satisfy strict data-residency rules while offering access to global cloud services, resulting in a 20.69% CAGR through 2030.

Which country records the fastest growth in cloud-application adoption?

Qatar posts the highest 20.11% CAGR thanks to post-World-Cup digital-economy investments.

How does talent scarcity affect cloud deployments?

Limited local cloud architects inflate costs and prolong project timelines, trimming the overall CAGR by an estimated 1.8%.

What strategic move illustrates rising hyperscale investment in the region?

Microsoft and du’s AED 2 billion venture to expand UAE data centers exemplifies hyperscale commitment to regional growth.

Page last updated on: