Cloud Security In Energy Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 5.43 Billion |

| Market Size (2031) | USD 10.83 Billion |

| Growth Rate (2026 - 2031) | 14.82% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cloud Security In Energy Market Analysis by Mordor Intelligence

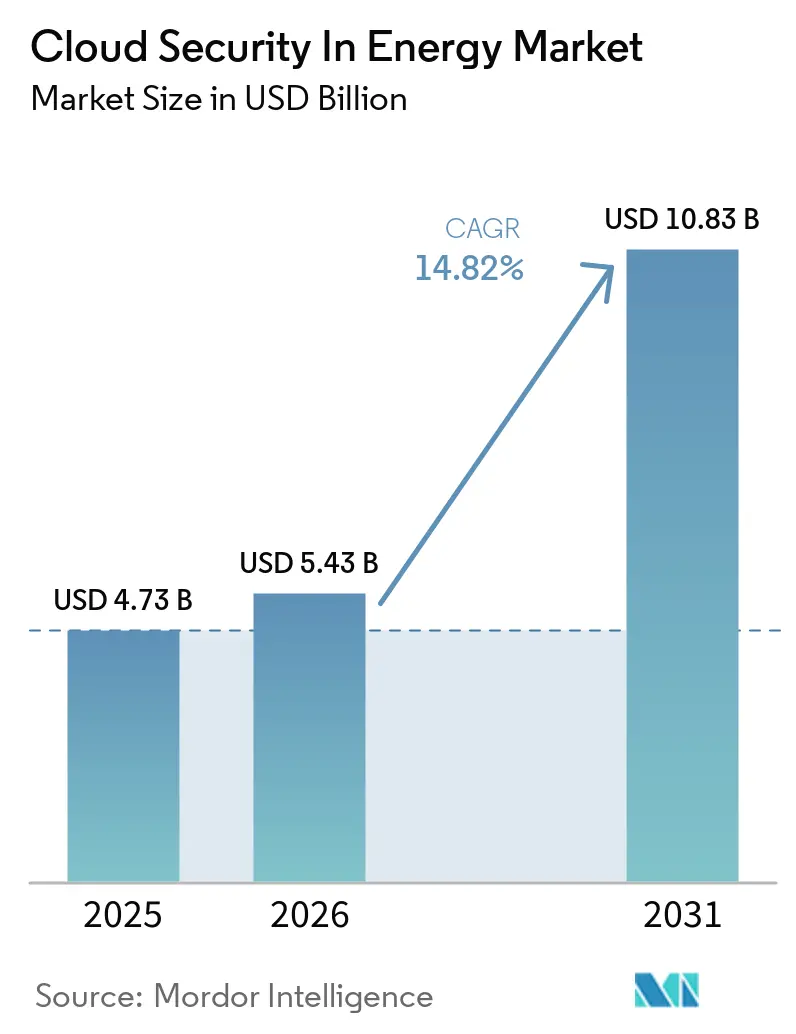

The Cloud Security In Energy Market size is expected to increase from USD 4.73 billion in 2025 to USD 5.43 billion in 2026 and reach USD 10.83 billion by 2031, growing at a CAGR of 14.82% over 2026-2031.

The shift from perimeter-based defenses to cloud-native architectures, the merging of operational technology and information technology networks, and the escalation of advanced persistent threats are driving sustained investment. Utilities see cloud controls as the most viable path for embedding zero-trust principles, automating compliance, and gaining real-time visibility across geographically dispersed assets. Hyperscalers have responded by integrating security services into energy-specific reference architectures, while operational technology specialists embed protocol-level detection that addresses the unique risk profile of turbines, substations, and distributed energy resources. Capital is increasingly directed toward solutions that correlate field telemetry with cloud activity and rapidly remediate misconfigurations, cutting dwell time and reducing the blast radius of inevitable breaches.[1]U.S. Cybersecurity and Infrastructure Security Agency, “Volt Typhoon Critical Infrastructure Intrusion Advisory,” cisa.gov

Key Report Takeaways

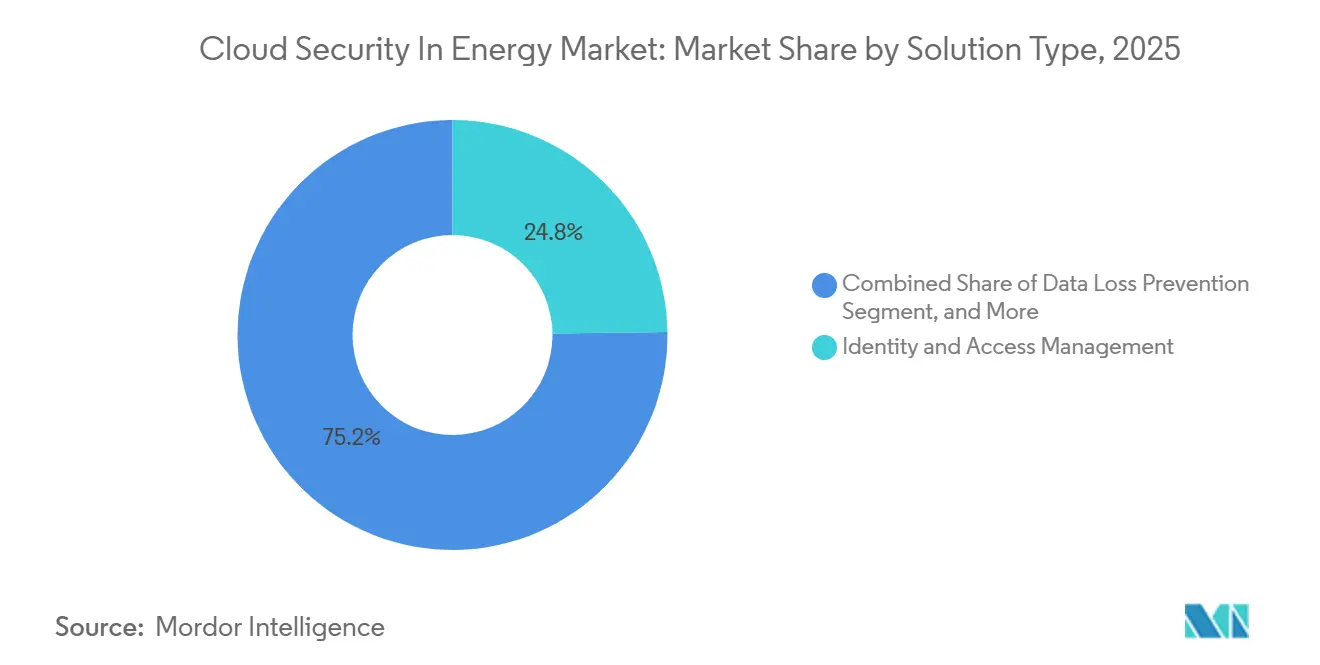

- By solution type, Identity and Access Management led with 24.78% revenue share in 2025; Security Information and Event Management is forecast to expand at a 15.96% CAGR through 2031.

- By security type, Network Security accounted for 34.68% of the cloud security in energy industry share in 2025, while Application Security is projected to advance at a 17.28% CAGR through 2031.

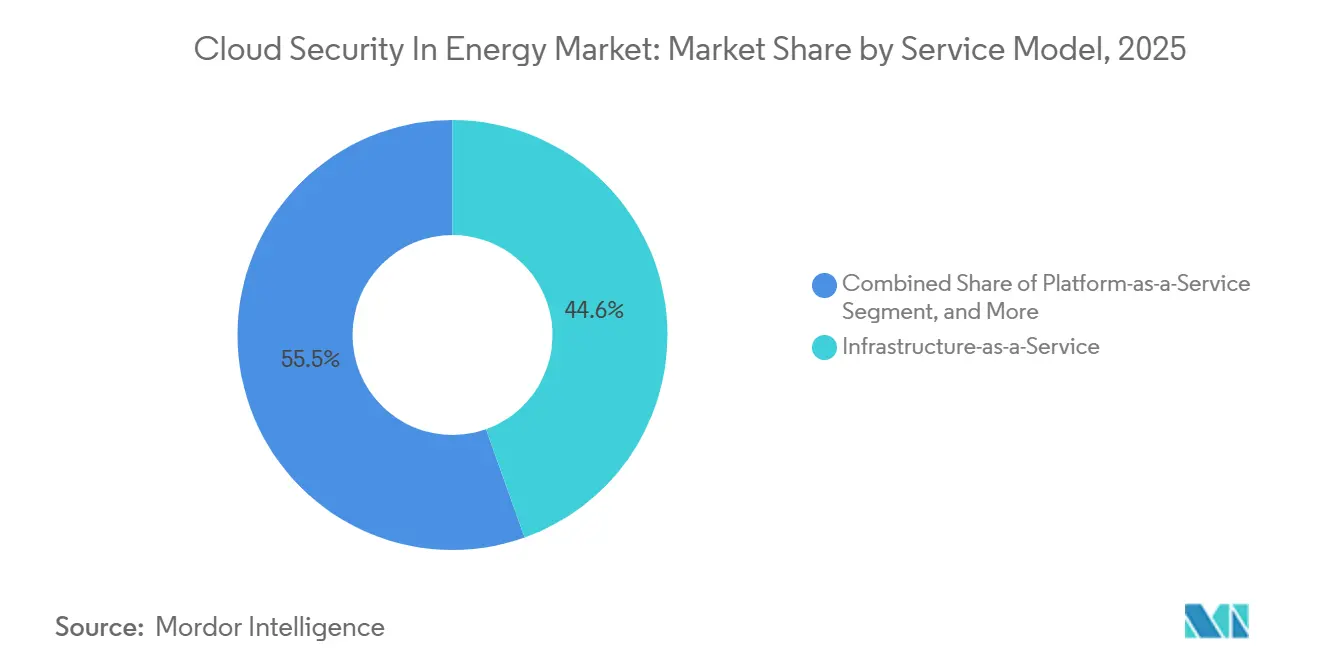

- By service model, Infrastructure-as-a-Service commanded 44.55% of the cloud security in energy industry size in 2025, and Platform-as-a-Service is projected to grow at 18.05% by 2031.

- By deployment, the Public Cloud segment held a 64.37% share in 2025; Hybrid Cloud is set to register a 18.74% CAGR through 2031.

- By geography, North America captured a 39.72% share in 2025, whereas the Asia Pacific is poised to expand at a 16.32% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cloud Security In Energy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Number of Cyber Threats | +3.2% | North America and Europe | Short term (≤ 2 years) |

| Increasing Adoption of IoT Across the Supply Chain | +2.8% | Global, focus on North America and the Asia Pacific | Medium term (2-4 years) |

| Rising Integration of Smart Grid and Distributed Energy Resources | +2.5% | North America, Europe, Asia Pacific | Medium term (2-4 years) |

| Growing Regulatory Mandates for Zero-Trust Architectures in Critical Infrastructure | +2.1% | North America and Europe | Short term (≤ 2 years) |

| Emergence of Cloud-Native Operational Technology Security Platforms Specific to Energy | +1.9% | Global, early adoption in North America | Long term (≥ 4 years) |

| Declining Costs of Edge-to-Cloud Secure Connectivity Solutions Enabled by 5G Private Networks | +1.7% | Asia Pacific, North America, the Middle East | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Number of Cyber Threats

Ransomware and state-sponsored campaigns surged in 2024, with 47 major incidents targeting North American utilities and pipelines, a 38% jump from the prior year. Attackers exploit gaps between legacy supervisory control and data acquisition assets and cloud analytics platforms, a seam where multi-factor authentication is still absent on many endpoints. Agencies such as the Cybersecurity and Infrastructure Security Agency have documented multi-year intrusions, like Volt Typhoon, that remained undetected in critical infrastructure for up to five years. Utilities now prioritize platforms that ingest operational technology telemetry, correlate it with identity data, and spot anomalous breaker commands before physical damage occurs. This demand is driving the adoption of Security Information and Event Management, reducing the mean time to detect and respond from hours to minutes.

Increasing Adoption of IoT Across the Supply Chain

The International Energy Agency reported 2.5 billion connected devices in global energy operations as of 2024, and the total is expected to exceed 4 billion by 2028. Pipelines, transformers, and offshore turbines generate constant telemetry that must be transmitted securely over public networks. Each unmanaged sensor introduces a new attack surface, as illustrated by the 2024 Mirai variant, which co-opted 180,000 energy devices in a distributed denial-of-service attack. Operators now insist on device attestation, encrypted data-in-transit, and policy enforcement at the edge, channeling funds toward cloud platforms capable of onboarding and securing millions of field sensors at scale. These controls also support predictive maintenance programs that boost uptime and reduce truck rolls.

Rising Integration of Smart Grid and Distributed Energy Resources

Distributed energy resources are expected to surpass 180 gigawatts in North America by 2024, making every rooftop solar inverter and community battery a potential target for investment.[2]Federal Energy Regulatory Commission, “Order 2222 Implementation Status Report,” ferc.gov Order 2222 opened wholesale markets to aggregated resources, forcing utilities to expose application programming interfaces to third-party aggregators. Many of these assets ship with default credentials and limited patching mechanisms, prompting utilities to adopt cloud platforms that automate asset discovery, firmware validation, and vulnerability management. Compliance with IEC 62443 is gaining momentum, yet audits reveal that fewer than 30% of deployed devices meet Level 2 security requirements, thereby widening the addressable market for cloud-first vulnerability management tools.

Growing Regulatory Mandates for Zero-Trust Architectures in Critical Infrastructure

United States federal directives and the North American Electric Reliability Corporation Critical Infrastructure Protection version 8 standards align around zero-trust segmentation, least-privilege access, and continuous authentication.[3]U.S. Office of Management and Budget, “Federal Zero Trust Architecture Strategy Memorandum M-24-07,” whitehouse.gov Utilities serving federal loads must now document equivalent controls. In Europe, the NIS2 Directive threatens fines up to EUR 10 million (USD 10.8 million) for inadequate risk management. These policies drive utilities to adopt modern Identity and Access Management, which federates operational technology and information technology directories, supports legacy protocols, and logs every privilege elevation in immutable ledgers. Vendors with native support for industrial protocols enjoy a clear advantage.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of Skilled Cloud Security Professionals in Operational Technology | -1.8% | North America and Europe | Medium term (2-4 years) |

| Integration with Existing Architecture | -1.4% | Global, acute in Europe and North America | Short term (≤ 2 years) |

| Sovereign Cloud Compliance and Data Residency Constraints | -1.2% | Europe, the Middle East, Asia Pacific | Medium term (2-4 years) |

| High Perceived Cost of Continuous Cloud Security Posture Management | -0.9% | Global, especially mid-sized utilities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Shortage of Skilled Cloud Security Professionals in Operational Technology

In 2024, 68% of U.S. electric utilities lacked personnel fluent in both industrial protocols and cloud controls, according to the Department of Energy.[4]U.S. Department of Energy, “Grid Deployment Office Funding Announcement,” energy.gov The talent gap necessitates a heavier reliance on managed service providers, yet many external teams lack the operational experience necessary for zero-downtime environments. Asia Pacific faces similar deficits: India alone needs 15,000 additional operational technology security specialists by 2030. Utilities increasingly outsource detection and response, but third-party access expands the chain of trust and mandates rigorous contract oversight, ultimately constraining near-term adoption velocity.

Sovereign Cloud Compliance and Data Residency Constraints

Data localization rules in Europe, China, and the Middle East compel utilities to operate hybrid architectures that store operational telemetry onshore while using public cloud for analytics. China's Data Security Law prohibits unauthorized cross-border transfers of grid data, and Saudi Arabia now requires locally hosted cloud services for critical infrastructure. Maintaining duplicate controls across regions can increase costs by as much as 40% compared to centralized deployments, erode economies of scale, and slow multinational rollout schedules. Vendors offering sovereign cloud instances are gaining traction, yet integration and operational complexity remain pronounced.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution Type: SIEM Platforms Drive Unified Visibility

The segment generated the strongest growth outlook, with Security Information and Event Management tools forecast to expand at a 15.96% CAGR. This pace reflects the sector’s shift from standalone firewalls to analytics that integrate firewall logs, supervisory control and data acquisition alarms, and identity signals. Identity and Access Management still held 24.78% revenue share in 2025, underscoring the continuing need for foundational credential controls. The cloud security in energy market size for Security Information and Event Management solutions is set to double by 2031 as utilities adopt pre-built correlation packs that flag unauthorized breaker trips or turbine shutdown commands. Vendors such as Splunk and IBM integrate energy-specific rules, compressing incident investigation cycles to minutes.

Security spending on Data Loss Prevention, Intrusion Detection Systems, and Encryption rounds out the solution stack. In upstream oil and gas, Data Loss Prevention protects seismic models valued at billions, preventing inadvertent exposure via misconfigured storage buckets. Operational technology-aware Intrusion Detection Systems now inspect Modbus and DNP3 traffic for abnormal register writes. Encryption remains mandatory for edge-to-cloud pathways: utilities are refreshing libraries to align with post-quantum standards finalized in 2024. Collectively, these tools underpin a defense-in-depth posture that can handle the heightened threat tempo without increasing headcount.

By Security Type: Application Controls Accelerate with Cloud-Native Migration

Application Security is projected to grow at 17.28% as utilities modernize monolithic supervisory control and data acquisition human-machine interfaces into microservices. While Network Security retained a 34.68% share in 2025, its share is being diluted as enforcement shifts from the perimeter to application programming interface (API) gateways and service meshes. The cloud security in energy sector market share for Application Security is widening because every distributed energy resource aggregator connects through application programming interface (API) calls that must be rate-limited, input-sanitized, and OAuth-authenticated. The Open Web Application Security Project ranked broken object-level authorization as the top risk for 2024, an acute concern for grid operators that dispatch power across dynamic endpoints.

Database, Endpoint, and Email controls complement this progression. Database Security protects trading desks where millisecond latency drives profit; tokenization and field-level encryption defend sensitive bids. Extended detection and response on endpoints detects anomalous field engineer behavior before data exfiltration occurs. Email gateways block spear-phishing campaigns, which, according to the Cybersecurity and Infrastructure Security Agency, accounted for 62% of breaches in 2024. Together, these layers tighten the zero-trust perimeter around every asset, identity, and workload.

By Service Model: Platform-as-a-Service Catalyzes Operational Agility

Infrastructure-as-a-Service held a 44.55% share in 2025 as utilities lifted and shifted legacy virtual machines. Platform-as-a-Service, however, is the fastest mover at an 18.05% CAGR through 2031. The cloud security in energy market size for Platform-as-a-Service is expanding because operators can deploy Python models for demand forecasting, ingest weather feeds, and publish dispatch schedules without managing operating systems. Renewable energy players utilize Platform-as-a-Service to refine solar and wind predictions in real-time, thereby avoiding costly over-production penalties. Vendors now embed North American Electric Reliability Corporation Critical Infrastructure Protection logging and role-based access in their Platform-as-a-Service offerings, removing compliance roadblocks and accelerating adoption.

Software-as-a-Service uptake remains selective. Identity and Access Management as a service is widely consumed, yet utilities hesitate to place industrial telemetry in generic Software-as-a-Service environments that lack IEC 61850 support. Consequently, Platform-as-a-Service serves as the compromise, permitting code-level customization while insulating developers from infrastructure chores. Future growth hinges on the development of sovereign Platform-as-a-Service (PaaS) capacity in Europe, China, and the Middle East, where localization mandates influence procurement decisions.

By Deployment Type: Hybrid Cloud Balances Latency and Compliance

Public Cloud accounted for 64.37% of the 2025 spend, as non-critical workloads, such as billing and human resources, benefit from elastic storage and compute. Yet Hybrid Cloud deployments will rise at a 18.74% CAGR as utilities reconcile sub-10 millisecond latency demands with data sovereignty imperatives. The cloud security in energy market size for Hybrid Cloud solutions is poised to exceed USD 5.41 billion by 2031, fueled by grid-edge data centers that process synchrophasor feeds locally while streaming insights to hyperscaler analytics engines. Utilities distribute workloads across AWS, Azure, and Google Cloud to avoid vendor lock-in, but multi-cloud sprawl complicates policy enforcement.

Private Cloud installations remain a niche market, catering to jurisdictions that prohibit the use of public infrastructure for critical systems. Where permitted, utilities adopt cloud security posture management platforms that normalize policy across on-premises and public estates, exposing misconfigurations before auditors do. As data residency rules proliferate, the Hybrid model offers the flexibility to isolate protected telemetry while retaining compute economics.

Geography Analysis

North America held a 39.72% share in 2025, propelled by the North American Electric Reliability Corporation's Critical Infrastructure Protection regulations and federal funding. The U.S. Department of Energy allocated USD 3.5 billion in 2024 for grid modernization, stipulating advanced cybersecurity controls. Canada followed with a similar mandate, and Mexico’s market liberalization led to greenfield deployments that adopted zero-trust from day one. Utilities in the region heavily rely on Security Information and Event Management (SIEM) and Identity and Access Management (IAM) solutions to meet audit benchmarks, and the presence of hyperscale data centers accelerates the adoption of these technologies. Despite its maturity, the region remains vulnerable to ransomware, which continues to drive high investment levels.

Asia Pacific is forecast to grow at 16.32%, the fastest regional pace. China’s plan to achieve 1,200 gigawatts of renewable energy by 2030 drives massive cloud adoption, exemplified by State Grid’s 2024 deployment, which covers 1.1 billion customers. India’s Smart Grid Mission and Japan’s resilience agenda are bolstering demand for hybrid cloud, which combines on-premises sovereignty with burst capacity. Australia mandates multi-factor authentication and encrypted links for all market participants, further lifting security budgets. Skills shortages, however, pose a brake, pushing utilities toward managed services.

Europe, South America, the Middle East, and Africa form the remainder. Europe enforces the toughest compliance regime under the NIS2 and the Cyber Resilience Act, prompting utilities to adopt continuous monitoring. Germany’s Energiewende created over 2 million distributed energy resources, demanding secure onboarding. Brazil’s 2024 resolution requires annual penetration tests and the deployment of Security Information and Event Management (SIEM). In the Middle East, megaprojects such as NEOM in Saudi Arabia specify cloud-native operational technology security from the blueprint stage. African nations are deploying solar mini-grids with embedded controls, thereby bypassing legacy technical debt and opening direct paths to cloud-first architectures.

Competitive Landscape

The cloud security market in the energy exhibits moderate fragmentation, with the five largest providers controlling only a nominal slice of the revenue. Hyperscalers Amazon, Microsoft, and Google bundle security into infrastructure, offering pre-certified templates that speed compliance. Their scale allows for competitive pricing, pressuring pure-play companies to emphasize deep operational technology protocol coverage. Specialists such as Nozomi Networks and Dragos focus on visibility for Modbus, DNP3, and IEC 61850, winning accounts that value granular detection over single-vendor convenience. The result is a dual-track procurement pattern: utilities pair hyperscaler benefits with niche sensors that feed specialized analytics engines.

Industrial automation majors Siemens and Schneider Electric blur traditional lines through acquisitions and partnerships. Siemens acquired Claroty in 2025, delivering asset discovery and vulnerability management capabilities directly integrated into its control platforms. Schneider Electric integrated Palo Alto Networks’ Prisma Cloud to extend zero-trust across EcoStruxure deployments. These moves resonate with utilities seeking end-to-end solutions rather than juggling multiple vendors. Artificial intelligence is emerging as a key differentiator; Palo Alto Networks’ 2024 patent for protocol anomaly detection underscores the race to embed machine learning directly in security stacks.

Opportunities abound in sovereign cloud delivery. European and Middle Eastern utilities require local hosting but still want global analytics. Microsoft invested USD 750 million to expand sovereign Azure regions for energy workloads, highlighting market appetite. Vendors able to deliver region-specific clouds with global policy orchestration can secure long-term contracts. The talent shortage also creates openings for managed detection and response providers with operational technology fluency. Firms that combine 24/7 monitoring, incident response, and compliance reporting under one roof are well-positioned to capture a growing annuity stream.

Cloud Security In Energy Industry Leaders

IBM Corporation

Broadcom Inc.

Cisco Systems, Inc.

Microsoft Corporation

Google LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Microsoft Corporation invested USD 750 million to add eight sovereign Azure regions in Europe and the Middle East, embedding IEC 62443-compliant segmentation and automated North American Electric Reliability Corporation Critical Infrastructure Protection reporting.

- October 2025: Amazon Web Services launched AWS Energy Security Hub, unifying asset discovery, threat detection, and encrypted edge connectivity for Modbus and DNP3 traffic.

- September 2025: Siemens AG closed its USD 1.8 billion acquisition of Claroty Ltd., adding industrial asset visibility and vulnerability management across 1,200 energy facilities.

- August 2025: Palo Alto Networks partnered with Schneider Electric to integrate Prisma Cloud into EcoStruxure, offering automated compliance scanning and zero-trust access for remote operational technology staff.

Global Cloud Security In Energy Market Report Scope

The Cloud Security in Energy Industry Report is Segmented by Solution Type (Identity and Access Management, Data Loss Prevention, IDS or IPS, Security Information and Event Management, Encryption, and Other Solution Type), Security Type (Application Security, Database Security, Endpoint Security, Network Security, Web and Email Security, and Other Security Type), Service Model (Infrastructure-as-a-Service, Platform-as-a-Service, and Software-as-a-Service), Deployment Type (Public Cloud, Private Cloud, and Hybrid Cloud), and Geography. Market Forecasts are Provided in Terms of Value (USD).

| Identity and Access Management |

| Data Loss Prevention |

| IDS or IPS |

| Security Information and Event Management |

| Encryption |

| Other Solution Type |

| Application Security |

| Database Security |

| Endpoint Security |

| Network Security |

| Web and Email Security |

| Other Security Type |

| Infrastructure-as-a-Service |

| Platform-as-a-Service |

| Software-as-a-Service |

| Public Cloud |

| Private Cloud |

| Hybrid Cloud |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Egypt | |

| Rest of Africa |

| By Solution Type | Identity and Access Management | |

| Data Loss Prevention | ||

| IDS or IPS | ||

| Security Information and Event Management | ||

| Encryption | ||

| Other Solution Type | ||

| By Security Type | Application Security | |

| Database Security | ||

| Endpoint Security | ||

| Network Security | ||

| Web and Email Security | ||

| Other Security Type | ||

| By Service Model | Infrastructure-as-a-Service | |

| Platform-as-a-Service | ||

| Software-as-a-Service | ||

| By Deployment Type | Public Cloud | |

| Private Cloud | ||

| Hybrid Cloud | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large is the cloud security in energy market in energy today?

The cloud security in energy market size reached USD 5.43 billion in 2026 and is projected to reach USD 10.83 billion by 2031.

Which solution type is growing fastest among energy utilities?

Security Information and Event Management platforms are advancing at a 15.96% CAGR through 2031 as operators seek unified visibility across operational technology and information technology.

Why is Hybrid Cloud deployment gaining momentum in utility security?

Hybrid Cloud balances latency-sensitive operational technology workloads that must stay on-premises with the elastic analytics power of public cloud, driving a 18.74% CAGR.

What is the primary regulatory driver in North America?

The North American Electric Reliability Corporation's Critical Infrastructure Protection version 8 standards require segmentation, least privilege, and continuous monitoring, prompting utilities to adopt zero-trust solutions.

Which region is forecast to expand fastest through 2031?

The Asia Pacific is expected to grow at a 16.32% CAGR, driven by China’s massive renewable energy build-out and India’s smart grid initiatives.

How severe is the talent gap in operational technology cloud security?

In 2024, 68% of U.S. utilities reported having insufficient staff skilled in both industrial protocols and cloud controls, resulting in a heavier reliance on managed services.

Page last updated on: