Cloud Security In Manufacturing Industry Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

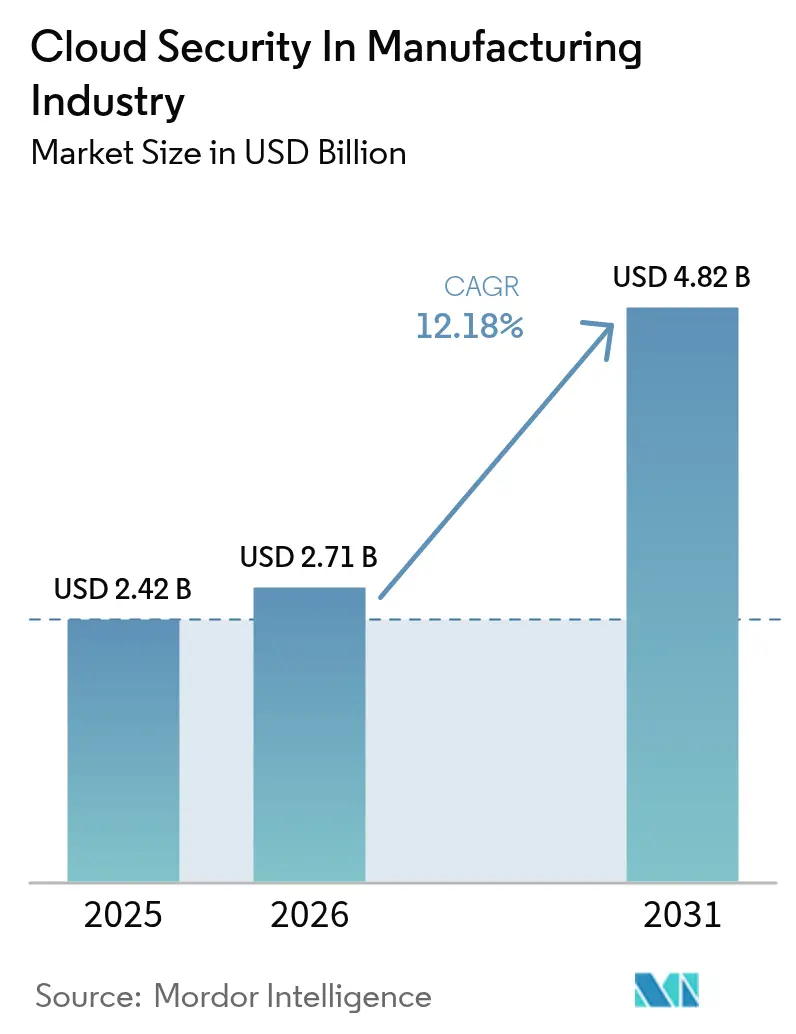

| Market Size (2026) | USD 2.71 Billion |

| Market Size (2031) | USD 4.82 Billion |

| Growth Rate (2026 - 2031) | 12.18% CAGR |

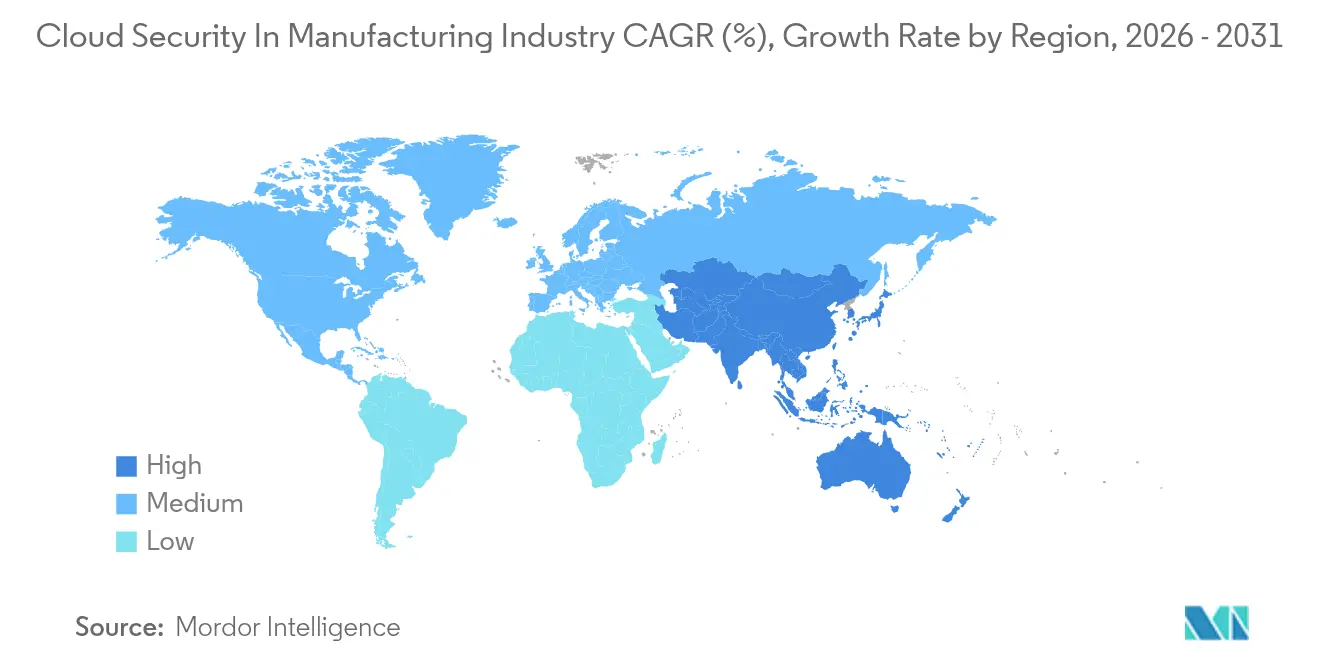

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

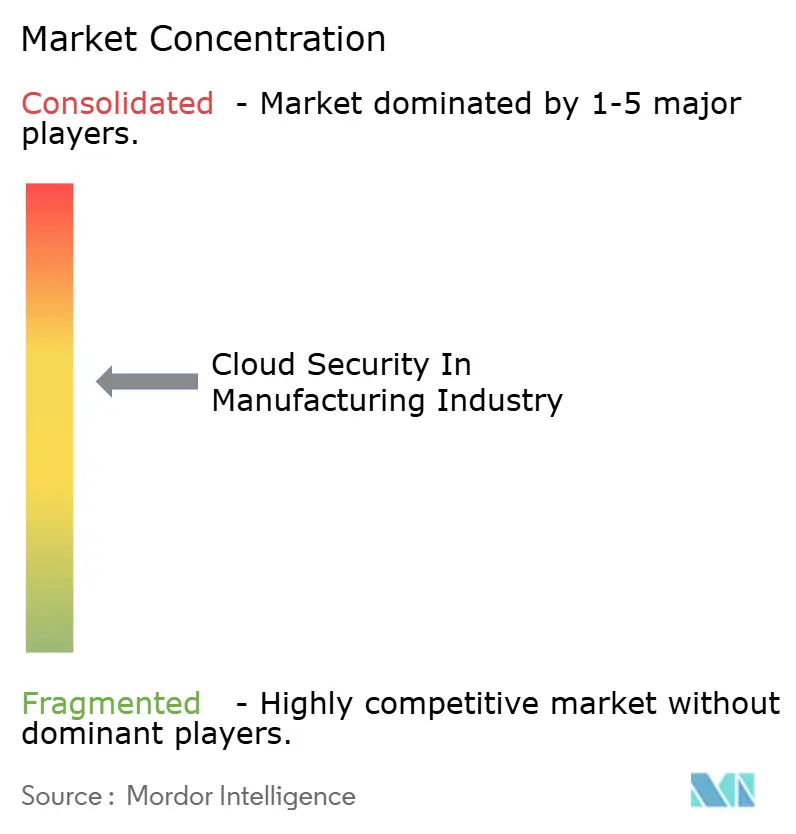

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cloud Security In Manufacturing Industry Analysis by Mordor Intelligence

The cloud security in manufacturing industry market size is expected to grow from USD 2.42 billion in 2025 to USD 2.71 billion in 2026 and is forecast to reach USD 4.82 billion by 2031 at 12.18% CAGR over 2026-2031. The steady migration of production systems to public and hybrid clouds, coupled with 25.7% of all global cyber incidents affecting manufacturers in 2024, drives spending on resilient, industry-specific defenses. Average breach costs rose to USD 5.56 million in 2024, and unplanned downtime averaged USD 22,000 per minute, making proactive investment in identity controls, zero-trust architectures, and AI-driven threat response a board-level imperative.[1]IBM, “Cost of a Data Breach Report 2024,” ibm.com Vendor platform consolidation is accelerating as buyers favor integrated capabilities that cover both IT and OT assets, while sovereign-cloud mandates in Europe and Asia influence deployment choices. Competitive differentiation now hinges on AI-powered analytics, low-latency remediation, and support for quantum-ready encryption as manufacturers seek future-proof security roadmaps.

Key Report Takeaways

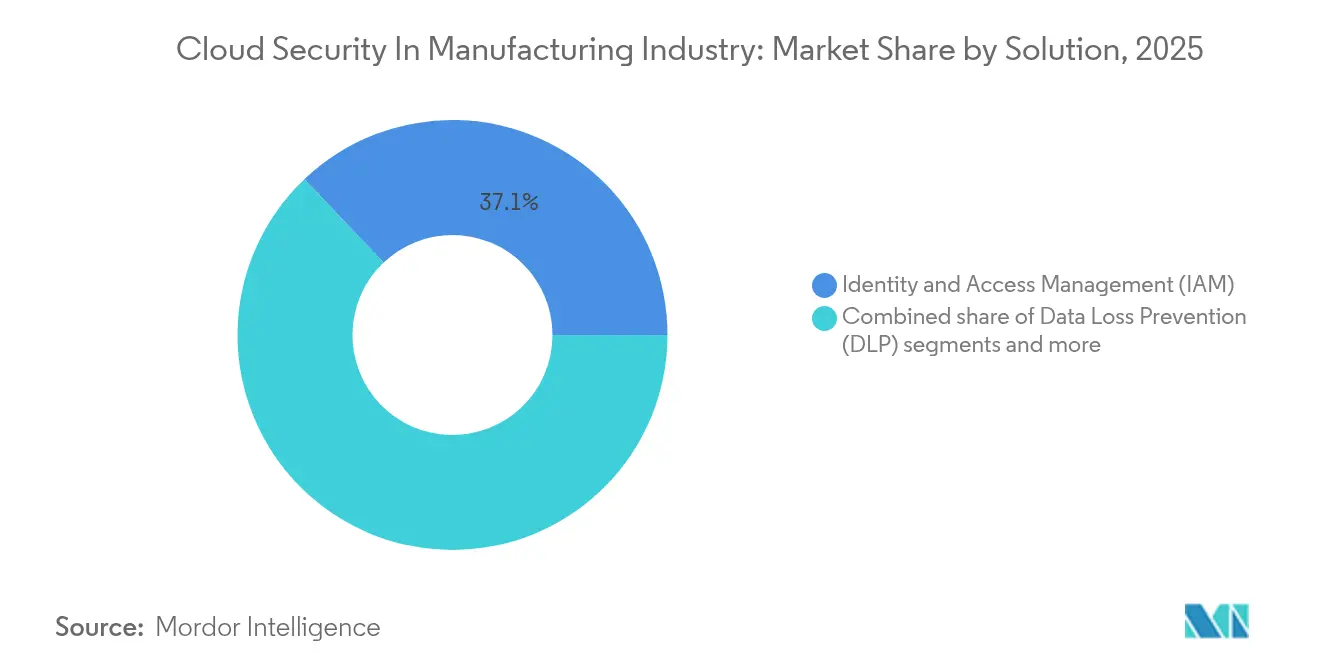

- By solution, Identity and Access Management led with 37.10% of cloud security in manufacturing industry share in 2025; Data Loss Prevention is projected to expand at a 12.37% CAGR through 2031.

- By security type, Application Security accounted for 37.75% revenue share in 2025, whereas Network Security posts the fastest 12.62% CAGR to 2031.

- By service model, Platform-as-a-Service Security captured 56.10% of the cloud security in manufacturing industry size in 2025; Software-as-a-Service Security is set to grow at 13.14% CAGR through 2031.

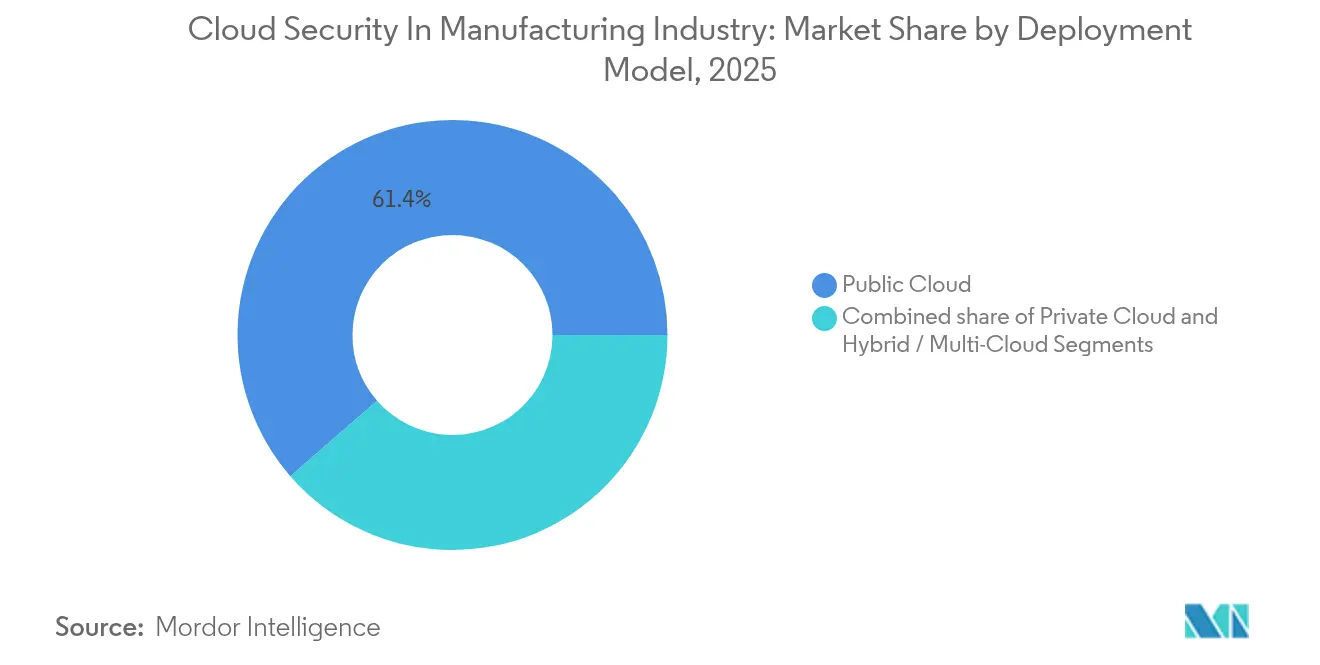

- By deployment model, Public Cloud held 61.40% adoption in 2025, while Hybrid/Multi-Cloud configurations rise at a 13.32% CAGR.

- By organization size, large enterprises accounted for 69.10% of spending in 2025, while SMEs are projected to show a stronger 13.74% CAGR to 2031.

- By geography, North America retained 38.20% market leadership in 2025; Asia-Pacific is the fastest-growing region at 12.88% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cloud Security In Manufacturing Industry Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging multi-cloud complexity elevating attack surface | +2.1% | Global, with highest impact in North America & Europe | Medium term (2-4 years) |

| Regulatory mandates accelerate security spend | +2.8% | Europe (NIS2), North America (CMMC), expanding to APAC | Short term (≤ 2 years) |

| AI-driven autonomous remediation cutting MTTR | +1.9% | Global, led by North America and Europe early adopters | Medium term (2-4 years) |

| Cloud-native application protection platform (CNAPP) consolidation wave | +1.7% | Global, concentrated in mature cloud markets | Medium term (2-4 years) |

| API economy exposure driving security budgets | +1.5% | Global, particularly in digitally advanced manufacturing hubs | Short term (≤ 2 years) |

| Quantum-safe encryption pilots in hyperscalers | +0.8% | North America & Europe, expanding to APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Multi-Cloud Complexity Elevating Attack Surface

Manufacturers now operate across AWS, Azure and Google Cloud, with 95% using at least two providers. Connecting these environments to legacy shop-floor systems multiplies threat entry points and complicates compliance alignment. Unified cloud security platforms that interpret both IT and OT telemetry command premium budgets. Demand is acute for agentless, runtime-aware controls that safeguard programmable logic controllers without disrupting production. Vendors that simplify policy orchestration across heterogeneous estates gain clear advantage.

Regulatory Mandates Accelerate Security Spend

Implementation of the EU NIS2 Directive and U.S. CMMC Level 2 obligations forces immediate upgrades to monitoring, incident reporting and supply-chain assurance.[2]European Commission, “NIS2 Directive,” ec.europa.eu Manufacturers invest in FedRAMP-authorized services and automated compliance tooling to avoid contract exclusion. Similar rules in India and Japan magnify complexity, spurring adoption of regionally hosted sovereign clouds to localize sensitive data. Short deployment windows turn compliance from a governance task into a primary budget catalyst.

AI-Driven Autonomous Remediation Cutting MTTR

Google Cloud’s Gemini agents and Siemens SIBERprotect illustrate how AI shrinks mean time to respond in both IT and OT zones. Autonomous playbooks that isolate malware-infected robots within milliseconds preserve production continuity and avert million-dollar downtime losses. Successful deployments couple machine-learning analytics with granular identity controls to execute safe-by-design actions, although governance teams still validate overrides to maintain operational assurance.

Cloud-Native Application Protection Platform (CNAPP) Consolidation Wave

Fortinet’s June 2024 acquisition of Lacework and Palo Alto Networks’ QRadar buy show momentum toward single-pane CNAPP suites. Manufacturers tired of tool sprawl favor vendors merging posture management, workload protection and entitlement governance under one license. Consolidation also unlocks deeper context sharing, allowing AI engines to prioritize alerts by production impact. Agentless scanning appeals to plants reluctant to install code on deterministic control hardware.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Identity debt from unmanaged machine identities | -1.8% | Global, particularly acute in automated manufacturing environments | Short term (≤ 2 years) |

| Shortage of cloud-literate security engineers | -2.2% | Global, most severe in North America and Europe | Medium term (2-4 years) |

| Cross-border data-sovereignty frictions slow roll-outs | -1.4% | Global, with highest impact in Europe and Asia-Pacific due to GDPR and sovereign cloud requirements | Medium term (2-4 years) |

| Hidden egress fees inflate TCO of secure cloud architectures | -1.1% | Global, particularly affecting multi-cloud and hybrid deployments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Identity Debt from Unmanaged Machine Identities

IoT sensors, robots and edge gateways outnumber humans on the factory floor, yet 75% of firms lack lifecycle oversight for their credentials. Stale certificates and hard-coded keys provide covert persistence paths for attackers. Scaling zero-trust to millions of non-human identities demands automated discovery, rotation and revocation workflows that many plants still lack, constraining immediate uptake of advanced cloud services.

Shortage of Cloud-Literate Security Engineers

Hybrid security roles spanning Kubernetes, LDAP and PLC firmware remain scarce. Manufacturing lags behind technology and finance in employer brand appeal, resulting in a widening of vacancies for DevSecOps and OT security architects. Without staff to tune policies or investigate alerts, some firms postpone migrations or over-rely on managed service providers, trimming potential growth in the cloud security in manufacturing industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution: IAM Leadership Amid DLP Acceleration

Identity and Access Management commanded 37.10% of the cloud security in manufacturing industry in 2025, reflecting the urgent need to gate every user and machine session. Manufacturers integrate privileged-access vaults with zero-trust segmentation to curb lateral movement. Modern IAM stacks embed certificate authorities for robots and additive printers, unifying policy across IT and OT. Data Loss Prevention, growing at a 12.37% CAGR, gains traction as export-controlled design files are exchanged between CAD systems and contract assemblers. Advanced DLP that classifies engineering blueprints and blocks exfiltration by anomaly peaks addresses rising IP theft.

Micro-segmentation features bolster IAM by binding dynamic policies to workloads in Kubernetes clusters that feed production lines. Conditional access using real-time risk scores throttles credentials during suspected compromise, lifting resilience against ransomware. Meanwhile, encryption and key-management modules gain relevance as quantum-ready algorithms enter pilots. Collectively, these trends keep the cloud security in manufacturing industry focused on identity-centric controls that can scale to millions of endpoints without impairing uptime.

By Security Type: Application Focus Drives Network Innovation

Application Security held a 37.75% share of the cloud security in manufacturing industry in 2025 as industrial firms re-platform MES and PLM workloads into containers hosted in public clouds. Runtime protection, software-composition analysis and API gateways form core defense layers. Network Security is projected to grow 12.62% annually, driven by east-west inspection for OT traffic traversing SD-WAN links to cloud data lakes. Manufacturers apply deep-packet inspection tuned for Modbus and OPC UA protocols to thwart command spoofing.

Edge rollouts that leverage 5G private networks further elevate demand for micro-firewalls and zero-trust network access. Database, endpoint and email security maintain steady uptake, yet incremental spending converges on network detection-and-response engines that correlate traffic anomalies with application logs. This convergence underscores how the cloud security in manufacturing industry is increasingly treating the application and network layers as a single, unified fabric governed by a single policy engine.

By Service Model: PaaS Dominance Challenges SaaS Growth

Platform-as-a-Service Security accounted for 56.10% revenue in 2025, underscoring manufacturers’ desire to control compiler chains and runtime libraries while still benefiting from managed infrastructure. Vendors supply hardening blueprints, least-privilege defaults and drift detection that map neatly to DevSecOps pipelines. Software-as-a-Service Security, however, expands at 13.14% CAGR as ERP, PLM and quality-management vendors cut on-prem options. Secure access brokers that enforce granular OAuth scopes and contextual policies have become essential for protecting multi-tenant SaaS data sets.

Infrastructure-as-a-Service Security remains foundational, delivering host hardening, virtual network segmentation and policy-as-code frameworks. Yet, the cloud security in manufacturing industry increasingly gravitates toward abstraction layers where security controls are embedded by default, allowing plants to innovate without requiring deep in-house cloud talent.

By Deployment Model: Public Cloud Leadership Faces Hybrid Challenge

Public Cloud represented 61.40% of the cloud security in manufacturing industry in 2025 as hyperscalers met ISO 27001 and sector-specific compliance benchmarks. Lower capex, global reach and managed AI services continue to attract production analytics and digital-twin workloads. Hybrid and Multi-Cloud adoption, advancing 13.32% annually, reflects sovereignty rules and latency-sensitive use cases placing edge nodes inside plants. Unified posture-management portals help teams visualize policy gaps across VMware-based private clouds and Kubernetes clusters hosted by hyperscalers.

Private Cloud persists for export-controlled defense programs or continuous-process plants that shun internet links. Flexible orchestration between tiers enables the burst-capacity rendering of computationally intensive simulations while sensitive parameters remain on-premises. Such patterns keep the cloud security in manufacturing industry diversified, ensuring suppliers must support consistent controls across all deployment options.

By Organization Size: Enterprise Dominance Amid SME Acceleration

Large Enterprises contributed 69.10% of spending in 2025, leveraging scale to negotiate enterprise-wide platform licenses and fund red-team programs. However, SMEs drive the highest 13.74% CAGR as cloud-native offerings bundle best-practice configurations and managed detection out of the box. Consumption-based billing suits seasonal production cycles, enabling smaller plants to match security spend with throughput.

Vendor roadmaps increasingly include low-touch portals, automated onboarding and AI assistants that draft compliance reports, empowering SMEs to meet supply-chain mandates without hiring scarce cloud architects. As a result, the cloud security industry in manufacturing gains broader penetration across the supplier network, strengthening overall ecosystem resilience.

Geography Analysis

North America held 38.20% of the cloud security in manufacturing industry in 2025 due to strict CMMC enforcement on defense contractors and multi-billion-dollar federal programs such as the USD 5.6 billion Mission Partner Environment. U.S. automotive and aerospace primes demand proof of zero-trust adoption from tier-one suppliers, spurring platform standardization. Canada’s CPCSC, effective winter 2025, introduces NIST-aligned certification for cross-border components, further reinforcing its regional leadership.

Europe accelerates on the back of the NIS2 Directive, compelling manufacturing firms to deploy incident monitoring, risk management, and supply-chain security by 2025. Germany, France, and the United Kingdom invest heavily in sovereign cloud zones managed by local telcos to comply with GDPR and upcoming AI Act data-governance clauses. Unified dashboards that map exposure across multinational plants are in demand as firms juggle varied national guidance.

Asia-Pacific records the fastest 12.88% CAGR, fuelled by national Industry 4.0 initiatives and rising awareness after headline OT attacks. China, India, and Japan combine smart-factory subsidies with stricter data-localization mandates, prompting hybrid architectures that keep telemetry onshore. Regional manufacturers show strong interest in AI-enabled threat hunting: 77% prioritise cybersecurity in digital roadmaps and 67% place cloud platform security among the top three investments. Sovereign clouds and shared-responsibility guidance tailored to multilingual workforces differentiate vendors seeking APAC market share.

Competitive Landscape

The cloud security in manufacturing industry remains moderately consolidated. Palo Alto Networks deepened platform breadth by acquiring Protect AI for USD 650-700 million in April 2025, bolstering AI code-supply-chain scanning. T-Mobile’s managed SASE launch with Prisma SASE 5G demonstrates how telco-security partnerships create vertical bundles that embed SIM-based authentication for IoT machines.

Fortinet’s integration of Lacework’s agentless CNAPP, completed in 2024, positions its Security Fabric to serve plants seeking unified policy across Kubernetes, serverless, and OT assets. CyberArk’s alliance with Device Authority and Microsoft targets certificate sprawl on factory equipment, blending privileged-access controls with automated identity issuance. Nozomi Networks secured USD 100 million from Mitsubishi Electric and Schneider Electric to accelerate protocol-aware detection for multi-vendor lines.[4]Nozomi Networks, “Mitsubishi Electric and Schneider Electric Back USD 100 Million Investment,” nozominetworks.com

Vendors differentiate through embedded AI, low-impact deployment, and domain expertise. Leaders who couple IT-grade analytics with deterministic-control safety validations stand to capture expanding budgets as the cloud security in manufacturing industry matures.

Cloud Security In Manufacturing Market Leaders

Trend Micro Inc.

Imperva Inc.

Broadcom Inc.

IBM Corporation

Cisco Systems Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: T-Mobile and Palo Alto Networks introduced a managed SASE 5G service for manufacturing enterprises.

- April 2025: Palo Alto Networks agreed to acquire Protect AI for USD 650-700 million to enhance large-language-model security.

- March 2025: CyberArk, Device Authority and Microsoft launched a secure device-authentication stack for factory IoT, aligned with NIST reference architecture.

- October 2024: Darktrace unveiled Darktrace/Cloud for real-time misconfiguration detection across multi-cloud estates.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Cloud security in manufacturing captures the software controls, policy frameworks, and managed safeguards that protect cloud-hosted enterprise and shop-floor workloads for discrete and process manufacturers. Spending on identity and access management, data-loss prevention, intrusion detection or prevention, encryption, and continuous monitoring that secures production, supply-chain, and product-lifecycle workloads on public, private, or hybrid clouds is sized in our study. According to Mordor Intelligence, the segment is expected to reach USD 2.42 billion in 2025 and expand at a 12.4 percent CAGR through 2030 (mordorintelligence.com).

Scope exclusion: Security solutions purchased by non-manufacturing verticals or for purely on-premise operational technology stacks fall outside this assessment.

Segmentation Overview

- By Solution

- Identity and Access Management (IAM)

- Data Loss Prevention (DLP)

- Security Information and Event Management (SIEM)

- Encryption and Key Management

- Other Solutions

- By Security Type

- Application Security

- Database Security

- Endpoint Security

- Network Security

- Web and Email Security

- By Service Model

- SaaS Security

- PaaS Security

- IaaS Security

- By Deployment Model

- Public Cloud

- Private Cloud

- Hybrid / Multi-Cloud

- By Organization Size

- Large Enterprises

- Small and Medium Enterprises (SMEs)

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Nigeria

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

We interview CISOs of automotive and electronics plants, cloud architects at leading platforms, and regional managed service advisors across North America, Europe, and Asia-Pacific. Their feedback tests adoption assumptions, surfaces license prices, and flags emerging use cases that numbers alone might miss.

Desk Research

Our team starts with authoritative, non-paywalled datasets from the US Cybersecurity and Infrastructure Security Agency, Eurostat digital economy tables, and Japan's METI smart factory surveys to quantify cloud adoption by plant size. Trade groups such as the International Society of Automation and the Manufacturing Leadership Council add incident context, while customs statistics reveal regional inflows of security appliances transitioning toward cloud delivery.

Those insights are blended with company 10-Ks, investor day transcripts, and curated news feeds from D&B Hoovers and Dow Jones Factiva, enabling us to map vendor revenue trails and triangulate average selling prices. The sources listed illustrate our open-source backbone; many additional references are reviewed to collect figures, validate anomalies, and clarify gray areas.

Market-Sizing & Forecasting

The model begins with a top-down reconstruction of spending pools derived from the count of cloud-hosted manufacturing workloads and typical security spend per workload. Selective supplier roll-ups and channel checks provide a bottom-up lens to adjust totals where penetration diverges. Key variables include active industrial IoT node counts, off-premise workload migration rates, multi-cloud penetration, SaaS security price erosion, and region-specific compliance deadlines. Multivariate regression, layered with scenario analysis, produces forecasts that accommodate macro shocks and policy changes.

Data Validation & Update Cycle

Outputs pass variance and anomaly screens before senior analysts audit assumptions and re-contact sources where outliers persist. The dataset is refreshed annually, with interim updates triggered by material vendor disclosures, regulatory shifts, or major breaches.

Why Mordor's Cloud Security Manufacturing Baseline Is Most Trustworthy

Published estimates differ because firms adopt dissimilar vertical boundaries, count overlapping security layers, or anchor to different base years. Competing studies place 2024 values at USD 3.24 billion and 2025 values as high as USD 5 billion.

Key gap drivers include bundling generic cloud security revenue from other industries, converting multi-year contract bookings to single-year revenue, and applying workload migration curves that our interviews did not confirm.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.42 B (2025) | Mordor Intelligence | |

| USD 3.24 B (2024) | Global Consultancy A | Broader security stack and different base year |

| USD 5.00 B (2025) | Industry Data Firm B | Includes upstream supplier spend and books to revenue conversion |

The comparison shows that once scope, contract accounting, and migration realism are normalized, Mordor's figure offers decision-makers a balanced, transparent baseline that ties back to clear variables and repeatable steps.

Key Questions Answered in the Report

What is the projected value of the cloud security in manufacturing industry by 2031?

The market is expected to reach USD 4.82 billion by 2031, expanding at a 12.18% CAGR.

Which solution currently holds the largest market share?

Identity and Access Management leads with 37.10% share in 2025.

Why is Asia-Pacific the fastest-growing region?

Aggressive smart-factory investment, rising sovereign-cloud rules and heightened awareness after OT breaches drive a 12.88% CAGR in the region.

How are regulatory mandates influencing spending?

Frameworks such as the EU’s NIS2 and U.S. CMMC require demonstrable controls, prompting immediate upgrades that add 2.8 percentage points to forecast CAGR.

What role does AI play in manufacturing cloud security?

AI-driven autonomous remediation cuts mean time to respond by automating alert triage and isolating compromised equipment within milliseconds, limiting costly downtime.

Are small and medium-sized manufacturers adopting cloud security?

Yes, SMEs are the fastest-growing customer group at 13.74% CAGR, aided by subscription-based platforms and managed service offerings that reduce the need for in-house expertise.

Page last updated on: