Cloud Network Security Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

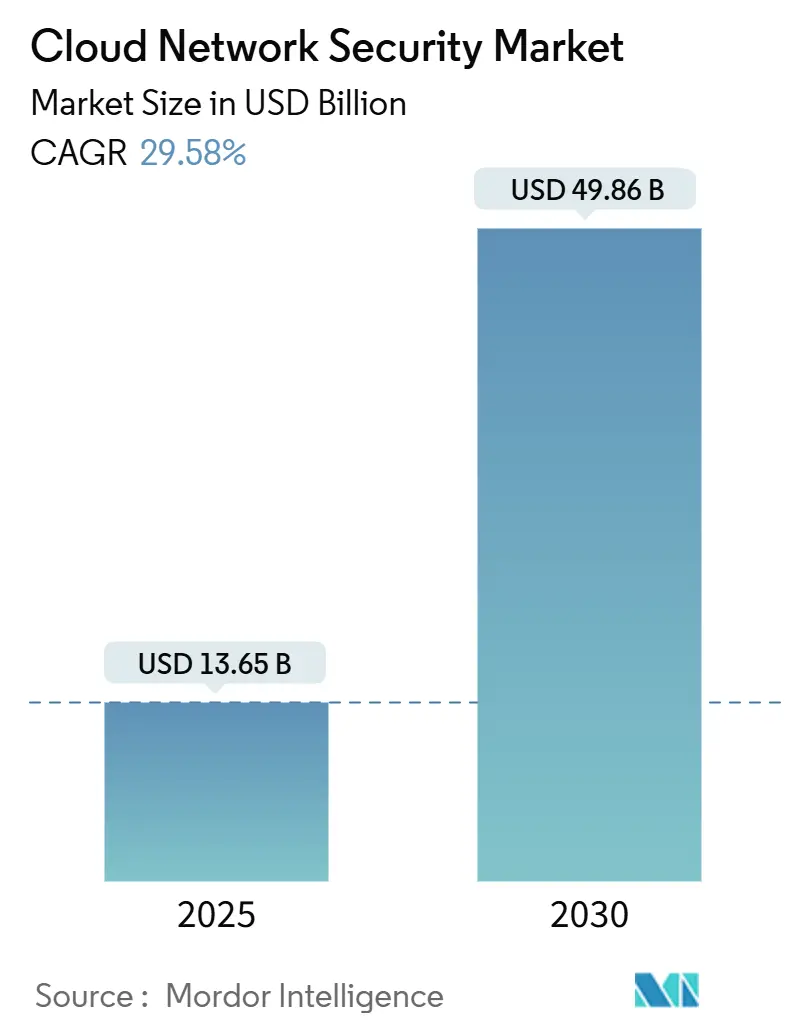

| Market Size (2025) | USD 13.65 Billion |

| Market Size (2030) | USD 49.86 Billion |

| Growth Rate (2025 - 2030) | 29.58% CAGR |

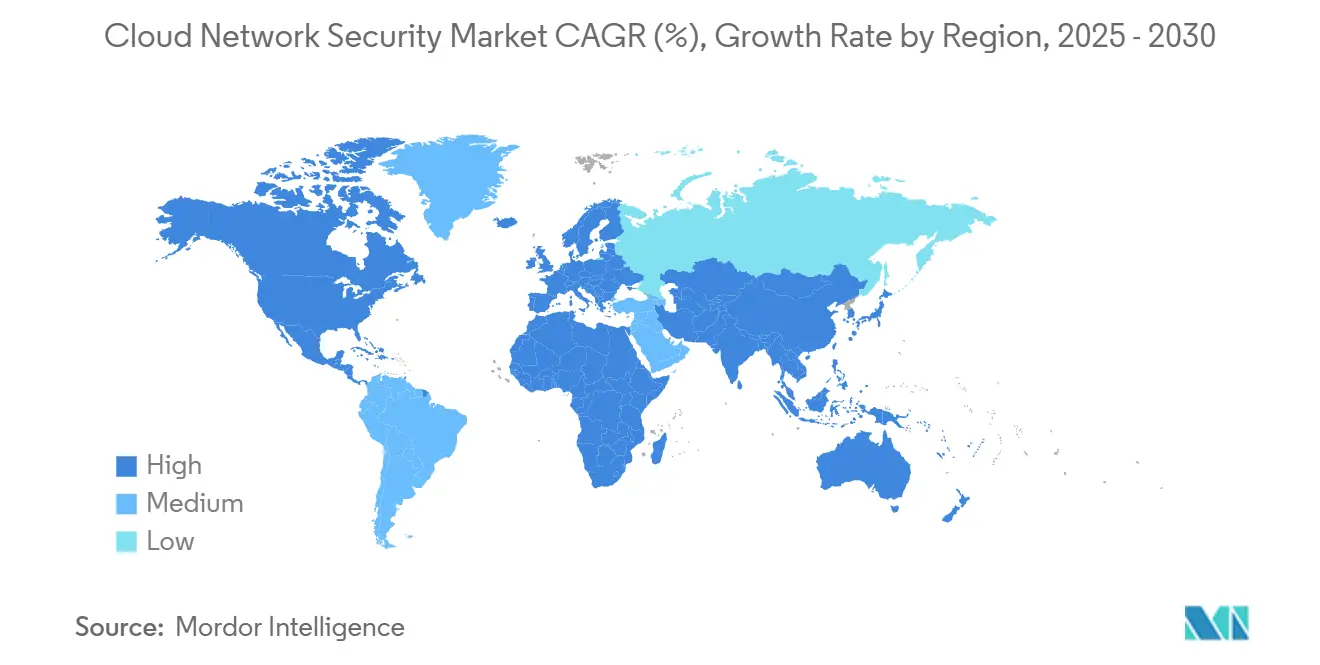

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cloud Network Security Market Analysis by Mordor Intelligence

The Cloud network security market size stood at USD 13.65 billion in 2025 and is forecast to reach USD 49.86 billion by 2030, advancing at a 29.58% CAGR. Strong growth reflects enterprises’ switch from perimeter devices to unified, cloud-native platforms that merge secure access service edge (SASE) designs with zero-trust verification. Heightened ransomware losses projected to lift worldwide cybercrime costs to USD 10.5 trillion in 2025 keep security spending non-discretionary even as FinOps teams curb wider IT budgets. Post-quantum encryption pilots, large language model adoption, and automated policy orchestration are expanding addressable demand across every vertical. Vendor consolidation accelerates because CISOs want integrated controls that reduce tool sprawl, while AI-driven analytics compensate for the 4.8 million-person talent shortfall. Regionally, North America retains early-mover scale, but Asia-Pacific registers the fastest gains thanks to sovereign-cloud mandates, 5G roll-outs, and new data-residency laws.

Key Report Takeaways

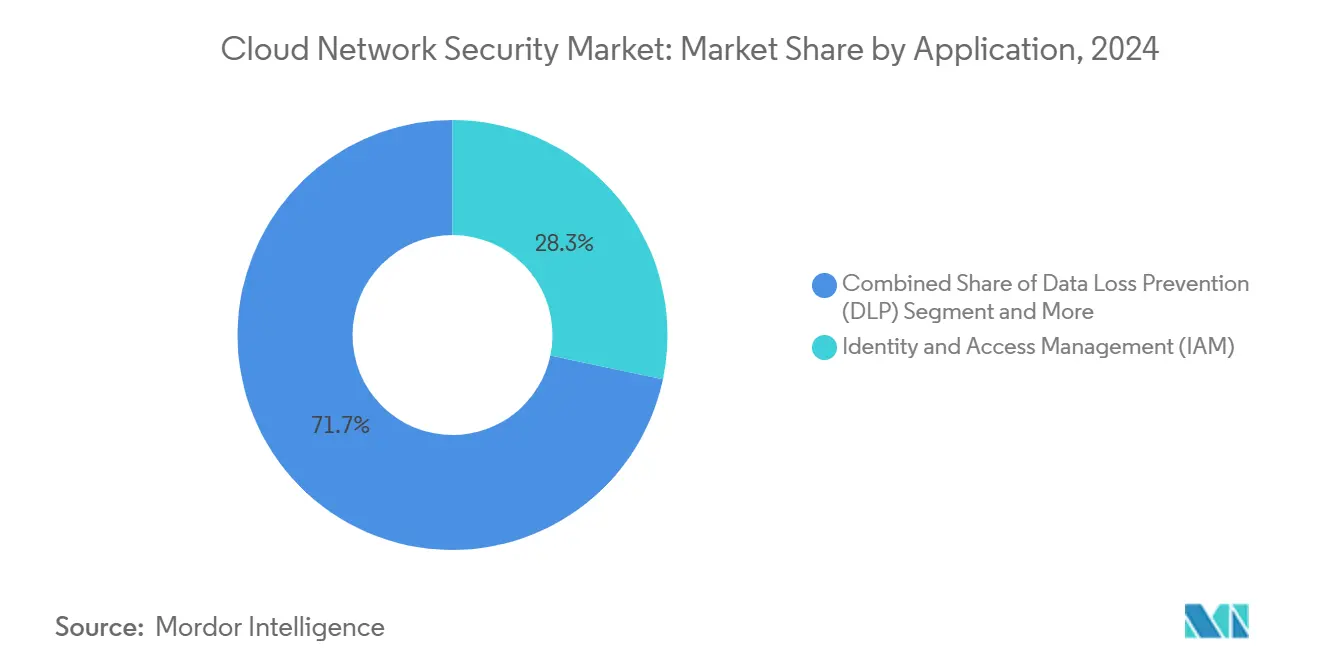

- By application, Identity and Access Management (IAM) led with 28.3% revenue share of the Cloud network security market in 2024, while Cloud Infrastructure Entitlement Management (CIEM) is projected to expand at 34.5% CAGR to 2030.

- By security type, Network Security accounted for 32.4% share of the Cloud network security market size in 2024; Cloud Workload Protection Platform (CWPP) is rising at 31.8% CAGR through 2030.

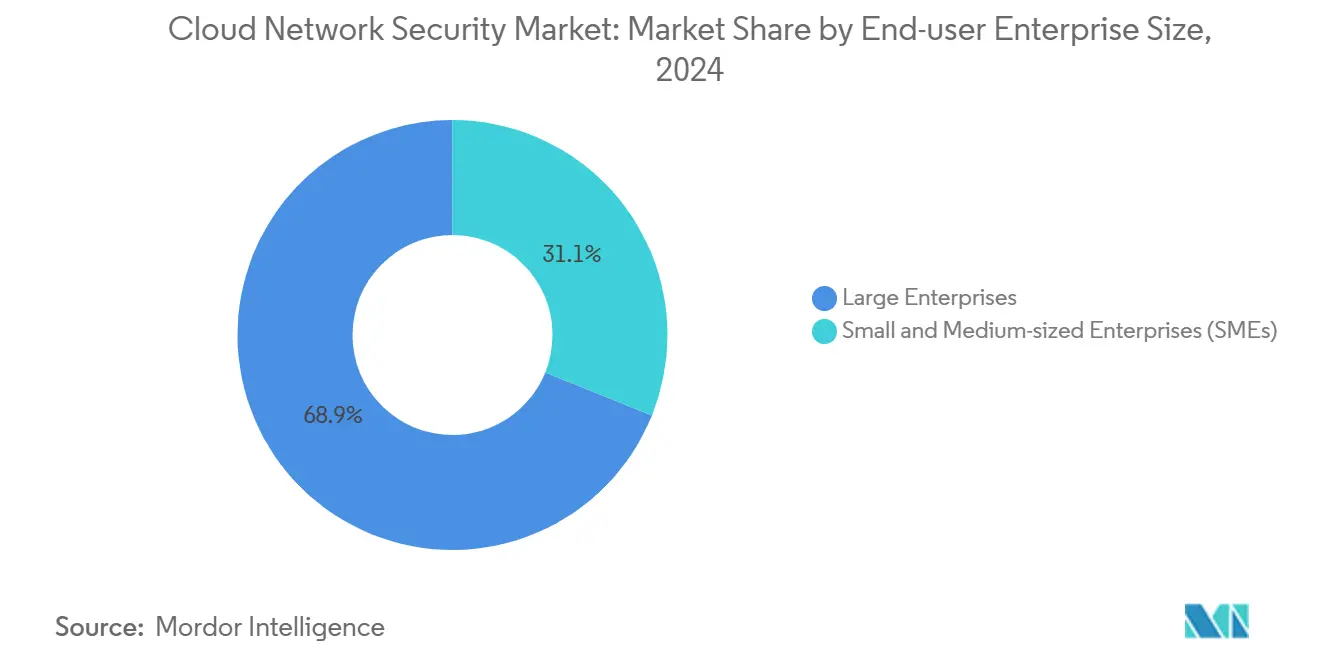

- By organisation size, large enterprises commanded 68.9% share of the Cloud network security market in 2024, and the same segment posts the highest projected 29.8% CAGR to 2030.

- By end-user industry, IT and Telecom held 16.3% revenue share in 2024, whereas retail/e-commerce is forecast to climb at 32.4% CAGR to 2030.

- By geography, North America captured 34.7% of the Cloud network security market size in 2024; Asia-Pacific is set to register the quickest 37.2% CAGR to 2030.

Global Cloud Network Security Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid adoption of cloud services | +8.5% | Global, Asia-pacific strongest | Medium term (2-4 years) |

| Surge in cyber-attacks and ransomware incidents | +7.2% | Global, South America highest growth | Short term (≤2 years) |

| Stringent data-protection regulations | +5.8% | Europe and North America, expanding to Asia-pacific | Long term (≥4 years) |

| BYOD / CYOD and remote-work proliferation | +4.3% | Global, developed markets ahead | Medium term (2-4 years) |

| Convergence of SASE and cloud network security | +6.1% | North America and Europe lead, Asia-pacific follows | Long term (≥4 years) |

| Quantum-resistant encryption investment cycle | +2.8% | Global, finance and government focus | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Rapid adoption of cloud services

Enterprise cloud outlays exceeded USD 825 billion in 2025, and 87% of companies now run workloads on multiple providers. Integration gaps across those environments multiply risk, so buyers prefer platforms that enforce uniform policy and micro-segmentation at scale. Financial institutions typify the urgency: 75% view cloud migration as core to modernisation, yet fewer than 55% consume their committed spending, leaving Asia-Pacific for incremental security roll-outs. SASE roadmaps shorten deployment cycles, while usage-based pricing aligns with FinOps governance. Together these factors heighten demand for elastic controls that track workloads from build to runtime.

Surge in cyber-attacks and ransomware incidents

Groups such as RansomHub, 8Base, and Cl0P weaponise zero-day exploits to evade endpoint detection. Latin America logs 2 569 weekly attacks 40% above the global norm pushing healthcare and government networks beyond legacy defences. Active Directory remains a favoured foothold even after Microsoft’s hardening updates, forcing organisations to adopt AI-enriched detection that predicts lateral movement before privilege escalation.[1]Microsoft Corporation, “Introducing Microsoft Security Copilot,” microsoft.comContinuous threat-intelligence feeds and behavioural analytics therefore shift from optional to baseline capabilities inside every modern bundle of the Cloud network security market.

Stringent data-protection regulations

The EU’s NIS2 directive, effective October 2024, extends mandatory cyber-hygiene to more than 100 000 operators of essential and important services. Fines climb to EUR 10 million or 2% of global turnover for non-compliance, incentivising broader investment in encryption, incident reporting, and supply-chain due diligence.[2]European Commission, “NIS2 Directive: Higher Level of Cybersecurity Across the EU,” ec.europa.euSimilar mandates appear in Canada, Japan, and Saudi Arabia, intensifying cross-border compliance complexity. Vendors that embed policy libraries and audit templates into their consoles gain competitive edge because regulated customers value out-of-the-box alignment.

BYOD / CYOD and remote-work proliferation

After the pandemic normalised hybrid work, 80% of firms formalised BYOD policies and 68% attribute productivity gains to the model. Still, 21% of remote employees working abroad experienced data theft; unencrypted file transfer and password reuse account for most incidents. Endpoint posture assessment, secure browser isolation, and cloud access security broker (CASB) integration now matter as much as traditional next-generation firewalls in the Cloud network security market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-privacy and residency concerns | -4.2% | Europe and Asia-pacific with strict sovereignty rules | Medium term (2-4 years) |

| Multi-cloud complexity and integration overhead | -3.8% | Global, enterprise accounts | Short term (≤2 years) |

| Shortage of cloud-security talent | -2.9% | Global, acute in developed economies | Long term (≥4 years) |

| FinOps budget squeeze on security projects | -3.1% | Global, cost-centric adopters | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data-privacy and residency concerns

Nineteen percent of organisations in Asia-Pacific plan higher sovereign-cloud spending, and 64% of Australian firms evaluate residency strategies, yet sovereign architectures raise cost per protected workload. Europe mirrors the pattern as Schrems II limits pressure cross-border data flows, compelling region-locked deployments that split operational teams. The outcome is fragmented visibility plus duplicate tooling that drags on ROI and slows overall Cloud network security market adoption.

Multi-cloud complexity and integration overhead

Seventy-six percent of enterprises cite confusion created by dozens of point solutions that leave blind spots across AWS, Azure, and Google Cloud IAM constructs. Over-privileged identities, inconsistent RBAC mapping, and API-centric attacks force CISOs to orchestrate third-party connectors that raise total cost of ownership instead of reducing it. Until vendors deliver plug-and-play policy rationalisation, some buyers delay platform refreshes, constraining near-term revenue in the Cloud network security industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: IAM dominance anchors control; CIEM accelerates privileged access governance

Identity and Access Management generated the largest 28.3% slice of the Cloud network security market in 2024 as identity became the de-facto perimeter. Ongoing MFA roll-outs and conditional-access analytics keep IAM a core budget item even for cost-sensitive buyers. IAM suites now extend beyond human users into machine-to-machine secrets management, certificate rotation, and just-in-time entitlement workflows that reduce attack surfaces.

CIEM, rising at a 34.5% CAGR, responds to rampant privilege drift inside multi-cloud estates. Each new SaaS integration multiplies entitlement objects, so security teams seek graph-based engines that baseline least-privilege across tenants. CIEM’s policy simulation and remediation recommendations integrate into CI/CD pipelines, improving DevSecOps velocity. Vendors that combine IAM and CIEM dashboards gain upsell runs inside renewals, reinforcing platform lock-in within the Cloud network security market.

By Security Type: Network protection leads; workload shielding races ahead

Network Security held 32.4% of the Cloud network security market size in 2024 because firewalls, gateways, and segmentation policies remain non-negotiable for compliance audits. However, pure virtual-appliance models now give way to policy-as-code and service-mesh-based enforcement that insert identity headers at the packet level.

CWPP expands 31.8% annually as container and serverless adoption spur demand for runtime kernel telemetry, eBPF-based drift detection, and snapshot isolation. Zero-trust overlay networking merges with CWPP so that micro-services call only authorized APIs. Distributors report higher attach rates when CWPP modules come bundled with intrusion-prevention and vulnerability-scanning features, underpinning cross-sell logic across the Cloud network security market.

By End-User Enterprise Size: Enterprise wallets dominate yet SMEs ride SaaS democratisation

Large corporations contributed 68.9% revenue in 2024 and still chart the swiftest 29.8% CAGR because their migration roadmaps stretch several petabytes of data into SaaS-first models. FedRAMP High, PCI-DSS 4.0, and ISO 27001:2022 updates oblige these firms to unify audit trails across global subsidiaries. Coupled with board-level scrutiny of cyber insurance premiums, the impetus fuels multi-year master-service agreements favoring single-vendor ecosystems.

Small and medium enterprises gain leverage through subscription-based bundles that avoid capex. Low-touch deployment and AI-assisted policy templates offset the acute talent gap impeding in-house security operations. Vendors thus calibrate freemium tiers with auto-scaling sensors to capture volume, converting to advanced analytics add-ons once customer maturity rises broadening exposure to the Cloud network security market.

By End-User: IT and Telecom upfront; retail sprints on digital commerce exposure

IT and Telecom providers retained 16.3% share because their backbone infrastructure and managed-service offerings require airtight guardrails that preserve uptime and trust. Telcos embed inspection engines inside 5G edge nodes, while hyperscale’s wrap DDoS mitigation and zero-trust connectivity into their backbone subscriptions, amplifying cross-tier monetization.

Retail and e-commerce shows the steepest 32.4% CAGR as omnichannel payments elevate personally identifiable information (PII) risk. Tokenization, behavioral biometrics, and real-time fraud scoring anchor cloud-native security portfolios targeting merchants. Public disclosures of high-profile breaches raise executive urgency, sparking alliance with managed detection and response (MDR) partners that specialize in the Cloud network security market.

Geography Analysis

North America continued to lead with a 34.7% revenue share in 2024, powered by USD 13 billion of federal cybersecurity outlays and White House-mandated zero-trust architecture across agencies. Eighty percent of US government cloud buyers already run hybrid estates, while 71% multi-home workloads across two or more public clouds, intensifying demand for aggregated telemetry pipelines. Private-sector enterprises mirror the pattern, channeling compliance dollars into FedRAMP-aligned SaaS that shrink audit cycles. The Cloud network security market therefore benefits from early-mover reference architectures and a mature channel ecosystem.

Asia-Pacific records the quickest 37.2% CAGR through 2030 on the back of sovereign-cloud frameworks, 5G densification, and hyper-scale data-center investments. China alone targets a doubling of cloud spend by 2025, backing 448 operational data centers and USD 9.2 billion in annual infrastructure outlays. At the same time, 31% of global cyber-attacks land in the region, accelerating adoption of in-country security nodes that satisfy residency clauses. Australian organizations trial confidential-computing enclaves, while India promotes Digital Personal Data Protection Act compliance kits bundled into the Cloud network security market.

Europe sustains momentum because the NIS2 regime extends obligations to an extra 150 000 firms, and GDPR penalties underscore that data guardianship is perpetual. Supply-chain risk evaluation now encompasses upstream SaaS vendors, prompting wider uptake of automatic software-bill-of-materials (SBOM) generators within security suites. Meanwhile, the Middle East and Africa project network-security spend topping USD 500 million in 2025, with 12.5% annual growth as governments introduce AI oversight laws. Latin America, facing 2 569 weekly ransomware strikes and USD 4.45 million average breach costs, imports managed SOC Asia-Pacific and pushes encrypted traffic inspection to the cloud edge, advancing readiness across the Cloud network security market.

Competitive Landscape

The Cloud network security market exhibits moderate fragmentation but active consolidation. Palo Alto Networks closed 17 deals worth USD 5.5 billion since 2018 including the purchase of IBM QRadar SaaS assets to deliver a full life-cycle cloud security platform. Microsoft embeds Security Copilot across Azure, processing 84 trillion daily signals that drive continuous model tuning. Fortinet leverages ASIC-accelerated firewalls to link campus networks with zero-trust edge fabric, recently integrating CrowdStrike AI sensors for endpoint-to-firewall telemetry correlation.

Strategic partnerships also reshape rivalries. Zscaler joined NVIDIA to co-engineer generative-AI assistants that parse 400 billion daily transactions for anomaly detection. Cisco and Splunk align observability with threat-intelligence graphs following Cisco’s USD 28 billion acquisition of the analytics vendor, opening bidirectional queries that speed mean-time-to-respond across hybrid clouds.

Emerging challengers differentiate through self-learning AI and quantum-safe cryptography modules. Darktrace, Netskope, and Wiz scale from SMB to enterprise use cases via agentless scans and API hooks. Meanwhile, customer demand for managed security services creates co-sell motions between telcos and software firms, adding another distribution lever inside the Cloud network security market.

Cloud Network Security Industry Leaders

Palo Alto Networks Inc.

Fortinet Inc.

Cisco Systems Inc.

Microsoft Corporation

Netskope Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Zscaler partnered with NVIDIA to launch ZDX Copilot, combining generative AI with Zscaler’s Zero Trust Exchange that already processes 400 billion daily transactions.

- April 2025: IBM closed its USD 6.4 billion all-cash takeover of HashiCorp, integrating Terraform and Vault into IBM Hybrid Cloud Management.

- March 2025: Google signed an agreement to buy Wiz for USD 32 billion, strengthening Google Cloud’s security posture management across AI and multi-cloud estates.

- February 2025: Fortinet announced the acquisition of Lacework, adding an AI-powered CNAPP with nearly 1000 customers to Fortinet Security Fabric.

Global Cloud Network Security Market Report Scope

The Cloud Network Security Market Report Is Segmented by Application (Identity and Access Management (IAM), Data Loss Prevention (DLP), Security Information and Event Management (SIEM), and Other Applications), Security Type (Network Security, Application Security, Database Security, Web and Email Security, Cloud Workload Protection, and Encryption and Tokenization), End-User Enterprise Size (Large Enterprises and Small and Medium Enterprises (SMEs)), End-User (BFSI, Healthcare and Life Sciences, Retail and Consumer Services, Manufacturing, Transport and Logistics, IT and Telecom, Government and Public Sector, and Other End Users), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts Are Provided in Terms of Value (USD).

| Identity and Access Management (IAM) |

| Data Loss Prevention (DLP) |

| Security Information and Event Management (SIEM) |

| Others |

| Network Security |

| Application Security |

| Database Security |

| Web and Email Security |

| Cloud Workload Protection |

| Encryption and Tokenization |

| Large Enterprises |

| Small and Medium Enterprises |

| BFSI |

| Healthcare and Life Sciences |

| Retail and Consumer Services |

| Manufacturing |

| Transport and Logistics |

| IT and Telecom |

| Government and Public Sector |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

| By Application | Identity and Access Management (IAM) | ||

| Data Loss Prevention (DLP) | |||

| Security Information and Event Management (SIEM) | |||

| Others | |||

| By Security Type | Network Security | ||

| Application Security | |||

| Database Security | |||

| Web and Email Security | |||

| Cloud Workload Protection | |||

| Encryption and Tokenization | |||

| By End-User Enterprise Size | Large Enterprises | ||

| Small and Medium Enterprises | |||

| By End-User | BFSI | ||

| Healthcare and Life Sciences | |||

| Retail and Consumer Services | |||

| Manufacturing | |||

| Transport and Logistics | |||

| IT and Telecom | |||

| Government and Public Sector | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Colombia | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Kenya | |||

| Rest of Africa | |||

Key Questions Answered in the Report

Which application segment holds the largest share?

Identity and Access Management leads with 28.3% revenue share of the Cloud network security market in 2024, reflecting identity’s role as the new perimeter.

Which region is growing fastest?

Asia-Pacific records the highest 37.2% CAGR through 2030, driven by sovereign-cloud mandates and rapid digitisation across emerging economies.

Who are the key players in the Cloud network security industry?

Who are the key players in the Cloud network security industry?

What is driving investment in quantum-resistant encryption?

Organisations aim to safeguard long-lived data against future quantum attacks, prompting early adoption of post-quantum cryptography inside cloud-native platforms.

Page last updated on: