Australia And New Zealand Cloud Computing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

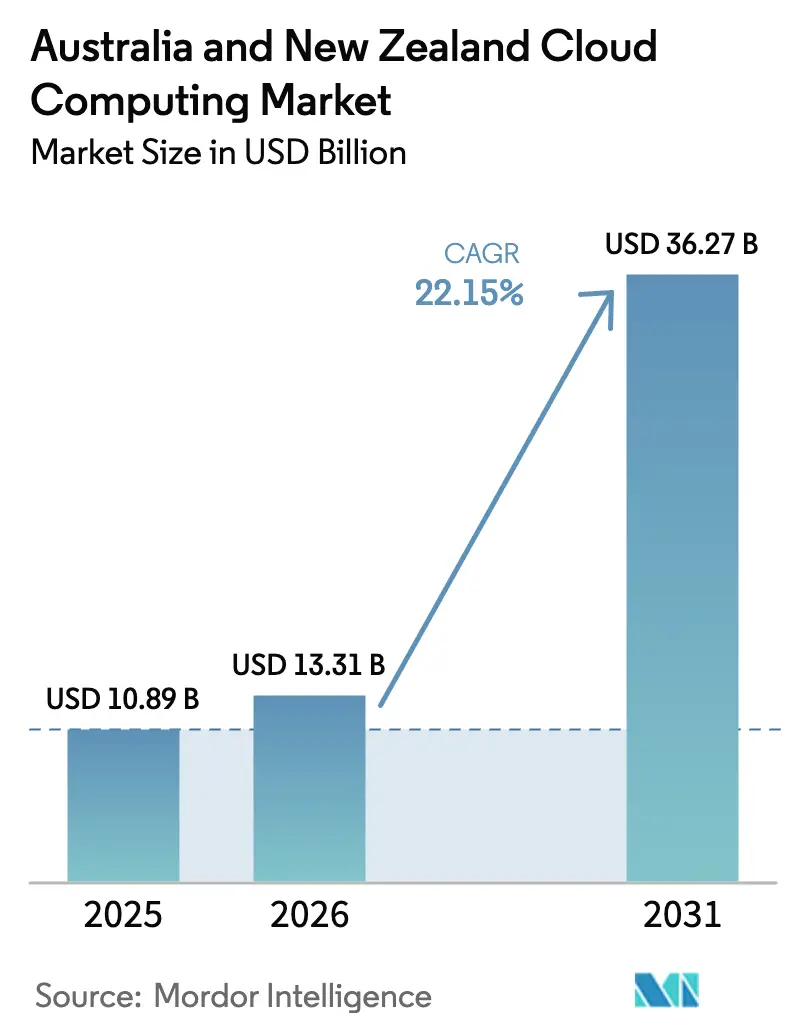

| Base Year Market Size (2025) | USD 10.89 Billion |

| Market Size (2026) | USD 13.31 Billion |

| Market Size (2031) | USD 36.27 Billion |

| Growth Rate (2026 - 2031) | 22.15% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Australia And New Zealand Cloud Computing Market Analysis by Mordor Intelligence

The Australia and New Zealand cloud computing market size in 2026 is estimated at USD 13.31 billion, growing from 2025 value of USD 10.89 billion with 2031 projections showing USD 36.27 billion, growing at 22.15% CAGR over 2026-2031. Momentum in the Australia and New Zealand cloud computing market is gathering pace as sovereign-cloud strategies, AI workload optimization, and edge-cloud convergence become mainstream across mining and agriculture operations. Regulatory mandates on data residency under Australia’s Cyber Security Act 2024 and New Zealand’s Customer and Product Data Bill have reinforced the demand for locally hosted hyperscale capacity that meets compliance requirements while retaining global performance advantages. Enterprises in the Australia and New Zealand cloud computing market are also accelerating platform modernization through containerized architectures that shorten release cycles, while rising carbon-neutral commitments are steering investments toward renewable-powered data centers. Over the forecast horizon, the rebalancing of public, hybrid, and edge deployments is expected to shape spending patterns as organizations look to combine hyperscale elasticity, local sovereignty, and sub-50-millisecond latency for mission-critical workloads.

Key Report Takeaways

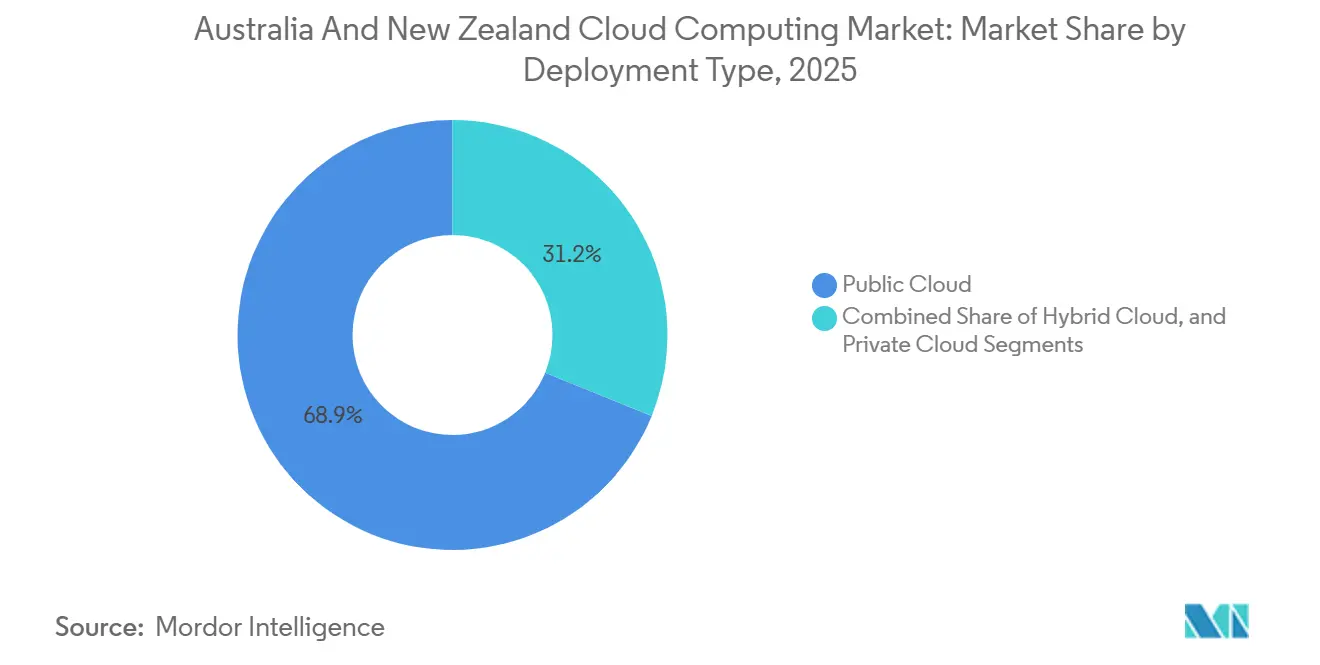

- By deployment type, public cloud captured 68.85% of the Australia and New Zealand cloud computing market share in 2025, while hybrid cloud is expanding at a 22.40% CAGR during 2026-2031.

- By service model, software as a service led with a 46.75% revenue share in 2025; platform as a service is advancing at a 24.89% CAGR through 2031.

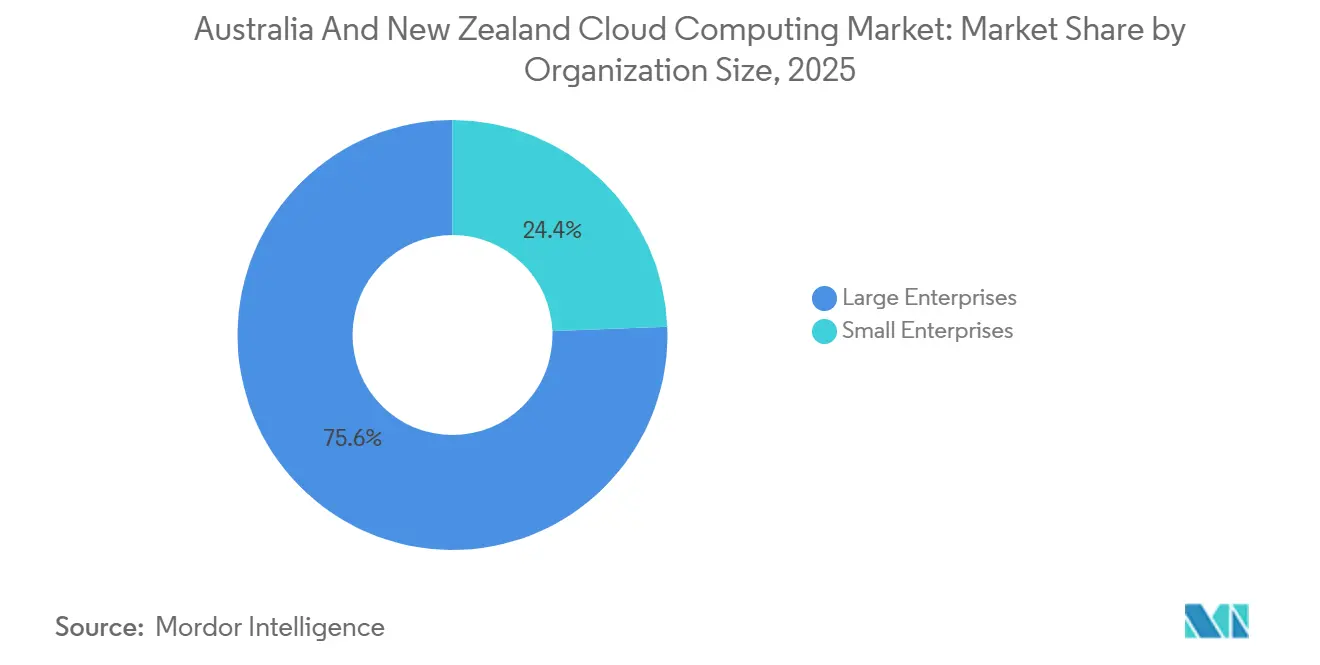

- By organization size, large enterprises represented 75.62% of the Australian and New Zealand cloud computing market size in 2025; however, small and medium-sized enterprises are expected to grow at a 23.42% CAGR to 2031.

- By end-user industry, banking, financial services, and insurance held a 20.88% revenue share in 2025, whereas the healthcare sector is forecast to post a 22.76% CAGR from 2025 to 2031.

- By geography, Australia accounted for 78.92% of the 2025 revenue, while New Zealand is projected to grow at a 24.98% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Australia And New Zealand Cloud Computing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated adoption of cloud-native technologies | +4.2% | Australia and New Zealand, with concentrations in Sydney, Melbourne, and Auckland | Medium term (2-4 years) |

| Surge in enterprise demand for flexible IT infrastructure | +3.8% | Australia and New Zealand are, strongest in the BFSI and healthcare sectors. | Short term (≤ 2 years) |

| Heightened government digital transformation programs | +3.5% | Australia and New Zealand, national initiatives with early gains in Canberra, Wellington | Medium term (2-4 years) |

| AI-driven workload optimization in public cloud platforms | +4.5% | Australia and New Zealand, led by hyperscaler regions in Sydney, Melbourne. | Long term (≥ 4 years) |

| Edge-cloud convergence for remote mining and agriculture sites | +2.9% | Australia (Western Australia, Queensland, Northern Territory) and New Zealand (rural regions) | Long term (≥ 4 years) |

| Rising carbon-offset mandates promoting green data centres | +2.4% | Australia and New Zealand, driven by Climate Active and net-zero commitments. | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerated Adoption of Cloud-Native Technologies

Enterprises are decomposing monolithic systems into microservices to gain portability, reduce vendor lock-in, and meet audit controls under APRA CPS 234, increasing overall velocity in the Australia and New Zealand cloud computing market.[1]Australian Prudential Regulation Authority, “Prudential Standard CPS 234 Information Security,” Australian Prudential Regulation Authority, apra.gov.au Major banks refactored their payment platforms on container stacks, which cut latency by 30% and enabled real-time fraud monitoring. Managed Kubernetes services from global providers now mask cluster complexity, bringing 94% of Australian SMEs into the cloud in 2025, up from 78% two years earlier. The result is shorter development sprints, more frequent feature drops, and faster time-to-value for digital products. As organizations target multi-cloud resilience, service-mesh overlays are emerging as standard blueprints for secure east-west traffic management across distributed workloads.

Surge in Enterprise Demand for Flexible IT Infrastructure

Hybrid adoption continues to swell as 72% of organizations orchestrate regulated data on-premises or in sovereign facilities while bursting variable workloads to public regions.[2]IBM Corporation, “Hybrid Cloud Adoption in Australia,” ibm.com Financial institutions exemplify this pattern, anchoring core ledgers in IRAP-certified sites while leveraging public-cloud analytics for enhanced customer insights. Government policies that classify PROTECTED data force agencies to blend private and public footprints, reinforcing hybrid as the default in the Australia and New Zealand cloud computing market. Terraform and Ansible scripts abstract infrastructure differences, enabling workload mobility and real-time cost comparison. Over time, organizations plan to shift 15-25% of total workloads between providers each year to optimize price-performance profiles.

Heightened Government Digital Transformation Programs

Australia’s myGov and New Zealand’s Te Whatu Ora migrations demonstrate how cloud-first mandates accelerate modernization.[3]New Zealand Government, “Digital Strategy for Aotearoa,” New Zealand Government, digital.govt.nz Funding pools exceeding USD 720 million in New Zealand, along with associated compliance frameworks such as ISO 27001, have raised the bar for security and observability. Consolidating fragmented legacy estates into unified cloud backbones supports seamless citizen services, reduces infrastructure overhead by up to 40%, and future-proofs applications for AI integration. Vendors holding continuous-monitoring certifications gain procurement preference, spurring competition among sovereign and hyperscale providers.

AI-Driven Workload Optimization in Public Cloud Platforms

The adoption of generative AI is driving demand for GPU-dense instances and custom accelerators in every major cloud region. The local launch of AWS Trainium2 chips and Google TPUs reduces training costs by approximately 30%, enabling enterprises to fine-tune large language models on domestic datasets without incurring cross-border transfer penalties. Healthcare systems utilize cloud-hosted AI to reduce diagnostic turnaround times by half, and agricultural players analyze sensor data in near real-time. Auto-scaling ML pipelines and built-in hyper-parameter tuning democratize advanced analytics, particularly for smaller organizations that lack in-house data science teams.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating data privacy and sovereignty concerns | -2.8% | Australia and New Zealand have seen heightened activity in the government and BFSI sectors. | Short term (≤ 2 years) |

| Limited cloud skills talent pool in regional areas | -2.1% | Australia (regional Queensland, Tasmania, Northern Territory) and New Zealand (South Island) | Medium term (2-4 years) |

| High egress costs are hindering multi-cloud portability | -1.6% | Australia and New Zealand, affecting enterprises with multi-cloud strategies | Medium term (2-4 years) |

| Supply-chain volatility in semiconductor and server hardware | -1.9% | Australia and New Zealand, impacting data centre expansion timelines | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Escalating Data Privacy and Sovereignty Concerns

Mandatory ransomware incident reporting and restrictions on offshore transfers under recent legislation compel enterprises to keep sensitive workloads within national borders, thereby inflating architectural complexity. Surveys reveal that 74% of Australians distrust foreign data storage, directing attention to sovereign vendors who must still mirror hyperscale economics. In New Zealand, proposed rules banning transfers where equivalent safeguards do not exist raise uncertainty for backup and disaster-recovery designs that once relied on Singapore or the United States. Compliance spends now add 15-25% to cloud project budgets in the Australia and New Zealand cloud computing market, nudging firms toward multi-region redundancy and more sophisticated encryption schemes.

Limited Cloud Skills Talent Pool in Regional Areas

Tech Council projections indicate a 200,000-person technology shortfall in Australia by 2030, with cloud computing identified as one of the most acute gaps.[4]Tech Council of Australia, “Getting to 1.2 Million Tech Jobs by 2030,” techcouncil.com.au Despite scholarship initiatives, only a fraction of graduates reach advanced certification levels each year. Regional enterprises pay salary premiums or contract managed-service providers, adding unplanned operational costs and occasionally stalling migration schedules. Programs like AWS re/Start, while promising, graduate fewer than 200 participants per year in New Zealand, insufficient to close a 5,000-vacancy gap. Over the medium term, unfilled roles could cap the growth trajectory of the Australia and New Zealand cloud computing market outside capital cities.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Type: Hybrid Cloud Gains as Sovereignty Concerns Mount

Hybrid architectures represent the fastest-growing model with a 22.40% CAGR through 2031, underscoring how compliance rules drive enterprises to split workloads between sovereign and public environments. Although public cloud controlled 68.85% of revenue in 2025, risk mitigation is prompting a deliberate reallocation of applications across multiple venues. The Australia and New Zealand cloud computing market size for hybrid solutions is forecast to more than triple by the end of the decade as banks place ledgers in IRAP-certified data halls while leveraging hyperscalers for machine-learning inference bursts. Progressive miners are running edge nodes at remote pits that synchronize via service meshes to public regions for broader analytics.

Hybrid adoption offers pay-as-you-grow scalability while preserving data integrity in accordance with national cybersecurity frameworks, making it an attractive option across industries seeking cost efficiency without compromising on regulatory compliance. Vendors differentiate themselves through cross-platform orchestration, with Terraform blueprints and Federated Kubernetes clusters enabling seamless workload redeployment. As Local Zones emerge in Perth and Adelaide, latency benefits further validate hybrid strategies for autonomous haulage and defense simulations, strengthening the commercial case in the Australia and New Zealand cloud computing market.

By Service Model: Platform Services Accelerate Developer Velocity

Platform as a service outpaces other layers with a 24.89% CAGR, driven by the need to abstract infrastructure management and shorten release cycles. While software as a service (SaaS) accounted for 46.75% of spending in 2025, organizations are increasingly leveraging fully managed Kubernetes platforms and AI services that embed auto-scaling, security patching, and observability, thereby freeing internal teams to focus on code development. The Australia and New Zealand cloud computing market share for PaaS is set to rise as banks adopt Red Hat OpenShift clusters for regulated workloads and retailers deploy Vertex AI pipelines for recommendation engines.

As more enterprises pivot to event-driven architecture, PaaS offers serverless runtime environments that charge solely for resource consumption, enhancing cost predictability. Hyper-automation capabilities embedded within PaaS stacks deliver built-in CI/CD pipelines and policy-as-code guardrails, further lowering barriers for SMEs. Aggregate demand signals that PaaS will occupy a larger slice of the Australia and New Zealand cloud computing market by 2031, establishing it as the developer platform of choice for innovation-oriented firms.

By Organization Size: Small Enterprises Embrace Consumption-Based Pricing

Consumption-based economics underpin SME adoption, propelling a 23.42% CAGR as small businesses pivot from capital-intensive servers to cloud-native stacks. At the same time, large enterprises claimed 75.62% of the 2025 revenue. Incentive programs, such as AWS SME Accelerate and New Zealand’s cloud voucher scheme, level the playing field by offsetting migration fees. Flexible billing aligns opex with revenue cycles, a critical lifeline for startups navigating volatile demand in the Australia and New Zealand cloud computing market.

Nevertheless, SMEs face skill shortages and integration challenges when linking cloud platforms to legacy software. Managed service providers plug gaps through fixed-price migration bundles, yet markups can erode anticipated savings. Over time, widespread availability of no-code automation tools and vertical SaaS applications is expected to narrow capability gaps, allowing smaller firms to capture greater value within the Australia and New Zealand cloud computing market.

By End-User Industry: Healthcare Leads Growth Amid Digital Health Transformation

Healthcare usage is rising at a 22.76% CAGR as electronic health record projects and telehealth consultations scale nationwide. National initiatives expanded cloud backbones supporting My Health Record for 16 million citizens, enabling real-time data sharing among providers and pharmacies. Hospitals deploy AI-enabled imaging workloads that cut diagnostic cycles by half, illustrating life-or-death advantages of low-latency cloud capacity. BFSI still commands 20.88% of spending, with open banking APIs driving modernization of core ledgers and payment rails.

Growing reliance on analytics, personalized medicine, and data-driven clinical pathways will sustain momentum in the Australian and New Zealand cloud computing market. Privacy obligations are stringent, however, dictating sovereign hosting and end-to-end encryption. Vendors that combine IRAP-aligned infrastructure with HIPAA-equivalent controls are poised to benefit as digital health ecosystems continue to proliferate.

Geography Analysis

Australia accounted for 78.92% of 2025 revenue, buoyed by large enterprise footprints and multi-billion-dollar hyperscale investments. Australia’s dominance is rooted in its deep hyperscale infrastructure and mature enterprise demand. Microsoft, Amazon, and Google collectively operate dozens of zones, host GPU-dense clusters, and plan Local Zones to push compute closer to Western Australia’s mining corridor. Sovereign specialist NEXTDC will add 150 MW of IT load by 2027 in its Sydney S4 site, ensuring IRAP-aligned capacity for sensitive government workloads. At the policy level, federal agencies must evaluate cloud-first approaches while ensuring that data at the PROTECTED level or higher remains onshore, thereby reinforcing national data-center builds.

New Zealand, although smaller, is registering a 24.98% CAGR, thanks to its cloud-first procurement stance and domestic sovereign providers like Catalyst Cloud. New Zealand’s outsize growth projection stems from Digital Strategy 2.0, which earmarks USD 720 million to modernize public-sector IT and mandates cloud-native designs unless justified by risk assessments. Catalyst Cloud’s expansion and Oracle’s presence in the Auckland region create local options for industries bound by strict residency requirements. Spark’s bundled managed services and private connectivity address the talent shortage by simplifying onboarding and operations, thereby further strengthening uptake.

Edge-cloud convergence is reshaping the topologies of rural deployments. Zella DC built an Outback Edge site in Western Australia to host AI pipelines for autonomous haulage, meeting latency requirements of under 50 ms. Additionally, Telstra’s 5G-embedded edge nodes reduce backhaul costs for IoT analytics. In New Zealand, precision farming initiatives synchronize soil sensor output with cloud AI platforms, enabling per-hectare irrigation optimization.

Competitive Landscape

Amazon Web Services, Microsoft Azure, and Google Cloud capture a prominent share of infrastructure-as-a-service revenue, giving the market a moderately concentrated profile. Their dominance rests on deep capital commitments and integrated AI toolchains that anchor customers in proprietary ecosystems. Amazon Web Services has launched Local Zones in Perth and Adelaide to secure latency-sensitive workloads for mining and defense, expanding its regional footprint beyond the Sydney and Melbourne hubs. Microsoft committed AUD 5 billion to expand from 20 to 29 availability zones by 2026 and introduced Azure AI Studio in the Australia East region, enabling enterprises to deploy generative AI models in accordance with local data-residency rules. Google Cloud has doubled its capacity in the Sydney region and deployed Tensor Processing Units to lower model-training costs, a move that appeals to startups and research institutions pursuing advanced analytics.

A parallel competitive tier has emerged around sovereign cloud services that meet stringent certification thresholds for classified and regulated data. AUCloud achieved Certified Strategic status and, in 2025, secured an AUD 200 million contract to host Australian Department of Defence workloads at the SECRET level, underscoring its position as the go-to provider for government agencies. Macquarie Telecom opened the IC3 Super West facility in Canberra and acquired Symbio Holdings to combine cloud and unified-communications offerings that target public-sector and critical-infrastructure clients. NEXTDC’s S4 Sydney data center will add 150 MW of IT load by 2027, supplying IRAP-aligned capacity for federal workloads and private enterprises seeking sovereign hosting. In New Zealand, Catalyst Cloud expanded its OpenStack environment with NVIDIA GPU instances, capturing research grants tied to the Digital Strategy 2.0 program.

Competition is also intensifying at the edge and in green-energy sourcing. Oracle’s Alloy framework enables partners, such as TEAM Cloud, to white-label Oracle Cloud Infrastructure in sovereign regions, adding fresh capacity without the overhead typically associated with hyperscalers. VMware and Macquarie Telecom have introduced a Sovereign Cloud offering that combines VMware Cloud Foundation with IRAP-certified facilities, addressing the needs for workload repatriation and data localization. Telstra and Google Cloud committed AUD 1 billion to embed distributed cloud nodes across Telstra’s 5G network, positioning telcos as critical enablers of sub-50-millisecond compute for autonomous systems. Providers are racing to verify carbon neutrality, with Equinix sourcing 100% renewables for its new SY6 site and NEXTDC earning Climate Active certification in Melbourne, signaling that sustainability has become a core differentiator alongside price and performance.

Australia And New Zealand Cloud Computing Industry Leaders

Microsoft Corporation

Amazon Web Services (AWS)

Google LLC (Alphabet Inc.)

IBM Corporation

Oracle Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Google Cloud expanded the Sydney region with three new availability zones and deployed Tensor Processing Units to support local AI workloads.

- October 2025: NEXTDC completed phase one of its M3 Melbourne expansion, adding 30 MW and receiving Climate Active carbon-neutral certification.

- September 2025: Microsoft Azure rolled out AI Studio in Australia East, with Commonwealth Bank adopting the platform for chatbot services.

- August 2025: Oracle opened its first Auckland cloud region featuring three availability zones to serve data-residency-sensitive industries.

Australia And New Zealand Cloud Computing Market Report Scope

The Australia and New Zealand Cloud Computing Market Report is Segmented by Deployment Type (Public Cloud, Private Cloud, Hybrid Cloud), Service Model (Infrastructure as a Service, Platform as a Service, Software as a Service), Organization Size (Small and Medium Enterprises, Large Enterprises), End-user Industry (Manufacturing, Education, Retail, Transportation and Logistics, Healthcare, Banking Financial Services and Insurance, Telecom and Information Technology, Government and Public Sector, Utilities, Media and Entertainment, Other End-user Industries), and Geography (Australia, New Zealand). The Market Forecasts are Provided in Terms of Value (USD).

| Public Cloud |

| Private Cloud |

| Hybrid Cloud |

| Infrastructure as a Service (IaaS) |

| Platform as a Service (PaaS) |

| Software as a Service (SaaS) |

| Small and Medium Enterprises |

| Large Enterprises |

| Manufacturing |

| Education |

| Retail |

| Transportation and Logistics |

| Healthcare |

| Banking, Financial Services, and Insurance (BFSI) |

| Telecom and Information Technology |

| Government and Public Sector |

| Utilities |

| Media and Entertainment |

| Other End-user Industries |

| Australia |

| New Zealand |

| By Deployment Type | Public Cloud |

| Private Cloud | |

| Hybrid Cloud | |

| By Service Model | Infrastructure as a Service (IaaS) |

| Platform as a Service (PaaS) | |

| Software as a Service (SaaS) | |

| By Organization Size | Small and Medium Enterprises |

| Large Enterprises | |

| By End-user Industry | Manufacturing |

| Education | |

| Retail | |

| Transportation and Logistics | |

| Healthcare | |

| Banking, Financial Services, and Insurance (BFSI) | |

| Telecom and Information Technology | |

| Government and Public Sector | |

| Utilities | |

| Media and Entertainment | |

| Other End-user Industries | |

| By Country | Australia |

| New Zealand |

Key Questions Answered in the Report

How fast is spending on cloud services growing in Australia and New Zealand?

The Australia and New Zealand cloud computing market is forecast to expand at a 22.15% CAGR from 2026 to 2031, rising from USD 13.31 billion to USD 36.27 billion.

Which deployment model is gaining the most traction?

The hybrid cloud is the fastest-growing model, with a 22.40% CAGR through 2031, blending on-premises sovereignty with public-cloud elasticity.

What drives healthcare adoption of cloud platforms?

Electronic health record rollouts, telehealth expansion, and AI-driven diagnostics are propelling the growth of healthcare, which is expected to grow at a 22.76% CAGR through 2031.

Why is New Zealand growing faster than Australia?

Government cloud-first mandates, local sovereign providers, and forthcoming hyperscale regions are lifting New Zealand’s CAGR to 24.98% through 2031.

What are the main barriers to wider cloud migration?

Data-sovereignty regulations, limited regional talent, high egress fees, and hardware supply-chain risks are the primary restraints.

Which companies dominate the competitive landscape?

Amazon Web Services, Microsoft Azure, and Google Cloud collectively account for roughly 80% of IaaS revenue, with AUCloud, Macquarie Telecom, NEXTDC, and Catalyst Cloud holding key sovereign niches.

Page last updated on: