Market Overview

| Study Period | 2020 - 2031 |

|---|---|

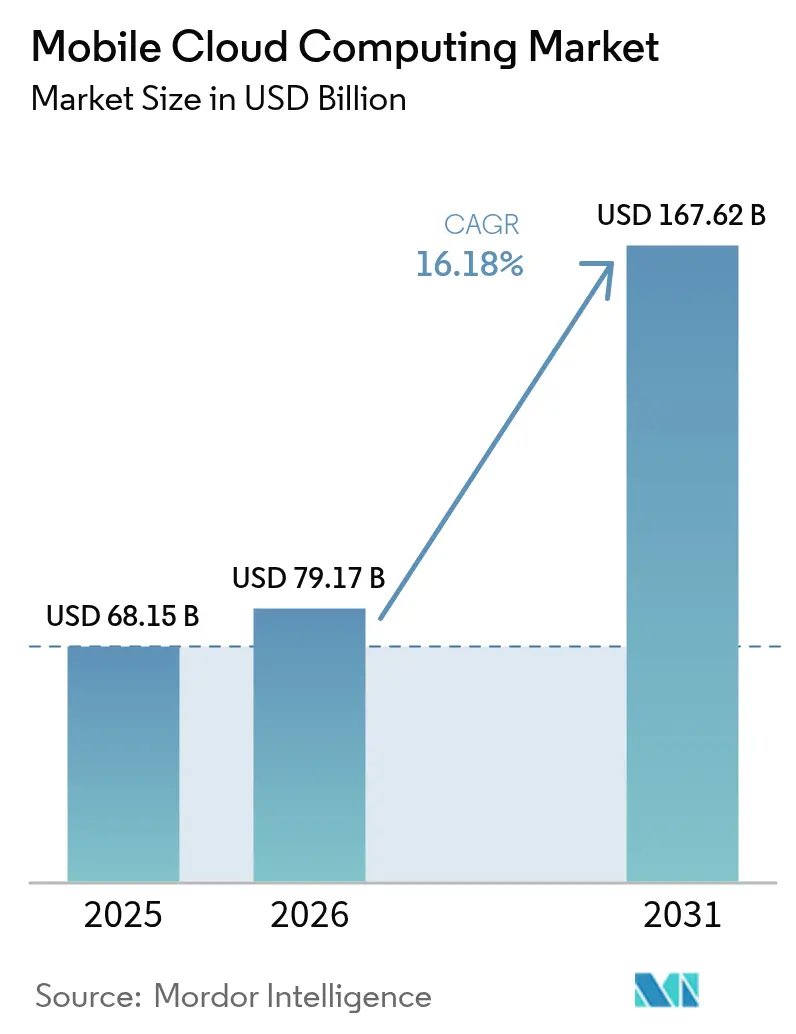

| Market Size (2026) | USD 79.17 Billion |

| Market Size (2031) | USD 167.62 Billion |

| Growth Rate (2026 - 2031) | 16.18% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

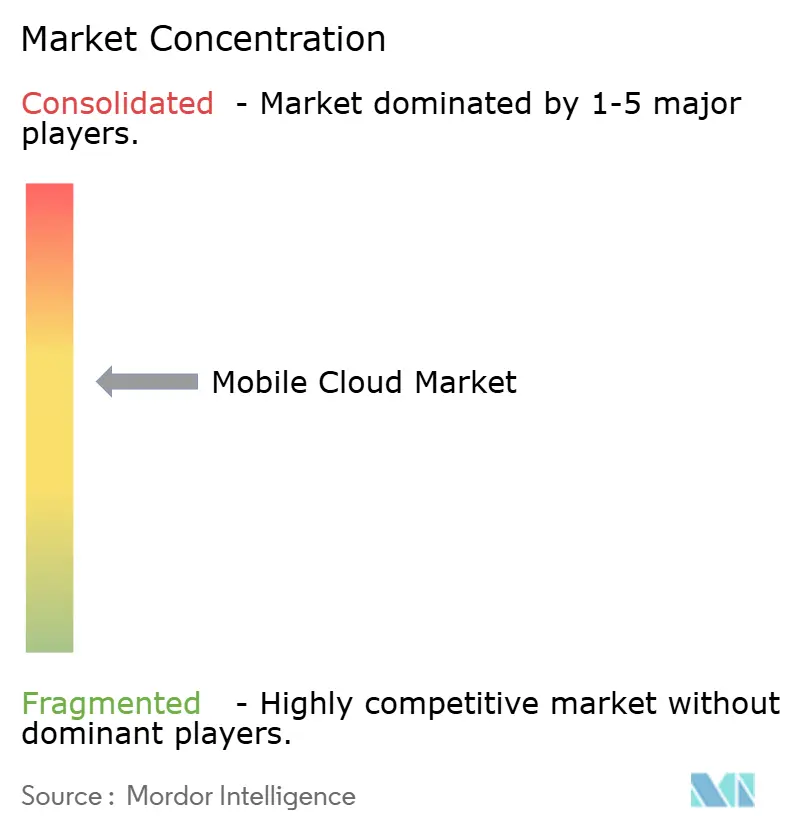

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mobile Cloud Computing Market Analysis by Mordor Intelligence

The mobile cloud computing market size was valued at USD 68.15 billion in 2025 and estimated to grow from USD 79.17 billion in 2026 to reach USD 167.62 billion by 2031, at a CAGR of 16.18% during the forecast period (2026-2031). Falling 5G latency, ubiquitous low-code platforms, and developer demand for scalable back-ends pull new workloads into the cloud, while edge AI orchestration sends only heavy inference and model-training tasks to hyperscale clusters, keeping response time near on-device speeds. Public cloud still dominates volumes, yet regulated industries are pivoting toward hybrid topologies that pair sovereign data centers with elastic hyperscaler zones, preserving compliance without sacrificing agility. Competitive intensity remains elevated as providers differentiate on gaming-grade latency, egress-fee transparency, and vertical bundles for healthcare, banking, and industrial IoT. Near-term demand spikes center on multiplayer cloud gaming, tele-diagnostic imaging, and real-time language translation, each signaling how user experience becomes hardware-agnostic once compute lifts into the cloud continuum.

Key Report Takeaways

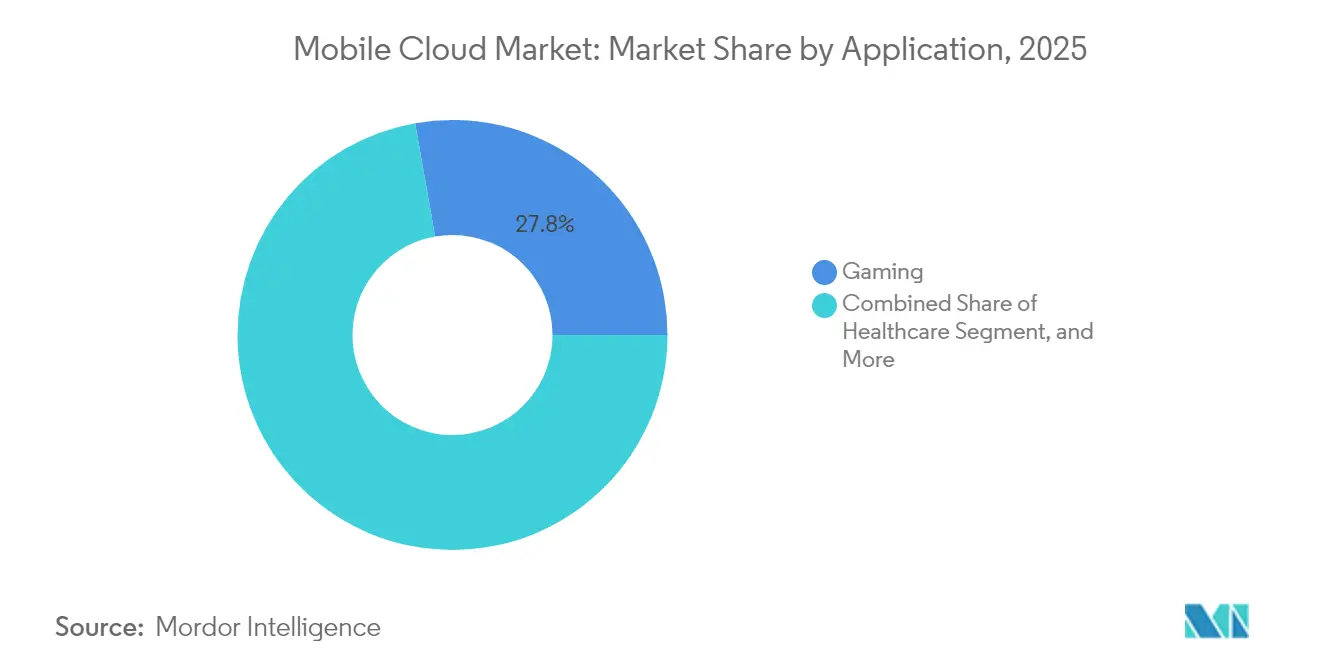

- By application, gaming led with 27.78% revenue share in 2025, while healthcare is projected to grow at a 17.12% CAGR through 2031.

- By user, the enterprise segment held 70.55% of the mobile cloud computing market share in 2025, and the consumer segment is expanding at an 17.95% CAGR to 2031.

- By service model, Software-as-a-Service accounted for 63.60% share of the mobile cloud computing market size in 2025, whereas Platform-as-a-Service is rising at a 16.44% CAGR between 2026 and 2031.

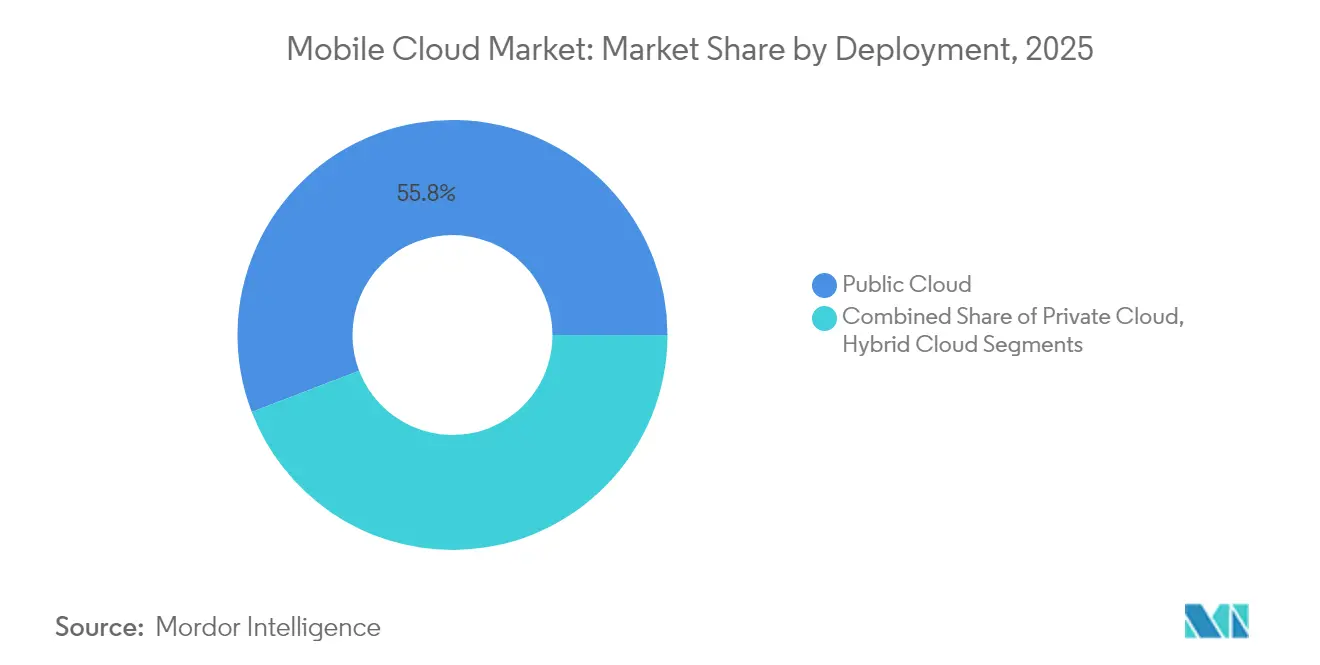

- By deployment, public cloud remained dominant with 55.82% share in 2025, yet hybrid cloud is advancing at a 17.38% CAGR to 2031.

- By mobile operating system, Android devices captured 71.10% revenue share in 2025, and iOS users generated higher average spend per subscriber.

- By geography, North America generated 36.25%% of 2025 revenue, yet Asia-Pacific is poised to grow at a 16.65%% CAGR over the forecast window.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Mobile Cloud Computing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Development in IT Infrastructure in Emerging Countries | +2.8% | Asia Pacific, Middle East, Africa, South America | Medium term (2-4 years) |

| Advancing Internet Connectivity | +3.1% | Global, stronger in Asia Pacific and Africa | Short term (≤ 2 years) |

| Growing Adoption of Edge AI for Mobile Applications | +2.5% | North America, Europe, Asia Pacific core markets | Medium term (2-4 years) |

| Rising Usage of Cloud Gaming Platforms | +1.9% | North America, Europe, Asia Pacific urban centers | Short term (≤ 2 years) |

| Expansion of 5G Stand-Alone Networks | +3.4% | Global, led by North America, Europe, China, South Korea | Medium term (2-4 years) |

| Proliferation of Low-Code Mobile Backend Services | +1.7% | Global, early traction in North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Development in IT Infrastructure in Emerging Countries

Massive fiber backbones and sovereign data-center mandates in India, Indonesia, Brazil, and Nigeria are shrinking latency and widening coverage, making cloud-backed apps viable in tier-2 and tier-3 cities. India’s Digital India program allocated USD 1.2 billion in 2024 to build state-owned cloud zones that local start-ups can tap without foreign dependency.[1]Government of India, “Digital India Initiative,” digitalindia.gov.in Indonesia’s requirement that public mobile apps reside in domestic zones has already triggered new hyperscale facilities in Jakarta and Surabaya. Similar upgrades in Brazil lifted 4G availability to 94% of municipalities in 2024, catalyzing rural agribusiness adoption. As edge nodes propagate, application publishers migrate functions closer to users, sustaining double-digit expansion in the mobile cloud computing market.

Advancing Internet Connectivity

Global mobile data traffic reached 131 exabytes per month in 2024, a 25% jump year-on-year, underpinned by high-definition video streaming and always-synced productivity apps.[2]Ericsson, “Ericsson Mobility Report,” ericsson.com Submarine systems such as 2Africa lowered wholesale bandwidth prices 30%, letting carriers in Senegal, Kenya, and Tanzania bundle unlimited data with cloud storage, flipping intermittent users into daily uploaders. LEO satellite constellations from Starlink and OneWeb filled connectivity gaps in Alaska and the Amazon basin, widening the accessible base for cloud-powered mobile services. The reinforcing cycle of cheaper gigabytes and higher usage accelerates service uptake, boosting the mobile cloud computing market.

Growing Adoption of Edge AI for Mobile Applications

Frameworks like TensorFlow Lite allow phones to run light inference while pushing heavier model-training tasks to the cloud, balancing latency and battery life. A 2024 developer survey showed 41% of respondents shipping edge AI features, up from 28% in 2023. Qualcomm’s Snapdragon 8 Gen 3 delivers 45 TOPS on-device, trimming cloud API calls for virtual assistants by 60%. Apple’s privacy-first design processes health metrics locally and syncs anonymized results, overcoming compliance hurdles. This hybrid model cements cloud platforms as the training hub while positioning handsets for instant inference, a dynamic lifting long-run demand in the mobile cloud computing market.

Rising Usage of Cloud Gaming Platforms

Subscriber counts hit 75 million in 2024 as services such as Xbox Cloud Gaming, GeForce Now, and PlayStation Plus streamed AAA titles to handsets without console hardware.[3]Microsoft, “Xbox Cloud Gaming,” microsoft.comMobile now accounts for 40% of Xbox Cloud Gaming sessions, proof that portability expands engagement. Telecoms in South Korea placed edge nodes within 50 kilometers of gamers, slicing latency to 15 milliseconds and monetizing premium routing plans. Such performance hinges on hyperscaler footprints, reinforcing scale advantages and steering more traffic and revenue into the mobile cloud computing market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Concerns Associated with Data Security | -1.8% | Global, heightened in Europe and North America | Short term (≤ 2 years) |

| Limited Battery Life of Mobile Devices | -1.3% | Global, higher friction for power users | Medium term (2-4 years) |

| Escalating Cloud-Service Egress Fees | -1.1% | Global, multi-cloud setups | Short term (≤ 2 years) |

| Data-Residency and Digital-Sovereignty Regulations | -1.5% | Europe, China, India, Middle East | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Concerns Associated with Data Security

Multi-tenant architectures elevate exposure to interception during transit and unauthorized access at rest. A 2024 study of 1,200 enterprises found 62% delayed migrations over key-management uncertainty and audit gaps, notably in healthcare and banking sectors. European regulators tightened scrutiny around mobile banking apps caching transaction data in foreign clouds, pushing several banks back to private zones. End-to-end encryption layers add 10-15 milliseconds of latency, impairing real-time experience and tempering uptake.

Limited Battery Life of Mobile Devices

Always-on sync drains smartphone batteries 30% faster than periodic uploads, according to an IEEE power study. Augmented-reality streams consume 2.5 watts, emptying a 4,000 mAh cell in under 3 hours. Although new 5G modems reduce idle draw by 40%, active data transfer remains energy-heavy, forcing users in price-sensitive markets to carry backup packs and blunting enthusiasm for high-frequency cloud interactions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Healthcare Mobilizes Cloud Diagnostics

The healthcare slice of the mobile cloud computing market size is on track to expand at a 17.12% CAGR through 2031 as telemedicine, remote patient monitoring, and cloud-sourced diagnostics scale. The U.S. FDA cleared 87 mobile medical apps for cloud data processing in 2024, up from 52 in 2023. Philips rolled out a mobile ultrasound that streams images to radiologists, shortening rural diagnostic cycles from 48 hours to 4 hours. Gaming still holds 27.78% revenue share, but growth is maturing in saturated markets. Finance, entertainment, and education apps ride steady demand, yet healthcare’s regulatory green lights and reimbursement models position it as the catalytic vertical shaping the next wave of the mobile cloud computing market.

Cloud gaming’s share leadership signals entrenched demand for low-latency rendering, micro-transactions, and social play features. Yet first-person shooters require sub-30 millisecond round-trip time, compelling providers to deploy edge compute within 50 kilometers of users, capital-intensive for all but the largest hyperscalers. In contrast, healthcare gains from longer tolerance for latency seconds rather than milliseconds allowing workloads to reside deeper in the cloud and easing rollout across emerging markets with limited edge presence. By 2031, the healthcare segment’s expanding user base and regulatory clarity will narrow the share gap with gaming and solidify multi-vertical resilience in the mobile cloud computing market.

By User: Enterprises Dominate Volume While Consumers Accelerate

Enterprises contributed 70.55% of 2025 revenue as mobile workforces demanded continuous access to customer records, collaboration suites, and field service apps. Salesforce, Microsoft 365, and SAP mobile clients anchor this spend. A survey of 800 IT leaders in 2024 showed 73% view mobile-cloud integration as top-three purchase criteria for new software deployments JMIR.ORG. Meanwhile, consumers are expanding at an 17.95% CAGR as subscription cloud storage, streaming, and gaming services gain traction. Dropbox reported 35% year-on-year growth in mobile uploads in 2024, and Apple recorded more than 1 billion paid iCloud accounts the same year.

The consumer trajectory forces providers to optimize for intermittent connectivity, lighter UI flows, and lower entry-level price points, shifting design priorities previously centered on enterprise compliance and service-level agreements. Enterprises will continue to wield budget influence, but the swelling consumer base adds volume scale and brand visibility, widening the funnel for the mobile cloud computing market.

By Service Model: PaaS Narrows the Gap

Software-as-a-Service retained 63.60% share of the mobile cloud computing market size in 2025 because turnkey apps deliver instant productivity without customization. However, Platform-as-a-Service is projected to climb at a 16.44% CAGR as low-code tools lower technical barriers. Google’s Firebase logged 5 million active projects in 2024, with 60% originating from small businesses lacking formal development teams. AWS Amplify’s generative AI assistant automatically builds authentication flows and APIs from natural-language prompts, cutting development cycles by 70% . Infrastructure-as-a-Service remains for specialists needing granular resource control, yet abstractions are winning mindshare, closing the gap and intensifying competition within the mobile cloud computing market.

PaaS growth reflects a shift from hardware-oriented differentiation to developer experience. Hyperscalers package analytics, messaging, and AI inference as drag-and-drop services, letting startups focus on front-end differentiation while the provider captures recurring margins. As PaaS convenience pushes deeper into corporate IT backlogs, the mobile cloud computing industry will normalize on these higher-level constructs, relegating raw compute to niche needs.

By Deployment: Hybrid Cloud Finds Its Moment

Hybrid implementations are expanding at 17.38% CAGR to 2031 as financial services, healthcare, and government workloads straddle sovereign on-premises zones and elastic public regions. Public deployments still hold 55.82% revenue share because startups and digital natives value global scale. JPMorgan Chase’s 2024 mobile banking architecture processes transactions on-premises for compliance then exports fraud analytics to AWS, trimming infrastructure spend 22%. Europe’s Digital Operational Resilience Act effective 2025 compels institutions to validate that critical mobile services function under multi-cloud scenario, accelerating hybrid adoption.

Hybrid demands mature IT operations identity federation, network peering, data-synchronization orchestration creating services revenue for integrators such as IBM and Accenture. Over the forecast window, regulated entities seeking agility without regulatory exposure will keep hybrid the fastest-growing slice of the mobile cloud computing market.

By Mobile Operating System: Android Scales, iOS Monetizes

Android owned 71.10% share in 2025, supported by availability across all price tiers and Google’s cloud API integration, logging 2.1 billion daily calls to Drive, Photos, and Firebase. Yet iOS monetizes more aggressively Apple users buy iCloud storage at 2.3× the rate of Android users. Developers prioritize iOS for premium subscriptions because unified hardware and payment rails shorten time-to-market by 30%.

HarmonyOS, at 700 million units shipped, builds its own mobile cloud ecosystem inside China, anchored by Huawei Cloud. Providers must therefore sustain parity across Android’s scale engine and iOS’s spend engine, threading offerings to each platform’s economics to capture full value from the mobile cloud computing market.

Geography Analysis

North America generated 36.25% of 2025 revenue, benefiting from dense availability zones and 280 million 5G standalone subscribers, which deliver sub-20 millisecond latency for mobile workloads. Amazon Web Services, Microsoft Azure, and Google Cloud operate more than 40 zones in the region, powering autonomous vehicle telemetry, industrial IoT, and high-frequency finance apps. Canada mandated sovereign cloud for public mobile services in 2024, prompting Telus and Bell investments but leaving most commercial traffic on U.S. hyperscalers.

Asia Pacific is projected to lead growth at a 16.65% CAGR to 2031. China surpassed 3.5 million 5G base stations in 2024, covering 95% of urban zones, allowing Alibaba Cloud and Tencent Cloud to place edge nodes within 10 milliseconds of 800 million mobile users. India’s Unified Payments Interface processed 12 billion mobile transactions monthly in 2024 over cloud payment gateways, illustrating mobile-first scale. Japan’s carrier network slicing guarantees enterprise latency, while South Korea doubled hyperscale capacity to feed live streaming and gaming hunger.

Europe, the Middle East and Africa, and South America present mixed scenarios. Europe’s Gaia-X hardens data sovereignty, requiring local cloud processing for public mobile apps. Dubai’s Smart City uses mobile cloud for civic services, inspiring neighboring Gulf states. Africa benefits from new subsea capacity and bundled data-plus-cloud offerings, yet power instability compels on-premises backups. South America contends with macro volatility, though new Tencent Cloud regions in São Paulo and Lagos cut latency for fintech and gaming. The imbalance of regulatory stringency, infrastructure maturity, and consumer purchasing power sets a mosaic growth profile for the mobile cloud computing market.

Competitive Landscape

The mobile cloud computing market is moderately concentrated. The top five Amazon Web Services, Microsoft Azure, Google Cloud, Alibaba Cloud, and Tencent Cloud command roughly 65% of infrastructure revenue in 2024, leaving 35% to regional providers and vertical specialists. AWS operates 450 edge locations, Microsoft 60 zones, and Google invests heavily in subsea cables to thin inter-regional latency, while Alibaba and Tencent scale Asia Pacific edge density. Oracle’s 2024 zero-egress policy attacked incumbents’ lock-in economics, winning mindshare among multi-cloud architects.

Emerging disruptors include Cloudflare, leveraging content delivery roots to offer serverless edge compute, and Fastly, targeting real-time mobile workloads with sub-10-millisecond guarantees. DigitalOcean courts independent developers via price simplicity, while IBM’s 2024 patent filing on federated workload routing hints at an interoperability future. Telcos such as Verizon and Deutsche Telekom are bundling connectivity with edge compute to monetize latency advantages, adding competitive vectors.

Strategic motions center on vertical integration. Hyperscalers buy mobile back-end platforms to lock developer pipelines, partner with carriers to plant micro-zones in metro areas, and roll out AI inference chips to lower in-cluster operating cost. With scale effects preserved, the market rewards depth edge nodes, sovereignty zones, AI services more than headline core compute. Providers that solve cross-border compliance and edge orchestration will capture outsized share as workloads proliferate across the mobile cloud computing market.

Mobile Cloud Computing Industry Leaders

IBM Corporation

Amazon Web Services Inc.

Google LLC

Oracle Corporation

Microsoft Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Microsoft Azure committed USD 80 billion to AI-optimized data centers, reserving 40% of new capacity for mobile edge inference nodes in Asia Pacific and Europe.

- December 2024: Amazon Web Services released Amplify Gen 2, adding generative AI code assistants that cut mobile back-end development time by 70%.

- November 2024: Alibaba Cloud and China Mobile launched 5G standalone slices for cloud gaming in 50 cities, hitting 12-millisecond latency and 2 million users in one month.

- October 2024: Google Cloud acquired Wiz for USD 23 billion to deepen zero-trust security for mobile workloads.

Global Mobile Cloud Computing Market Report Scope

The mobile cloud-primarily refers to cloud-based data, applications, and services designed specifically for mobile and various other portable devices. It allows the delivery of applications and services to mobile users powered by a remote cloud environment or server. Mobile cloud utilizes cloud computing to deliver applications to mobile devices. These cloud-based mobile apps use cloud technology to process and store data so that the app is usable on all types of old as well as new mobile devices.

The Mobile Cloud Computing Market Report is Segmented by Application (Gaming, Finance and Business, Entertainment, Education, Healthcare, Travel, Other Applications), User (Enterprise, Consumer), Service Model (Software-as-a-Service, Platform-as-a-Service, Infrastructure-as-a-Service), Deployment (Public Cloud, Private Cloud, Hybrid Cloud), Mobile Operating System (Android, iOS, Others), and Geography (North America, Europe, Asia Pacific, Middle East, Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

By Application

| Gaming |

| Finance and Business |

| Entertainment |

| Education |

| Healthcare |

| Travel |

| Other Applications |

By User

| Enterprise |

| Consumer |

By Service Model

| Software-as-a-Service (SaaS) |

| Platform-as-a-Service (PaaS) |

| Infrastructure-as-a-Service (IaaS) |

By Deployment

| Public Cloud |

| Private Cloud |

| Hybrid Cloud |

By Mobile Operating System

| Android |

| iOS |

| Others |

Geography

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia | |

| Middle East | Israel |

| Saudi Arabia | |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Application | Gaming | |

| Finance and Business | ||

| Entertainment | ||

| Education | ||

| Healthcare | ||

| Travel | ||

| Other Applications | ||

| By User | Enterprise | |

| Consumer | ||

| By Service Model | Software-as-a-Service (SaaS) | |

| Platform-as-a-Service (PaaS) | ||

| Infrastructure-as-a-Service (IaaS) | ||

| By Deployment | Public Cloud | |

| Private Cloud | ||

| Hybrid Cloud | ||

| By Mobile Operating System | Android | |

| iOS | ||

| Others | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia | ||

| Middle East | Israel | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the mobile cloud computing market?

The mobile cloud computing market size is USD 79.17 billion in 2026.

How fast is the market expected to grow through 2031?

It is projected to advance at a 16.18% CAGR, reaching USD 167.62 billion by 2031.

Which application segment is growing the fastest?

Healthcare mobile cloud applications are forecast to expand at a 17.12% CAGR due to telemedicine and remote diagnostics.

Why are enterprises adopting hybrid cloud for mobile workloads?

Hybrid topologies let regulated sectors keep sensitive data on-premises while scaling analytics and AI in public clouds, balancing compliance and agility.

Which region will post the highest growth?

Asia Pacific is expected to grow at a 16.65% CAGR on the back of dense 5G rollouts and government digital-first programs.

Who are the leading providers in this space?

Amazon Web Services, Microsoft Azure, Google Cloud, Alibaba Cloud, and Tencent Cloud collectively control around 65% of infrastructure revenue.

Page last updated on: