Cloud Communication Platform Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

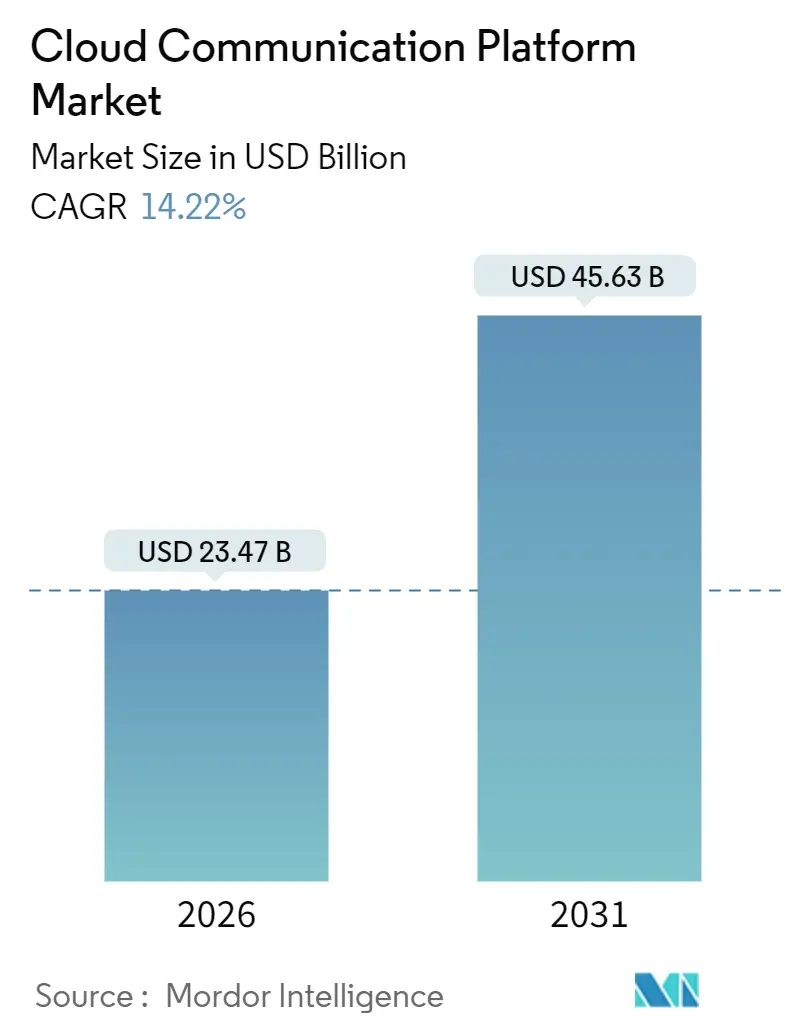

| Market Size (2026) | USD 23.47 Billion |

| Market Size (2031) | USD 45.63 Billion |

| Growth Rate (2026 - 2031) | 14.22% CAGR |

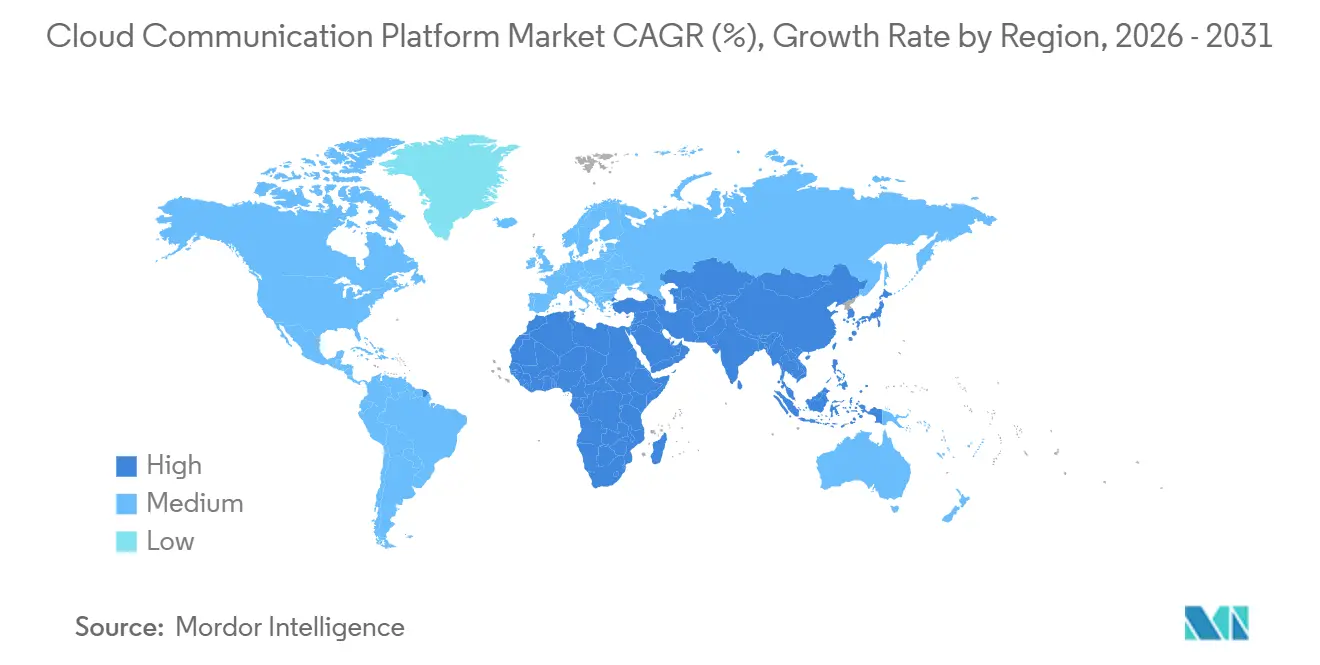

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cloud Communication Platform Market Analysis by Mordor Intelligence

The cloud communication platform market reached USD 23.47 billion in 2026 and, at a 14.22% CAGR, is projected to attain USD 45.63 billion by 2031. Market size acceleration stems from enterprises dismantling on-premises PBX estates and adopting API-driven, pay-per-use models that support real-time voice, video, and messaging across hybrid workforces.[1]Microsoft Corp., “Fiscal 2025 Annual Report,” MICROSOFT.COM Financial institutions and healthcare providers are migrating faster than other sectors because cloud-native platforms now embed voice biometrics and audit trails that simplify regulatory compliance. Hyperscalers are bundling communication APIs with their existing infrastructure, lowering entry barriers and sparking price competition. Meanwhile, edge computing nodes and 5G network slicing are reducing latency to single-digit milliseconds, enabling time-critical use cases in trading, telemedicine, and gaming. Data-sovereignty mandates in Europe and Asia-Pacific are reshaping deployment choices, spurring hybrid architectures that localize sensitive call records yet keep non-real-time workloads in public clouds. Heightened scrutiny of the carbon footprint of hyperscale data centers is prompting operators to shift workloads to regions with abundant renewable power, influencing vendor selection as enterprises add sustainability metrics to procurement scorecards.

Key Report Takeaways

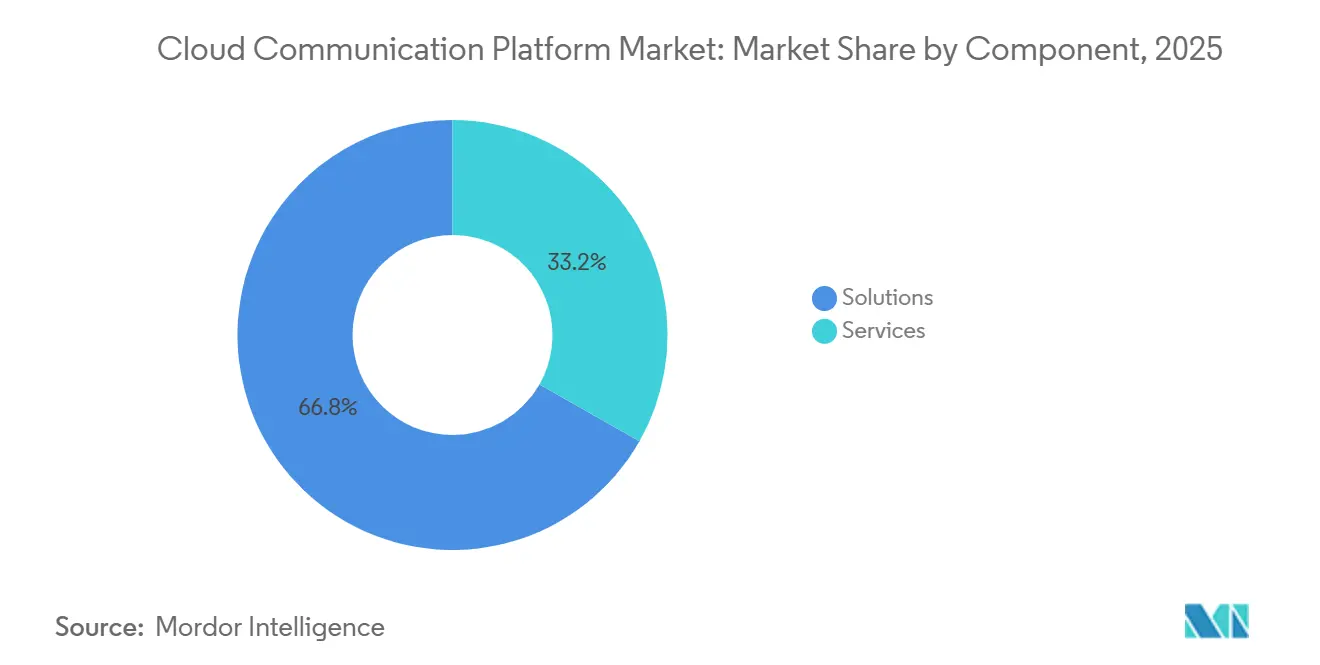

- By component, Solutions led with 66.78% revenue share in 2025, while Services are expanding at a 15.80% CAGR through 2031.

- By deployment, Public Cloud captured 72.59% of 2025 revenue, whereas Hybrid Cloud is advancing at a 15.30% CAGR through 2031.

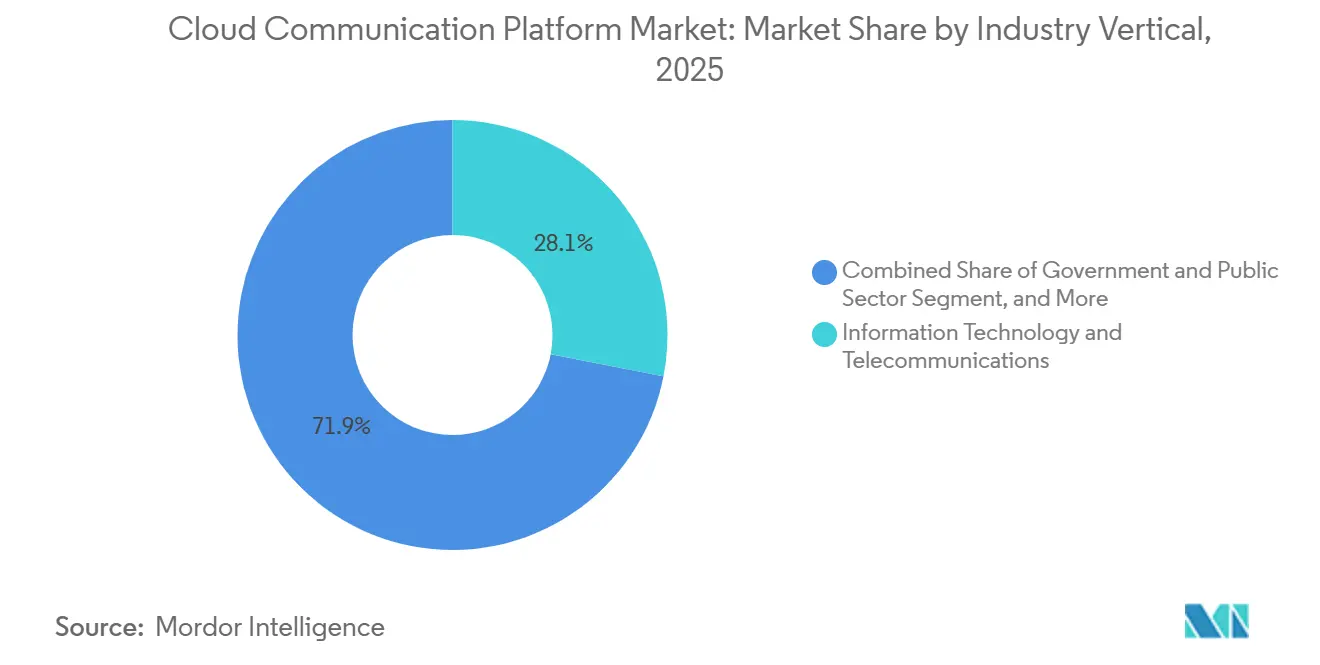

- By industry vertical, Information Technology and Telecommunications held 28.07% of 2025 revenue; Healthcare is forecast to expand at a 14.60% CAGR to 2031.

- By enterprise size, Large Enterprises contributed 67.21% of 2025 revenue, yet Small and Medium-sized Enterprises are registering a 16.10% CAGR through 2031.

- By geography, North America accounted for 38.47% of 2025 revenue, while Asia-Pacific is projected to grow at a 15.00% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Cloud Communication Platform Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of CPaaS and Omni-Channel APIs | +3.2% | Global, concentrated in North America and Asia-Pacific | Medium term (2-4 years) |

| Rapid Adoption of Hybrid and Remote Work Models | +2.8% | Global, high in North America and Europe | Short term (≤ 2 years) |

| Growing Bring-Your-Own-Device Culture in Enterprises | +1.5% | Urban centers worldwide | Medium term (2-4 years) |

| Edge Computing-Enabled Ultra-Low-Latency Experiences | +2.1% | Global, early in retail and financial services | Long term (≥ 4 years) |

| 5G Stand-Alone Network Slicing for QoS-Critical Traffic | +2.3% | Asia-Pacific core, North America and Middle East emerging | Long term (≥ 4 years) |

| Artificial Intelligence-Driven Voice Biometrics for Compliance | +1.6% | Global, strongest in BFSI and healthcare | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Proliferation of CPaaS and Omni-Channel APIs

Enterprises are decomposing legacy contact centers into microservices that orchestrate SMS, WhatsApp, voice, and video through unified APIs, enabling marketing teams to launch campaigns without requiring IT support.[2]Twilio Inc., “Q4 2025 Shareholder Letter,” TWILIO.COM No-code workflow builders shorten idea-to-launch cycles from months to days, and retail brands embed click-to-call buttons tied to live inventory feeds, boosting conversion rates. Adoption is highest where pre-built connectors to Salesforce, Shopify, and SAP eliminate the need for custom coding, giving platforms with large integration marketplaces a structural advantage. These omni-channel APIs shift vendor differentiation from raw telephony features toward ecosystem breadth. As a result, the cloud communication platform market rewards providers who cultivate robust developer communities that accelerate time-to-value.

Rapid Adoption of Hybrid and Remote Work Models

Permanent hybrid work policies at 68% of Fortune 500 firms in 2025 fueled migration from VPN-bound softphones to browser-based WebRTC clients that provision voice and video on demand. Microsoft Teams Phone has surpassed 15 million seats by bundling PSTN calling within collaboration workflows, and enterprises are increasingly negotiating usage-based contracts that shift idle-capacity risk to vendors. Security frameworks such as ISO 27001 are now baseline requirements for platforms that must defend home-network endpoints outside corporate firewalls. In turn, platform roadmaps emphasize zero-trust network access and continuous device posture checks. This trend enlarges the cloud communication platform market by converting erstwhile hardware refresh budgets into recurring API consumption.

Edge Computing-Enabled Ultra-Low-Latency Experiences

Financial institutions deploy edge nodes in carrier hotels to process voice biometrics within 10 milliseconds, meeting regulatory verification deadlines. Bandwidth’s 2025 partnership with Cloudflare cached routing logic at 275 sites, cutting call setup time by 40% for tier-two cities. Developers are compiling call-control flows into WebAssembly binaries that execute at edge locations, moving latency ownership from network engineers to software teams. Gaming, live-event, and brokerage applications treat sub-30 millisecond delays as table stakes for differentiated customer experience. Consequently, vendors with dense edge footprints and programmable routing win deals where latency sensitivity intersects with revenue impact.

5G Stand-Alone Network Slicing for QoS-Critical Traffic

Commercial 5G standalone launches enable enterprises to reserve dedicated slices for mission-critical voice and video, bypassing congested internet paths. SK Telecom provisioned a 50 Mbps uplink slice for hospital tele-consults, guaranteeing stable video during procedures. For vendors, integration with 3GPP Network Exposure Function APIs is becoming mandatory to request slices programmatically. Manufacturing and logistics pilots demonstrate that sliced traffic can replace on-premises PBX for autonomous vehicle coordination, where millisecond jitter can halt production. This capability extends the cloud communication platform market into workloads previously deemed too latency-sensitive for the cloud.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-Security and Privacy Vulnerabilities | -2.1% | Acute in Europe and North America | Short term (≤ 2 years) |

| Fragmented Cross-Border Telecommunications Regulation | -1.8% | Europe, Asia-Pacific, South America | Medium term (2-4 years) |

| Emergence of Private 5G Networks Diluting Cloud Reliance | -1.3% | Manufacturing hubs in Asia-Pacific and North America | Long term (≥ 4 years) |

| Carbon-Footprint Scrutiny on Hyperscale Data Centers | -0.9% | Europe, North America, select Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Data-Security and Privacy Vulnerabilities

The 2024 Snowflake incident exposed call detail records and payment data, driving a 23% spike in cyber-insurance premiums for SaaS providers. Enterprises now demand encryption-at-rest, customer-managed keys, and 24-hour breach notification clauses before signing multi-year API contracts. Microsoft Teams vulnerabilities publicized in 2024 accelerated zero-trust adoption and FedRAMP High certification pursuits among vendors courting U.S. public sector buyers. The result is a flight to platforms that can display third-party attestations, such as SOC 2 Type II and FIPS 140-2 validation, pushing smaller providers toward consolidation.

Fragmented Cross-Border Telecommunications Regulation

CPaaS vendors must navigate 27 EU numbering regimes, India’s Other Service Provider licenses, and Brazil’s rising interconnection fees, each adding complexity and cost. Compliance windows of 6-9 months delay product launches and erode margins, while multinational enterprises gravitate to suppliers offering one-stop regulatory coverage. The landscape bifurcates between global platforms with legal teams in every region and regional specialists optimizing for local rules, leaving limited room for mid-scale challengers. As a result, regulatory fragmentation caps cross-border scale efficiencies, tempering growth in parts of the cloud communication platform market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Rise as Integration Complexity Grows

Solutions controlled 66.78% of 2025 revenue, yet Professional and Managed Services are growing at a 15.80% CAGR, as migrating legacy PBX estates and integrating communication APIs into CRM workflows demand specialist skills. Financial institutions complying with MiFID II call-recording rules and healthcare providers adhering to HIPAA increasingly outsource architecture design and uptime monitoring. CPaaS usage minutes surpassed 1.2 trillion in 2025, marking a significant shift from desk phones to event-driven communications. Contact-center APIs that unify transcribed voice, chat, and email streams lower average handle time, attracting enterprises seeking operational efficiencies.

The consumption-based pricing inherent to CPaaS reduces capex yet raises integration workload, so vendors bundle consulting, migration, and optimization into recurring packages. Mid-market firms lacking DevOps staff lean on managed services partners that monitor API latency and handle carrier interconnects. Consequently, service providers that certify engineers on multiple ecosystems, such as Salesforce, SAP, and Epic, differentiate themselves in the cloud communication platform market, while pure software margins compress as functionality becomes commoditized.

By Deployment Type: Hybrid Architectures Balance Latency and Compliance

Public Cloud accounted for 72.59% of 2025 deployment revenue as enterprises prized agility and limitless scaling. However, Hybrid Cloud is advancing at a 15.30% CAGR because BFSI workloads demand sub-10 millisecond round-trip times that public regions cannot always guarantee.[3]Financial Industry Regulatory Authority, “Latency Standards,” FINRA.ORG Hybrid setups keep signaling servers on-premises while routing analytics and storage to the cloud, blending control with elasticity. Microsoft’s Sovereign Cloud regions promise EU residency for recordings and transcripts, exemplifying localization tactics that win public-sector deals.

Private Cloud persists in defense agencies requiring air-gapped environments, yet its share diminishes as zero-trust overlays prove adequate for many confidential workloads. Smaller CPaaS vendors strike alliances with regional infrastructure providers to deliver local hosting without building data centers, trading gross margin for geographic reach. Hybrid adoption is therefore a permanent posture rather than a migration waypoint, expanding the cloud communication platform market size for orchestration and observability tools that span mixed estates.

By Industry Vertical: Healthcare Surges on Telehealth Parity

IT and telecommunications firms accounted for 28.07% of 2025 revenue by utilizing APIs for customer support and internal collaboration. Healthcare is poised for a 14.60% CAGR through 2031 after U.S. reimbursement parity for virtual visits became permanent in 2024. Epic and Cerner integrated video APIs into electronic health records, allowing clinicians to launch sessions directly from patient charts without context switching. Voice biometrics satisfy Know Your Customer mandates in banking, replacing fallible security questions and curbing call-center fraud.

Retailers embed click-to-call widgets that route shoppers to agents with live inventory visibility, cutting cart abandonment. Government agencies modernize citizen hotlines to manage seasonal surges in tax filings, while manufacturers integrate voice commands into industrial IoT systems for hands-free defect reporting. Across these use cases, sector-specific compliance templates shorten deployment cycles, broadening the addressable cloud communication platform market.

By Enterprise Size: SMEs Embrace Consumption-Based APIs

Large enterprises contributed 67.21% of 2025 revenue, leveraging volume deals and dedicated account teams. Yet SMEs, expanding at a 16.10% CAGR, are the fastest movers because self-service portals allow developers to buy phone numbers and send SMS messages with a credit card, skipping lengthy procurement processes. In the Asia-Pacific region, mobile-first startups integrate messaging into logistics and home-service apps, generating outsized demand relative to their headcount. RingCentral’s USD 15 entry-tier plan lowered the cost of full-stack UCaaS for 10-50 employee firms, replacing consumer tools with carrier-grade reliability.

SME growth is concentrated in high-communication-intensity verticals, such as home healthcare and field services. Vendors offering unified billing across CPaaS and UCaaS simplify administration for lean IT teams. As a result, the cloud communication platform market rewards providers that blend self-service onboarding with scalable support tiers as customers mature.

Geography Analysis

North America accounted for 38.47% of the 2025 global revenue, driven by Fortune 500 UCaaS migrations and substantial venture funding for contact-center-as-a-service startups. U.S. enterprises retired Avaya and Cisco PBXs to cut capex and accommodate remote workers, while Canada’s bilingual mandates spurred demand for dual-language IVR and agent routing. Mexico’s nearshore BPO sector captured Spanish-language traffic from U.S. retailers seeking cost-effective yet culturally aligned support, further enlarging the regional cloud communication platform market.

The Asia-Pacific region is forecast to grow at a 15.00% CAGR through 2031, driven by India’s USD 1.2 billion Digital India broadband program and China’s data localization statutes, which bifurcate domestic and multinational platform choices. India’s blockchain-based call authentication mandate pushed vendors to integrate distributed ledgers, lengthening time-to-market but raising trust. Southeast Asia leapfrogged fixed telephony by transacting directly over WhatsApp Business APIs, with conversational commerce normalizing end-to-end ordering inside chat threads. Japan and South Korea are leading 5G slicing pilots that ensure call quality for telemedicine and factory automation, expanding the cloud communication platform market into latency-critical scenarios.

Europe’s uptake is moderated by fragmented numbering and lawful-intercept rules that force country-specific deployments. Post-Brexit divergence introduced a separate UK data-protection regime, complicating the rollouts of transatlantic platforms. Germany’s strict GDPR interpretation initially slowed the adoption of AI voice analytics until vendors implemented explicit dual-party consent flows. France and Italy are digitizing their citizen hotlines, while Saudi Arabia and the United Arab Emirates are mandating omnichannel government services under their national digital agendas. Africa’s growth centers on SMS and USSD engagement in markets with sporadic broadband, whereas Brazil’s interconnection fee hike favored domestic carriers, tilting South American market economics toward local providers.

Competitive Landscape

The cloud communication platform market remains moderately fragmented: the top five vendors, Twilio, Microsoft, Cisco, RingCentral, and Amazon Web Services, held roughly 45% of 2025 revenue. Hyperscalers cross-sell APIs alongside compute and storage, compressing prices and forcing pure-play CPaaS vendors to differentiate through vertical templates, low-latency edge points, and developer experience. Microsoft bundled Teams Phone with Microsoft 365 at near-zero marginal cost, scaling seats to 15 million and compelling UCaaS rivals to pivot toward AI transcription and sentiment features.

Twilio’s 2020 acquisition of Segment created unified customer profiles that raise switching costs beyond basic telephony integration, anchoring wallet share. Carrier-grade providers such as Bandwidth and Telnyx capture latency-sensitive workloads by offering sub-50 millisecond global termination. Smaller vendors pursue ISO 27001 and SOC 2 Type II audits to win business in regulated verticals, while those lacking security maturity often seek mergers or exits. White-space opportunities emerge in pharmaceuticals, legal services, and energy, where compliance-ready workflows remain scarce. Consequently, competitive dynamics hinge on security posture, integration breadth, and AI-enhanced agent productivity, rather than raw call routing.

Cloud Communication Platform Industry Leaders

Twilio Inc.

Vonage Holdings Corp.

Sinch AB

Infobip Ltd.

Bandwidth Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- Oct 2025: Twilio acquired Khoros for USD 1.1 billion, adding social community channels to its engagement suite.

- September 2025: Microsoft launched Azure Communication Services Direct Routing for Teams to connect on-premises SIP trunks without carrier changes.

- August 2025: RingCentral embedded native calling and messaging inside Salesforce Service Cloud and Sales Cloud interfaces.

- July 2025: Amazon Web Services rolled out Amazon Connect Forecasting, an AI staffing optimizer that cut pilot labor costs by 12-15%.

Global Cloud Communication Platform Market Report Scope

Cloud Communication is an internet-based data and voice communication method. Cloud communication allows users to work from any device. The Cloud Communication Platform provides a customized application program interface for the developers to decide the interaction of their product with SMS, voice, video, and verification features. Cloud management permits storing and computing data that can be accessed over the internet publicly. The Cloud Communication Platform Market Report is Segmented by Component (Solutions including CPaaS, UCaaS, WebRTC Gateways, Contact-Center APIs; Services including Professional and Managed Services), Deployment Type (Public, Private, Hybrid Cloud), Industry Vertical (IT and Telecom, BFSI, Healthcare, Retail, and More), Enterprise Size (Large, SME), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Solutions | Communications Platform as a Service (CPaaS) |

| Unified Communications as a Service (UCaaS) | |

| WebRTC Gateways | |

| Contact-Center APIs | |

| Services | Professional Services |

| Managed Services |

| Public Cloud |

| Private Cloud |

| Hybrid Cloud |

| Information Technology and Telecommunications |

| Banking, Financial Services and Insurance |

| Healthcare |

| Retail and E-Commerce |

| Government and Public Sector |

| Manufacturing |

| Travel and Hospitality |

| Education |

| Large Enterprises |

| Small and Medium-Sized Enterprises |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Benelux | |

| Nordics | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Southeast Asian Nations | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Kuwait | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Kenya | |

| Egypt | |

| Rest of Africa |

| By Component | Solutions | Communications Platform as a Service (CPaaS) |

| Unified Communications as a Service (UCaaS) | ||

| WebRTC Gateways | ||

| Contact-Center APIs | ||

| Services | Professional Services | |

| Managed Services | ||

| By Deployment Type | Public Cloud | |

| Private Cloud | ||

| Hybrid Cloud | ||

| By Industry Vertical | Information Technology and Telecommunications | |

| Banking, Financial Services and Insurance | ||

| Healthcare | ||

| Retail and E-Commerce | ||

| Government and Public Sector | ||

| Manufacturing | ||

| Travel and Hospitality | ||

| Education | ||

| By Enterprise Size | Large Enterprises | |

| Small and Medium-Sized Enterprises | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Benelux | ||

| Nordics | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Southeast Asian Nations | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| Kuwait | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large is the cloud communication platform market today?

The cloud communication platform market reached USD 23.47 billion in 2026 and is set to grow to USD 45.63 billion by 2031 at a 14.22% CAGR.

Which deployment mode is growing fastest?

Hybrid Cloud deployments are expanding at a 15.30% CAGR as enterprises balance low-latency on-premises workloads with public cloud elasticity.

Why is healthcare adopting cloud communication platforms rapidly?

Telehealth reimbursement parity and electronic health record integrations are driving a 14.60% CAGR for healthcare use cases through 2031.

What is the main security challenge for cloud communication platforms?

High-profile breaches heightened focus on encryption, key management, and zero-trust architecture, making third-party security attestations a procurement prerequisite.

Which region is projected to post the strongest growth?

Asia-Pacific is forecast to grow at a 15.00% CAGR, fueled by broadband expansion, 5G rollouts, and widespread mobile-first consumer behavior.

Who are the leading vendors in the space?

Twilio, Microsoft, Cisco, RingCentral, and Amazon Web Services together held about 45% of global revenue in 2025, with numerous regional and specialist providers occupying the rest.

Page last updated on: