Cloud Based Business Analytics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

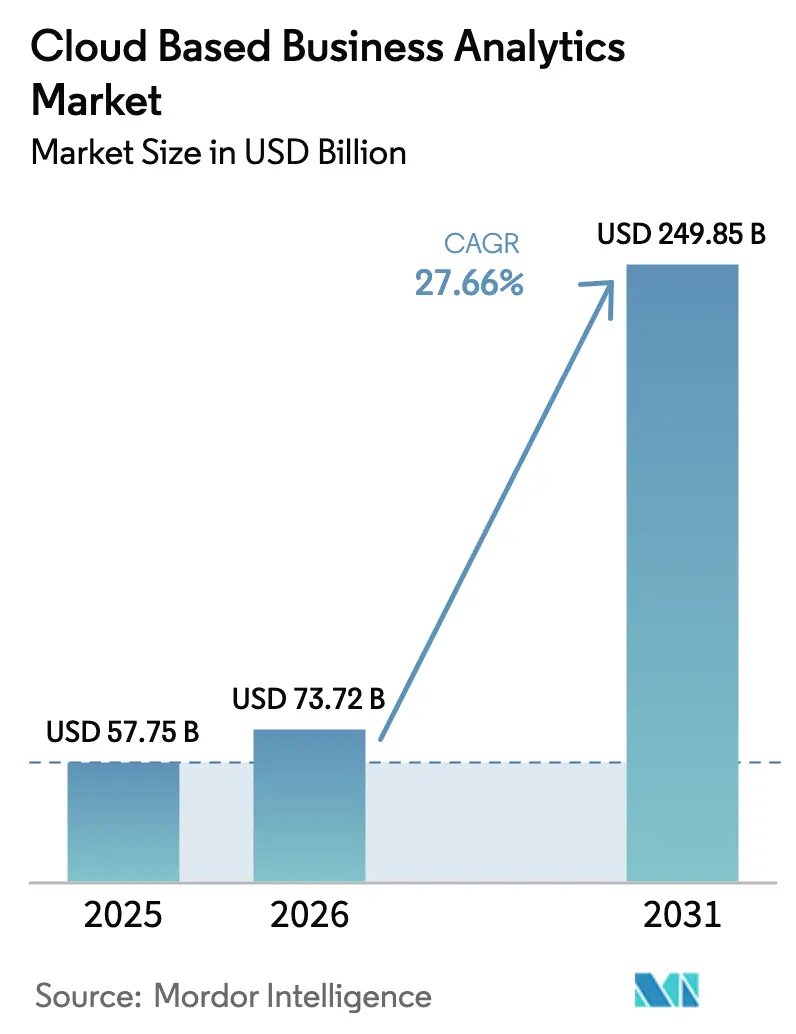

| Market Size (2026) | USD 73.72 Billion |

| Market Size (2031) | USD 249.85 Billion |

| Growth Rate (2026 - 2031) | 27.66% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cloud Based Business Analytics Market Analysis by Mordor Intelligence

The cloud-based business analytics market size in 2026 is estimated at USD 73.72 billion, growing from 2025 value of USD 57.75 billion with 2031 projections showing USD 249.85 billion, growing at 27.66% CAGR over 2026-2031. Intensifying demand for data-driven decisions, the shift from on-premises to cloud-native deployments, and rapid integration of generative AI underpin this sharp expansion. Enterprises favour multi-cloud strategies that support data federation across disparate platforms, while privacy-preserving architectures guard sensitive information and satisfy regional regulations. Competitive differentiation now centres on AI-enhanced insights, real-time analytics, and industry-tailored solutions that lower latency and accelerate outcomes. Heightened regulatory scrutiny, rising egress fees, and talent shortages temper growth yet simultaneously expand opportunities for managed services and automation tools that alleviate complexity. Consequently, the cloud-based business analytics market is evolving into an ecosystem where hyperscale infrastructure, specialised software, and domain-expert services converge to deliver end-to-end analytical value.

Key Report Takeaways

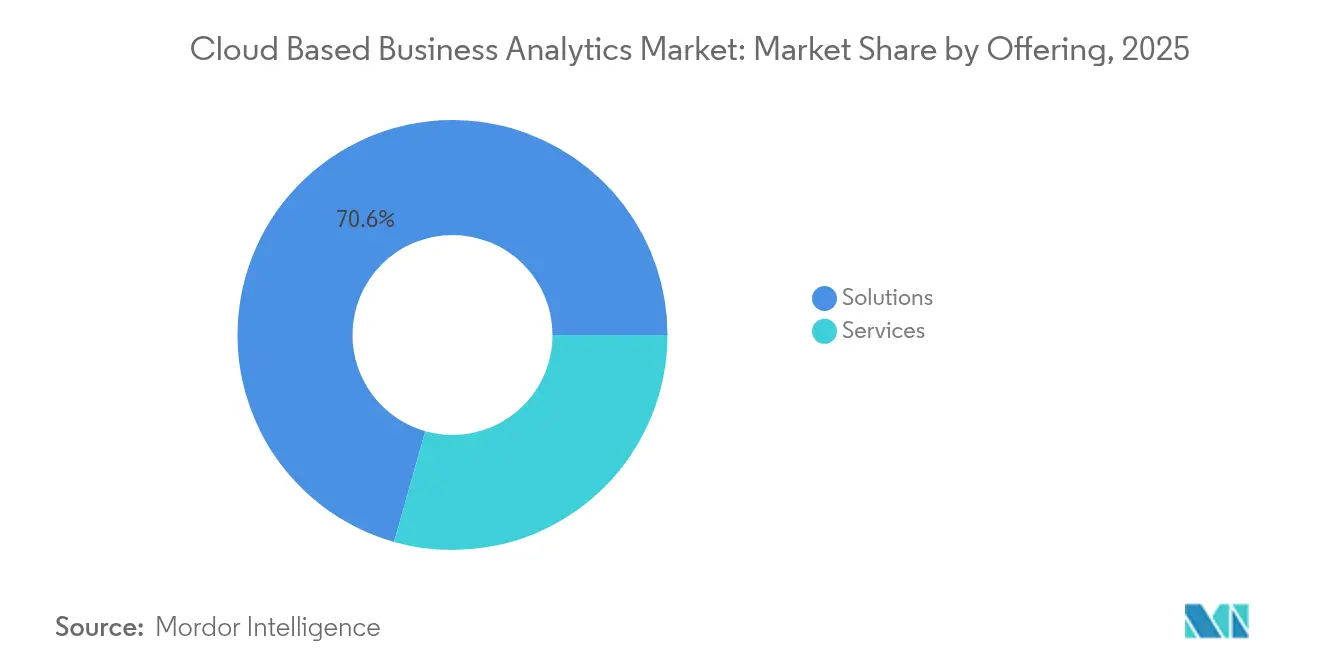

- By offering, solutions held 70.62% revenue share in 2025, whereas services are forecast to rise fastest at a 31.91% CAGR through 2031.

- By deployment model, public cloud led with 58.04% of the cloud-based business analytics market share in 2025, while private cloud is expected to expand at a 35.20% CAGR to 2031.

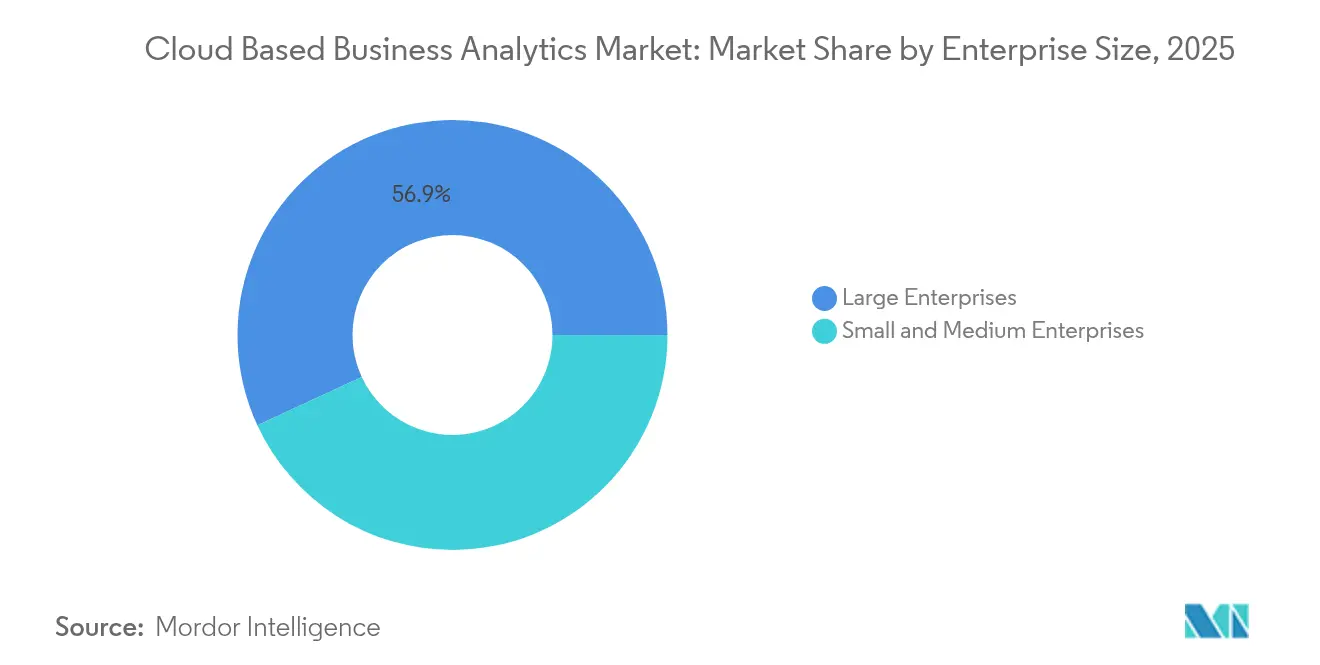

- By enterprise size, large enterprises contributed 56.89% of the cloud-based business analytics market size in 2025; small and medium enterprises are projected to grow at a 30.93% CAGR through 2031.

- By industry vertical, BFSI led with 27.93% revenue share in 2025, whereas healthcare is forecast to advance at a 32.54% CAGR to 2031.

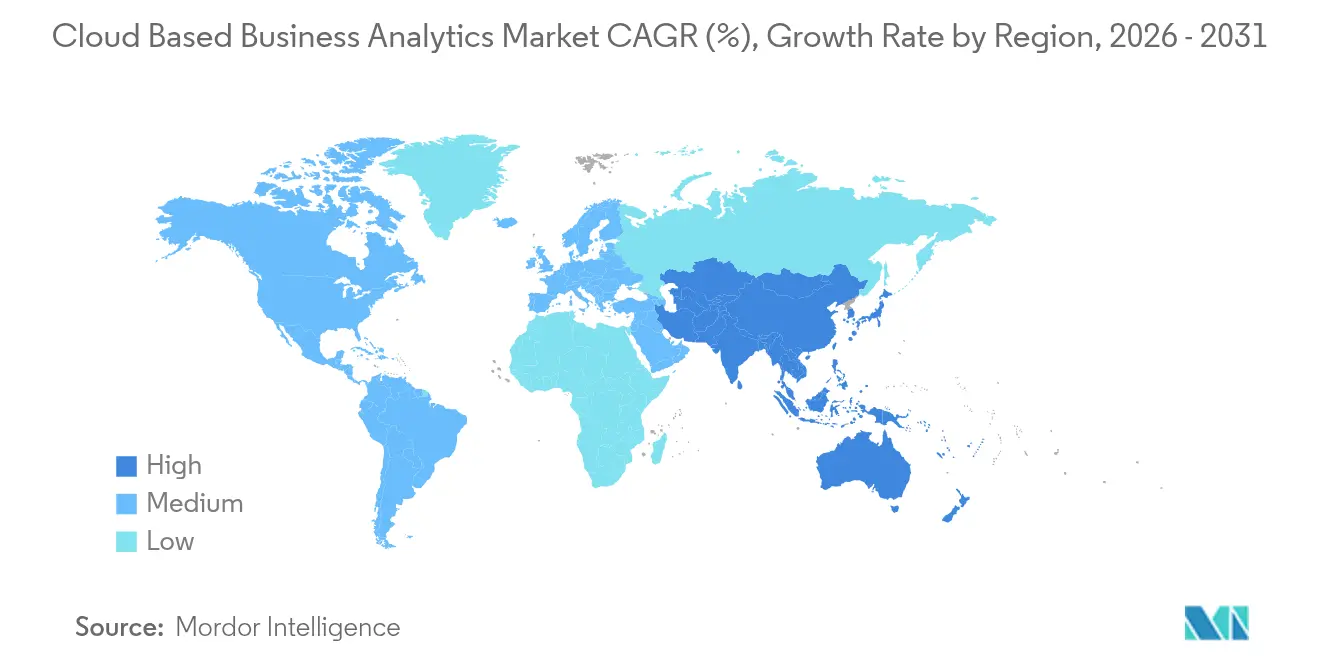

- By geography, North America commanded 42.06% revenue share in 2025; Asia-Pacific is set to record the quickest pace at a 33.86% CAGR over the same period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cloud Based Business Analytics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Exploding multi-cloud data volumes | +8.2% | Global, with concentration in North America and Asia-Pacific | Medium term (2-4 years) |

| Real-time decision-making imperatives | +6.8% | Global, led by BFSI and Manufacturing sectors | Short term (≤ 2 years) |

| SME digital-first adoption of SaaS analytics | +5.4% | Asia-Pacific core, spill-over to Latin America | Medium term (2-4 years) |

| Generative-AI workloads driving analytic modernization | +7.1% | North America and EU leading, Asia-Pacific following | Long term (≥ 4 years) |

| FinOps-led cost-governance analytics demand | +4.3% | Global, with emphasis in mature cloud markets | Short term (≤ 2 years) |

| Emergence of privacy-preserving clean-room analytics | +3.7% | EU and North America due to regulatory frameworks | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Exploding multi-cloud data volumes

Hybrid and multi-cloud adoption exceeds 92%, and the average enterprise already employs 2.2 cloud providers, creating significant data fragmentation. Such dispersion magnifies integration complexity and triples the number of data-movement challenges relative to single-cloud estates. Modern analytics platforms answer this need with real-time federation, data mesh, and zero-copy sharing functionality that shorten insight cycles by 19% once maturity is achieved.[1]VMware, “Multi-Cloud Strategies for the Modern Enterprise,” vmware.com

Real-time decision-making imperatives

Latency-sensitive sectors such as high-frequency trading, automated manufacturing, and dynamic retail pricing require analytics responses measured in milliseconds. The fusion of 5G networks with edge computing now enables 45% of IoT data to be processed near the device, slashing transport costs and unlocking immediate intervention at the point of action. Retailers leveraging real-time analytics for surge pricing have realized revenue lifts between 15% and 25%.[2]Renesas Electronics Corporation, “Edge Analytics and IoT Data Processing,” renesas.com

SME digital-first adoption of SaaS analytics

Subscription-based cloud analytics remove capital barriers, making enterprise-grade intelligence reachable for SMEs that previously lacked infrastructure and expertise. Awareness of business analytics tools among small firms now stands at 70%, and adoption rates accelerate across retail, e-commerce, and fintech. Low-code features empower non-technical users to deliver insights rapidly, although financial limitations and skills gaps persist. Dedicated SME packages featuring guided onboarding, bundled training, and consumption-based pricing help mitigate these obstacles.

Generative-AI workloads driving analytic modernization

Global spending on generative AI infrastructure is projected to reach USD 644 billion in 2025. Enterprises upgrading for AI-native processing report returns exceeding USD 3.71 on every dollar invested. Clean-room technologies and differential privacy guard sensitive datasets while allowing large-language models to train effectively. Vendors weave AI agents directly into analytics layers, enabling contextual narrative generation, anomaly detection, and guided data preparation at scale.[3]Snowflake, “AI Agents Announcement,” snowflake.com

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Complex regulatory compliance (GDPR, CCPA, DPDPA) | -4.2% | EU leading, expanding to APAC and Americas | Medium term (2-4 years) |

| Persistent data-security and sovereignty concerns | -3.8% | Global, with emphasis in regulated industries | Short term (≤ 2 years) |

| Rising cloud-egress costs throttling data mobility | -2.9% | Global, affecting multi-cloud deployments | Short term (≤ 2 years) |

| Scarcity of cloud-native analytics talent | -3.1% | Global, acute in North America and EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Complex regulatory compliance (GDPR, CCPA, DPDPA)

Divergent privacy laws force enterprises to maintain region-specific analytics stacks that satisfy data residency, consent, and audit requirements. Compliance spending absorbs up to 20% of cloud analytics budgets within finance and healthcare, prompting interest in sovereign cloud zones that balance locality with hyperscale capabilities. European and Asia-Pacific statutes such as PIPL and DPDPA complicate cross-border data exchange, making unified global analytics architectures difficult.

Scarcity of cloud-native analytics talent

A global shortage of over 85 million IT professionals by 2030 is expected to cost USD 5.5 trillion in unrealised output. Cloud analytics roles are among the hardest to fill because engineers must understand distributed architectures, AI pipelines, and evolving security frameworks. Automation and managed services offer partial relief, yet strategic design and model stewardship still demand experienced specialists, intensifying wage inflation and delaying project timelines.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: solutions dominate while services accelerate

The solutions segment generated 70.62% of 2025 revenue, buoyed by integrated platforms from hyperscale cloud vendors that simplify procurement and deliver rapid time-to-value. However, implementation complexity across multi-cloud estates drives a 31.91% CAGR for professional and managed services through 2031. Enterprises rely on specialists to architect secure pipelines, embed AI engines, and satisfy compliance mandates, especially when working with regulated datasets. Providers gain traction by bundling advisory, deployment, optimisation, and FinOps governance in a single contract. Harmonisation between platform and service delivery reduces tool sprawl and strengthens vendor stickiness as workloads scale across geographies.

Managed service offerings also expand to monitor performance, control costs, and automate patching in the face of constant feature rollouts. Continuous collaboration between service partners and platform owners mitigates downtime and ensures that AI functions remain transparent and explainable. By 2031, over 40% of buyers are expected to prefer outcome-based contracts where service fees align with business-value metrics rather than hours consumed, reinforcing the strategic importance of trusted partners to the cloud-based business analytics market.

By Deployment Model: private cloud gains on sovereignty imperatives

The public cloud owns 58.04% of deployments, supported by on-demand scalability and an ever-growing catalog of analytical tools. Yet data sovereignty and low-latency demand to propel private cloud at a 35.20% CAGR, particularly within financial services and healthcare, where sensitive workloads cannot cross borders. Sovereign-cloud initiatives from global providers offer dedicated regions, contractual safeguards, and third-party attestations that address localization requirements without sacrificing cloud agility. This compromise drives mixed portfolios where sensitive data remains in private instances while less regulated assets leverage public elasticity.

Hybrid and multi-cloud patterns dominate architectural planning, with 92% of enterprises preferring workload portability to avert lock-in and exploit best-of-breed services. Analytics vendors, therefore, extend orchestration layers that abstract infrastructure differences and unify governance. Such interoperability will become table stakes as the cloud-based business analytics market expands into jurisdictions that demand granular control yet expect seamless insight pipelines.

By Data Type: unstructured data drives innovation

Structured data accounted for 63.68% of revenue in 2025, underlining the enduring value of transactional systems. Nonetheless, unstructured data such as documents, images, and sensor feeds is expanding at a 32.35% CAGR as computer vision, natural language processing, and generative AI unlock new business models. Organizations now view these assets as competitive differentiators rather than storage liabilities. Vendors respond with vector databases, object storage integrations, and AI-native query engines that deliver rapid search, summarisation, and content generation.

Semi-structured data, typified by JSON and IoT payloads, enjoys steady growth as API ecosystems flourish and connected devices proliferate. Together these dynamics reinforce the imperative for platforms capable of harmonizing schema-rich and schema-less inputs and delivering governance, lineage, and observability across the full spectrum of enterprise data.

By Enterprise Size: SMEs embrace cloud-first analytics

Large enterprises retained 56.89% revenue share in 2025, courtesy of expansive budgets and multi-domain analytics programs. Small and medium enterprises are the fastest movers, posting a 30.93% CAGR and demonstrating that cloud subscriptions level the playing field. Frictionless sign-ups, bundled AI assistants, and pay-as-you-grow pricing minimize capital exposure while democratizing sophisticated insight generation. As a result, nearly half of new analytics customers joining the cloud-based business analytics market each year now originate from the SME segment.

Skill shortages pose a greater hurdle for smaller firms than for multinationals that can outbid rivals for talent. Platform vendors, therefore, prioritise automation-first roadmaps featuring auto-generated data models, guided query suggestions, and embedded governance templates. These capabilities allow non-specialists to derive value quickly, sustain adoption, and justify renewals even when budgets tighten.

By Industry Vertical: healthcare accelerates past BFSI leadership

BFSI contributed 27.93% of 2025 revenue due to stringent regulatory reporting, risk analytics, and fraud-prevention needs. Healthcare, expanding at a 32.54% CAGR, now edges toward the leadership position as cloud-ready electronic health record systems, AI-based diagnostics, and population-health analytics take center stage. Regional reimbursement models increasingly reward outcome-centric care, further incentivizing predictive insights derived from massive, heterogeneous patient datasets.

Retail and e-commerce continue to adopt cloud analytics for dynamic pricing, inventory optimization, and hyper-personalized experiences. Manufacturing leans on real-time quality inspections and predictive maintenance that cut downtime and reduce scrap. Public-sector modernization and telecom network intelligence add breadth to vertical demand, ensuring that the cloud-based business analytics market continues to diversify its revenue base.

Geography Analysis

North America generated 42.06% of 2025 revenue, anchored by robust federal cloud spending, deep enterprise adoption across finance, healthcare, and technology, and proximity to leading hyperscale providers. The United States emphasises SaaS as the preferred deployment model for civilian agencies, while Canada invests steadily in skills and automation to offset talent shortages. Regulatory certainty and mature digital ecosystems sustain growth even as penetration approaches saturation.

Asia-Pacific is the fastest-growing territory at a 33.86% CAGR through 2031, buoyed by government cloud-first mandates, accelerated digital transformation, and a swelling data-center footprint. China, Japan, India, and South Korea spearhead regional expansion with large-scale infrastructure investment, while ASEAN economies benefit from policy harmonisation that eases cross-border data flows. Colocation capacity across Asia-Pacific is expected to nearly double between 2023 and 2028, providing a resilient foundation for the widening pool of analytics workloads.

Europe experiences steady uptake, guided by GDPR and national sovereignty imperatives that favour providers offering deterministic data-residency guarantees. France, Germany, and the United Kingdom constitute the principal markets, yet Eastern European members show increasing momentum as EU membership accelerates technology transfer. Middle East and Africa represent nascent but promising opportunities, particularly in oil-rich Gulf nations driving smart-city projects and in pan-African banking ecosystems partnering with global cloud providers.

Competitive Landscape

The cloud-based business analytics market blends moderate concentration with vigorous innovation. AWS, Microsoft, and Google Cloud collectively account for 63% of global cloud spending, leveraging scale to introduce AI accelerators, vector databases, and domain-specific models faster than smaller rivals CRN. Microsoft and Google Cloud currently grow AI-related workloads at roughly twice the pace of AWS, demonstrating the shifting centre of gravity toward AI services. Oracle exhibits double-digit growth on the back of multicloud database momentum and a USD 30 billion contract pipeline expected to deliver material revenue by 2028.

Best-of-breed analytics vendors such as Snowflake, Databricks, and Palantir compete successfully by offering decoupled storage and compute, open data formats, and extensive AI tooling. Snowflake’s recent launch of AI agents and an OpenFlow orchestration layer signals a deep push into workload automation that simplifies complex pipeline design .Strategic MandA remains brisk as suppliers acquire niche capabilities in privacy technology, low-code ML deployment, and domain expertise. IBM’s acquisition of Hakkoda for Snowflake services, Salesforce’s Gemini integration with Google Cloud, and CoreWeave’s purchase of Weights and Biases for effort-less AI development illustrate this consolidation trend.

Cloud Based Business Analytics Industry Leaders

International Business Machines Corporation (IBM)

Microsoft Corporation

Amazon Web Services, Inc.

Google LLC (Alphabet Inc.)

Oracle Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Snowflake launched AI agents and the OpenFlow platform to accelerate multi-environment data workflow management.

- June 2025: Oracle stock rose sharply after disclosure of a cloud contract expected to yield over USD 30 billion in annual revenue starting FY 2028.

- February 2025: Snowflake integrated Microsoft Azure OpenAI Service, giving customers direct access to the latest OpenAI models within the Snowflake interface.

- November 2024: Snowflake partnered with Anthropic to embed Claude models into Cortex AI and purchased Datavolo to enhance data-pipeline management.

Global Cloud Based Business Analytics Market Report Scope

Cloud based business analytics allows organizations to collect, store, and analyze data using algorithms to find business insights using cloud technologies. It a model in which data analytics and business intelligence (BI) processes take place on vendor-managed infrastructure.

The cloud based business analytics market is segmented by type (solutions, services), by data type (structured, unstructured), by enterprises (SMEs, large enterprises), by end-users (BFSI, IT and telecom, healthcare, retail and ecommerce, government, other end-users), by geography (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Solutions |

| Services |

| Public Cloud |

| Private Cloud |

| Hybrid / Multi-cloud |

| Structured Data |

| Semi-Structured Data |

| Unstructured Data |

| Large Enterprises |

| Small and Medium Enterprises |

| BFSI |

| IT and Telecom |

| Healthcare and Life Sciences |

| Retail and E-commerce |

| Government and Public Sector |

| Manufacturing |

| Others (Energy, Media, etc.) |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| UAE | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

| By Offering | Solutions | ||

| Services | |||

| By Deployment Model | Public Cloud | ||

| Private Cloud | |||

| Hybrid / Multi-cloud | |||

| By Data Type | Structured Data | ||

| Semi-Structured Data | |||

| Unstructured Data | |||

| By Enterprise Size | Large Enterprises | ||

| Small and Medium Enterprises | |||

| By Industry Vertical | BFSI | ||

| IT and Telecom | |||

| Healthcare and Life Sciences | |||

| Retail and E-commerce | |||

| Government and Public Sector | |||

| Manufacturing | |||

| Others (Energy, Media, etc.) | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| UAE | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Kenya | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected value of the cloud-based business analytics market by 2031?

The market is forecast to reach USD 249.85 billion by 2031, expanding at a 27.66% CAGR.

Which deployment model is growing fastest?

Private cloud exhibits the highest growth, expected to post a 35.20% CAGR through 2031 as data-sovereignty rules tighten.

Why are SMEs adopting cloud analytics so rapidly?

SaaS platforms eliminate large capital outlays, provide automated onboarding, and offer subscription pricing that aligns with SME budgets, driving a 30.93% CAGR for the segment.

Which industry vertical is poised for the quickest expansion?

Healthcare leads with a projected 32.54% CAGR, enabled by cloud-based electronic health records, AI diagnostics, and population-health analytics.

Page last updated on: