UK Cloud Computing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

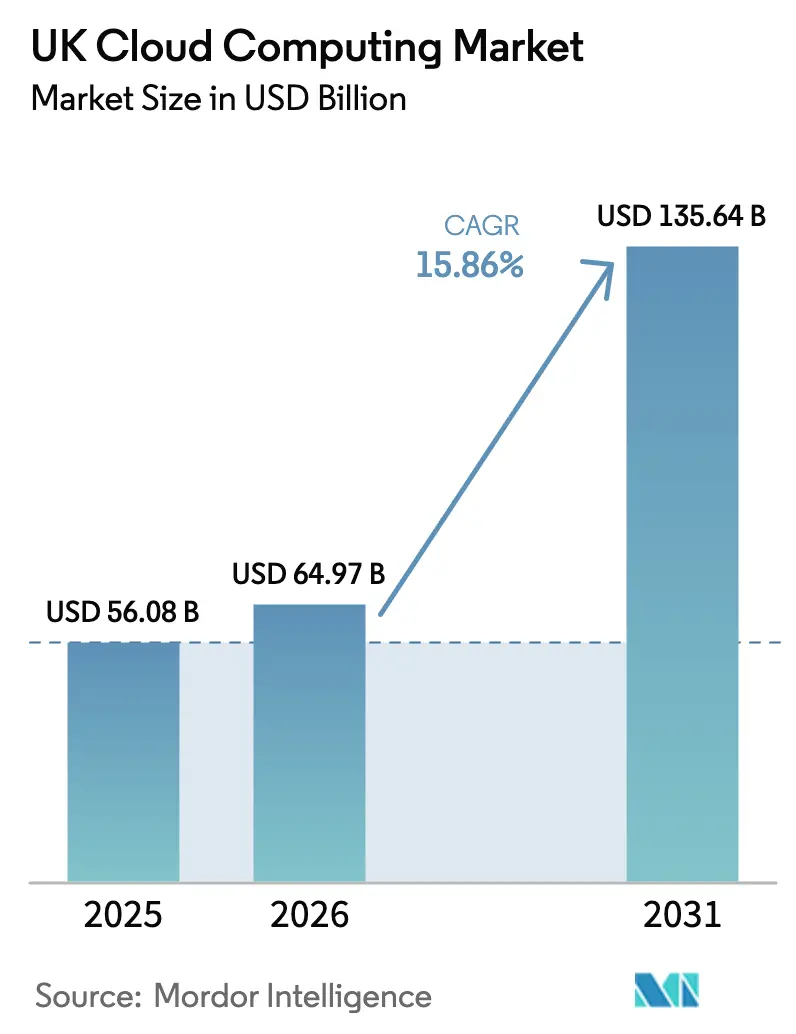

| Base Year Market Size (2025) | USD 56.08 Billion |

| Market Size (2026) | USD 64.97 Billion |

| Market Size (2031) | USD 135.64 Billion |

| Growth Rate (2026 - 2031) | 15.86% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

UK Cloud Computing Market Analysis by Mordor Intelligence

The UK Cloud Computing Market size is expected to grow from USD 56.08 billion in 2025 to USD 64.97 billion in 2026 and is forecast to reach USD 135.64 billion by 2031 at 15.86% CAGR over 2026-2031. This rapid scale-up reflects persistent public-sector digitization mandates, hyperscale providers’ multibillion-pound infrastructure outlays, and enterprise demand for AI-optimised platforms. The government’s Cloud-First policy continues to funnel high-value contracts through G-Cloud, while financial-services and healthcare regulations push mission-critical workloads toward resilient hybrid architectures. Low-latency 5G roll-outs, a widening AI skills base, and carbon-budget incentives further accelerate cloud service uptake across England, Scotland, Wales, and Northern Ireland. Competitive intensity remains high but concentrated: a duopoly holds a combined 60-80% share, prompting investigations that may redefine switching costs and pricing transparency over the forecast horizon.[1]Competition and Markets Authority, “Cloud services market investigation: provisional findings,” gov.uk

Key Report Takeaways

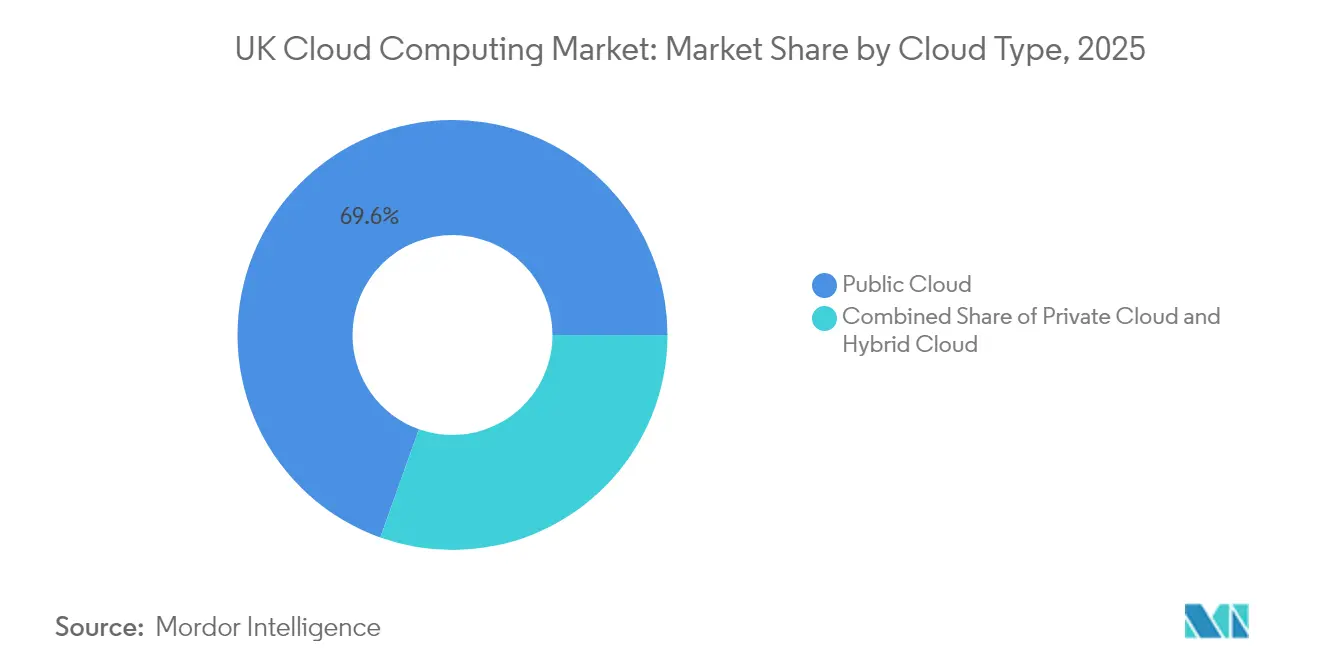

- By cloud type, public cloud led with 69.55% revenue share in 2025, while hybrid cloud is projected to grow at a 19.4% CAGR through 2031.

- By organization size, large enterprises accounted for 68.10% of the UK cloud computing market share in 2025; SMEs are advancing at a 20.1% CAGR to 2031.

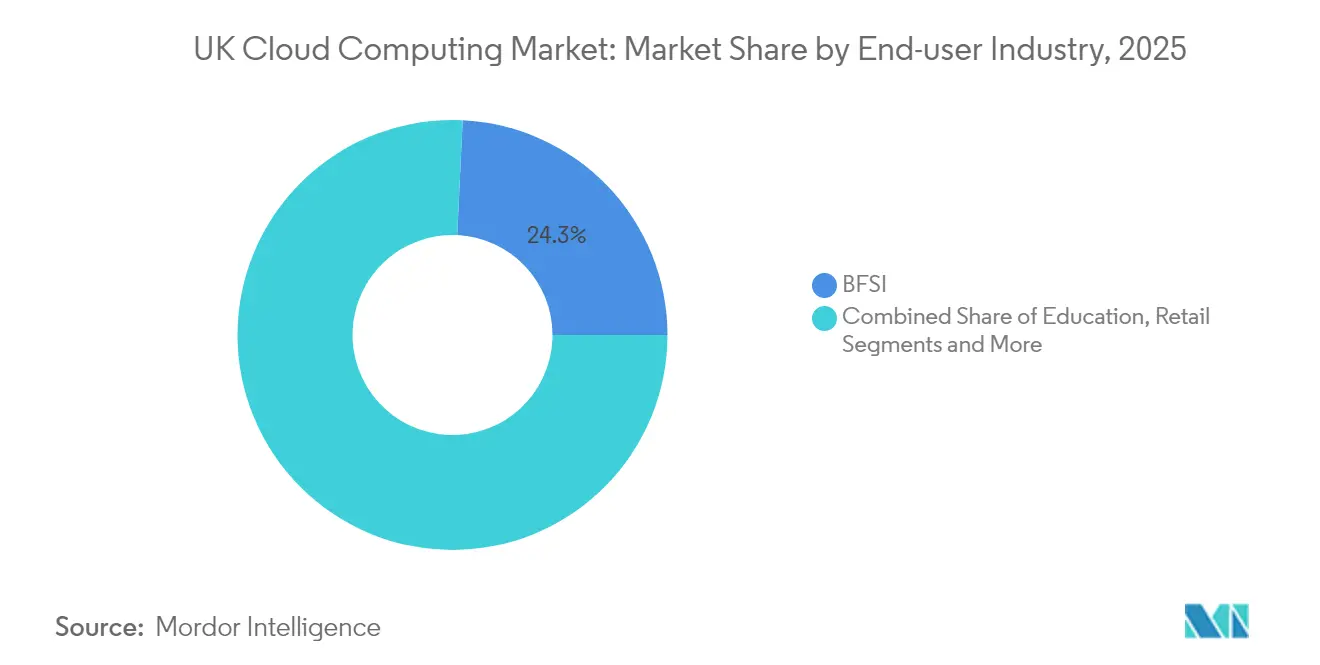

- By end-user industry, BFSI retained 24.25% share of the UK cloud computing market size in 2025; healthcare shows the highest expected CAGR at 22.6% to 2031.

- By service model, SaaS dominated with 45.15% share in 2025, while PaaS is forecast to expand at a 22.9% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United kingdom operates as part of an interconnected international environment rather than as a self-contained country level unit. The cloud computing market research by Mordor Intelligence places together all major developments across the globe within that wider frame.

UK Cloud Computing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud-First procurement and G-Cloud framework | +2.8% | England, Scotland, Wales, Northern Ireland | Medium term (2-4 years) |

| AI/ML, 5G, and IoT workload surge | +3.2% | England core, spill-over to Scotland and Wales | Long term (≥ 4 years) |

| Hybrid / multi-cloud adoption for compliance | +2.1% | England, Scotland | Medium term (2-4 years) |

| Hyperscale data-centre build-out and local-zone expansion | +2.9% | England, Northern Ireland, Scotland | Long term (≥ 4 years) |

| CMA portability remedies boosting switching incentives | +1.4% | England, Scotland, Wales | Short term (≤ 2 years) |

| Sustainability-linked cloud contracts and carbon budgets | +1.8% | England, Scotland, Wales | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cloud-First procurement and G-Cloud framework

The Crown Commercial Service awarded cloud contracts worth GBP 6.5 billion under G-Cloud 14, shifting from 12-month to 36-month terms to reduce administrative burden and encourage supplier investment.[2]Crown Commercial Service, “G-Cloud 14 – CCS,” crowncommercial.gov.uk Flagship deals such as the Department for Work and Pensions’ GBP 710 million Oracle-IBM agreement consolidate HR and finance systems, paving a template for cross-departmental data sharing. Mandatory science-based carbon targets embedded in these contracts align public spending with sustainability, setting de-facto standards later mirrored by private buyers.

AI/ML, 5G and IoT workload growth

The government’s AI Opportunities Action Plan targets a 20-fold increase in public compute capacity by 2030, spurring hyperscalers to deploy GPU-rich clusters across new local zones.[3]Data Center Frontier, “UK Government’s Bold AI Plan,” datacenterfrontier.com Edge-ready 5G networks slash latency for autonomous systems and industrial automation, while NHS pilots show ambient-voice documentation working three to five times faster than keyboard input. Nebius’s Blackwell Ultra deployment illustrates the specialised hardware profile required for next-gen AI services.

Hybrid / multi-cloud compliance push

Financial-services and healthcare boards increasingly embrace multi-vendor strategies to meet data-sovereignty and operational-resilience mandates. Legal and General cut total cost of ownership by 50% after migrating core workloads to Azure SQL Database while meeting FCA security thresholds.[4]Microsoft, “Legal and General increases safety, security, and business agility with Azure SQL DB,” microsoft.com The Data (Use and Access) Act 2025 further accelerates API-first architectures to support real-time data portability.

Hyperscale data-center build-out

Amazon’s planned GBP 40 billion UK investment from 2025-27 marks the largest tech-infrastructure outlay in national history. Critical-national-infrastructure status has streamlined approvals, catalysing projects such as CloudHQ’s GBP 1.9 billion Didcot campus and Microsoft’s GBP 106 million Leeds facility. Regional local-zone roll-outs bring compute closer to end-users, supporting latency-sensitive trading and manufacturing workloads.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cyber-attacks and data-sovereignty pressures | –1.8% | England, Scotland, Wales, Northern Ireland | Short term (≤ 2 years) |

| Skills shortage and rising FinOps costs | –2.3% | England core, spill-over to Wales and Scotland | Medium term (2-4 years) |

| Vendor lock-in from restrictive licensing | –1.2% | England, Scotland, Wales | Short term (≤ 2 years) |

| Power-grid limits and planning delays for new data centers | –1.5% | England, Scotland, Northern Ireland | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating cyber-attacks and data-sovereignty worries

Forty-three percent of UK firms reported cloud-related breaches in 2024, heightening caution around sensitive workload migration. A GBP 2.3 million fine on a genomics platform underscored tougher enforcement under updated privacy rules, prompting enterprises to insist on UK-resident data stores. Pending “Secure-by-Default” requirements for public-sector clouds could limit vendor options and elongate procurement cycles.

Cloud-skills gap and FinOps cost pressures

Research from the University of Birmingham warns that 380,000 job-equivalent positions could remain unfilled, risking a GBP 27.6 billion economic hit by 2030. Wage inflation for certified engineers and rising multi-cloud complexity elevate operating costs, especially for SMEs lacking dedicated FinOps expertise. Government spending of GBP 1.1 billion on advanced-skills training will ease long-term shortages but offers little near-term relief.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Cloud Type: Hybrid Solutions Drive Enterprise Transformation

Public environments captured 69.55% of the UK cloud computing market share in 2025, reflecting faith in hyperscale security baselines and regulatory certifications. Hybrid architectures, however, are accelerating at a 19.4% CAGR as regulated industries retain sensitive data on-premises while flexing burst workloads to the cloud. This shift supports the UK cloud computing market’s pivot toward resilient multi-cloud governance. Vodafone’s USD 1.5 billion ten-year partnership with Microsoft shows large telcos closing legacy data centers while embracing Azure regions for core operations.

Hybrid adoption also benefits from vendor concentration scrutiny: the CMA’s portability-remedy proposals are expected to lower switching friction, encouraging boards to hold dual or triple cloud contracts. Large banks now routinely tier workloads to balance latency and compliance, while NHS trusts use edge gateways to synchronise anonymised research datasets with public-cloud analytics. Together, these patterns entrench hybrid as the de-facto enterprise default inside the UK cloud computing market.

By Organization Size: SME Growth Outpaces Enterprise Adoption

Large enterprises held 68.10% revenue in 2025, underpinned by multi-year digital transformation roadmaps and deep IT benches. Yet SMEs are expanding faster at 20.1% CAGR, catalysed by simplified SaaS onboarding and government vouchers that cut entry costs. The SME Digital Adoption Taskforce advocates AI-powered helpdesks and standard e-invoicing to remove complexity, a blueprint that should unlock new subscriptions across the UK cloud computing market.

Cash-flow-aligned consumption pricing appeals to smaller firms, but skills shortages increase reliance on managed service partners. Hyperscalers have responded with SME-specific bundles that package infrastructure, productivity apps, and security monitoring. By diversifying channel partnerships, providers aim to embed themselves early in fast-growing businesses, deepening the customer pool that underpins the UK cloud computing market.

By End-user Industry: Healthcare Transformation Accelerates Digital Adoption

BFSI retained a 24.25% slice of the UK cloud computing market size in 2025, the outcome of early adoption and robust compliance frameworks. Healthcare is the breakout vertical, forecast to climb at a 22.6% CAGR through 2031 as every NHS trust races to meet the March 2026 electronic-patient-record deadline. Ambient-voice and AI triage systems ease clinician workloads, while strict residency rules keep diagnostic data inside sovereign zones, supporting vendor diversification.

Manufacturing, retail, telecom, and government follow close behind, each with sector-specific catalysts such as 5G network function virtualisation or omnichannel commerce analytics. Flexible PaaS tools let developers embed machine-learning models directly into line-of-business workflows, strengthening cloud stickiness. These sectoral dynamics collectively reinforce robust demand across the UK cloud computing market.

By Service Model: Platform Services Enable AI Innovation

SaaS accounted for 45.15% of 2025 spend, but PaaS is growing quicker at 22.9% CAGR as enterprises seek integrated data-engineering and model-training stacks. Microsoft Fabric’s addition of 21,000 paying UK customers highlights appetite for single-pane analytics workspaces. The rising dominance of developer-centric services is shifting value creation away from raw infrastructure toward higher-margin platforms, broadening monetisation options inside the UK cloud computing market.

IaaS remains critical for compute-intensive AI workloads, while BPaaS gains traction for back-office automation. Lloyds Banking Group cut mortgage-income-verification times from days to seconds after moving 80 machine-learning models onto Vertex AI, illustrating how sector leaders capture speed advantages via platform capabilities.

Geography Analysis

England dominated the UK cloud computing market in 2025 with an 84.35% share, driven by London’s finance cluster and a dense ecosystem of hyperscale data centers positioned near international fiber landing sites. High-consumption segments such as algorithmic trading and e-commerce anchor demand for sub-millisecond latency, reinforcing provider preference for London and the wider South-East. Nonetheless, land scarcity and power-availability constraints are prompting operators to favour satellite facilities in the Thames Valley and East Midlands.

Northern Ireland is the fastest-growing region, tracking a 19.2% CAGR to 2031 as renewable-energy availability and lower operating costs entice new builds. Government designation of AI Growth Zones channels incentives toward Belfast and Londonderry, attracting sovereign-cloud investments serving public-sector workloads. Scotland leverages abundant wind capacity and robust academic research to court energy-efficient data-center projects tied to its GBP 206 million NHS cloud-integration program.

Wales shows steady, if slower, expansion as Cardiff’s fintech hub matures and local councils migrate citizen-service portals to SaaS platforms. Across the four nations, streamlined planning laws and critical-infrastructure status reduce deployment barriers, while regional agencies compete on green-power tariffs and skills grants. This diffusion of capital supports national resilience and broadens addressable workloads across the UK cloud computing market.

The cloud computing market is assessed by Mordor Intelligence through a multi-layered geographic lens, covering other regions such as Europe, North America, and Asia, along with detailed country-level analysis for Italy, Spain, United States, China, South Korea, and Nigeria.

Competitive Landscape

Amazon Web Services and Microsoft Azure each command an estimated 30-40% share, forming a de facto duopoly that shapes pricing and product roadmaps. The Competition and Markets Authority’s Strategic Market Status process could impose portability and interoperability remedies, moderating lock-in and boosting multi-cloud take-up. Microsoft’s bundled licensing and reserved-instance discounts exemplify tactics used to reinforce share, while AWS leverages a deep ISV marketplace and custom silicon to reduce total cost-per-compute.

Google Cloud, IBM, and Oracle intensify mid-tier rivalry by focusing on specialist workloads. Oracle’s USD 5 billion UK infrastructure build and headline USD 30 billion multiyear cloud deal position it as a major AI hosting option. IBM’s partnership with the Hartree National Centre for Digital Innovation underlines a strategy of coupling cloud capacity with quantum-computing R&D, offering differentiated value to research-heavy clients.

Niche players such as Rackspace and OVHcloud pursue sovereignty-assured services, targeting public-sector tenders that demand UK data residency. Local specialists UKCloud and Yobitel fill compliance and managed-services gaps for SMEs. Channel integrators including Accenture and Capgemini translate hyperscaler roadmaps into vertical solutions, capturing a growing share of professional-services spend. Together, these actors keep innovation high and pricing competitive across the UK cloud computing market.

UK Cloud Computing Industry Leaders

Alibaba Group Holding Limited

Amazon Web Services (AWS)

Google LLC

IBM Corporation

Microsoft Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Oracle announced a USD 30 billion annual cloud deal expected to generate revenue starting in FY 2028; market speculation points to OpenAI as the customer.

- June 2025: Amazon Web Services revealed plans for a GBP 40 billion investment in UK cloud infrastructure from 2025-27.

- June 2025: NHS Scotland published a GBP 206 million tender for cloud integration solutions.

- April 2025: Microsoft reported record quarterly cloud revenue of USD 42 billion and added 10 new datacenter countries.

UK Cloud Computing Market Report Scope

Cloud computing provides on-demand access to computer resources, particularly data storage and processing power, without requiring users to manage them directly. Computing resources, including physical and virtual servers, data storage, networking capabilities, application development tools, software, and AI-powered analytics, are now accessible over the Internet with a pay-per-use pricing model.

The report covers cloud computing companies in the United Kingdom. The market is segmented by type (public cloud (IaaS, PaaS, and Saas), private cloud, and hybrid cloud), organization type (SMEs and large enterprises), and end-user industries (manufacturing, education, retail, transportation and logistics, healthcare, BFSI, telecom and IT, government, and public sector). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Public Cloud |

| Private Cloud |

| Hybrid Cloud |

| Small and Medium-sized Enterprises (SMEs) |

| Large Enterprises |

| Manufacturing |

| Education |

| Retail |

| Transportation and Logistics |

| Healthcare |

| BFSI |

| Telecom and IT |

| Others |

| Infrastructure-as-a-Service (IaaS) |

| Platform-as-a-Service (PaaS) |

| Software-as-a-Service (SaaS) |

| Business-Process-as-a-Service (BPaaS) |

| By Cloud Type | Public Cloud |

| Private Cloud | |

| Hybrid Cloud | |

| By Organization Size | Small and Medium-sized Enterprises (SMEs) |

| Large Enterprises | |

| By End-user Industry | Manufacturing |

| Education | |

| Retail | |

| Transportation and Logistics | |

| Healthcare | |

| BFSI | |

| Telecom and IT | |

| Others | |

| By Service Model | Infrastructure-as-a-Service (IaaS) |

| Platform-as-a-Service (PaaS) | |

| Software-as-a-Service (SaaS) | |

| Business-Process-as-a-Service (BPaaS) |

Key Questions Answered in the Report

What is the current value of the UK cloud computing market?

The UK cloud computing market size reached USD 64.97 billion in 2026.

How fast is the UK cloud computing market expected to grow?

It is projected to expand at a 15.86% CAGR, reaching USD 135.64 billion by 2031.

Which cloud service model is growing the quickest?

Platform-as-a-Service is forecast to grow at a 22.9% CAGR through 2031, driven by AI development needs.

Why are hybrid deployments gaining traction in the UK?

Regulatory data-sovereignty rules and CMA portability remedies encourage enterprises to split sensitive and elastic workloads across multiple environments.

Page last updated on: