Cloud System Management Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

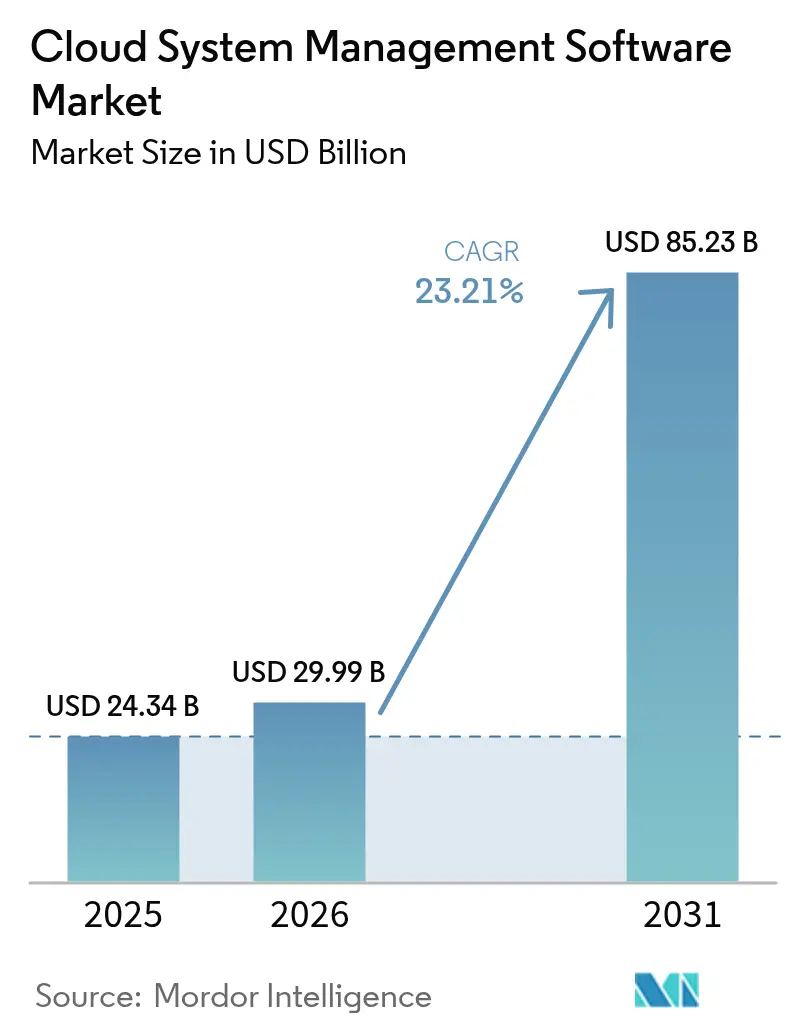

| Market Size (2026) | USD 29.99 Billion |

| Market Size (2031) | USD 85.23 Billion |

| Growth Rate (2026 - 2031) | 23.21% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cloud System Management Software Market Analysis by Mordor Intelligence

The cloud system management software market size is expected to grow from USD 24.34 billion in 2025 to USD 29.99 billion in 2026 and is forecast to reach USD 85.23 billion by 2031 at 23.21% CAGR over 2026-2031. Demand is rising as enterprises shift from reactive monitoring toward proactive, AI-enabled orchestration across multi-cloud and hybrid estates. Consolidation such as Broadcom’s integration of VMware signals strategic scale-ups, yet the arena stays sufficiently fragmented for specialist observability and automation startups to win logos. Growth also reflects board-level cost governance, the need to manage GenAI GPU clusters, and new telemetry layers tied to Scope-3 carbon accounting and quantum-safe encryption. Vendors able to unify logs, metrics, costs, and sustainability data across clouds continue to capture premium pricing power.

Key Report Takeaways

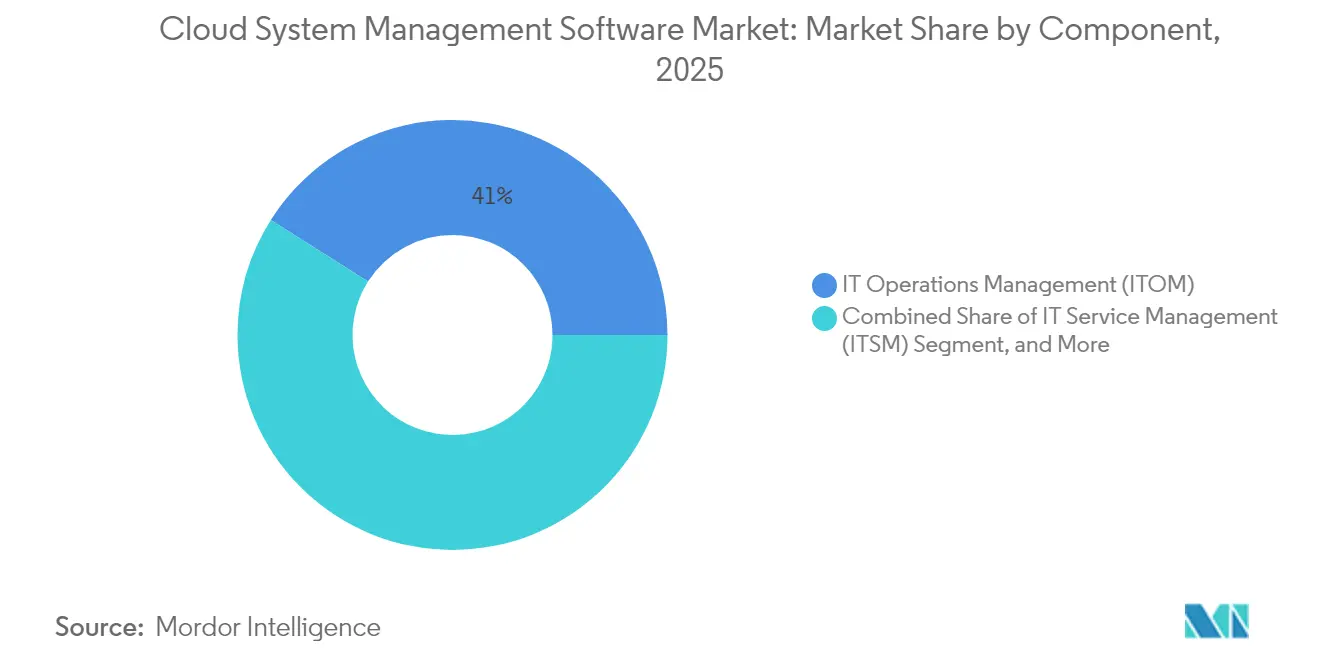

- By component, IT operations management led with 41.02% of the cloud system management software market share in 2025 while IT automation and configuration management is expanding at a 24.18% CAGR through 2031.

- By deployment model, public cloud deployments held 52.21% revenue share in 2025 in the cloud system management software market; hybrid cloud is the fastest-growing approach at a 24.42% CAGR.

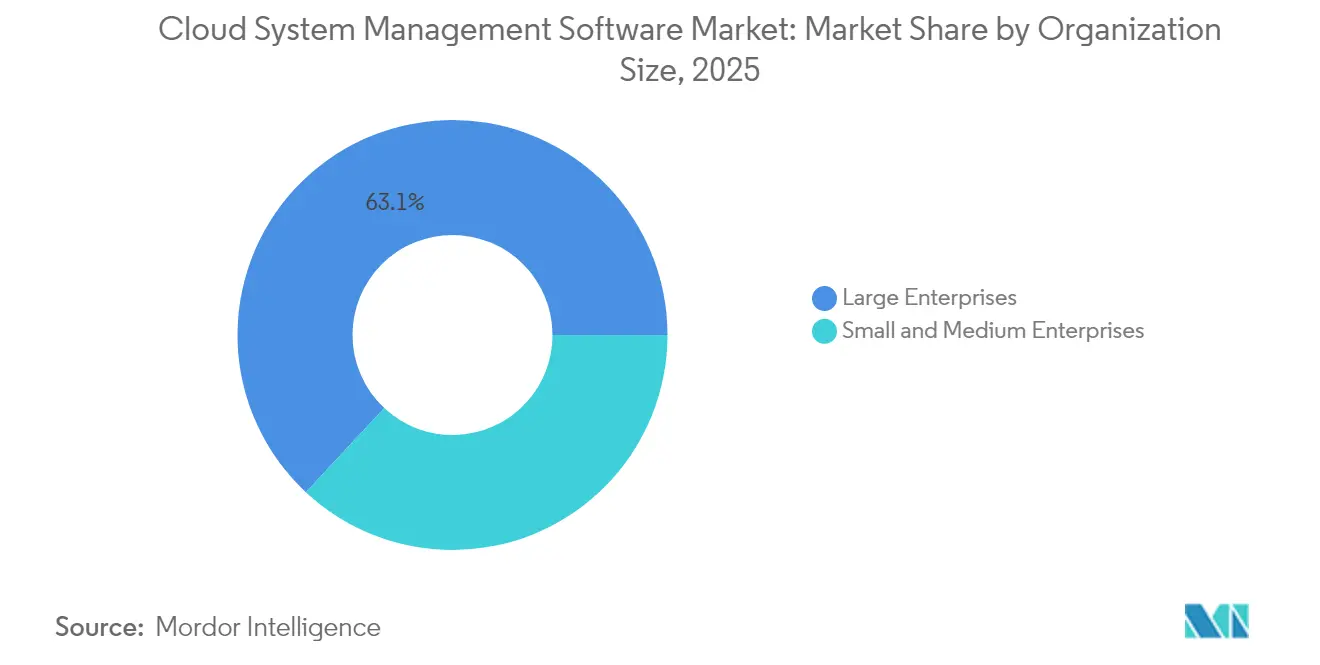

- By organization size, large enterprises accounted for 63.05% spend in 2025 in the cloud system management software market, yet small and medium enterprises are growing at a 24.58% CAGR.

- By end-user industry, IT and Telecommunications generated 29.12% of 2025 revenue in the cloud system management software market, whereas healthcare is pacing fastest at a 23.89% CAGR.

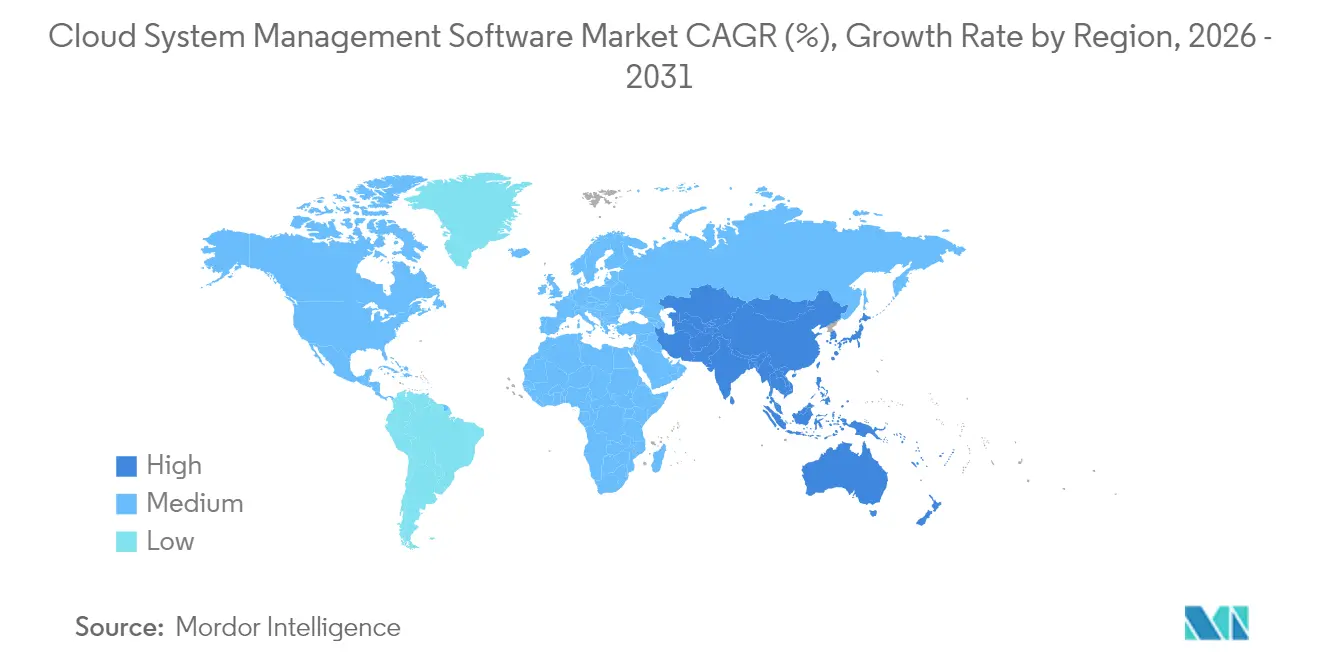

- By geography, North America contributed 38.26% of 2025 revenue in the cloud system management software market and Asia-Pacific is projected to rise at a 23.98% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cloud System Management Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Explosion of multi-cloud and hybrid adoption | +5.2% | Global, with peak intensity in North America and Europe | Medium term (2-4 years) |

| Shift-left DevOps driving demand for unified observability | +4.8% | North America, Europe, Asia-Pacific urban hubs | Short term (≤ 2 years) |

| FinOps as a board-level mandate for cloud cost control | +4.3% | Global, led by North America and Europe | Short term (≤ 2 years) |

| Emergence of GenAI-ready GPU orchestration layers | +3.9% | North America, China, select Asia-Pacific markets | Medium term (2-4 years) |

| Sustainability reporting mandates (Scope-3) embedded in CMPs | +2.7% | Europe, North America, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Quantum-safe crypto modules entering cloud management stacks | +1.9% | North America, Europe, government sectors globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Explosion of Multi-Cloud and Hybrid Adoption

Organizations ran an average of 2.6 public clouds in 2024, up from 2.2 the previous year, as visibility gaps increased with each additional provider.[1]Flexera, “2024 State of the Cloud Report,” flexera.com Platforms that normalize telemetry across AWS, Azure, and Google Cloud are displacing point tools that require manual scripting. Pre-built connectors and policy translation kits, such as Terraform providers, are speeding rollouts and boosting compliance. Enterprises now cite inconsistent tooling as the top barrier to optimization, reinforcing demand for abstraction layers that mask proprietary APIs.

Shift-Left DevOps Driving Demand for Unified Observability

DevOps teams instrument code at commit time, shrinking mean-time-to-resolution by 40% and elevating observability to a developer concern. Unified platforms correlate traces, metrics, and business KPIs, enabling engineers to identify misconfigurations before users are affected. New Relic customers who employ full-stack observability reduce alert noise by 35%. Datadog’s 2024 purchase of Bits AI pulled LLM-powered root-cause analysis into mainstream operations, turning plain-language explanations into a differentiator.

FinOps as a Board-Level Mandate for Cloud Cost Control

With cloud bills now scrutinized by CFOs, real-time budget alerts and chargeback models are shifting management suites from IT utilities to financial governance platforms. Companies adopting automated rightsizing and idle-resource reclamation have lowered waste by nearly one-third within six months according to hyperscaler case studies.[2]AWS, “Carbon-Aware Workload Placement,” aboutamazon.com Leading suites surface idle resources, reserved-instance gaps, and anomaly detection that flags spend spikes in minutes rather than weeks.

Emergence of GenAI-Ready GPU Orchestration Layers

Training and fine-tuning large language models consumes bursty GPU clusters. Cloud management platforms that schedule accelerators across on-premises and public resources now push utilization rates into the mid-80% range, up from historical baselines of around 60%. Features such as automated spot bidding and multi-region failover deliver up to 40% savings on training workloads. Enterprises therefore prize unified schedulers that pair GPU efficiency with workload-level cost attribution.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating cyber-attacks on control planes | -2.8% | Global, acute in North America and Europe | Short term (≤ 2 years) |

| Persistent skills shortage in cloud operations and AIOps | -2.1% | Global, most severe in Asia-Pacific and emerging markets | Medium term (2-4 years) |

| Opaque licensing of proprietary telemetry APIs | -1.6% | Global, particularly affecting multi-cloud enterprises in North America and Europe | Medium term (2-4 years) |

| Edge-to-cloud data-sovereignty fragmentation | -1.4% | Europe, Asia-Pacific, Middle East, with regulatory spillover to other regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Cyber-Attacks on Control Planes

Centralized control planes hold high-value credentials and configuration data. The 2024 Snowflake breach, traced to compromised admin accounts, exposed multi-tenant risks and drove firms to adopt hardware-backed MFA and immutable audit logs. Similar incidents at identity providers heightened scrutiny on third-party integrations. Regulatory agencies now recommend zero-trust architectures that enforce least privilege and continuous authentication. Vendors unable to demonstrate rigorous security controls often face longer procurement cycles, particularly in regulated industries.

Persistent Skills Shortage in Cloud Operations and AIOps

It is estimated that there is a global deficit of millions of persons, cloud architects, and site-reliability engineers. SMEs struggle most, lacking budgets for specialist staff capable of tuning anomaly-detection thresholds or interpreting AI-generated root-cause analyses. Vendors embed guided workflows, pre-built dashboards, and natural language queries to lower barriers. Yet, advanced users often require deeper configurability. Cloud-provider certification programs are expanding, but the talent pipeline remains at least 18–24 months behind demand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Automation Gains as DevOps Matures

IT Automation and Configuration Management is on track to post a 24.18% CAGR, the quickest clip among components as organizations replace manual scripts with declarative infrastructure-as-code. The cloud system management software market size for IT Automation is projected to grow from USD 9.67 billion in 2025 to USD 35.45 billion by 2031. HashiCorp Terraform’s vendor-neutral language now governs thousands of resource types, reinforcing demand for tools that span public clouds and on-premises systems. IT Operations Management retained a 41.02% market share of cloud system management software in 2025, as unified observability remains foundational. Acquisitions, such as Cisco's acquisition of Splunk, fuse network telemetry with application traces to close visibility gaps.

Enterprises are increasingly seeking platforms that cover provisioning, configuration, runtime monitoring, and service management from end to end. Kubernetes-native projects, such as Argo CD and Flux, extend GitOps workflows, while ITSM suites integrate AI chat to resolve tickets more efficiently. For teams with legacy estates, agentless discovery and drift detection expedite migration roadmaps and reduce toil. The convergence of observability with automation positions vendors offering cohesive portfolios to out-execute niche point solutions.

By Deployment Model: Hybrid Architectures Surge on Sovereignty Concerns

Public cloud kept 52.21% revenue in 2025, yet hybrid models are expanding at a 24.42% CAGR as data-sovereignty mandates rise. The cloud system management software market size for hybrid cloud solutions is forecast to exceed USD 44.8 billion by 2031. EU rules now require providers to enable data portability without punitive fees, strengthening demand for open orchestration layers like Kubernetes that abstract workload placement. AWS Outposts, Azure Arc, and Google Anthos push public-cloud APIs into customer data centers, giving teams one control plane for disparate resources.

Private clouds remain relevant for regulated workloads but grow slower due to capital intensity. Enterprises adopt hybrid so analytics can burst to hyperscale regions while personally identifiable information stays on-premises. Unified cost allocation, security posture management, and observability across locations therefore become non-negotiable. Vendors lacking feature parity between on-premises and public endpoints risk churn as customers consolidate around consistent experiences.

By Organization Size: SMEs Narrow the Gap with SaaS Platforms

Large enterprises contributed 63.05% of 2025 spending thanks to sprawling multi-cloud estates that demand sophisticated governance. However, SMEs are accelerating at a 24.58% CAGR as consumption-based pricing and no-install SaaS onboarding lower barriers. The cloud system management software market size for SME buyers is set to surpass USD 23.6 billion by 2031. Vendors like Datadog and New Relic court this cohort with free or low-cost tiers and guided setups that turn value visible in hours.

Ease of use ranks higher than deep configurability for mid-market firms without dedicated SRE teams. Natural-language queries, automated baselining, and prescriptive remediation reduce the skills dependency highlighted earlier. Conversely, large enterprises continue to demand granular role-based access controls, custom integrations, and API extensibility to fit complex IT service catalogs. Modular product lines that allow each segment to adopt features at its own pace now differentiate market leaders.

By End-User Industry: Healthcare Accelerates on EHR Migrations

IT and Telecommunications retained 29.12% of 2025 revenue as operators leverage cloud management to monetize 5G edge computing. The healthcare and Life Sciences Sectors show the fastest trajectory, advancing at a 23.89% CAGR to 2031, driven by the modernization of electronic health records and the scale-out of telemedicine. The cloud system management software market share for healthcare is forecast to climb above 12.34% by the end of the decade as HIPAA and similar rules demand audit-ready logging and encryption-key rotation.

BFSI sectors embed cost-governance dashboards directly into consoles to cap real-time spending, while manufacturing orchestrates factory IoT telemetry with ERP backends for predictive maintenance. Retail chains correlate point-of-sale feeds with inventory analytics to inform dynamic pricing, and logistics firms automate route optimization across hybrid clouds. Each vertical value unifies visibility while tailoring policies around its own compliance frameworks, making configurable reporting templates a key feature.

Geography Analysis

North America led the cloud system management software market in 2025 with 38.26% revenue, supported by early AIOps adoption and stringent breach-notification statutes that raise the premium on centralized security-event correlation. U.S. enterprises also benefit from the regional presence of hyperscalers and a dense ecosystem of observability startups, which accelerates innovation and partnership velocity. Consolidation moves such as Broadcom–VMware and Cisco–Splunk accentuate competition and keep spending momentum high among Fortune 500 users seeking integrated control planes.

The Asia-Pacific region is projected to post the fastest growth rate of 23.98% through 2031. India’s public-sector cloud mandate requires government data to stay within national borders under the MeghRaj framework, driving hybrid architectures that blend local data centers with hyperscale capacity. China’s cybersecurity and data-security laws push critical infrastructure operators toward sovereign-cloud stacks anchored by domestic providers. Japan’s digital agency initiatives further draw enterprises into managed platforms that unify cost, sustainability, and security metrics across vendors.

Europe sits at the center of data-sovereignty debate, with GDPR and the 2024 EU Data Act prompting enterprises to keep sensitive workloads on-premises while bursting analytics to the public cloud. Germany’s BSI promotes multi-cloud designs to mitigate vendor lock-in, spurring adoption of open orchestration layers. Middle East sovereign-wealth-fund investments in hyperscale facilities shorten latency for local enterprises, while Africa’s mobile-first economies value lightweight, API-driven suites that function over constrained bandwidth. Latin America’s GDPR-style regulations likewise accelerate adoption of management tools with granular access controls and auditability.

Competitive Landscape

The cloud system management software industry remains moderately fragmented. The top five vendors, VMware (Broadcom), Microsoft, AWS, ServiceNow, and IBM, held an estimated 48% share in 2024, with no single firm above 15%. Broadcom’s integration of VMware tightened hybrid-cloud licensing strategies, but customer unease over pricing opens space for open-source alternatives such as Red Hat OpenShift and Terraform. IBM’s 2024 acquisition of HashiCorp strengthened its multi-cloud automation play, adding a declarative layer that spans hyperscalers.

Hyperscalers bundle native cost, security, and observability features into consumption pricing, encouraging single-vendor loyalty. Yet specialized providers thrive by tackling cross-cloud pain points, offering API-first architectures, and focusing on root-cause analysis powered by large language models. Datadog reported 32% year-on-year revenue growth in 2025 as customers sought unified monitoring for Kubernetes, serverless, and edge workloads. New Relic, Dynatrace, Harness, and CloudBolt differentiate via usage-based licensing, continuous deployment hooks, and policy-as-code frameworks.

Strategic moves emphasize AI and sustainability. IBM filed dozens of patents for predictive capacity algorithms, while Google Cloud’s intellectual-property focus lies in carbon-aware scheduling and quantum-safe key rotation. Cisco’s absorption of Splunk blends network and security telemetry into a single analytics lake. Smaller disruptors exploit hyperscaler blind spots, edge-to-cloud orchestration, multi-cloud cost attribution, and compliance for niche regulations, to win accounts resistant to vendor lock-in.

Cloud System Management Software Industry Leaders

IBM Corporation

Microsoft Corporation

Vmware Inc.

BMC Software Inc.

Cisco Systems Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Microsoft released Azure Monitor Predictive Insights for general use. The service applies machine-learning models to forecast resource strain and performance slow-downs up to 72 hours before they occur, then works with Azure Resource Manager to spin up extra capacity automatically, a shift that has already cut unexpected downtime by roughly 40% in early rollouts

- October 2025: Datadog introduced Cloud Cost Intelligence, a FinOps add-on that links infrastructure spend with business metrics such as revenue per transaction and customer-acquisition cost. Generative-AI recommendations now guide engineers toward architecture changes that balance price and performance, answering growing CFO demands for real-time ROI tracking

- September 2025: AWS unveiled the Amazon CloudWatch Sustainability Dashboard, giving teams live carbon-emissions data at the workload level and suggesting where to move batch jobs into regions rich in renewable power. The dashboard ties into the AWS Carbon Footprint Tool and aligns with Scope-3 reporting rules under the EU Corporate Sustainability Reporting Directive

- August 2025: Google Cloud expanded its Confidential Computing lineup by adding post-quantum encryption for Kubernetes control planes, adopting NIST-approved CRYSTALS-Kyber algorithms to shield cluster traffic against future quantum threats, a move welcomed by federal and defense clients seeking long-term cryptographic resilience

Global Cloud System Management Software Market Report Scope

The cloud system management software market refers to the market for software solutions designed to manage and optimize cloud-based systems and services. These solutions enable organizations to monitor, automate, and control their cloud infrastructure, ensuring efficient operations and resource utilization.

The Cloud System Management Software Market Report is Segmented by Component (IT Operations Management, IT Service Management, IT Automation and Configuration Management), Deployment Model (Public Cloud, Private Cloud, Hybrid Cloud), Organisation Size (Large Enterprises and Small and Medium Enterprises), End-User Industry (IT and Telecommunications, Banking, Financial Services and Insurance (BFSI), Healthcare and Life Sciences, Manufacturing, Retail and Consumer Services, Transport and Logistics, Media and Entertainment, Government and Public Sector), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| IT Operations Management (ITOM) |

| IT Service Management (ITSM) |

| IT Automation and Configuration Management (ITACM) |

| Public Cloud |

| Private Cloud |

| Hybrid Cloud |

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| IT and Telecommunications |

| Banking, Financial Services and Insurance (BFSI) |

| Healthcare and Life Sciences |

| Manufacturing |

| Retail and Consumer Services |

| Transport and Logistics |

| Media and Entertainment |

| Government and Public Sector |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Component | IT Operations Management (ITOM) | ||

| IT Service Management (ITSM) | |||

| IT Automation and Configuration Management (ITACM) | |||

| By Deployment Model | Public Cloud | ||

| Private Cloud | |||

| Hybrid Cloud | |||

| By Organisation Size | Large Enterprises | ||

| Small and Medium Enterprises (SMEs) | |||

| By End-user Industry | IT and Telecommunications | ||

| Banking, Financial Services and Insurance (BFSI) | |||

| Healthcare and Life Sciences | |||

| Manufacturing | |||

| Retail and Consumer Services | |||

| Transport and Logistics | |||

| Media and Entertainment | |||

| Government and Public Sector | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Netherlands | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the Cloud system management software market?

The market is valued at USD 29.99 billion in 2026 and is forecast to reach USD 85.23 billion by 2031.

Which component is growing fastest within this space?

IT Automation and Configuration Management leads growth, expanding at a 24.18% CAGR as organizations adopt infrastructure-as-code and policy-as-code workflows.

Why are hybrid deployments outpacing public-only deployments?

Data sovereignty mandates and latency-sensitive workloads drive enterprises to blend on-premises and multiple cloud providers, producing a 24.42% CAGR for hybrid approaches.

Which industry will see the highest adoption through 2031?

Healthcare and Life Sciences, propelled by electronic health record migrations and stringent compliance needs, is anticipated to record a 23.89% CAGR.

What regions are poised for the fastest market expansion?

Asia-Pacific is projected to grow at 23.98% CAGR thanks to sovereign-cloud mandates in India and China and digital-government programs in Japan.

Page last updated on: