India Cloud Computing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

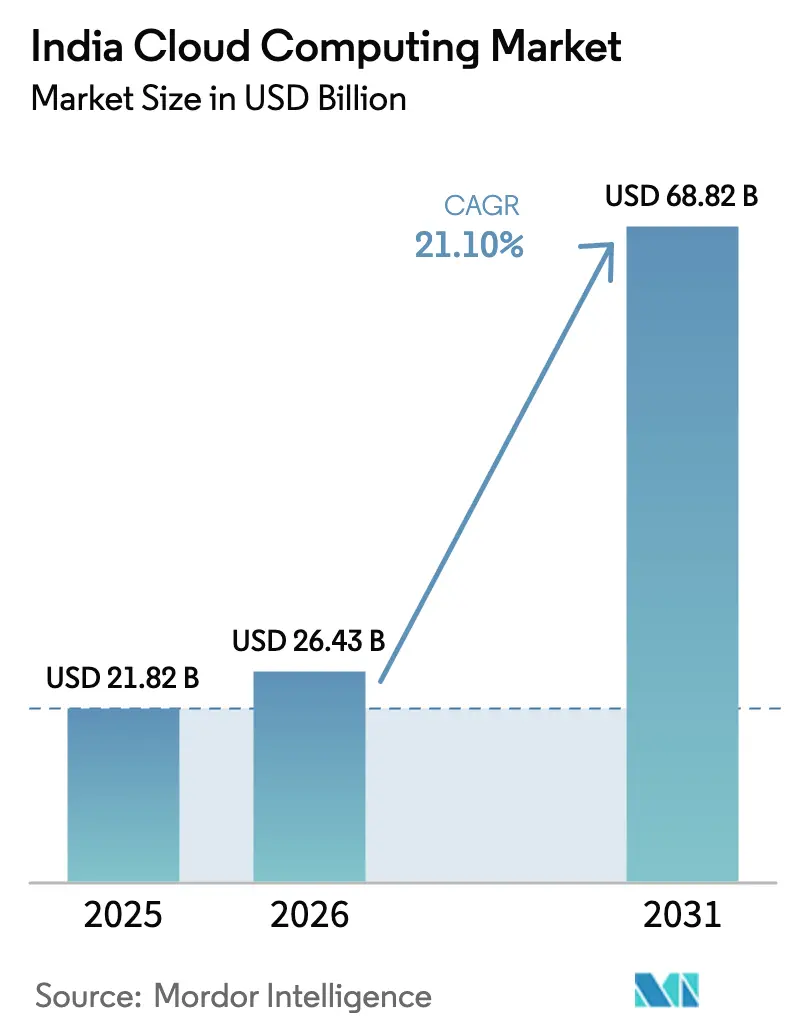

| Base Year Market Size (2025) | USD 21.82 Billion |

| Market Size (2026) | USD 26.43 Billion |

| Market Size (2031) | USD 68.82 Billion |

| Growth Rate (2026 - 2031) | 21.10% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Cloud Computing Market Analysis by Mordor Intelligence

India Cloud Computing Market size in 2026 is estimated at USD 26.43 billion, growing from 2025 value of USD 21.82 billion with 2031 projections showing USD 68.82 billion, growing at 21.10% CAGR over 2026-2031. Accelerated public-sector digitization, robust hyperscale investments, and the continued shift of enterprises toward data-intensive workloads give the India cloud computing market sustained momentum. Government data-sovereignty mandates, rising AI adoption, and an expanding base of small and medium enterprises (SMEs) deepen the addressable pool of cloud users, while datacenter build-outs in multiple regions compress latency and support real-time applications. Enterprises pivot from lift-and-shift migrations to platform-centric transformations that bundle infrastructure, data, and intelligence capabilities, thereby lifting average cloud spending per workload. At the same time, energy requirements for expanding datacenter footprints and lingering semiconductor tightness create cost and supply constraints that providers must navigate.

Key Report Takeaways

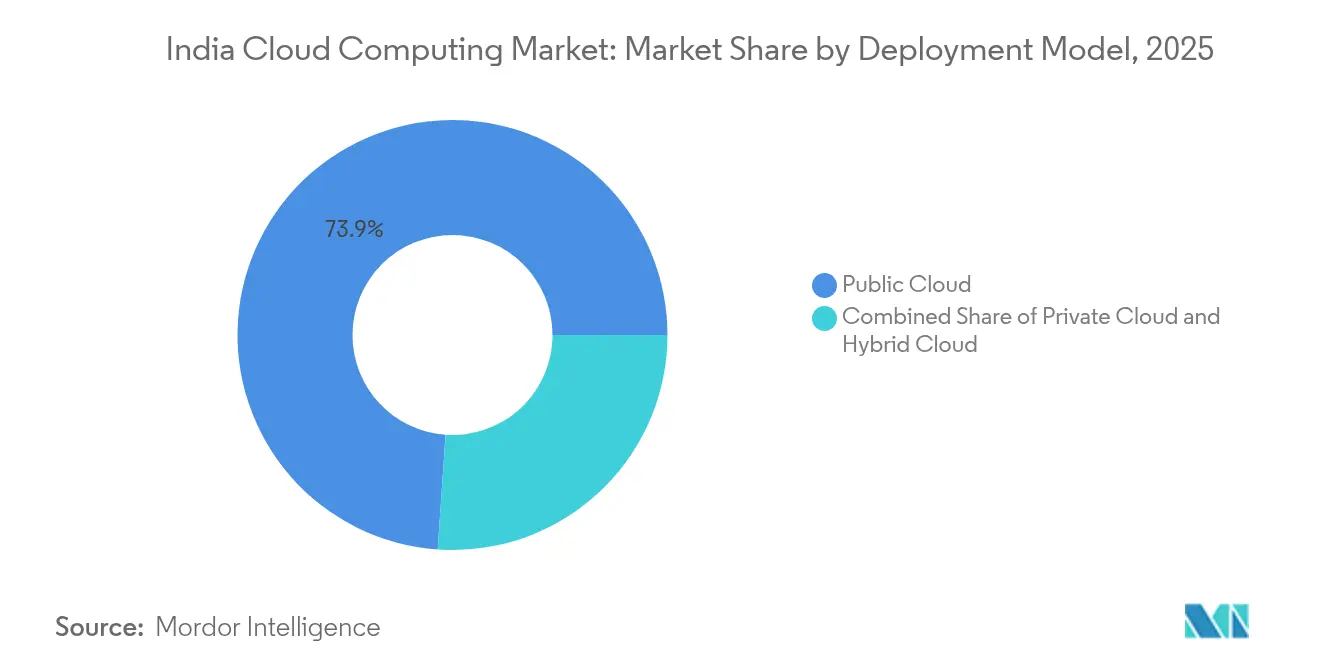

- By deployment model, public cloud led with 73.90% of the India cloud computing market share in 2025; hybrid cloud is forecast to expand at 27.20% CAGR through 2031.

- By service type, Software-as-a-Service captured 54.40% revenue share in 2025, while AI/ML Platform-as-a-Service is expected to accelerate at 30.30% CAGR to 2031.

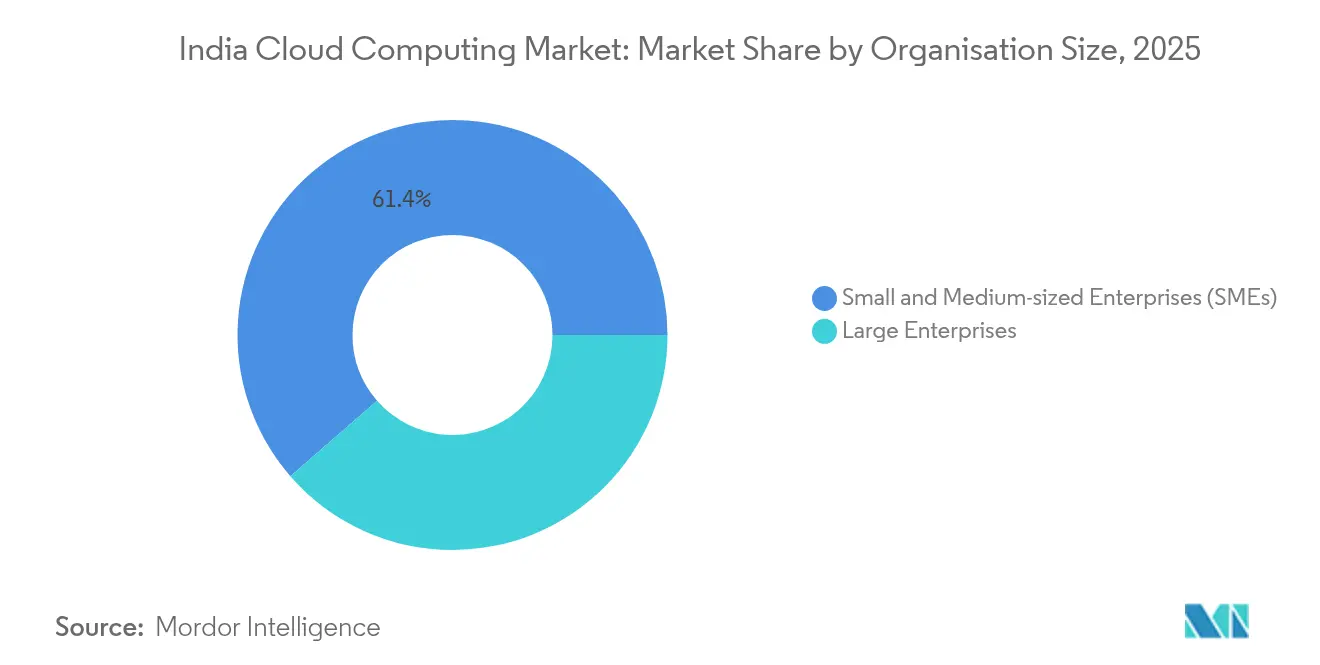

- By organisation size, SMEs accounted for 61.40% adoption in 2025 and are growing at 23.40% CAGR, highlighting the democratization of the India cloud computing market.

- By industry vertical, the BFSI segment held 18.60% revenue share in 2025; Healthcare and Life Sciences is projected to log the highest CAGR at 28.10% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Projections can easily extend beyond country and regional trends as they are defined by movement across the full international system. Mordor Intelligence's worldwide cloud computing market outlook captures this forward trajectory.

India Cloud Computing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government-driven cloud-first push under Digital India | +4.2% | National; early traction in Delhi, Mumbai, Bengaluru | Medium term (2–4 years) |

| Enterprise-wide digital transformation surge | +5.8% | National; strongest in metropolitan clusters | Short term (≤2 years) |

| Rapid build-out of hyperscale and edge datacenters | +3.9% | West and South, expanding nationwide | Long term (≥4 years) |

| RBI-led sovereign-cloud mandate for regulated sectors | +2.7% | Major BFSI hubs country-wide | Short term (≤2 years) |

| Generative-AI workloads needing GPU-dense instances | +4.1% | Tech corridors in Bengaluru, Hyderabad, Pune | Medium term (2–4 years) |

| Uptake of industry-specific clouds in heavily regulated sectors | +1.8% | Sector-focused, nationwide | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Government Cloud-First and Digital India Policies

The MeghRaj framework positions cloud as the default option for public systems, with more than 300 citizen services earmarked for migration. Explicit data-protection statutes now provide clarity on storage location, retention obligations, and cross-border transfer approvals, which lowers compliance risk for enterprises that want to host regulated workloads in the India cloud computing market. Consistent political sponsorship keeps funding streams open, enabling distributed government datacenters that extend coverage beyond Tier-1 cities. The result is a multiplier effect: public-sector success stories validate cloud economics and trigger similar moves in private enterprises, stimulating broader market demand.[1]Times of India Bureau, “Digital India Turns Ten,” timesofindia.indiatimes.com

Digital Transformation Boom Across Enterprises

Indian companies migrate core applications to cloud platforms to sustain competitiveness in faster product cycles and data-driven decision making. Leading IT service providers establish business units dedicated to cloud-native solutions, redirecting workforce reskilling toward platform engineering and AI accelerators. Cloud-enabled ERP rollouts shave processing times on mission-critical workflows, while new capabilities around predictive analytics justify additional workload placements. Multinational corporations continue to establish Global Capability Centers that rely on domestically hosted cloud regions for audit compliance and latency needs. As project scopes tilt toward AI, budgets move from basic compute to higher-value services, deepening provider revenue per client.

Explosive Build-Out of Hyperscale and Edge Datacentres

Installed IT load crossed 1,000 MW in 2024 and is on course for another growth spurt as global and domestic investors earmark billions of USD for capacity. Hyperscalers place facilities in Hyderabad, Chennai, and Mumbai, while local conglomerates commit multi-gigawatt builds that rely on green-energy tie-ups. Edge nodes in Tier-2 cities bring compute closer to end users, allowing low-latency use cases such as autonomous factory equipment and high-frequency trading. Infrastructure growth redistributes regional supply, narrows price gaps across metros, and lowers entry barriers for smaller firms to join the India cloud computing market.

Sovereign-Cloud Push by RBI for Regulated Sectors

The central bank’s localization norms now require payment data to be stored domestically within 24 hours, spawning demand for certified sovereign clouds that combine modern elasticity with jurisdictional control. A forthcoming RBI-backed platform will target financial institutions needing purpose-built compliance hooks such as continuous audit logs and granular encryption. These frameworks also influence insurance, capital-markets, and fintech companies that seek uniform governance across their multi-cloud estates. Providers that integrate hardware root-of-trust and domestic security operations centers gain preferential status, steering regulated workloads into Indian facilities.[2]Reuters Staff, “India’s Central Bank Plans Sovereign Cloud,” reuters.com

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing cyber-threat surface and data-sovereignty concerns | –2.8% | Nationwide; acute in BFSI and healthcare | Short term (≤2 years) |

| Complex legacy-IT migrations and talent shortages | –3.2% | Nationwide; sharper in traditional industries | Medium term (2–4 years) |

| Unreliable grid power inflating datacenter operating costs | –2.1% | Nationwide; acute in tier-2/3 cities and industrial belts | Long term (≥4 years) |

| Limited local semiconductor supply chain | –1.4% | Nationwide; exposed to global dependency risks | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Escalating Cyber-Attack Surface and Data-Sovereignty Risks

Rapid workload migration broadens the threat landscape, and healthcare’s heightened breach frequency sharpens focus on cyber resilience. Multi-cloud estates dilute perimeter controls, forcing enterprises to adopt zero-trust principles that rely on continuous verification of users, devices, and data flows. Attackers deploy AI tools to bypass traditional defenses, raising the baseline for required security investments. Regulators heighten penalties for breaches involving sensitive personal data, compelling firms to implement robust encryption and sovereign-storage measures, which, in turn, add complexity and cost.[3]Data Security Council of India, “DSCI Digest 2025,” dsci.in

Legacy-IT Migration Complexity and Skills Deficit

Decades-old mainframes, proprietary interfaces, and line-of-business customizations hinder straightforward cloud moves. Modernization demands refactoring codebases, orchestrating data pipelines, and training staff on containerized architectures. Supply of certified cloud architects and site-reliability engineers remains tight, leading to project delays and budget overruns. External shocks, such as global semiconductor shortages and macroeconomic uncertainty, exacerbate resource constraints and slow procurement, weighing on overall growth trajectories.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Hybrid Architectures Drive Enterprise Flexibility

Hybrid deployments expand at a 27.20% CAGR even though public clouds retained 73.90% of the India cloud computing market in 2025. Enterprises mix on-premises resources with multiple hyperscale regions, aligning workloads with performance, cost, and compliance needs. Financial institutions host customer-facing microservices in the cloud for elasticity and keep core banking engines on private clusters to meet regulatory audits. Sovereign-cloud options add a third layer, allowing regulated entities to comply with data-residency requirements without foregoing scalability.

Enterprises anchor AI experimentation in public clouds where GPU capacity scales on demand, then revert to hybrid footprints once usage stabilizes. Edge integrations streamline data flows between factory devices and regional nodes, eliminating latency bottlenecks. Managed connectivity services simplify network provisioning across clouds, and unified control planes bring observability to dispersed environments, thereby easing operations teams’ workload.

By Service Type: AI-Driven Platform Services Reshape Value Propositions

Software-as-a-Service maintained 54.40% share in 2025, but growth is now tilted toward AI/ML Platform-as-a-Service, which registers a 30.30% CAGR. Integrated toolchains that combine data lakes, model training pipelines, and governance functions encourage enterprises to focus on business outcomes rather than infrastructure management. Function-as-a-Service gains momentum for event-driven use cases, while Infrastructure-as-a-Service persists for workloads that demand control over virtual machines and storage tiers.

Healthcare firms gravitate to AI-ready platforms that bundle imaging recognition, clinical-decision support, and controlled data-sharing. Manufacturers deploy IoT-enabled platforms that capture sensor telemetry and feed predictive-maintenance models. The interplay of service types drives a layered consumption pattern where enterprises start with infrastructure, move to SaaS for horizontal processes, and settle on platform services for innovation.

By Organisation Size: SME Cloud Democratization Accelerates

SMEs accounted for 61.40% adoption in 2025 and will compound at 23.40% annually as pay-as-you-go offerings lower entry barriers. Subscription models cut capital expenditure, letting smaller firms deploy ERP, analytics, and AI features once exclusive to large enterprises. Targeted government programs under Digital India subsidize onboarding costs and provide training resources, widening the talent pool for cloud operations.

Large enterprises still dominate absolute spend, especially on multi-cloud governance, cybersecurity, and specialized AI accelerators. They increasingly transform procurement practices to favor outcome-based contracts that frame cloud as an operational expense aligned with revenue streams. The divergent needs of SMEs and large firms create tiered market opportunities for providers ranging from plug-and-play SaaS suites to customized platform builds.

By Industry Vertical: Healthcare Leads Digital Health Revolution

Healthcare and Life Sciences is projected to grow 28.10% annually, propelled by telemedicine, AI-aided diagnostics, and electronic health-records modernization that demand scalable compute and compliant storage. The BFSI sector, which holds 18.60% share of the India cloud computing market size, shifts attention from core migrations to advanced analytics and fraud-detection models executed in real time.

Manufacturers leverage cloud-powered digital twins and IoT telemetry to optimize processes and reduce downtime. Retail and e-commerce employ cloud analytics to refine inventory positioning and personalize consumer experiences, while energy utilities use cloud IoT platforms for smart-grid control. Each vertical’s maturity level shapes workload priorities, determining whether investments flow to infrastructure, platform, or AI services.

By Workload: AI/ML Workloads Transform Computing Paradigms

Core compute and storage sustained a 40.90% share in 2025; however, AI/ML and generative-AI workloads expand at 34.20% CAGR as enterprises pivot to intelligence-centric operations. GPU clusters, model repositories, and vector databases turn into essential service layers. Insights from predictive analytics feed back into business processes, spawning iterative demand for additional compute cycles.

Analytics workloads continue steady growth as firms integrate streaming data into decision loops. ERP, CRM, and HR migrate to multi-tenant SaaS suites that promise lower maintenance and faster innovation. Disaster-recovery and backup remain foundational but are increasingly automated through policy-driven scheduling, freeing IT staff to focus on higher-value initiatives.

Geography Analysis

The West’s 38.10% stake mirrors its concentration of banking, fintech, and manufacturing clients that pursue sophisticated multi-cloud deployments. Hyperscalers deepen footprints near Mumbai to meet BFSI data-residency mandates, while adjoining Pune benefits from colocated disaster-recovery zones and engineering hubs. Continuous power-supply improvements and fiber upgrades maintain region-wide service-level agreements needed for mission-critical workloads.

The South’s faster growth arises from proactive state policies that court capital-expenditure commitments with land-allocation support, renewable-energy linkages, and streamlined permits. Hyderabad attracts GPU-intensive workloads due to cooler climate zones that lower cooling costs, and Chennai’s port connectivity supports equipment imports. Bangalore’s established developer ecosystem seeds rapid uptake among digital natives and start-ups, which in turn expands ancillary demand for managed services.

Northern adoption accelerates through central-government workloads migrating under the MeghRaj scheme and the new sovereign-cloud framework. Delhi-NCR’s enterprise belt demands low-latency access to policymaking agencies and regulators, while proximity to academic institutions fosters research collaborations in AI and cybersecurity. Eastern India remains early in its build-out cycle yet benefits from the Guwahati datacenter that shortens latency for the northeast corridor, spurring digital inclusion projects and expanding the India cloud computing market footprint.

The cloud computing market is analyzed by Mordor Intelligence across multiple other geographies, with in-depth regional assessments available for South America, North America, and Europe. This is complemented by country-specific insights for Japan, China, Brazil, Canada, Spain, and France, reflecting various localized market behavior and policy environments' coverage.

Competitive Landscape

The India cloud computing market features global hyperscalers—Amazon Web Services, Microsoft Azure, and Google Cloud—that supply elastic infrastructure and advanced AI services. Domestic integrators such as Tata Consultancy Services, Infosys, and Wipro complement these offerings with localized compliance solutions, sovereign-cloud overlays, and vertical accelerators that bridge legacy migrations. Market concentration is moderate because no provider exceeds a dominant threshold, while customer preference for multi-cloud strategies disperses workloads across vendors.

Strategic moves underscore intensifying rivalry. AWS pledged USD 8.2 billion for additional datacenters that embed renewable-energy sourcing, reinforcing power sustainability commitments. Microsoft earmarked USD 3 billion to expand AI infrastructure and skill programs, strengthening hybrid-cloud positioning through integrated edge stacks. Google Cloud opened a Delhi region to address public-sector proximity mandates and partnered with local firms to launch industry clouds for healthcare and retail.

Domestic players advance from systems-integration roots into platform models. Tata Consultancy Services unveiled a sovereign-cloud network that packages compliance, data-protection, and AI toolkits; Infosys extended its AI-powered Cobalt cloud portfolio; and Wipro rolled out edge-computing frameworks to capture industrial IoT demand. Specialized providers, including ESDS, target cooperative banks with community clouds that blend low-cost infrastructure and regulatory alignment. High-performance GPU capacity and low-carbon datacenter footprints differentiate service portfolios as enterprises weigh performance, sustainability, and sovereignty factors.

India Cloud Computing Industry Leaders

Alibaba Group Holding Limited

Amazon Web Services (AWS)

Google LLC

IBM Corporation

Microsoft Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Amazon Web Services confirmed USD 8.2 billion investment in Maharashtra to expand datacenter capacity and renewable-energy integration.

- February 2025: Tata Power selected Amazon Web Services for grid modernization using AI, IoT, and analytics.

- February 2025: Tata Consultancy Services broadened its alliance with Google Cloud to deliver generative-AI solutions across verticals.

- January 2025: Microsoft announced USD 3 billion for new AI and cloud infrastructure projects across India.

India Cloud Computing Market Report Scope

Cloud computing provides on-demand access to computer resources, especially data storage and processing power, without the user needing direct management. Computing resources, including physical and virtual servers, data storage, networking capabilities, application development tools, software, and AI-powered analytics, are now accessible over the Internet with a pay-per-use pricing model.

The report covers India's cloud computing companies, and the market is segmented by type (public cloud, private cloud, and hybrid cloud), organization type (SMEs and large enterprises), and end-user industries (manufacturing, education, retail, transportation and logistics, healthcare, BFSI, telecom and IT, and government and public sector). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Public Cloud |

| Private Cloud |

| Hybrid Cloud |

| Infrastructure-as-a-Service (IaaS) |

| Platform-as-a-Service (PaaS) |

| Software-as-a-Service (SaaS) |

| Function-as-a-Service (FaaS) |

| Small and Medium-sized Enterprises (SMEs) |

| Large Enterprises |

| BFSI |

| Manufacturing |

| Retail and E-commerce |

| Healthcare and Life-Sciences |

| Telecom and IT |

| Government and Public Sector |

| Transportation and Logistics |

| Others |

| Core Compute and Storage |

| Analytics and Big-Data |

| AI / ML and Gen-AI |

| Business Applications (ERP/CRM/HR) |

| Disaster Recovery and Backup |

| Collaboration and Productivity |

| By Deployment Model | Public Cloud |

| Private Cloud | |

| Hybrid Cloud | |

| By Service Type | Infrastructure-as-a-Service (IaaS) |

| Platform-as-a-Service (PaaS) | |

| Software-as-a-Service (SaaS) | |

| Function-as-a-Service (FaaS) | |

| By Organisation Size | Small and Medium-sized Enterprises (SMEs) |

| Large Enterprises | |

| By Industry Vertical | BFSI |

| Manufacturing | |

| Retail and E-commerce | |

| Healthcare and Life-Sciences | |

| Telecom and IT | |

| Government and Public Sector | |

| Transportation and Logistics | |

| Others | |

| By Workload | Core Compute and Storage |

| Analytics and Big-Data | |

| AI / ML and Gen-AI | |

| Business Applications (ERP/CRM/HR) | |

| Disaster Recovery and Backup | |

| Collaboration and Productivity |

Key Questions Answered in the Report

What is the current size of the India cloud computing market in 2026?

The India cloud computing market size is USD 26.43 billion in 2026.

How fast is the market expected to grow?

Market value is projected to reach USD 68.82 billion by 2031, reflecting a 21.10% CAGR during the forecast period (2026-2031).

Which deployment model is growing the fastest?

Hybrid cloud configurations are expanding at 27.20% CAGR as enterprises balance compliance and performance needs.

Which industry vertical is likely to see the highest growth?

Healthcare and Life Sciences lead with a projected 28.10% CAGR through 2031, driven by telemedicine and AI diagnostics.

What regions are attracting the most datacenter investments?

The Southern region, particularly Hyderabad and Chennai, is drawing significant hyperscale commitments and is forecast to grow at 24.10% CAGR.

How are sovereign cloud initiatives influencing adoption?

RBI-driven localization rules spur demand for domestic cloud regions that offer regulatory compliance alongside scalable services.

Page last updated on: