MRI Coils Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

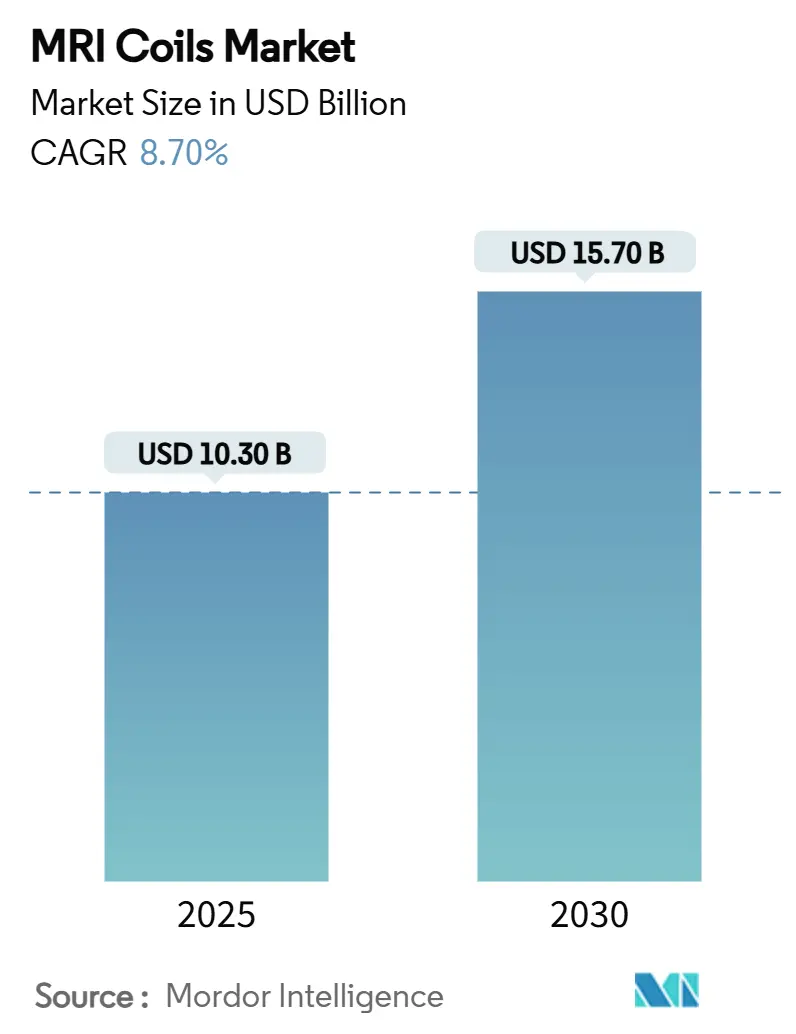

| Market Size (2025) | USD 10.30 Billion |

| Market Size (2030) | USD 15.70 Billion |

| Growth Rate (2025 - 2030) | 8.70% CAGR |

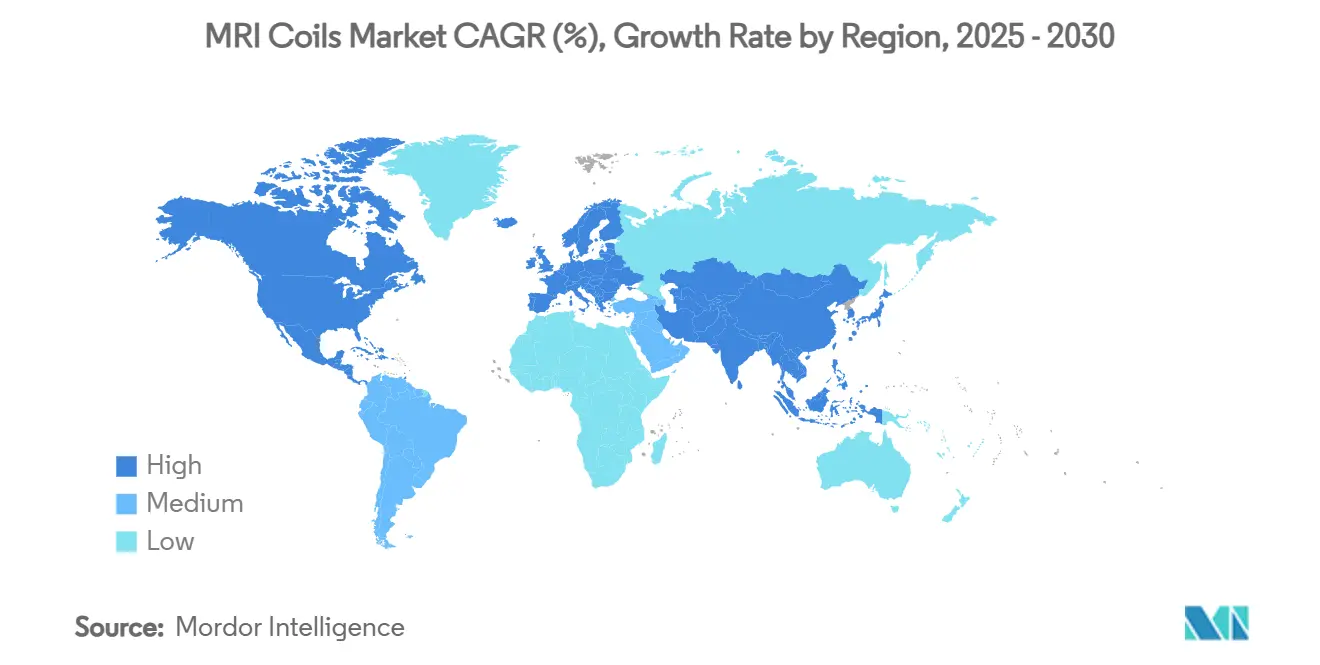

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

MRI Coils Market Analysis by Mordor Intelligence

The MRI coils market size stands at USD 10.3 billion in 2025 and is forecast to reach USD 15.7 billion by 2030, expanding at an 8.7% CAGR over the period. Continued modernization of diagnostic imaging suites, the shift toward helium-free magnets, and the rapid pairing of artificial-intelligence reconstruction tools sustain a healthy demand pipeline that is no longer purely volume driven. Providers now treat coils as productivity enablers that compress table times, elevate patient comfort, and unlock new reimbursement opportunities. At the same time, flexible engineering platforms shorten design-to-market cycles, helping vendors respond quickly to specialty use cases in neurology, orthopedics, and point-of-care settings. Capital-intensive health systems in North America and Western Europe choose premium phased-array products that preserve throughput, whereas emerging regions accelerate procurement of low-field portable scanners with ultralight coils that work in non-shielded rooms. Competitive intensity therefore pivots on how well manufacturers balance high-end performance with accessible price points.

Key Report Takeaways

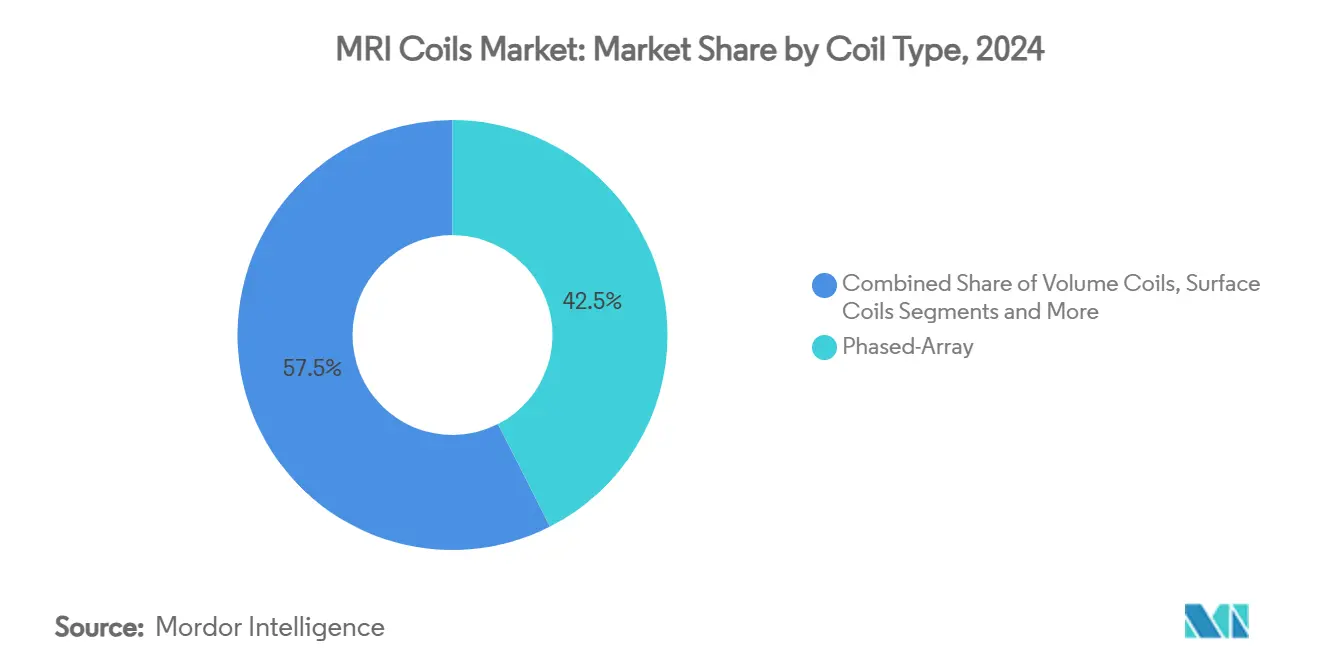

- By coil type, phased-array products commanded a 42.5% revenue share in 2024; flexible cable coils are projected to post an 11.2% CAGR through 2030.

- By field-strength compatibility, 3 T coils held 46.1% of the MRI coils market share in 2024, while low-field point-of-care coils are advancing at a 12.5% CAGR to 2030.

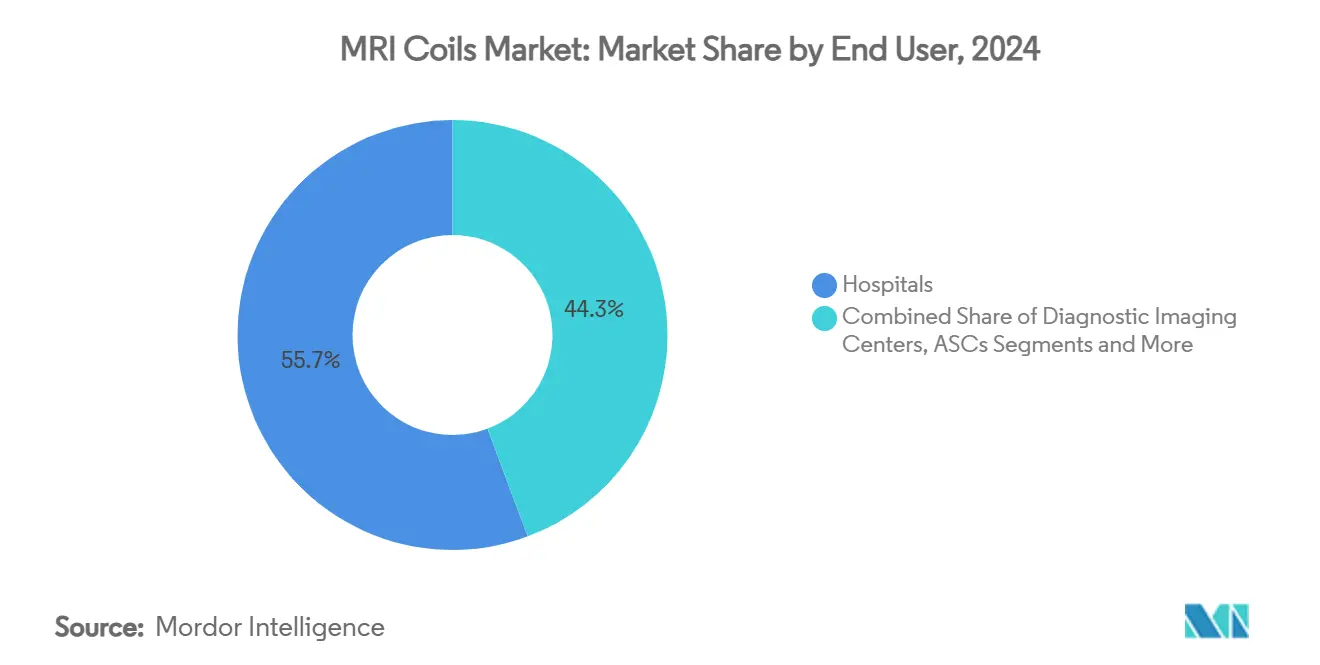

- By end user, hospitals accounted for 55.7% of the MRI coils market size in 2024, while ambulatory surgical centers are projected to grow at 7.4% CAGR through 2030.

- By geography, North America led with 32.8% revenue share in 2024; Asia-Pacific is set to expand at an 8.5% CAGR over the forecast horizon.

Global MRI Coils Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Adoption Of Multi-Channel Phased-Array Coils | +1.80% | Global, with early adoption in North America & EU | Medium term (2-4 years) |

| Growing Installed Base Of ≥3 T MRI Scanners | +2.10% | North America, Europe, APAC core markets | Long term (≥ 4 years) |

| Upgrade Cycle Driven By Helium-Free & Lightweight Coil Designs | +1.50% | Global, particularly regions with helium supply constraints | Medium term (2-4 years) |

| Reimbursement Tailwinds For High-Resolution Neuro & MSK Imaging | +1.20% | North America & EU, with spillover to developed APAC | Short term (≤ 2 years) |

| Expansion Of Low-Field POC MRI Requiring Novel Flexible Coils | +1.40% | APAC, MEA, with pilot programs in rural North America | Long term (≥ 4 years) |

| AI-Enhanced Coil Diagnostics Lowering Downtime Cost | +0.70% | Global, led by technology-advanced healthcare systems | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Adoption of Multi-Channel Phased-Array Coils

Parallel imaging has reached a tipping point as 64- and 128-channel phased-array coils consistently deliver two- to three-fold scan-time reductions without sacrificing spatial resolution.[1]Rapid Adoption of Multi-Channel Coils, “Self-Decoupled Radiofrequency Coils for MRI,” Nature Communications, nature.com Higher patient throughput converts into incremental revenue even in flat reimbursement environments, making coil upgrades financially attractive for private and public institutions alike. Workflow benefits compound when AI-based reconstruction engines further shorten time-to-diagnosis, a feature already standard on flagship systems in North America. Customer preference, therefore, skews toward modular phased-array platforms that can be tailored to neuro, cardiac, or body imaging without extensive hardware swaps.

Growing Installed Base of ≥3 T MRI Scanners

The prevalence of 3 T equipment now exceeds 45% of annual MRI installations, generating a direct pull-through effect for coils that tolerate higher RF power deposition and manage B1 inhomogeneity. Neuro-focused centers adopt asymmetrical gradient coils to exploit advanced diffusion techniques, while musculoskeletal practices value the finer depiction of cartilage enabled by 3 T phased arrays. Vendors that supply application-specific coils, such as head-only or extremity, secure premium pricing and long-term service contracts, reshaping the competitive map in favor of technically differentiated specialists.

Upgrade Cycle Driven by Helium-Free & Lightweight Coil Designs

Dry-cool technology requiring under 1 L of helium accelerates magnet replacement, but it also drives demand for coils optimized for altered magnetic and thermal profiles. In parallel, elastomer-based coils weigh up to 60% less than conventional copper coils and contour more comfortably to pediatric and bariatric patients.[2]Elastomer Coils, “Wearable MR Detection,” Magnetic Resonance in Medicine, onlinelibrary.wiley.com Hospitals engaged in sustainability pledges view lighter coils as a practical way to minimize energy use during transport and positioning. The combined sustainability-plus-usability rationale shortens the investment payback period, keeping the MRI coils market on a double-digit replacement rhythm.

Reimbursement Tailwinds for High-Resolution Neuro & MSK Imaging

New 2025 CPT codes reward detailed MR scans of patients with implants, expanding the billable volume for high-resolution protocols that rely on dedicated neuro and musculoskeletal coils.[3]American College of Radiology, “New MR Safety CPT Codes in 2025,” American College of Radiology, acr.orgAcademic centers estimate revenue lifts of 8–10% per scanner once the codes are fully adopted, offsetting inflationary cost pressures. The policy signal also nudges private insurers in Europe toward covering advanced neuroimaging, reinforcing a pan-Atlantic reimbursement alignment that stabilizes long-term coil demand.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply-Chain Bottlenecks In High-Purity Copper & Rare-Earth Capacitors | -1.30% | Global, with acute impact in APAC manufacturing hubs | Short term (≤ 2 years) |

| Capital-Expenditure Freeze Among Tier-2 Hospitals Post-COVID | -0.90% | North America & EU mid-tier facilities, emerging markets | Medium term (2-4 years) |

| RF-Induced Heating Concerns Limiting Coil Design Freedom | -0.80% | Global, particularly affecting high-field and ultra-high-field systems | Long term (≥ 4 years) |

| Stagnant Reimbursement For Abdominal MRI Scans | -0.60% | North America & EU, with spillover to developed APAC markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Supply-Chain Bottlenecks in High-Purity Copper & Rare-Earth Capacitors

Seventy-three percent of the world’s medical-grade copper now originates from three smelters clustered in East Asia, leaving coil assemblers vulnerable to single-point disruptions. Spot prices have risen 12% since 2024, eroding margins on entry-level products. Rare-earth capacitor shortages present an even tighter choke-point, forcing some vendors to redesign matching networks for surface coils. Short-run alternative sourcing, such as recycled niobium, buys time but escalates unit costs until new refining capacity comes online.

Capital-Expenditure Freeze Among Tier-2 Hospitals Post-COVID

Community hospitals still operate under cash-conservation mandates enacted after pandemic revenue shocks, delaying discretionary upgrades across imaging portfolios. While essential maintenance continues, administrators hesitate to allocate USD 350,000-plus for high-density arrays when legacy coils remain functional. This adoption lag widens the technology gap between academic hubs and regional providers, potentially diluting growth in the mid-tier customer segment of the MRI coils market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Coil Type: Phased-Array Leadership, Flexible Cable Momentum

Phased-array products held a 42.5% stake in the MRI coils market in 2024, mirroring their ability to shorten scan windows by up to 40% and thus maximize scanner utilization. Flexible cable coils are projected to climb at an 11.2% CAGR through 2030 as outpatient and emergency departments gravitate toward patient-adaptive designs that enhance comfort during trauma, neonatal, and bariatric exams. The phased-array segment benefits from innovations such as self-decoupled elements that drop pre-amp counts by 25%, lowering noise and power draw. Volume coils, while niche, retain demand from full-body oncology protocols, whereas birdcage architectures remain mainstream for head imaging. Wireless derivatives show promise: inductively coupled prototypes already achieve 86% of cabled signal-to-noise ratios, hinting at a cord-free future.

The MRI coils market size for flexible cable products is expected to reach USD 3.2 billion by 2030, accounting for nearly 20% of overall revenues. Hospitals assess return on investment against metrics such as reduced repositioning events and shorter technologist setup times, both of which translate into appreciable labor savings. Durable elastomer layers also extend lifespan in high-utilization environments, lessening the total cost of ownership and further reinforcing adoption.

By Field-Strength Compatibility: 3 T Dominance Amid Point-of-Care Upsurge

Coils rated for 3 T magnets controlled 46.1% of MRI coils market share in 2024, reflecting the modality’s indispensability in neuro-oncology, advanced cardiac and cartilage studies. The MRI coils market size for low-field point-of-care applications is forecast to expand 12.5% annually as rural clinics deploy portable 0.05–0.3 T scanners requiring lightweight, battery-efficient coils. Portable systems consume under 2 kW and eliminate cryogens, enabling imaging at disaster sites and sports events. Ultra-high-field 7 T coils, although representing under 2% of shipments, seed future design language with metamaterial-enhanced arrays that triple local signal-to-noise ratios.

Mid-field 1-1.5 T coils continue to serve cost-sensitive buyers, and open magnet coils secure a steady niche among claustrophobic or pediatric populations. The combined interplay of these segments underscores a bimodal configuration: premium centers gravitate upward in field strength while large swathes of the care continuum open new demand at the sub-1 T end.

By End User: Hospitals Retain Scale Advantage, ASCs Accelerate

Hospitals represented 55.7% of the MRI coils market in 2024 thanks to integrated service lines and capacity to absorb high-performance coils into enterprise imaging budgets. The MRI coils market size for ambulatory surgical centers is, however, poised to expand quickly as these facilities increasingly perform same-day orthopedic repairs that mandate on-site MRI clearance. ASCs value quick turnarounds, making flexible and wireless coils an attractive investment that eases room turnover.

Diagnostic imaging centers occupy a middle strata, offering advanced studies without surgical capability but competing largely on patient experience. Research institutes, meanwhile, purchase next-generation arrays—often ahead of commercial release—to explore ultra-high-field or animal studies that spin off clinical applications later. Veterinary clinics form a nascent but rising customer base as midsize practices adopt refurbished 1.5 T scanners.

Geography Analysis

North America captured 32.8% of revenue in 2024 and continues to set procurement benchmarks through early pilots of helium-light magnets and AI-native workflows. A seven-year strategic alliance between GE HealthCare and Sutter Health covering 300 facilities exemplifies the region’s scale-driven technology refresh cadence. Academic nodes add further momentum: The Ohio State University Wexner Medical Center initiated a USD 105 million imaging partnership focused on coil-intensive neuro applications. New MR safety codes effective in 2025 boost procedure volume for patients with implants, encouraging investment in high-density arrays that lower artifact risk.

Asia-Pacific is projected to log an 8.5% CAGR by 2030 as healthcare modernization programs expand scanner footprints across both metropolitan hospitals and rural community clinics. China’s domestic manufacturers focus on 0.3–1.5 T systems adapted for high-humidity environments, generating incremental coil demand across six coastal production hubs. India’s private sector adds momentum through energy-efficient 1.5 T launches that promise 20% lower power consumption. Japan and Australia remain premium 3 T coil markets, whereas Southeast Asia increasingly opts for low-field mobile units to bridge infrastructure deficits.

Europe ranks second by value, supported by a strong manufacturing ecosystem and cross-border research networks. Siemens Healthineers’ USD 314 million UK facility will assemble helium-free magnets and next-gen coils under carbon-neutral guidelines. Regulatory harmonization through IEC 60601-2-33:2022 eases the adoption of wireless coils by clarifying RF exposure thresholds. Central-Eastern Europe, with rising EU structural-fund allocations for diagnostic equipment, is expected to tilt toward mid-field systems, offering a stepping stone for coil vendors that bundle upgrade paths into procurement contracts.

Competitive Landscape

The MRI coils market shows a moderate concentration, with the top five vendors accounting for the majority of the market share. Siemens Healthineers, GE Healthcare, and Philips dominate integrated offerings, while Canon and United Imaging carve space through cost-competitive bundles. Siemens is doubling coil output by 2027 at its new British plant, coupling production efficiency with helium-free architecture. GE HealthCare bets on sealed Freelium magnets that cut helium use 99%, pairing them with 48-channel body arrays designed for quick-swap servicing.

Niche innovators target wireless, metamaterial-enhanced, and pediatric-specific coils. Start-ups working with metamaterials report three-fold SNR gains at 1.5 T, positioning them as acquisition targets for tier-one OEMs. Regulatory reforms under the FDA’s unified Quality System Regulation, effective in 2026, may lower compliance overhead, enabling mid-size manufacturers to accelerate U.S. launches.

Strategic partnerships remain pivotal. Canon Healthcare secured a downtown Cleveland facility to co-locate R&D teams with the Cleveland Clinic, reinforcing supply-chain proximity and clinician feedback loops. Meanwhile, Philips addressed a recall of SENSE XL torso coils linked to overheating, underscoring the reputational risks tied to RF safety.

MRI Coils Industry Leaders

Siemens Healthineers

GE Healthcare

Philips Healthcare

Canon Medical Systems

ScanMed

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: GE HealthCare opened an MRI R&D center at the University of Cincinnati to co-develop next-generation coils for pediatric and adult imaging.

- June 2025: The Weizmann Institute unveiled a nano-MRI platform that images individual molecules at 1 nm resolution.

- May 2025: GE HealthCare introduced SIGNA Sprint, an ultra-premium 1.5 T system featuring gradient coils designed for cardiac and oncology studies.

- November 2024: Siemens Healthineers expanded the Magnetom Flow platform with a 70 cm bore helium-free model.

Global MRI Coils Market Report Scope

| Volume Coils |

| Surface Coils |

| Phased-Array Coils |

| Birdcage Coils |

| Extremity Coils |

| Low-Field (<1 T) |

| Mid-Field (1-1.5 T) |

| High-Field (3 T) |

| Ultra-High-Field (7 T +) |

| Open MRI Systems |

| Hospitals |

| Diagnostic Imaging Centers |

| Ambulatory Surgical Centers |

| Research Institutes |

| Veterinary Clinics |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Coil Type | Volume Coils | |

| Surface Coils | ||

| Phased-Array Coils | ||

| Birdcage Coils | ||

| Extremity Coils | ||

| By Field-Strength Compatibility | Low-Field (<1 T) | |

| Mid-Field (1-1.5 T) | ||

| High-Field (3 T) | ||

| Ultra-High-Field (7 T +) | ||

| Open MRI Systems | ||

| By End User | Hospitals | |

| Diagnostic Imaging Centers | ||

| Ambulatory Surgical Centers | ||

| Research Institutes | ||

| Veterinary Clinics | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the MRI coils market and its expected growth rate?

The market is valued at USD 10.3 billion in 2025 and is projected to grow at an 8.7% CAGR to reach USD 15.7 billion by 2030.

Which coil type leads revenue contributions?

Phased-array coils led with 42.5% of global revenue in 2024, driven by their ability to shorten scan times and boost throughput.

Why are flexible cable coils gaining traction?

Flexible designs improve patient comfort and support point-of-care scanners, fueling an 11.2% CAGR forecast through 2030.

How does the growth outlook differ between 3 T and low-field coils?

3 T coils dominate today, but low-field point-of-care coils are the fastest climbers at a 12.5% CAGR as portable scanners proliferate.

Which region is expanding fastest in coil demand?

Asia-Pacific is expected to post an 8.5% CAGR through 2030, propelled by healthcare infrastructure upgrades and portable MRI adoption.

What impact will helium-free magnets have on coil upgrades?

Helium-free systems reshape magnetic and thermal profiles, prompting a broad replacement cycle for coils optimized for the new environment.

Page last updated on: