Radiofrequency Ablation Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

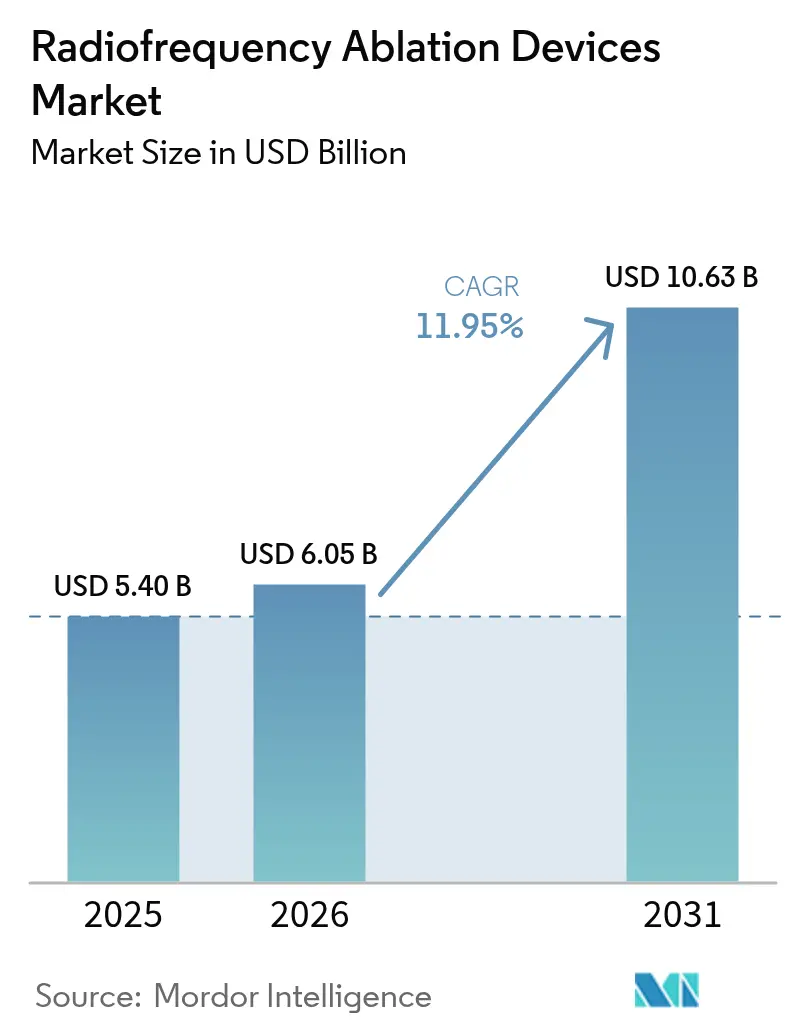

| Market Size (2026) | USD 6.05 Billion |

| Market Size (2031) | USD 10.63 Billion |

| Growth Rate (2026 - 2031) | 11.95% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Radiofrequency Ablation Devices Market Analysis by Mordor Intelligence

Radiofrequency ablation devices market size in 2026 is estimated at USD 6.05 billion, growing from 2025 value of USD 5.40 billion with 2031 projections showing USD 10.63 billion, growing at 11.95% CAGR over 2026-2031. Rising life expectancy is swelling the pool of patients with cardiac arrhythmias and solid tumors, updated clinical guidelines now endorse ablation as a first-line treatment in electrophysiology and oncology, and manufacturers are releasing next-generation systems that combine real-time imaging with AI-driven temperature control. In parallel, new CPT codes improve U.S. reimbursement, disposable catheters create predictable recurring revenue, and ambulatory surgical centers (ASCs) are absorbing cases that were previously inpatient, enhancing procedure accessibility. Competitive intensity is mounting as pulsed field ablation gains traction, yet conventional thermal systems still dominate installed bases, sustaining a sizable replacement market.

Key Report Takeaways

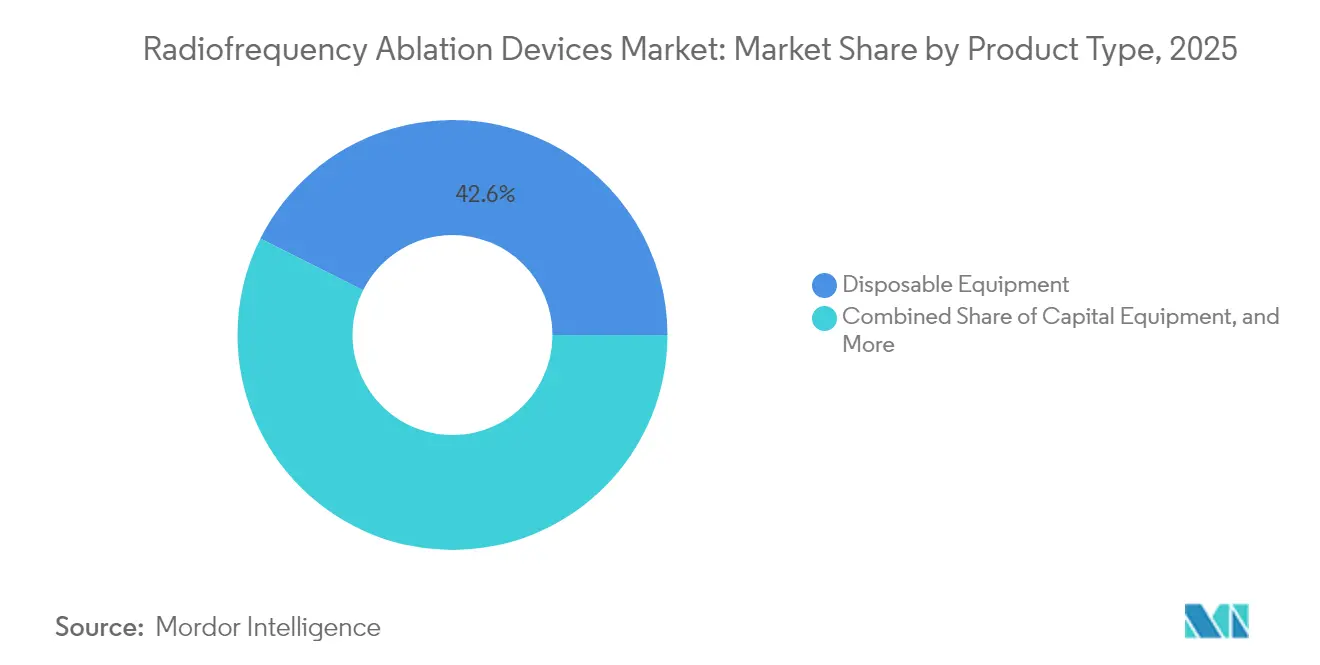

- By product type, disposable equipment held 42.60% of radiofrequency ablation devices market share in 2025, while capital-sparing outpatient centers are propelling disposable catheters at a 14.52% CAGR through 2031.

- By application, cardiology accounted for 37.60% revenue share in 2025; oncology is set to expand at a 13.95% CAGR, the fastest among all clinical areas.

- By end user, hospitals controlled 59.30% of the radiofrequency ablation devices market size in 2025, whereas ASCs are forecast to grow at a 12.88% CAGR as same-day discharge protocols mature.

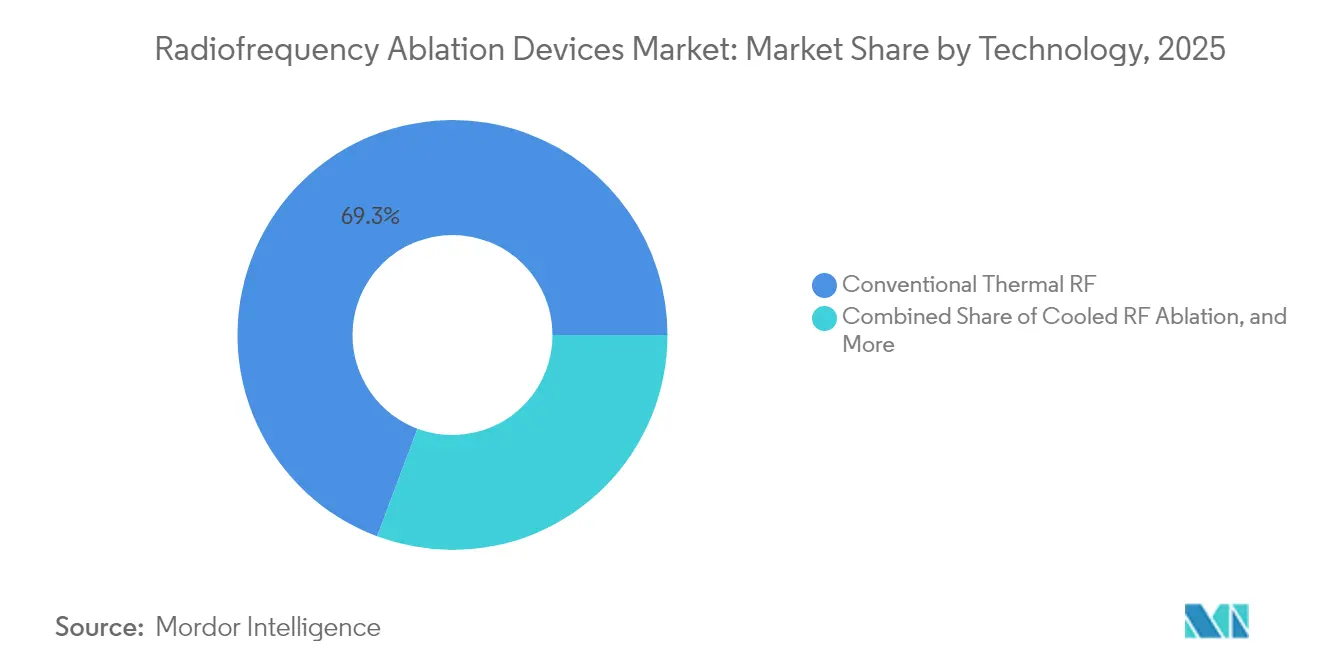

- By technology, conventional thermal platforms retained 69.30% share in 2025, but pulsed RF systems are projected to climb 15.05% annually through 2031.

- By approach, catheter-based procedures held 59.40% share of the radiofrequency ablation devices market in 2025, while percutaneous image-guided ablation is forecast to expand at a 13.55% CAGR through 2031.

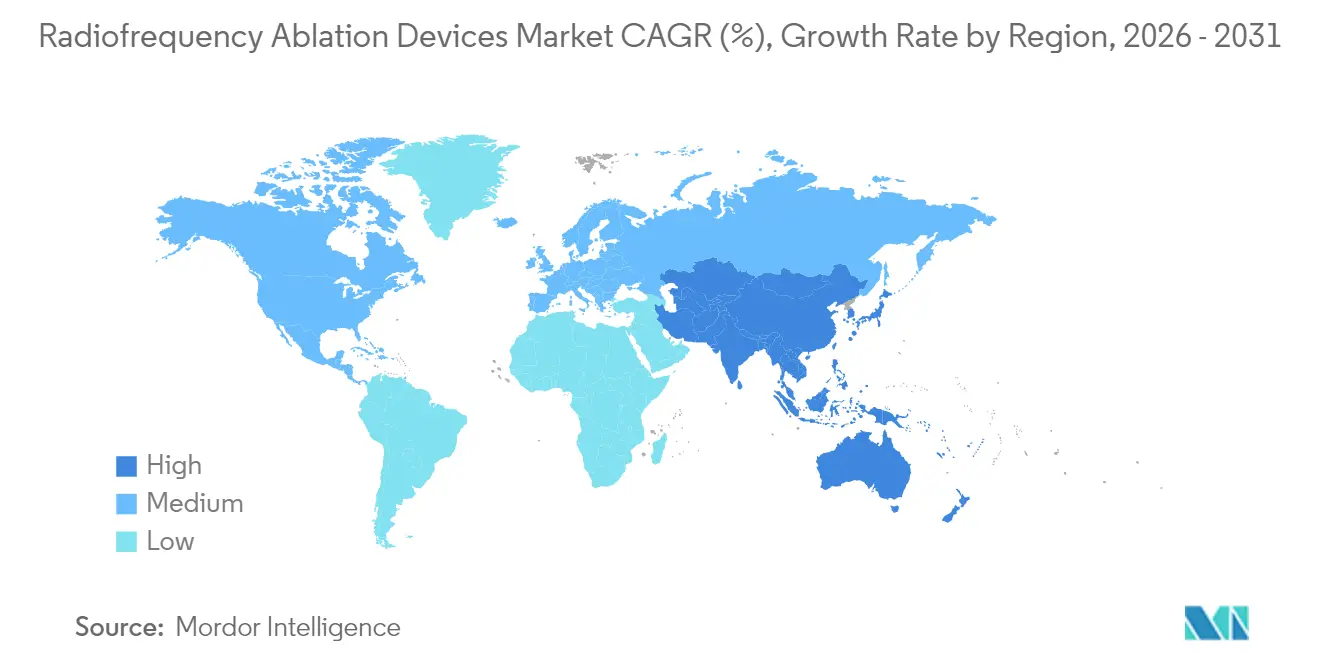

- By geography, North America led with 47.50% revenue share in 2025, while Asia-Pacific is poised for the quickest expansion at a 14.52% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Radiofrequency Ablation Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Global Burden of Cardiac Arrhythmias & Solid Tumors Fueling RF Ablation Utilization | +2.8% | Global, with highest impact in North America & Europe | Long term (≥ 4 years) |

| Upgraded Clinical Guidelines Positioning RF Ablation as Front-Line Treatment in EP & Oncology | +2.1% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Expansion of Ambulatory Surgical Centers Driving Shift to Outpatient Minimally-Invasive Procedures | +1.7% | North America core, spill-over to Europe | Medium term (2-4 years) |

| Broadened Reimbursement & Value-Based Care Models Improving Procedure Economics | +1.5% | North America & EU primarily | Medium term (2-4 years) |

| Integration of Real-Time Imaging & Navigation with RF Systems Boosting Success Rates | +1.3% | Global, led by developed markets | Short term (≤ 2 years) |

| Technology Advances (Contact-Force, Cooled RF, AI Temperature Control) Enhancing Safety & Precision | +1.9% | Global, led by developed markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Global Burden of Cardiac Arrhythmias & Solid Tumors

An aging population is lifting the prevalence of atrial fibrillation, which now affects more than 60 million individuals worldwide[1]American Heart Association, “2023 ACC/AHA Guideline for the Management of Atrial Fibrillation,” ahajournals.org. RF ablation is also firmly established for sub-3 cm hepatocellular carcinoma lesions, delivering survival outcomes comparable to surgery while sparing patients an open resection. Adoption is widening in emerging economies where diagnostic capabilities have improved and surgical capacity remains limited. Because the technique is minimally invasive, it suits elderly patients with multiple comorbidities. Clinical evidence supporting RF ablation for oligometastatic disease is enlarging its therapeutic window and fueling multi-specialty procedure growth.

Upgraded Clinical Guidelines Positioning RF Ablation as Front-Line Treatment

The 2023 ACC/AHA guideline elevated catheter ablation to first-line therapy for symptomatic paroxysmal atrial fibrillation, ending the long-standing “drug-first” paradigm. The 2024 ESC statement harmonized European practice, creating a trans-Atlantic consensus that accelerates adoption. In liver oncology, National Comprehensive Cancer Network recommendations endorse RF ablation for non-resectable candidates, expanding procedural eligibility. Earlier intervention widens the addressable population and increases repeat procedures, directly boosting the radiofrequency ablation devices market.

Expansion of Ambulatory Surgical Centers Driving Outpatient Shift

ASCs performed 26.7 million procedures in 2023, and industry associations identify RF ablation as a prime candidate for migration from hospitals to outpatient suites. The HRS/ACC scientific statement confirms low complication rates for same-day discharge after intracardiac ablation, supporting broader outpatient use. Medicare's removal of numerous codes from its inpatient-only list is paving the way for an 18% rise in outpatient surgical volumes by 2033, aligning incentives among payers, providers, and patients.

Broadened Reimbursement & Value-Based Care Models

New CPT codes 60660 and 60661 for percutaneous thyroid nodule ablation, effective January 2025, carry work RVUs of 5.75 and 4.25, respectively, reinforcing revenue visibility for providers. Several European payers now reimburse RF ablation under bundled DRG frameworks aimed at lowering total episode costs, while U.S. value-based arrangements reward avoidance of antiarrhythmic drug toxicity. Improved economics strengthen hospital purchase intent and foster ASC expansion.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competitive Cannibalization from Emerging Non-Thermal Modalities (Pulsed-Field, Cryo, Microwave) | -1.8% | Global, most pronounced in developed markets | Short term (≤ 2 years) |

| Stringent Regulatory Oversight & Thermal-Injury Related Recalls Extending Time-to-Market | -1.2% | North America & EU primarily | Medium term (2-4 years) |

| Limited Supply of Skilled EPs & Interventional Radiologists in Developing Regions | -0.9% | APAC, MEA, Latin America | Long term (≥ 4 years) |

| High Capital & Per-Procedure Costs Limiting Adoption in Cost-Sensitive Settings | -1.1% | Global, most impact in emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Competitive Cannibalization from Emerging Non-Thermal Modalities

Pulsed field ablation (PFA) has rapidly captured cardiac volumes because it selectively targets myocardial cells and minimizes oesophageal or phrenic nerve injury. Boston Scientific’s Farapulse system treated more than 125,000 patients within the first year of U.S. clearance, translating to triple-digit growth in its electrophysiology franchise. Cryo and microwave systems are also advancing, offering alternative energy profiles that challenge traditional RF leadership. As physicians gain confidence in non-thermal options, equipment budgets and capital allocations may shift away from conventional RF platforms.

Stringent Regulatory Oversight & Thermal-Injury-Related Recalls

Thermal injury concerns keep regulators vigilant. The FDA’s review of Medtronic’s Sphere-9 catheter required extensive heat-injury modeling and lesion durability data, elongating time-to-market[2]U.S. Food and Drug Administration, “Sphere-9 Catheter and Affera Ablation System,” fda.gov. Similar scrutiny in the EU lengthens Notified Body audits. Smaller firms often struggle to fund the pivotal trials demanded, which reduces pipeline diversity and can slow innovation cycles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Disposables Underpin Predictable Growth

Disposable probes and catheters commanded 42.60% of the radiofrequency ablation devices market in 2025, a lead reinforced by infection-control protocols that favor single-use devices. Manufacturers benefit from annuity-like revenue since each procedure requires new consumables. Hospitals simultaneously reduce sterilization overheads, and ASCs avoid capital expenditures associated with reprocessable inventory. Product development is concentrating on embedding sensors and micro-electronics directly into disposable tips, driving average selling prices upward. Capital consoles still represent strategic anchor points, but replacement cycles are lengthening as software upgrades extend system life. Merit Medical’s STAR platform illustrates how specialized disposables aimed at spinal metastases can capture premium margins.

Second-generation single-use catheters now offer contact-force feedback, rotational orientation markers, and integrated thermocouples, features that were once exclusive to reusable devices. The cumulative effect is a recurring consumables stream that shields suppliers from cyclical capital budgets. AngioDynamics’ 2024 decision to divest legacy RF lines and double-down on alternative energy systems shows how smaller firms are rationalizing portfolios amid competitive pressure. The capital equipment segment’s 14.52% forecast CAGR highlights its central role in sustaining the radiofrequency ablation devices market.

By Application: Cardiology Still Dominant as Oncology Accelerates

Cardiac rhythm management retained 37.60% revenue share in 2025 and remains foundational because guideline committees now position ablation earlier in the treatment pathway. Hospitals with established electrophysiology labs favor RF because staff are trained and capital infrastructure exists. Oncology, however, is the fastest climber, backed by data demonstrating curative outcomes for early-stage liver, kidney, and lung tumors. RF ablation for sub-3 cm hepatocellular lesions routinely achieves 5-year overall survival exceeding 70% in fit patients. National payers now reimburse RF for bone metastases-related pain, broadening use beyond cytoreduction into palliation.

Pain management volumes are also rising, fueled by an opioid-sparring imperative. Medicare allows four sessions per spinal region within a rolling 12-month window, underpinning procedural demand. Gynecology represents a high-growth niche as minimally invasive fibroid ablation systems gain traction following Hologic’s acquisition of Gynesonics. Collectively these dynamics underpin a diversified demand base that insulates the radiofrequency ablation devices market from volatility in any single clinical arena.

By End User: Hospitals Hold Volume, ASCs Capture Momentum

Hospitals performed 59.30% of global ablation cases in 2025, leveraging installed EP labs, anesthesia teams, and 24/7 critical-care coverage. Yet ASCs are forecast to post a 12.88% CAGR through 2031 as payers push procedures into lower-cost sites. Same-day discharge for intracardiac ablation has been validated in a multicenter JACC study, reporting 0.8% unplanned readmissions at 30 days. ASCs also appeal to physicians via ownership models that allow direct participation in facility revenue.

Specialty pain and electrophysiology clinics are proliferating in the United States’ Sun Belt states where Certificate of Need regulations are less restrictive. Academic centers continue to serve as early adopters for novel technologies, supplying critical evidence that accelerates diffusion into community practice. The interplay of these settings creates a balanced channel structure that stabilizes the radiofrequency ablation devices market size for hospitals at USD 3.20 billion in 2025 while enabling incremental growth in outpatient venues.

By Technology: Thermal Platforms Face Non-Thermal Disruption

Conventional thermal systems still represent 69.30% of installed base owing to decades of physician familiarity and large bodies of outcome data. Cooled RF platforms improve lesion size predictability by circulating saline through the probe, thereby mitigating charring and impedance rise. Bipolar configurations offer tighter energy confinement in anatomically delicate zones such as the spinal canal. Nevertheless, pulsed RF is growing at 15.05% annually and already represents a USD 1.01 billion slice of radiofrequency ablation devices market size in 2025. Medtronic’s Affera platform integrates pulsed field and RF modes, giving operators flexibility to tailor energy delivery.

Artificial-intelligence-enabled temperature control algorithms, such as Volta Medical’s VX1 software, shorten learning curves and may reduce repeat ablations by identifying latent conduction gaps in real time. The convergence of hybrid energy platforms with AI guidance suggests that modality boundaries will blur, forcing vendors to offer multi-energy consoles to safeguard share.

By Approach: Catheter-Based Dominance With Image-Guided Percutaneous Surge

Catheter-based procedures accounted for 59.40% of 2025 volumes, reflecting entrenched workflows in arrhythmia and pain therapy. Percutaneous image-guided ablation is, however, forecast to grow 13.55% annually, powered by advanced navigation such as Philips’ LumiGuide, which cuts fluoroscopy time by 56% and eliminates ionizing radiation exposure. Endoscopic and laparoscopic routes remain niche but vital for tumors adjacent to sensitive structures, enabling direct visualization.

ASC operators favor percutaneous approaches because they speed turnover and require lighter anesthesia. The approach mix is therefore tilting toward image-guided percutaneous systems, further invigorating the radiofrequency ablation devices market. Olympus’ acquisition of Taewoong Medical augments its endoscopic soft-tissue ablation portfolio, signaling rising interest in hybrid optical-RF platforms.

Geography Analysis

North America generated 47.50% of 2025 revenue as widespread insurance coverage, extensive EP lab capacity, and early adoption of pulsed field technology aligned to maintain leadership. New thyroid CPT codes with favorable RVUs extend reimbursement into endocrine surgery, suggesting upside for outpatient ENT providers. Boston Scientific recorded 177% year-over-year electrophysiology growth after Farapulse approval, illustrating the region’s appetite for innovation.

Europe follows with a science-driven ecosystem underpinned by academic collaboration. Germany’s prolific publication output and its cluster of high-volume university hospitals feed evidence-based guideline updates. ESC 2024 recommendations synchronize with U.S. standards, ensuring procedural uniformity across the Atlantic. Funding mechanisms differ, statutory health insurers in Germany pay under DRGs whereas the U.K. leans on NHS tariff bundles, but both encourage day-case delivery, supporting RF uptake. AI-powered mapping tools pioneered by French firm Volta Medical have found early adopters in Belgium and Italy, reinforcing Europe’s reputation for digital innovation.

Asia-Pacific is the fastest-growing geography with a projected 14.52% CAGR to 2031, underpinned by aging demographics and accelerating device approvals. China now matches the United States in annual scholarly output on RF ablation. Mindray’s acquisition of APT Medical furnishes a domestic alternative to imported catheters and consoles, strengthening local supply chains. Japan’s PMDA imposes stringent dossier requirements, yet once an approval is secured, reimbursement tends to be swift, supporting predictable adoption trajectories. India’s private hospital networks are piloting RF ablation for liver metastases; however, self-pay dynamics can limit volume outside metropolitan centers.

Competitive Landscape

The radiofrequency ablation industry exhibits moderate concentration anchored by Boston Scientific, Medtronic, and Abbott, each offering broad portfolios that span energy modalities. Boston Scientific’s USD 850 million Relievant acquisition secures a foothold in basivertebral nerve ablation and complements its Farapulse platform. Medtronic’s dual-energy Affera console gives physicians a single workstation that toggles between pulsed field and thermal RF, creating switching costs for competitors. Abbott leverages its EnSite X mapping system to pair with its TactiFlex contact-force catheter, banking on procedural efficiency to safeguard share.

Second-tier players concentrate on niche indications. Stryker’s OptaBlate system addresses vertebrogenic pain, while Olympus focuses on endoscopic soft-tissue applications. Autonomix is developing transvascular ablation for pancreatic cancer pain, an area where thermal injury avoidance is paramount. These specialized plays differentiate through targeted clinical data rather than scale.

Competitive behavior increasingly revolves around ecosystem control. Vendors integrate mapping, navigation, generator, and AI decision-support into unified suites that lock in consumables. Pricing pressure is intensifying as PFA entrants undercut legacy RF disposables. Nevertheless, high switching costs, physician familiarity, and extensive service networks insulate incumbents, sustaining medium concentration in the radiofrequency ablation devices market.

Radiofrequency Ablation Devices Industry Leaders

Avanos Medical, Inc.

Medtronic

Boston Scientific Corporation

Stryker Corporation

Abbott Laboratories

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: NeuroOne Medical Technologies accelerated its 510(k) submission timeline to the FDA for the OneRF Trigeminal Nerve Ablation System, aiming to treat severe facial pain in a market expected to exceed USD 416 million by 2030

- October 2024: Medtronic received FDA approval for the Affera Mapping and Ablation System with Sphere-9 catheter, enabling operators to switch between pulsed field and radiofrequency energy in a single procedure.

- February 2024: Medtronic obtained clearance for the OsteoCool 2.0 RF Ablation System for palliative treatment of spinal metastases and osteoid osteoma.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the radiofrequency ablation (RFA) devices market as every capital generator, catheter, probe, electrode, cable, and single-use accessory that delivers 200-750 kHz thermal current to ablate soft tissue during catheter-guided, percutaneous, laparoscopic, or open procedures in hospital and ambulatory settings.

Scope Exclusions: Non-thermal modalities such as pulsed-field, microwave, cryogenic, laser, and ultrasound ablation devices are excluded.

Segmentation Overview

- By Product Type

- Capital Equipment

- Disposable Equipment

- Reusable Accessories

- By Application

- Cardiology & Cardiac Rhythm Management

- Oncology

- Pain Management

- Gynecology

- Other Applications (Dermatology, ENT, etc.)

- By End User

- Hospitals

- Ambulatory Surgical Centers

- Specialty Pain & EP Clinics

- Academic & Research Institutes

- By Technology

- Conventional Thermal RF Ablation

- Cooled RF Ablation

- Pulsed RF Ablation

- Bipolar vs Monopolar RF Systems

- By Approach

- Catheter-Based Ablation

- Percutaneous Image-Guided Ablation

- Endoscopic / Laparoscopic RF Ablation

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Interviews with electrophysiologists, interventional oncologists, device engineers, and purchasing managers across North America, Europe, and Asia provided live insight on catheter pull-through rates, generator replacement cycles, and upcoming reimbursement moves.

Follow-up surveys with ASC supply heads allowed Mordor Intelligence to fine-tune ASP decay curves and verify the rising share of single-use probes.

Desk Research

The team first mapped import-export codes for RFA generators and catheters in UN Comtrade, then matched them with FDA 510(k), CE, and NMPA approvals to confirm active product counts.

We reviewed guideline updates from the American College of Cardiology, ESMO, and WHO-GHE that signal future procedure growth, while hospital charge masters, CMS outpatient files, and peer-reviewed meta-analyses supplied baseline volumes and device usage per case.

Company 10-K disclosures plus investor decks helped cross-check distributor mark-ups and regional ASP drift.

The desk sources listed are illustrative only, and many other public as well as paid datasets, including D&B Hoovers and Factiva, informed data collection and validation.

Market-Sizing & Forecasting

Our top-down model rebuilds demand from annual ablation procedures reported by national registries and extrapolated to 32 countries through prevalence-to-treatment ratios, which are then multiplied by verified device-usage coefficients.

Results are pressure-tested against sampled supplier revenue splits to catch any over-shoot.

Key drivers include atrial-fibrillation prevalence, solid-tumor incidence, outpatient surgery penetration, disposable-to-capital mix shift, and tender-led ASP erosion.

Five-year forecasts draw on multivariate regression tied to demographic aging, elective-surgery backlog clearance, and innovation adoption flags.

Regional tender logs and customs receipts bridge remaining gaps before final triangulation.

Data Validation & Update Cycle

Outputs pass analyst peer review, senior domain lead approval, and a variance dashboard that flags deviations greater than five percent from historical trends.

Reports refresh annually, and mid-cycle updates are triggered when material events such as major recalls, guideline changes, or blockbuster approvals shift the baseline, so clients always receive the latest vetted view.

Why Mordor's Radiofrequency Ablation Devices Baseline Commands Confidence

Published estimates often differ because firms apply distinct device mixes, geographic reach, and procedure multipliers.

We align scope with thermal RF technology only and refresh inputs every year, which limits drift.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 5.40 B (2025) | Mordor Intelligence | - |

| USD 4.63 B (2024) | Regional Consultancy A | Combines RF with cryo and microwave devices, uses static 2019 ASPs |

| USD 4.72 B (2024) | Global Consultancy A | Revenue declarations only, no procedure alignment |

| USD 4.80 B (2023) | Industry Journal B | Excludes reusable accessories and Latin America demand |

The comparison shows that Mordor's disciplined scope, multi-source variable set, and annual refresh cycle provide a transparent, repeatable baseline that decision-makers can rely upon.

Key Questions Answered in the Report

What is the current size of the radiofrequency ablation devices market and how fast is it growing?

The market stands at USD 6.05 billion in 2026 and is projected to reach USD 10.63 billion by 2031, reflecting a 11.95% CAGR.

Which product segment generates the largest revenue?

Disposable equipment leads with 42.60% of 2025 revenue, supported by infection-control protocols and recurring per-procedure demand.

Which region is expected to post the fastest growth through 2031?

Asia-Pacific is forecast to expand at a 14.52% CAGR thanks to aging populations, rising procedure volumes and improving device approvals.

How quickly is the oncology application expanding within the market?

Oncology represents the fastest-growing clinical use, advancing at a 13.95% CAGR through 2031 as indications broaden for solid tumors.

What proportion of procedures are catheter-based, and which approach is accelerating most?

Catheter-based ablations account for 59.40% of 2025 procedures, while percutaneous image-guided ablation is growing at a 13.55% CAGR.

How does pulsed radiofrequency technology compare with conventional thermal systems in growth terms?

Conventional thermal platforms still hold 69.30% market share, but pulsed RF systems are gaining momentum with a 15.05% projected CAGR.

Page last updated on: