Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

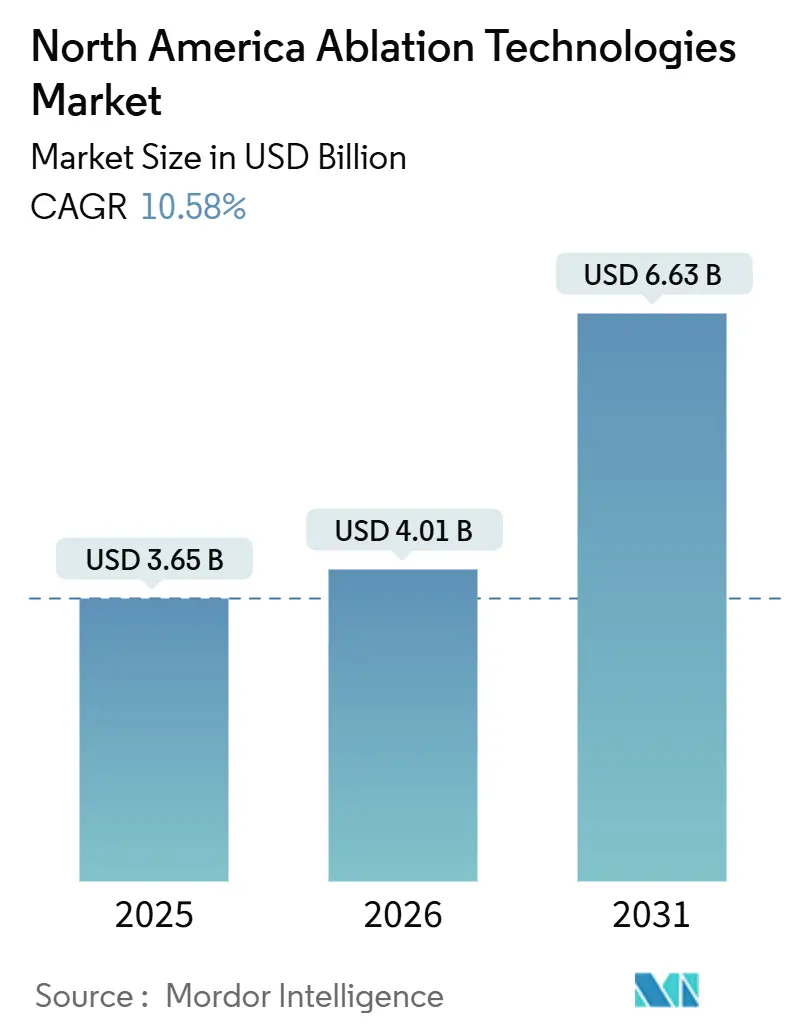

| Base Year Market Size (2025) | USD 3.65 Billion |

| Market Size (2026) | USD 4.01 Billion |

| Market Size (2031) | USD 6.63 Billion |

| Growth Rate (2026 - 2031) | 10.58% CAGR |

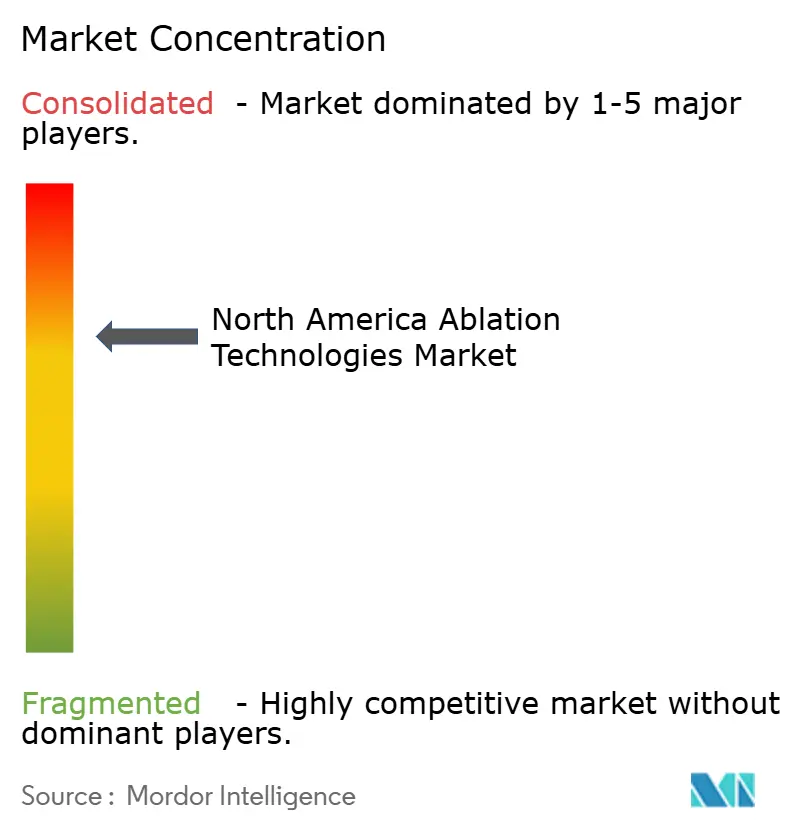

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Ablation Technologies Market Analysis by Mordor Intelligence

The North America Ablation Technologies Market size is expected to increase from USD 3.65 billion in 2025 to USD 4.01 billion in 2026 and reach USD 6.63 billion by 2031, growing at a CAGR of 10.58% over 2026-2031.

Expansion is fueled by the rapid commercialization of pulsed field ablation (PFA), rising prevalence of cancer and atrial fibrillation, and the creation of a Medicare Severity Diagnosis-Related Group for dual left-atrial appendage closure and ablation, which pays hospitals USD 44,026 per case. Hospitals are refreshing electrophysiology capital stock faster than in prior technology cycles because PFA eliminates thermal injury to the esophagus, a complication that occurred in 1.9% of radiofrequency cases but 0% of PFA cases in pivotal trials. High-intensity focused ultrasound (HIFU) and histotripsy are likewise accelerating market opportunities in oncology and gynecology, while specialty clinics and ambulatory surgery centers (ASCs) are growing procedure volume in pain and women’s health. Collectively, these factors are propelling the North America ablation technologies market toward double-digit growth despite workforce shortages that lengthen wait times in rural counties.

Key Report Takeaways

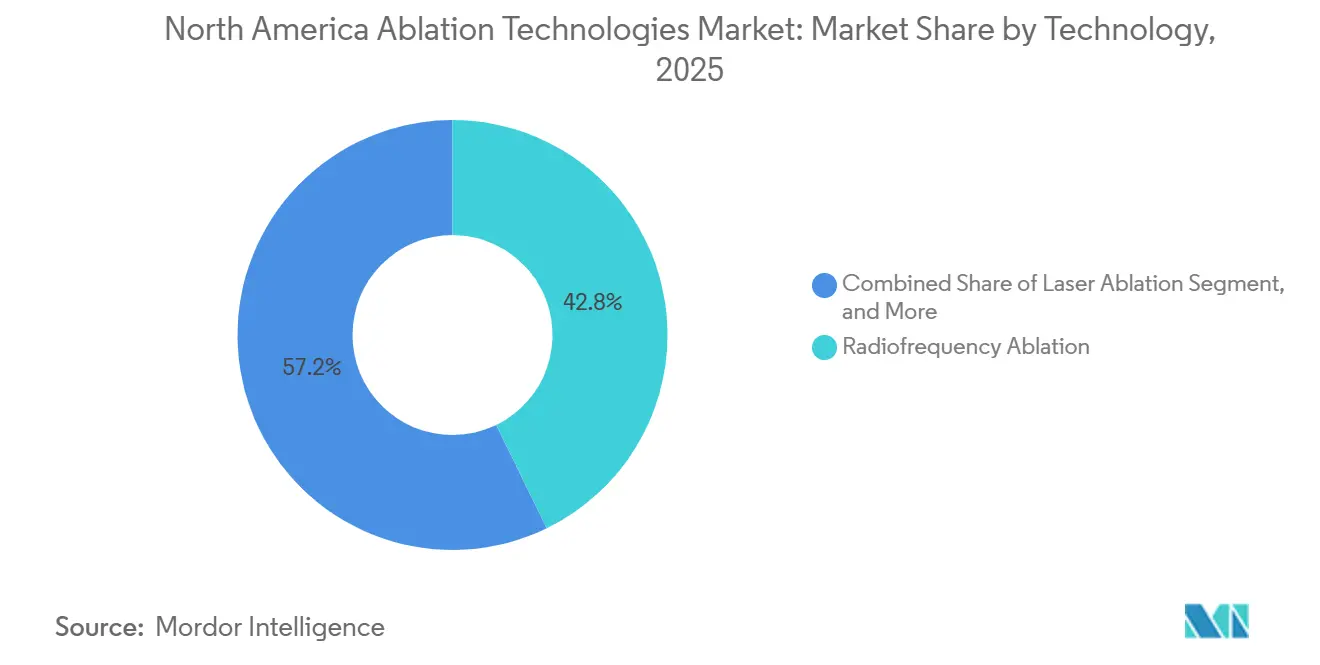

- By technology, radiofrequency ablation led with 42.78% of North America ablation technologies market share in 2025, whereas HIFU and histotripsy are projected to expand at a 14.06% CAGR through 2031.

- By application, oncology accounted for 48.24% of the North America ablation technologies market size in 2025, and gynecology is advancing at a 12.63% CAGR through 2031.

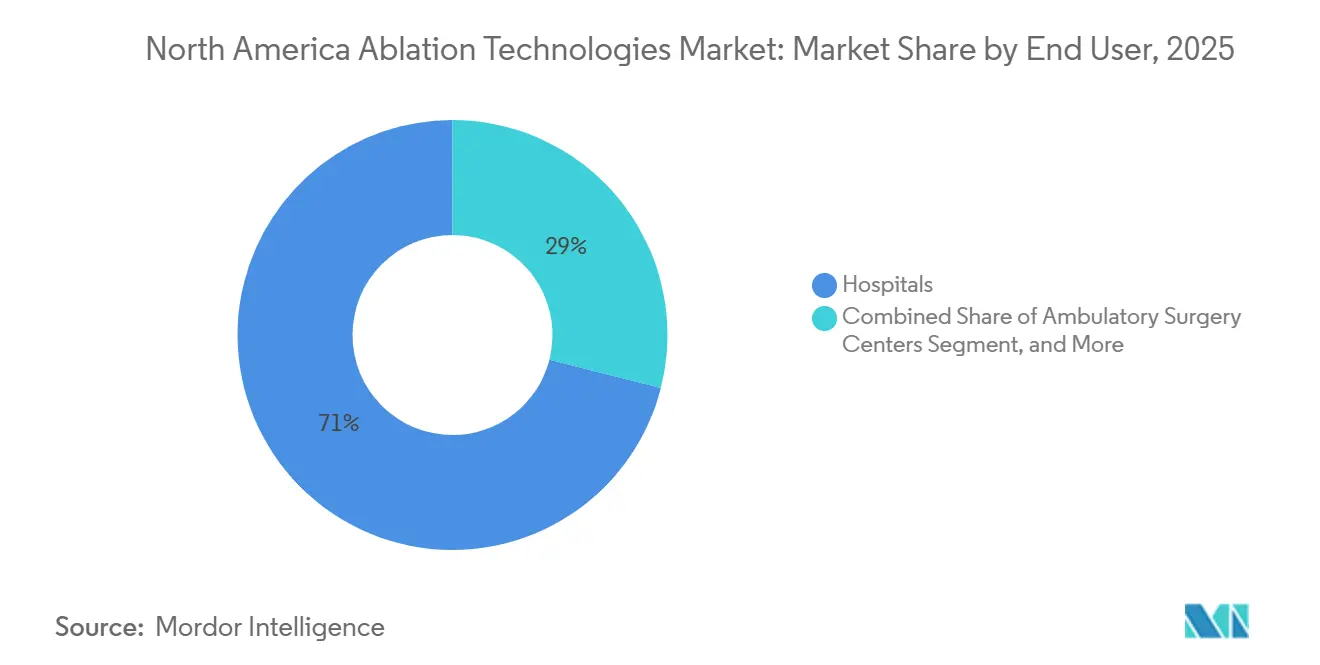

- By end user, hospitals accounted for 71.03% of revenue in 2025; specialty clinics are projected to have the highest growth rate at 11.18% CAGR through 2031.

- By geography, the United States captured 83.81% of regional sales in 2025, while Mexico is forecast to grow at a 13.27% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Ablation Technologies Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Cancer & Cardiac Disease Prevalence | +2.8% | United States, Canada | Long term (≥ 4 years) |

| Growing Demand for Minimally-Invasive Care | +2.3% | Urban United States & Canada, Mexico City | Medium term (2-4 years) |

| Advances in Image-Guided & Robotic Systems | +1.9% | U.S. tertiary centers, select Canadian provinces | Medium term (2-4 years) |

| Favorable U.S. CMS Reimbursement Policies | +1.7% | United States | Short term (≤ 2 years) |

| Geriatric Demographic Expansion | +1.4% | United States & Canada | Long term (≥ 4 years) |

| ASC-Led Microwave System Adoption | +0.9% | United States | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Cancer & Cardiac Disease Prevalence

Cancer incidence and atrial fibrillation prevalence are climbing together, generating parallel demand for ablative therapies. The American Cancer Society projects 2 million new U.S. cancer diagnoses in 2026, while atrial fibrillation affects 6.7 million adults, up 33% from 2019.[1]American Cancer Society, “Cancer Facts & Figures 2026,” cancer.org Five-year overall survival after microwave liver-tumor ablation reached 75.3% for hepatocellular carcinoma <3 cm, proving ablation’s curative potential in non-surgical candidates. Because 18% of people aged ≥ 75 carry both oncologic and cardiac diagnoses, low-morbidity ablation is becoming the treatment of choice in frail patients.

Growing Demand for Minimally-Invasive Care

Patients favor same-day discharge and quick recovery. PFA shortens procedure time by 30%, allowing five cases per lab per day and adding roughly USD 220,000 incremental yearly revenue for hospitals.[2]Heart Rhythm Journal, “ADVENT Trial Results,” heartrhythmjournal.com After percutaneous microwave lung ablation, seniors resume normal activity within 3 days, compared with 21 days after surgical wedge resection. These efficiency and quality-of-life gains are key demand accelerants for the North America ablation technologies market.

Advances in Image-Guided & Robotic Systems

Robotics and real-time imaging reduce operator variability. XACT Robotics’ platform delivers sub-millimeter needle placement accuracy, trimming CT-guided liver-ablation time by 22%. Quantum Surgical’s Epione fuses MRI and ultrasound to cut positive margins from 12% to 4%. Medtronic’s Affera system integrates mapping with dual-energy ablation, lowering fluoroscopy by 35%. These innovations broaden provider access, sustaining momentum in the North America ablation technologies market.

Favorable U.S. CMS Reimbursement Policies

Targeted payments speed adoption. The New Technology Add-on Payment grants up to USD 6,337.50 per PFA case, almost covering PFA catheter costs. CMS also boosted outpatient cardiac-ablation rates 8.3% for 2025, enhancing hospital margins, while MS-DRG 317 pays USD 44,026 for combined appendage closure and ablation, incentivizing dual procedures.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital & Disposable Costs | –1.6% | U.S. community hospitals, rural Canada, Mexico public sector | Medium term (2-4 years) |

| Stringent FDA Regulatory Pathway | –1.2% | United States | Long term (≥ 4 years) |

| Shortage of Electrophysiologists & IRs | –1.4% | Rural U.S. & Canadian provinces | Long term (≥ 4 years) |

| Reimbursement Uncertainty for Histotripsy | –0.8% | United States academic centers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capital & Disposable Costs

Generators cost USD 30,000-3 million; single-use catheters run USD 3,000-8,000. A 200-bed hospital performing 150 cardiac ablations accrues up to USD 1.2 million in annual disposables, requiring 180+ cases to break even. Rural Canadian facilities and Mexican public hospitals face even tougher budget ceilings, stalling equipment purchases.

Stringent FDA Regulatory Pathway

PMA trials enroll 200-500 patients, cost USD 15-30 million, and stretch development by 3-5 years. HistoSonics’ Edison histotripsy system endured a 24-month pivotal trial before October 2023 approval, allowing thermal incumbents to entrench.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Pulsed Field Ablation Disrupts Thermal Dominance

Radiofrequency ablation retained 42.78% of 2025 revenue, but PFA is siphoning cardiac volume, and HIFU plus histotripsy are set to post 14.06% CAGR through 2031. PFA eliminates esophageal damage, enabling same-day discharge and lowering monitoring costs. Microwave ablation outperforms radiofrequency for tumors >3 cm by shortening procedure time by 30% and expanding ablation zones, while cryoablation achieves 97.1% local control in small renal masses.

Across community hospitals, legacy radiofrequency consoles are being replaced, and 40% of U.S. electrophysiology labs plan to convert to PFA by 2027. Johnson & Johnson’s VARIPULSE adds closed-loop integration with the CARTO mapping system, cementing customer stickiness. PFA catheter ASPs average USD 7,000, 60% above thermal tools, but NTAP subsidies shrink payback periods, underpinning technology migration in the North America ablation technologies market.

By Application: Oncology Dominance Masks Gynecology Acceleration

Oncology captured 48.24% of 2025 revenue. Liver metastasis ablation delivers 51.5% five-year survival in colorectal cancer, broadening candidacy for non-surgical patients. Pairing ablation with checkpoint inhibitors produced 68% objective responses, far above ablation alone, hinting at combination-therapy upside.

Gynecology’s 12.63% CAGR is propelled by uterine-sparing fibroid management. HIFU reduces symptom severity 70-80% without a six-week hysterectomy recovery. Endometrial ablation achieves 90-95% satisfaction and averts hysterectomy in 85% of cases, thereby improving outpatient procedure flow. Pain-management ablation in ASCs benefits from tighter opioid regulations. Radiofrequency denervation ensures 50-80% pain relief for six-12 months, supporting recurring volume in the North America ablation technologies market.

By End User: Specialty Clinics Capture Outpatient Migration

Hospitals accounted for 71.03% of 2025 spend, reflecting ICU backup needs for complex cardiac and oncology care. Specialty clinics are growing at a 11.18% CAGR, building co-located outpatient departments that trim ablation wait times to 2 weeks and allow physicians to collect both professional and facility fees. Ambulatory surgery centers handle 15-18% of revenue, mostly in pain and gynecology, because CMS removed cardiac ablation from the ASC list in 2025, stripping USD 2 billion in potential volume.

Private cardiology and interventional oncology centers are capitalizing on value-based care. Their integration of scheduling, imaging, and procedure suites accelerates diagnosis-to-treatment cycles, boosting patient satisfaction by 22%. Microwave ablation equipment reaches breakeven inside one year under commercial insurance, fueling adoption across urban specialty groups.

Geography Analysis

The United States dominates the North American ablation technologies market, accounting for 83.81% of 2025 revenue. Federal reimbursement levers such as MS-DRG 317 and NTAP underpin technology uptake, yet 62% of rural counties lack an electrophysiologist, causing 10-12-week delays and raising stroke risk 8-12%. Academic centers adopt PFA and histotripsy rapidly, widening outcome gaps versus community sites.

Canada’s single-payer model slows capital spending; Alberta budgeted CAD 180 million (USD 133 million) for devices across 108 hospitals in 2025, confining new ablation consoles to Calgary and Edmonton. Wait times stretch to 18-24 months in the Atlantic provinces, while Health Canada approvals lag the FDA by up to a year, delaying market entry.

Mexico offers the fastest growth at a 13.27% CAGR, catalyzed by MXN 150 billion (USD 8.8 billion) in 2024-2030 hospital modernization funds. Private chains in Mexico City and Monterrey import radiofrequency and microwave systems to serve an expanding 55 million privately insured population, but INSABI-funded public hospitals purchase only 15-20 consoles per year due to budget constraints, reinforcing urban-rural disparities.

Competitive Landscape

The top 5 suppliers, Medtronic, Boston Scientific, Johnson & Johnson, Abbott, and AtriCure, controlled a significant portion of the 2025 revenue. Boston Scientific installed FARAPULSE in 400-plus hospitals within 9 months of the January 2024 launch, growing electrophysiology sales by 27% year over year. Medtronic’s PulseSelect gained NTAP support but entered two months later, conceding early-mover advantage. Biosense Webster’s VARIPULSE leverages its 1,200-site CARTO base to defend its share.

White-space entrants include HistoSonics in histotripsy and XACT Robotics in needle-based automation. Patent filings cluster around PFA waveforms; Medtronic lodged 18 applications in 2024-2025, Boston Scientific 12, raising entry hurdles for low-cost Asian competitors.

North America Ablation Technologies Industry Leaders

Abbott Laboratories

Boston Scientific Corporation

Johnson and Johnson (Biosense Webster, Inc)

Medtronic

AngioDynamics Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Pulse Biosciences released new clinical data showing durable treatment outcomes from its Vybrance Percutaneous Electrode System using nanosecond Pulsed Field Ablation (nsPFA). Durability is a critical milestone because benign thyroid nodules often recur after thermal ablation; demonstrating sustained efficacy strengthens nsPFA’s clinical value proposition.

- February 2026: Medtronic reported Q3 revenue growth of 80% worldwide and 137% in the U.S. for its Cardiac Ablation Solutions, driven by strong adoption of pulsed-field ablation (PFA) technologies for atrial fibrillation. This highlights rapid U.S. uptake of Medtronic’s PFA platform.

- February 2026: Baird Medical announced clinical progress in the U.S. with its Microwave Ablation (MWA) technology, reinforcing its strategy to expand patient access to minimally invasive therapies and accelerate global growth.

- December 2025: Abbott secured FDA approval for its Volt PFA System for the treatment of atrial fibrillation. Abbott is preparing for U.S. commercialization and expanding European adoption following CE Mark approval earlier in 2025.

North America Ablation Technologies Market Report Scope

As per the scope of the report, ablation generally refers to the surgical removal of a part of biological tissue. Ablation devices offer a minimally invasive alternative to traditional surgical treatment of liver, prostate, kidney, and lung cancers.

The North America Ablation Technologies Market Report is Segmented by Technology (Radiofrequency Ablation, Microwave Ablation, Cryoablation, Laser Ablation, HIFU & Histotripsy), Application (Oncology, Cardiology, Pain Management, Gynecology, Other Applications), End User (Hospitals, Ambulatory Surgery Centers, Specialty Clinics), and Geography (United States, Canada, Mexico). The Market Forecasts are Provided in Terms of Value (USD).

By Technology

| Radiofrequency Ablation |

| Microwave Ablation |

| Cryoablation |

| Laser Ablation |

| HIFU & Histotripsy |

By Application

| Oncology |

| Cardiology |

| Pain Management |

| Gynecology |

| Other Applications |

By End User

| Hospitals |

| Ambulatory Surgery Centers |

| Specialty Clinics |

By Country

| United States |

| Canada |

| Mexico |

| By Technology | Radiofrequency Ablation |

| Microwave Ablation | |

| Cryoablation | |

| Laser Ablation | |

| HIFU & Histotripsy | |

| By Application | Oncology |

| Cardiology | |

| Pain Management | |

| Gynecology | |

| Other Applications | |

| By End User | Hospitals |

| Ambulatory Surgery Centers | |

| Specialty Clinics | |

| By Country | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

What is the projected value of the North America ablation technologies market by 2031?

The market is forecast to reach USD 6.63 billion by 2031.

How fast is pulsed field ablation expected to grow compared with thermal modalities?

HIFU and histotripsy, including PFA systems, are projected to grow at a 14.06% CAGR, the quickest among technology segments.

Which application area generates the largest revenue today?

Oncology held 48.24% of 2025 revenue thanks to broad use across liver, lung, and kidney tumors.

Why are specialty clinics gaining share against hospitals?

Co-located outpatient departments let physicians capture facility fees and reduce wait times, supporting an 11.18% CAGR through 2031.

What policy change most benefits combined cardiac procedures?

CMS introduced MS-DRG 317 at USD 44,026 per case, making same-session appendage closure plus ablation financially attractive.

Page last updated on: