Tumor Ablation Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

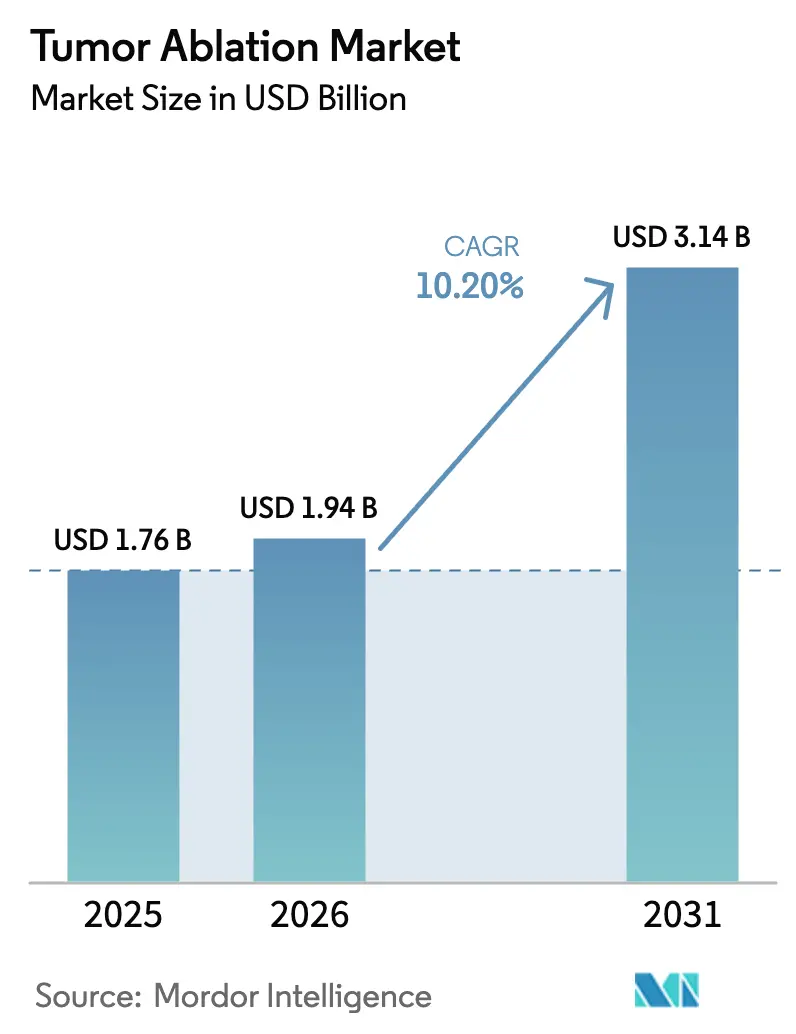

| Market Size (2026) | USD 1.94 Billion |

| Market Size (2031) | USD 3.14 Billion |

| Growth Rate (2026 - 2031) | 10.20% CAGR |

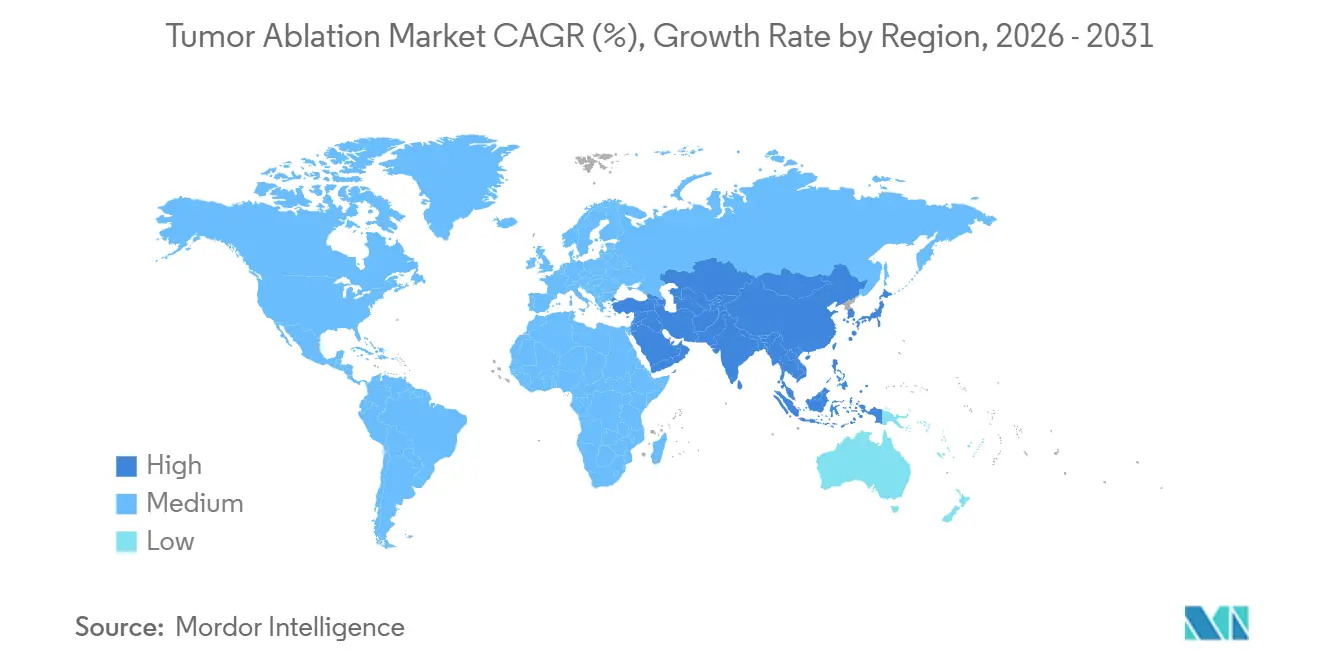

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

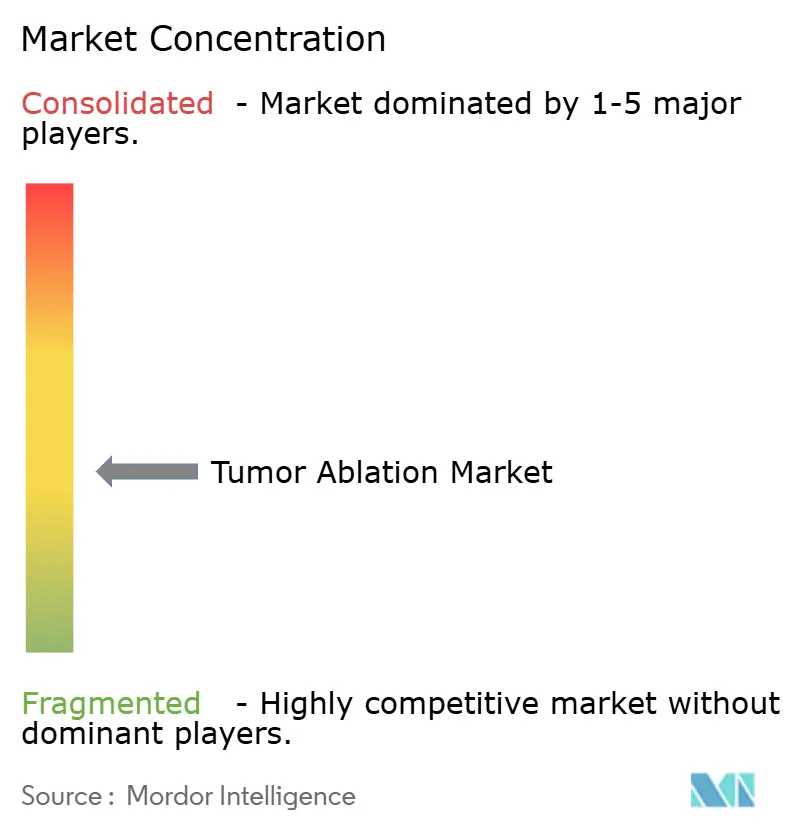

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Tumor Ablation Market Analysis by Mordor Intelligence

The Tumor Ablation Market size is projected to expand from USD 1.76 billion in 2025 and USD 1.94 billion in 2026 to USD 3.14 billion by 2031, registering a CAGR of 10.20% between 2026 to 2031.

This growth is underpinned by the steady rise in cancer incidence, clinician demand for minimally invasive therapies, and regulatory support for non-thermal platforms that solve heat-sink constraints in vascular organs. Hospitals are directing capital from open surgery suites to image-guided ablation rooms, payers are granting codes for emerging modalities, and suppliers are integrating artificial intelligence (AI) to predict lesion margins in real time. Together, these factors improve clinical outcomes, shorten inpatient stays, and expand addressable patient pools, positioning the tumor ablation market as a core pillar of interventional oncology. Strategic acquisitions and joint ventures signal that incumbents aim to hedge thermal portfolios with mechanical and electrical solutions, while local manufacturing incentives in Asia-Pacific are compressing device prices and enlarging the user base.

Key Report Takeaways

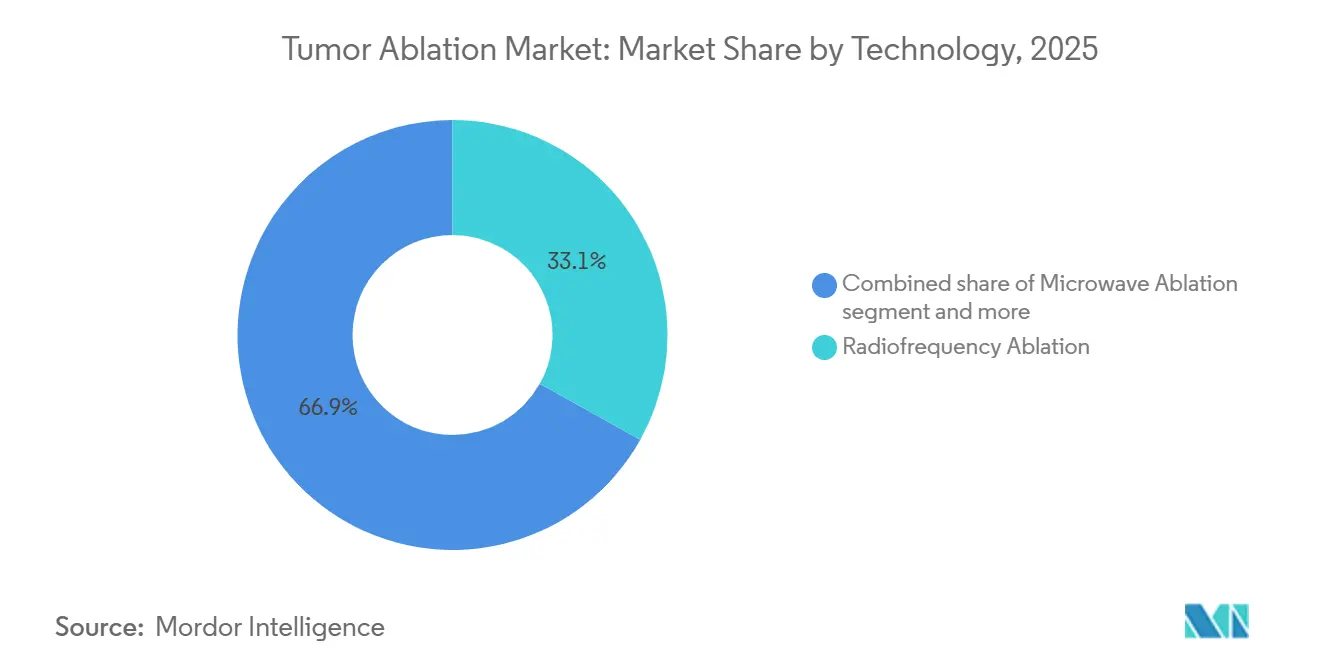

- By technology, radiofrequency ablation held a 33.1% tumor ablation market share in 2025. Histotripsy is forecast to expand at an 11.4% CAGR through 2031, the fastest rate among modalities.

- By mode of treatment, percutaneous access accounted for 46.1% of procedures in 2025, whereas robotic and endoluminal systems are advancing at an 11.1% CAGR through 2031.

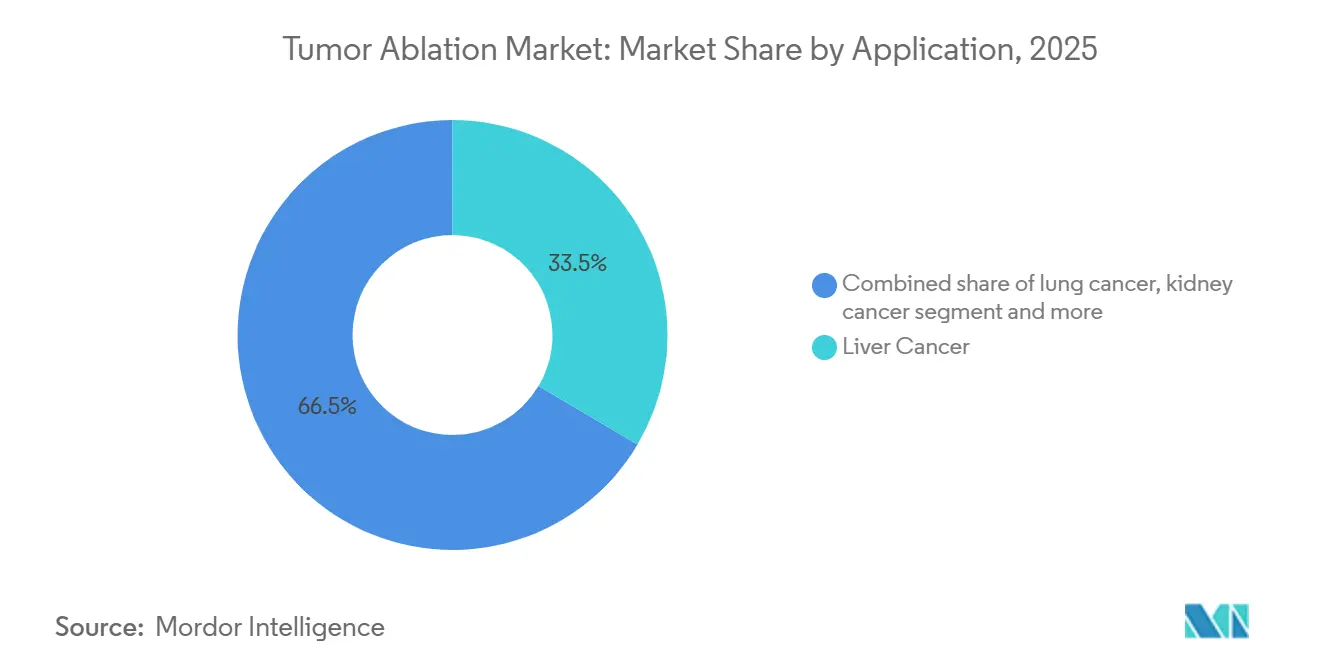

- By application, liver indications commanded 33.5% of value in 2025; lung indications are growing at a 10.8% CAGR to 2031.

- By end user, hospitals retained 46.5% revenue in 2025, yet cancer centers are rising at an 11.8% CAGR on the strength of payer-credentialed interventional oncology suites.

- By geography, North America generated 42.1% of global revenue in 2025, but Asia-Pacific is accelerating at an 11.4% CAGR, supported by domestic production subsidies for ablation generators.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Tumor Ablation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing cancer incidence & prevalence | +2.2% | Global, with highest burden in Asia-Pacific and sub-Saharan Africa | Long term (≥ 4 years) |

| Demand for minimally-invasive surgeries | +1.8% | North America & Europe, expanding to urban APAC centers | Medium term (2-4 years) |

| Device technology innovations (RF, MW, Cryo) | +1.6% | Global, led by North America and Western Europe | Medium term (2-4 years) |

| AI-driven real-time image-guided ablation | +1.5% | North America, Europe, Japan, South Korea | Short term (≤ 2 years) |

| Reimbursable expansion of non-thermal modalities | +1.4% | North America & Europe, with pilot programs in APAC | Medium term (2-4 years) |

| Local manufacturing incentives in emerging markets | +1.3% | APAC core (India, China), spill-over to MEA and Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Cancer Incidence & Prevalence

Global diagnoses for liver, lung, and kidney cancers continue to climb, intensifying demand for focal therapies that spare organ function. The GLOBOCAN 2024 update logged 2.5 million new liver-cancer cases 6% higher than 2022, concentrated in hepatitis-B-endemic East Asia and sub-Saharan Africa. Lung cancer rose to 2.4 million cases in 2024, driven by persistent smoking and urban radon exposure. Kidney cancer reached 430,000 global cases; small renal masses under 4 cm are now routinely managed by percutaneous cryoablation to preserve nephrons. Prostate cancer exceeded 1.4 million cases, and focal high-intensity focused ultrasound (HIFU) is gaining traction for intermediate-risk disease. Collectively, these epidemiologic trends expand the tumor ablation market by creating larger cohorts unsuitable for resection or systemic therapy.

Demand for Minimally Invasive Surgeries

Payers prioritize shorter stays and lower complication rates, driving hospitals to adopt percutaneous and laparoscopic techniques. A 2024 JAMA Surgery study showed that percutaneous radiofrequency ablation (RFA) for colorectal liver metastases reduced median length of stay to 1.2 days from 5.8 days for hepatectomy and saved USD 12,000 per case [1]JAMA Surgery, “Outcomes of Percutaneous Liver Ablation,” jamanetwork.com. Robotic single-port thoracic ablation halved postoperative pain compared with video-assisted thoracoscopic surgery. Laparoscopic microwave ablation achieved 5-year local progression below 8% in early-stage hepatocellular carcinoma, rivaling resection outcomes. Patient surveys indicate 68% of candidates for small renal masses prefer ablation over surgery, citing faster recovery. These findings enlarge the tumor ablation market by persuading clinicians and payers to shift volume from open surgery.

Device Technology Innovations & AI-Guided Ablation

Ablation platforms now integrate AI for real-time margin prediction and adaptive power modulation. The Edison histotripsy system earned FDA clearance in May 2024, enabling mechanical tissue fractionation within 5 mm of bile ducts. Siemens Healthineers fused cone-beam CT with Edison to cut targeting errors to under 2 mm [2]Siemens Healthineers, “Cone-Beam CT Fusion,” siemens-healthineers.com. IceCure Medical’s liquid-nitrogen ProSense cryoablation reaches −160 °C in 10 minutes, with ultrasound-based alerts for critical structures. Medtronic’s Emprint HP microwave generator adjusts wattage based on impedance feedback, improving ablation zone sphericity. Such innovations raise procedure efficiency and safety, broadening physician confidence and accelerating tumor ablation market adoption.

Reimbursable Expansion of Non-Thermal Modalities & Local Manufacturing Incentives

Reimbursement headway and industrial policy are narrowing cost barriers. In January 2024 the Centers for Medicare & Medicaid Services (CMS) introduced Category III CPT 0686T for histotripsy, enabling local coverage decisions and paving the way for national consensus by 2027. Private U.S. insurers followed with positive irreversible-electroporation (IRE) policies in 2025, citing 12-month survival gains in pancreatic cancer. India’s Production-Linked Incentive scheme dedicates INR 50 billion to subsidize homegrown ablation-generator manufacturing, slashing import duty from 28% to 5%. China’s Healthy China 2030 roadmap drove 14 domestic RFA and microwave launches in 2024 priced 40% below multinational devices. These measures reshape pricing dynamics and expand the tumor ablation market footprint in cost-sensitive regions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent regulatory approval pathways | −1.2% | Global, most acute in Europe under MDR and in emerging markets with limited regulatory capacity | Short term (≤ 2 years) |

| High capital cost of advanced platforms | −1.1% | Global, most acute in community hospitals and emerging markets | Medium term (2-4 years) |

| Reimbursement gaps for emerging modalities | −1.0% | North America & Europe for private payers; APAC and MEA for public systems | Medium term (2-4 years) |

| Workforce skill shortages for complex image-guided procedures | −0.9% | Global, especially acute in APAC, MEA, and rural North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Regulatory Approval Pathways & High Capital Cost

The European Union Medical Device Regulation (MDR) that took full effect in May 2024 compels post-market clinical follow-up and periodic safety reporting, adding 12–18 months to CE marking and inflating compliance costs significantly [3]European Commission, “Medical Device Regulation,” ec.europa.eu. Notified-body bottlenecks stretch reviews to 24 months, delaying revenue for mid-tier firms. Capital hurdles intensify the challenge: a turnkey histotripsy suite surpasses USD 1.5 million, while IRE and HIFU systems range from USD 400,000 to USD 1.2 million. Hospitals need 80+ procedures yearly to break even within five years, an unattractive proposition without guaranteed reimbursement. These cost-regulatory combinations slow device deployment and temporarily temper tumor ablation market velocity.

Reimbursement Gaps & Workforce Skill Shortages

As of 2026, only 12 U.S. states have Medicare Administrative Contractors that reimburse histotripsy; 38 states lack clarity. German, French, and U.K. health-technology-assessment agencies await 3-year survival data before adding histotripsy to diagnosis-related group schedules, discouraging hospital investment. Simultaneously, workforce supply is tight: the Society of Interventional Radiology (SIR) cites 1,200 fellowship slots globally versus an annual requirement of 2,500 specialists. Training spans 12–18 months of supervised cone-beam CT fusion and electromagnetic tracking. Rural hospitals face additional recruitment hurdles, and tele-mentoring pilots remain hamstrung by licensure barriers. Together, these gaps moderate near-term expansion of the tumor ablation market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Mechanical Modalities Challenge Thermal Dominance

Radiofrequency systems retained a 33.1% tumor ablation market share in 2025, supported by decades of evidence and established CPT codes. Nevertheless, histotripsy leads segment growth with an 11.4% CAGR, reflecting clinician demand for non-thermal approaches that avoid heat-sink effects near vessels. Microwave ablation overcomes perfusion cooling by achieving intratumoral temperatures above 100 °C and captured further share through Medtronic’s Emprint HP platform. Cryoablation appeals in renal and breast indications because ice-ball boundaries are visible on CT and ultrasound, facilitating precise margins.

As capital budgets migrate toward multi-modality rooms, hospitals evaluate lifetime costs across thermal and mechanical systems. Histotripsy’s ability to treat tumors within 5 mm of vital structures widens clinical candidacy and elevates procedure reimbursement, reinforcing its rapid uptake. In aggregate, these dynamics sustain robust growth while gradually diversifying the modality mix within the tumor ablation market.

By Mode of Treatment: Robotic Platforms Redefine Access

Percutaneous procedures dominated 46.1% of volumes in 2025 and remain the workhorse for hepatocellular carcinoma and small renal masses. Robotic and endoluminal systems, however, are rising at an 11.1% CAGR as hospitals invest in electromagnetic navigation and single-port access to cut recovery time. The Monarch robotic bronchoscopy platform delivers microwave probes to peripheral lung nodules through natural airways, lowering chest-tube complications to under 2%. Hybrid operating rooms that combine fixed CT gantries with robotic arms enable diagnosis and ablation in a single session, reducing patient cycle time and driving higher throughput. These workflow gains expand the tumor ablation market size for advanced access solutions.

By Application: Lung Ablation Outpaces Liver Growth

Liver applications accounted for 33.5% of value in 2025, validated by Barcelona Clinic protocols that recommend RFA or microwave for solitary tumors under 3 cm. Lung applications are projected to grow at a 10.8% CAGR, propelled by oligometastatic paradigms and National Comprehensive Cancer Network (NCCN) guideline inclusion. Percutaneous microwave achieves 88% local control for lesions under 2 cm, and transbronchial routes reduce pneumothorax risk. Kidney, bone, prostate, and breast indications represent secondary opportunities but collectively enrich procedure diversity, supporting incremental expansion of the tumor ablation market.

By End User: Cancer Centers Capture Specialized Volume

Hospitals held 46.5% revenue in 2025 thanks to existing imaging infrastructure, yet dedicated cancer centers are advancing at an 11.8% CAGR as payers credential interventional oncology suites offering faster throughput. Bundled-payment contracts allow centers to undercut hospital charges by 20% while maintaining margins through higher case volumes. These specialized environments are early adopters of histotripsy and IRE, accelerating diffusion of next-generation systems and lifting overall tumor ablation market adoption curves.

Geography Analysis

North America generated 42.1% of revenue in 2025, anchored by 1.9 million annual cancer diagnoses, 400 fellowship graduates each year, and Medicare coverage for established modalities. The January 2024 CPT 0686T code for histotripsy accelerated hospital purchasing committees, and private insurers in 15 states issued policies within 18 months. Canada is piloting bundled payments to shift 30% of hepatocellular cases from surgery to percutaneous ablation by 2027, while Mexico’s social-security agency procured 50 microwave units in 2025 to clear treatment backlogs.

Asia-Pacific is forecast to grow at an 11.4% CAGR and is the primary arena for manufacturing incentives. India’s INR 50 billion subsidy lowers domestic device prices by 35%. China’s 14 local manufacturers launched RFA and microwave platforms in 2024, prompting Siemens Healthineers and Medtronic to localize production to protect share. Japan reimbursed IRE for pancreatic tumors in 2025, and South Korea invested KRW 120 billion in regional histotripsy hubs. These initiatives collectively expand the tumor ablation market across Asia’s large patient base.

Europe benefits from the EU Beating Cancer Plan, which earmarked EUR 4 billion for oncology modernization, including ablation suites. Germany’s statutory insurers added histotripsy to benefits in 2025, triggering orders at major university hospitals. The U.K.’s National Health Service is piloting microwave ablation for colorectal liver metastases to cut surgical waitlists by 15%. Middle East & Africa and South America remain nascent but are leveraging international finance facilities and local-content rules to accelerate device uptake, gradually enlarging their share of the tumor ablation market.

Competitive Landscape

The tumor ablation industry is moderately concentrated: the top five vendors captured the majority of global revenue in 2025. Medtronic, Boston Scientific, AngioDynamics, Johnson & Johnson, and Siemens Healthineers dominate thermal modalities, yet venture-backed entrants are fragmenting share with mechanical and electrical solutions. Medtronic’s 2024 co-marketing deal with HistoSonics grants access to histotripsy without cannibalizing its Emprint microwave line. Boston Scientific’s 2025 minority stake in Emblation extends reach into liquid-jet ablation for cardiac arrhythmias that could segue into oncology.

Competitive thrust now centers on AI-driven thermometry, electrode geometry, and real-time imaging fusion. Vendors integrating cone-beam CT and electromagnetic tracking boast 18–22% shorter procedures, a metric that strongly influences capital committees. Regulatory complexity under MDR is prompting mid-tier firms to exit Europe, freeing shares for multinationals with robust quality-system budgets. Meanwhile, local manufacturers in India and China are pricing systems 35–40% below imported equivalents, compelling multinationals to establish joint ventures or risk eroding their position in these high-growth segments. These dynamics reinforce a fluid competitive backdrop that will shape tumor ablation market trajectories over the next decade.

Tumor Ablation Industry Leaders

Medtronic plc

Johnson & Johnson (Ethicon)

Boston Scientific Corp.

AngioDynamics Inc.

Siemens Healthineers

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: IceCure Medical received FDA marketing authorization for its ProSense cryoablation system specifically for treating low-risk breast cancer in women aged 70 and older.

- July 2025: Varian (a Siemens Healthineers company) launched its next-generation IntelliBlate microwave ablation system in Europe following CE Mark approval.

- June 2025: Medtronic received U.S. FDA 510(k) clearance for the Visualase V2 MRI-Guided Laser Ablation System. It provides a minimally invasive option for brain tumors, focal epilepsy, and radiation necrosis.

Global Tumor Ablation Market Report Scope

As per the scope of the report, Tumor ablation is a minimally invasive medical procedure that destroys cancerous or benign cells by delivering targeted energy or chemicals directly into a tumor. This approach is often used for patients who are not suitable candidates for traditional surgery due to the tumor's location, poor health, or reduced organ function, and it is a common treatment for tumors in the liver, kidneys, lungs, and bones.

The tumor ablation market is segmented by technology, mode of treatment, application, end user, and geography. By technology, the market is categorized into radiofrequency ablation, microwave ablation, cryoablation, irreversible electroporation, high-intensity focused ultrasound (HIFU), and histotripsy. By mode of treatment, it is segmented into surgical ablation, laparoscopic ablation, percutaneous ablation, and robotic/endoluminal ablation. By application, it is segmented into Liver Cancer, Lung Cancer, kidney cancer, bone metastasis, prostate Cancer, breast & soft-tissue tumors, and other cancers (incl. pancreas, bladder, brain). By end user, the segmentation includes hospitals, cancer centers, and others. Geographically, the market is segmented across North America, Europe, the Asia-Pacific region, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Radiofrequency (RF) Ablation |

| Microwave Ablation |

| Cryoablation |

| Irreversible Electroporation |

| High-Intensity Focused Ultrasound (HIFU) |

| Histotripsy |

| Surgical Ablation |

| Laparoscopic Ablation |

| Percutaneous Ablation |

| Robotic / Endoluminal Ablation |

| Liver Cancer |

| Lung Cancer |

| Kidney Cancer |

| Bone Metastasis |

| Prostate Cancer |

| Breast & Soft-Tissue Tumors |

| Other Cancers (incl. Pancreas, Bladder, Brain) |

| Hospitals |

| Cancer Centers |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Technology | Radiofrequency (RF) Ablation | |

| Microwave Ablation | ||

| Cryoablation | ||

| Irreversible Electroporation | ||

| High-Intensity Focused Ultrasound (HIFU) | ||

| Histotripsy | ||

| By Mode of Treatment | Surgical Ablation | |

| Laparoscopic Ablation | ||

| Percutaneous Ablation | ||

| Robotic / Endoluminal Ablation | ||

| By Application | Liver Cancer | |

| Lung Cancer | ||

| Kidney Cancer | ||

| Bone Metastasis | ||

| Prostate Cancer | ||

| Breast & Soft-Tissue Tumors | ||

| Other Cancers (incl. Pancreas, Bladder, Brain) | ||

| End User | Hospitals | |

| Cancer Centers | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the tumor ablation market?

The tumor ablation market size is expected to reach USD 1.94 billion in 2026 and is forecast to grow to USD 3.14 billion by 2031.

Which technology is growing the fastest?

Histotripsy leads growth with an 11.4% CAGR through 2031, outpacing thermal modalities.

Why is Asia-Pacific expanding more quickly than other regions?

Domestic manufacturing incentives in India and China, coupled with rising cancer incidence, are driving an 11.4% CAGR in Asia-Pacific.

What limits wider adoption of next-generation platforms?

High capital costs and fragmented reimbursement, especially for histotripsy and irreversible electroporation, slow hospital purchasing.

Page last updated on: