Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

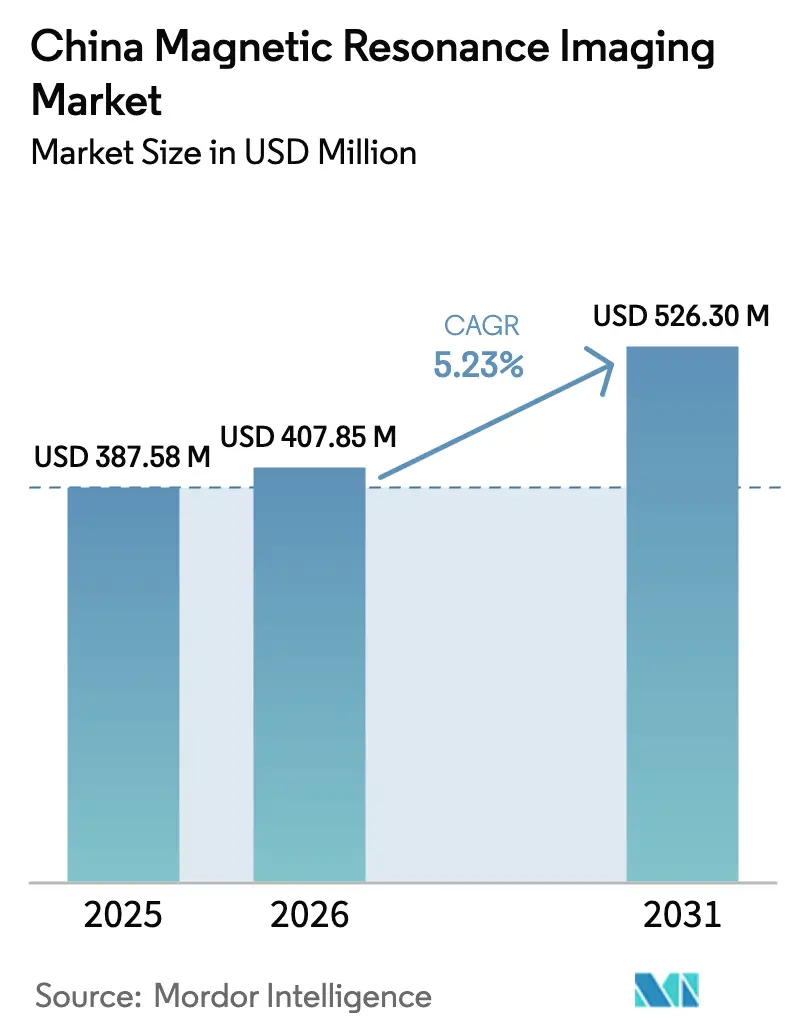

| Base Year Market Size (2025) | USD 387.58 Million |

| Market Size (2026) | USD 407.85 Million |

| Market Size (2031) | USD 526.3 Million |

| Growth Rate (2026 - 2031) | 5.23% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

China Magnetic Resonance Imaging Market Analysis by Mordor Intelligence

The China MRI market size was valued at USD 387.58 million in 2025 and estimated to grow from USD 407.85 million in 2026 to reach USD 526.3 million by 2031, at a CAGR of 5.23% during the forecast period (2026-2031). Continued public-health spending, helium-free magnet roll-outs, and widespread hospital AI adoption keep demand resilient despite lingering macro-economic uncertainty. Domestic vendors now supply most mid-field units, encouraged by volume-based procurement rounds that compress prices yet expand installed base coverage. Helium scarcity is accelerating solid-cooling innovation, while portable low-field systems open an entirely new access tier for rural stroke care. Finally, regulatory fast-tracks under the “Healthy China 2030” policy shorten time-to-market for novel systems and safeguard domestic R&D investment.

Key Report Takeaways

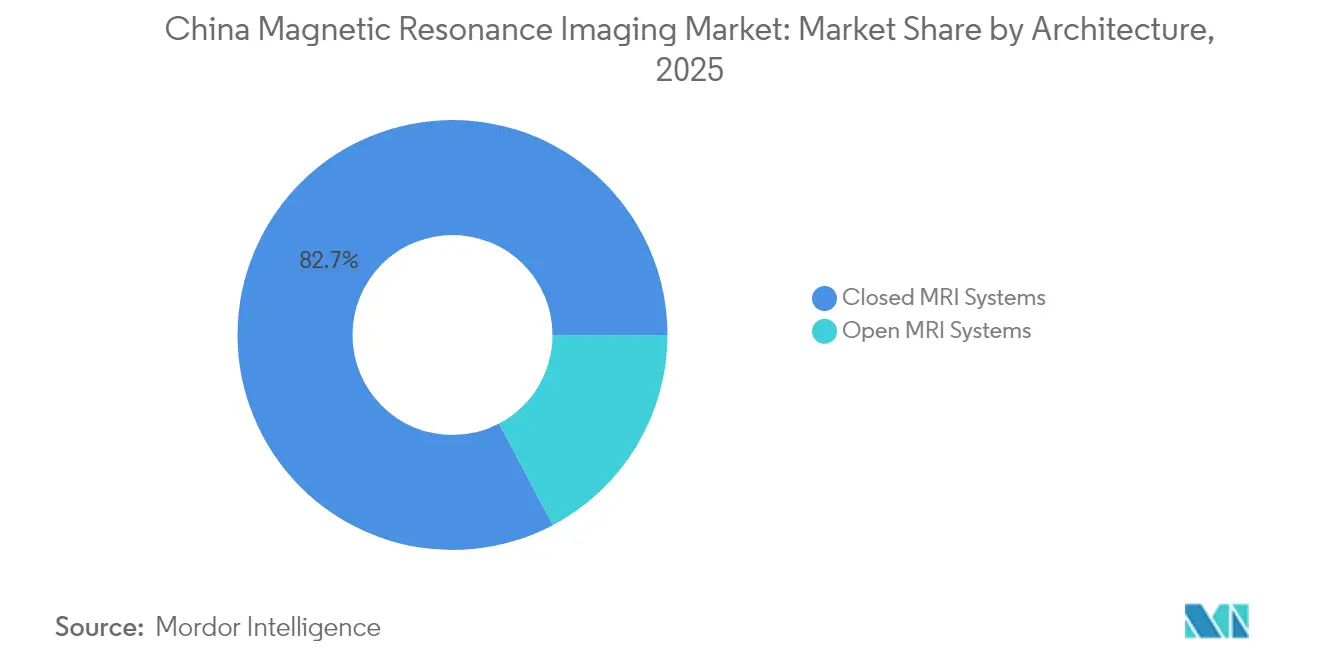

- By architecture, closed MRI systems led with 82.73% revenue share in 2025, while open systems are projected to expand at a 6.02% CAGR through 2031.

- By field strength, mid/high-field (1–3 T) systems held 55.74% of the China MRI market share in 2025, and ultra-high-field (>3 T) systems are forecast to grow 5.63% CAGR to 2031.

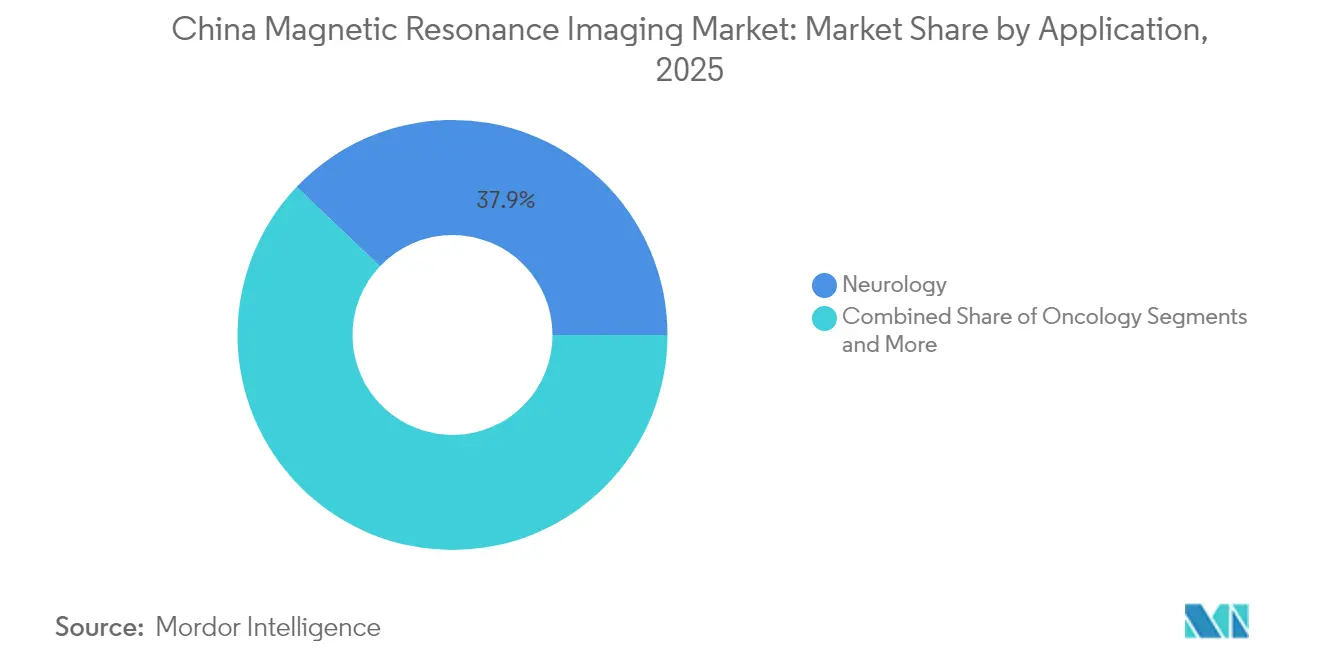

- By application, neurology accounted for 37.92% share of the China MRI market size in 2025 and oncology is advancing at a 6.03% CAGR through 2031.

- By end user, hospitals captured 47.88% share of the China MRI market size in 2025 while stand-alone imaging centers record the fastest projected CAGR at 6.18% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Magnetic Resonance Imaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging Population & Chronic-Disease Burden | +1.2% | National, concentrated in tier-1 cities | Long term (≥ 4 years) |

| Expansion Of Universal Health Coverage | +0.8% | National, with rural emphasis | Medium term (2-4 years) |

| Strong Central-Government Commitments Under "Healthy China 2030" | +1.0% | National | Long term (≥ 4 years) |

| Adoption Of High-/Ultra-High-Field & Hybrid MRI | +0.7% | Tier-1 and tier-2 cities | Medium term (2-4 years) |

| Volume-Based Procurement Fueling Domestic OEMs | +0.9% | National | Short term (≤ 2 years) |

| Rise Of Portable Low-Field MRI For Stroke Triage | +0.5% | Rural and emergency care settings | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Aging Population & Chronic-Disease Burden

China’s fast-graying society fuels imaging demand as inpatient costs for citizens aged ≥ 65 averaged USD 1,199.24 per stay in 2024 and continue to climb [1]He Shanheng, “Older Adults’ Hospitalization Costs Study in China,” Frontiers in Public Health, frontiersin.org. Chronic cardiac and neurovascular conditions often require MRI follow-up, and intracranial-aneurysm prevalence of 7%—well above global norms—further concentrates neurologic workload. Tier-1 hospitals respond with high-field upgrades that improve signal-to-noise ratios essential for micro-vascular scans. AI-enabled cardiac MRI now screens 11 cardiovascular pathologies at AUC 0.988 across eight centers, illustrating clinical gains that reinforce adoption. Together these demographic and disease trends lift exam volumes and justify broader capital budgets for next-generation systems.

Expansion of Universal Health Coverage

Commercial medical-insurance premiums reached RMB 900 billion in 2025, complementing public insurance and broadening reimbursement for advanced imaging. Diagnosis-Related Group payment caps cover more than 80% of inpatient expenditure, motivating hospitals to buy faster multipurpose scanners that clear patient backlogs. Rural capsule-clinic pilots rely on portable units that plug into wall outlets and deliver stroke triage accuracy comparable to fixed 1.5 T rooms, bridging access gaps. Together, coverage expansion and flexible reimbursement frameworks extend MRI utilization well beyond metropolitan corridors.

Strong Central-Government Commitments under “Healthy China 2030”

Regulatory reform remains pivotal: the National Medical Products Administration (NMPA) issued twenty-four measures in January 2025 that include parallel reviews and tax credits for innovative devices. Capital subsidies and procurement preferences favor domestic OEMs, aligning with targets to list six Chinese device firms among the global top 50 by 2025. Strategic mergers—such as Neusoft Medical’s state-backed equity infusion—build national champions that can compete overseas and defend local market share.

Adoption of High-/Ultra-High-Field & Hybrid MRI

United Imaging’s FDA-cleared 5 T scanner bridges the gap between mainstream 3 T and research-grade 7 T units, making sub-millimeter neuro-imaging viable in routine practice. Ultra-high-gradient 3 T platforms now finish a prostate study in 5.5 minutes while retaining diagnostic quality. Hybrid PET/MRI continues its oncology base yet gains traction in cardiology and epilepsy care as radiopharmaceutical approvals rise. These upgrades pivot hospitals toward premium modalities that shorten throughput time and enhance precision.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital & Helium-Related Opex | -1.5% | National, acute in tier-2/3 cities | Medium term (2-4 years) |

| Lengthy NMPA Class III Device Approval | -0.8% | National | Short term (≤ 2 years) |

| Radiologist Shortage & Workflow Bottlenecks | -0.7% | National, severe in rural areas | Long term (≥ 4 years) |

| Margin Squeeze From Centralized Price Caps | -1.0% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capital & Helium-Related Opex

China consumes 25.65 million m³ of helium annually yet produces only 1.3 million m³, driving 95% import dependence. Spot prices have spiked 250% since 2015, squeezing hospital budgets and delaying service contracts. Conventional scanners consume roughly 27% of global helium each year, prompting shutdowns when supply is rationed [2]Henderson Mary, “Keeping an Eye on the Potential Shortage of Helium for MRIs,” RSNA News, rsna.org . OEMs now race to deploy solid-cooling magnets; Wandong Medical’s helium-free 1.5 T system maintains –269 °C coil temperature while reducing operating costs by more than one-half. These engineering gains mitigate, but do not yet eliminate, cost pressure in lower-tier cities.

Lengthy NMPA Class III Device Approval

Class III MRI devices undergo the most rigorous Chinese review cycle, requiring multi-center trials that prolong market entry. Despite the 2025 reform package, imported models still face longer queues than locally developed units and must establish on-shore quality-management systems before bidding eligibility. The time lag disadvantages foreign vendors in fast-moving procurement rounds and slows technology diffusion to end users eager for the latest software features.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Architecture: Closed Systems Maintain Dominance

Closed units accounted for 82.73% of the China MRI market in 2025 because their higher field strength supports complex neuro-oncologic and cardiac protocols. Throughput pressure and newer algorithms that automate patient positioning now let these sealed tunnels finish a brain scan in as little as 4 minutes. The arrival of wider-bore closed systems further improves patient comfort, eroding historical open-MRI advantages. Open designs nonetheless grow at a 6.02% CAGR as surgeons adopt intra-operative guidance and imaging centers cater to bariatric or claustrophobic populations. Hospitals in secondary cities increasingly buy hybrid models that promise closed-style image fidelity within semi-open form factors, balancing versatility with workflow efficiency.

A parallel engineering trend focuses on helium-free closed magnets, which slash long-term ownership costs and temper supply-chain exposure. Domestic vendors leverage government grants to redesign coil architecture around solid cryogens, strengthening their value proposition in tender documents. As end users weigh capital expenditure against function, closed systems retain the largest slice of the China MRI market size even as architectural preferences diversify.

By Field Strength: Mid-Field Rules, Ultra-High Field Accelerates

Mid/high-field 1-3 T units captured 55.74% of the China MRI market size in 2025 thanks to their clinical versatility and moderate siting requirements. Dual-gradient hardware and AI-driven reconstruction now let 1.5 T scanners rival 3 T detail in some orthopedic tests, protecting installed mid-field bases from immediate obsolescence. Concurrently, ultra-high-field >3 T platforms post a 5.63% CAGR on the back of precision-medicine research, advanced epilepsy mapping, and micro-vasculature imaging in dementia trials. United Imaging’s 5 T entry offers a pragmatic bridge that fits existing suites yet unlocks sub-millimeter resolution, foreshadowing broader ultra-high-field clinical mainstreaming.

Low-field systems, once relegated to niche uses, return to relevance via deep-learning reconstruction that compensates for weaker signal. Whole-body 0.05 T prototypes now produce diagnostic images in open wards without RF-shielded rooms. This resurgence addresses access inequity in county-level hospitals while offering stroke care within ambulance-based units.

By Application: Neurology Leads, Oncology Gains Speed

Neurology contributed 37.92% to the China MRI market share in 2025, mirroring the nation’s disproportionate intracranial-aneurysm and stroke burden. High-resolution vascular sequences and post-processing AI spot sub-3 mm aneurysms often missed by manual reads. Oncology, expanding at a 6.03% CAGR, benefits from aggressive screening programs for lung and colorectal cancer alongside growing PET/MRI adoption for treatment planning. Cardiology pushes AI-enabled CMR into daily practice, achieving near-real-time strain analysis and boosting throughput for ischemic heart-disease clinics. Musculoskeletal and gastroenterology segments also gain from motion-correction software and nanoprobe-based contrast agents that improve liver-fibrosis staging.

By End User: Hospitals Dominate, Imaging Centers Surge

Hospitals owned 47.88% of the China MRI market size in 2025, leveraging bundled procurement contracts and integrated service coverage. DRG-tied reimbursement incentives push tertiary centers to install faster scanners with automated workflows that maximize daily slot turnover. Stand-alone imaging centers, however, advance at 6.18% CAGR as commercial insurance channels reimburse premium studies and entrepreneurs build high-throughput facilities in suburban catchments. Rural mobile clinics and research labs form a smaller but strategic “Others” segment, often adopting portable or specialty coils to satisfy targeted diagnostic needs without heavy infrastructure.

Geography Analysis

Tier-1 cities—Beijing, Shanghai, Guangzhou, and Shenzhen—house the densest concentration of 3 T and above systems, reflecting higher disposable income and research-hospital clusters. Many academic centers place 7 T scanners in dedicated neuroscience wings to study micro-bleeds and small-vessel disease, reinforcing their reputation as technology incubators. Provincial capital hospitals emulate these leaders by purchasing 1.5 T helium-free units that reduce operating costs yet still deliver comprehensive protocol coverage. Migration from rural provinces to coastal megacities maintains imaging volumes and underpins supplementary service contracts.

Tier-2 and tier-3 cities constitute the next adoption wave. Local governments leverage central stimulus grants to modernize medical equipment, prioritizing mid-field scanners that avoid the power-upgrade costs tied to legacy 3 T rooms. Volume-based procurement rounds allow multiple county hospitals to combine orders, driving unit pricing down and reinforcing domestic manufacturers’ competitive edge. As private insurers expand, imaging centers in these cities deploy open configurations that cater to geriatrics and interventional pain management, diversifying revenue channels.

Rural regions still face access gaps, but mobile capsule clinics equipped with 0.23 T stroke-triage systems now bridge distances of hundreds of kilometers. Real-time teleradiology over 5G networks connects village doctors with urban neuroradiologists, ensuring timely interpretation even when staffing is thin. Government “Internet + Healthcare” policies fund these tele-network backbones, and AI triage algorithms further suppress report turnaround time. Over the forecast horizon, balanced regional deployment is expected as domestic OEMs refine ruggedized units suited to China’s vast interior.

Competitive Landscape

The China MRI market is moderately consolidated, with United Imaging Healthcare, Neusoft Medical, and Wandong Medical expanding share through cost-competitive bids and helium-free differentiation. International incumbents Siemens Healthineers, GE HealthCare, and Philips Healthcare remain technology leaders in ultra-high-field research, yet price caps on centralized tenders compress margins. Domestic firms increasingly secure Class III clearances abroad—the 5 T Jupiter scanner gained U.S. FDA approval in 2024—bolstering export credibility and leveling the prestige gap.

Strategic alliances proliferate. Neusoft Medical teamed with General Technology Group to secure financing and broaden service networks, while Siemens committed USD 314 million to a new Suzhou manufacturing site that localizes 1.5 T and 3 T production. Hyperfine extended portable-scanner distribution to Middle-Eastern markets, demonstrating global appetite for point-of-care ultralow-field platforms [3]Hyperfine Inc., “Hyperfine Expands Distribution to Europe and the Middle East,” hyperfine.io . The resulting innovation race spans AI workflow engines, quantum-accelerated reconstruction software, and sealed-magnet cooling stacks.

Pricing power tilts toward buyers under volume-based procurement, pressing vendors to bundle service contracts, AI modules, and training into one recurrent-revenue subscription. Companies that master this model secure renewal stickiness and data-lake assets critical for algorithm refinement. Over the next five years, the interplay between regulatory encouragement for domestic champions and relentless helium constraints will dictate share realignment.

China Magnetic Resonance Imaging Industry Leaders

-

Siemens AG

-

Canon Medical Systems

-

GE Healthcare

-

Koninklijke Philips NV

-

JiangSu Magspin Instrument Co. Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: The world’s first multi-position, cryogen-free MRI, co-developed with University of Nottingham Ningbo China, entered routine use at a Ningbo hospital.

- January 2025: As part of retaliation against new U.S. tariffs, China unveiled plans to restrict certain rare-earth exports used in medical-imaging components.

- July 2023: A Chinese 1.5 T scanner developed by Shenzhen Institute of Advanced Technology began mass production, lowering exam fees for patients.

- March 2023: United Imaging debuted the uMR Jupiter 5 T whole-body system at the European Congress of Radiology.

China Magnetic Resonance Imaging Market Report Scope

As per the scope of this report, magnetic resonance imaging is a medical imaging technique, which is used in radiology to produce pictures of the anatomy and the physiological processes of the body. These pictures are further used to diagnose and detect the presence of abnormalities in the body. China Magnetic Resonance Imaging (MRI) Market is segmented by Architecture (Closed MRI Systems and Open MRI Systems), Field Strength (Low Field MRI Systems, High Field MRI Systems, Very High Field MRI Systems and Ultra-high MRI Systems), Application (Oncology, Neurology, Cardiology, Gastroenterology, Musculoskeletal, and Other Applications). The report offers the value (in USD million) for the above segments.

By Architecture

| Closed MRI Systems |

| Open MRI Systems |

By Field Strength

| Low-Field (<1T) |

| Mid/High-Field (1–3T) |

| Very- & Ultra-High-Field (>3T) |

By Application

| Neurology |

| Oncology |

| Cardiology |

| Musculoskeletal |

| Gastroenterology |

| Others (urology, gynecology, etc.) |

By End User

| Hospitals |

| Stand-alone Imaging Centers |

| Others |

| By Architecture | Closed MRI Systems |

| Open MRI Systems | |

| By Field Strength | Low-Field (<1T) |

| Mid/High-Field (1–3T) | |

| Very- & Ultra-High-Field (>3T) | |

| By Application | Neurology |

| Oncology | |

| Cardiology | |

| Musculoskeletal | |

| Gastroenterology | |

| Others (urology, gynecology, etc.) | |

| By End User | Hospitals |

| Stand-alone Imaging Centers | |

| Others |

Key Questions Answered in the Report

How big is the China Magnetic Resonance Imaging Market?

The China Magnetic Resonance Imaging Market size is expected to reach USD 407.85 million in 2026 and grow at a CAGR of 5.23% to reach USD 526.3 million by 2031.

What segment is growing fastest by application?

Oncology imaging shows the quickest expansion at a 6.03% CAGR through 2031.

Who are the key players in China Magnetic Resonance Imaging Market?

Siemens AG, Canon Medical Systems, GE Healthcare, Koninklijke Philips NV and JiangSu Magspin Instrument Co. Ltd are the major companies operating in the China Magnetic Resonance Imaging Market.

How does helium scarcity affect MRI ownership costs?

Helium prices up 250% over the past decade have heightened operating expenses, spurring demand for helium-free magnets.

Page last updated on: