Fundus Camera Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

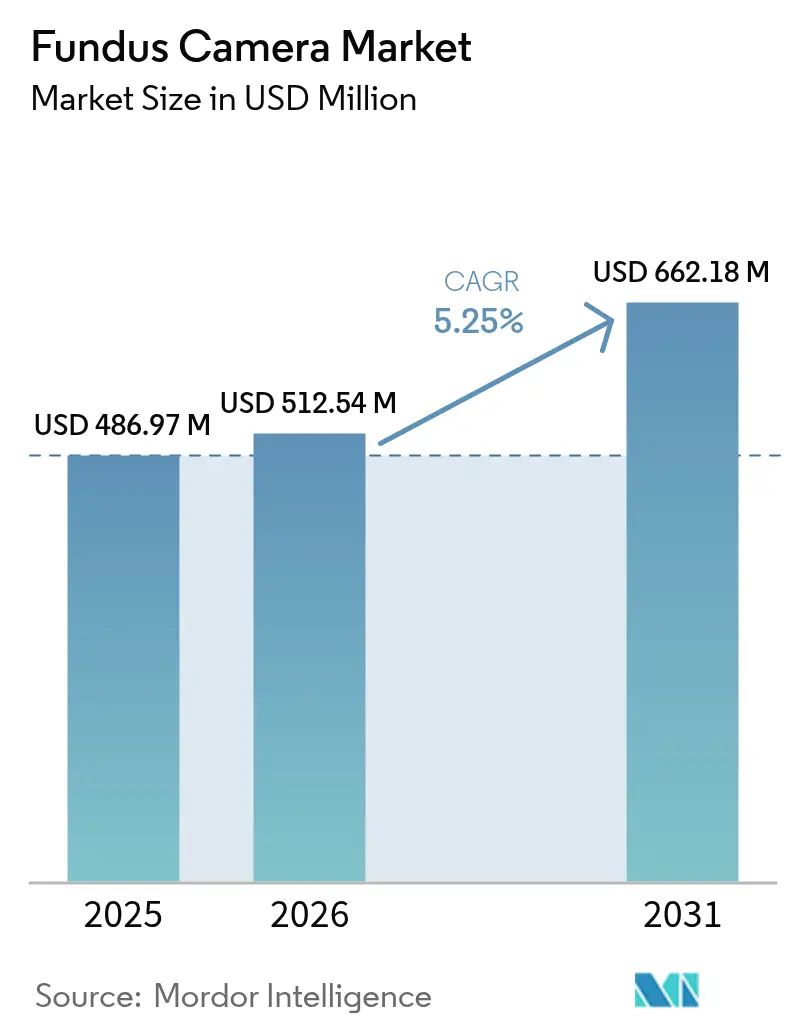

| Market Size (2026) | USD 512.54 Million |

| Market Size (2031) | USD 662.18 Million |

| Growth Rate (2026 - 2031) | 5.25% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Fundus Camera Market Analysis by Mordor Intelligence

Fundus Camera Market size in 2026 is estimated at USD 512.54 million, growing from 2025 value of USD 486.97 million with 2031 projections showing USD 662.18 million, growing at 5.25% CAGR over 2026-2031.

Demand strengthens as artificial-intelligence algorithms move from pilot to routine use, with FDA-cleared platforms such as IDx-DR and EyeArt showing more than 96% sensitivity for diabetic-retinopathy detection. Mandatory screening programs, improved reimbursement for tele-ophthalmology, and CMS guidance that recognizes AI-interpreted fundus photography as medically necessary are expanding adoption. Product preferences continue to favor non-mydriatic systems that integrate smoothly with electronic health records, yet hybrid and ultra-widefield devices are growing fastest because they capture up to 200 degrees of retinal surface. Portable hand-held cameras dominate modality demand, while combination platforms that fuse OCT and fundus photography gain momentum for comprehensive retinal assessment. Regionally, North America leads on market share, but Asia-Pacific posts the highest growth as diabetes prevalence rises and governments invest in community eye-care delivery.

Key Report Takeaways

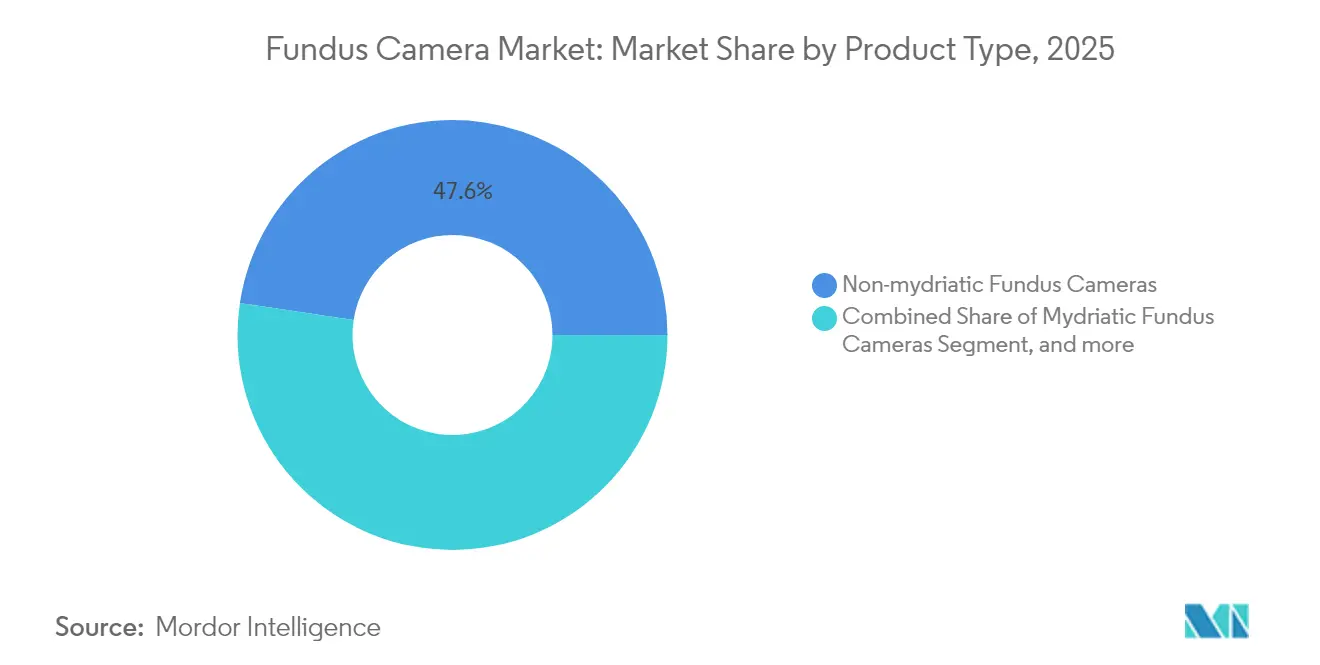

- By product type, non-mydriatic systems held 47.62% of fundus camera market share in 2025, whereas hybrid and wide-field cameras are projected to grow at a 6.32% CAGR to 2031.

- By modality, hand-held devices accounted for 53.10% share of the fundus camera market size in 2025; combination imaging platforms are advancing at a 7.02% CAGR through 2031.

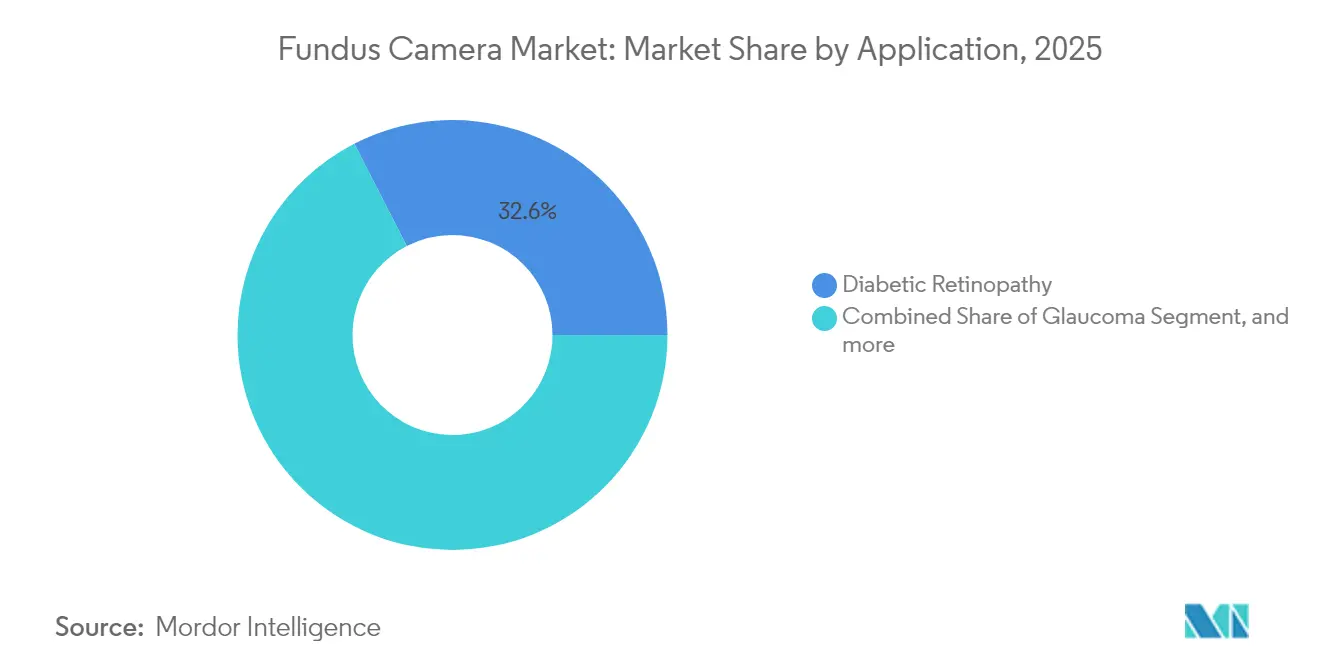

- By application, diabetic-retinopathy screening led with 32.55% revenue share in 2025, while age-related macular degeneration applications are forecast to expand at an 8.28% CAGR to 2031.

- By end user, hospitals captured 52.10% share of the fundus camera market in 2025, whereas specialty clinics are set to grow at a 8.88% CAGR up to 2031.

- By geography, North America dominated with a 41.20% share in 2025, yet Asia-Pacific shows the fastest 6.55% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Fundus Camera Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating Diabetic-Retinopathy Screening Mandates | +1.2% | Global, with early gains in North America, EU | Medium term (2-4 years) |

| Rapid Adoption of AI-Embedded Imaging Workflows | +1.8% | North America & EU, spill-over to APAC core | Short term (≤ 2 years) |

| Prevalence Spike of Age-Related Macular Degeneration | +0.9% | Global, concentrated in aging populations | Long term (≥ 4 years) |

| Tele-Ophthalmology Reimbursement Parity | +1.1% | North America, expanding to EU and APAC | Medium term (2-4 years) |

| Smartphone-Based Neonatal ROP Screening Roll-Outs | +0.7% | APAC core, emerging in MEA and Latin America | Medium term (2-4 years) |

| ESG-Linked Procurement Favouring Low-Energy Handhelds | +0.4% | EU leading, North America following | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerating Diabetic-Retinopathy Screening Mandates

Many countries now require annual retinal exams for people with diabetes, and U.S. Medicare policies deem AI-interpreted fundus images medically necessary. These rules spur bulk purchases of cameras that produce AI-ready images and support telemedicine workflows. More than 4.1 million U.S. adults live with diabetic retinopathy, and systematic screening using fundus cameras prevents avoidable vision loss while lowering long-term care costs.[1]Medicare Coverage Database, Centers for Medicare & Medicaid Services, cms.gov

Rapid Adoption of AI-Embedded Imaging Workflows

FDA-cleared AI platforms such as IDx-DR deliver ≥ 96% sensitivity and ≥ 93% specificity, producing results within three minutes of capture. Optos, Nikon and Google have co-developed ultra-widefield AI tools that detect macular edema alongside retinopathy.[2]Optos AI-Based Ultra-Widefield Imaging, Optos, optos.com Clinicians value the speed, consistency and reduced dependence on specialist readers, making AI-enabled cameras an essential element of expanded screening programs.

Prevalence Spike of Age-Related Macular Degeneration

AMD rates are climbing as populations age. Ultra-widefield imaging and AI algorithms detect drusen and pigment changes earlier than standard methods, enabling timely therapies that preserve vision.[3]Global Burden of Disease Study 2024, Nature, nature.com Manufacturers are embedding AMD-specific analytics into camera software, positioning the technology for broader preventive use.

Tele-Ophthalmology Reimbursement Parity

U.S. payers such as Aetna reimburse fundus photography delivered via telehealth under dedicated CPT codes, treating it as equal to in-office exams. Similar policies are advancing in the EU and parts of APAC. Parity removes financial barriers, especially for rural programs that rely on portable cameras linked to cloud readers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capex Versus OCT-Combo Systems | -0.8% | Global, particularly affecting smaller practices | Medium term (2-4 years) |

| Shortage of Trained Ophthalmic Technicians in LMICs | -0.6% | APAC, MEA, Latin America rural regions | Long term (≥ 4 years) |

| Data-Privacy Hurdles for Cloud-Based Retinal Archives | -0.4% | EU leading due to GDPR, expanding globally | Short term (≤ 2 years) |

| Import-Tariff Volatility on Optical Components | -0.5% | Global, with highest impact in North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capex Versus OCT-Combo Systems

Combination imaging platforms command premium pricing due to their sophisticated technology integration, with systems often exceeding USD 100,000 compared to standalone fundus cameras priced below USD 50,000. This cost differential becomes particularly challenging for specialty eye clinics and ambulatory surgical centers operating under tight budget constraints while seeking to offer comprehensive diagnostic capabilities. The economic pressure intensifies when considering ongoing maintenance costs, software licensing fees, and staff training requirements associated with complex imaging systems.

Shortage of Trained Ophthalmic Technicians in LMICs

Many rural centers lack staff who can capture high-quality images or maintain equipment. Training gaps lead to underused cameras and inconsistent screening outcomes. Training infrastructure remains underdeveloped in many regions, with limited access to certification programs and continuing education opportunities for ophthalmic technicians. This human resource constraint often renders sophisticated fundus cameras underutilized or improperly operated, reducing their clinical effectiveness and return on investment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Non-Mydriatic Systems Drive Workflow Efficiency

Non-mydriatic systems secured 47.62% share of the fundus camera market in 2025 thanks to painless, drop-free imaging that accelerates patient throughput. Their seamless EHR integration enables instant upload for AI review, supporting large screening programs. Zeiss’s CIRRUS 6000 adds network-grade cybersecurity and the largest OCT reference database in the United States. Hybrid and wide-field devices are slated to expand at a 6.32% CAGR, capturing up to 200 degrees of retina in a single shot and doubling lesion detection rates.

Demand for ultra-widefield cameras grows in diabetic and peripheral-retinal disease management. Mydriatic cameras remain essential when maximum image clarity or research-grade color depth is required. Pediatric-specific cameras fill niche needs with tailored optics. The product palette thus enables providers to match imaging depth with clinical complexity while balancing capital budgets.

By Modality: Portable Solutions Transform Access Paradigms

Hand-held devices held 53.10% of the fundus camera market share in 2025 as portability opened doors to rural clinics, emergency rooms and drive-through screenings. Smartphone-coupled models achieve comparable accuracy with lower acquisition cost. Combination platforms that merge OCT and fundus imaging will grow at a 7.02% CAGR, responding to clinics that want comprehensive data in one sitting.

Stationary table-top cameras remain common in high-volume centers that prioritize image consistency over mobility. Portable OCT units such as SightSync extend point-of-care diagnostics to community programs. User-friendly designs reduce technician training needs, supporting wider deployment across general-practice offices.

By Application: Diabetic-Retinopathy Screening Anchors Market Growth

Diabetic-retinopathy screening generated 32.55% of 2025 revenue and maintains momentum as guidelines prescribe annual exams and AI tools verify lesions with ≥ 96% sensitivity. Age-related macular degeneration imaging is the fastest-growing application at an 8.28% CAGR, propelled by earlier diagnosis through drusen-detection algorithms. Glaucoma screening benefits from optic-nerve analytics with 93.26% sensitivity, while retinopathy of prematurity programs rely on pediatric optics.

Retinopathy of prematurity screening utilizes specialized pediatric fundus cameras and smartphone-based systems to address critical gaps in neonatal eye care, particularly in low- and middle-income countries where ROP incidence can exceed 40% among screened infants.

By End User: Specialty Clinics Accelerate Adoption Rates

Hospitals commanded 52.10% of fundus camera market size in 2025, pairing high patient throughput with capital budgets for multimodal platforms. Specialty eye clinics are set to grow at 8.88% CAGR as they deploy AI-driven models that streamline routine screening and free ophthalmologists for complex cases. Ambulatory surgery centers add imaging to pre- and post-operative workflows, capturing ancillary revenue.

Tele-ophthalmology programs use hand-held cameras in community vans, pharmacies and primary-care offices. Automated image-grading software lowers reliance on scarce retinal specialists, supporting economic sustainability for remote services.

Geography Analysis

North America maintains market leadership with 41.20% share in 2025, supported by robust healthcare infrastructure, favorable reimbursement policies, and early adoption of AI-enabled diagnostic systems. The region benefits from comprehensive diabetic retinopathy screening programs and established telemedicine frameworks that facilitate fundus camera integration across diverse clinical settings. Major healthcare systems invest in advanced combination platforms that provide multimodal imaging capabilities, while rural areas increasingly adopt portable solutions to address geographic access barriers.

Asia-Pacific demonstrates the highest growth trajectory at 6.55% CAGR through 2031, driven by expanding healthcare access initiatives, rising diabetes prevalence, and government-backed screening programs across China, India, and Southeast Asian countries. The region's growth reflects substantial investments in healthcare infrastructure and increasing recognition of preventive eye care's economic benefits. Rural community-based eye care models emphasize portable fundus cameras and smartphone-based imaging solutions to overcome geographic and economic barriers that traditionally limited specialist access. Europe maintains steady growth supported by ESG-driven procurement policies that favor energy-efficient handheld devices and comprehensive regulatory frameworks that ensure device quality and safety standards.

Competitive Landscape

The fundus camera industry is moderately fragmented. Canon, Carl Zeiss Meditec and Topcon leverage optical heritage and global sales channels. Consolidation is advancing: EssilorLuxottica bought 80% of Heidelberg Engineering in 2024 to integrate imaging with spectacle-lens sales.

Technology partnerships drive differentiation. Optos, Nikon and Google co-created an AI algorithm that flags diabetic macular edema on ultra-widefield images at 96% sensitivity. Start-ups target new domains such as cardiovascular screening; Heart Eye Diagnostics positions its Dr.Noon CVD camera for cardiology and primary care. Success now hinges on delivering integrated hardware-software ecosystems that raise diagnostic accuracy while reducing exam time.

Fundus Camera Industry Leaders

NIDEK Co., Ltd.

Epipole Ltd.

Canon Inc.

Carl Zeiss Meditec AG

Topcon Healthcare

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Canon Healthcare USA acquired a building in Cleveland's Innovation District to establish its U.S. headquarters and comprehensive imaging resource center, aimed at accelerating medical imaging innovation including advanced fundus camera technologies. The facility will support development of next-generation imaging solutions and foster collaboration with Cleveland Clinic and other medical institutions.

- March 2025: Topcon Corporation announced a management buyout, potentially reshaping the company's strategic focus and market positioning in ophthalmic imaging solutions including fundus cameras and multimodal diagnostic platforms.

- March 2025: iCare received U.S. FDA clearance for the new iCare MAIA microperimeter, featuring renewed hardware platform, fully automated operations, and 15-inch multi-touch display with 60-degree field of view and TrueColor confocal technology.

- October 2024: EssilorLuxottica completed acquisition of an 80% stake in Heidelberg Engineering, enhancing image processing and analytics capabilities for eye care while integrating AI into the HEYEX healthcare IT platform. The transaction received clearance from competition authorities and maintains Heidelberg's brand identity.

Global Fundus Camera Market Report Scope

As per the scope of the report, a fundus camera, also known as a retinal camera, is referred to as a specialized low-power microscope with an attached camera. Its optical design is established on the indirect ophthalmoscope. They provide an objective photographic profile of any condition in the fundus. The device is also used to take photographs of the anterior segment of the eye.

The fundus camera market is segmented by product type (mydriatic fundus cameras, nonmydriatic fundus cameras, hybrid fundus cameras, and others), end user (hospitals, specialty clinics, and others), and geography (North America, Europe, Asia-Pacific, Middle East, and Africa, and South America). The report also covers the estimated market sizes and trends for 17 countries across major regions globally.

The report offers the value (in USD) for the above segments.

| Mydriatic Fundus Cameras |

| Non-mydriatic Fundus Cameras |

| Hybrid / Wide-field Fundus Cameras |

| Other Product Types |

| Hand-held Devices |

| Table-top / Stationary Systems |

| Combination Imaging Platforms |

| Diabetic Retinopathy |

| Glaucoma |

| Age-related Macular Degeneration |

| Retinopathy of Prematurity |

| Other Indications |

| Hospitals |

| Specialty & Eye Clinics |

| Ambulatory Surgical Centres |

| Screening & Tele-ophthalmology Programs |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Mydriatic Fundus Cameras | |

| Non-mydriatic Fundus Cameras | ||

| Hybrid / Wide-field Fundus Cameras | ||

| Other Product Types | ||

| By Modality | Hand-held Devices | |

| Table-top / Stationary Systems | ||

| Combination Imaging Platforms | ||

| By Application | Diabetic Retinopathy | |

| Glaucoma | ||

| Age-related Macular Degeneration | ||

| Retinopathy of Prematurity | ||

| Other Indications | ||

| By End User | Hospitals | |

| Specialty & Eye Clinics | ||

| Ambulatory Surgical Centres | ||

| Screening & Tele-ophthalmology Programs | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the fundus camera market?

The fundus camera market stands at USD 512.54 million in 2026 and is projected to reach USD 662.18 million by 2031 at a 5.25% CAGR.

Which fundus-camera product segment leads in revenue?

Non-mydriatic systems lead with 47.62% market share, favored for drop-free imaging and EHR integration.

Why is Asia-Pacific the fastest-growing region?

Rising diabetes prevalence, government screening programs and portable-camera deployments fuel a 6.55% CAGR in Asia-Pacific.

How is artificial intelligence changing fundus-camera use?

FDA-cleared AI platforms provide ≥ 96% sensitivity, deliver three-minute results and reduce reliance on specialist graders, accelerating adoption.

What restrains wider uptake of advanced combination cameras?

High capital cost often exceeding USD 100,000 plus maintenance fees delay purchases by smaller practices.

Which companies recently expanded in fundus-camera technology?

Canon opened a U.S. imaging center, Topcon restructured ownership, and EssilorLuxottica acquired Heidelberg Engineering to deepen AI capabilities.

Page last updated on: