Photoacoustic Imaging Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

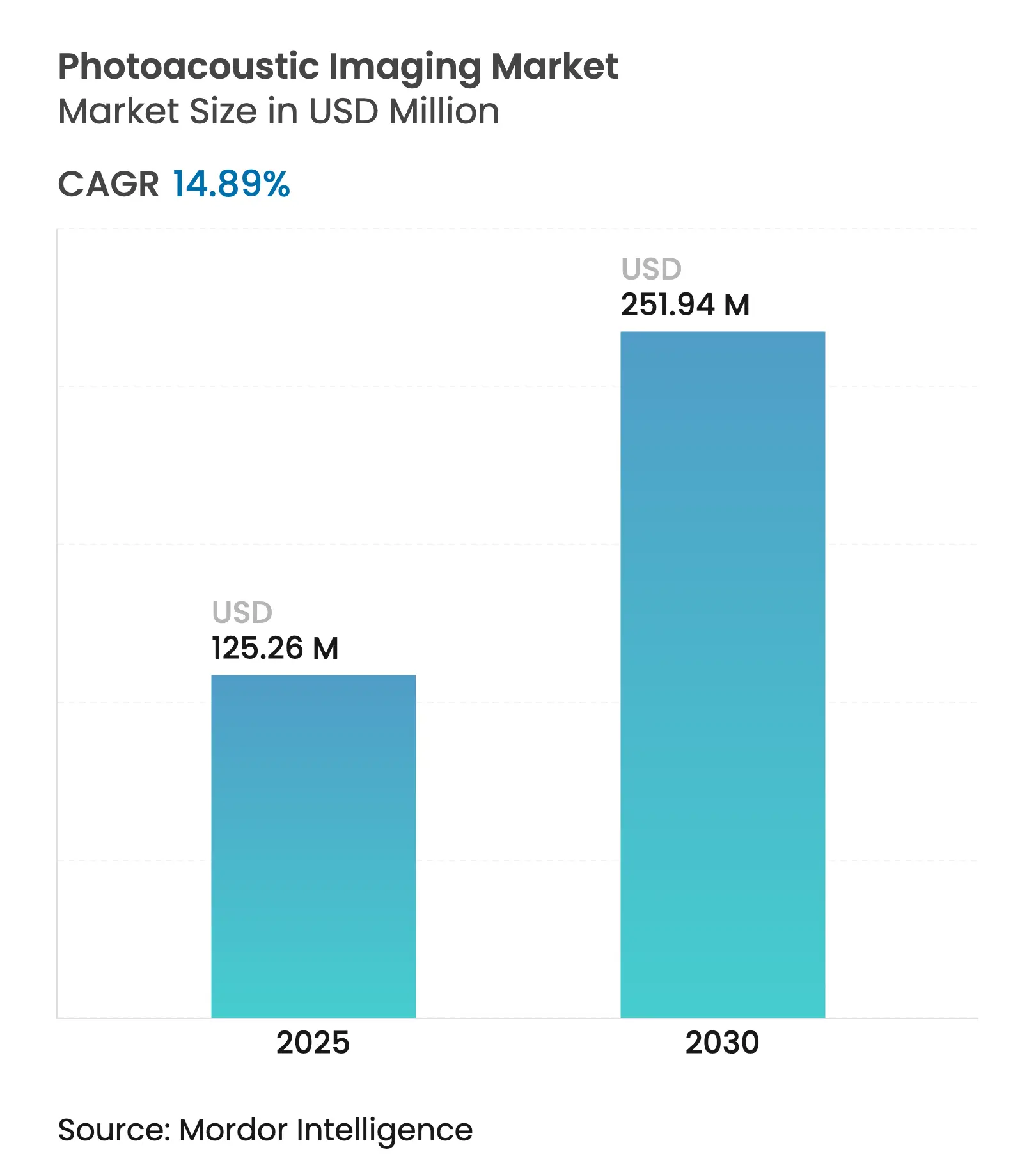

| Market Size (2025) | USD 125.26 Million |

| Market Size (2030) | USD 251.94 Million |

| Growth Rate (2025 - 2030) | 14.89 % CAGR |

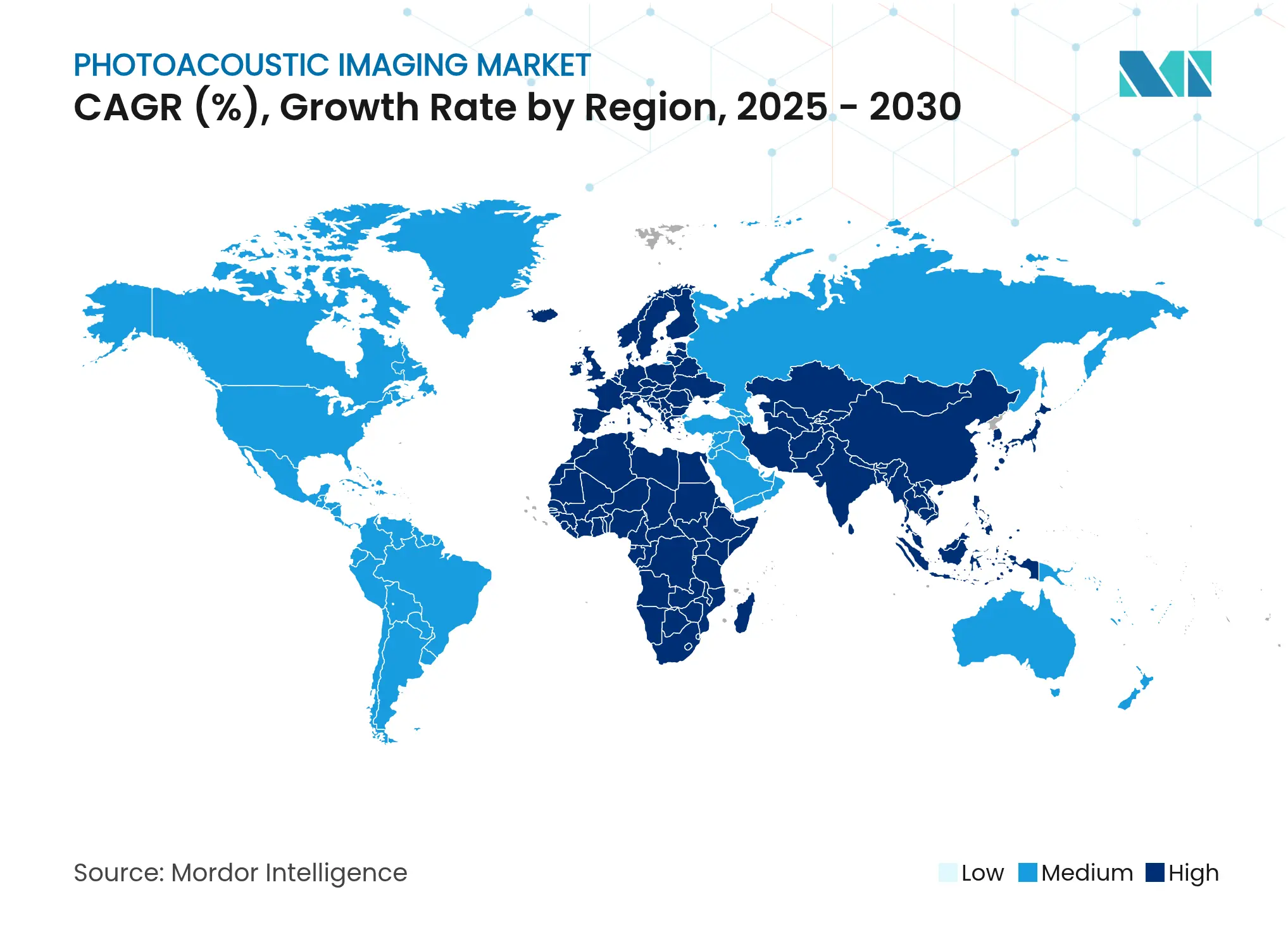

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

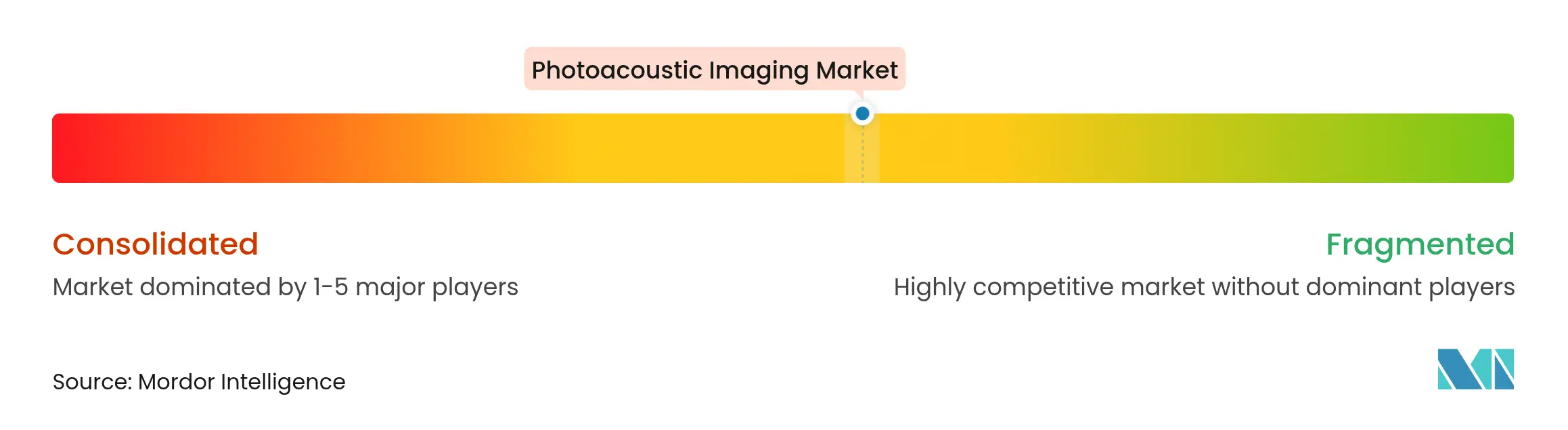

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Photoacoustic Imaging Market Analysis by Mordor Intelligence

The technology’s fusion of optical and ultrasound physics delivers high-resolution, real-time insight into tissue oxygenation, perfusion and molecular composition, making it attractive for oncology, cardiology and neurology diagnostics. Regulatory clarity from the FDA on artificial-intelligence-enabled devices encourages commercial roll-outs, while cost-down innovations in lasers and data-acquisition modules reduce ownership barriers. Breakthroughs such as Caltech’s photoacoustic computed-tomography breast system illustrate clinical validity and the potential to lower radiation exposure for patients. Adoption momentum is especially strong in Asia-Pacific where rising chronic-disease prevalence amplifies the need for cost-effective, high-accuracy imaging solutions.

Key Report Takeaways

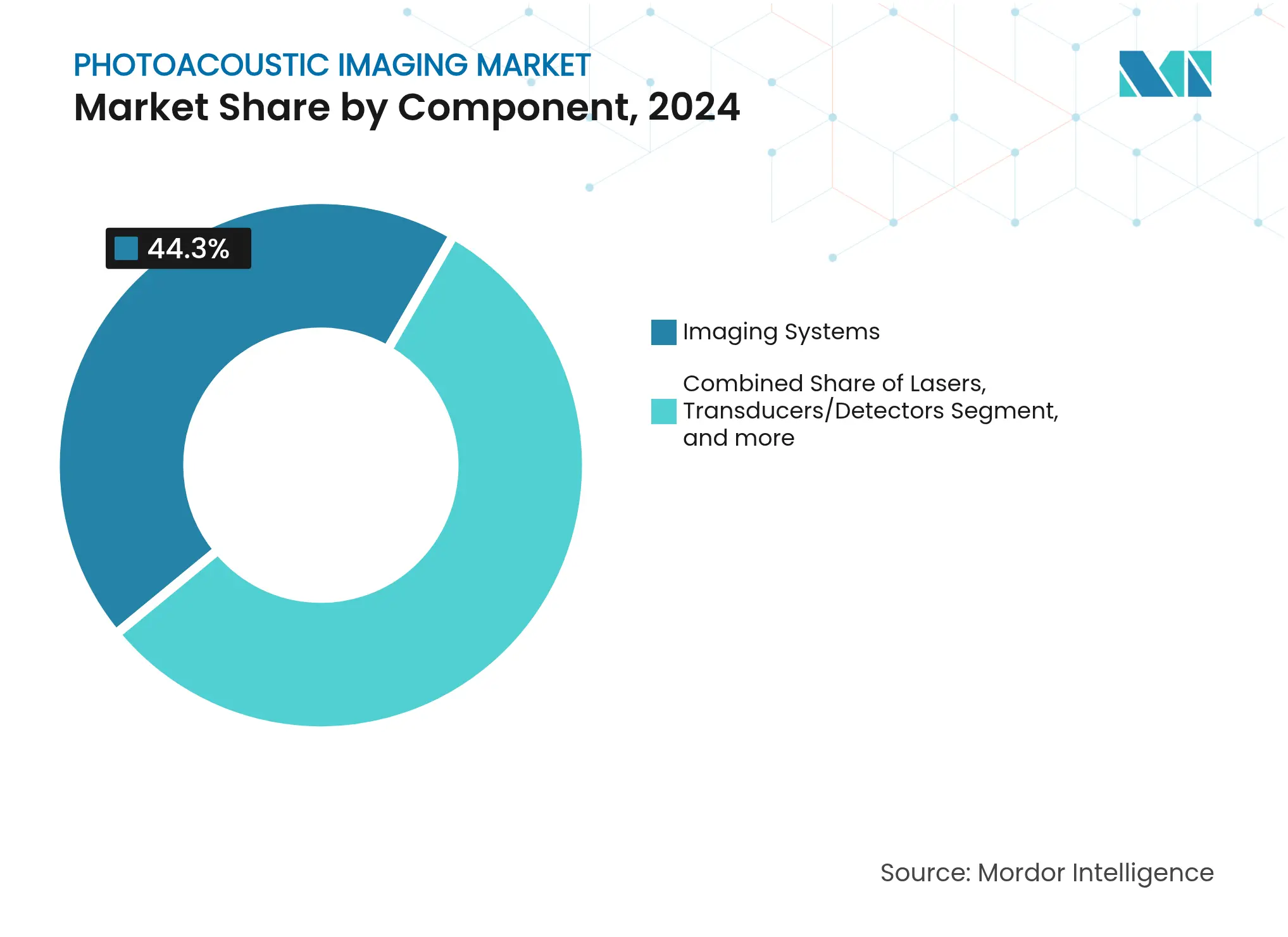

- By component, imaging systems led with 44.27% of photoacoustic imaging market share in 2024; contrast agents are projected to expand at a 15.13% CAGR through 2030.

- By imaging modality, photoacoustic tomography captured 55.64% of revenue in 2024, while optoacoustic mesoscopy is forecast to grow at a 20.03% CAGR to 2030.

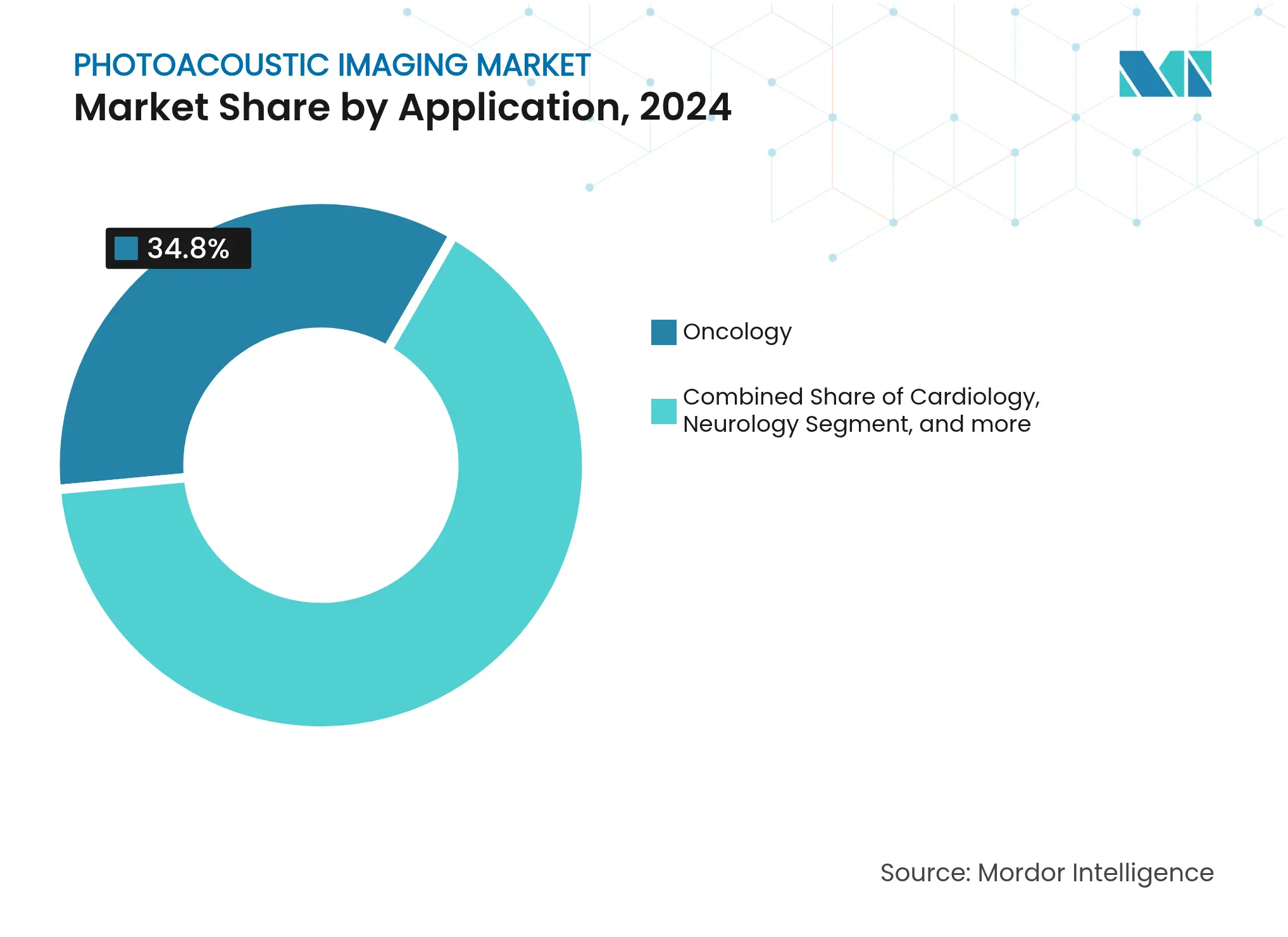

- By application, oncology accounted for 34.82% of the photoacoustic imaging market size in 2024; neurology is expected to record a 20.62% CAGR over 2025-2030.

- By end user, hospitals held 39.12% revenue in 2024; pharmaceutical and biotechnology companies are advancing at a 16.33% CAGR as they embed the technology in drug-discovery workflows.

- By geography, North America accounted for 38.74% of the photoacoustic imaging market size in 2024; neurology is expected to record a 18.54% CAGR over 2025-2030.

Global Photoacoustic Imaging Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising

Prevalence of Cancer & Cardiovascular Diseases

Rising

Prevalence of Cancer & Cardiovascular Diseases

| +3.2% | Global, with highest impact in North America & Europe | Long term (≥ 4 years) |

(~) %

Impact on CAGR Forecast

:

+3.2%

|

Geographic

Relevance

:

Global, with

highest impact in North America & Europe

|

Impact

Timeline

:

Long term (≥

4 years)

|

Growing

Adoption in Pre-Clinical Drug Discovery & Toxicology

Growing

Adoption in Pre-Clinical Drug Discovery & Toxicology

| +2.8% | North America & EU core, spill-over to APAC | Medium term (2-4 years) | |||

Advancements

In Hybrid PAI-Ultrasound Platforms

Advancements

In Hybrid PAI-Ultrasound Platforms

| +2.1% | Global, early adoption in developed markets | Medium term (2-4 years) | |||

Regulatory

Approvals for Handheld Vascular PAI Devices

Regulatory

Approvals for Handheld Vascular PAI Devices

| +1.9% | North America & EU, expanding to APAC | Short term (≤ 2 years) | |||

AI-Enabled

Real-Time Multispectral Guidance in Surgery

AI-Enabled

Real-Time Multispectral Guidance in Surgery

| +1.7% | North America & EU, selective APAC markets | Medium term (2-4 years) | |||

Cost-Down

Innovations in Lasers & DAQ Modules

Cost-Down

Innovations in Lasers & DAQ Modules

| +1.4% | Global, with accelerated adoption in emerging markets | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Rising Prevalence of Cancer & Cardiovascular Diseases

Escalating cancer and heart-disease burdens reshape diagnostic priorities, and clinicians increasingly require modalities able to visualize angiogenesis and tissue hypoxia in vivo. Photoacoustic imaging delivers label-free haemoglobin-contrast pictures without ionizing radiation, allowing earlier lesion detection and longitudinal follow-up. The method’s real-time blood-oxygen mapping supports precision-medicine strategies that correlate oxygen deficits with therapeutic resistance. Growing survivor populations necessitate repeat imaging; the non-invasive nature of the modality limits cumulative-dose concerns while preserving image fidelity. Hospitals adopt the technology to enhance tumour-board decision making and to improve cardiovascular-risk stratification workflows.[1]American Cancer Society, “Cancer Facts & Figures 2024,” cancer.org

Growing Adoption in Pre-Clinical Drug Discovery & Toxicology

Pharmaceutical pipelines integrate photoacoustic platforms to monitor drug-distribution kinetics, vascular remodelling and tissue-oxygen shifts in small-animal models. FDA initiatives that prioritise predictive toxicology encourage deployment of imaging biomarkers that flag off-target effects earlier than histology alone. Longitudinal, radiation-free imaging reduces animal numbers and study duration, supporting Phase 0 microdosing protocols. The addition of AI-driven segmentation shortens analysis times, enabling high-throughput screens that align with compressed discovery timelines. Resulting productivity gains strengthen the business case for widespread laboratory adoption.[2]Royal Society of Chemistry, “Predictive Toxicology Frameworks,” pubs.rsc.org

Advancements in Hybrid PAI-Ultrasound Platforms

Integrated systems co-register structural ultrasound with functional photoacoustic signals, offering clinicians depth penetration beyond optical limits while maintaining microvascular detail. Transparent transducers with 80% optical throughput now deliver 63% bandwidth, eliminating the classic trade-off between acoustic sensitivity and optical access. Hybrid scanners reach depths beyond 15 mm at sub-50 µm resolution, reducing procedure count and cutting operator learning curves. Hospitals view the “single-console” approach as capital-efficient because it leverages existing ultrasound skills. This convergence accelerates inclusion in perioperative and point-of-injury settings, broadening the addressable photoacoustic imaging market.[3]Nature Communications, “Transparent Ultrasound Transducer Enables Optical Access,” nature.com

Regulatory Approvals for Handheld Vascular PAI Devices

The FDA’s streamlined pathway for handheld units shortens market-entry timelines and spurs engineering towards portable, point-of-care formats. Approved devices demonstrate 79% sensitivity and 84% specificity for large-vessel-occlusion stroke triage, surpassing traditional prehospital scales. Lightweight probes weighing 40 g enable bedside cerebral blood-flow checks and home monitoring programmes. Clearer thermal-safety guidance reassures users and procurement teams, supporting adoption in emergency departments, ambulances and rural clinics. These handheld solutions underpin a shift from hospital-centric imaging to distributed care networks.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High Capital

Cost & Limited Reimbursement

High Capital

Cost & Limited Reimbursement

| -2.7% | Global, most severe in emerging markets | Long term (≥ 4 years) |

(~) %

Impact on CAGR Forecast

:

-2.7%

|

Geographic

Relevance

:

Global, most

severe in emerging markets

|

Impact

Timeline

:

Long term (≥

4 years)

|

Shortage of

Trained PAI Specialists

Shortage of

Trained PAI Specialists

| -1.8% | Global, acute in rural and developing regions | Medium term (2-4 years) | |||

Lack of

Standardized QA Protocols & Benchmarks

Lack of

Standardized QA Protocols & Benchmarks

| -1.5% | Global, with regulatory focus in North America & EU | Medium term (2-4 years) | |||

Budget

Cannibalization by Competing Hybrid Modalities

Budget

Cannibalization by Competing Hybrid Modalities

| -1.2% | North America & EU, selective APAC markets | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

High Capital Cost & Limited Reimbursement

Advanced systems still list above USD 500,000, and payors have yet to create dedicated procedural codes, forcing hospitals to absorb costs or seek research grants. Unbundling of high-priced radiopharmaceuticals signals reimbursement evolution but omits photoacoustic procedures. Value-based payment models magnify scrutiny on capital outlays because devices complement rather than replace existing scanners. Economic analyses show potential per-patient savings in cardiac use cases, yet finance committees often prioritise modalities with recognised reimbursement. Entry-level LED platforms should ease acquisition hurdles, but scale manufacturing is required to translate savings fully .

Shortage of Trained PAI Specialists

Radiology-workforce shortages leave 1,400 U.S. positions unfilled, and very few residency curricula cover photoacoustic interpretation. Medicare caps on training slots add further constraints, while recent allocations focused on primary-care disciplines. Academic centres run short courses, but community hospitals—the settings that could benefit most—lack access. The American Board of Radiology’s alternate-pathway update opens doors for internationally trained radiologists, yet visa and licensing complexities delay relief. AI-assisted reading software promises throughput gains but awaits regulatory validation.

Segment Analysis

By Component: Systems Drive Hardware Innovation

Imaging systems generated 44.27% of 2024 revenue, underscoring their role as turnkey platforms that integrate lasers, transducers, and real-time processors in a single workflow. Many providers view the systems’ modular architecture as insurance against obsolescence because firmware upgrades deliver new imaging sequences without further hardware spend. Contrast-agent sales rise at a 15.13% CAGR as nanoparticle formulations improve target specificity and biocompatibility, supporting functional tumour imaging and vascular mapping. LED-powered configurations that match signal levels once limited to costly solid-state lasers broaden the photoacoustic imaging market in ambulatory centres and emerging economies.

Software and accessory revenue grow steadily thanks to AI pipelines that automate reconstruction, segmentation, and quantitative analytics. Data-acquisition vendors now ship 128-channel digitizers with 46.1 dB SNR, driving down per-scan costs. These hardware and software advances collectively lower the total cost of ownership, a prerequisite for accelerating the photoacoustic imaging industry’s transition from research to routine care. Widespread component interoperability also stimulates third-party innovation as niche suppliers create probes tailored to dermatology, endocrinology, and ophthalmology.

Note: Segment shares of all individual segments available upon report purchase

By Imaging Modality: Tomography Leads Clinical Translation

Photoacoustic tomography commanded 55.64% market share in 2024 by delivering volumetric data at depths beyond 15 mm and resolutions near 40 µm, attributes vital for breast and vascular imaging. The modality’s compatibility with existing ultrasound ergonomics simplifies staff training and accelerates departmental uptake inside large hospitals. Optoacoustic mesoscopy, advancing at a 20.03% CAGR, bridges microscopic and macroscopic scales, allowing clinicians to visualise cellular detail within tissue context and thereby expand the photoacoustic imaging market into dermatologic oncology and rheumatoid-arthritis assessments.

Microscopy retains importance in preclinical studies where single-cell resolution guides drug-target validation, while endoscopy supports minimally invasive procedures including gastrointestinal bleeding localisation. Hybrid tomography–ultrasound scanners offer quasi-simultaneous anatomical and haemodynamic images, reducing total exam time. Recent transcranial demonstrations that compensate for skull-induced aberration extend the technique to neurology, a leap that could unlock stroke and epilepsy monitoring markets. Machine-learning artefact suppression continues to enhance image quality, reinforcing tomography’s leadership in clinical workflows.

By Application: Oncology Dominance Faces Neurology Challenge

Oncology contributed 34.82% of 2024 revenue, reflecting entrenched demand for label-free angiogenesis mapping and hypoxia assessment during radiation-therapy planning. Real-time visualisation of microvascular remodelling provides oncologists with early biomarkers of treatment response, limiting unnecessary exposure to ineffective regimens and reducing repeat biopsies. Neurology is the fastest-rising segment with a 20.62% CAGR, buoyed by handheld cerebral perfusion scanners that detect large-vessel occlusions within the critical therapeutic window. Demonstrations of continuous intracranial haemodynamic monitoring are persuading stroke centres to invest, thereby enlarging the photoacoustic imaging market.

Cardiology employs the technique for plaque characterisation and myocardial oxygenation mapping, while peripheral vascular clinicians exploit imaging depths that outperform optical coherence tomography. Dermatology leverages sub-50 µm resolution to discern pigmented-lesion architecture, assisting melanoma staging without excisional biopsy. Functional photoacoustic Doppler angiography now images blood flow up to 1 cm deep, addressing diseases once deemed beyond optical modalities. As precision medicine spreads, demand for quantitative functional biomarkers will further elevate the photoacoustic imaging industry's relevance.

Note: Segment shares of all individual segments available upon report purchase

By End User: Pharma Adoption Accelerates Discovery

Hospitals captured 39.12% of 2024 spending, benefiting from infrastructure, skilled staff and reimbursement familiarity that smooth capital-equipment justification. Large academic centres use multi-modal suites to support translational trials, adding credibility that influences downstream community-hospital purchasing committees. Pharmaceutical and biotechnology companies, expanding at 16.33% CAGR, integrate scanners into toxicology and efficacy pipelines. Longitudinal small-animal imaging reduces drug-candidate attrition, while human Phase I trials deploy non-ionising perfusion markers to de-risk safety profiles—developments that increase the photoacoustic imaging market size for contract-research organisations.

Diagnostic-imaging centres and outpatient clinics see steady growth as portable systems, weighing less than 10 kg, require minimal installation. Academic institutions remain innovation hubs, publishing protocols that extend the modality into endocrinology and maternal-fetal medicine. Vendors eye consumer-health niches, prototyping wearables for ankle-brachial blood-index tracking and skin-health monitoring, hinting at an eventual shift toward distributed, preventive-health ecosystems.

Geography Analysis

North America generated 38.74% of 2024 revenue, leveraging progressive FDA guidance, mature reimbursement frameworks and concentrated R&D spending. Clinical-trial networks expedite evidence generation, while sizeable venture-capital flows help start-ups pilot disruptive portable devices. Canada follows with public-health investments in indigenous and remote-care diagnostics; Mexico’s private hospitals adopt scalable LED platforms for diabetic-foot monitoring, diversifying the regional photoacoustic imaging market.

Asia-Pacific is the fastest-expanding geography at an 18.54% CAGR to 2030 owing to rising chronic-disease prevalence, hospital-modernisation drives and supportive industrial policies. China anchors demand through large-scale public-hospital upgrades and domestic manufacturing incentives that localise system production. Japan’s super-aged demographics fuel cardiovascular and oncologic imaging volumes, while South Korea capitalises on semiconductor expertise to supply lasers and detectors. India and ASEAN states adopt low-cost, AI-enabled scanners for primary-care centres, broadening access to high-resolution functional imaging.

Europe exhibits stable yet material growth as national health systems emphasise evidence-backed adoption. Germany’s innovation clusters host multi-centre trials that demonstrate patient-outcome improvements, facilitating procurement approvals. The United Kingdom forms public-private consortia to explore portable stroke-monitoring units for ambulance deployment. France channels Bpifrance funds toward start-ups refining intraoperative guidance probes. Eastern-European nations show emergent demand, but budget constraints channel purchases toward refurbished or LED-based configurations. Across the continent, partnerships with academic hospitals strengthen competitive positioning for domestic and international manufacturers.

Competitive Landscape

Market Concentration

The photoacoustic market is semi consolidated due to the presence of several companies operating globally as well as regionally. The competitive landscape includes analyzing a few international and local companies that hold market shares and are well known. Some of the key market players include illumiSonics Inc., Seno Medical, InnoLas Laser GmbH, Fujifilm Holdings Corporation (Fujifilm Visualsonics, Inc.), Kibero, and iThera Medical GmbH, among others.

Photoacoustic Imaging Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: FUJIFILM VisualSonics Inc. has officially launched the Vevo F2 LAZR-X20 Photoacoustic Imaging Platform, a cutting-edge multi-modal system designed for preclinical tissue characterization. Featuring high-powered, intelligent laser technology, the LAZR-X20 offers exceptional anatomical accuracy and imaging precision—reinforcing FUJIFILM’s leadership in ultra-high frequency ultrasound and photoacoustics.

- June 2025: Verasonics, Inc., a global prominent player in research ultrasound, has announced a partnership with PhotoSound Technologies, Inc. to integrate the PhotoSound Legion AMP128 amplifier into its Vantage and Vantage NXT Ultrasound Systems. This collaboration expands capabilities in photoacoustic imaging, thermoacoustic imaging, and radiation therapy monitoring, giving researchers a more flexible and powerful platform for advanced applications.

- September 2024: University College London (UCL) researchers have developed a handheld scanner capable of generating 3D photoacoustic images in seconds, using photoacoustic tomography (PAT). Published in Nature Biomedical Engineering, this breakthrough promises early diagnosis of cancer, cardiovascular disease, and arthritis by delivering high-resolution, real-time imaging of blood vessels—a transformative step for clinical care.

Table of Contents for Photoacoustic Imaging Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Rising Prevalence of Cancer & Cardiovascular Diseases

- 4.2.2Growing Adoption in Pre-Clinical Drug Discovery & Toxicology

- 4.2.3Advancements In Hybrid PAI-Ultrasound Platforms

- 4.2.4Regulatory Approvals for Handheld Vascular Pai Devices

- 4.2.5AI-Enabled Real-Time Multispectral Guidance in Surgery

- 4.2.6Cost-Down Innovations in Lasers & DAQ Modules

- 4.3Market Restraints

- 4.3.1High Capital Cost & Limited Reimbursement

- 4.3.2Shortage of Trained PAI Specialists

- 4.3.3Lack of Standardized QA Protocols & Benchmarks

- 4.3.4Budget Cannibalization by Competing Hybrid Modalities

- 4.4Technological Outlook

- 4.5Porter’s Five Forces Analysis

- 4.5.1Threat of New Entrants

- 4.5.2Bargaining Power of Buyers

- 4.5.3Bargaining Power of Suppliers

- 4.5.4Threat of Substitutes

- 4.5.5Competitive Rivalry

5. Market Size & Growth Forecasts (Value in USD)

- 5.1By Component

- 5.1.1Imaging Systems

- 5.1.2Lasers

- 5.1.3Transducers/Detectors

- 5.1.4Contrast Agents

- 5.1.5Software & Accessories

- 5.1.6Others

- 5.2By Imaging Modality

- 5.2.1Photoacoustic Tomography (PAT)

- 5.2.2Photoacoustic Microscopy (PAM)

- 5.2.3Photoacoustic Endoscopy (PAE)

- 5.2.4Optoacoustic Mesoscopy (OAM)

- 5.2.5Hybrid PAI-Ultrasound Systems

- 5.2.6Others

- 5.3By Application

- 5.3.1Oncology

- 5.3.2Cardiology

- 5.3.3Neurology

- 5.3.4Hematology

- 5.3.5Peripheral Vascular Disease

- 5.3.6Dermatology

- 5.3.7Other Applications

- 5.4By End User

- 5.4.1Hospitals

- 5.4.2Diagnostic Imaging Centers & Out-patient Clinics

- 5.4.3Academic & Research Institutes

- 5.4.4Pharmaceutical & Biotechnology Companies

- 5.5By Geography

- 5.5.1North America

- 5.5.1.1United States

- 5.5.1.2Canada

- 5.5.1.3Mexico

- 5.5.2Europe

- 5.5.2.1Germany

- 5.5.2.2United Kingdom

- 5.5.2.3France

- 5.5.2.4Italy

- 5.5.2.5Spain

- 5.5.2.6Rest of Europe

- 5.5.3Asia-Pacific

- 5.5.3.1China

- 5.5.3.2Japan

- 5.5.3.3India

- 5.5.3.4Australia

- 5.5.3.5South Korea

- 5.5.3.6Rest of Asia-Pacific

- 5.5.4Middle East & Africa

- 5.5.4.1GCC

- 5.5.4.2South Africa

- 5.5.4.3Rest of Middle East & Africa

- 5.5.5South America

- 5.5.5.1Brazil

- 5.5.5.2Argentina

- 5.5.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1FUJIFILM Holdings Corp. (VisualSonics)

- 6.3.2iThera Medical GmbH

- 6.3.3Seno Medical Instruments Inc.

- 6.3.4ENDRA Life Sciences Inc.

- 6.3.5TomoWave Laboratories Inc.

- 6.3.6Luxonus Inc.

- 6.3.7illumiSonics Inc.

- 6.3.8Advantest Corp.

- 6.3.9InnoLas Laser GmbH

- 6.3.10Kibero GmbH

- 6.3.11Aspectus GmbH

- 6.3.12PhotoSound Technologies Inc.

- 6.3.13VibroniX Inc.

- 6.3.14Optoacoustics Ltd.

- 6.3.15OPOTEK LLC

- 6.3.16Canon Inc. (Medical Systems)

- 6.3.17GE HealthCare (Strategic Partner)

- 6.3.18Philips Healthcare

- 6.3.19Siemens Healthineers

- 6.3.20Hitachi Medical Systems

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-need Assessment

Global Photoacoustic Imaging Market Report Scope

As per the report's scope, photoacoustic imaging (PAI) is a non-invasive biomedical imaging procedure that generates ultrasonic waves by irradiating the material with a pulsed laser and reconstructs the image of light energy absorption distribution in the tissue. The Photoacoustic Imaging Market is segmented by type (imaging systems, lasers, and others), product type (photoacoustic tomography and photoacoustic microscopy), application (oncology, cardiology, hematology, and other applications), end-user (hospitals, diagnostic centers, and academic and research institutes), and Geography (North America, Europe, Asia-Pacific, and rest of the world). The report offers the value (in USD) for the above segments.