Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

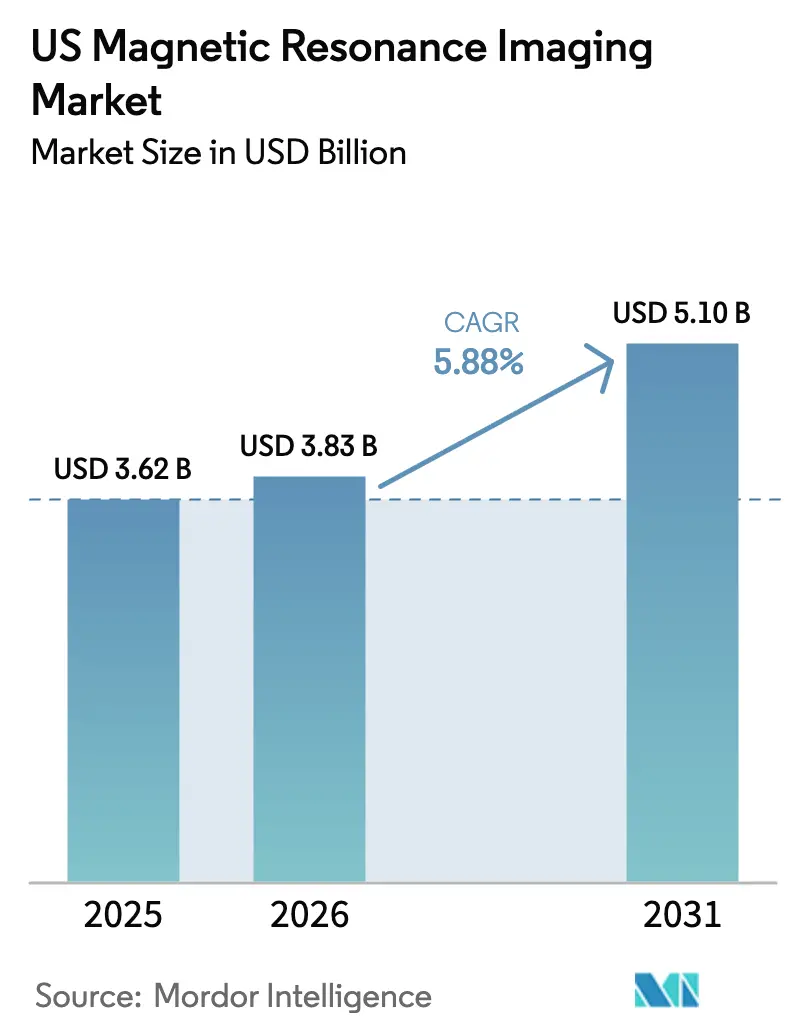

| Base Year Market Size (2025) | USD 3.62 Billion |

| Market Size (2026) | USD 3.83 Billion |

| Market Size (2031) | USD 5.1 Billion |

| Growth Rate (2026 - 2031) | 5.88% CAGR |

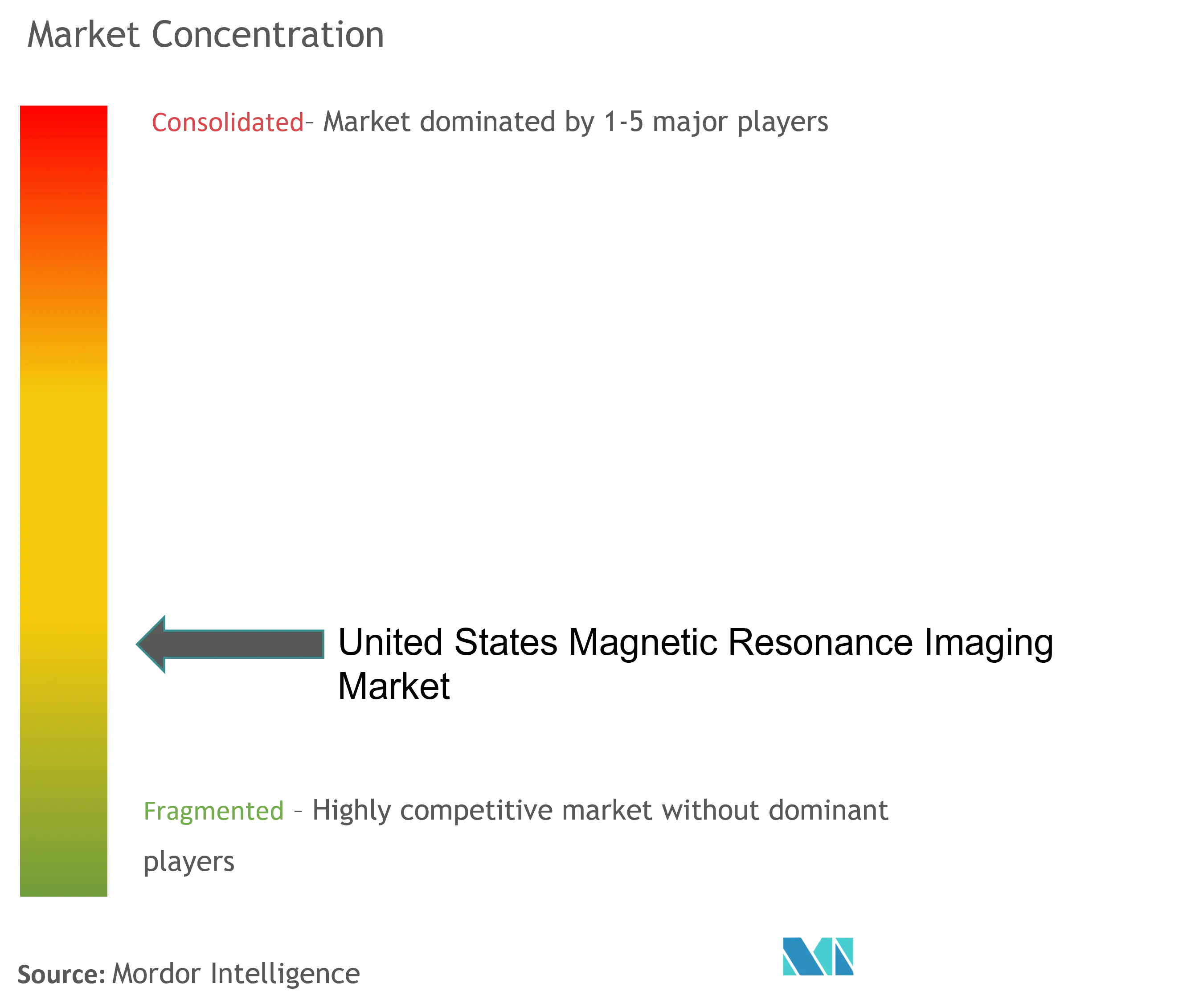

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

US Magnetic Resonance Imaging Market Analysis by Mordor Intelligence

US MRI market size in 2026 is estimated at USD 3.83 billion, growing from 2025 value of USD 3.62 billion with 2031 projections showing USD 5.1 billion, growing at 5.88% CAGR over 2026-2031. Demographic aging, the broad rise of chronic diseases, and continuous modernization of both hospital and outpatient imaging infrastructure collectively sustain demand. Closed‐bore systems remain the clinical workhorse, yet portable and ultra‐low‐field platforms gain ground as providers seek flexibility and lower capital outlays. Reimbursement policy gradually becomes more supportive because Medicare Advantage enrollment growth balances fee-for-service pressure. Artificial intelligence reduces scan times and improves image quality, which allows providers to boost scanner throughput without additional magnets. Competitive differentiation now centers on workflow software, helium-free magnets, and service partnerships that guarantee uptime.

Key Report Takeaways

- By architecture, closed systems led with 77.62% of US MRI market share in 2025, while portable units are projected to post a 6.31% CAGR through 2031.

- By field strength, the mid-field 1.5 T category held 47.62% of the US MRI market share in 2025; ultra-high-field platforms are advancing at a 5.98% CAGR to 2031.

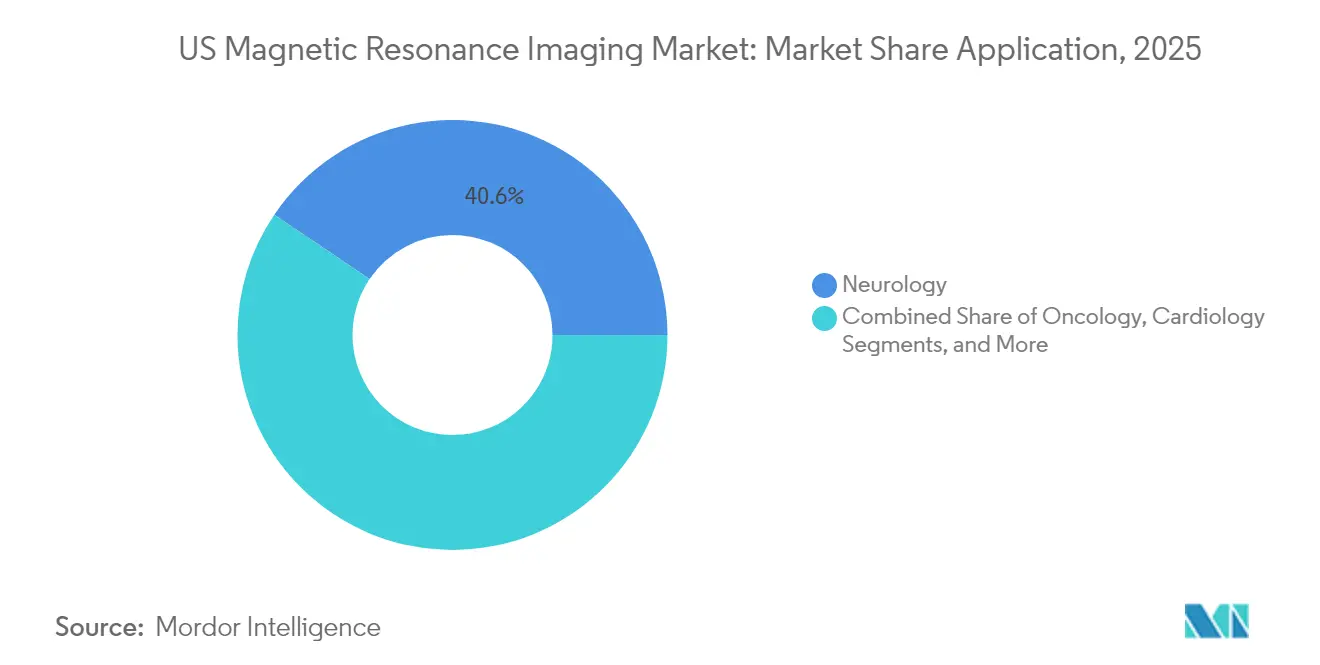

- By application, neurology accounted for a 40.55% share of the US MRI market size in 2025; oncology imaging is set to widen fastest at a 6.86% CAGR over the forecast window.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

US Magnetic Resonance Imaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising global burden of chronic and age-related diseases | +1.5% | National, with higher concentration in aging population centers and metropolitan areas | Long term (≥ 4 years) |

| Increasing reimbursement coverage and government support for high-value imaging modalities | +1.0% | National, with emphasis on Medicare Advantage expansion and state Medicaid programs | Medium term (2-4 years) |

| Technological breakthroughs in MRI | +1.2% | National, with early adoption in major metropolitan areas and academic medical centers | Medium term (2-4 years) |

| Steady growth in healthcare spending and modernization of hospital & outpatient imaging infrastructure worldwide | +0.8% | National, with accelerated growth in underserved rural areas and suburban markets | Long term (≥ 4 years) |

| Expanding clinical indications for MRI | +0.6% | National, with concentration in specialty care centers and research institutions | Medium term (2-4 years) |

| Shift toward patient-centric, non-ionizing diagnostic alternatives | +0.5% | National, with higher adoption in consumer-focused healthcare markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Global Burden of Chronic and Age-Related Diseases

Seventy-six point four percent of US adults reported at least one chronic condition in 2025, a pattern that translates into sustained MRI utilization for neurological, oncological, and cardiac evaluations. Providers favor the modality’s soft-tissue contrast to diagnose Alzheimer’s, multiple sclerosis, and ischemic stroke, where early detection improves therapeutic outcomes. FDA clearance for GE HealthCare’s head-only SIGNA MAGNUS 3.0 T platform exemplifies industry response, delivering specialized neuro-imaging in shorter sessions [1]GE HealthCare, “SIGNA MAGNUS 3.0 T Neuroimaging System Receives FDA Clearance,” gehealthcare.com. The same demographic shift accelerates oncology imaging because precision medicine protocols rely on repeat, high-resolution tumor mapping. Collectively, the chronic disease burden adds a 1.8-percentage-point lift to long-term market growth.

Increasing Reimbursement Coverage and Government Support for High-Value Imaging Modalities

CMS finalized a 5.06% rate hike for Medicare Advantage plans in 2026, releasing more than USD 25 billion in extra funding that will flow into diagnostic imaging volumes [2]Centers for Medicare & Medicaid Services, “2026 Medicare Advantage Rate Announcement,” cms.gov. Administrative relief also arrived when CMS removed the lumbar-spine MRI measure from quality reporting, easing provider workflow. Commercial payers follow suit by steering patients to cost-efficient outpatient centers, which often invest in new scanners to win network contracts. These moves collectively add 1.2-percentage-points to medium-term growth while reducing historical revenue volatility tied to fee-schedule cuts.

Technological Breakthroughs in MRI

Deep-learning reconstruction shrinks scan times by roughly 30%, lifting daily scanner capacity by as much as one-third without sacrificing image quality. Philips’ SmartSpeed Precise engine doubles this benefit by pairing two AI algorithms to enhance sharpness 80% and cut exam time by a factor of three. At the opposite end of the spectrum, 0.05 T ultra-low-field prototypes plug into standard wall power and waive RF-shielding needs, trimming install cost close to 90%. Bayer’s gadoquatrane contrast agent lowers gadolinium exposure 60%, a safety gain for renally impaired patients. Collectively, technology adds 1.5 percentage-points to CAGR as hospitals adopt AI suites and helium-free magnets.

Steady Growth in Healthcare Spending and Modernization of Hospital & Outpatient Imaging Infrastructure Worldwide

Allegheny Valley Hospital invested USD 12 million to expand its radiology suite, inserting a mobile MRI to open 40 new weekly slots. Certificate-of-need reform quickens outpatient build-outs; US Radiology Specialists plans 12 freestanding centers in 2025 to extend reach into underserved communities. Vizient projects advanced outpatient imaging to climb 13% over the next decade, a shift that supports the US MRI market trajectory. GE HealthCare’s seven-year pact with Sutter Health covers 300 facilities and integrates AI triage tools, illustrating how vendors secure long-run volume through enterprise deals.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of MRI systems | -0.8% | National, with pronounced impact in rural and underserved areas, community hospitals | Long term (≥ 4 years) |

| Shortage of Certified MRI Technologists | -1.2% | National, with severe shortages in rural areas, secondary markets, and non-metropolitan regions | Short term (≤ 2 years) |

| Declining reimbursement rates for advanced imaging | -0.9% | National, with particular impact on Medicare-dependent providers and rural hospitals | Short term (≤ 2 years) |

| Safety and compatibility concerns for patients | -0.4% | National, with higher impact in facilities serving elderly populations and patients with implants | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost of MRI Systems

A high-field scanner typically costs more than USD 225,000 and demands expensive site prep that includes RF shielding and cryogenic cooling [3]IEEE, “Cost Barriers for Rural MRI Installations,” ieee.org. Rural hospitals already under fiscal strain defer such purchases, contributing to more than 100 facility closures since 2010 that removed imaging access for nearly one-fifth of rural residents. Technology is starting to blunt the barrier: ultra-low-field hardware priced near USD 22,000 eliminates helium, while Philips BlueSeal magnets save 5 million liters of helium and 40 MWh of energy per system since 2018. Even as acquisition costs erode, price remains a drag of 0.8-percentage-points on long-term growth.

Shortage of Certified MRI Technologists

Vacancy rates for radiologic technologists stood at 18.1% in 2025 compared with 6.2% three years earlier [4]Radiology Society of North America, “Radiologic Technologist Vacancy Survey 2025,” rsna.org. Staffing gaps lengthen wait times and force some departments to curtail evening or weekend schedules, limiting throughput by up to 20%. Salaries climbed to a median USD 83,740, yet training capacity lags demand. Providers respond with apprenticeship programs like US Radiology Specialists’ Technologist Advancement Academy, which graduated 19 technologists and enrolled 27 trainees in 2025. AI automation lightens repetitive positioning and protocol selection, but human oversight of patient safety and quality assurance remains non-negotiable, subtracting 1.2-percentage-points from short-term growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Architecture: Closed Systems Dominate Despite Portable Innovation

Closed units held 77.62% of the US MRI market in 2025, confirming the modality’s reliance on full-body, high-field imaging for complex neuro and oncology cases. The canonical wide-bore 70 cm format eases patient anxiety without compromising gradient performance, a mix ideal for community hospitals that require versatility. Extremity-specific magnets cater to orthopedic clinics, yet their impact on total revenue remains modest. Portable systems contribute the fastest growth at 6.31% CAGR through 2031 as emergency departments, intensive-care units, and rural sites seek point-of-care diagnostic options. Hyperfine’s FDA-cleared Swoop employs NVIDIA AI to improve brain image quality and demonstrates a mobile install footprint the size of a ventilator cart. Open magnets retain relevance for claustrophobic or bariatric patients, though their lower field strength limits nuanced neurovascular work compared with closed 1.5 T or 3 T designs.

Portable MRI’s rise intersects with value-based care goals because bedside imaging avoids costly patient transport and lowers sedation risk. Yet reimbursement codes still favor conventional rooms, so adoption concentrates within academic centers able to fund pilots. Vendors now bundle financing and AI software to convert pilot orders into fleet rollouts, a tactic reflecting broader competition on total cost of ownership rather than sticker price. Hospitals that replace aging 1.5 T scanners often opt for helium-free magnets to hedge against commodity volatility, a choice that further cements closed architecture leadership while portable units carve new revenue streams in non-traditional settings.

By Field Strength: Mid-Field Dominance with Ultra-High Growth

One-point-five-tesla scanners represented 47.62% of the US MRI market size for field strength in 2025, favored for balanced acquisition cost, maintenance, and clinically adequate signal-to-noise ratios. Community hospitals prefer 1.5 T because gradient upgrades and AI reconstruction now rival 3 T performance in many body and cardiac applications. Low-field magnets under 0.3 T stay relevant where metal implants or cost constraints preclude high-field use, but their share declines as portable high-performance options emerge. GE SIGNA Sprint pushes 1.5 T gradient power to 200 mT/m, blurring the historical performance gap with 3 T systems.

Ultra-high-field platforms above 7 T log a 5.98% CAGR through 2031, primarily within research hospitals that require micro-structural brain imaging or spectroscopy. FDA cleared 7 T for limited clinical use, and presurgical mapping for epilepsy benefits from submillimeter resolution that guides resection margins. However, siting a 7 T unit entails reinforced flooring and new power feeds, which caps volumes to top neurology centers. Very-high-field 3 T maintains an important niche in advanced musculoskeletal and prostate work, where higher signal-to-noise ratios permit multiparametric protocols without contrast. Investors weigh ultra-high-field revenue potential against utilization risk; therefore many choose 3 T upgrades combined with AI acceleration as an interim path toward precision imaging.

By Application: Neurology Leadership with Oncology Acceleration

Neurology retained 40.55% of the US MRI market size by application in 2025, underscoring MRI’s dominant role in stroke triage, dementia workups, and multiple sclerosis monitoring. The SIGNA MAGNUS head-only platform signals manufacturers’ commitment to neurology, where focused field homogeneity yields superior cortical detail. Cardiac applications grow steadily thanks to contrast advances such as flurpiridaz that sharpen perfusion mapping. Musculoskeletal imaging benefits from dedicated extremity coils, serving sports medicine and aging baby boomers seeking joint replacements.

Oncology commands the fastest trajectory at a 6.86% CAGR, reflecting both incidence trends and precision therapy. Abbreviated breast MRI protocols bring exam time under ten minutes, making high-risk screening feasible in busy outpatient centers. The University of Waterloo’s synthetic diffusion sequence makes malignant tissue glow, allowing surgeons to plan margins with confidence. AI drives lesion segmentation and response assessment, giving radiologists quantitative biomarkers that translate directly into clinical trial endpoints. As payers link reimbursement to outcomes, such analytics elevate MRI from anatomical snapshot to longitudinal decision platform.

Geography Analysis

The United States exhibits regional contrasts that influence scanner mix and procedure volume. Major metro areas such as New York, Los Angeles, and Chicago account for the densest concentration of 3 T and experimental 7 T installations owing to academic medical centers and higher per-capita health expenditure. CMS projects national health-spending growth of 5.6% annually through 2032, a trend that funds continued fleet renewal in these hubs. Northeast and West Coast providers execute early AI rollouts because strong capital reserves offset software subscription fees. Patients in these regions receive MRI earlier in the diagnostic chain, which raises utilization to levels that eclipse national averages.

Rural communities house nearly 20% of the population yet witnessed more than 100 hospital closures since 2010, creating imaging deserts that pressure state health agencies to subsidize point-of-care solutions. Hyperfine and other portable vendors position ultra-low-field units as bridge technology that brings neuroimaging to critical-access hospitals without infrastructure overhaul. Southern and Midwest states show mixed dynamics; urban centers invest in 3 T upgrades while farming counties struggle with staffing shortages. Regional Certificate-of-Need reform loosens restrictions, enabling outpatient developers to open imaging centers near growing suburbs, a change likely to lift regional scan volumes over the next five years.

Medicare Advantage penetration varies widely, topping 55% in Florida yet below 25% in Wyoming, which shapes reimbursement appetites for new technology. States with generous Medicaid expansion also channel demand; community hospitals in California leverage supplemental payments to finance helium-free magnets as part of decarbonization pledges. The 300-facility Sutter Health–GE pact in California illustrates how vendor-provider alliances expand AI capability statewide, while Mid-Atlantic systems pursue similar deals to counter competitive threat from regional for-profit chains.

Competitive Landscape

The US MRI market shows moderate concentration as three multinationals—GE HealthCare, Siemens Healthineers, and Philips—control the broadest portfolios. Each invests over USD 1 billion in R&D yearly and secures enterprise contracts that lock in service revenue. GE paired with Sutter Health for a seven-year, system-wide imaging refresh and separately joined RadNet to pilot SmartTechnology AI suites that promise double-digit productivity gains. Siemens counters with DeepResolve reconstruction and an open subscription model that bundles software updates for the life of the magnet. Philips focuses on sustainability; BlueSeal helium-free magnets minimize downtime linked to global helium scarcity.

Disruptors attack niche pain points. United Imaging gained FDA clearance for the uMR Jupiter 5 T scanner and offers a white-glove delivery model that compresses site planning timelines from months to weeks. Hyperfine monetizes bedside neuroimaging in stroke units, a workflow incumbents find difficult to replicate without cannibalizing flagship products. Patent activity remains brisk: Philips filed 594 medical-technology applications at the European Patent Office during 2024 alone, signaling continued arms race in magnet design, AI, and workflow orchestration.

Price competition intensifies around mid-field systems where a crowded vendor slate—Canon, Fujifilm, Esaote, and Neusoft—offers robust performance at lower cost. Service differentiation emerges through remote monitoring that predicts coil failures and prescribes maintenance parts before downtime occurs. Tier-two hospitals weigh multivendor service contracts to rationalize fleets featuring mixed brands, forcing OEMs to prove value beyond the hardware sale. Overall, market rivalry rewards suppliers that blend hardware, software, and lifecycle financing into a single proposition that aligns with provider cost constraints and quality metrics.

US Magnetic Resonance Imaging Industry Leaders

-

Fujifilm Holdings Corporation

-

Siemens Healthcare GmbH

-

GE HealthCare

-

Canon Inc. (Canon Medical Systems Corporation)

-

Koninklijke Philips N.V

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: GE HealthCare introduced Sonic DL, a deep-learning acceleration engine that delivers single-heartbeat cardiac MRI acquisitions.

- May 2024: Cincinnati Children’s Hospital imaged its first patient using XENOVIEW xenon gas for enhanced lung ventilation mapping after FDA approval in late 2022.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the United States magnetic resonance imaging (MRI) market as all new, factory-built scanners sold into U.S. healthcare settings, grouped by architecture (open, closed, wide-bore, extremity), field strength (<=0.3 T to >=7 T), and clinical application streams such as neurology or oncology.

Scope exclusion: service revenue from installed scanners and sales of refurbished or pre-owned MRI units fall outside this value assessment.

Segmentation Overview

-

By Architecture

- Closed MRI Systems

- Open MRI Systems

- Wide-Bore MRI Systems

- Extremity MRI Systems

-

By Field Strength

- Low Field MRI Systems (≤0.3 T)

- Mid Field MRI Systems (0.3 T–1.0 T)

- High Field MRI Systems (1.5 T)

- Very-High Field MRI Systems (3 T)

- Ultra-High Field MRI Systems (≥7 T)

-

By Application

- Oncology

- Neurology

- Cardiology

- Gastroenterology

- Musculoskeletal

- Other Applications

Detailed Research Methodology and Data Validation

Primary Research

Analysts interview radiologists, biomedical engineers, procurement managers, and payor advisers across the Northeast, Midwest, South, and West. These dialogues test adoption rates of ultra-high-field systems, average scan tariffs, and upcoming replacement budgets, letting us refine assumptions surfaced in desk work.

Desk Research

We begin with structured reviews of public datasets from bodies such as the OECD (scanner density), the Centers for Medicare & Medicaid Services (procedure volumes and reimbursement tariffs), and the National Cancer Institute (disease prevalence that influences imaging demand). Trade associations like the Medical Imaging & Technology Alliance, peer-reviewed journals on radiology utilization, and U.S. International Trade Commission shipment records provide additional inputs. Paid repositories that Mordor analysts access, including D&B Hoovers for vendor revenue splits and Dow Jones Factiva for regulatory news, enrich competitive and pricing benchmarks. The sources listed illustrate our desk research mix; many more items are consulted during validation.

Market-Sizing & Forecasting

A top-down reconstruction starts with the installed base and annual scan counts, which are multiplied by average selling price trajectories that differ by field strength and bore size. Supplier roll-ups and channel checks then cross-verify totals, closing gaps where unit shipment data are sparse. Key variables in the model include chronic disease incidence, hospital capital-budget growth, reimbursement policy shifts, scan-throughput gains from AI acceleration, and expected unit price deflation on platforms. Forecasts employ multivariate regression that links these drivers to demand. After this, scenario analysis tests upside from portable scanners.

Data Validation & Update Cycle

Outputs flow through variance checks against external benchmarks, senior analyst reviews, and anomaly re-contacts. The model refreshes each year, with interim adjustments triggered by material FDA clearances or reimbursement code revisions before final client delivery.

Why Our US Magnetic Resonance Imaging Baseline Commands Reliability

Diverse publishers post differing dollar values because they often apply narrow hospital-only scopes, older procedure datasets, or single-point ASP estimates. Mordor's disciplined mix of scope, live variables, and yearly refresh keeps our baseline aligned with current market reality.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 3.62 B (2025) | Mordor Intelligence | - |

| USD 2.00 B (2024) | Regional Consultancy A | excludes extremity and wide-bore units, uses 2019 ASPs |

| USD 2.09 B (2024) | Trade Journal B | relies on global share ratios, lacks primary validation of U.S. replacement cycle |

The comparison shows that when scope breadth, live pricing curves, and multi-source validation converge, Mordor's estimate becomes the balanced reference point decision-makers can trust.

Key Questions Answered in the Report

How big is the US Magnetic Resonance Imaging Market?

The US Magnetic Resonance Imaging Market size is expected to reach USD 3.83 billion in 2026 and grow at a CAGR of 5.88% to reach USD 5.1 billion by 2031.

Which MRI architecture holds the largest share?

Closed-bore systems commanded 77.62% of US MRI market share in 2025 owing to superior image quality and scan versatility.

Who are the key players in US Magnetic Resonance Imaging Market?

Fujifilm Holdings Corporation, Siemens Healthcare GmbH, GE HealthCare, Canon Inc. (Canon Medical Systems Corporation) and Koninklijke Philips N.V are the major companies operating in the US Magnetic Resonance Imaging Market.

What main challenge limits market growth?

A shortage of certified MRI technologists remains the most immediate bottleneck, with vacancy rates at 18.1% in 2025.

Page last updated on: