Breast Imaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 6.73 Billion |

| Market Size (2031) | USD 9.92 Billion |

| Growth Rate (2026 - 2031) | 8.12% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

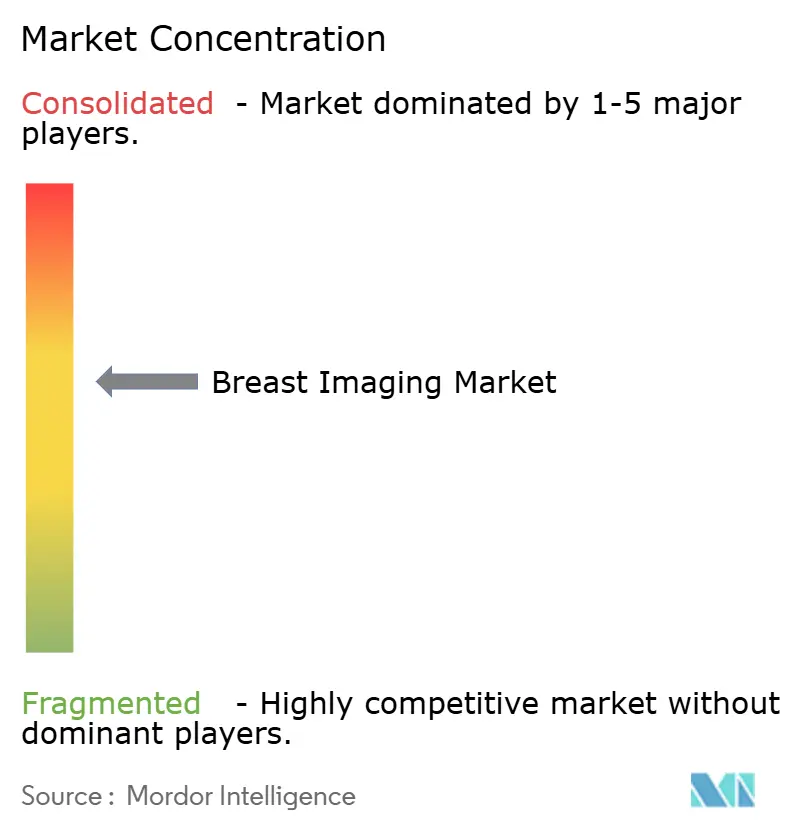

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Breast Imaging Market Analysis by Mordor Intelligence

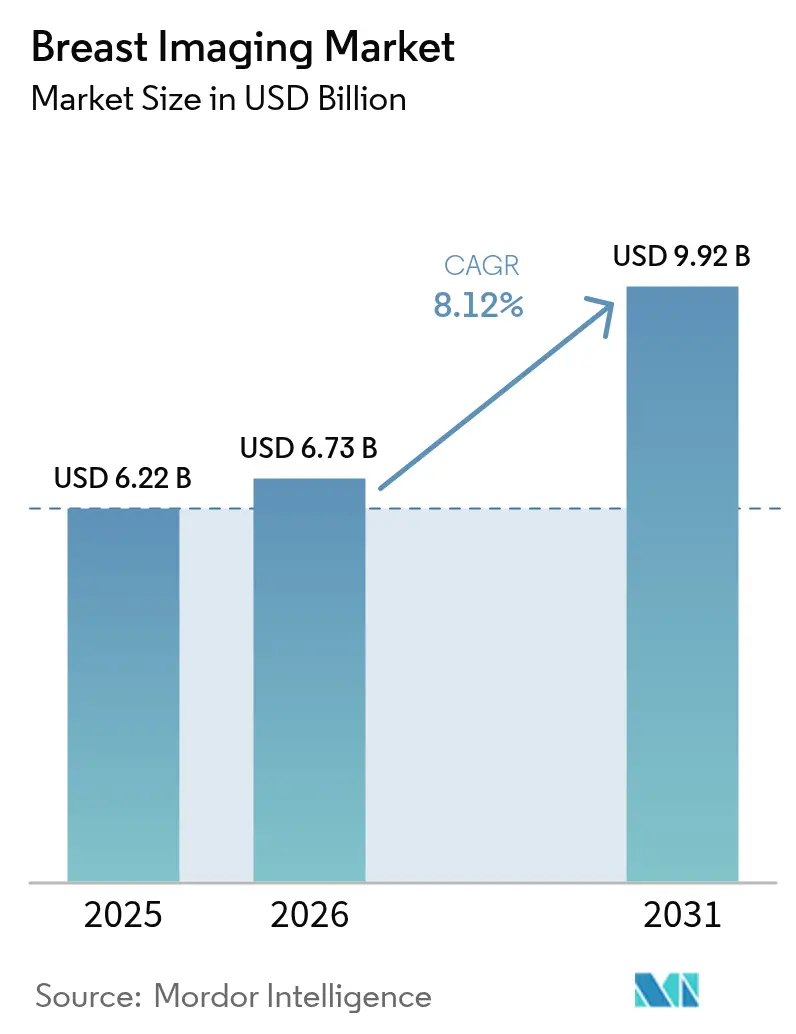

The breast imaging market size in 2026 is estimated at USD 6.73 billion, growing from 2025 value of USD 6.22 billion with 2031 projections showing USD 9.92 billion, growing at 8.12% CAGR over 2026-2031. Growth stems from widespread AI adoption that accelerates reading times, evolving FDA Mammography Quality Standards Act (MQSA) regulations that require dense-breast notifications, and a steady shift toward three-dimensional screening. Hospitals remain the foundation of service delivery, yet outpatient imaging centers scale rapidly as payers push care into lower-cost settings and patients look for convenience. Rising procedure volumes also magnify the urgency of workforce and cybersecurity shortfalls, both of which shape purchase criteria for new equipment. Regionally, North America keeps its leadership position, but Asia-Pacific delivers the greatest incremental revenue on the back of government-funded screening rollouts and middle-class expansion. Competitive intensity tightens as established vendors pair hardware strength with proprietary algorithms while smaller AI specialists carve out high-value workflow niches.

Key Report Takeaways

- By imaging technique, mammography held 38.12% of breast imaging market share in 2025, whereas 3-D/DBT mammography is set to advance at a 12.38% CAGR to 2031.

- By technology, ionizing systems represented 61.74% of revenue in 2025; non-ionizing modalities are forecast to grow at a 10.29% CAGR through 2031.

- By stage of care, screening generated 53.16% of breast imaging market size in 2025, while interventional applications are expanding fastest at a 10.21% CAGR.

- By end user, hospitals commanded 61.95% of the market in 2025; diagnostic imaging centers register the highest growth rate at 11.28% CAGR.

- By geography, North America contributed 35.98% of 2025 revenue, but Asia-Pacific is projected to post the strongest 10.61% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Breast Imaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Prevalence Of Breast Cancer | +1.8% | Global, with highest impact in North America & Europe | Long term (≥ 4 years) |

| Rapid Adoption Of 3-D/DBT Mammography | +2.1% | North America & EU core, expanding to APAC | Medium term (2-4 years) |

| AI-Powered Image-Analysis Improves Workflow Efficiency | +1.5% | Global, with early adoption in developed markets | Short term (≤ 2 years) |

| Expansion Of Portable, Handheld Ultrasound For Remote Screening | +0.9% | APAC core, spill-over to MEA and rural markets | Medium term (2-4 years) |

| Government-Mandated Dense-Breast Notification Laws | +1.2% | North America primary, expanding to EU | Short term (≤ 2 years) |

| Rapid Roll-Out Of Contrast-Enhanced Mammography (CEM) | +0.8% | Global, with concentration in specialized centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing prevalence of breast cancer

An expanding at-risk female population sustains demand for advanced imaging. The American Cancer Society predicts 310,720 new invasive cases and 42,250 deaths in the United States during 2024, reinforcing the value of early detection.[1]American Cancer Society, “Cancer Facts & Figures 2024,” cancer.org Incidence climbs fastest in Eastern Europe, while rising obesity and later first-birth age widen the screening cohort across emerging economies. Ageing demographics amplify volumes because risk escalates steeply after menopause, driving planners to enlarge capacity and upgrade to higher-sensitivity tools. Regular screening improves five-year survival, and payers increasingly treat it as a cost-saving measure rather than a discretionary expense.

Rapid uptake of 3-D/DBT mammography

Digital breast tomosynthesis reduces tissue-overlap artefacts and lowers false-positive callbacks by up to 15% Updated EU guidelines recommend DBT for routine screening, prompting wholesale replacement of 2-D units in public fleets. Providers in the United States still upgrade despite Medicare fee cuts because DBT attracts patient preference and mitigates medicolegal risk. When paired with triage algorithms, DBT shortens interpretation time and lifts throughput, enabling centres to balance lower unit reimbursement with higher daily exam counts.

AI-powered image analysis boosts workflow efficiency

Radiologist shortages leave more than 1,400 breast-imaging posts vacant in the United States in 2025. Cloud-delivered algorithms now mark suspicious regions, stratify risk, and auto-populate structured reports. RadNet’s USD 48 million purchase of iCAD in 2024 highlights the competitive value of owning differentiated AI pipelines.[2]RadNet Inc., “RadNet Completes Acquisition of iCAD,” radnet.com EU Artificial Intelligence Act rules lengthen certification cycles, yet uniform regulation promises pan-European scale once clearance is achieved. Facilities adopt subscription models to access continual software improvements without fresh capital outlay.

Portable handheld ultrasound broadens access

Handheld probes priced far below cart-based systems reach community clinics, mobile vans, and primary-care offices where fixed rooms are scarce. During the COVID-19 emergency these devices preserved screening continuity while limiting hospital visits. Cloud upload lets city specialists read exams captured in rural settings, closing equity gaps and sustaining breast imaging market growth in low-resource geographies. Image resolution still trails premium ultrasound, restricting use in complex diagnostic work-ups, but manufacturers improve probe bandwidth and AI-driven noise reduction with each generation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Cost Of Digital Breast Tomosynthesis Systems | -1.4% | Global, with highest impact in emerging markets | Medium term (2-4 years) |

| Shortage Of Sub-Specialty Radiologists In Emerging Markets | -1.1% | APAC, MEA, and rural markets globally | Long term (≥ 4 years) |

| Cyber-Security Risks For Cloud-Connected Imaging Modalities | -0.8% | Global, with concentration in developed markets | Short term (≤ 2 years) |

| Limited Third-Party Reimbursement For Advanced Breast-Imaging Modalities | -1.6% | North America primary, expanding globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High upfront cost of DBT systems

Full-featured scanners list between USD 400,000 and USD 600,000, stretching capital budgets for independent sites. Consecutive Medicare fee cuts of 11.72% in 2024 and 9.67% in 2025 erode payback calculations. Vendors counter with trade-in credits and usage-based financing, yet adoption lags in price-sensitive regions, slowing replacements of ageing 2-D fleets.

Shortage of sub-specialty radiologists

Graduate caps restrict training slots, and retirements outpace new entrants, lengthening reading queues in rural and middle-income markets. Tele-interpretation and AI relieve volume spikes, but complex cases still demand board-certified expertise. Workforce gaps therefore limit the full utilisation of installed imaging capacity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Imaging Technique: 3-D Evolution Reinforces Mammography’s Core Role

Mammography produced 38.12% of 2025 revenue, anchoring the breast imaging market even as DBT reshapes modality mix. The 3-D upgrade path supports a 12.38% CAGR to 2031, validated by European Commission screening guidance that highlights superior invasive-cancer detection. Breast ultrasound persists as the leading adjunct, providing radiation-free evaluation in dense tissue and in high-risk cohorts. Magnetic resonance imaging (MRI) retains gold-standard status for hereditary risk populations but faces cost and contrast-agent barriers.

Image-guided biopsy workflows integrate seamlessly with diagnostic imaging, streamlining tissue sampling under mammographic, ultrasound, or MRI guidance. Vacuum-assisted systems improve diagnostic yield and patient comfort, while clip-placement advances aid surgical localization. Molecular breast imaging (MBI) remains a targeted problem-solver when other modalities deliver inconclusive results, though radiation exposure limits broad use. AI overlays on each technique raise diagnostic consistency and cut observer variability, further embedding algorithmic support in daily practice.

By Technology: Non-Ionizing Modalities Gain Momentum

Ionizing platforms still account for 61.74% of global sales, reaffirming their ubiquity in national screening programs. Yet non-ionizing modalities post a 10.29% CAGR through 2031 as payer and patient sentiment shifts toward radiation-free solutions. Automated breast ultrasound (ABUS) and contrast-enhanced ultrasound expand beyond handheld scans, addressing reproducibility and sensitivity concerns. High-field MRI systems push anatomic detail higher, while abbreviated protocols shorten table time and cost.

Artificial intelligence reduces exposure in ionizing studies by optimizing acquisition parameters, and hybrid workstations suggest second-look ultrasound for suspicious mammograms, blending both technology classes. Capital costs still tilt higher for MRI, but lifecycle savings accrue from reduced regulatory compliance on radiation. Over the forecast horizon, market competition will likely hinge on delivering diagnostic power with minimal or no ionizing dose.

By Stage of Care: Screening Dominates but Intervention Climbs

Screening programs generated 53.16% of 2025 revenue, proving that early detection anchors the breast imaging market size. However, interventional or therapeutic imaging rides a 10.21% CAGR, propelled by advances in MRI-guided focused ultrasound, stereotactic radiosurgery planning, and real-time navigation during minimally invasive procedures. Diagnostic imaging sits squarely in the middle, translating screening recalls into actionable lesion characterization through contrast, diffusion, or elastography sequences.

Clinicians increasingly monitor therapy with imaging biomarkers, adjusting regimens mid-course to spare toxicity and boost outcomes. Post-procedure surveillance also relies on high-resolution modalities to spot recurrences early. As workflow ties tighten between detection and treatment, vendors position integrated platforms that cover the continuum rather than sell stand-alone scanners.

By End User: Outpatient Players Accelerate

Hospitals retained 61.95% revenue share in 2025, yet diagnostic imaging centers outpace all others with an 11.28% CAGR. Payers favor these outpatient venues for lower facility fees, and patients appreciate faster scheduling. The RadNet–iCAD deal reflects how algorithmic speed gains translate directly into center profitability through higher daily throughput. Ambulatory surgery centers invest in advanced guidance systems so surgeons can biopsy or ablate tumors without hospital admission, broadening addressable procedure volumes.

Academic hospitals nevertheless hold the edge in complex cases requiring multidisciplinary input, threading imaging, pathology, and oncology under one roof. They also act as early adopters of cutting-edge research protocols, setting the stage for downstream community uptake. Tele-radiology partnerships now let suburban sites tap city-center expertise, blurring the lines between care settings and allowing the breast imaging market to follow patients outside traditional walls.

Geography Analysis

North America produced 35.98% of 2025 revenue. The breast imaging market benefits from federally mandated dense-breast notifications effective September 2024, which lift demand for supplemental ultrasound and MRI. AI adoption matures fastest here because early algorithm clearances and venture funding support broad deployment. Growth moderates, however, because replacement purchases dominate a saturated installed base.

Europe follows with high screening penetration and unified clinical guidelines that now recommend DBT. The European Artificial Intelligence Act sets a harmonised approval path, lengthening validation but ultimately creating a single digital market. Public health agencies co-finance refresh cycles, and competitive tenders encourage volume-based discounts that widen access to mid-sized clinics.

Asia-Pacific shows the strongest 10.61% CAGR. Government insurance schemes in China fund biennial mammograms for millions of women, while India’s Ayushman Bharat drives mobile vans into secondary cities. Middle-class awareness campaigns and international NGO partnerships further widen screening coverage. Capital spending migrates from tier-one metros to provincial hubs, where handheld ultrasound and entry-level MRI enable affordable services. Regulatory heterogeneity persists, but local manufacturing incentives attract global vendors into joint ventures.

The Middle East & Africa and South America trail in revenue but post steady single-digit growth. Oil-exporting Gulf states buy premium suites for public centres, whereas sub-Saharan Africa relies on mobile vans and donor funding. Brazil expands public screening capacity, but reimbursement lags, restraining wholesale adoption of DBT.

Competitive Landscape

The breast imaging market is moderately consolidated. Hologic, GE HealthCare, and Siemens Healthineers anchor the top tier, combining detectors, gantry ergonomics, and integrated AI dashboards. Canon Medical pushes ergonomics and dose reduction, while Fujifilm’s open-architecture PACS eases algorithm onboarding. AI-first firms such as Lunit, Kheiron, and Vara supply modality-agnostic engines that plug into rival hardware, intensifying feature competition.

Strategic alliances accelerate capability gaps. RadNet’s iCAD purchase secures exclusive cancer-detection algorithms for its 350-site chain. Volpara adds risk-stratification to SimonMed’s national network, letting technologists tailor exam protocols per patient. Global equipment leaders court these software boutiques, offering co-marketing deals and revenue-share models to speed adoption.

Cybersecurity surfaces as a differentiator after a 2024 CMS breach of nearly 950,000 records. Vendors now highlight zero-trust architecture, end-to-end encryption, and 24 × 7 monitoring. Facilities rank security audits alongside detector technology when issuing tenders, reshaping procurement criteria and pushing smaller suppliers to partner with managed security providers.

Breast Imaging Industry Leaders

GE Healthcare

Hologic Inc.

Siemens Healthineers

Fujifilm Holdings Corp.

Koninklijke Philips N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Penn Medicine launched a mobile mammography program that will circulate year-round across Philadelphia neighbourhoods.

- June 2025: Dharamshila Narayana Superspeciality Hospital introduced a 3-D mammography system and announced free women’s screening under Ayushman Bharat.

- November 2024: GE HealthCare unveiled the Pristina Via system at RSNA 2024, adding ergonomics and AI-guided positioning to enhance technologist productivity.

Global Breast Imaging Market Report Scope

As per the scope, Breast imaging is a subspecialty of diagnostic radiology. It involves various imaging procedures with various tools and technologies to screen, detect, and diagnose breast cancer. If cancer is detected, these tests help our doctors find the type of cancer, as well as determine the stage and location of the cancer. The breast cancer imaging market is segmented by type of imaging technique (mammography, breast ultrasound, breast MRI, image-guided breast biopsy, other imaging techniques), end users (hospitals, diagnostic centers, others), and geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Mammography |

| Breast Ultrasound |

| Breast MRI |

| Image-guided Breast Biopsy |

| Molecular Breast Imaging (MBI) |

| Ionizing Technology |

| Non-Ionizing Technology |

| Screening |

| Diagnostic |

| Interventional / Therapeutic |

| Hospitals |

| Diagnostic Imaging Centers |

| Ambulatory Surgery Centers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Imaging Technique | Mammography | |

| Breast Ultrasound | ||

| Breast MRI | ||

| Image-guided Breast Biopsy | ||

| Molecular Breast Imaging (MBI) | ||

| By Technology | Ionizing Technology | |

| Non-Ionizing Technology | ||

| By Stage of Care | Screening | |

| Diagnostic | ||

| Interventional / Therapeutic | ||

| By End User | Hospitals | |

| Diagnostic Imaging Centers | ||

| Ambulatory Surgery Centers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the breast imaging market?

The breast imaging market size stands at USD 6.73 billion in 2026 and is projected to reach USD 9.92 billion by 2031.

Which modality is expanding fastest within breast imaging?

Three-dimensional digital breast tomosynthesis leads growth with a 12.38% CAGR through 2031.

Why is Asia-Pacific the most dynamic region?

Government-funded screening programs, new hospital construction, and larger middle-class cohorts underpin a 10.61% CAGR in Asia-Pacific.

How does AI improve breast-imaging workflows?

AI marks lesions, raises suspicious cases to the top of the list, and auto-drafts reports, reducing radiologist workload while maintaining accuracy.

What challenges restrain market growth?

High capital costs for DBT equipment, persistent radiologist shortages, and tightening reimbursement all slow the pace of technology adoption.

Page last updated on: