Millet Snacks Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

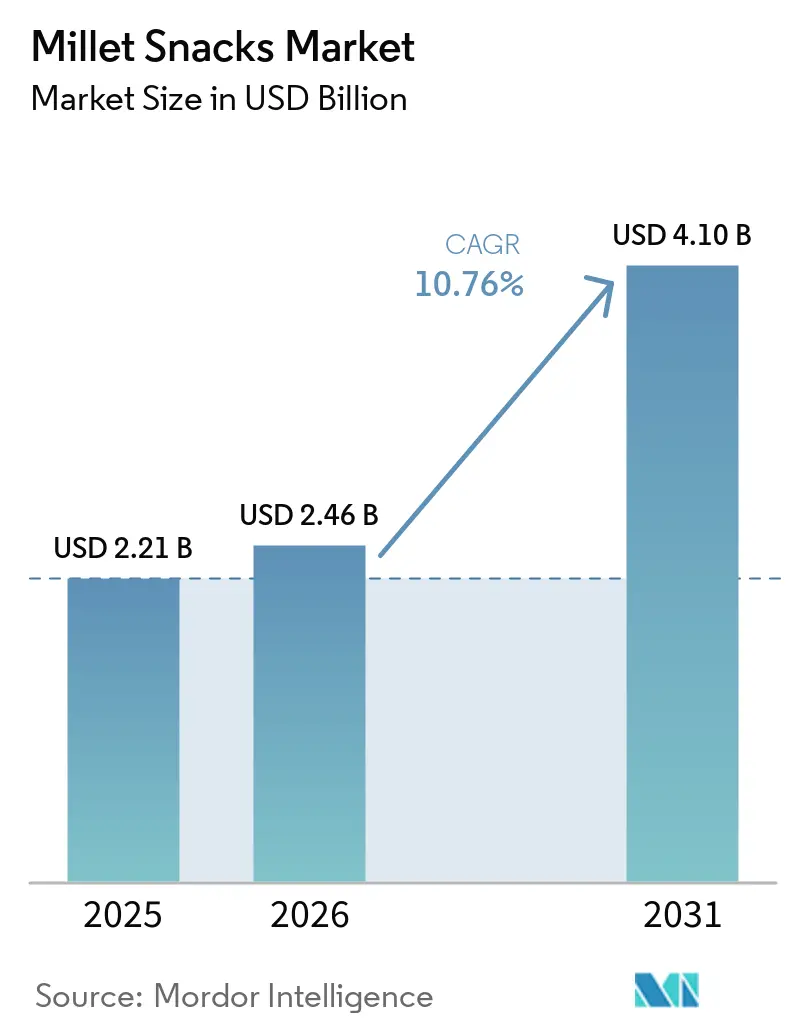

| Market Size (2026) | USD 2.46 Billion |

| Market Size (2031) | USD 4.10 Billion |

| Growth Rate (2026 - 2031) | 10.76% CAGR |

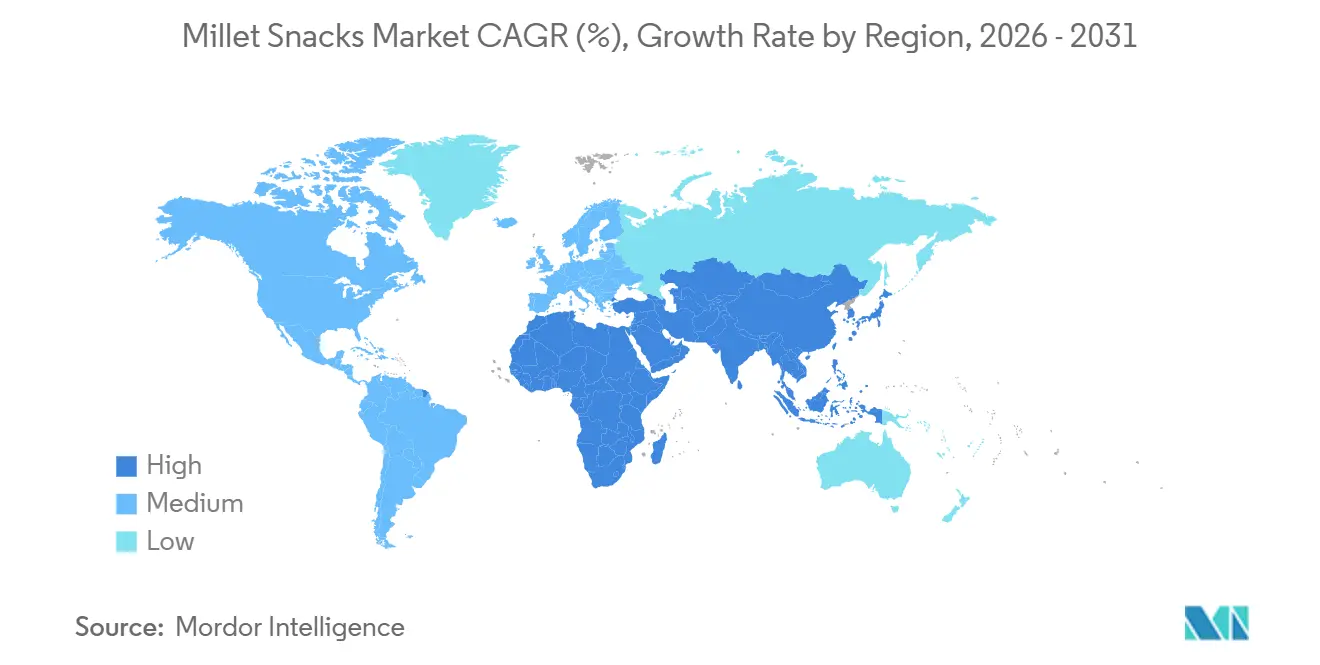

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Millet Snacks Market Analysis by Mordor Intelligence

The millet snacks market size is projected to expand from USD 2.21 billion in 2025 and USD 2.46 billion in 2026 to USD 4.10 billion by 2031, registering a CAGR of 10.76% between 2026 and 2031. This growth underscores a shift towards gluten-free ancient-grain snacking, driven by health trends, supportive government initiatives, and diverse retail strategies. In 2025, the Asia-Pacific region leads with a 48.40% share, bolstered by India's impressive 180.15 lakh-tonne harvest, accounting for 38.4% of the global millet output, as reported by the Ministry of Agriculture and Farmers Welfare. Meanwhile, the Middle East and Africa are witnessing a surge, boasting an 11.92% CAGR, fueled by Yemen's notable 47,000-tonne per-capita consumption and the UAE's growing demand. On the innovation front, while product developers predominantly favor baked formats, there's a notable resurgence of fried variants. Techniques like vacuum-frying and air-puffing are being embraced, ensuring nutrient retention and a return to indulgent textures. In retail, supermarkets remain dominant, yet online platforms and subscription services are reshaping consumer access.

Key Report Takeaways

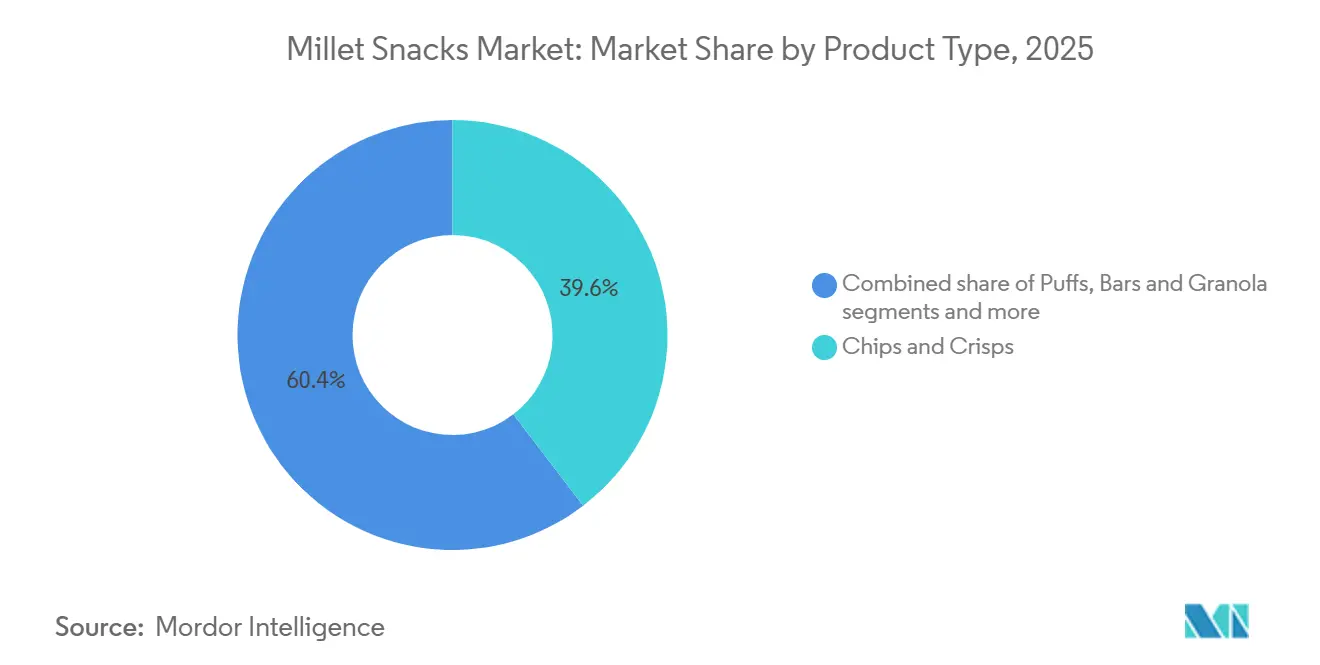

- By product type, chips and crisps held 39.59% of the millet snacks market share in 2025, while puffs are projected to advance at an 11.08% CAGR through 2031.

- By form, baked formats captured 65.69% revenue share in 2025; fried variants are forecast to rise at an 11.97% CAGR between 2026 and 2031.

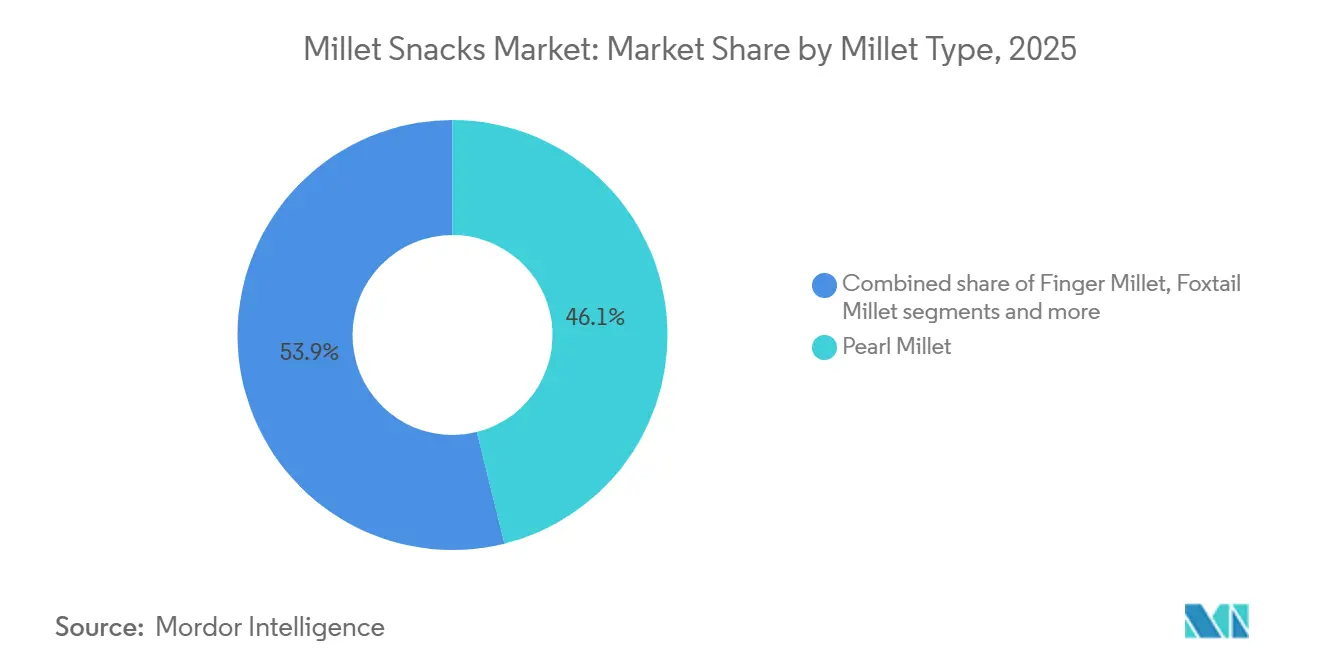

- By millet type, pearl millet accounted for 46.12% of the millet snacks market size in 2025, whereas finger millet is expected to expand at an 11.91% CAGR to 2031.

- By distribution channel, supermarkets and hypermarkets controlled 47.72% of sales in 2025, but online retail is poised to grow at a 12.11% CAGR over 2026-2031.

- By geography, Asia-Pacific led with 48.40% share in 2025, yet the Middle East and Africa region is on track for the fastest 11.92% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Millet Snacks Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Gluten-free and allergen-free snacking boom | +2.1% | Global, with concentration in North America, Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Government initiatives and support programs | +1.8% | Asia-Pacific core (India, China, Thailand), spill-over to the Middle East and Africa, and South America | Long term (≥ 4 years) |

| Health-conscious consumers seeking high-fiber ancient grains and superfoods | +1.6% | Global, led by North America and Europe, is expanding in the Asia-Pacific metros | Medium term (2-4 years) |

| Rise of plant-based and whole-grain diets | +1.4% | North America, Europe, Australia, and urban Asia-Pacific | Medium term (2-4 years) |

| Appeal to convenience and on-the-go snacking | +1.3% | Global, strongest in North America, Europe, and the Asia-Pacific urban centers | Short term (≤ 2 years) |

| Demand for clean-label and natural food products | +1.2% | North America, Europe, with emerging traction in Asia-Pacific and Middle East and Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Gluten-Free and Allergen-Free Snacking Boom

Globally, celiac disease prevalence has stabilized at around 1%. However, non-celiac gluten sensitivity impacts an estimated 6-10% of populations in developed markets[1]Source: National Institutes of Health, “Prevalence of Non-Celiac Gluten Sensitivity,” nih.gov. This creates a consistent demand for gluten-free ancient grain snacks, as highlighted by the National Institutes of Health. Millets, being inherently gluten-free and hypoallergenic, are increasingly favored in formulations catering to diverse dietary restrictions. This is especially pertinent given the rising co-occurrence of gluten sensitivity and other food allergies. The Whole Grains Council found that 84% of US consumers trust products with the Whole Grain Stamp. Furthermore, 81% show a heightened intent to purchase items bearing the stamp, indicating a direct correlation between awareness and sales. Regulatory changes bolster this trend. The FDA's 2022 revision of the "healthy" nutrient content claim and 2023 sodium-reduction guidance encourage a shift towards whole grains. In contrast, the Pan American Health Organization's octagon warning-label mandate, affecting over 30 countries, penalizes snacks made from refined flour. Manufacturers are capitalizing on these insights, marketing millet snacks as both gluten-free and whole-grain to appeal to a broader audience. A case in point is Tata Soulfull's May 2026 debut of Corn Flakes+, which integrates finger millet for enhanced fiber content while proudly flaunting its gluten-free certification.

Government Initiatives and Support Programs

Since its inception in 2018-19, India's National Food Security Mission - Nutri Cereals has allocated a substantial INR 793.27 crore (USD 95.2 million) under the PLI scheme to 29 companies by 2024-25[2]Source: Ministry of Food Processing Industries, “PLI Scheme Progress Report,” mofpi.gov.in. This funding, as reported by the Ministry of Food Processing Industries, Government of India, has been directed towards millet procurement, bolstering processing infrastructure, and advancing research and development. Additionally, through the PMFME scheme, this subsidy has reached 4,366 millet entrepreneurs, disbursing loans amounting to INR 226.40 crore (USD 27.2 million) and establishing 17 incubation centers. The impact of these policies is evident in the production metrics: India's millet output hit 180.15 lakh tonnes in 2024-25. Furthermore, sales of millet-based packaged foods skyrocketed from INR 35 crore (USD 4.2 million) in 2020-21 to an impressive INR 814 crore (USD 97.7 million) in 2024-25, marking a staggering 23.3-fold increase, as highlighted by the Ministry of Agriculture & Farmers Welfare, Government of India. To bolster these efforts, over 10 Indian states have initiated state-level millet missions. Coupled with a hike in the Minimum Support Price (MSP) - notably, ragi's MSP saw an increase of INR 596 per quintal in 2025-26 - these measures aim to de-risk farmer adoption and ensure a steady availability of raw materials. On a broader scale, African nations, with the backing of FAO's technical assistance, are championing millet cultivation as a climate-resilient crop. Notably, both Nigeria and Ethiopia have been ramping up their millet acreage by an impressive 12-15% annually since 2024[3]Source: FAO, “Millet Acreage Expansion in Africa,” fao.org. Highlighting the global momentum, the UN's proclamation of 2023 as the International Year of Millets spurred a flurry of activity, leading to the launch of over 500 new millet-based SKUs within just a year.

Health-Conscious Consumers Seeking High-Fiber Ancient Grains and Superfoods

Finger millet boasts 11.5 g of dietary fiber per 100 g, tripling the fiber content found in polished rice. With a glycemic index ranging from 54 to 68, it stands in contrast to wheat-based snacks, which have a glycemic index of 70 to 85. This positions finger millet as a prime candidate for those seeking glycemic control. Supporting this assertion, a 2024 meta-analysis in the Journal of Nutritional Science highlighted that consistent millet consumption led to a 12-15% reduction in fasting blood glucose levels among prediabetic individuals over a span of 12 weeks. Such findings empower brands to make health claims under the FSSAI and FDA guidelines, setting millet snacks apart from standard whole-grain products. The narrative of millet as a superfood goes beyond just glycemic control. For instance, pearl millet offers 11.6 mg of iron per 100 g, a boon for combating anemia, which affects a staggering 1.6 billion people worldwide. Additionally, foxtail millet boasts an antioxidant capacity, measured by DPPH radical scavenging, that's 40% superior to wheat, as per USDA FoodData Central. Despite 77% of U.S. consumers acknowledging the importance of choosing whole grains, only 61% manage to do so consistently, highlighting a gap that targeted marketing could bridge, as noted by the Whole Grains Council. Brands are capitalizing on this by integrating millets into familiar products like breakfast cereals, granola bars, and cookies, thereby easing the transition for consumers. For instance, Tata Soulfull's Ragi Bites Crème Wafers, introduced in May 2025, swiftly made their way into over 12,000 retail outlets within just six months. These wafers, designed to replicate the sensory experience of traditional wafers, also pack in 3.2 g of fiber per serving.

Rise of Plant-Based and Whole-Grain Diets

According to the EAT-GlobeScan 2024 survey, while 68% of global consumers show interest in plant-based foods, only 20% consume them regularly, highlighting a significant 48-percentage-point gap between intent and behavior. Price stands out as the main hurdle, affecting 42% of consumers globally, with even higher concerns in North America (48%) and Europe (46%). Flavor and taste issues follow closely at 35%. Millet snacks are stepping in to bridge these gaps. Innovations like hot-air puffing at 300°C and twin-screw extrusion have slashed production costs by 18-22% compared to traditional methods, allowing for competitive pricing. Additionally, co-extruding millet with legumes like chickpeas and lentils effectively masks its natural bitterness. Demographics play a crucial role: Millennials (72%) and Gen Z (69%) are at the forefront of the plant-based movement. These younger generations also show a pronounced preference for online retail, the distribution channel growing at a robust 12.11% CAGR. Regional differences in whole-grain consumption are evident: while UK intake remained flat at 28.3 g per day from 2008 to 2019, a survey by the British Nutrition Foundation revealed nearly 50% of Canadians reported no whole-grain consumption on recall days. Such disparities highlight potential markets for millet snacks as alternatives to refined-flour products. Regulatory changes further bolster this trend. The EU's development of front-of-pack nutrition scoring systems, including Nutri-Score, NutrInform, and Keyhole, aims to penalize low-fiber snacks. This creates a prime opportunity for millet-based products, which are likely to score better, to gain shelf space, as noted by the European Commission.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sensory acceptance for taste and texture | -1.4% | Global, most acute in North America, Europe, and non-traditional millet markets | Medium term (2-4 years) |

| Competition from established snack alternatives | -1.2% | Global, particularly intense in North America and Europe | Short term (≤ 2 years) |

| Low consumer awareness and familiarity | -0.9% | North America, Europe, Latin America, and non-Asia-Pacific regions | Medium term (2-4 years) |

| High retail prices compared to alternatives | -0.8% | Global, with heightened sensitivity in price-conscious Middle East and Africa, and South America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Sensory Acceptance for Taste and Texture

Millet, with its nutty and slightly bitter flavor profile, presents challenges in markets accustomed to lighter and sweeter snack textures. The EAT-GlobeScan 2024 survey highlighted flavor and taste as the second-most significant barrier to plant-based food adoption, cited by 35% of respondents, just behind price concerns. While extrusion processing offers a solution, it's not without limitations. Twin-screw extruders, set at 140-160°C and maintaining 18-20% moisture content, can achieve expansion ratios between 1.24 and 3.95. This produces a puffed texture reminiscent of traditional corn-based snacks. Yet, these ratios fall short of corn's potential 4.5-5.0 expansion, leading to a denser product that some consumers find less appealing. To counteract millet's inherent bitterness, flavor-masking techniques are employed. Co-extrusion with a 20-30% blend of chickpea flour not only neutralizes the bitterness but also boosts protein content. Additionally, post-extrusion seasoning with robust flavors like barbecue, cheese, or chili-lime effectively masks millet's base notes. PepsiCo's Kurkure Jowar Puffs, introduced in September 2025, exemplified this strategy. By combining sorghum, a grain closely related to millet, with a bold masala seasoning, they achieved a remarkable 38% trial rate in urban Indian markets within just three months. Furthermore, to minimize launch failures, sensory testing now involves trained panels and consumer acceptance metrics, typically aiming for a score of 6.5 or higher on a 9-point hedonic scale. While this approach has proven effective, it does extend development timelines by an additional 4 to 6 months.

Competition from Established Snack Alternatives

Millet snacks are challenging well-established competitors that boast decades of brand loyalty, extensive distribution networks, and significant economies of scale. While potato chips, corn-based puffs, and wheat crackers enjoy ingredient costs that are 30-40% lower than those of millets, they can price their products 40-60% cheaper than their millet counterparts [Industry analysis]. Global giants like PepsiCo's Lay's and Frito-Lay, Mondelez's Ritz crackers, and Kellogg's (now Kellanova) Pringles, collectively rake in multi-billion-dollar revenues and dominate premium shelf spaces in supermarkets. Instead of yielding ground to these niche entrants, these established players are reformulating their products in response to health trends, integrating whole grains, cutting down sodium, and eliminating artificial colors. Kellanova's strategic acquisitions, particularly its interest in brands adjacent to millet, hint at a trend of consolidation that might absorb these new entrants rather than push out the old guard. The challenge is even starker in developed markets, where snacking is a deeply ingrained habit: USDA Economic Research Service data reveals that U.S. consumers indulge in an average of 2.7 snacking occasions daily, with 68% of these moments featuring brands they know and trust. To carve out a niche, millet snacks must either offer a compelling health narrative, backed by clinical evidence, certifications like USDA Organic and Non-GMO Project Verified, and endorsements from influencers, or collaborate with established players for co-branded ventures that leverage existing brand loyalty. A case in point is Tata Consumer's January 2025 collaboration with PepsiCo, launching 'Kurkure x Ching's Secret Schezwan', merging Tata's expertise in millets with PepsiCo's vast distribution network.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Puffs Propel Innovation Wave

Puffs are set to grow at a CAGR of 11.08% through 2031, outpacing the overall market's 10.76% growth. This is driven by manufacturers using hot-air puffing machines (HAPM) at 300°C for oil-free expansion while preserving micronutrients. In 2025, chips and crisps held a 39.59% market share due to consumer familiarity and versatile flavors but faced margin pressures from fluctuating potato and corn prices. Bars and granola, positioned as premium products, leveraged convenience and clean-label appeal to price 50-70% higher than chips. However, their growth is limited by a 6-9 month shelf-life and crumbly textures. Cookies and biscuits, popular for tea-time and breakfast, saw ITC's Sunfeast Farmlite Super Millets Cookies distributed in over 85,000 outlets by May 2025. Yet, the segment's 8.9% CAGR is hindered by sugar content concerns. Breakfast cereals and muesli are gaining traction among health-conscious consumers. Tata Soulfull's Corn Flakes+, launched in May 2026, doubled fiber content to 4.3 g per serving, meeting FDA "healthy" claim standards. The "Others" category, including millet-based pasta, noodles, and savory mixes, remains nascent but attracts innovation.

Extrusion technology drives puff growth: twin-screw extruders achieve expansion ratios of 1.24 to 3.95 for multi-millet blends (finger, pearl, foxtail). Key parameters include die configuration, barrel temperature (140-160°C), and moisture content (18-20%). Barnyard millet snacks reached a 3.949 expansion ratio, nearing corn's 4.5-5.0 benchmark. PepsiCo's Kurkure Jowar Puffs, launched in September 2025, combined sorghum with masala seasoning, achieving a 38% trial rate in urban Indian markets within three months. Chips and crisps face innovation challenges; vacuum-frying reduces oil by 30-40% but raises costs by 15-20%, limiting adoption to premium SKUs. Bars and granola struggle with millet's low gluten content, requiring alternative binders like dates or chicory root fiber, complicating formulations. Breakfast cereals use millet's low glycemic index (54-68 vs. wheat's 70-85) to target diabetic and prediabetic consumers, a group projected to exceed 700 million globally by 2045, per the International Diabetes Federation.

By Form: Fried Formats Stage Comeback

Fried variants are set to grow at a CAGR of 11.97% through 2031, surpassing baked formats' growth despite baked's 65.69% market share in 2025. Innovations like vacuum-frying and air-puffing are enhancing fried snacks' health appeal. Vacuum-frying, operating at 90-120°C under reduced pressure (5-10 kPa), reduces oil absorption by 30-40% and preserves heat-sensitive vitamins like thiamine and riboflavin. This positions fried snacks as "better-for-you" options, appealing to consumers seeking indulgent textures without guilt. Baked formats, dominant through 2025 due to clean-label trends, face sensory drawbacks, such as 18-22% lower crispness scores and shorter shelf-life (8-9 months vs. 12 months for fried).

Air-puffing, using hot-air puffing machines (HAPM) at 300°C, eliminates oil while achieving expansion ratios of 2.8-3.2 for finger millet. Bonvie Snacks' Millet Chips - Mint, launched in May 2025, used air-puffing to deliver 4.1 g fiber per 30 g serving with zero trans fat, earning USDA Organic and Non-GMO Project Verified certifications. Regulatory changes, like the FDA's 2023 sodium-reduction guidance and the Pan American Health Organization's octagon warning-label mandate, penalize high-sodium baked snacks, leveling competition. Fried formats also cater to ethnic flavors like chili-lime and masala, appealing to growing diaspora segments in North America and Europe. While baked formats dominate institutional channels due to low-fat policies, fried snacks are regaining ground in retail through improved processing and targeted marketing.

By Millet Type: Finger Millet's Nutritional Edge

Finger millet is projected to grow at a CAGR of 11.91% through 2031, narrowing the gap with pearl millet, which held a 46.12% market share in 2025. This growth is driven by its superior micronutrient profile: 340 mg of calcium and 11.5 g of dietary fiber per 100 g, compared to pearl millet's 42 mg of calcium and 8.5 g of fiber. A 2024 meta-analysis in the Journal of Nutritional Science found finger millet reduced fasting blood glucose by 12-15% in prediabetic individuals over 12 weeks, supporting health claims under FSSAI and FDA guidelines. Pearl millet remains dominant due to its shorter growing cycle (70-90 days vs. 120-150 days for finger millet), higher drought tolerance, and established supply chains in Rajasthan, Gujarat, and Haryana, which produce 8.6 million tonnes annually (Ministry of Agriculture & Farmers Welfare, Government of India). Foxtail millet, with a 15-20% price premium due to its antioxidant capacity (40% higher than wheat) and organic appeal, faces scalability challenges, with India producing only 0.42 million tonnes in 2024-25 (IIMR). Little millet and other minor varieties (kodo, proso, barnyard) hold an 8-10% market share, driven by cultural demand in Odisha, Chhattisgarh, and Jharkhand.

Processing innovations favor finger millet. Its 7.3 g protein content per 100 g enhances dough elasticity, while its polyphenol-driven darker color reduces baking times by 10-12%. Tata Soulfull's Ragi Bites line, including Crème Wafers (May 2025), Choco Sticks (August 2023), and No Maida Choco (May 2026), leverages these properties to match wheat-based textures. Pearl millet's neutral flavor suits savory snacks like chips and puffs, while finger millet's nutty flavor complements sweet products like cookies and cereals. Foxtail millet's 1.5-2.0 mm grain size works well in granola and muesli, offering visual and textural appeal. The "Others" category benefits from 276 new millet varieties introduced in 2024-25, including high-yielding, pest-resistant types, expanding raw material options and reducing procurement risks (Ministry of Agriculture & Farmers Welfare, Government of India).

By Distribution Channel: Online Retail's Disruptive Ascent

Online retail stores are projected to grow at a CAGR of 12.11% through 2031, surpassing the 47.72% market share of supermarkets and hypermarkets in 2025. Growth is driven by D2C models, subscription services, and algorithm-driven personalization, reducing customer acquisition costs by 25-30%. E-commerce platforms like Amazon and BigBasket attract health-conscious shoppers willing to pay 15-20% premiums for curated assortments. Millet snacks benefit from "better-for-you" category placements, enhancing visibility. Subscription models, such as Troo Good's millet snack boxes, secure recurring revenue and reduce inventory waste by 18-22%, addressing their 8-12 month shelf-life constraints. Supermarkets retain dominance through impulse purchases, cross-merchandising, and shelf-space expansion, though North American retailers face margin pressures from slotting fees and promotions.

Specialty health stores command 30-40% price premiums through expert staff, sampling, and organic certifications but hold only 8-10% market share due to limited reach and competition from mass-market retailers like Walmart and Tesco. Convenience stores cater to on-the-go consumers with single-serve SKUs but face stagnation as vending machines favor high-velocity brands. The "Others" category, including food-service channels, direct sales, and farmers' markets, sees growth in food-service as institutions adopt healthier procurement policies. Tata Consumer's Joyfull Millets muesli, launched in Canada in June 2024, secured listings in 450+ cafeterias and dining halls within six months. In APAC, where smartphone penetration exceeds 70%, online retail is rising, supported by digital payment systems like UPI and Alipay, enabling rural access to millet snacks. Supermarkets counter with click-and-collect services and partnerships with delivery aggregators, pushing brands toward omnichannel strategies.

Geography Analysis

Asia-Pacific, holding a 48.40% market share in 2025, is expected to maintain its lead through 2031. India's production of 180.15 lakh tonnes in 2024-25, representing 38.4% of global millet output, and government policies allocating INR 793.27 crore (USD 95.2 million) under the PLI scheme to 29 millet-processing companies, drive this growth. Millet-based packaged food sales in India rose from INR 35 crore (USD 4.2 million) in 2020-21 to INR 814 crore (USD 97.7 million) in 2024-25, a 23.3-fold increase, driven by over 500 new SKU launches following the UN's 2023 International Year of Millets declaration. In China, millet consumption is concentrated in northern provinces like Shanxi and Hebei, while urbanization and Western dietary trends are boosting snack-format adoption in tier-1 cities, with modern retail channels growing 14-16% annually. Japan's USD 30 billion health-food market increasingly incorporates millets into functional snacks targeting elderly consumers (28.4% of the population aged 65+), focusing on bone health and glycemic control. Thailand, Indonesia, and South Korea are seeing gluten-free product launches rise 18-22% annually since 2024, driven by expatriate communities and health-conscious millennials. Australia's organic snack market, growing at 12% CAGR, positions millets as a native alternative to imported quinoa, with retailers like Woolworths and Coles increasing millet SKU counts by 30% in 2025.

The Middle East and Africa, growing at 11.92% CAGR through 2031, lead regional growth. Yemen's per-capita consumption of 47,000 tonnes (35% of the regional total) and the UAE's 22,000 tonnes consumption drive demand. Nigeria and Ethiopia, Africa's largest millet producers, are expanding acreage by 12-15% annually with FAO support to promote climate-resilient crops. The UAE's retail sector, led by Carrefour and Lulu, stocks millet snacks in "free-from" sections catering to expatriate demand. Saudi Arabia's Vision 2030 allocates SAR 500 million (USD 133 million) to millet-processing clusters in Al-Qassim and Hail. South Africa's urban centers see rising millet-snack penetration in Woolworths and Pick'n Pay, driven by health-conscious consumers and government nutrition campaigns. Egypt and Morocco leverage Mediterranean diets to position millets as alternatives to imported wheat, with brands like Mansour Group launching millet-based biscuits in 2025.

North America, with a 25% market share in 2025, is led by the U.S., where gluten-free and ancient-grain segments exceed USD 8 billion in annual sales. Health snack shelf space grew 22% in 2024, with retailers like Whole Foods and Walmart dedicating 12-15% of snack aisles to millet-based products. Canada's millet snack market benefits from multicultural demographics, with South Asian, African, and Middle Eastern communities (22% of the population) easing adoption. Tata Consumer's Joyfull Millets muesli launched in Canada in June 2024, securing listings in 450+ cafeterias within 6 months. Mexico's snack market, dominated by corn-based products, is seeing millet chips gain traction in premium supermarkets in urban centers. Europe, with a 30% market share in 2025, is led by the UK, Germany, and France. UK retailers like Tesco expanded millet SKU counts by 25% in 2025, positioning them in "Free From" aisles. Germany's Bio-Siegel and EU Organic certifications enable millet snacks to access premium channels like Alnatura. France's Nutri-Score labeling, favoring high-fiber, low-sodium products, boosts millet snacks' visibility. South America, the smallest market, sees Brazil, Argentina, and Colombia growing at 9-11% CAGRs, driven by urbanization and health-awareness campaigns.

Competitive Landscape

In the millet snacks market, moderate fragmentation is evident. The top five players, Tata Consumer Products, ITC Limited, Britannia Industries, Nestle, and Kellanova, hold a majority share. Meanwhile, regional specialists like Haldiram, Troo Good, and Urban Millets, along with artisanal producers, account for the rest. Consolidation is on the rise, with incumbents employing acquisition strategies for growth. In February 2026, Marico made headlines by acquiring a 60% stake in Cosmix Wellness for INR 375 crore (USD 45 million), eyeing the premium wellness segment. Just two months later, in April 2026, ITC brought Yoga Bar under its wing as a wholly-owned subsidiary, seamlessly merging its protein-bar lineup with ITC's expansive distribution network, which boasts over 6 million retail outlets. PepsiCo's reported interest in a minority stake in Haldiram, India's leading ethnic-snack manufacturer with annual revenues surpassing INR 8,000 crore (USD 960 million), underscores the recognition of millet snacks as a strategic addition to core portfolios. Three key areas present white-space opportunities: first, institutional channels like schools and hospitals, where healthier procurement policies are on the rise, yet millet penetration lingers below 5%; second, single-serve formats (30-50 g packs) priced under USD 1.50, catering to price-sensitive consumers in emerging markets; and third, co-branded partnerships, such as Tata Consumer's January 2025 collaboration with PepsiCo for Kurkure x Ching's Secret Schezwan.

Technology deployment sets the winners apart. For instance, twin-screw extrusion systems achieving 3.5-3.9 expansion ratios for barnyard millet are bridging the sensory acceptance gap with corn-based puffs. Meanwhile, vacuum-frying and hot-air puffing machines (HAPM) operating at 300°C not only eliminate oil but also preserve micronutrients. This innovation is reviving the health credentials of fried formats, appealing to consumers desiring indulgent textures without the guilt. Smaller disruptors are turning to direct-to-consumer (D2C) models, sidestepping traditional retail markups. True Good, for example, runs 17 incubation centers under India's PMFME scheme, produces 2 million units daily, and is on track for revenues of INR 100 crore (USD 12 million). By sourcing from over 15,000 farmers, Troo Good showcases how vertical integration can reduce costs and ensure a steady supply.

Certification strategies play a pivotal role: certifications like USDA Organic, Non-GMO Project Verified, and gluten-free can command price premiums of 20-30%. They also pave the way for distribution in specialty channels such as Whole Foods and Sprouts Farmers Market, which attract health-conscious shoppers. Patent filings shed light on innovation trends: recent applications spotlight extrusion die configurations, flavor-encapsulation techniques, and methods for extending shelf life. Notably, India's Council of Scientific and Industrial Research (CSIR) has filed 12 millet-processing patents in 2024-25. Regulatory compliance is crucial. Adhering to FSSAI's 2016 regulations and the FDA's updated "healthy" nutrient content claim definition influences product formulations. Brands that align with these thresholds not only ensure compliance but also gain a competitive edge in health-claim marketing.

Millet Snacks Industry Leaders

Nestlé S.A.

Tata Consumer Products

ITC Limited

Kellanova

Minkan Agro Industries Private Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Tata Consumer Products launched Soulfull Corn Flakes+ with millets, embedding finger millet to boost dietary fiber from 2.1 g to 4.3 g per serving, directly addressing FDA's updated "healthy" claim thresholds and targeting diabetic and prediabetic consumers in India's 101-million-strong diabetic population.

- February 2026: Marico acquired a 60% stake in Cosmix Wellness for INR 375 crore (USD 45 million), targeting the premium wellness segment with millet-based protein powders, snack bars, and breakfast mixes that command 30-40% price premiums over conventional offerings.

- September 2025: PepsiCo India launched Kurkure Jowar Puffs, pairing sorghum (a millet-adjacent grain) with masala seasoning and deploying twin-screw extrusion to achieve expansion ratios of 3.2, capturing trial rates of 38% in urban markets within 3 months and signaling multinational entry into the millet-snacks category.

Global Millet Snacks Market Report Scope

Millet snacks are ready-to-eat or minimally processed packaged foods made primarily from millet grains, a group of small-seeded, gluten-free ancient grains from the grass family. The global millet snacks market is segmented by product type, form, millet type, distribution channel, and geography. By product type, the market is segmented into chips and crisps, puffs, bars and granola, cookies and biscuits, breakfast cereal and muesli, and others. By form, the market is segmented into fried and baked. By Millet Type, the market is segmented into finger millet, pearl millet, foxtail millet, little millet, and others. By Distribution Channel, the market is segmented into supermarkets/hypermarkets, convenience stores, specialty health stores, online retail stores, and others. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The Market Forecasts are Provided in Terms of Value (USD).

| Chips and Crisps |

| Puffs |

| Bars and Granola |

| Cookies and Biscuits |

| Breakfast Cereal and Muesli |

| Others |

| Fried |

| Baked |

| Finger Millet |

| Pearl Millet |

| Foxtail Millet |

| Little Millet |

| Others |

| Supermarkets/Hypermarkets |

| Convenience Stores |

| Specialty Health Stores |

| Online Retail Stores |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Sweden | |

| Belgium | |

| Poland | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Thailand | |

| Singapore | |

| Indonesia | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Peru | |

| Chile | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Saudi Arabia | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| Product Type | Chips and Crisps | |

| Puffs | ||

| Bars and Granola | ||

| Cookies and Biscuits | ||

| Breakfast Cereal and Muesli | ||

| Others | ||

| Form | Fried | |

| Baked | ||

| Millet Type | Finger Millet | |

| Pearl Millet | ||

| Foxtail Millet | ||

| Little Millet | ||

| Others | ||

| Distribution Channel | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Specialty Health Stores | ||

| Online Retail Stores | ||

| Others | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Sweden | ||

| Belgium | ||

| Poland | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Thailand | ||

| Singapore | ||

| Indonesia | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Peru | ||

| Chile | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Saudi Arabia | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the millet snacks market in 2026, and how fast is it growing?

The millet snacks market size stands at USD 2.46 billion in 2026 and is forecast to reach USD 4.10 billion by 2031, expanding at a 10.76% CAGR over 2026-2031.

Which region leads global demand for millet-based snacks?

Asia-Pacific holds the lead with 48.40% share in 2025, backed by India’s dominant production base and rising urban consumption.

What product form is expected to grow the fastest?

Fried millet snacks, empowered by vacuum-frying and air-puffing, show the quickest 11.97% CAGR through 2031.

Why is finger millet gaining popularity over pearl millet in snacks?

Finger millet’s superior calcium (340 mg/100 g) and fiber content (11.5 g/100 g) deliver clinically proven glycemic benefits, fueling its 11.91% CAGR.

Page last updated on: