Meat Snacks Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

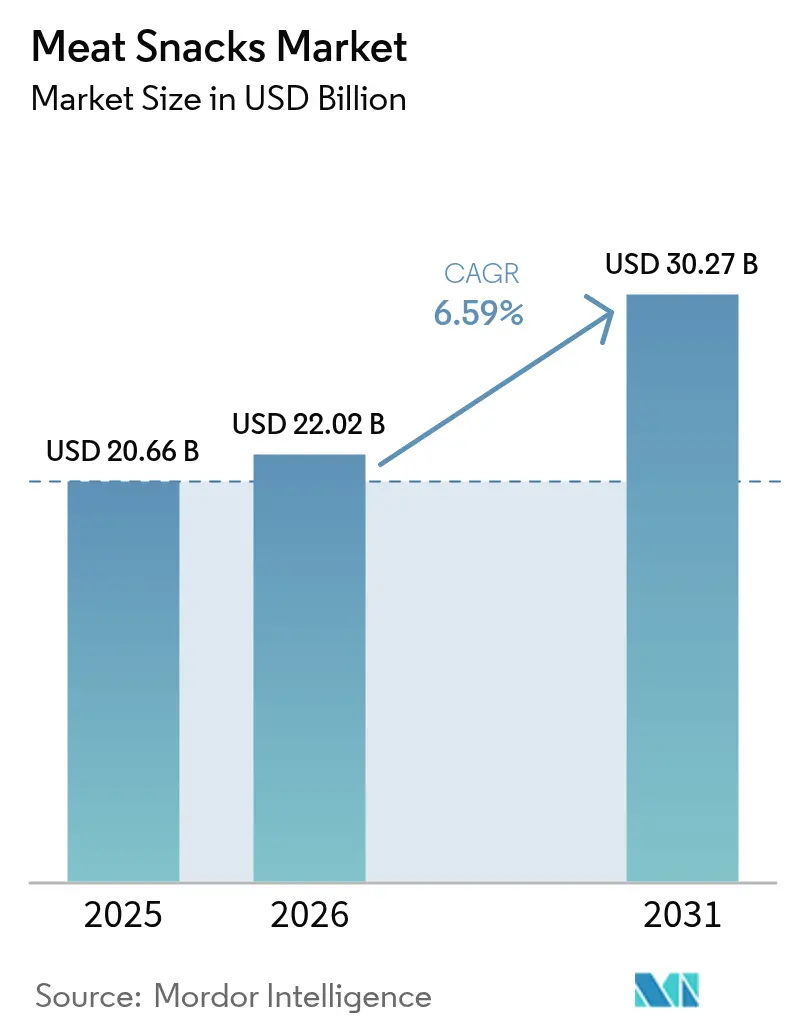

| Market Size (2026) | USD 22.02 Billion |

| Market Size (2031) | USD 30.27 Billion |

| Growth Rate (2026 - 2031) | 6.59% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Meat Snacks Market Analysis by Mordor Intelligence

The meat snacks market size is expected to grow from USD 20.66 billion in 2025 to USD 22.02 billion in 2026 and is forecast to reach USD 30.27 billion by 2031 at 6.59% CAGR over 2026-2031. This growth is primarily driven by the rising popularity of protein-rich diets and the increasing demand for convenient food options. Products like beef jerky remain popular as they provide an affordable and complete source of protein. Even with rising food prices, consumers are opting for bulk purchases and value packs to save costs. The availability of meat snacks in convenience stores and online platforms has further expanded their accessibility. Premium and clean-label products are gaining traction, offering higher profit margins and paving the way for artisanal brands to enter the market. While regulatory concerns about processed meat have led to reformulation efforts and the introduction of plant-based alternatives, these factors have not significantly slowed the market's growth. The market is moderately consolidating, with key players such as Conagra Brands, Tyson Foods, and Hormel Foods Corporation maintaining a strong presence.

Key Report Takeaways

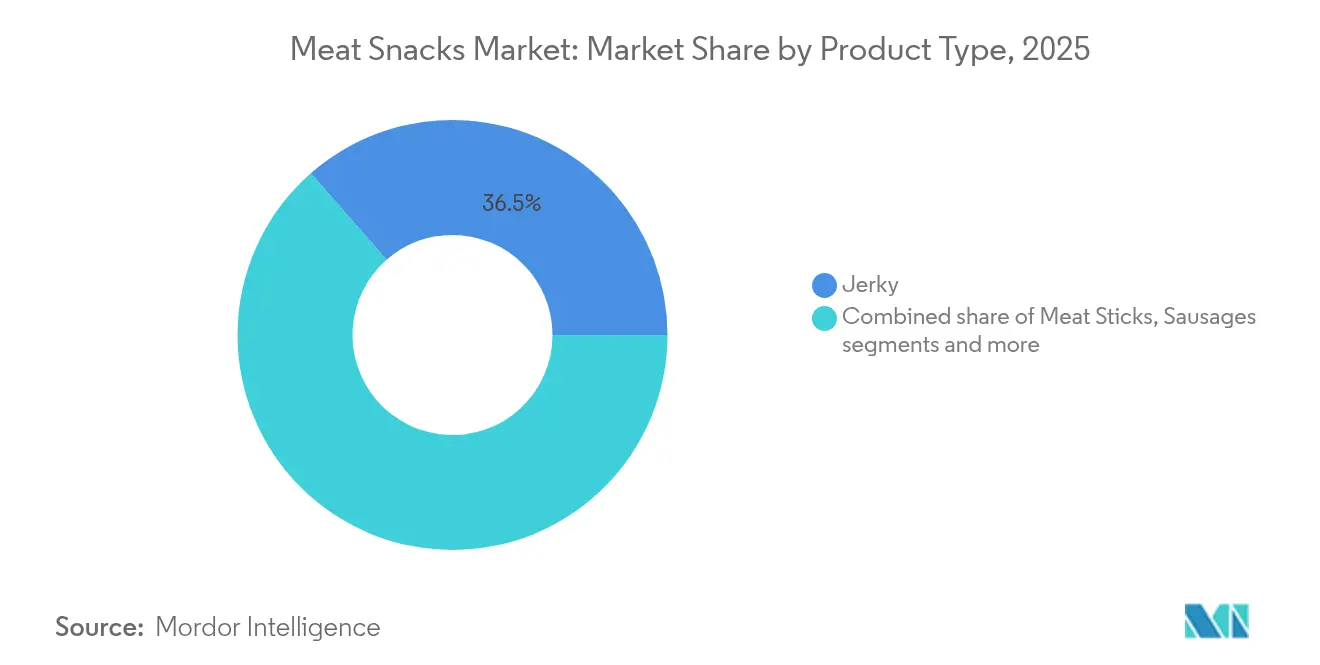

- By product type, jerky led with 36.45% of the meat snacks market share in 2025; meat sticks are advancing at a 7.09% CAGR through 2031.

- By source, beef captured 48.10% share of the meat snacks market size in 2025, while pork is set to expand at a 6.68% CAGR between 2026 and 2031.

- By category, conventional offerings dominated with 87.40% revenue share in 2025; organic lines are growing at an 8.32% CAGR over the same horizon.

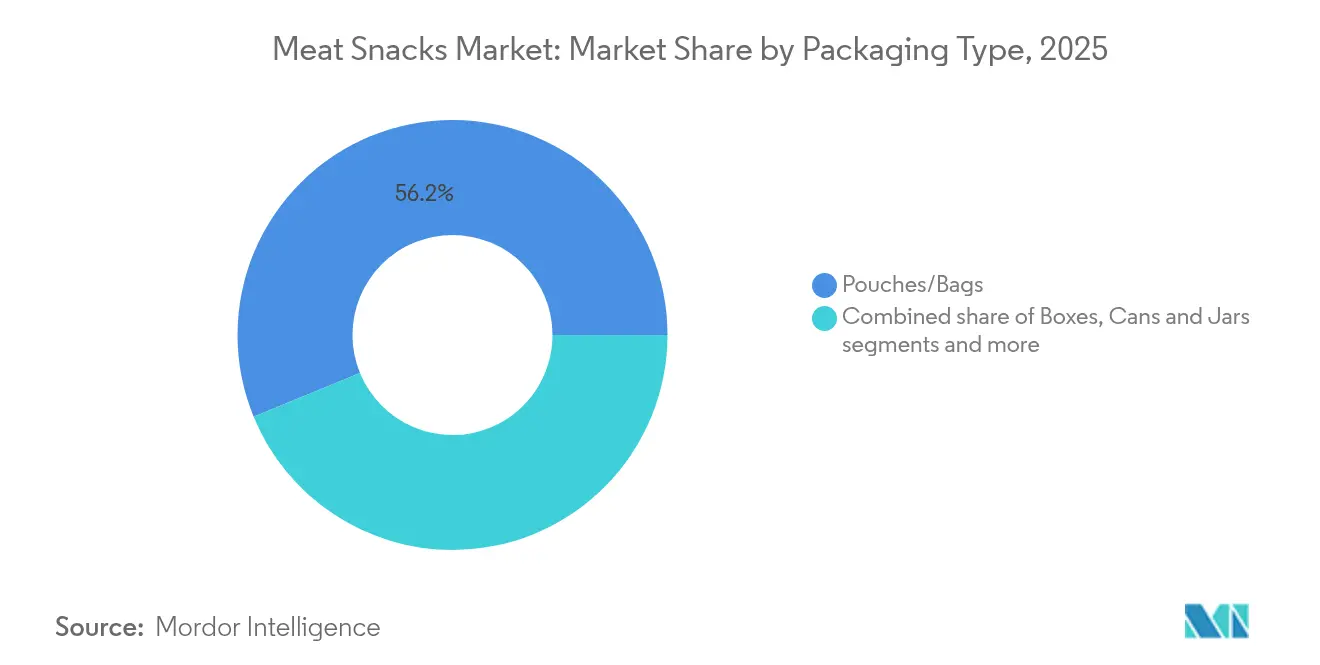

- By packaging, pouches/bags commanded 56.20% of the meat snacks market size in 2025, whereas boxes will grow at a 7.34% CAGR to 2031.

- By distribution channel, supermarkets/hypermarkets held 44.70% of the meat snacks market share in 2025, yet online retail stores are accelerating at a 9.32% CAGR through 2031.

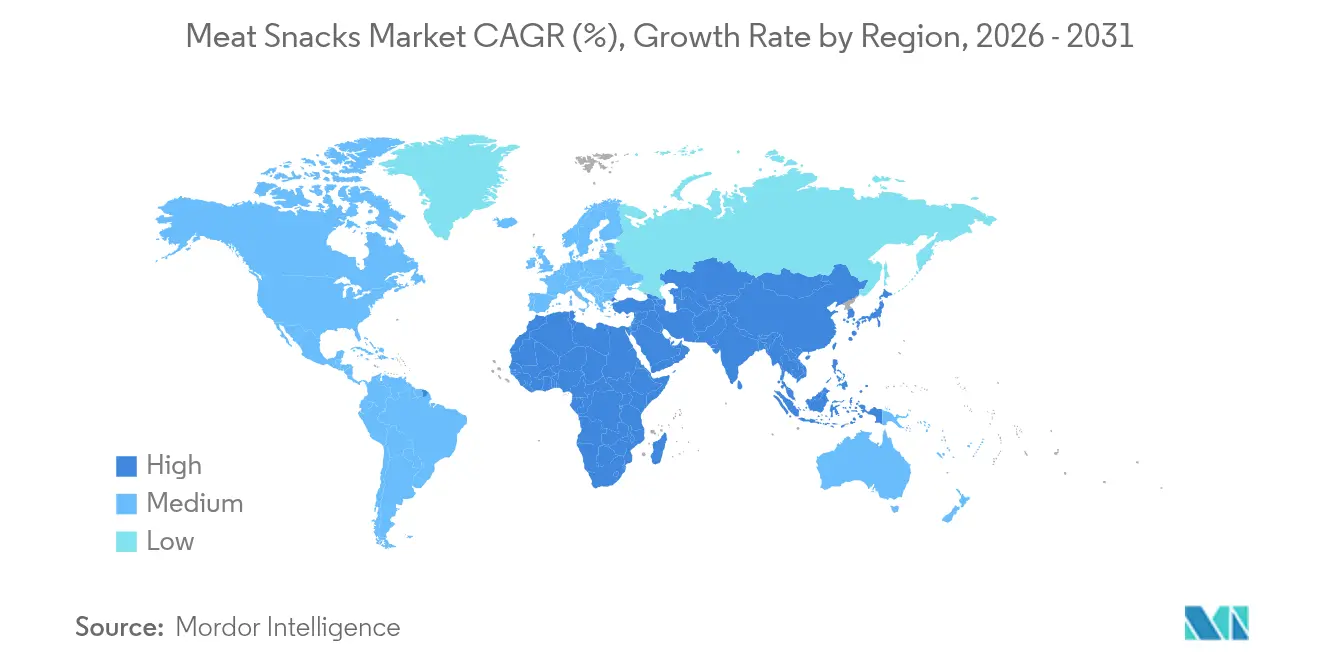

- By geography, North America commanded 44.90% of the global meat snacks market size in 2025, whereas Asia-Pacific will grow at a 8.92% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Meat Snacks Market Trends and Insights

Drivers Impact Table*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising demand for high-protein snacks | +1.2% | Global, with strongest impact in North America and Europe | Medium term (2-4 years) |

| Increasing convenience and on-the-go consumption | +0.8% | Global, particularly urban centers in Asia-Pacific | Short term (≤ 2 years) |

| Increasing popularity of premium and gourmet products | + 1.1% | North America and Europe, expanding to Asia-Pacific affluent segments | Medium term (2-4 years) |

| Product innovation and flavor expansion | +0.9% | Global, with regional flavor preferences | Medium term (2-4 years) |

| Focus on clean ingredient lists | + 0.7% | North America and Europe, regulatory-driven adoption | Long term (≥ 4 years) |

| Expansion of plant-based meat snacks | +1.0% | Global, led by North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising demand for high-protein snacks

The demand for high-protein, low-carb, and convenient snack options is driving the growth of the meat snacks market. According to the International Food Information Council (IFIC), as of 2024, 71% of American consumers are actively looking to include more protein in their diets, highlighting a shift toward healthier and functional snacking[1]Source: International Food Information Council Org, "2024 IFIC Food and Health Survey", ific.org. To meet this demand, brands are introducing clean-label meat snacks that focus on high protein, convenience, clear protein benefits, and high-quality ingredients. For instance, in May 2025, Wenzel’s Farm launched its PRO snack stick line, which includes single-serve beef and pork sticks in four bold flavors. Each stick provides 16 grams of protein with minimal sugar, catering to health-conscious and busy consumers. This growing preference for health, convenience, and clean nutrition is expected to drive the global meat snacks market's growth in the coming years.

Increasing convenience and on-the-go consumption

The growing need for convenience and on-the-go eating is driving the meat snacks market. As people lead busier lives, they are replacing full meals with easy-to-carry, protein-packed snacks that are both filling and convenient. According to Mondelez International Inc.'s 2024 state of snacking report, 91% of global consumers snack at least once a day, and 61% snack twice or more, showing a clear shift toward flexible eating habits[2]Source: Mondelez International Inc., "2024: State of Snacking", mondelezinternational.com. Meat snacks like jerky and sticks fit this trend well because they are easy to store, come in portioned sizes, and require no preparation. Features like resealable packaging, vacuum-sealed options, and single-serve packs are especially appealing to busy workers, travelers, and fitness enthusiasts. These qualities not only make meat snacks easy to carry and keep fresh but also allow brands to capture a wide consumer base, making these snacks a practical choice for today’s snacking needs.

Increasing popularity of premium and gourmet products

Consumers are increasingly opting for premium and gourmet meat snacks due to rising incomes, changing preferences, and a growing focus on healthier ingredients and clean-label products. According to the International Monetary Fund (IMF), as of 2024, purchasing power parity stands at USD 206.88 thousand, reflecting a greater ability and willingness among consumers to spend on high-quality, indulgent food options[3]Source: International Monetary Fund, "GDP, Current Prices, Purchasing power parity; Billions of International Dollars", imf.org. In October 2023, Country Archer Provisions launched rosemary turkey mini sticks and original beef jerky snack packs. These products are clean-label and rich in protein, catering to health-conscious individuals who value premium and nutritious snacks. This shift highlights how higher incomes, combined with a desire for healthier, flavorful, and authentic snack options, are driving changes in the global meat snacks market, encouraging brands to innovate and meet evolving consumer expectations.

Product innovation and flavor expansion

Product innovation and new flavors are key drivers of growth in the global meat snacks market, as brands work to meet the changing preferences of consumers. This trend is largely driven by the growing demand for snacks that offer variety, global flavors, and a balance of indulgence and nutrition. For example, in 2025, Jack Link’s collaborated with PepsiCo’s Doritos to launch cool ranch chicken sticks, which combine the popular chip flavor with a protein-rich snack in a creative and convenient format. Similarly, in June 2025, Michelin-trained chefs behind the Carnal brand introduced umami cut beef jerky and black truffle and garlic beef sticks. These products bring a premium touch to meat snacks by incorporating high-end culinary techniques and unique flavors. Such innovations are transforming meat snacks into more exciting and indulgent options, appealing to a broader audience that seeks both taste and quality in their snacks.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Health concerns related to processed meat | -0.9% | Global, strongest in Europe and North America | Long term (≥ 4 years) |

| Consumer perception of price premium | -0.6% | Global, particularly price-sensitive emerging markets | Short term (≤ 2 years) |

| Sustainability and environmental concerns | -0.4% | Europe and North America, expanding globally | Long term (≥ 4 years) |

| Stringent regulatory and labeling requirements | -0.5% | Global, varying compliance complexity by region | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Health concerns related to processed meat

Health concerns about processed meat are becoming a major challenge for the meat snacks market. Studies, including those by the World Health Organization, have linked regular consumption of processed meats to higher risks of chronic diseases like colorectal cancer and type 2 diabetes. For example, a 2024 study by Eating Better Org found that eating just 50 grams of processed meat daily could increase the risk of type 2 diabetes by 30% and colorectal cancer by 26%[4]Source: Eating Better Org, "Processed meat and public health: Time for a change,", eating-better.org. These findings have led to stricter dietary guidelines, more public awareness, and a growing preference for cleaner, less processed options. To address these concerns, manufacturers are creating products with natural preservatives, lower sodium levels, and clearer labeling. In March 2025, Lorissa’s Kitchen launched a line of no-sugar-added, non-GMO meat snacks made from grass-fed beef, free from the top nine allergens, to meet the demand for healthier, safer protein snacks.

Consumer perception of price premium

High prices are a major challenge for the growth of the meat snacks market. While these snacks are promoted as high-protein, convenient, and nutritious, many consumers see them as too expensive compared to other snacks like chips or baked goods. This is especially true in markets where people are more price-sensitive or during tough economic times when shoppers focus on getting more for their money. The cost of using quality meat, clean-label ingredients, and premium packaging adds to the higher prices, making single-serve meat snacks less affordable for regular use. As a result, even though there is growing interest in healthier snacks, high prices can discourage people from trying or buying these products repeatedly, especially among lower- and middle-income groups.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Jerky Maintains Lead while Sticks Outpace Growth

In 2025, jerky dominated the meat snacks market with a 36.45% share, driven by its long-standing popularity and widespread availability in supermarkets, convenience stores. Its growth is further supported by innovations like grass-fed sourcing and resealable packaging that enhance convenience and impulse purchases. Companies have also introduced family-size bundles to offer better value, helping to maintain sales even as inflation impacts consumer spending. Brands keep consumers engaged by offering diverse flavors such as chili-lime, maple bourbon. Certifications like keto and paleo further attract health-conscious buyers, ensuring jerky remains a top choice in the market.

Meat sticks are expected to grow at the fastest rate among meat snack formats, with a projected CAGR of 7.09% from 2026 to 2031. Their growth is fueled by their portability, portion control, and flexible placement in locations like offices. The expansion of production facilities, such as Chomps’ new Missouri plant set to open in 2025, highlights the category's momentum and increasing demand. Other formats, including bars, sausages, and nuggets, are also gaining traction due to their high-protein appeal, though their growth will likely be slower than meat sticks. These formats contribute to a diverse product range that keeps consumers interested and reduces the risk of losing market share to non-protein snack alternatives.

By Source: Beef Dominates, Pork Accelerates

Beef remained the most preferred choice in the meat snacks market in 2025, contributing 48.10% of the total revenue. Its popularity stems from strong consumer demand, dependable supply chains, and its connection to grilling trends and high-protein diets. The rich flavor and familiarity of beef snacks make them a preferred choice among consumers across different regions. These snacks are versatile, fitting into various eating occasions, whether as a quick snack or a meal replacement. The established availability of beef products ensures a consistent supply, further strengthening its position in the market. This combination of taste, convenience, and accessibility has helped beef maintain its dominance in the meat snacks segment.

Pork is projected to grow the fastest among all meat sources, with an expected CAGR of 6.68% from 2026 to 2031. This growth is largely driven by its affordability and the rising demand for bold, regional flavors, particularly in the Asia-Pacific region. Pork snacks are increasingly popular as they cater to diverse taste preferences while offering a cost-effective protein option. Their ability to adapt to local flavor trends makes them appealing to a wide range of consumers. Meanwhile, poultry snacks continue to see steady growth due to their lean and healthy profile, which resonates with health-conscious buyers. Exotic meats are also gaining traction in niche markets, attracting premium consumers seeking unique and high-quality protein alternatives.

By Category: Conventional Still Rules, Organic Gains Traction

In 2025, conventional meat snacks dominated the market, contributing 87.40% of the total revenue. Their success is largely due to established livestock supply chains, which ensure consistent production and lower costs. These products are widely available in discount stores and mass-market retailers, making them accessible to a broad audience. The use of protein claims on packaging and the availability of private-label options have made them particularly attractive to cost-conscious consumers. This combination of affordability, accessibility, and effective marketing has solidified their leading position in the market.

Organic meat snacks are expected to grow rapidly, with a projected CAGR of 8.32% from 2026 to 2031, making them the fastest-growing category. This growth is driven by younger consumers who prioritize ethical sourcing, clean ingredients, and transparency in production. Although organic snacks currently hold a smaller share of the market, they offer higher profit margins and are gaining more shelf space in both mainstream and specialty stores. These factors enable brands to focus on innovation and sustainability, which appeal to health-conscious and environmentally aware buyers. As a result, organic meat snacks are steadily gaining popularity and carving out a niche in the market.

By Packaging Type: Pouches/Bags Lead, Boxes Rise

In 2025, pouches/bags were the leading packaging type in the global meat snacks market, accounting for 56.20% of total sales. These pouches are popular because they are lightweight, affordable, and easy to display on shelves using hang-tabs. They also come with features like resealable zippers and oxygen-barrier layers, which help keep the snacks fresh for longer without needing artificial preservatives. This makes them a great fit for the growing demand for clean-label products. Their transparent windows and modern designs allow consumers to see the product inside, making them more appealing and helping brands attract new customers.

Boxes are expected to grow the fastest, with a projected CAGR of 7.34% through 2031. This growth is driven by the increasing preference for bulk purchases among households and the popularity of club stores, where sturdy packaging is essential for long-distance shipping. Recent innovations, such as recyclable mono-material boxes, are also making these multipacks more attractive to eco-conscious consumers. These advancements not only enhance the packaging's sustainability but also improve its visual appeal, meeting the rising demand for environmentally friendly and preservative-free options in the market.

By Distribution Channel: Supermarkets/Hypermarkets Anchor, Online Retail Stores Surge

In 2025, supermarkets/hypermarkets made up 44.70% of the meat snacks sales, due to their ability to showcase products prominently and offer attractive multipack deals. These stores provide a wide variety of options, making them a convenient choice for many shoppers. Convenience stores also contributed significantly by driving impulse purchases, while specialty stores cater to customers who are willing to spend more for unique and high-quality products, adding diversity to the market.

Online retail stores are projected to grow at a strong 9.32% CAGR through 2031, making them the fastest-growing sales channel. The rise of digital shopping allows brands to reach customers in remote or underserved areas where physical stores are less accessible. Subscription-based models that offer directly to consumers are becoming popular, as they provide personalized flavor options and exclusive products, building customer loyalty. Advancements in cold-chain logistics and insulated shipping ensure that products remain fresh during delivery, especially in warmer regions, encouraging more consumers to shop online with confidence.

Geography Analysis

In 2025, North America dominated the global meat snacks market with a 44.90% share, driven by the region's strong preference for protein-rich diets and a well-established retail network. Strict United States Department of Agriculture (USDA) Food Safety and Inspection Service (FSIS) regulations ensure product safety, boosting consumer confidence. Trade agreements like the United States-Mexico-Canada Agreement (USMCA) have further reduced sourcing costs, making products more competitive. The rising consumption of beef, which is expected to reach 122 kg per capita by 2027, continues to support the market's growth. The region's diverse retail formats, including supermarkets, convenience stores, and online platforms, also contribute to its leading position.

The Asia-Pacific region is the fastest-growing market, with a projected CAGR of 8.92%, supported by urbanization, increasing disposable incomes, and the growing influence of Western snacking habits. Countries like China and India are emerging as high-growth markets due to their expanding middle-class populations and changing food preferences. Meanwhile, Japan and Australia maintain high-quality standards through strict food safety regulations, ensuring consumer trust. Efforts like ASEAN labeling harmonization are simplifying regional distribution, enabling companies to expand their presence across multiple countries. This combination of factors is driving significant growth in the region.

Europe offers both opportunities and challenges for the meat snacks market. The region faces regulatory hurdles, such as EU Regulation 1169/2011, which mandates detailed allergen and nutrition labeling, increasing compliance costs for manufacturers. However, the demand for premium and sustainable products remains strong, particularly in countries like Germany and the United Kingdom. Consumers in these markets are drawn to gourmet options and grass-fed sourcing, which align with their preferences for high-quality and environmentally friendly products. Despite the regulatory complexities, these factors are helping drive steady growth in the European market.

Competitive Landscape

The meat snacks market is moderately concentrated, indicating the dominance of established players like Conagra Brands, Hormel Foods Corporation, Tyson Foods Inc., among others. Companies are primarily expanding through strategic acquisitions to improve distribution and premium product offerings. For instance, in 2024, Conagra Brands acquired Sweetwood Smoke & Co. to enhance its portfolio of healthier meat snacks. These strategies aim to secure raw materials, improve automation, and gain shelf space, especially as markets like Asia-Pacific and online channels continue to grow.

Newer players are also making progress by using direct-to-consumer platforms, offering transparent ingredient lists, and targeting younger audiences with relatable messaging. Chomps, for example, has shown significant growth, supported by a new large-scale production facility that helps lower costs and speed up delivery. Plant-based meat snack startups, backed by venture capital, are entering the market with a focus on sustainability and innovative textures. Automation technologies, such as rotary vacuum packers, are helping companies reduce labor costs and improve food safety, giving advanced processors a competitive edge over traditional ones.

Changing regulations are increasing competition by enforcing stricter rules on labeling and food safety. Larger companies benefit from faster product rollouts using tools like generic-label approvals, while smaller firms often depend on specialized co-packers to meet compliance requirements. As consumers prioritize claims like grass-fed, nitrate-free, or carbon-neutral sourcing, supply-chain transparency has become essential for staying competitive. The market now features a mix of established processors, digital-first brands, and retail platforms, all competing to lead the protein-snack category through cleaner labels, faster innovation, and efficient operations.

Meat Snacks Industry Leaders

-

ConAgra Brands Inc.

-

Hormel Foods Corporation

-

Link Snacks, Inc.

-

Tyson Foods, Inc.

-

General Mills

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Jack Link's announced a groundbreaking global partnership with MrBeast (Jimmy Donaldson). This collaboration was intended to launch an exciting new line of protein-packed meat snack products.

- January 2025: Jack Link’s and Doritos have collaborated to introduce a new range of meat snacks inspired by the flavor of Doritos’ Sweet & Tangy Barbeque chips.

- August 2024: Conagra Brands acquired Sweetwood Smoke & Co., the maker of FATTY Smoked Meat Sticks, as part of its strategy to expand its portfolio of high-protein snack offerings. This acquisition aimed to strengthen Conagra's position in the growing meat snacks market by leveraging Sweetwood Smoke & Co.'s established brand and product line.

- January 2024: PepsiCo collaborated with Jack Link’s to launch Fritos-branded jerky, showcasing a strategic move to leverage cross-category branding. This partnership aimed to combine the strong brand equity of Fritos with the expertise of Jack Link’s in the meat snacks market, creating a unique product offering to attract a broader consumer base.

Global Meat Snacks Market Report Scope

Meat snacks are on-the-go food products that are made from different animal sources such as beef, turkey, poultry, and more. They are also available in a variety of pre-packaged formats, depending on preference. The meat snacks market is segmented by type, distribution channel, and geography. By type, the market is segmented by jerky, stick, sausage, and other product types. By distribution channel, the market is segmented into supermarkets/hypermarkets, convenience stores/grocery stores, online retail stores, and other distribution channels. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, the Middle East, and Africa. For each segment, the market sizing and forecasts have been done on the basis of value (in USD).

| Jerky |

| Meat Sticks |

| Sausages |

| Meat Bars |

| Nuggets |

| Other Product Types |

| Beef |

| Pork |

| Chicken/Poultry |

| Others |

| Organic |

| Conventional |

| Boxes |

| Cans and Jars |

| Pouches/Bags |

| Others |

| Supermarkets/Hypermarkets |

| Convenience and Grocery Stores |

| Online Retail Stores |

| Specialty Stores |

| Other Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Colombia | |

| Chile | |

| Peru | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Jerky | |

| Meat Sticks | ||

| Sausages | ||

| Meat Bars | ||

| Nuggets | ||

| Other Product Types | ||

| By Source | Beef | |

| Pork | ||

| Chicken/Poultry | ||

| Others | ||

| By Category | Organic | |

| Conventional | ||

| By Packaging Type | Boxes | |

| Cans and Jars | ||

| Pouches/Bags | ||

| Others | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Convenience and Grocery Stores | ||

| Online Retail Stores | ||

| Specialty Stores | ||

| Other Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Colombia | ||

| Chile | ||

| Peru | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the global meat snacks market?

The market stands at USD 22.02 billion in 2026 and is projected to reach USD 30.27 billion by 2031.

Which product format is growing fastest in meat snacks?

Meat sticks are forecast to post a 7.09% CAGR between 2026 and 2031, outpacing other formats.

Which region shows the highest growth momentum?

Asia-Pacific leads with a projected 8.92% CAGR through 2031, driven by urbanization and rising incomes.

How big is beef’s share in global meat snacks?

Beef products represented 48.10% of 2025 revenue and continue to dominate despite pork’s faster growth.

Page last updated on: