Extruded Snacks Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 67.95 Billion |

| Market Size (2031) | USD 84.56 Billion |

| Growth Rate (2026 - 2031) | 4.47% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

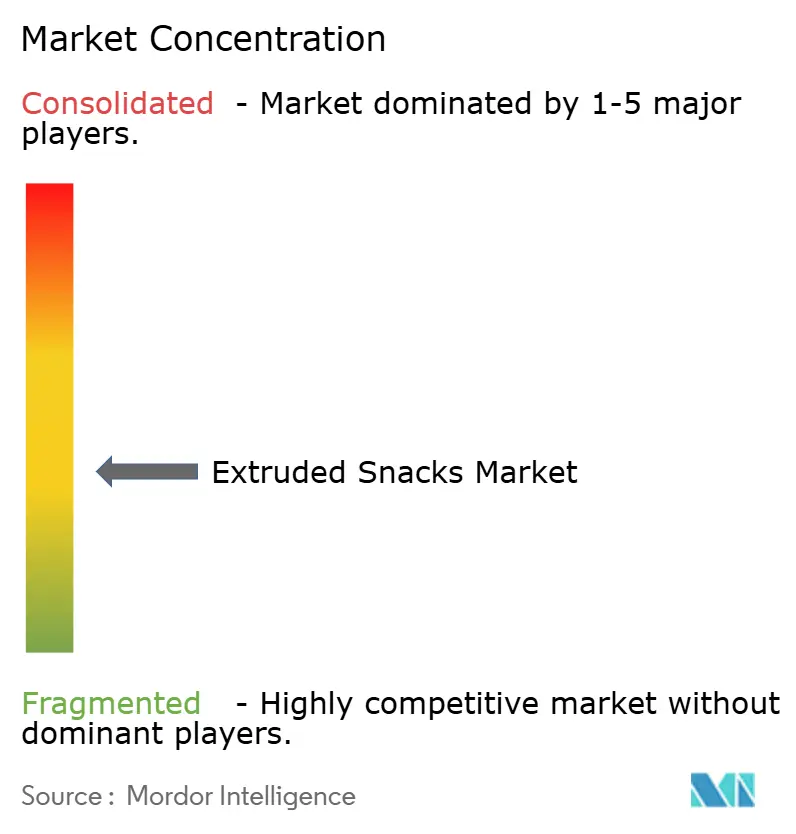

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Extruded Snacks Market Analysis by Mordor Intelligence

The extruded snacks Market size is projected to expand from USD 65.27 billion in 2025 and USD 67.95 billion in 2026 to USD 84.56 billion by 2031, registering a CAGR of 4.47% between 2026 and 2031. The market growth is driven by increasing consumer demand for convenient and healthier snacking options, particularly among urban populations with busy lifestyles. Technological advancements in extrusion processing have enabled manufacturers to develop innovative product textures, shapes, and flavors while maintaining nutritional value. The integration of alternative ingredients, such as whole grains, legumes, and vegetables, has expanded product offerings to meet diverse dietary preferences. The market growth is driven by regulatory changes that support sodium reduction through salt substitutes, particularly the U.S. Food and Drug Administration's proposed amendments to standards of identity regulations[1]Source: U.S. Food and Drug Administration, “Use of Salt Substitutes in Standardized Foods,” fda.gov. These regulations have prompted companies to reformulate their products, focusing on better-for-you options without compromising taste. Additionally, the market benefits from improved distribution networks and retail penetration, making extruded snacks more accessible to consumers across various regions.

Key Report Takeaways

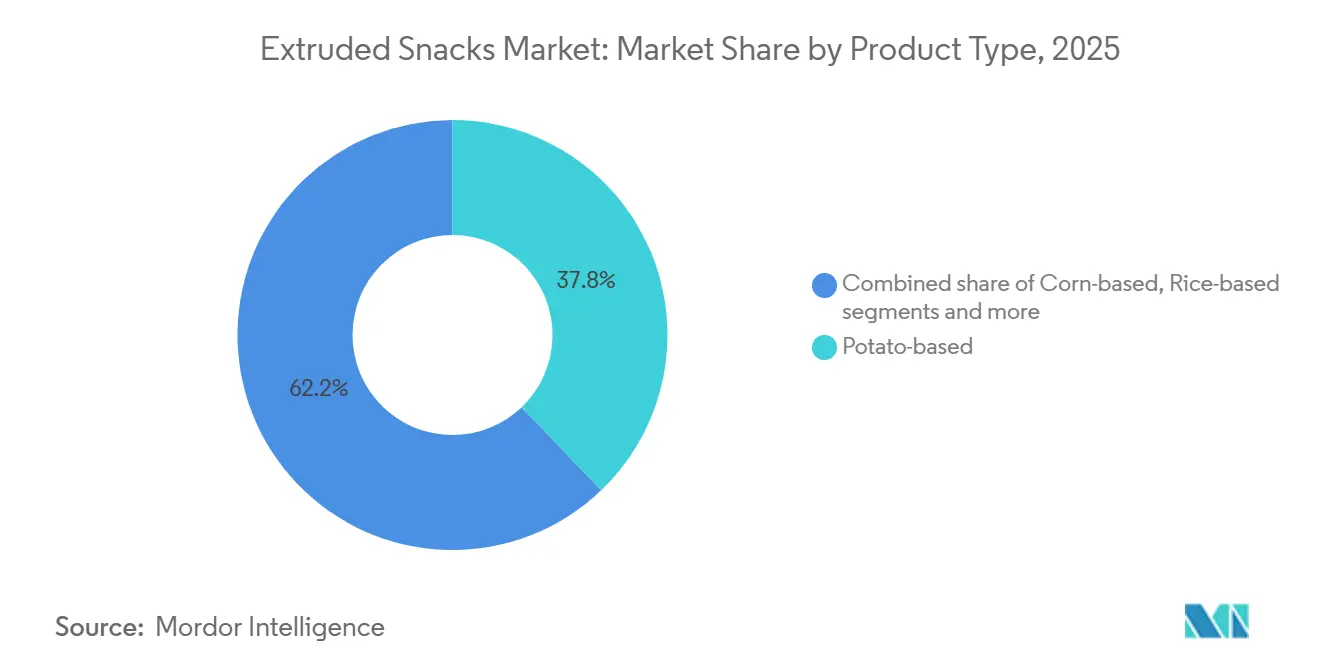

- By product type, potato-based snacks dominated the extruded snacks market with a 37.83% share in 2025, while multigrain formats are expected to grow at a 5.67% CAGR through 2031.

- By the extrusion process, hot extrusion held an 82.13% market share in 2025, with cold extrusion projected to grow at a 6.12% CAGR during 2025-2031.

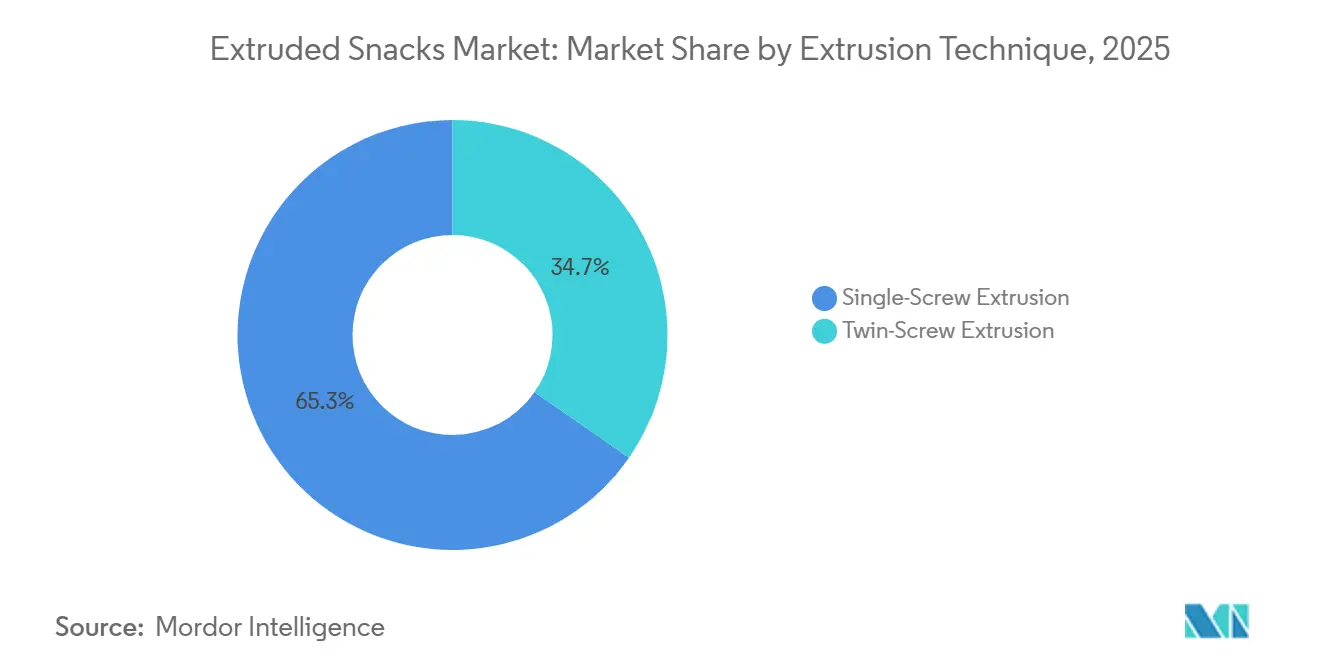

- By extrusion technique, single-screw extrusion represented 65.33% of the extruded snacks market size in 2025, while twin-screw extrusion is expected to grow at a 6.37% CAGR through 2031.

- By distribution channel, supermarkets/hypermarkets generated 56.13% of revenue in 2025, with online retail projected to grow at a 6.55% CAGR through 2031.

- By geography, Europe held 32.45% of the market value in 2025, while Asia-Pacific is anticipated to grow at a 6.69% CAGR during the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Extruded Snacks Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for convenient RTE snacks | +1.2% | Global, with stronger penetration in North America and Europe | Medium term (2-4 years) |

| Health-centric reformulation (low-oil, baked) | +0.8% | North America and Europe leading, Asia-Pacific following | Long term (≥ 4 years) |

| Launch of novel and innovative flavors and textures | +0.6% | Global, with regional flavor preferences driving localization | Short term (≤ 2 years) |

| Growing demand for premium and gourmet snacks | +0.4% | Europe and North America core, expanding to urban Asia-Pacific | Medium term (2-4 years) |

| Twin-screw technology enabling high-protein/fiber snacks | +0.7% | Global, with early adoption in developed markets | Long term (≥ 4 years) |

| Direct-to-consumer micro-brands scaling via e-commerce | +0.5% | North America and Europe leading, Asia-Pacific emerging | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing demand for convenient RTE snacks

The shift from traditional meals to snacks is changing consumption patterns across age groups. Busy lifestyles increase the demand for portable, shelf-stable options that offer both convenience and nutrition. This trend spans age groups, from millennials to those over 60, who seek nutritious and functional ingredients in their snacks. Extrusion technology produces a variety of textures and incorporates nutritional elements, making it an effective manufacturing method. The process helps manufacturers produce snacks with longer shelf life while maintaining taste and texture, meeting the market's demand for convenient options. Extruded snacks are portable, affordable, and available in a wide range of flavors, making them ideal for on-the-go consumption. Urbanization and rising modern retail penetration are further boosting accessibility and impulse purchases of convenient RTE snacks.

Health-centric reformulation driving low-oil, baked innovations

Manufacturers use advanced extrusion techniques to reduce oil content while maintaining texture and flavor, meeting consumer demand for healthier snacks. Twin-screw extrusion technology provides better control over moisture content and mechanical energy, enabling production of baked snacks with lower oil absorption. This technology helps create products with clean labels and transparent ingredient lists. Studies show that adding wheat bran fiber (125 grams per kilogram) improves texture and nutritional value, helping manufacturers develop products for health-conscious consumers. Manufacturers also focus on sodium reduction, using salt alternatives to meet U.S. Food and Drug Administration voluntary targets while preserving taste.

Launch of novel and innovative flavors and textures

Manufacturers gain competitive advantages by creating unique sensory experiences through flavor innovation and texture differentiation. Extrusion technology enables the development of complex flavor profiles and textures that traditional processing methods cannot achieve. The integration of natural medicinal and edible plants through extrusion cooking improves functional properties and sensory characteristics, as research demonstrates increased polysaccharide content and enhanced antioxidant activities after processing. This allows manufacturers to meet consumer demand for functional foods while maintaining broad market appeal. The growing popularity of ethnic and regional flavors, especially in Asia-Pacific markets, presents opportunities for local product development using extrusion's adaptability to various ingredients.

Growing demand for premium and gourmet snacks

Consumer preference for premium products with superior quality, unique ingredients, and artisanal characteristics enables manufacturers to expand profit margins. Manufacturers can capitalize on this trend by positioning their extruded products in premium segments while maintaining efficient production processes. The use of extrusion technology to incorporate ancient grains, plant-based proteins, and functional ingredients allows companies to develop premium-priced products that meet health and sustainability requirements. European markets demonstrate strong adoption of this trend, with organic ingredients and sustainability certifications becoming important product differentiators. Manufacturers must maintain consistent product quality through precise process control while effectively communicating their value proposition to succeed in premium segments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High sodium and additive perceptions | -0.6% | Global, with heightened sensitivity in North America and Europe | Medium term (2-4 years) |

| Volatile raw-material costs | -0.4% | Global, with particular impact on emerging markets | Short term (≤ 2 years) |

| Stringent regulatory and compliance requirements | -0.3% | North America and Europe leading, expanding globally | Long term (≥ 4 years) |

| High competition from alternative snacks | -0.2% | Global, with intensifying competition in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High sodium and additive perceptions

Growing consumer awareness about sodium's health effects presents challenges for traditional extruded snack formulations, especially as regulatory bodies strengthen reduction targets. The U.S. Food and Drug Administration's Phase II voluntary sodium reduction goals seek to lower average daily intake from 3,400 mg to 2,750 mg, requiring manufacturers to modify product formulations while preserving taste [2]Source: U.S. Food and Drug Administration, “Sodium Reduction in the Food Supply,” fda.gov. This challenge intensifies due to consumers' concerns about additives and preservatives in extruded snacks. The regulatory environment supports innovation through proposed amendments that permit salt substitutes in standardized foods, offering manufacturers options to reduce sodium while maintaining product functionality. The reformulation process requires substantial research and development investment, which may affect short-term profitability as companies work to develop healthier products.

Volatile raw-material costs

The extruded snacks industry faces significant challenges from fluctuating commodity prices, particularly corn, wheat, and oil, which directly affect production costs. The snacks category experienced inflation for overall food products, creating an environment where manufacturers must carefully manage costs while considering consumer price sensitivity. This price volatility especially impacts smaller manufacturers who have limited purchasing power and hedging capabilities compared to larger companies. Supply chain disruptions and geopolitical tensions further compound these challenges by affecting agricultural commodity markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Potato-Based Dominance Faces Multigrain Challenge

Potato-based extruded snacks hold 37.83% of the market share in 2025, maintaining their dominant position through established supply chains and efficient large-scale production capabilities. Multigrain variants are growing at 5.67% CAGR through 2031, as consumers increasingly prefer products with perceived nutritional benefits. Corn-based snacks hold a significant share due to their flavor adaptability and cost efficiency, while rice-based products serve gluten-sensitive consumers. Tapioca-based snacks maintain a specialized presence, primarily in Asian markets where the ingredient has traditional significance and processing advantages.

Twin-screw extrusion technology enables the development of protein-rich formulations, as manufacturers incorporate plant proteins to improve nutritional content. Studies show that sorghum-based extrudates combined with whey protein isolate exhibit higher expansion ratios than soy flour variants, helping manufacturers optimize their formulations. The "others" segment, which includes legume-based and alternative grain formulations, shows significant growth as manufacturers develop new ingredients to differentiate their products and target health-conscious consumers seeking functional benefits.

By Extrusion Process: Hot Extrusion Dominance Challenged by Cold Innovation

Hot extrusion holds 82.13% market share in 2025, due to its proven efficiency in creating expanded textures and flavors in traditional extruded snacks. The process effectively gelatinizes starches and creates desired puffing characteristics essential for mainstream product categories. Cold extrusion is growing at 6.12% CAGR through 2031, driven by its energy efficiency and better retention of heat-sensitive nutrients, appealing to health-conscious consumers. This technology is particularly effective in processing protein-rich formulations where high temperatures can degrade nutrients and affect functionality.

The market dynamics between hot and cold extrusion technologies reflect industry shifts toward sustainability and nutrition optimization. Cold extrusion requires less energy, supporting manufacturers' sustainability goals while enabling the use of functional ingredients that high-temperature processing would damage. The technology preserves bioactive compounds and protein functionality, making it suitable for premium and functional snack production. Manufacturers investing in cold extrusion equipment aim to serve consumers who value both health benefits and environmental impact in their purchase decisions.

By Extrusion Technique: Twin-Screw Technology Drives Innovation

Single-screw extrusion holds 65.33% of the market share in 2025, due to its lower capital requirements and operational simplicity, making it attractive to cost-conscious manufacturers. The technology's reliability and established supply chains make it the preferred choice for traditional snack production where product requirements are straightforward. Twin-screw extrusion accounts for 34.67% of current capacity and grows at 6.37% CAGR through 2031, owing to its enhanced mixing capabilities and precise processing control. This technology allows manufacturers to incorporate proteins, fibers, and functional additives while ensuring consistent product quality.

Twin-screw systems demonstrate technological advantages in high-protein and fiber-enriched formulations by enabling precise ingredient distribution and processing control. Twin-screw extrusion allows manufacturers to produce snacks containing up to 24.94% protein while maintaining consumer acceptance, creating opportunities in the protein snack market. The technology accommodates diverse ingredient combinations and processing conditions, making it suitable for manufacturers developing nutritionally enhanced products. Companies targeting premium and health-focused markets increasingly invest in twin-screw capabilities to meet consumer demands.

By Distribution Channel: Online Retail Disrupts Traditional Channels

Supermarkets/hypermarkets hold 56.13% market share in 2025, maintaining their dominance in mainstream snack categories through extensive reach and established manufacturer relationships. Convenience stores constitute a significant share of the distribution channel, capitalizing on impulse purchases and strategic locations for on-the-go consumption. Online retail stores demonstrate the highest growth rate at 6.55% CAGR through 2031, as direct-to-consumer micro-brands utilize e-commerce platforms to expand operations and target specific consumer segments. Specialty stores focus on premium and health-oriented products, differentiating through expert staff and selective product offerings.

E-commerce channels are transforming the competitive environment by enabling smaller brands to challenge established companies through direct distribution. Direct-to-consumer models increase manufacturer margins while fostering consumer relationships and enabling quick product adjustments based on market feedback. Online purchasing continues to grow following pandemic-driven acceleration, as consumers value convenience and expanded product selection through digital platforms. Traditional retailers are adapting by developing omnichannel capabilities and establishing partnerships with emerging brands to maintain their market position.

Geography Analysis

Europe holds the largest regional market share at 32.45% in 2025, driven by consumer preferences for premium and artisanal snack products. The region's sustainability framework, including the EU's Farm to Fork strategy and circular economy action plan, benefits manufacturers who demonstrate environmental responsibility in their operations and product formulations. European consumers' preference for organic and sustainably produced snacks supports market value growth despite moderate volume expansion.

Asia-Pacific exhibits the fastest growth rate at 6.69% CAGR through 2031, driven by urbanization, increasing disposable incomes, and changing consumer preferences in China and India. The region's population size and growing adoption of Western snacking habits create opportunities for manufacturers who adapt products to regional tastes and price sensitivity. China's middle-class expansion and India's young population increase demand for convenient, branded snacks offering quality and flavor innovation. The region's manufacturing advantages and infrastructure development support both domestic and export markets.

North America represents an established market with strong competition and consumer demand for health-conscious and premium products. The region's snacking culture and high consumption rates ensure consistent demand, while regulations on sodium content and clean labeling influence product development. The 2024 IFIC Food & Health Survey indicates 73% of Americans snack at least once daily [3]Source: International Food Information Council, “2024 IFIC Food & Health Survey,” ific.org. The United States leads regional consumption, with consumers seeking products that meet specific dietary requirements, including plant-based, gluten-free, and high-protein options.

Competitive Landscape

The extruded snacks market exhibits moderate fragmentation, creating opportunities for both established multinational corporations and emerging regional players to compete effectively. This competitive structure reflects the industry's diverse product categories, distribution channels, and geographic markets that prevent any single player from achieving dominant market control. Major players, including PepsiCo Inc., Shearer's Foods, LLC, ITC Limited, and Intersnack Group, leverage scale advantages in procurement, manufacturing, and distribution, while smaller companies compete through innovation, niche positioning, and direct-to-consumer strategies.

Technology adoption patterns reveal strategic differentiation opportunities, with companies investing in twin-screw extrusion capabilities to enable high-protein and functional ingredient incorporation that commands premium pricing. Patent filings in extrusion technology demonstrate ongoing innovation, particularly in protein processing methods that address traditional challenges in whey protein extrusion through controlled acidification processes.

Companies that combine efficient manufacturing processes with accelerated product development cycles gain significant competitive advantages in the market. This integration allows them to swiftly adapt their product offerings to emerging consumer preferences and evolving regulatory requirements. White-space opportunities exist in plant-based protein snacks, ethnic flavor profiles, and sustainable packaging solutions that align with evolving consumer values and regulatory mandates.

Extruded Snacks Industry Leaders

PepsiCo, Inc.

Shearer's Foods, LLC

ITC Limited

Intersnack Group

Mars, Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: The Hershey Company acquired LesserEvil, a maker of organic snacks including popcorn made with avocado oil and organic corn rings. This acquisition expands Hershey's portfolio in the better-for-you snack category and enhances its manufacturing capabilities in organic products.

- January 2025: Ferrero Group announced its agreement to acquire Power Crunch, a protein snacks brand from Bio-Nutritional Research Group, expanding its presence in the high-growth protein snack market. The acquisition includes Power Crunch's complete product lineup of protein bars and crisps.

- August 2024: Mars Incorporated agreed to acquire Kellanova for USD 35.9 billion, marking one of the largest food industry deals in recent years. The acquisition aims to enhance Mars' sustainable snacking business and expand its portfolio of global brands including Pringles and Cheez-It.

Global Extruded Snacks Market Report Scope

The Extruded Snacks Market Report is Segmented by Product Type (Potato-Based, Corn-Based, Rice-Based, Tapioca-Based, Multigrain, Others), Extrusion Process (Hot Extrusion, Cold Extrusion), Extrusion Technique (Single-Screw Extrusion, Twin-Screw Extrusion), Distribution Channel (Supermarkets/Hypermarkets, Convenience Stores, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Potato-based |

| Corn-based |

| Rice-based |

| Tapioca-based |

| Multigrain |

| Others |

| Hot Extrusion |

| Cold Extrusion |

| Single-Screw Extrusion |

| Twin-Screw Extrusion |

| Supermarkets/Hypermarkets |

| Convenience Stores |

| Online Retail Stores |

| Specialty Stores |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Potato-based | |

| Corn-based | ||

| Rice-based | ||

| Tapioca-based | ||

| Multigrain | ||

| Others | ||

| By Extrusion Process | Hot Extrusion | |

| Cold Extrusion | ||

| By Extrusion Technique | Single-Screw Extrusion | |

| Twin-Screw Extrusion | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Online Retail Stores | ||

| Specialty Stores | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the extruded snacks market?

The extruded snacks market size stands at USD 65.27 billion in 2025 and is projected to reach USD 84.56 billion by 2031.

Which product segment leads the market?

Potato-based snacks lead with 37.83% of 2025 value, although multigrain variants are the fastest-growing at a 5.67% CAGR.

Why is twin-screw extrusion gaining traction?

Twin-screw systems enable higher protein and fiber incorporation, support cleaner labels and are forecast to expand at a 6.37% CAGR through 2031.

Which region is expected to grow the fastest?

Asia-Pacific is projected to advance at a 6.69% CAGR, driven by urbanization and income growth across China and India.

Page last updated on: