Baked Savoury Snacks Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

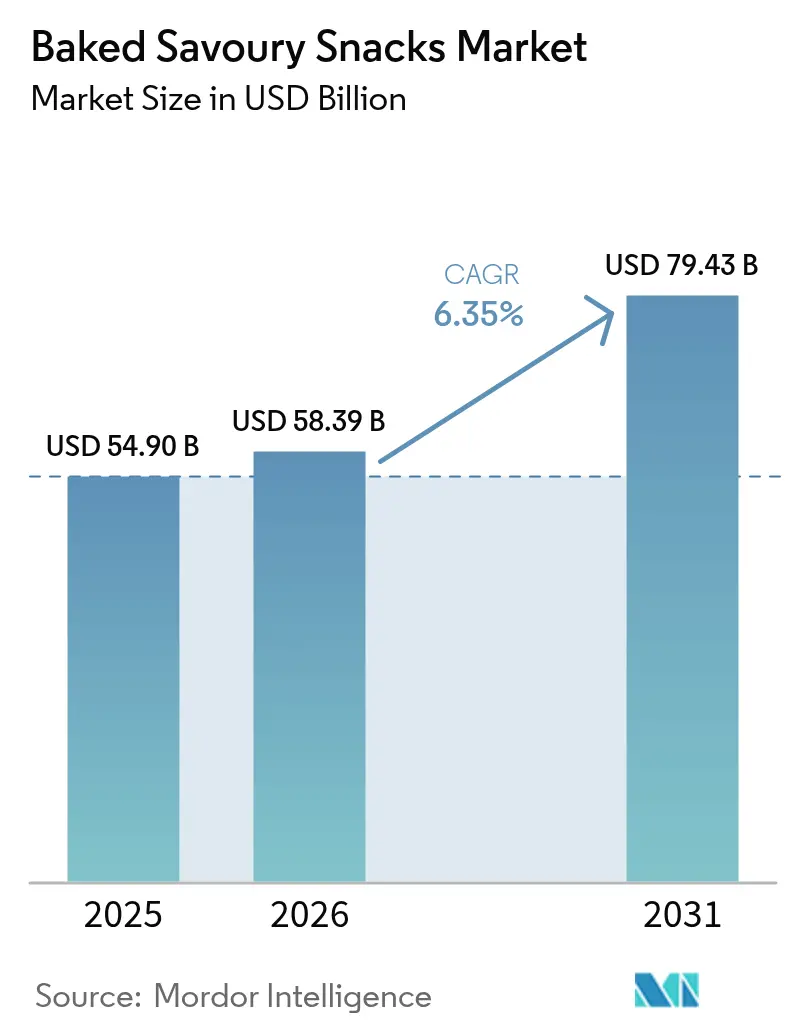

| Market Size (2026) | USD 58.39 Billion |

| Market Size (2031) | USD 79.43 Billion |

| Growth Rate (2026 - 2031) | 6.35% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Baked Savoury Snacks Market Analysis by Mordor Intelligence

The baked savoury snacks market size is expected to grow from USD 54.90 billion in 2025 to USD 58.39 billion in 2026 and is forecast to reach USD 79.43 billion by 2031 at 6.35% CAGR over 2026-2031. A notable shift is occurring as consumers pivot from fried to baked snacks, drawn by their lower fat content, cleaner labels, and retailer incentives promoting healthier choices. The growing urban lifestyles in the Asia-Pacific region are driving demand for baked savory snacks, as busy schedules lean towards portable and shelf-stable products. Meanwhile, North America is spearheading this trend, with retailers now considering reduced-oil offerings as standard. Ingredient innovation is becoming a game-changer: the introduction of multigrain blends, upcycled pulses, and probiotics not only commands premium pricing but also shields brands from the encroachment of private labels. Furthermore, e-commerce subscriptions and direct-to-consumer channels are revolutionizing the market, ensuring repeat purchases, slashing slotting costs, and accelerating innovation cycles from 18 months down to a mere six.

Key Report Takeaways

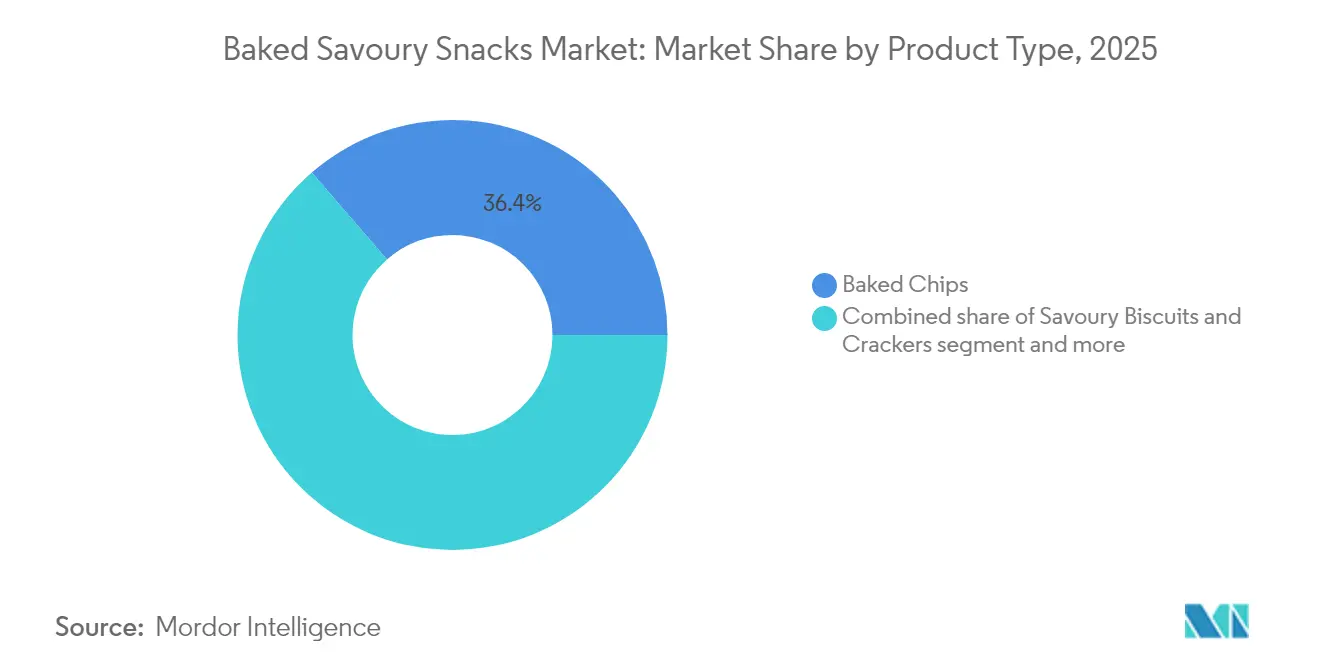

- By product type, baked chips held 36.36% of the baked savoury snacks market share in 2025, while savoury biscuits and crackers are expanding at a 7.46% CAGR through 2031.

- By ingredient base, wheat represented 42.34% of the market share in 2025, yet multigrain blends are growing at a 7.55% CAGR.

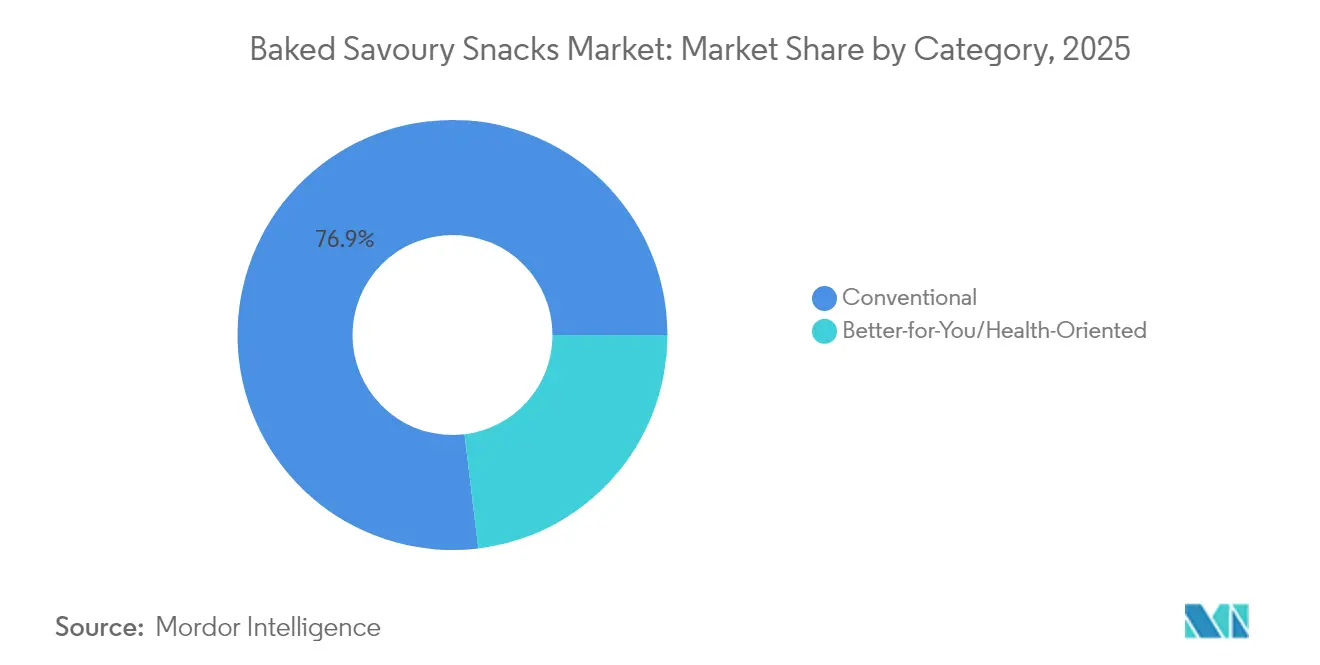

- By category, conventional products commanded 76.92% of market share in 2025, whereas the better-for-you segment is rising at an 8.31% CAGR.

- By distribution channel, supermarkets and hypermarkets captured 54.49% of market share in 2025, yet online retail is advancing at a 9.45% CAGR.

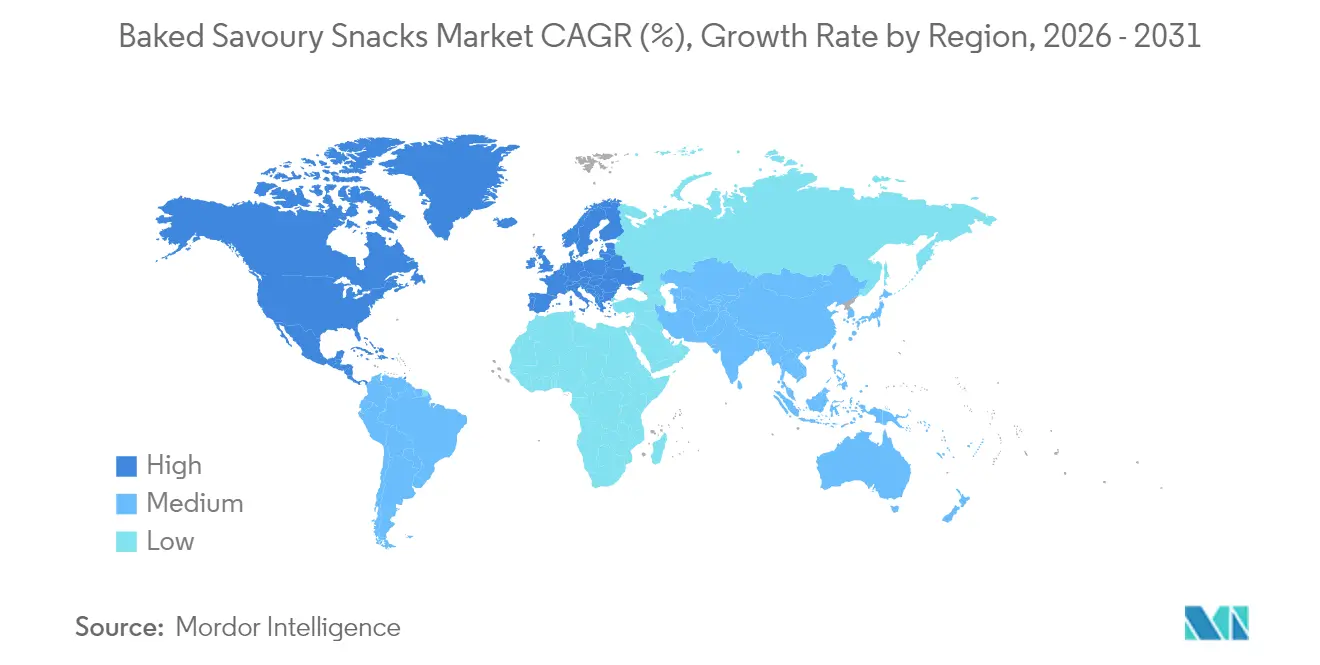

- By geography, Asia-Pacific accounted for 35.23% of market share in 2025, while North America posts the fastest regional CAGR at 8.12% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Baked Savoury Snacks Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising consumer preference for healthier baked over fried snacks | +1.2% | Global, with North America and Europe leading adoption | Medium term (2-4 years) |

| Flavor and format innovation appealing to Millennials and Gen Z | +1.0% | Global, particularly strong in North America, Asia Pacific urban centers | Short term (≤ 2 years) |

| Expansion of e-commerce and DTC distribution | +0.9% | North America, Europe, Asia Pacific tier-1 cities | Short term (≤ 2 years) |

| On-the-go lifestyles are driving single-serve demand | +0.8% | Global, with Asia Pacific and North America showing the highest growth | Medium term (2-4 years) |

| Hybrid infrared baking ovens enhance texture and throughput | +0.5% | North America, Europe, select Asia Pacific manufacturers | Long term (≥ 4 years) |

| Up-cycled grains/legumes aligned with corporate ESG goals | +0.4% | North America, Europe, with spillover to the Asia Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising consumer preference for healthier baked over fried snacks

As obesity rates in OECD countries hover above 25%, governments are incentivizing reformulation through tax breaks and front-of-pack labeling schemes. The UK Government, in 2024, refreshed its voluntary salt-reduction targets, favoring baked formats that achieve flavor intensity through fermentation and enzyme treatments over sodium loading[1]Source: Department for Environment, Food & Rural Affairs, “Reducing Salt in Food,” gov.uk. PepsiCo's Off The Eaten Path line, leveraging chickpea and lentil bases, saw double-digit volume growth in North America in 2024. This surge underscores the potency of health positioning, even among price-sensitive consumers. Baked products offer a supply-chain edge: they need 20-30% less oil per kilogram, shielding manufacturers from the vegetable-oil price fluctuations that squeezed fried-snack margins in 2024. Retailers are capitalizing on this trend, dedicating more shelf space to healthier SKUs. This move pressures traditional fried brands to either reformulate or make way for the rising baked contenders.

Flavor and format innovation appealing to millennials and Gen Z

Today's younger consumers are redefining snacks, viewing them more as meal replacements than mere indulgences. This shift has heightened their expectations, emphasizing protein density, diverse global flavors, and packaging that's as visually appealing as it is functional. In tune with this trend, Mondelez rolled out its Ritz Crisp and Thins in sriracha-lime and miso-sesame flavors in 2024. Within just six months, these variants found their way into over 15,000 stores across North America. The new format is not only thinner and crunchier but also portion-controlled, addressing a unique challenge: while Gen Z seeks indulgence, they also rely on brands to manage portion sizes, effectively delegating self-control to packaging. Reflecting changing consumption patterns solidified by the pandemic, single-serve packs have carved out a significant share of baked-snack sales in North America. Moreover, flavor innovation isn't just about taste; it's a strategic move. Limited-edition SKUs create a social media stir, driving trials without the need for ongoing marketing expenses. This approach was notably employed by Kellanova with its Pringles Mingles line, which artfully combines sweet and savory notes to attract a diverse range of snack enthusiasts.

Expansion of E-commerce and DTC distribution

In 2024, online channels captured around 12% of baked-snack sales. However, with a projected CAGR of 9.91% through 2030, it's evident that marketing budgets are increasingly shifting towards digital channels for both acquisition and retention. Subscription models, like Graze's curated snack boxes and PepsiCo's PantryShop platform, are not just turning one-time buyers into loyal customers but also gathering valuable zero-party data. This data plays a crucial role in shaping SKU development and refining inventory planning. Direct-to-consumer (DTC) sales present a lucrative opportunity: while gross margins can outpace those of traditional retail, the challenge lies in high customer-acquisition costs, especially without the advantage of physical product trials. E-commerce is revolutionizing product innovation; brands can swiftly introduce niche flavors or functional claims, such as added collagen or adaptogens, bypassing the hurdles of shelf space negotiations or minimum order quantities. This agility has shortened innovation cycles from 18 months to just 6. On the regulatory front, the EU's Digital Services Act, coming into full effect in 2024, is pushing for transparent ingredient disclosures for online-only SKUs[2]Source: European Commission, “Digital Services Act,” europa.eu . This move aims to create a level playing field, bridging the gap between digital-native brands and established omnichannel players.

On-the-go lifestyles driving single-serve demand

Urbanization and hybrid work models have reshaped eating habits, with many North Americans now snacking at least three times a day. For example, a 2025 survey by the International Food Information Council found that most U.S. respondents snacked daily, with around 12% indulging three or more times in addition to their main meals. Single-serve formats, typically weighing 25-35 grams, cater to this trend, easily fitting into commuter bags, gym lockers, and desk drawers, and turning any location into a potential eating spot. This trend is especially pronounced in the Asia Pacific region. In cities like Tokyo, Singapore, and Shanghai, metro-system vending machines now offer baked-chip multipacks alongside traditional sweets, highlighting transit authorities' understanding that longer dwell times can lead to impulse buys. In response, manufacturers have developed resealable single-serve packs that keep snacks crisp for 48 hours after opening. Achieving this required a shift from oriented polypropylene to metallized polyester laminates. This innovation not only enhances product appeal but also shields brands from private-label competition. Retailers find it hard to justify the tooling costs for single-serve SKUs, especially when established brands already dominate the segment, creating a unique advantage in a typically commoditized market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-material cost volatility (wheat, oils) | -0.7% | Global, with Europe and North America most exposed | Short term (≤ 2 years) |

| Private-label and cross-category competition | -0.6% | Europe, North America, with emerging pressure in the Asia Pacific | Medium term (2-4 years) |

| Tightening acrylamide limits (EU/California) raises compliance costs | -0.5% | Europe, California, with potential spillover to other United States’s states | Medium term (2-4 years) |

| Shelf-life hurdles for clean-label formulations | -0.4% | Global, particularly acute in emerging markets with limited cold-chain infrastructure | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Tightening acrylamide limits raise compliance cost

Starting January 2024, the European Commission has set new benchmark levels for acrylamide in potato crisps and cereal-based snacks. The permissible concentration has been reduced from 750 µg/kg to 500 µg/kg[3]Source: European Commission, “Commission Regulation on Acrylamide,” europa.eu. This change pushes manufacturers to adopt asparagine-reducing enzymes and alter their baking methods. At the same time, California's Proposition 65 has tightened its "safe harbor" threshold. Now, products with more than 140 µg per daily serving must carry warning labels. This threshold is particularly challenging, as many standard baked chips exceed it without any reformulation. Compliance presents a financial disparity: while global giants like PepsiCo and Kellanova can spread the costs of enzyme licensing and pilot-plant trials across their worldwide operations, local producers grapple with costs that significantly impact their already narrow profit margins. The crux of the challenge is achieving acrylamide reduction without compromising taste. Techniques like lowering baking temperatures or reducing dwell times can decrease acrylamide levels by 40%. However, these methods often diminish the Maillard-reaction compounds, which are essential for that sought-after roasted flavor. As a result, reformulation teams are turning to yeast extracts or fermented ingredients, leading to an 8-12% increase in raw material costs.

Shelf-life hurdles for clean-label formulations

Removing synthetic preservatives like BHA, BHT, and TBHQ shortens shelf life from 12 months to 6-9 months. This reduction disrupts distribution economics in markets where retailers mandate a minimum of 180 days of shelf life upon delivery. While natural alternatives such as rosemary extract and mixed tocopherols provide some respite, they fall short of the broad-spectrum efficacy offered by synthetic antioxidants. This is especially evident in high-fat baked goods, where lipid oxidation hastens rancidity. High-pressure processing (HPP) can enhance microbial stability without the use of heat. However, its capital-intensive nature limits adoption to large-scale producers, creating a competitive divide between multinational and regional players. This challenge is pronounced in the Asia Pacific and Latin America regions. Here, ambient distribution is standard, and cold-chain infrastructure services less than 30% of retail outlets. Brands unable to ensure a 9-month shelf life at 30°C lose access to rural and peri-urban channels, which account for 40% of the regional volume. Some manufacturers are turning to modified-atmosphere packaging (MAP), which substitutes oxygen with nitrogen or carbon dioxide to prolong shelf life. However, the added packaging costs can squeeze margins in price-sensitive markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Chips Lead, Crackers Accelerate

Savoury biscuits and crackers are set to grow at a rate of 7.46% through 2031, outpacing baked chips, which held a 36.36% market share in 2025. This growth is attributed to manufacturers incorporating functional ingredients, like plant protein, omega-3s, and prebiotics, into crackers, which consumers already view as a wholesome snack. Kellanova's Cheez-It Snap'd line, launched in late 2023, achieved USD 200 million in retail sales in its inaugural year. By blending whole-grain bases with bold flavors such as jalapeño jack and double cheese, Kellanova demonstrated that premiumization and indulgence can harmoniously coexist. While baked chips dominate in volume due to established distribution and consumer familiarity, their pace of innovation has lagged behind that of crackers. This stagnation suggests a potential market saturation and increasing susceptibility to competition from private labels.

Pretzels, extruded snacks, popcorn, and tortilla chips cater to diverse occasions and taste preferences. Praised for their lower fat content, 1-2 grams per serving compared to chips' 5-7 grams, pretzels have gained traction in school lunch programs, aligning with nutritional guidelines that emphasize sodium-reduced, whole-grain options. Extruded snacks, often made from corn or rice, captivate younger audiences with their playful shapes and bold seasonings. However, the high-temperature extrusion process can elevate acrylamide levels, incurring additional costs for necessary post-extrusion treatments. Popcorn is recognized as the only inherently healthy baked savoury snack. Yet, its bulkiness and fragility complicate single-serve packaging, limiting its appeal in the on-the-go market. Tortilla chips are experiencing a renaissance, with manufacturers transitioning from traditional corn to premium bases like cassava, chickpea, and black bean. These premium alternatives not only fetch higher prices but also align with the gluten-free and plant-based trends. While this segment faces limited regulatory scrutiny, the FDA's 2024 clarification on "whole grain" definitions has prompted reformulations in crackers and pretzels, ensuring they uphold their front-of-pack claims.

By Ingredient Base: Multigrain Gains on Wheat Dominance

In 2025, wheat accounted for 42.34% of ingredient volume, thanks to its cost efficiency, neutral flavor, and established supply chains. However, multigrain formulations are on the rise, growing at a rate of 7.55%. Brands are emphasizing nutrient-density claims alongside taste and texture. General Mills' Cascadian Farm Organic Crunch Bars, which feature a blend of oats, quinoa, and amaranth, saw an 18% year-over-year growth in 2024. This highlights consumers' willingness to pay a 20-30% premium for ancient grains, especially when paired with organic certification. The shift in ingredient preference also underscores supply-chain diversification. Wheat prices surged by 18% in early 2024 due to disruptions in Black Sea exports. In response, procurement teams began hedging their exposure, turning to corn, rice, and pulses sourced from a wider geographical range. Corn-based snacks, holding an estimated 28% market share, benefit from North America's surplus production and a robust extrusion infrastructure. However, their appeal is somewhat limited among diabetic and pre-diabetic consumers, an increasingly significant market, due to the snacks' glycemic index.

Rice continues to be a staple in Asia Pacific formulations, driven by cultural familiarity and its gluten-free attributes. Yet, its water-intensive cultivation is facing scrutiny. ESG-focused institutional investors are pressuring food companies to cut down on Scope 3 emissions. In 2024, Calbee, Japan's leading snack producer, pledged to source 30% of its rice from regenerative-agriculture pilots by 2027. While this commitment might inflate raw-material costs by 5-8%, it strategically aligns the brand with younger consumers who value environmental stewardship. Brands using multigrain blends, like wheat, oats, flax, and chia, can tout benefits like "good source of fiber" or "contains omega-3s". This sidesteps the regulatory complexities of fortification, which often mandates pre-market notification in many jurisdictions, including the FDA. The choice of ingredients also shapes manufacturing processes. While wheat and corn can endure high-shear mixing and extrusion, ancient grains such as teff and sorghum need gentler handling to maintain their nutrient profiles. This often leads to the adoption of hybrid baking protocols, sequencing infrared and convection heating to hit desired moisture levels.

By Category: Better-for-You Narrows the Gap

In 2025, conventional products dominated sales with a 76.92% share. However, the "better-for-you" segment, boasting an 8.31% CAGR projected through 2031, is poised to narrow that gap. This shift underscores a strategic conundrum: while conventional SKUs benefit from economies of scale and ingredient simplicity, yielding higher absolute margins, their "better-for-you" counterparts command price premiums. These premiums not only offset the elevated input costs but also account for their shorter shelf lives. PepsiCo's portfolio exemplifies this tension: its Lay's Baked line, positioned conventionally, boasts three times the unit volume of the "better-for-you" Off The Eaten Path range. Yet, thanks to a 25% retail-price premium, the latter enjoys a per-unit profitability that's 40% higher. Retailers are further fueling this transition, dedicating end-cap displays and promotional slots to "better-for-you" SKUs. Through temporary price reductions, they're effectively subsidizing trials and narrowing the premium gap.

The "better-for-you" category is diversifying into sub-segments: reduced-sodium, high-protein, gluten-free, organic, and non-GMO. Each sub-segment targets distinct consumer groups with varying price sensitivities. Reduced-sodium variants, which typically reduce salt content by 25-30%, cater to hypertensive consumers and align with government-backed reformulation initiatives. However, they face challenges in taste acceptance. Blind taste tests reveal that only 40% of consumers can accurately identify reduced-sodium snacks, indicating that perceived health benefits may drive purchase intent more than sensory differences. High-protein snacks, often made with whey isolate, pea protein, or cricket flour, appeal to fitness enthusiasts and older adults focused on muscle preservation. This demographic, skewing male and affluent, allows brands to command premiums exceeding 50% over conventional options. Organic certification, overseen by the USDA National Organic Program in the US and the EU Organic Regulation 2018/848 in Europe, mandates traceability from farm to finished product. This compliance burden tends to favor vertically integrated players, sidelining smaller producers lacking the necessary audit infrastructure.

By Distribution Channel: Online Retail Reshapes Shelf Dynamics

In 2025, supermarkets and hypermarkets accounted for 54.49% of total sales, serving as key shopping destinations where impulse purchases make up 60% of baked-snack transactions. However, online retail, with a 9.45% CAGR, signals a market shift as subscription models and targeted digital advertising reduce the dominance of physical shelf space. Convenience stores, contributing an estimated 20% to volume, cater to time-sensitive consumers willing to pay a premium for proximity. Their importance is growing in Asia Pacific, where 7-Eleven, FamilyMart, and Lawson operate over 80,000 outlets, increasingly stocking locally produced baked snacks tailored to regional tastes. Other channels, such as vending machines, foodservice, and specialty stores, are also gaining traction. Vending machines, in particular, are resurging due to cashless payment systems and IoT-enabled inventory management, which streamline operations.

Online retail offers brands the ability to bypass slotting fees, reaching up to USD 50,000 per SKU in major chains, and test niche formulations without minimum production runs. Amazon's Subscribe and Save program, offering 15% discounts on recurring snack deliveries, has converted about 8% of US baked-snack consumers into subscribers. This model ensures steady revenue, stabilizes demand, and informs production planning. Online platforms also highlight long-tail SKUs that physical stores cannot stock economically. For example, an Amazon fulfillment center carries over 200 baked-snack variants, compared to the 40-60 SKUs typical of large supermarkets, broadening access to specialty diets and regional flavors. Meanwhile, regulatory scrutiny is tightening. The EU's Digital Services Act, effective in 2024, requires online marketplaces to verify food-business-operator registrations for third-party sellers, reducing counterfeit and substandard products by eliminating unregistered vendors.

Geography Analysis

In 2025, Asia-Pacific accounted for 35.23% of global consumption, led by China, India, and Southeast Asia. Here, rising incomes and heightened health awareness have shifted preferences from fried to baked formats. China zeroes in on tier-1 and tier-2 cities, capitalizing on their high disposable incomes and deepening retail penetration. Meanwhile, in India, local powerhouses ITC and Parle are gaining ground by offering 10–20 gram packs at prices under their multinational counterparts, catering to the average annual budget for packaged snacks. In Indonesia and Malaysia, Halal certification is paramount, prompting investments in dedicated production lines that meet standards from organizations like MUI and CICOT. Japan and South Korea are leaning into premiumization, exemplified by Calbee’s high-priced Jagabee sticks, which tout artisanal production.

North America is set to witness an 8.12% CAGR growth rate through 2031, driven by a shift towards healthier options, a surge in e-commerce, and regulations on acrylamide that favor transparent sourcing. In the U.S., gluten-free, keto, and plant-based products have surged, now commanding a significant slice of retail sales, a jump from 14% in 2020. While Canada sees growth tempered by the rise of private labels, pushing branded companies to emphasize sustainability claims that resonate with eco-conscious consumers. In Mexico, deep-rooted taste preferences and household price sensitivity contribute to a high per-capita snack consumption.

Europe faces a dual challenge: stringent regulations that elevate compliance costs and simultaneously shield established players. The EU's Farm-to-Fork initiative aims for 25% of farmland to be organic by 2030. This ambition has already driven organic wheat prices up by 35%, squeezing margins for brands lacking long-term contracts. Germany and the U.K. dominate European volumes, though the U.K. grapples with post-Brexit tariffs, inflating import costs by 8–12% and pushing companies towards near-shoring. While France and Italy lean towards terroir-specific products, Spain and Poland are emerging as manufacturing powerhouses, capitalizing on lower labor costs and EU incentives to draw in investments. South America and the Middle East and Africa, together accounting for 15% of global demand, face challenges. Currency fluctuations, infrastructural shortcomings, and limited cold chain facilities stymie the entry of premium baked goods, making price the dominant purchasing factor in these markets.

Mordor Intelligence provides coverage of the baked savoury snacks market across other key regional markets, including North America, each with their regulatory frameworks and demand patterns.

Competitive Landscape

The baked savory snacks market is highly competitive, featuring global food giants, rapidly growing regional brands, and specialized health-focused startups competing for consumer loyalty. Major legacy players like PepsiCo, Mondelez International, and General Mills dominate the market with their extensive brand portfolios, robust retail distribution networks, and significant marketing budgets. These companies focus on product innovation, offering healthier versions of classic snacks (e.g., PepsiCo's Lay's Gourmet and Off The Eaten Path), experimenting with flavors to cater to diverse palates (e.g., Red Rock Deli launch in India), and leveraging data and AI to optimize product development. Additionally, they utilize omnichannel marketing strategies, including strong e-commerce and quick-commerce presence, to drive sales and maintain their market leadership.

Smaller and mid-sized players, along with challenger brands like HIPPEAS and Biena Snacks, as well as private labels from supermarkets, target niche segments such as plant-based, gluten-free, and high-protein snacks. These players often succeed by focusing on transparent marketing, sustainable packaging, and leveraging direct-to-consumer (D2C) and e-commerce models to attract wellness-focused consumers, particularly millennials and Gen Z. Regional players also play a significant role, especially in the Asia-Pacific market, by introducing localized flavors and adapting to regional snacking patterns. Their growth is often fueled by local manufacturing capabilities and the expansion of modern retail infrastructure.

The market is characterized by constant innovation in flavor, texture, and ingredients as companies strive to bridge the sensory gap with fried snacks while meeting the rising demand for healthier, "clean label" products. Despite the growth opportunities, intense competition and the challenge of replicating the taste and mouthfeel of fried snacks necessitate continuous and robust innovation for brand differentiation. Companies must remain agile and responsive to evolving consumer preferences to sustain their competitive edge in this dynamic market.

Baked Savoury Snacks Industry Leaders

The Kelloggs Company

PepsiCo Inc.

Mondelez International

Campbell Soup Company

Calbee Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: PepsiCo announced a USD 150 million investment to expand its baked-snack production capacity in Texas, adding 2 hybrid infrared baking lines capable of processing 12,000 kilograms per hour. The facility will focus on multigrain and plant-based SKUs, targeting the better-for-you segment.

- November 2024: Kellanova completed its acquisition of a controlling stake in a Brazilian snack manufacturer for USD 85 million, securing access to South American distribution networks and local ingredient sourcing that reduces exposure to currency volatility.

- October 2024: Mondelez International launched Ritz Crisp and Thins in 12 European markets, featuring sriracha-lime and miso-sesame variants formulated with 30% less sodium than conventional crackers. The product achieved distribution in 18,000 stores within 3 months.

- September 2024: General Mills partnered with a regenerative-agriculture consortium to source 25% of its oat supply from carbon-negative farms by 2027, a commitment that aligns with its Cascadian Farm brand positioning and targets consumers prioritizing environmental stewardship.

Global Baked Savoury Snacks Market Report Scope

The global baked savoury snacks market is diversely classified by product type into potato chips, extruded snacks, popcorn, savoury biscuits, pretzels and tortilla chips. By distribution channel, the market is segmented as supermarket/hypermarket, convenience stores, speciality stores, online stores, and others. Also, The market is segmented according to the geographical regions.

| Baked Chips |

| Savoury Biscuits and Crackers |

| Pretzels |

| Extruded Snacks |

| Popcorn |

| Tortilla Chips |

| Others |

| Wheat |

| Corn |

| Rice |

| Multigrain |

| Others |

| Conventional |

| Better-for-You/Health-Oriented |

| Supermarkets/Hypermarkets |

| Convenience Stores |

| Online Retail Stores |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Sweden | |

| Belgium | |

| Poland | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Thailand | |

| Singapore | |

| Indonesia | |

| South Korea | |

| Australia | |

| New Zealand | |

| Rest of Asia Pacific | |

| South America | Brazil |

| Argentina | |

| Peru | |

| Colombia | |

| Chile | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| Product Type | Baked Chips | |

| Savoury Biscuits and Crackers | ||

| Pretzels | ||

| Extruded Snacks | ||

| Popcorn | ||

| Tortilla Chips | ||

| Others | ||

| Ingredient Base | Wheat | |

| Corn | ||

| Rice | ||

| Multigrain | ||

| Others | ||

| Category | Conventional | |

| Better-for-You/Health-Oriented | ||

| Distribution Channel | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Sweden | ||

| Belgium | ||

| Poland | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Thailand | ||

| Singapore | ||

| Indonesia | ||

| South Korea | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Peru | ||

| Colombia | ||

| Chile | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the baked savoury snacks market in 2026?

The baked savoury snacks market size stands at USD 58.39 billion in 2026.

What is the expected growth rate for baked savoury snacks through 2031?

The category is projected to expand at a 6.35% CAGR to reach USD 79.43 billion by 2031.

Which product type is growing fastest inside baked savoury snacks?

Savoury biscuits and crackers are advancing at a 7.46% CAGR, outpacing baked chips.

Which region will post the highest growth?

North America is set to record the fastest regional CAGR at 8.12% through 2031.

How important is online retail for baked snack sales?

Online channels account for 12.28% of 2025 sales and are growing at a 9.45% CAGR, driven by subscriptions and direct-to-consumer platforms.

What technology is improving energy efficiency in baked snack production?

Hybrid infrared ovens cut energy use by 30% while delivering fried-like textures, helping brands meet sustainability targets.

Page last updated on: