Middle East And Africa Online Grocery Delivery Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

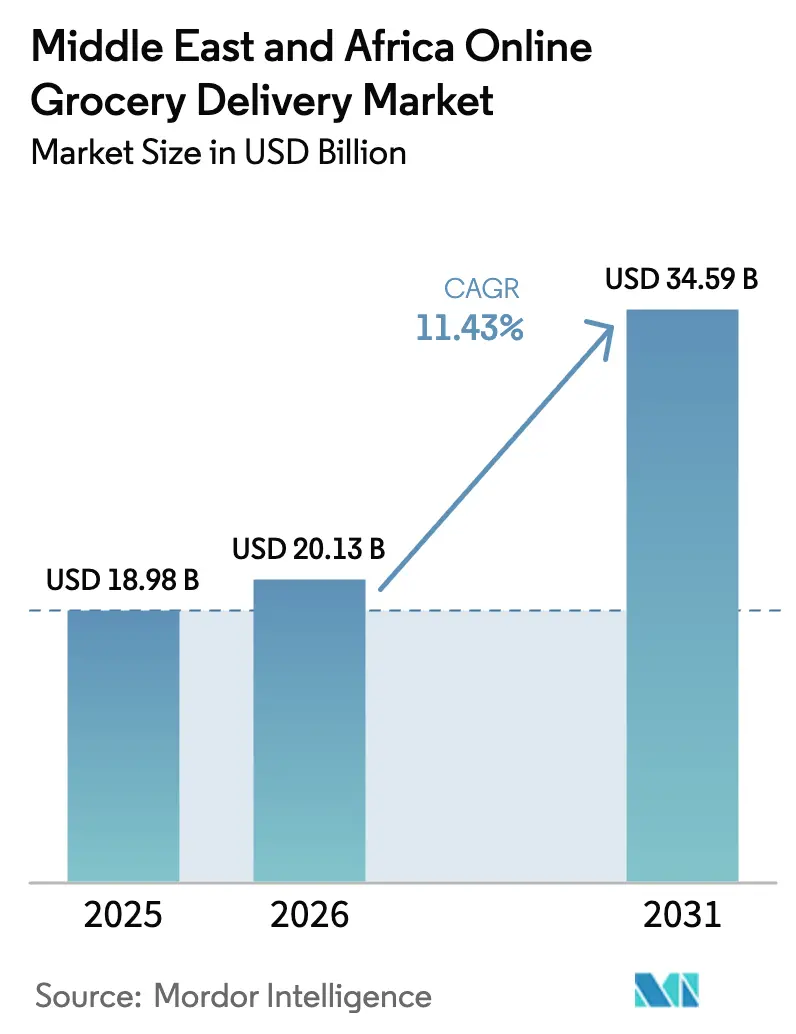

| Base Year Market Size (2025) | USD 18.98 Billion |

| Market Size (2026) | USD 20.13 Billion |

| Market Size (2031) | USD 34.59 Billion |

| Growth Rate (2026 - 2031) | 11.43% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East And Africa Online Grocery Delivery Market Analysis by Mordor Intelligence

The Middle East And Africa Online Grocery Delivery Market size is expected to increase from USD 18.98 billion in 2025 to USD 20.13 billion in 2026 and reach USD 34.59 billion by 2031, growing at a CAGR of 11.43% over 2026-2031.

Strong smartphone penetration, denser dark-store networks in Gulf cities, and innovative fulfilment formats anchored at fuel stations continue to compress delivery windows and broaden customer reach. Quick-commerce services offering sub-30-minute delivery are expanding the addressable market for time-pressed households, while scheduled services remain relevant for value-oriented bulk orders. Platforms that embed buy-now-pay-later, social commerce features, and artificial intelligence-driven inventory tools are boosting average basket values, reducing spoilage, and improving order accuracy. Competitive intensity is rising as well-capitalized regional champions collide with new entrants backed by global tech majors, nudging operators toward vertical integration, business-to-business expansion, and proprietary technology stacks.

Key Report Takeaways

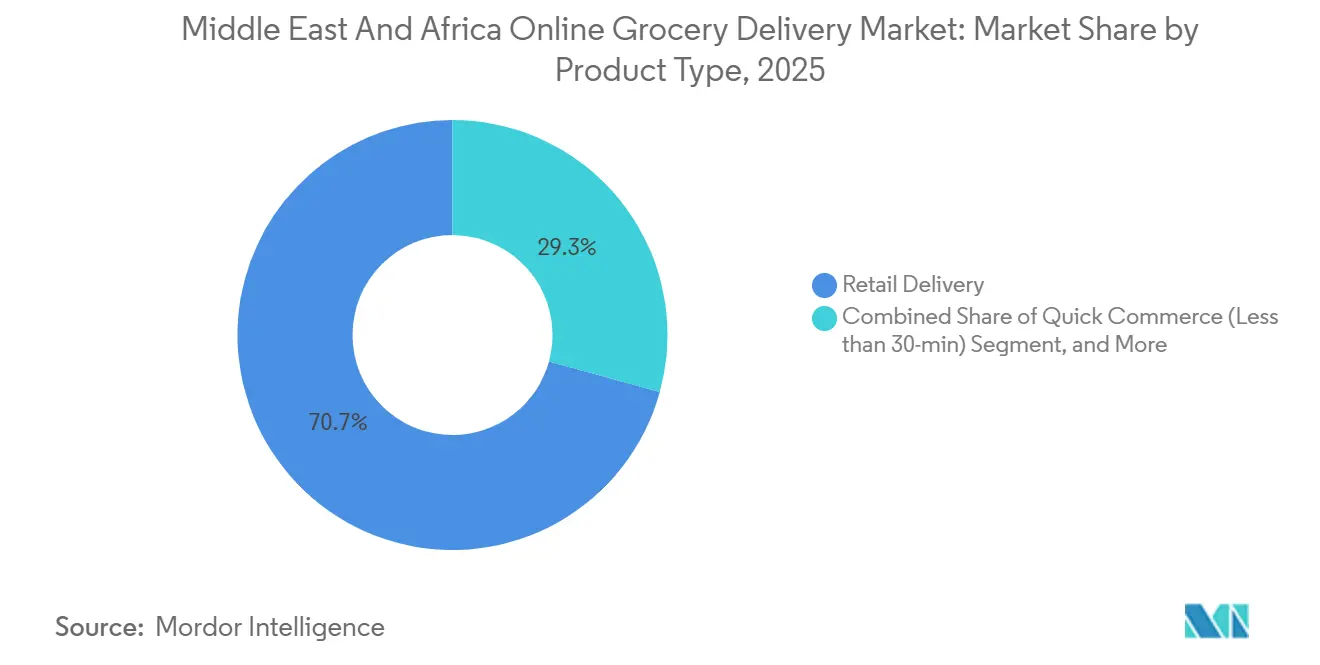

- By product type, retail delivery held 70.73% of the online grocery delivery market share in 2025, whereas Quick Commerce is forecast to expand at a 14.01% CAGR to 2031.

- By delivery speed, Standard delivery captured 56.91% of the online grocery delivery market size in 2025, while Instant delivery is advancing at a 13.23% CAGR through 2031.

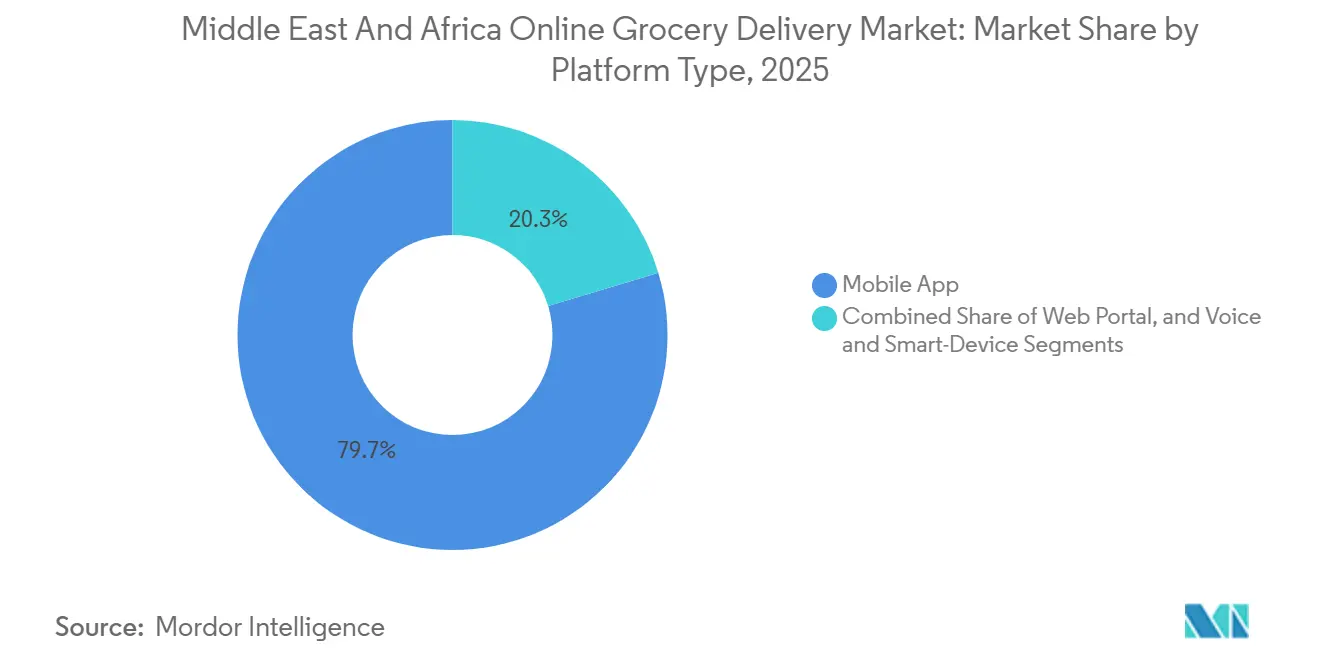

- By platform type, mobile apps processed 79.68% of 2025 transactions; web portals are projected to post the highest 11.86% CAGR to 2031.

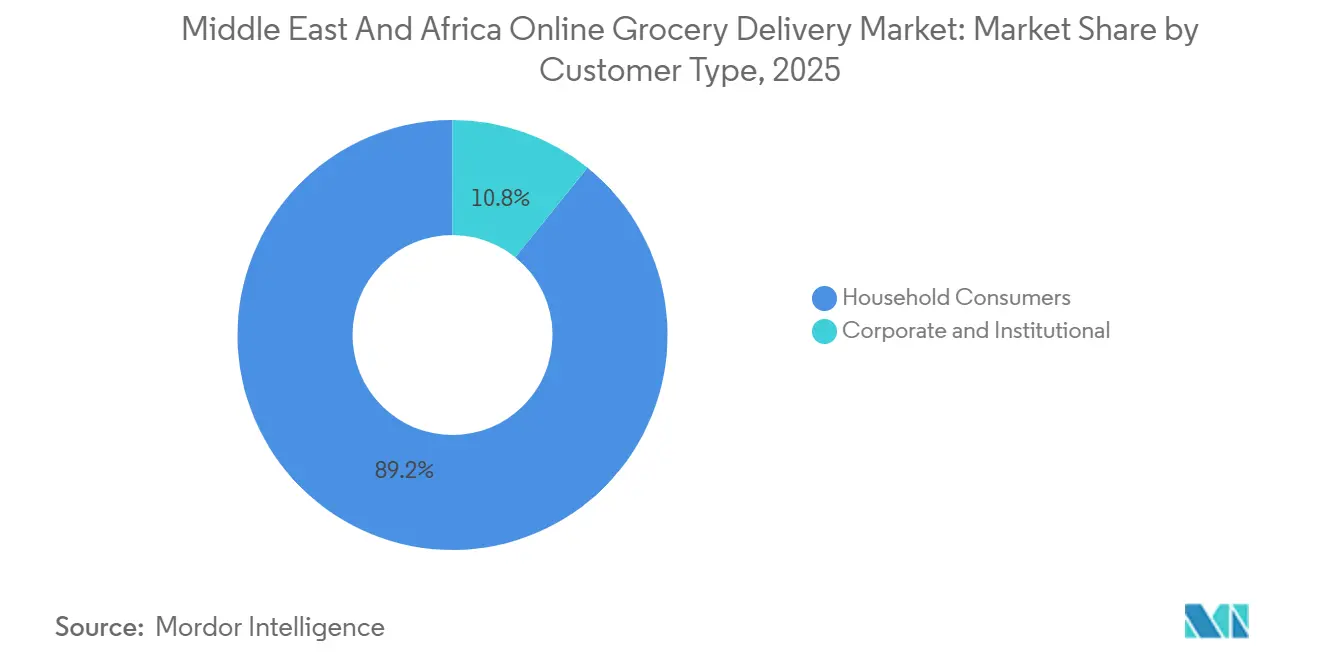

- By customer type, household consumers accounted for 89.19% of 2025 revenue, yet the corporate segment is projected to log an 11.48% CAGR to 2031.

- By geography, the United Arab Emirates led with 27.26% revenue share in 2025, while Saudi Arabia is poised for the fastest 12.67% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Worldwide, activity is shaped by contributions from multiple regions, with Middle east and africa representing one of the more structurally developed among them. The global report on online grocery delivery market by Mordor Intelligence reflects how these regional layers combine into a single system.

Middle East And Africa Online Grocery Delivery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of Quick-Commerce Dark-Store Networks | +2.8% | Gulf Cooperation Council, urban Egypt and South Africa | Short term (≤ 2 years) |

| Rising Smartphone and Internet Penetration | +2.3% | Saudi Arabia, United Arab Emirates, Qatar, Kuwait, Bahrain, Oman, Egypt, South Africa, Kenya, Nigeria | Medium term (2-4 years) |

| AI-Driven Hyperlocal Inventory Optimization | +1.9% | United Arab Emirates, Saudi Arabia, Qatar; pilots in Egypt and Kenya | Medium term (2-4 years) |

| Rapid Urbanization and Time-Pressed Lifestyles | +1.7% | Gulf Cooperation Council | Short term (≤ 2 years) |

| Increasing Digital Payment Adoption | +1.4% | United Arab Emirates, Saudi Arabia, Egypt, South Africa, Kenya, Nigeria | Short term (≤ 2 years) |

| Petro-Retail Fulfilment Hubs | +1.2% | Gulf Cooperation Council | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expansion of Quick-Commerce Dark-Store Networks

Dark stores in Gulf cities have shortened typical delivery windows to under 30 minutes, redefining consumer expectations for fresh groceries. Careem’s April 2025 tie-up with Tamimi Markets in Riyadh showcases premium, curated assortments delivered in 20 minutes.[1]Careem, “Careem and Tamimi Markets bring premium grocery delivery to Riyadh,” careem.com Carrefour’s 24-hour express service in Dubai fulfills orders within 60 minutes from a 10,000-SKU catalog. Deliveroo HOP and talabat Mart are scaling similar models, signaling a region-wide shift toward instant fulfillment. Well-capitalized operators enjoy first-mover advantages, though automation and real-time inventory systems raise capital barriers for smaller rivals.

Rising Smartphone and Internet Penetration

Smartphones are now a daily fixture for 96% of users in the United Arab Emirates and Saudi Arabia.[2]Deloitte Middle East, “Deloitte’s Digital Consumer Trends 2025,” deloitte.com PwC found that 57% of regional shoppers make purchases primarily via mobile, double the global average. High social-commerce engagement, with 73% of consumers buying through social media, encourages grocery apps to embed shoppable content. Growing use of generative artificial intelligence opens the door to chat-based ordering, though 25% of users remain privacy-conscious under new Gulf data-protection laws. Platforms that balance personalization and compliance are likely to capture incremental share.

AI-Driven Hyperlocal Inventory Optimization

Yango Tech’s AInventory, launched in March 2025, combines computer vision and IoT sensors to hit 98% order-fulfillment accuracy for Talabat Mart. Al-Futtaim’s trials of autonomous shelf-scanning robots further illustrate retailers’ appetite for data-rich replenishment tools. Personalized, artificial intelligence-powered promotions generate click-through rates 30% higher than generic offers, supporting larger baskets. Compliance with ISO 9001 and ISO 22000 standards ensures traceability as algorithms increasingly govern stocking decisions. Operators that master proprietary artificial intelligence stand to dominate premium and specialty categories.

Rapid Urbanization and Time-Pressed Lifestyles

More than 80% of Gulf residents now live in urban centers, amplifying demand for time-saving services. Dual-income households, expanded female workforce participation under Vision 2030, and congested commutes push shoppers toward instant convenience. Dark-store density and reliable road infrastructure make sub-30-minute delivery economically viable in cities such as Dubai and Riyadh. Platforms that couple round-the-clock service with targeted promotions during late-night and early-morning periods are monetizing latent demand that brick-and-mortar stores cannot reach.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Last-Mile Costs and Low Profit Margins | -1.8% | Nigeria, Kenya, Egypt, Morocco, secondary Gulf cities | Short term (≤ 2 years) |

| Limited Cold-Chain Capacity in Africa | -1.3% | Nigeria, Kenya, Egypt, Morocco, rest of Africa | Medium term (2-4 years) |

| Price Sensitivity and Perceived Premiums | -0.9% | Egypt, South Africa, Nigeria, Kenya, price-conscious Gulf | Short term (≤ 2 years) |

| Data-Localization and Compliance | -0.7% | United Arab Emirates, Saudi Arabia, Qatar, Egypt, South Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Last-Mile Costs and Low Profit Margins

Delivery expenses consume 15-25% of order value in Gulf cities and exceed 30% in sprawling African metros, eroding profitability. Jumia’s withdrawal from food delivery across seven African countries underlines the challenge. Rising fuel prices and local hiring mandates further inflate costs. Subscription models and minimum-basket thresholds help offset these pressures but favor scale players able to drive higher order density.

Limited Cold-Chain Capacity in Africa

Cold-chain gaps in Nigeria, Kenya, and Egypt elevate spoilage risk and confine platforms to ambient goods. Breadfast’s plan to raise USD 13 million for infrastructure upgrades underscores the capital intensity of chilled logistics.[3]Wamda, “Breadfast in talks with IFC for USD 13 million backing,” wamda.com Energy-reliant refrigeration adds operating costs where grid power is unreliable. Regulatory enforcement of food-safety standards is uneven, leaving compliance risks that discourage aggressive expansion into secondary cities.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Quick Commerce Outpaces Retail Delivery In Growth Velocity

Retail Delivery commanded 70.73% of 2025 revenue, confirming its role as the low-cost backbone of the online grocery delivery market. However, Quick Commerce is on track for a 14.01% CAGR, buoyed by platforms such as Careem and talabat that routinely meet 20-minute service levels. Meal-kit providers like Calo and JustCook are layering culinary expertise and portion-controlled packaging onto this ecosystem, appealing to health-conscious professionals. Specialty and ethnic grocery offerings meet the needs of expatriate communities, while pharmacy items further blur category lines. Operators must balance the capital intensity of dark stores with the culinary and packaging know-how required for meal kits, ensuring high inventory turnover to sustain margins.

Quick Commerce drives higher purchase frequency by converting top-up trips into digital orders. Meanwhile, Retail Delivery retains price-sensitive bulk baskets, underlining a bifurcated demand curve. Meal kits, although small in value, create brand stickiness and upselling opportunities. Platforms able to leverage private-label assortments and data-driven personalization are poised to capture incremental wallet share, even as category boundaries converge.

By Delivery Speed: Instant Fulfillment Captures Premium Segments

Standard delivery held 56.91% of 2025 sales, favored by value-oriented households planning weekly stock-ups. Instant delivery is growing at 13.23% as affluent consumers pay for speed, supported by Carrefour’s 24-hour express and Tamimi-Careem’s 20-minute premium service. Same-day fulfillment fills a middle ground for planned yet time-sensitive baskets. Subsidies and dynamic pricing help absorb high logistics costs, but densifying dark-store grids remain critical.

Ultra-fast entrants such as Keeta amplify competitive stakes by offering drone delivery and aggressive promotions. Operators that leverage artificial intelligence-based demand forecasting and automated micro-fulfillment center technology can improve pick-and-pack efficiency, making sub-two-hour windows profitable in dense urban corridors. Standard delivery will remain viable for large, non-urgent purchases, especially in peripheral African markets where infrastructure lags.

By Platform Type: Mobile Apps Dominate, Voice Commerce Emergent

Mobile apps processed 79.68% of 2025 transactions, reflecting the region’s mobile-first culture. Seamless user interfaces, in-app wallets, and social-commerce integrations sustain double-digit growth. Web portals, while a minority, serve corporate procurement needs and older desktop users, posting an 11.86% CAGR as InstaShop leverages its GroCart acquisition for bulk ordering. Voice and smart-device channels remain nascent but are poised for lift as connected-device adoption rises.

Super-apps that integrate ride-hailing, payments, and grocery delivery deepen customer engagement by cross-selling across verticals. Personalization through artificial intelligence and voice assistants can streamline basket building and boost repeat rates. Privacy-centric design, necessitated by Gulf data-protection laws, will become a differentiator as voice adoption scales.

By Customer Type: Household Consumers Anchor Demand, Corporate Segment Emerging

Household consumers generated 89.19% of 2025 revenue and will remain the dominant customer group through 2031 due to urban living and dual-income time pressures. High-frequency staples such as laban and bananas underscore habitual usage.[4]Gulf News, “What people ordered online in the UAE in 2025,” gulfnews.com Extreme purchase behavior, including single customers placing over 1,200 annual orders, validates stickiness.

Corporate and institutional demand is rising as hotels, restaurants, and small retailers digitize procurement. InstaShop-GroCart now offers 5,000 wholesale SKUs, while Emirates Flight Catering sources vertically farmed produce through GMG. Platforms must adapt with bulk-pack sizing, credit terms, and procurement dashboards. Early movers will likely command loyalty before broader competition intensifies.

Geography Analysis

The United Arab Emirates contributed 27.26% of 2025 revenue, supported by dense urban clusters and a tech-literate population. Talabat’s USD 7.4 billion gross merchandise value and Careem’s 3.4 million orders illustrate scale advantages, while Carrefour’s round-the-clock express service reinforces convenience. Saudi Arabia, however, is positioned for the fastest 12.67% CAGR through 2031 as Vision 2030 investments modernize digital infrastructure and diversify income sources. Jahez, HungerStation, and Keeta have ignited a price-and-speed race, each leveraging large delivery fleets and dark-store partnerships to secure share.

Qatar, Kuwait, Bahrain, and Oman form a lucrative second tier of high-income, densely populated markets, attracting expansion from Gulf incumbents and global entrants alike. Turkey’s sizable population and maturing e-commerce ecosystem represent a longer-term upside, though currency volatility poses risks.

Africa offers a fragmented yet promising landscape. South Africa’s Checkers Sixty60 and Woolworths show traditional retailers adapting quickly, while Egypt’s Breadfast secures development finance to extend into secondary cities. Nigeria and Kenya confront cold-chain and last-mile hurdles, yet growing mobile-money penetration and urbanization support gradual adoption. International retailers like Carrefour leverage franchise models to hedge risk, as evidenced by its 2026 Ethiopia entry. Operators targeting Africa must blend patient capital with partnerships that bridge logistics and payment gaps.

Mordor Intelligence provides coverage of the online grocery delivery market across other key regional markets, including Asia and South America, each with their regulatory frameworks and demand patterns.

Competitive Landscape

Regional leadership remains contestable. Talabat’s public listing and USD 7.4 billion 2024 gross merchandise value highlight its Gulf dominance, yet Careem’s super-app strategy captures cross-category wallet share. Noon capitalizes on petro-retail partnerships and a broad e-commerce base, while Instashop doubles down on wholesale after absorbing GroCart. Keeta, backed by Meituan, raises the bar with drone permits and deep subsidy war-chests, targeting 20% Middle East share by 2028.

Strategic moves concentrate on technology and vertical integration. Yango Tech’s artificial intelligence inventory system, FreshToHome’s farm-to-table model, and ADNOC-noon’s fuel-station micro-fulfillment hubs demonstrate varied paths to margin improvement. Regulatory compliance under Gulf data-protection laws elevates operational complexity, favoring incumbents with local data centers. Market entry barriers include capital-intensive dark-store automation and the need for proprietary artificial intelligence to sustain rapid fulfillment without eroding margins. Niche disruptors in meal kits, fresh produce, and wholesale procurement continue to exploit gaps that broad-based platforms overlook, keeping the market dynamic.

Middle East And Africa Online Grocery Delivery Industry Leaders

Talabat Holding plc

Noon AD Holdings One Person Company LLC

InstaShop Ltd.

HungerStation Company LLC

Kibsons International LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Carrefour agreed to rebrand 13 Ethiopian stores via a franchise with Queens Supermarket PLC and will open 17 additional outlets by 2028 to accelerate its Horn of Africa footprint.

- December 2025: Breadfast began negotiations with the International Finance Corporation for up to USD 13 million in equity to deepen Egyptian quick-commerce infrastructure.

- October 2025: Jahez partnered with noon to merge quick commerce and food delivery capabilities across Saudi Arabia within a single consumer app.

- August 2025: Keeta unveiled expansion plans into the United Arab Emirates, Kuwait, Qatar, Bahrain, and Oman, targeting 20% regional share and USD 6 billion gross merchandise value by 2028.

- July 2025: Jahez acquired 76.56% of Snoonu for USD 245 million, marking its first non-Saudi acquisition.

Middle East And Africa Online Grocery Delivery Market Report Scope

The Middle East and Africa Online Grocery Delivery Market Report is Segmented by Product Type (Retail Delivery, Quick Commerce, Meal-Kit Delivery, Specialty and Ethnic Grocery, and Pharmacy and Health Items), Delivery Speed (Standard, Same-Day, and Instant), Platform Type (Mobile App, Web Portal, and Voice and Smart-Device), Customer Type (Household Consumers, and Corporate and Institutional), and Geography). The Market Forecasts are Provided in Terms of Value (USD).

| Retail Delivery |

| Quick Commerce (Less than 30-min) |

| Meal-Kit Delivery |

| Specialty and Ethnic Grocery |

| Pharmacy and Health Items |

| Standard (Next-Day +) |

| Same-Day (2-12 h) |

| Instant (Less than 2 h) |

| Mobile App |

| Web Portal |

| Voice and Smart-Device |

| Household Consumers |

| Corporate and Institutional |

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Qatar | |

| Kuwait | |

| Bahrain | |

| Oman | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Kenya | |

| Morocco | |

| Rest of Africa |

| By Product Type | Retail Delivery | |

| Quick Commerce (Less than 30-min) | ||

| Meal-Kit Delivery | ||

| Specialty and Ethnic Grocery | ||

| Pharmacy and Health Items | ||

| By Delivery Speed | Standard (Next-Day +) | |

| Same-Day (2-12 h) | ||

| Instant (Less than 2 h) | ||

| By Platform Type | Mobile App | |

| Web Portal | ||

| Voice and Smart-Device | ||

| By Customer Type | Household Consumers | |

| Corporate and Institutional | ||

| By Geography | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Qatar | ||

| Kuwait | ||

| Bahrain | ||

| Oman | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Kenya | ||

| Morocco | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large is the Middle East and Africa online grocery delivery market today?

The online grocery delivery market size reached USD 20.13 billion in 2026 and is projected to hit USD 34.59 billion by 2031 at an 11.43% CAGR.

Which delivery model is growing fastest?

Quick Commerce, defined by sub-30-minute fulfillment, is forecast to grow at 14.01% annually through 2031, outpacing scheduled Retail Delivery.

Why is Saudi Arabia considered the key growth engine?

Government digital-infrastructure spending, rising female workforce participation, and aggressive platform partnerships are driving a 12.67% CAGR in Saudi Arabia through 2031.

What is the biggest operational challenge for platforms?

High last-mile costs, which can exceed 30% of order value in some African metros, remain the main barrier to profitability despite technology improvements.

How are companies improving inventory accuracy?

Operators deploy artificial intelligence-powered tools such as Yango Tech’s AInventory, achieving fulfillment accuracy rates of 98% and reducing stockouts.

Page last updated on: