Middle East And Africa Baby Food Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

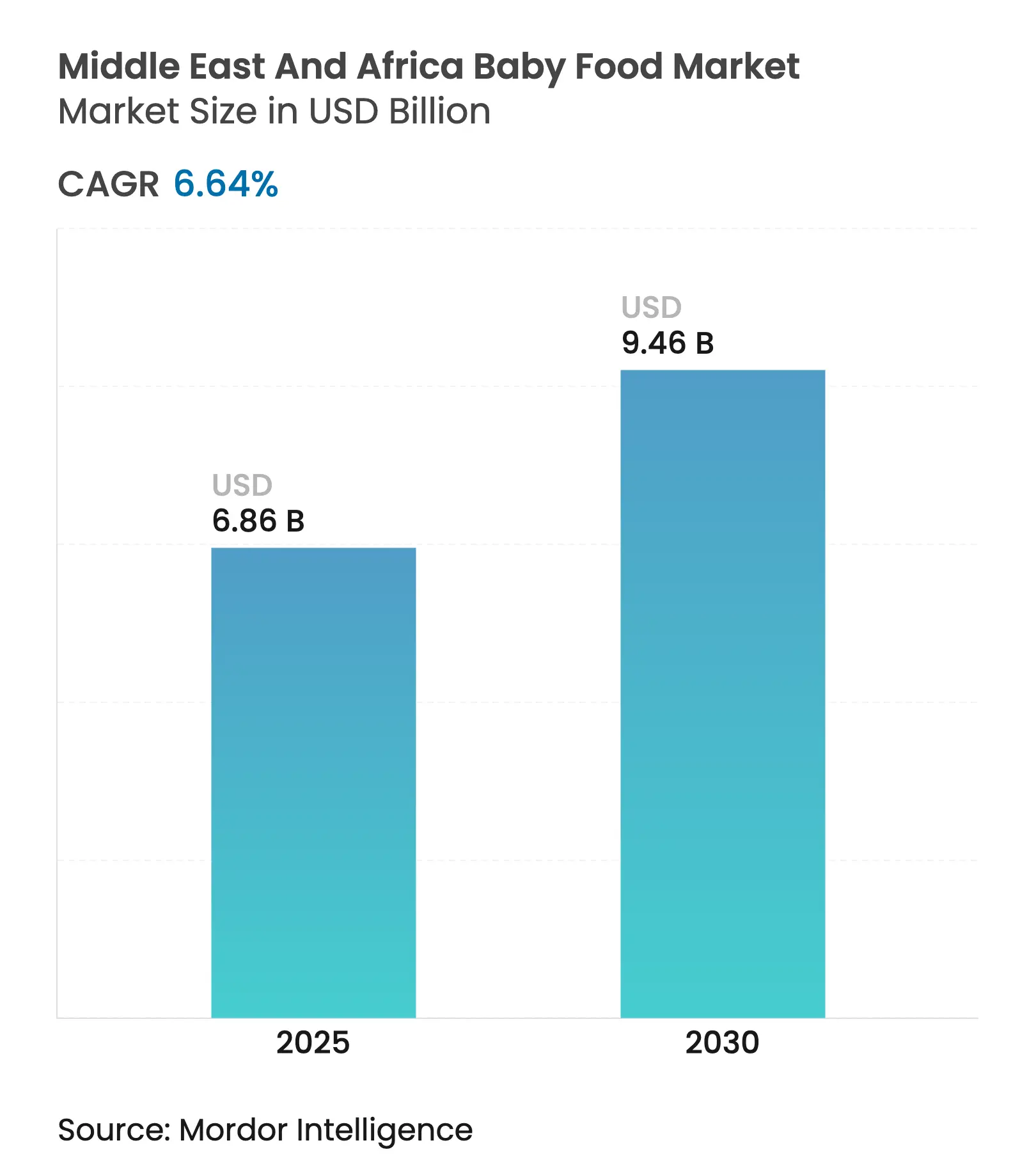

| Market Size (2025) | USD 6.86 Billion |

| Market Size (2030) | USD 9.46 Billion |

| Growth Rate (2025 - 2030) | 6.64 % CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Middle East And Africa Baby Food Market Analysis by Mordor Intelligence

The Middle East And Africa Baby Food Market size is estimated at USD 6.86 billion in 2025, and is expected to reach USD 9.46 billion by 2030, at a CAGR of 6.64% during the forecast period (2025-2030). This expansion trajectory positions the region as a critical growth frontier for infant nutrition companies, driven by demographic momentum and evolving consumer preferences that favor premium formulations over traditional feeding practices. Regional dynamics reveal Saudi Arabia commanding the largest market share at 30.04% in 2024, while the United Arab Emirates emerges as the fastest-growing geography with an 8.67% CAGR through 2030. The demographic foundation supporting this growth includes Saudi Arabia's birth rate of 16.42 per 1,000 population and Egypt's substantial 1.968 million births recorded in 2024, creating sustained demand for specialized infant nutrition products[1]Source: General Authority for Statistics Saudi Arabia, "Saudi Arabia's birth rate", stats.gov.sa. Premium organic, fortified, and plant-based lines are gaining traction as parents look beyond basic nourishment toward cognitive and immune-support benefits. Product innovation now focuses on human milk oligosaccharides, probiotics, and convenient ready-to-eat formats that shorten preparation time for dual-income families. Market opportunities intensify in urban clusters where e-commerce bridges distribution gaps and where regulators offer streamlined approvals that shorten launch cycles for advanced formulations. Competition therefore revolves around localization, regulatory agility, and scientific differentiation, creating an environment where technology-rich global majors coexist with nimble regional specialists.

Key Report Takeaways

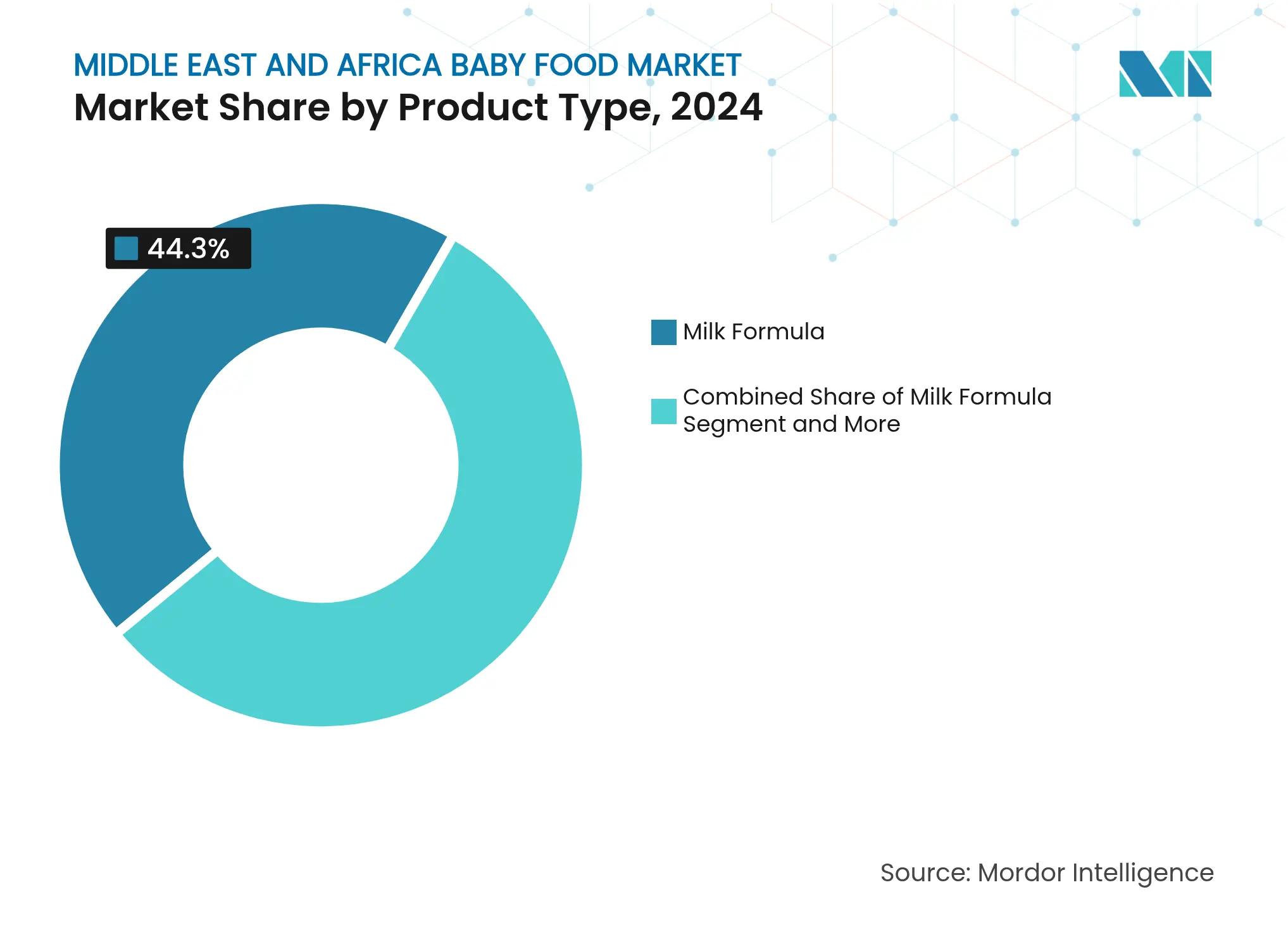

- By product type, milk formula led with 44.3% of Middle East and Africa baby food market share in 2024; liquid concentrate is forecast to expand at a 6.72% CAGR through 2030.

- By category, conventional products held 68.77% of the Middle East and Africa baby food market size in 2024, while organic is advancing at an 8.34% CAGR to 2030.

- By product format, powder accounted for 76.48% share of the Middle East and Africa baby food market size in 2024; liquid concentrate is the fastest-growing format at 7.27% CAGR.

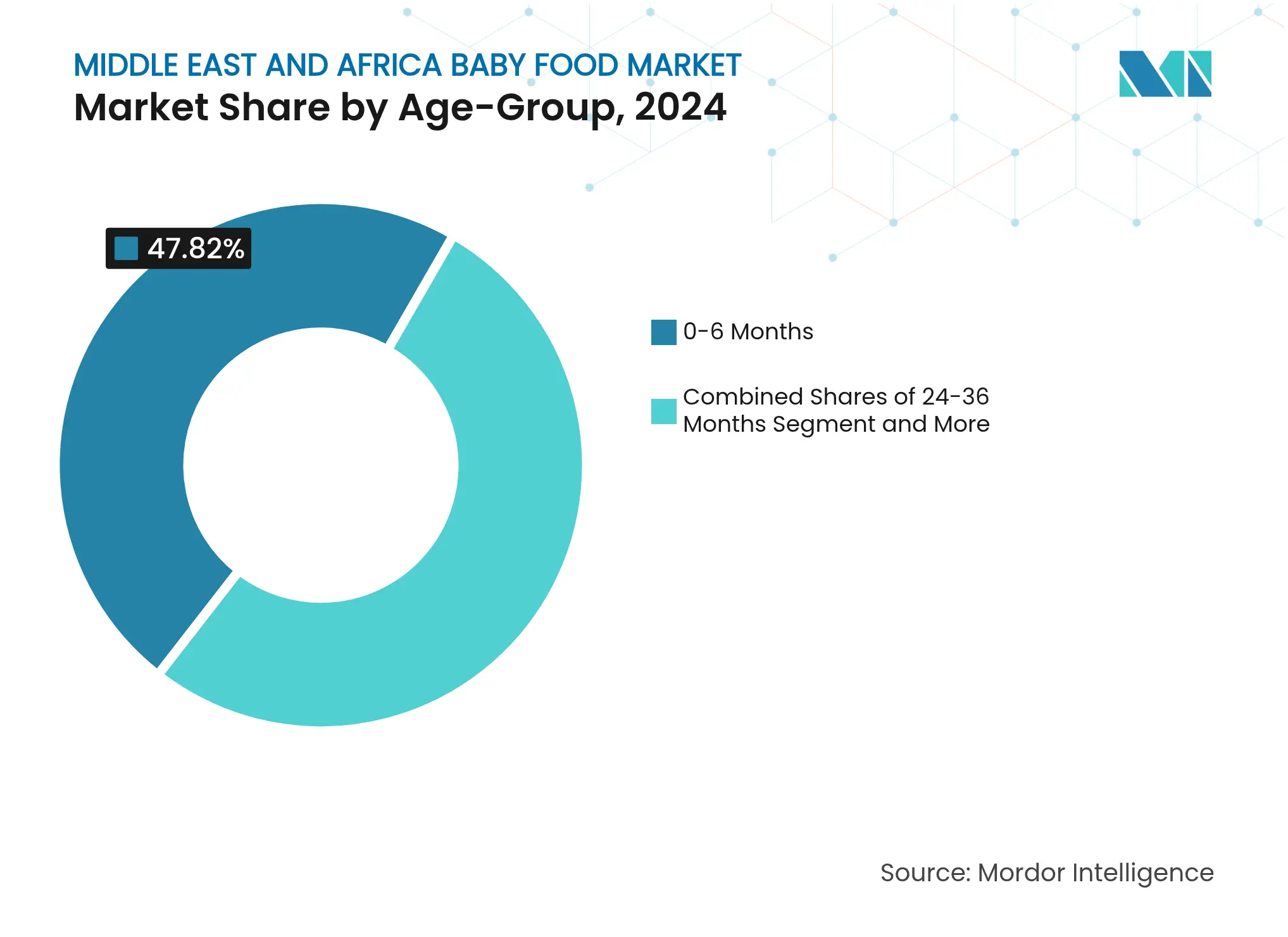

- By age group, the 0–6 months segment captured 47.82% revenue in 2024, whereas the 24–36 months segment is expanding at 7.38% CAGR through 2030.

- By distribution channel, supermarkets and hypermarkets held 37.84% of the Middle East and Africa baby food market share in 2024, while online retail shows a 6.83% CAGR to 2030.

- By geography, Saudi Arabia commanded 30.04% of the Middle East and Africa baby food market share in 2024; the United Arab Emirates registers the quickest rise at 8.67% CAGR toward 2030.

Middle East And Africa Baby Food Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Growing infant population and rising birth rates increase

demand

Growing infant population and rising birth rates increase

demand

| +1.2% | Egypt, Saudi Arabia, Nigeria core regions | Long term (≥ 4 years) |

(~) % Impact on CAGR Forecast

:

+1.2%

|

Geographic Relevance

:

Egypt, Saudi Arabia, Nigeria core regions

|

Impact Timeline

:

Long term (≥ 4 years)

|

More upper-middle-income families seek premium baby food

options

More upper-middle-income families seek premium baby food

options

| +0.8% | UAE, Saudi Arabia, South Africa urban centers | Medium term (2-4 years) | |||

Fortifying formulas with human milk oligosaccharides

boosts immunity

Fortifying formulas with human milk oligosaccharides

boosts immunity

| +0.6% | Global, with early adoption in UAE, Saudi Arabia | Medium term (2-4 years) | |||

Plant-based and hybrid formulas gain popularity among

health-conscious

Plant-based and hybrid formulas gain popularity among

health-conscious

| +0.4% | UAE, Turkey, South Africa metropolitan areas | Long term (≥ 4 years) | |||

Convenient ready-to-eat and portable baby food formats

grow

Convenient ready-to-eat and portable baby food formats

grow

| +0.5% | Global, accelerated in urban centers | Short term (≤ 2 years) | |||

Expanding e-commerce increases baby food product

accessibility online

Expanding e-commerce increases baby food product

accessibility online

| +0.7% | UAE, Saudi Arabia, Egypt leading adoption | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Growing Infant Population and Rising Birth Rates Increase Demand

Demographic fundamentals across the Middle East and Africa create sustained volume growth for baby food manufacturers, with Egypt recording 1.968 million births in 2024 and maintaining a fertility rate of 2.878 births per woman [2]Source: UN Population Division, "Population Division", un.org. Saudi Arabia's birth rate of 16.42 per 1,000 population, combined with its 35.3 million total population comprising 55.6% Saudi nationals, establishes a substantial domestic market for infant nutrition products. The demographic dividend extends beyond raw numbers, as urbanization rates exceeding 88% in the UAE create concentrated demand centers where modern retail infrastructure supports premium baby food distribution. Nigeria's population dynamics, despite economic challenges, contribute significant volume potential given its position as Africa's most populous nation. This demographic foundation provides baby food companies with predictable demand patterns that justify long-term manufacturing investments and product development initiatives.

More Upper-Middle-Income Families Seek Premium Baby Food Options

Economic prosperity in Gulf Cooperation Council countries drives premiumization trends that favor organic and fortified baby food formulations over basic milk powders. The UAE's per capita income levels and Saudi Arabia's Vision 2030 economic diversification initiatives create expanding middle-class segments willing to invest in advanced infant nutrition [3]Source: Saudi Vision 2030, "Saudi Vision", vision2030.gov.sa. Consumer spending patterns reveal preferences for products with functional benefits, including probiotics, DHA supplementation, and organic certifications that command price premiums of 20-40% over conventional alternatives. This trend accelerates in urban centers where dual-income households prioritize convenience and nutritional optimization for their children. The premiumization effect extends to packaging innovations, with single-serve formats and resealable containers gaining traction among affluent consumers who value portion control and product freshness.

Fortifying Formulas with Human Milk Oligosaccharides Boosts Immunity

Scientific advancement in human milk oligosaccharides (HMO) integration represents a technological breakthrough that differentiates premium formulas from conventional products, with regulatory approvals from the Saudi Food and Drug Authority enabling market introduction across the Gulf region according to the Saudi Food and Drug Authority. HMO fortification addresses parental concerns about immune system development, particularly relevant in regions where breastfeeding rates vary significantly due to cultural and economic factors. The UAE's advanced healthcare infrastructure and consumer awareness campaigns support adoption of scientifically enhanced formulations that mimic breast milk composition. Manufacturing complexity associated with HMO production creates barriers to entry that benefit established players with biotechnology capabilities, while regulatory frameworks require extensive clinical documentation to support health claims. This innovation cycle drives product differentiation and justifies premium pricing strategies that enhance profit margins for manufacturers investing in advanced nutritional science.

Plant-Based and Hybrid Formulas Gain Popularity Among Health-Conscious

Alternative protein sources gain acceptance among environmentally conscious consumers, particularly in urban centers where plant-based diets align with sustainability values and religious dietary requirements. Turkey's position as a bridge between European and Middle Eastern markets facilitates introduction of plant-based baby food innovations that cater to diverse dietary preferences according to the Turkish Ministry of Health. Hybrid formulations combining traditional dairy proteins with plant-based alternatives offer nutritional completeness while addressing lactose sensitivity concerns prevalent in certain population segments. Regulatory frameworks across the region are adapting to accommodate alternative protein sources, with the UAE's progressive food safety standards enabling faster market entry for innovative formulations. The trend reflects broader consumer shifts toward clean-label products and transparent ingredient sourcing that resonate with educated, affluent parents seeking optimal nutrition for their children.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Competition from traditional breastfeeding practices and

alternatives

Competition from traditional breastfeeding practices and

alternatives

| -0.9% | Global, stronger in rural Egypt, Nigeria, Morocco | Long term (≥ 4 years) |

(~) % Impact on CAGR Forecast

:

-0.9%

|

Geographic Relevance

:

Global, stronger in rural Egypt, Nigeria, Morocco

|

Impact Timeline

:

Long term (≥ 4 years)

|

Regulatory challenges and varying food safety standards

across regions

Regulatory challenges and varying food safety standards

across regions

| -0.6% | Cross-border trade affected, Nigeria, Egypt complexity | Medium term (2-4 years) | |||

Issues related to refrigeration and storage in some parts

of the region

Issues related to refrigeration and storage in some parts

of the region

| -0.4% | Rural areas, sub-Saharan Africa infrastructure gaps | Medium term (2-4 years) | |||

Limited awareness and trust in packaged baby foods in

rural areas

Limited awareness and trust in packaged baby foods in

rural areas

| -0.5% | Rural Egypt, Nigeria, Morocco traditional communities | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Competition from Traditional Breastfeeding Practices and Alternatives

WHO and UNICEF advocacy for exclusive breastfeeding during the first six months creates regulatory and cultural headwinds for commercial baby food adoption, particularly in regions where traditional feeding practices remain deeply embedded in social structures. Government health campaigns across Egypt and Nigeria emphasize breastfeeding benefits, while healthcare providers receive training to promote natural feeding methods over commercial alternatives. The challenge intensifies in rural communities where extended family support systems facilitate breastfeeding continuation, reducing demand for formula products during critical early months. Marketing restrictions under international codes limit promotional activities that could influence feeding decisions, requiring manufacturers to focus on complementary feeding periods rather than direct formula substitution. This dynamic creates market entry barriers and constrains volume growth potential, particularly for companies targeting the 0-6 months age segment that represents the largest market share.

Regulatory Challenges and Varying Food Safety Standards Across Regions

Fragmented regulatory frameworks across the Middle East and Africa create compliance complexity that increases market entry costs and delays product launches for manufacturers seeking regional expansion. The Saudi Food and Drug Authority's requirements for Breast Milk Substitute registration differ significantly from Egypt's Environmental Affairs Agency approval processes, necessitating multiple regulatory pathways for the same product. Cross-border trade faces additional challenges from varying GSO (Gulf Standards Organisation) technical regulations and local certification requirements that can extend approval timelines by 6-12 months. Smaller manufacturers lack resources to navigate multiple regulatory systems simultaneously, creating competitive advantages for established players with dedicated regulatory affairs capabilities. These barriers particularly impact innovative products requiring novel ingredient approvals, slowing the introduction of advanced formulations that could drive market premiumization and growth acceleration.

Segment Analysis

By Product Type: Milk Formula Dominance Drives Market Foundation

Milk formula commands 44.3% market share in 2024 while simultaneously achieving the fastest growth rate of 6.72% CAGR through 2030, reflecting both established market position and continued expansion potential across the Middle East and Africa region. This dual leadership stems from demographic trends favoring infant formula adoption in urban centers, where working mothers require feeding alternatives that support career continuity. Ready-to-feed baby food captures growing convenience demand, particularly in Gulf countries where dual-income households prioritize time-saving solutions. Dried baby food maintains steady market presence through cost-effectiveness and extended shelf life advantages crucial for regions with challenging distribution infrastructure.

The Saudi Food and Drug Authority's streamlined registration processes for milk formula products enable faster market entry for international manufacturers, while local production initiatives reduce import dependency and enhance supply chain resilience. Product innovation within milk formula segments focuses on functional ingredients including probiotics, DHA, and human milk oligosaccharides that address specific nutritional requirements for infant development. Other product types encompass specialized formulations for premature infants and children with dietary restrictions, representing niche opportunities for manufacturers with clinical expertise and regulatory capabilities to support health claims.

Note: Segment shares of all individual segments available upon report purchase

By Category: Conventional Products Face Organic Disruption

Conventional baby food products maintain 68.77% market share in 2024, yet organic alternatives accelerate at 8.34% CAGR through 2030, signaling a fundamental shift in consumer preferences toward premium, naturally-sourced infant nutrition. This growth differential reflects increasing awareness of pesticide residues and artificial additives among educated, affluent parents who prioritize clean-label products for their children. The UAE and Saudi Arabia lead organic adoption due to higher disposable incomes and government initiatives promoting sustainable agriculture that support organic food supply chains.

Regulatory frameworks across the region are evolving to accommodate organic certification requirements, with the Gulf Standards Organisation developing specific guidelines for organic baby food labeling and production standards. Conventional products retain dominance through price accessibility and widespread distribution networks that serve price-sensitive consumer segments, particularly in rural areas where organic premiums remain prohibitive. The category transition creates opportunities for manufacturers to develop hybrid products that incorporate organic ingredients while maintaining competitive pricing structures that appeal to middle-income families seeking nutritional upgrades without significant cost increases.

By Product Format: Powder Leadership Meets Liquid Innovation

Powder format dominates with 76.48% market share in 2024, leveraging cost advantages and extended shelf life that align with regional distribution challenges and consumer price sensitivity across diverse economic segments. However, liquid concentrate emerges as the fastest-growing format at 7.27% CAGR through 2030, driven by convenience preferences among urban consumers and improved cold chain infrastructure in major metropolitan areas. This format shift reflects changing lifestyle patterns where time-pressed parents value ready-to-use solutions over traditional powder preparation methods.

Manufacturing investments in liquid concentrate production require sophisticated processing capabilities and quality control systems that create barriers to entry for smaller regional players. The UAE's advanced logistics infrastructure and temperature-controlled warehousing facilities support liquid format distribution, while Saudi Arabia's MODON industrial cities provide manufacturing locations with integrated cold storage capabilities. Powder format retention stems from cultural familiarity and economic accessibility, particularly in price-sensitive markets where bulk purchasing patterns favor larger package sizes that offer better value propositions for families with multiple children.

Recognized by Experts. Trusted by Leaders.

A trusted intelligence partner to global decision-makers across 90+ countries.

By Age-Group: Early Infancy Dominance Yields to Toddler Growth

The 0-6 months segment captures 47.82% market share in 2024, reflecting the critical importance of early infant nutrition and the concentrated demand during the initial feeding transition period. However, the 24-36 months age group achieves the fastest growth at 7.38% CAGR through 2030, indicating evolving parental attitudes toward extended nutritional support for toddler development. This growth pattern aligns with pediatric recommendations for continued specialized nutrition beyond traditional weaning periods, particularly in regions where dietary diversity remains limited.

Toddler nutrition products command premium pricing due to advanced formulations that support cognitive development, immune function, and physical growth during critical developmental windows. The 6-12 months and 12-24 months segments maintain steady growth as parents recognize the importance of gradual nutritional progression that bridges breast milk or formula to solid food introduction. Regional variations in weaning practices influence segment performance, with Gulf countries favoring extended formula feeding while African markets emphasize earlier solid food introduction based on traditional feeding customs and economic considerations that prioritize cost-effective nutrition solutions.

Note: Segment shares of all individual segments available upon report purchase

By Distribution Channel: Traditional Retail Faces Digital Disruption

Supermarkets and hypermarkets maintain 37.84% market share in 2024 through established consumer shopping patterns and comprehensive product assortments that enable comparison shopping across multiple brands and formats. Online retail emerges as the growth leader with 6.83% CAGR through 2030, supported by government digital economy initiatives and improved last-mile delivery infrastructure across major urban centers. The UAE's e-commerce penetration and Saudi Arabia's Vision 2030 digital transformation goals create favorable conditions for online baby food sales growth.

Drugstores and pharmacies provide specialized retail environments where healthcare professionals offer product recommendations and nutritional guidance that influence purchase decisions, particularly for premium and specialized formulations. Convenience stores serve immediate needs and emergency purchases, while their extended operating hours cater to parents requiring flexible shopping schedules. The distribution evolution reflects broader retail transformation where omnichannel strategies become essential for manufacturers seeking comprehensive market coverage and consumer accessibility across diverse geographic and demographic segments within the region.

Geography Analysis

Saudi Arabia leads the Middle East and Africa baby food market with 30.04% share in 2024, leveraging its substantial birth rate of 16.42 per 1,000 population and government initiatives promoting local manufacturing through the "Made in Saudi Arabia" program launched in 2021. The kingdom's 35.3 million population, comprising 55.6% Saudi nationals, creates a stable domestic demand base supported by rising disposable incomes and urbanization trends that favor modern retail channels. MODON's operation of 1,300 food factories across 36 cities provides manufacturing infrastructure that attracts international baby food companies seeking regional production capabilities, while the Saudi Food and Drug Authority's streamlined registration processes facilitate faster product launches.

The United Arab Emirates achieves the fastest regional growth at 8.67% CAGR through 2030, driven by its position as a regional hub for premium baby food distribution and its advanced e-commerce infrastructure that supports online retail expansion. The UAE's 88% urbanization rate and high per capita income levels create ideal conditions for premium product adoption, while Dubai Municipality's progressive food safety regulations enable innovative product introductions including organic and plant-based formulations. The country's strategic location and world-class logistics infrastructure position it as a gateway for manufacturers targeting broader Middle East and North Africa markets, with free trade zones offering favorable conditions for regional distribution centers.

Egypt, Nigeria, Morocco, Turkey, and South Africa represent emerging opportunities with varying growth trajectories influenced by demographic patterns and economic development levels. Egypt's 1.968 million births in 2024 and declining fertility rates create concentrated demand in urban centers, while government tax incentives for local manufacturing attract foreign investment in food processing capabilities. Nigeria's large population base offers volume potential despite economic challenges, while Turkey's position as a European-Middle Eastern bridge facilitates product innovation transfer and regulatory harmonization. These markets require tailored strategies that balance premium product aspirations with price accessibility demands from diverse consumer segments seeking nutritional improvements within budget constraints.

Reports are available across multiple geographies.

Gain in-depth market insights across regions to support informed decisions.

Competitive Landscape

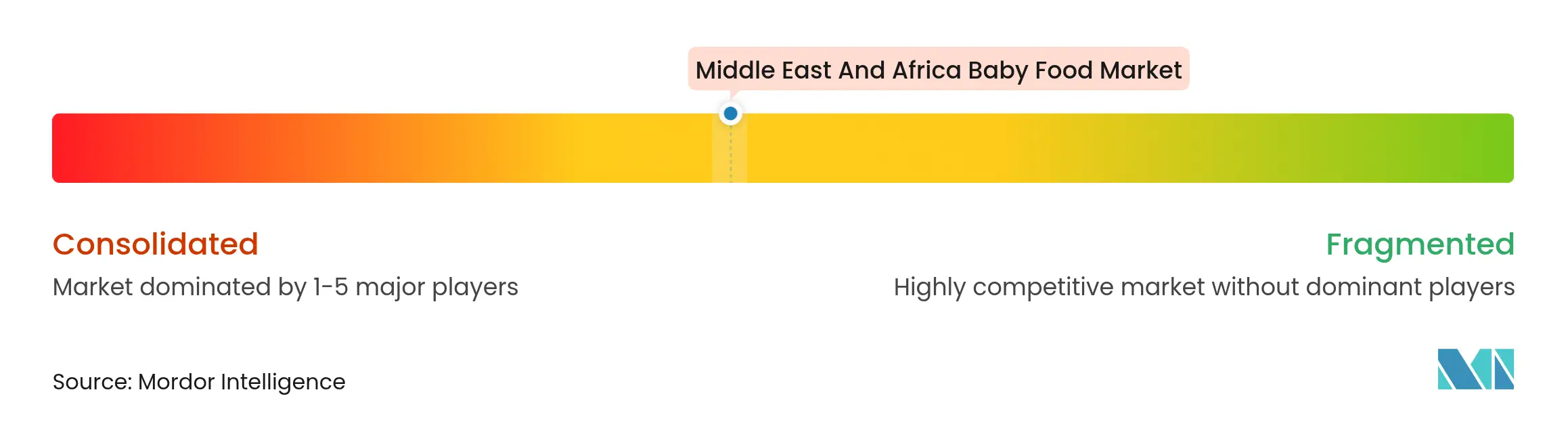

Market Concentration

The Middle East and Africa baby food market exhibits moderate concentration, creating space for both global leaders and regional specialists to capture market share through differentiated positioning strategies. Established players like Nestlé, Abbott Laboratories, and Danone leverage extensive distribution networks and regulatory expertise to maintain market leadership, while regional manufacturers such as Tiger Brands, Almarai, and local producers capitalize on cultural understanding and cost advantages.

Strategic patterns emphasize local manufacturing investments, with companies like Siniora Foods committing USD 40 million to Saudi Arabian production facilities that address supply chain resilience and government localization requirements. Technology adoption drives competitive differentiation through advanced formulations incorporating human milk oligosaccharides, probiotics, and plant-based proteins that command premium pricing and build brand loyalty among health-conscious consumers.

Opportunities exist in specialized nutrition segments including halal-certified organic products, culturally-adapted flavors, and packaging innovations that address regional climate challenges and storage limitations. The competitive dynamics reflect broader industry trends where regulatory compliance capabilities, manufacturing scale, and innovation pipelines determine market success, while emerging disruptors focus on e-commerce channels and direct-to-consumer models that bypass traditional retail intermediaries and capture digitally native parent demographics seeking convenience and product transparency.

Middle East And Africa Baby Food Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: South African entrepreneur Dorothy Dolly Fatima Mofomme, founder of natural baby food company Pojupoju, has introduced a new line of baby food purees. The products come in pouches with minicap/anti-choke lids that children can later use as building blocks.

- February 2025: Dubai-based sisters Qadreya and Maitha Al Awadhi established Bumblebee, a company that produces fresh, frozen meals for children aged six months to six years. The company's menu, created by a pediatric nutritionist and certified chef, incorporates local organic ingredients and hormone-free, grass-fed protein sources.

- February 2025: Happa Foods, recently launched in South Africa, offers organic baby food products that combine nutrition with convenience. The company produces organic meals free from additives, using fruits and vegetables to support infant development. The brand focuses on delivering nutritious options while addressing the needs of time-constrained parents who prioritize their children's health.

- September 2024: Nestlé has signed an agreement with the Saudi Authority for Industrial Cities and Technology Zones (MODON) to establish its first factory in Saudi Arabia. The USD 72 million facility will be located on a 117,000 square meter site in Jeddah Third Industrial City. The initial phase of operations will focus on baby food production, with plans to expand manufacturing to include other Nestlé food brands. This development aligns with Nestlé's strategy to localize supply chains in strategic markets.

Table of Contents for Middle East And Africa Baby Food Industry Report

1. INTRODUCTION

- 1.1Study Assumptions and Market Definition

- 1.2Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Growing infant population and rising birth rates increase demand

- 4.2.2More upper-middle-income families seek premium baby food options

- 4.2.3Fortifying formulas with human milk oligosaccharides boosts immunity

- 4.2.4Plant-based and hybrid formulas gain popularity among health-conscious

- 4.2.5Convenient ready-to-eat and portable baby food formats grow

- 4.2.6Expanding e-commerce increases baby food product accessibility online

- 4.3Market Restraints

- 4.3.1Competition from traditional breastfeeding practices and alternatives

- 4.3.2Regulatory challenges and varying food safety standards across regions

- 4.3.3Issues related to refrigeration and storage in some parts of the region

- 4.3.4Limited awareness and trust in packaged baby foods in rural areas

- 4.4Consumer Demand Analysis

- 4.5Regulatory Landscape

- 4.6Porter’s Five Forces

- 4.6.1Threat of New Entrants

- 4.6.2Bargaining Power of Buyers

- 4.6.3Bargaining Power of Suppliers

- 4.6.4Threat of Substitutes

- 4.6.5Competitive Rivalry

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1By Product Type

- 5.1.1Milk Formula

- 5.1.2Ready to Feed Baby Food

- 5.1.3Dried Baby Food

- 5.1.4Other Product Type

- 5.2By Category

- 5.2.1Organic

- 5.2.2Conventional

- 5.3By Product Format

- 5.3.1Powder

- 5.3.2Liquid Concentrate

- 5.4By Age-Group

- 5.4.10–6 Months

- 5.4.26–12 Months

- 5.4.312–24 Months

- 5.4.424–36 Months

- 5.5By Distribution Channel

- 5.5.1Supermarkets/Hypermarkets

- 5.5.2Drugstores/Pharmacies

- 5.5.3Convenience Stores

- 5.5.4Online Retail

- 5.5.5Other Distribution Channel

- 5.6By Geography

- 5.6.1South Africa

- 5.6.2Saudi Arabia

- 5.6.3United Arab Emirates

- 5.6.4Nigeria

- 5.6.5Egypt

- 5.6.6Morocco

- 5.6.7Turkey

- 5.6.8Rest of Middle East and Africa

6. COMPETITIVE LANDSCAPE

- 6.1Market Concentration

- 6.2Strategic Moves

- 6.3Market Positioning

- 6.4Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1Nestlé S.A.

- 6.4.2Abbott Laboratories

- 6.4.3The Baby Food Company

- 6.4.4Saipro Biotech Pvt. Ltd

- 6.4.5Orchard Baby Food

- 6.4.6Bumbles Baby Food

- 6.4.7Tiger Brands

- 6.4.8Danone S.A.

- 6.4.9Almarai Co. Ltd

- 6.4.10Ordesa

- 6.4.11Perrigo Company Plc

- 6.4.12Baby Gourmet Foods Inc.

- 6.4.13Mead Johnson Nutrition Company

- 6.4.14Morinaga Milk Industry Co Ltd

- 6.4.15The Kraft Heinz Company

- 6.4.16Hipp

- 6.4.17Hero AG

- 6.4.18Beech-Nut Nutrition Corporation

- 6.4.19Gerber Products Company

- 6.4.20Plum Organics (PBC)

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

Middle East And Africa Baby Food Market Report Scope

Baby food is any soft, easily digestible meal created particularly for human babies.

The Middle East and African baby food market is segmented by type, distribution channel, and geography. By type, the market has been segmented into milk formula, dried baby food, prepared baby food, and other types. By distribution channel, the market has been segmented into hypermarkets/supermarkets, convenience stores, drug/pharmacies, and other distribution channels. By geography, the market has been segmented into the United Arab Emirates, South Africa, and the Rest of the Middle East and Africa. The report offers market sizes and forecasts in value (USD million) for the abovementioned segments.